Bowie-Dick Test Pack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

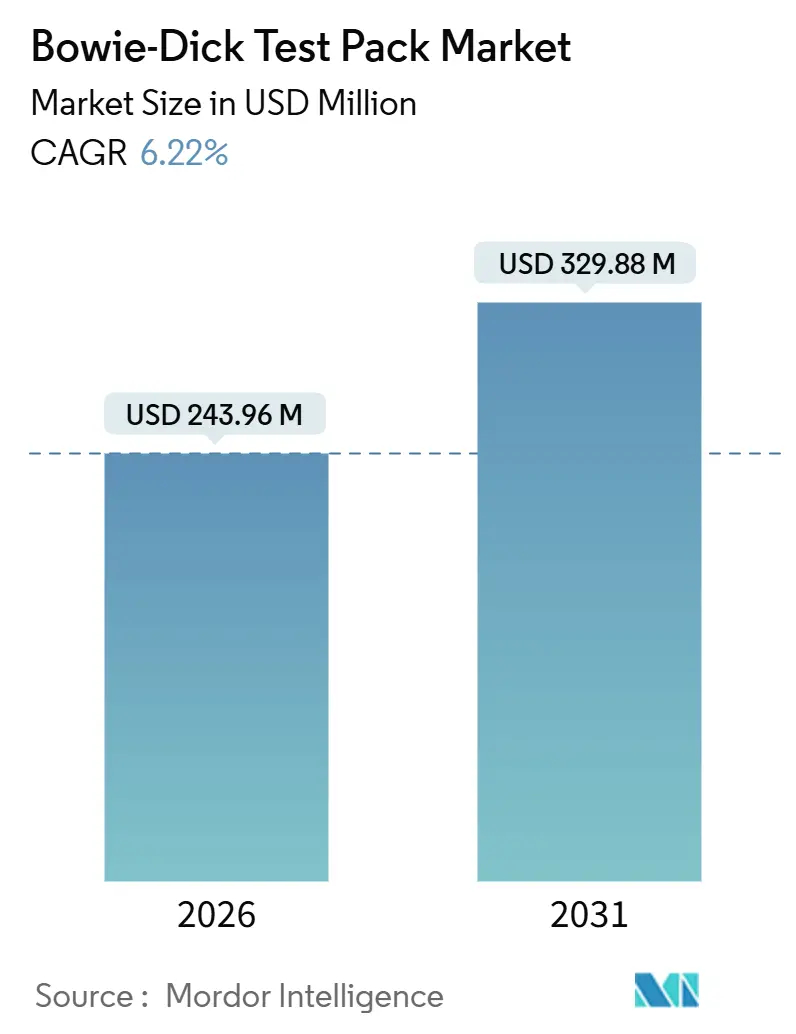

| Market Size (2026) | USD 243.96 Million |

| Market Size (2031) | USD 329.88 Million |

| Growth Rate (2026 - 2031) | 6.22% CAGR |

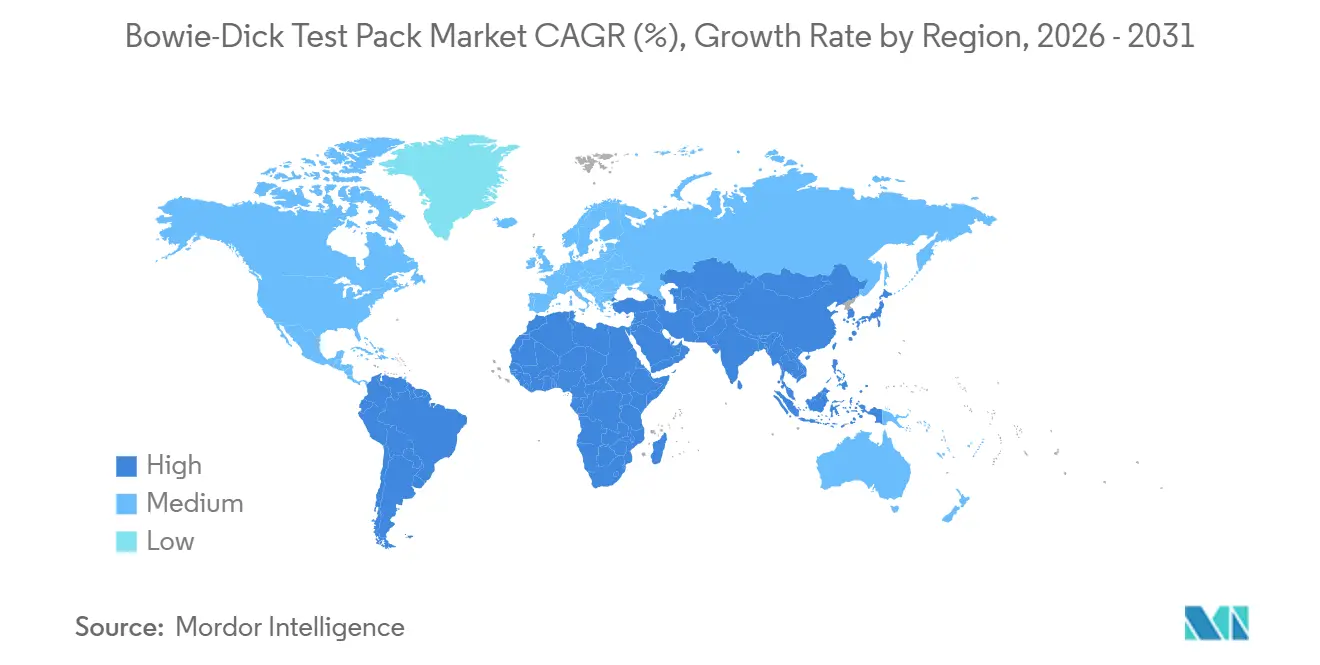

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

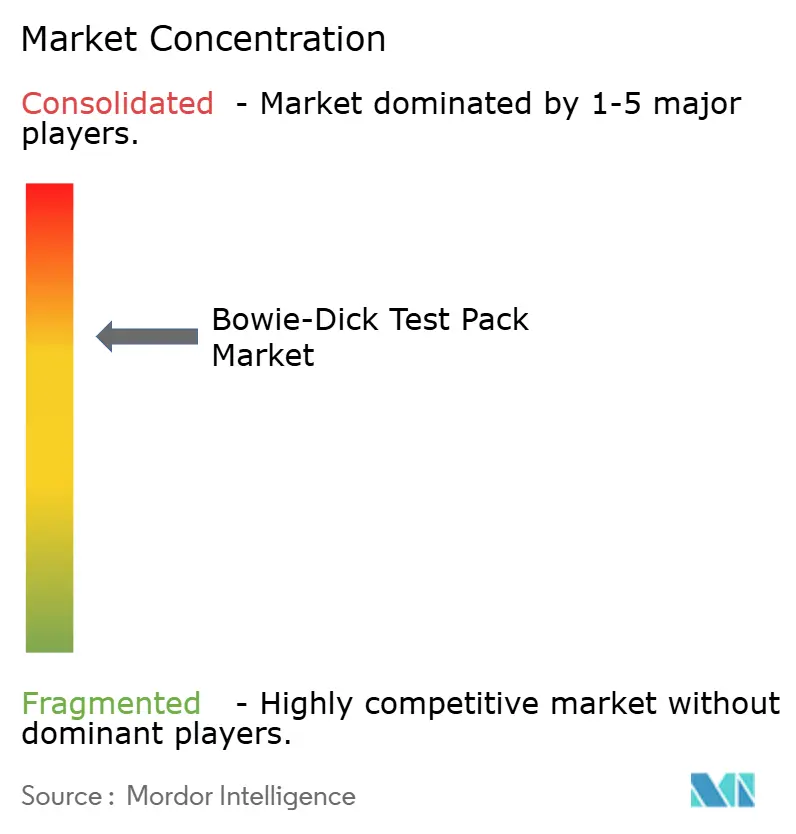

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bowie-Dick Test Pack Market Analysis by Mordor Intelligence

The Bowie-Dick Test Pack Market size is estimated at USD 243.96 million in 2026, and is expected to reach USD 329.88 million by 2031, at a CAGR of 6.22% during the forecast period (2026-2031).

Growth is anchored in daily sterilizer-verification mandates, widening surgical volumes, and the hospital sector’s push for automated documentation systems that align with ISO 11140-4 and AAMI ST-79 requirements. Digital devices are gaining ground as central sterile supply departments (CSSDs) integrate track-and-trace platforms, yet disposable paper-based packs still dominate based on price and entrenched practice. Geographically, North America remains the revenue leader, while Asia-Pacific offers the fastest expansion due to hospital‐construction programs and regulatory harmonization. Competitive dynamics are shaped by integrated equipment-plus-consumable bundles that lock in recurring revenue, but regional assemblers continue to fragment the long-tail of demand.

