Boric Acid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

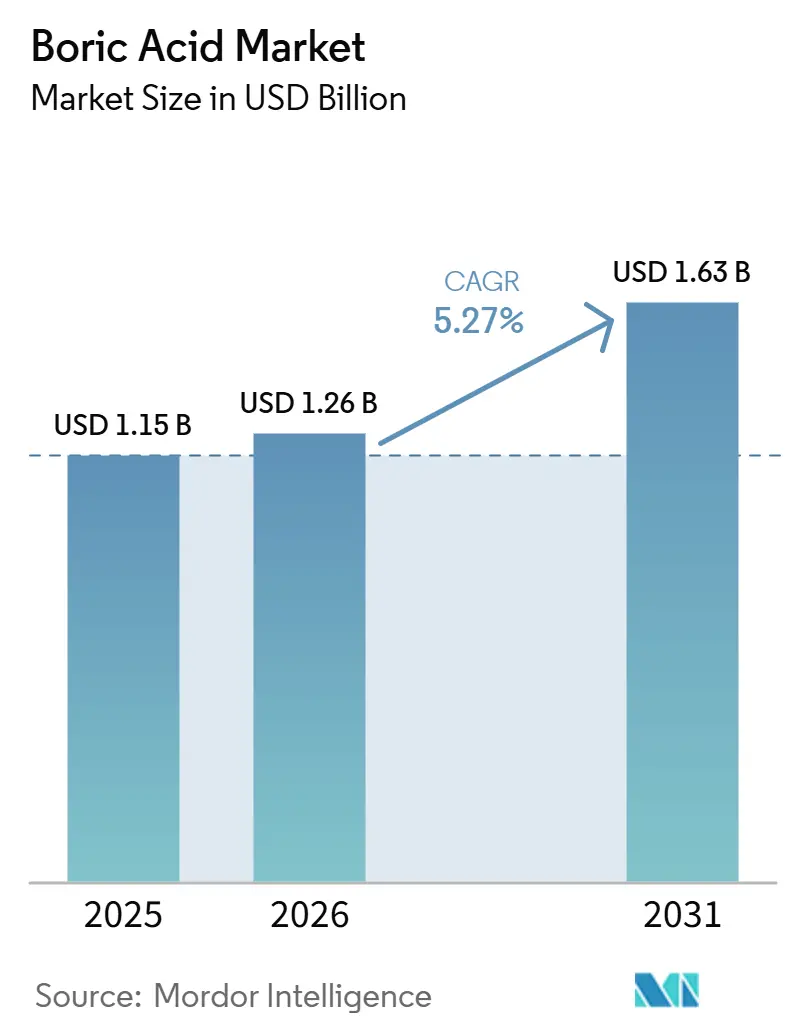

| Market Size (2026) | USD 1.26 Billion |

| Market Size (2031) | USD 1.63 Billion |

| Growth Rate (2026 - 2031) | 5.27% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Boric Acid Market Analysis by Mordor Intelligence

The Boric Acid Market size was valued at USD 1.15 billion in 2025 and is estimated to grow from USD 1.26 billion in 2026 to reach USD 1.63 billion by 2031, at a CAGR of 5.27% during the forecast period (2026-2031). The boric acid market continues to expand, with fiberglass and borosilicate glass accounting for a large share of demand. Both applications rely on boric acid for its flux behavior, thermal stability, and flame performance, which are difficult to replace within existing production systems. Turkey remains central to the boric acid market as Eti Maden controls 73% of the world's economically recoverable boron reserves. Its 2024 refined borate output reached 3 million metric tons, a 20% increase over 2023, reinforcing supply discipline at the upstream stage. The market is also seeing a gradual shift in application mix as pharmaceutical and electronics end uses take on a larger role, driving demand toward higher-purity grades, tighter documentation, and multi-step qualification processes. This shift presents an opportunity for suppliers to move beyond commodity tonnage and serve regulated, higher-purity, or application-specific demand with reliable quality systems, while continuing to supply large-volume glass and construction end uses. At the same time, the market remains exposed to regulatory pressure in Europe and parts of North America, which limits consumer-facing applications and raises handling, labeling, and compliance costs for producers and downstream users.