Key Report Takeaways

- By product type, traditional paper-based packs led with 53.13% revenue share in 2025; digital devices are projected to expand at a 10.22% CAGR through 2031.

- By form factor, disposable packs captured 61.54% share in 2025, whereas re-usable electronic process-challenge devices are poised for a 10.76% CAGR to 2031.

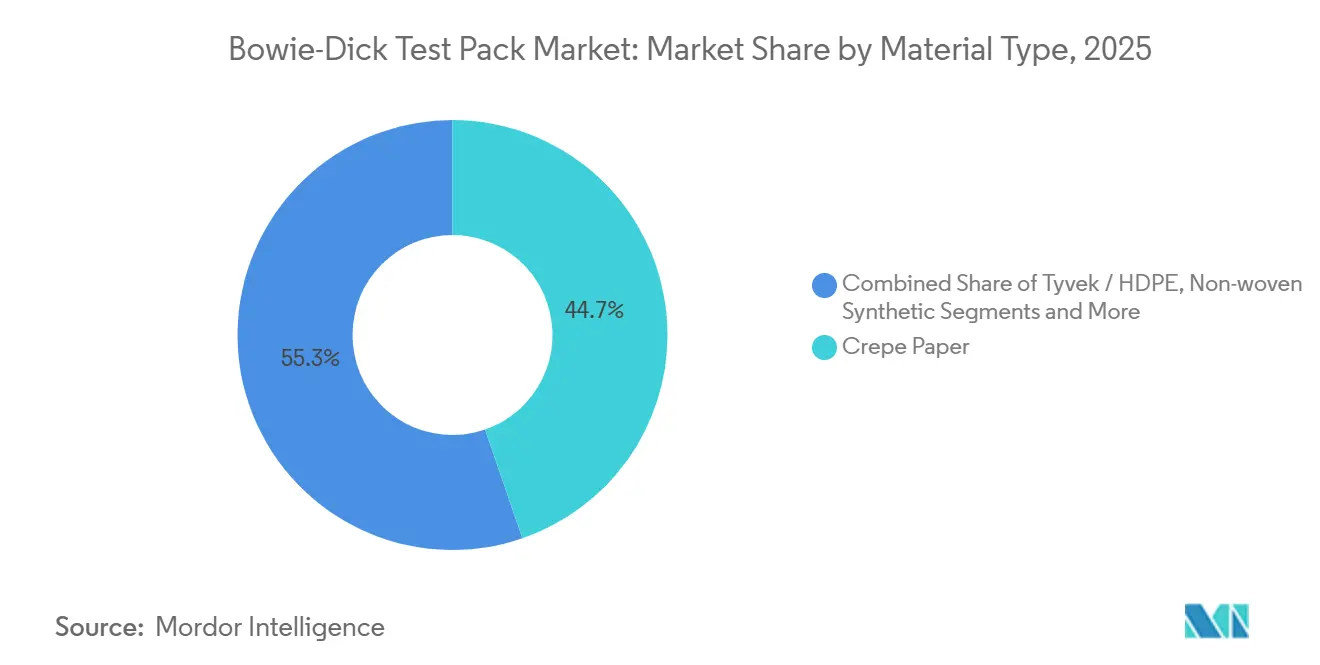

- By material, crepe paper dominated with 44.73% share in 2025; Tyvek and HDPE materials are expected to advance at a 9.11% CAGR over the forecast period.

- By end user, hospitals accounted for 61.76% of 2025 sales, while dental clinics hold the fastest trajectory with an 8.24% CAGR through 2031.

- By geography, North America secured 33.64% of 2025 global revenue; Asia-Pacific is set to grow at a 9.55% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bowie-Dick Test Pack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Procedure Volumes Requiring Daily Sterilizer Verification | +1.2% | Global, focus on North America, Europe, urban APAC | Medium term (2-4 years) |

| Stringent Regulatory Guidelines Mandating Bowie-Dick Testing | +1.0% | North America, Europe, South Korea, GCC | Long term (≥ 4 years) |

| Growing CSSD Automation Driving Routine Documentation | +0.9% | North America, Western Europe, Japan, Australia | Medium term (2-4 years) |

| Expansion of Hospital Infrastructure in Emerging Markets | +1.1% | China, India, Southeast Asia, Middle East, Latin America | Long term (≥ 4 years) |

| Mini-Benchtop Autoclave Uptake in Dental/Ophthalmic Clinics | +0.7% | Early adoption in North America, Western Europe | Short term (≤ 2 years) |

| RFID-Enabled Smart Test Packs Enabling Digital Traceability | +0.6% | North America, Germany, Nordics, Singapore | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Procedure Volumes Requiring Daily Sterilizer Verification

Elective and urgent surgeries rebounded in 2024 and 2025 as hospitals cleared pandemic-era backlogs, boosting the number of steam-sterilizer cycles performed each day. U.S. outpatient visits reached 883 million in 2024, up 4.7% over 2023, while inpatient admissions climbed to 35.1 million.[1]American Hospital Association, “Fast Facts on U.S. Hospitals, 2024,” American Hospital Association, aha.org Each pre-vacuum sterilizer must pass a Bowie-Dick test before processing the first load, so a 200-bed hospital running three units consumes roughly 1,095 packs per year. Ambulatory surgical centers (ASCs) that handled more than 28 million U.S. procedures in 2024 have begun installing small autoclaves on-site to accelerate instrument turnaround.[2]Centers for Medicare & Medicaid Services, “Medicare Provider Utilization and Payment Data,” Centers for Medicare & Medicaid Services, cms.govAs distributed reprocessing spreads across ASCs, ophthalmology centers, and specialty clinics, incremental demand for compact Bowie-Dick test packs rises. This driver delivers consistent volume growth that underpins the Bowie-Dick test pack market.

Stringent Regulatory Guidelines Mandating Bowie-Dick Testing

ISO 11140-4:2024 widened performance parameters for Type 2 chemical indicators, obliging suppliers to validate consistency across steam qualities.[3]International Organization for Standardization, “ISO 11140-4:2024—Sterilization of Health Care Products,” International Organization for Standardization, iso.org AAMI ST-79:2024 codified the daily Bowie-Dick test as non-negotiable and banned re-use of single-use packs. The FDA’s 2025 reprocessing guidance cited non-compliance as grounds for Class I recalls. Accreditation agencies such as The Joint Commission now review electronic test logs during inspections, making documented pass/fail outcomes essential for licensure. Regulators in South Korea and GCC states aligned local rules with ISO benchmarks in 2025, further broadening the global enforcement footprint.

Growing CSSD Automation Driving Routine Documentation of Test Results

Hospital sterile-processing teams are adopting digital track-and-trace systems that scan barcodes on Bowie-Dick packs and upload results to the electronic health record. STERIS’s Instrument Management System and Getinge’s T-DOC platform both add anomaly detection that flags partial color changes and recommends preventive maintenance. A 2025 International Association of Healthcare Central Service Materiel Management survey found 62% of U.S. hospitals with more than 300 beds had installed or piloted digital CSSD platforms, up from 41% in 2023. Automated logs reduce paperwork, support audit readiness, and elevate preference for digital Bowie-Dick devices that transmit data directly to these systems.

Expansion of Hospital Infrastructure in Emerging Markets

China intends to add 1,200 tertiary hospitals by 2030, each equipped with multiple pre-vacuum sterilizers, generating annual demand approaching 876,000 packs. India’s Ayushman Bharat Health Infrastructure Mission and ADB-financed projects in Southeast Asia are funding new district hospitals that must meet daily sterilizer-validation standards. Projects such as King Salman Medical City in Saudi Arabia adopt international CSSD layouts that standardize test-pack procurement. These greenfield facilities create multi-year tailwinds for the Bowie-Dick test pack market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Low-Temperature Sterilization Technologies | −0.8% | Global, led by North America and Western Europe | Long term (≥ 4 years) |

| Re-Use of Single-Use Test Packs in Cost-Constrained Settings | −0.5% | South Asia, Sub-Saharan Africa, Latin America | Short term (≤ 2 years) |

| Medical-Grade Crepe-Paper Supply Constraints | −0.6% | Global, acute in Europe and North America | Medium term (2-4 years) |

| Sustainability Regulations Discouraging Disposable Packs | −0.4% | European Union, California, select Canadian provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Low-Temperature Sterilization Technologies