Key Report Takeaways

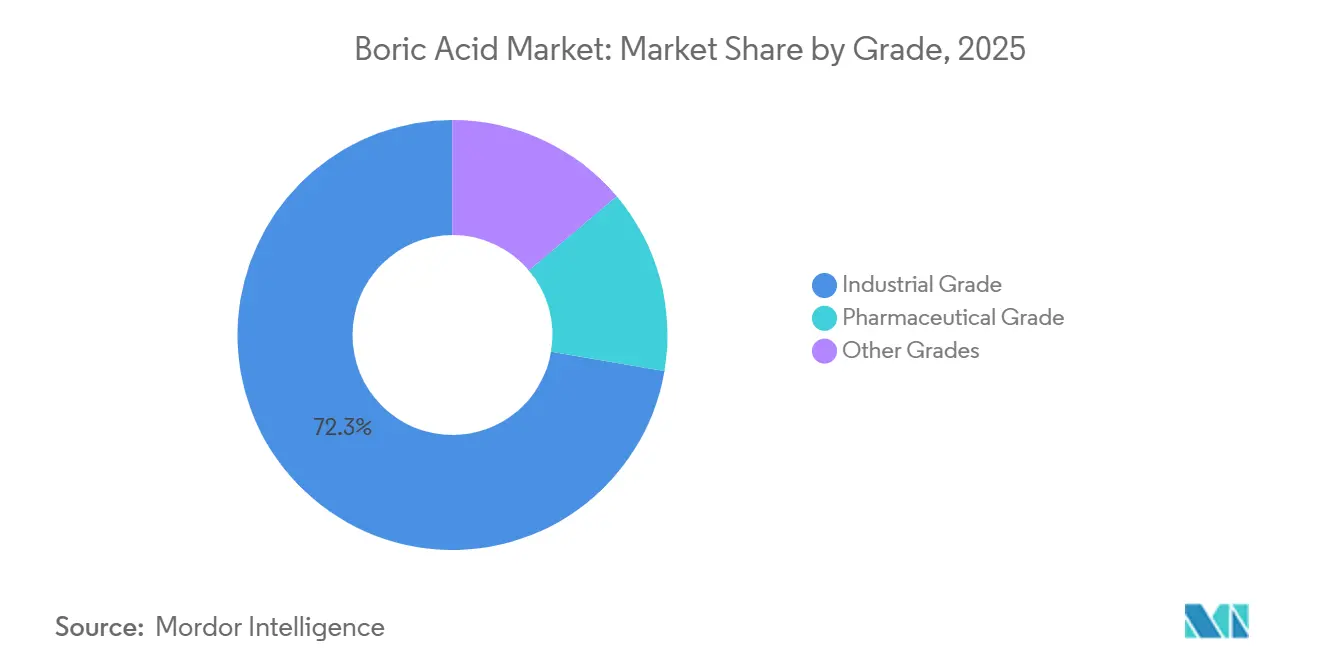

- By grade, industrial grade held 72.33% of the boric acid market share in 2025, while pharmaceutical grade is projected to expand at a 6.22% CAGR through 2031.