Hospitals installing vaporized hydrogen peroxide (VHP) and ethylene oxide alternatives reduce reliance on pre-vacuum steam and eliminate the need for Bowie-Dick testing altogether. STERIS’s V-PRO line recorded double-digit unit growth in 2025, fueled by demand to reprocess heat-sensitive robotic instruments. The EPA’s 2024 emission rule around ethylene oxide accelerated VHP adoption by tightening air-pollutant limits. Getinge’s Sterizone VP4 gained FDA clearance for more device materials in 2025, broadening low-temperature applicability. Though still only 15-20% of the sterilizer base, these units erode the installed foundation that drives Bowie-Dick test pack consumption.

Re-Use of Single-Use Test Packs in Cost-Constrained Settings

A 2024 WHO survey found 47% of district hospitals in 18 African nations reused single-use packs at least once, undermining indicator accuracy. Degraded cellulose alters air-removal resistance, risking false negatives that conceal sterilizer failure. While AAMI ST-79 prohibits re-use, enforcement remains weak where inspections are infrequent and budgets tight. Manufacturers offering lower-cost packs still struggle with fragmented supply chains, prolonging the practice and dampening legitimate sales in emerging economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Devices Gain Traction Amid Documentation Mandates

Digital devices are forecast to expand at 10.22% CAGR through 2031 as hospitals look for automated data capture that links directly to sterilization logs. The traditional paper-based segment retained 53.13% Bowie-Dick test pack market share in 2025, reflecting familiarity and low cost. Helix-type PCDs serve niche endoscope workflows, while indicator sheets appeal to facilities that assemble packs in-house despite regulatory pushback. Large health networks favor digital packs because accreditation audits increasingly insist on electronic records, a dynamic that pushes suppliers to bundle cloud dashboards with consumables. Solventum’s FDA-cleared Attest Rapid Readout device demonstrates the pace of innovation, offering a 1-hour incubation that supports same-day implant release.

Digital adoption varies by region. North American IDS chains and many EU university hospitals embed digital Bowie-Dick modules into their enterprise CSSD software. Emerging markets still prioritize unit cost, but as electronic health record penetration climbs, even mid-tier hospitals will view manual logbooks as operational risk. Overall, the Bowie-Dick test pack market benefits from a twin-track landscape where low-cost paper packs secure volume and digital devices secure margin while fulfilling compliance requirements for real-time documentation.

By Form Factor: Re-Usable Electronic PCDs Challenge Disposable Dominance

Disposable packs accounted for 61.54% of sales in 2025, yet re-usable electronic PCDs are growing 10.76% CAGR as hospitals weigh total cost of ownership and waste-reduction goals. Facilities performing more than 250 cycles a month can amortize a USD 300 electronic PCD inside three years, driving adoption in Germany, the Nordics, and high-volume U.S. centers. Indicator sheets remain popular in Latin America and South Asia, but regulatory shifts that forbid re-use erode their economic appeal. Hybrid formats pairing a low-cost disposable with a clip-on transmitter attract ASCs seeking digital logs without large capital outlays.

Terragene field trials logged 10,000 cycles on a single electronic unit without recalibration, easing concerns about device lifespan. STERIS introduced a lithium-ion model in 2025 rated for 500 tests and firmware updates via USB-C. Environmental, social, and governance (ESG) reporting pushes healthcare systems toward solutions that shrink landfill output, positioning re-usable formats as a strategic hedge. As regulatory pressure on disposables builds, the Bowie-Dick test pack market may see form-factor migration similar to the shift from single-use laparoscopic instruments to re-posable platforms.

By Material Type: Tyvek and HDPE Gain Ground on Supply Resilience

Crepe paper held 44.73% share in 2025 due to legacy usage and proven steam-permeation traits, yet Tyvek and HDPE substrates are poised for 9.11% CAGR through 2031. Hospital buyers appreciate Tyvek’s tear resistance and damp-heat stability, especially after DuPont’s 15% capacity expansion reduced order backlogs in 2024. HDPE packs resonate in Japan and South Korea, where incineration without dioxin generation is a purchasing criterion. Non-woven synthetics gain share where sterilizer OEMs warn against cellulose fiber shedding. PLA films remain experimental but signal future moves toward biodegradable options.

Raw-material diversification mitigates crepe-paper shortages and aligns with hospital ESG goals. Indicator-ink chemistries have been reformulated to adhere reliably to hydrophobic Tyvek surfaces, overcoming earlier technical challenges. As materials evolve, suppliers differentiate on both performance and supply-chain security, influencing purchasing decisions in the Bowie-Dick test pack market.

By End User: Dental Clinics Emerge as Fastest-Growing Segment

Hospitals consumed 61.76% of packs in 2025 thanks to their high sterilizer count and daily test protocol. Dental clinics, however, are growing at 8.24% CAGR as benchtop autoclave installations surge following ADA guideline revisions. ASCs that performed 28.3 million U.S. procedures in 2024 increasingly sterilize on-site, spurring demand for small-chamber test packs. Pharmaceutical plants remain steady users, though adoption plateaus as single-use bioreactors reduce steam-in-place steps. Device manufacturers rely on packs for batch validation under ISO 13485, keeping demand stable.

Group purchasing organizations (GPOs) lock large hospital chains into multi-year contracts, whereas independent dental offices purchase through distributors, creating a fragmented but fast-growing opportunity. Vendors that tailor compact packs and digital readers for single-practitioner settings can capture incremental share. As accreditation scrutiny intensifies across outpatient sectors, the Bowie-Dick test pack industry stands to broaden its customer base beyond traditional acute-care hospitals.

Geography Analysis

North America controlled 33.64% of the Bowie-Dick test pack market in 2025, supported by stringent AAMI ST-79 enforcement, high surgical volumes, and early uptake of digital verification systems. Roughly 6,090 U.S. acute-care hospitals operate centralized CSSDs that often run multiple pre-vacuum sterilizers, each requiring a weekday test. Canada synchronized provincial standards with ISO 11140-4 in 2024, producing a procurement wave for compliant packs. Mexico’s IMSS pipeline will add 50 public hospitals by 2027, though budget constraints slow migration from in-house assembled to ISO-certified options. Adoption of RFID-enabled packs is concentrated among U.S. IDNs focused on enterprise analytics.

Asia-Pacific is poised to grow at 9.55% CAGR between 2026 and 2031, the highest among all regions. China’s tertiary hospital expansion alone demands tens of thousands of packs per new facility. India’s NABH accreditation updates and Southeast Asia’s ADB-funded hospital projects replicate the trend, pushing imported and domestic suppliers to scale production. Mature markets such as Japan and South Korea shift toward digital devices and re-usable PCDs in line with nationwide hospital-digitalization programs. Australia’s updated AS/NZS 4187 guidance reinforces daily test requirements, ensuring steady demand regardless of facility size.

Europe represents a sizable but maturing opportunity. Germany, France, and the United Kingdom account for more than half of regional consumption, yet EU sustainability directives encourage reusable devices that may cap disposable-pack volume growth. Nordic and Benelux countries lead pilots that target a 10-15% reduction in single-use packs by 2030. Southern and Eastern Europe deploy EU structural funds for hospital upgrades, sustaining mid-single-digit growth. In the Middle East, GCC states invest in medical-tourism ventures that specify ISO-compliant sterilization consumables; African growth remains uneven due to funding variability but improves as multinational donors finance infection-control upgrades. South America, led by Brazil and Argentina, sees private hospital chains align with international standards to attract foreign patients, but economic swings temper pace.

Competitive Landscape

Key suppliers account for slightly more than half of global revenue, leaving ample room for regional distributors and pack assemblers. STERIS reported USD 3.24 billion in Healthcare segment revenue for fiscal 2024, bundling consumables with capital equipment to build sticky customer relationships. Getinge’s Infection Control sales reached SEK 11.2 billion (USD 1.05 billion) in 2024, illustrating similar integration. White-space opportunities lie in ASCs, dental clinics, and ophthalmic practices, segments underserved by traditional hospital-focused catalogs.

Sustainability and digitization now separate leaders from laggards. Terragene markets electronic PCDs that eliminate single-use waste and qualify for green-procurement credits in EU hospitals. Suppliers offering RFID packs or cloud reporting platforms can command price premiums and secure multi-site contracts from integrated delivery networks. GPOs such as Vizient and Premier negotiate national tenders that set pricing and volume guarantees for 2-3 years, posing barriers to new entrants unless they deliver unique value like re-usable devices. Patent activity concentrates on indicator chemistry tuned to new steam-quality profiles and on packaging designs that extend shelf life, though no single breakthrough appears imminent.