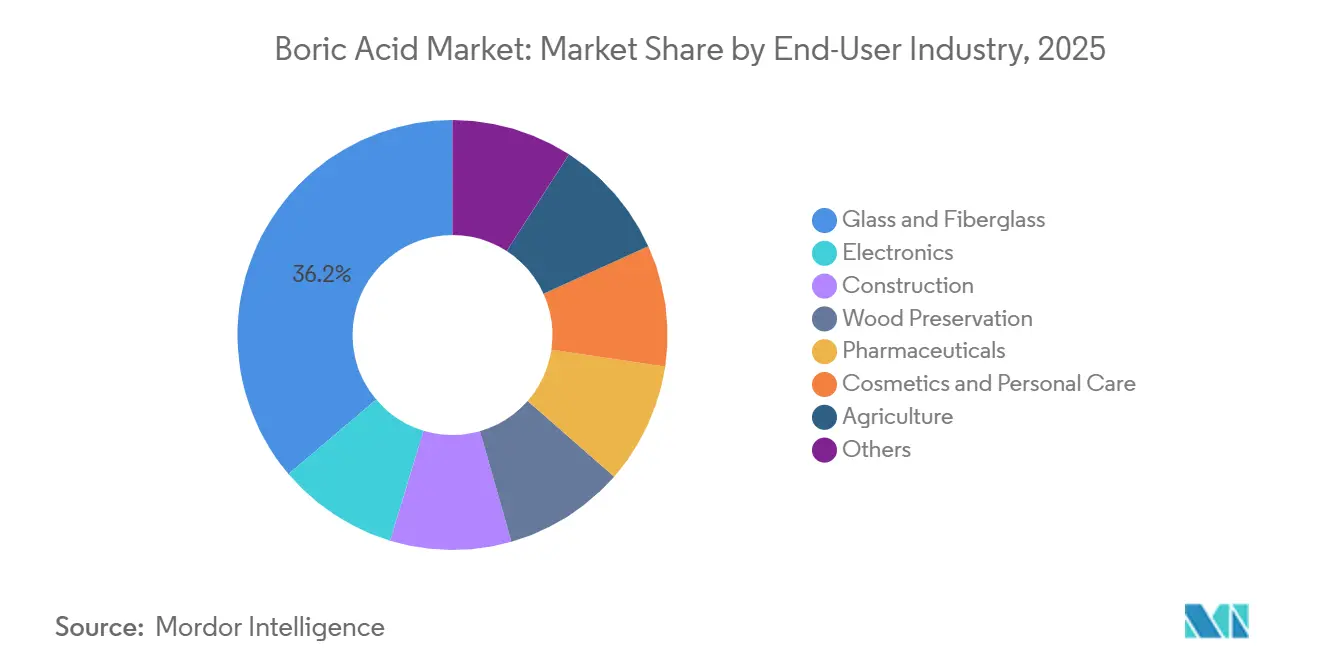

- By end-user industry, glass and fiberglass accounted for 36.18% of demand in 2025, while electronics are forecast to grow at a 6.51% CAGR through 2031.

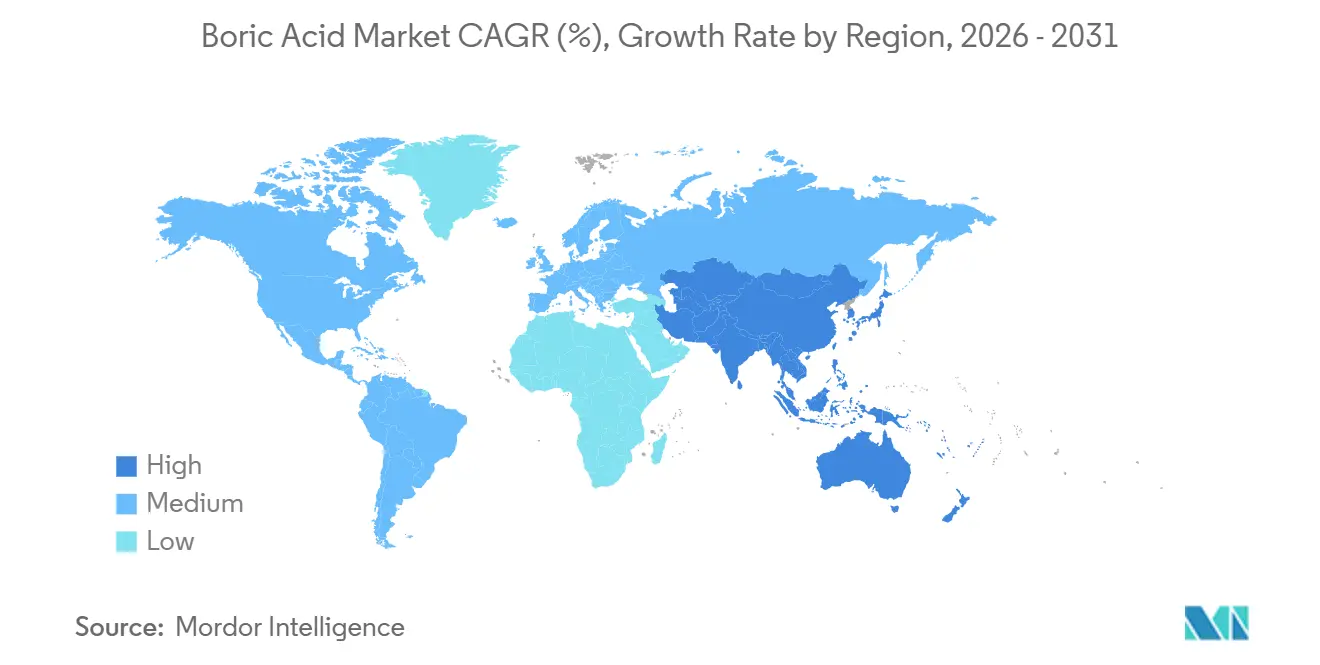

- By geography, Asia-Pacific held 43.15% of global demand in 2025, and the region is projected to advance at a 7.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Boric Acid Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Glass and Fiberglass | +2.1% | Global, particularly Asia-Pacific, North America, EU | Short term (≤ 2 years) |

| Expanding Use in Flame Retardants | +1.2% | Global, concentrated in North America and the EU | Medium term (2-4 years) |

| Growing Pharmaceutical Applications | +0.9% | Asia-Pacific, North America | Medium term (2-4 years) |

| Shift Toward Higher-Purity Grades | +0.6% | Asia-Pacific core, Japan, South Korea, Taiwan, China | Long term (≥ 4 years) |

| Increasing Substitution of Halogenated Compounds by Boron-Based Alternatives | +0.4% | North America and the EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Glass and Fiberglass

Fiberglass insulation and reinforcement composites represent the largest demand for boric acid, providing the market with a broad industrial base across construction, transportation, and engineered materials. In melt processes, boric acid reduces energy consumption during production and improves thermal stability and fire resistance in finished insulation materials, making it integral to both plant designs and product specifications. The American Chemistry Council reported continued growth in non-residential construction activity and energy-efficiency retrofits in North America through 2024, which supported fiberglass demand even as broader manufacturing conditions were less uniform[1]American Chemistry Council, “Non-Residential Construction Activity and Energy Efficiency in North America,” americanchemistry.com. This is significant for the boric acid market because retrofit activity generates replacement and upgrade demand independent of new construction cycles, making the insulation link more resilient than many commodity chemical end uses. The supply side reinforces this pattern, as boric acid remains tied to furnace settings, melt behavior, and equipment configurations that are not easily modified once a fiberglass line is operating at scale. As a result, the boric acid market benefits not only from increased building activity but also from the persistence of a material system that is already deeply integrated into insulation and reinforcement manufacturing.

Expanding Use in Flame Retardants

The boric acid market is gaining support from flame retardant applications because boron-based systems align more readily with stricter product safety regulations in construction boards, foams, textiles, and electrical insulation. Boric acid, zinc borate, and related boron compounds work through combustion inhibition pathways that help formulators meet fire performance targets while avoiding some of the regulatory burden associated with older halogen-based systems. Research published in Frontiers in Forests and Global Change confirmed the thermal performance of boron compounds in engineered wood and composite panel systems, supporting their growing role in structural and building material applications. The boric acid market also benefits from the shift away from brominated flame retardants, as compliance-driven material changes tend to move slowly at first and then become difficult to reverse once new formulations are qualified. This gives boron-based chemistries a practical advantage in applications where fire performance, regulatory compliance, and weight reduction must be balanced within the same formulation. The same dynamic explains why the boric acid market is not only retaining legacy flame retardant uses, but also strengthening its position as a replacement option where halogenated systems face increasing restrictions.

Growing Pharmaceutical Applications

The boric acid market is finding a wider range of pharmaceutical uses as demand extends beyond traditional ophthalmic and topical products into buffering, excipient, antifungal, and regulated formulation roles. India's pharmaceutical sector is projected to reach USD 130 billion by 2030, with growth above 10%, underscoring the rising demand for higher-purity boric acid across domestic production and export-oriented manufacturing. While pharmaceutical demand is smaller in tons than glass demand, it carries stricter purity thresholds, more extensive documentation requirements, and more stable pricing for qualified suppliers. Merck KGaA's EMPROVE API offering illustrates the level of compliance infrastructure required in this segment of the boric acid market, including International Council for Harmonization (ICH) Q7 alignment and support through Certificate of Suitability of the European Pharmacopeia (CEP) and US Drug Master File documentation. Once suppliers meet these standards, they gain access to customers that prioritize supply continuity, audit readiness, and validated quality systems over short-term price considerations. For this reason, the boric acid market is gradually developing a more stable revenue base through pharmaceutical use, even as volume growth continues to be driven by industrial applications.

Shift Toward Higher-Purity Grades

The boric acid market is shifting toward a more valuable product mix as semiconductor and precision electronics applications require very low contamination levels and consistent product performance. At advanced nodes below 7 nm, boric acid-based materials support silicon doping, gettering, chemical-mechanical planarization, and related process steps, where trace contamination can reduce wafer yields and increase manufacturing losses. This changes the economics of the boric acid market because producers with ion exchange, multi-stage crystallization, and cleanroom processing capabilities can command higher premiums than suppliers focused solely on technical grades. The transition also narrows the gap between commodity supply and premium pricing, as more end users now require documentation, repeatability, and purity rather than bulk availability alone. In practical terms, the boric acid market is becoming more segmented by process control and specification depth, rather than by grade names or traditional end-use categories. This shift favors suppliers that can maintain consistency over long qualification cycles, as semiconductor and electronics customers are generally unwilling to change qualified raw materials once production lines are established.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toxicity and Handling Concerns | -1.5% | EU, highest impact, North America, spillover to MEA and APAC via export compliance | Medium term (2-4 years) |

| Tightening Product Standards and Compliance Costs | -0.8% | Global, EU highest regulatory burden | Medium term (2-4 years) |

| Substitution Risk from Alternative Materials | -0.7% | North America and the EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Toxicity and Handling Concerns

The boric acid market faces a restraint from chemical safety regulations. Boric acid is classified under the EU Classification, Labeling and Packaging (CLP) framework as a Reproductive Toxicant Category 1B[2]European Chemicals Agency, “Boric Acid Substance Information, REACH Registration Dossier,” echa.europa.eu. This classification affects labeling, worker protection, documentation, and customer acceptance, particularly in consumer-facing or lightly processed applications where alternative ingredients are easier to adopt. Annex XVII restrictions under the Registration, Evaluation, Authorization and Restriction of Chemicals (REACH) limit concentrations above 0.1% by weight in consumer mixtures, which narrows product scope and requires reformulation in parts of the cosmetics and personal care segments. The market, therefore, absorbs costs beyond raw material handling, as closed-loop systems, training programs, and compliance documentation must be maintained across the value chain. Large suppliers can absorb these costs more readily, while mid-sized participants have less scale and limited ability to spread compliance spending across multiple product lines. The overall effect is a narrowing of addressable uses in lower-value consumer channels and a shift toward industrial, professional, and tightly controlled applications.

Substitution Risk from Alternative Materials

The boric acid market faces substitution pressure in construction and polymer systems where competing materials can deliver acceptable performance without boric acid as a processing aid. The United States Geological Survey (USGS) identified cellulose, foams, and mineral wool as established substitutes for boron-based insulation materials in construction, confirming that replacement risk exists in selected applications. Cellulose-based insulation and mineral wool are gaining traction in projects that emphasize moisture management, embodied carbon, or specification diversity, which can reduce boric acid demand in some building envelope systems. In agriculture, more targeted micronutrient programs and boron-free chelated blends can replace part of the demand that would otherwise go to standard boron supplementation in broad-acre applications. The market is less exposed in glass manufacturing, where boric acid is embedded in equipment settings and product requirements, but more exposed in foams, textiles, and other applications where formulation changes are more practical. This results in a mixed substitution profile, with protection in core industrial uses and pressure in parts of insulation, flame retardant, and nutrient formulation demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Industrial Dominance Sustained, Pharmaceutical Grade as a Margin Engine

Industrial grade held 72.33% of demand in 2025, keeping this segment at the center of the boric acid market. Glass, ceramics, construction, flame retardants, wood preservation, and agriculture all draw on large and recurring volumes. The segment's scale reflects the operational reality that a single large fiberglass plant can consume very high annual volumes, making industrial grade closely tied to the broad production base of the boric acid industry rather than to niche applications. This demand base also gives suppliers a volume cushion, since commodity-grade shipments continue to anchor plant utilization, freight efficiency, and customer relationships across multiple end uses even when downstream mix improves. The boric acid market therefore continues to depend on industrial grade for revenue stability, contract visibility, and throughput planning, even as value growth gradually shifts toward more specialized grades. Other grades, including agricultural granular products and laboratory reagents, hold smaller shares but serve defined uses where boron deficiency correction and analytical precision support repeat buying behavior.

Plant science literature has documented boron deficiency across 132 crop varieties in more than 80 countries, supporting the continuing role of boric acid in agricultural correction programs and explaining why non-pharmaceutical specialty grades remain commercially relevant. Pharmaceutical grade is the fastest-growing grade, and the boric acid market size for this segment is projected to expand at a 6.22% CAGR through 2031. Drug manufacturing, antiseptic use, vaginal health formulations, and excipient-related demand all require cleaner and more tightly documented inputs. The segment also benefits from compliance barriers, since current Good Manufacturing Practice (cGMP) requirements, International Council for Harmonisation (ICH) Q7 alignment, and Drug Master File (DMF) or Certificate of Suitability (CEP) support lengthen qualification cycles and reduce the number of acceptable suppliers. Merck KGaA's EMPROVE API portfolio illustrates the standard that customers expect in this segment, with product forms and documentation designed for regulated pharmaceutical use rather than bulk industrial trade. For the boric acid industry, this means the highest-margin grade is supported less by volume and more by qualification depth, audit readiness, and the ability to maintain quality consistency over long production and regulatory cycles.

By End-User Industry: Fiberglass Drives Volume, Electronics Commands the Premium Layer

Glass and fiberglass accounted for 36.18% of 2025 demand, making this segment the main volume base of the boric acid market. Boric acid remains central to insulation materials, structural composites, display substrates, and borosilicate glass production. The boric acid market size for glass and fiberglass stayed dominant because boric acid is converted into boron trioxide and embedded in material systems used for pharmaceutical packaging, laboratory ware, optical products, and other technically demanding glass applications. This segment also has strong process lock-in, since producers design melt chemistry, furnace behavior, and product performance around established boron inputs rather than switching easily between raw materials. In the boric acid market, that lock-in matters as much as volume because it keeps demand tied to installed industrial capacity and specification continuity, rather than short-term pricing cycles. Construction-linked uses reinforce the same pattern, since insulation, boards, and related materials keep fiberglass demand tied to retrofit activity, code-driven efficiency upgrades, and new building projects.

Electronics is the fastest-growing end-user segment, with a 6.51% CAGR, which is lifting the boric acid market through higher purity requirements rather than sheer volume alone. Semiconductor, Liquid Crystal Display (LCD), and photovoltaic applications require cleaner input streams, which allows qualified suppliers to capture a premium layer above standard technical-grade trade. The segment's role is therefore larger than its current volume share suggests, as electronics pulls the boric acid market toward stricter process controls, more advanced purification steps, and longer customer qualification periods. Pharmaceuticals, wood preservation, agriculture, cosmetics and personal care, and other niche uses add breadth to demand, but their growth profiles are shaped by different factors, with regulation supporting some channels and limiting others. Wood preservation retains relevance because boric acid functions as both a fungicide and an insecticide, while cosmetics and personal care face weaker momentum in Europe because consumer mixture restrictions limit where boric acid can still be used at viable concentrations.

Geography Analysis

Asia-Pacific accounted for 43.15% of global boric acid demand in 2025 and is forecast to grow at the fastest rate of 7.66% CAGR. This makes the market most exposed to regional developments in China, India, Japan, South Korea, and nearby manufacturing chains. The region leads due to its large-scale glass and ceramics output, rising pharmaceutical production, and a strong precision electronics base. Demand is spread across both commodity and premium applications rather than being tied to a single industrial segment. China is the largest consumption anchor in the region. Its broad manufacturing scale, combined with domestic boron ore quality limitations, keeps the country structurally dependent on imported material for part of its needs. This import dependence reduces the risk that domestic Chinese oversupply alone could reset global boric acid pricing, as is often the case with other industrial chemicals. India provides a different layer of support, with demand coming from both agriculture and pharmaceuticals. This gives the market seasonal support on one side and year-round process demand on the other. India's pharmaceutical sector is projected to reach USD 130 billion by 2030, which further supports sustained import demand for higher-purity material.

North America plays a distinct role in the boric acid market, as the United States functions as both a major exporter and a large industrial consumer. The United States Geological Survey (USGS) reported that the United States exported approximately 240,000 metric tons of boric acid in 2024, confirming the region's importance as a supply base for international buyers, not only as a demand center. Rio Tinto's U.S. Borax operations in California supply approximately 30% of global boron demand from a single geographic cluster, making North American supply concentrated from a logistics and asset perspective, even before downstream distribution is considered. Canada's demand remains more concentrated in agricultural boron and wood preservation, while Mexico benefits from growing ties to glass and ceramics manufacturing through ongoing regional industrial integration.

Europe's position in the boric acid market is defined by strong industrial demand and high import dependence, with Turkish supply remaining central to regional availability. Regulatory oversight is more stringent in Europe than in most other regions, meaning the market is shaped not only by demand from specialty glass, ceramics, and flame-retardant textiles, but also by handling and use restrictions that influence product mix. This combination of stable industrial demand and tighter compliance requirements favors suppliers that can manage documentation-heavy customer needs and maintain reliable export compliance. South America is relevant both as a producing region and as a consumption base, while the Middle East and Africa rely more heavily on imports. Demand in these regions is driven by selected industrial chemicals, ceramics, mining, and glass applications rather than by a broad domestic supply structure.

Competitive Landscape

The boric acid market is moderately consolidated at the upstream mining and refining stage, while downstream trade, formulation, and specialty distribution are more fragmented. Eti Maden and U.S. Borax together account for well over 80% of global refined borate supply, giving the boric acid market a narrow production base before it reaches more dispersed end-use channels. This structure gives the leading producers considerable influence over contract terms, supply reliability, and grade availability, particularly when buyers prioritize continuity over spot flexibility. It also explains why smaller participants tend to compete more effectively in regional service, packaging, logistics, or specialty grades rather than in large-scale upstream supply. The boric acid market is accessible to many downstream firms, but challenging the leading resource holders on reserves, scale, or integrated refining capacity remains difficult.

Eti Maden's official disclosures show that the Emet Boric Acid Operations Directorate has a capacity of 290,000 metric tons per