Regional pack assemblers remain competitive by purchasing bulk indicator sheets and compiling them into customized kits for local hospitals. While unit prices run lower, quality variability and regulatory scrutiny could squeeze these players as ISO 11140-4 enforcement tightens. Overall, the Bowie-Dick test pack market balances high-margin integrated offerings from multinationals with price-driven sales from local contenders, yielding a competitive but not overcrowded field.

Bowie-Dick Test Pack Industry Leaders

Propper Manufacturing Co. Inc.

STERIS plc

Solventum

Terragene S.A.

Getinge AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Lister expanded operations to Hangzhou, launching high-tech sterilization-validation solutions for medical, pharmaceutical, and industrial users.

- May 2025: Solventum introduced the Attest eBowie-Dick Test System, an electronic card and auto-reader that eliminates visual interpretation and manual record-keeping.

Global Bowie-Dick Test Pack Market Report Scope

A Bowie-Dick (BD) test pack is a disposable chemical indicator used to verify the effectiveness of air removal and steam penetration in prevacuum steam sterilizers (autoclaves).

The Anti-Neprilysin Drugs Market Report is segmented by Drug Type, Indication, Dosage Form, Distribution Channel, and Geography. By Drug Type, the market is segmented into Small-Molecule Inhibitors, Biologic Antibodies & Peptides, and Dual-Target Candidates. By Indication, the market is segmented into HFrEF, HFpEF/HFmrEF, Hypertension, Pain & CNS, and Alzheimer’s Disease. By Dosage Form, the market is segmented into Tablets, Suspension, and Injectables. By Distribution Channel, the market is segmented into Hospital, Retail, and Online & Specialty. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Traditional Paper-based Bowie-Dick Pack |

| Helix Type Process-Challenge Device |

| Digital Bowie-Dick Test Device |

| Indicator Sheets / Strips |

| Others |

| Disposable Paper-based Test Pack |

| Re-usable Electronic / Digital PCD |

| Indicator Sheets / Strips for In-house Pack Assembly |

| Hybrid (Disposable Pack + Digital Reader) |

| Crepe Paper |

| Tyvek / HDPE |

| Non-woven Synthetic |

| Mixed Cellulose Composites |

| Others |

| Hospitals |

| Ambulatory Surgical Centres |

| Pharmaceutical & Biotechnology Facilities |

| Medical Device Manufacturers |

| Dental Clinics |

| Research & Academic Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Traditional Paper-based Bowie-Dick Pack | |

| Helix Type Process-Challenge Device | ||

| Digital Bowie-Dick Test Device | ||

| Indicator Sheets / Strips | ||

| Others | ||

| By Form Factor | Disposable Paper-based Test Pack | |

| Re-usable Electronic / Digital PCD | ||

| Indicator Sheets / Strips for In-house Pack Assembly | ||

| Hybrid (Disposable Pack + Digital Reader) | ||

| By Material Type | Crepe Paper | |

| Tyvek / HDPE | ||

| Non-woven Synthetic | ||

| Mixed Cellulose Composites | ||

| Others | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centres | ||

| Pharmaceutical & Biotechnology Facilities | ||

| Medical Device Manufacturers | ||

| Dental Clinics | ||

| Research & Academic Laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Bowie-Dick test pack market in 2026?

The Bowie-Dick test pack market size is valued at USD 243.96 million in 2026.

What is the outlook for digital Bowie-Dick test devices?

Digital devices are projected to grow at 10.22% CAGR through 2031 as hospitals adopt automated documentation solutions.

Which region offers the fastest growth potential?

Asia-Pacific is forecast to record a 9.55% CAGR through 2031 due to aggressive hospital construction and regulatory upgrades.

Why are dental clinics becoming important customers?

Updated 2025 ADA infection-control guidelines require daily Bowie-Dick testing for benchtop autoclaves, driving rapid uptake in dental practices.

How are sustainability regulations affecting purchasing decisions?

EU and California rules that penalize disposable waste are encouraging hospitals to pilot re-usable electronic PCDs to reduce landfill output and life-cycle costs.

Which companies lead the competitive landscape?

STERIS, Getinge, Solventum, Cantel Medical, and 3M’s legacy portfolio collectively hold about 55-60% of global revenue.

Page last updated on: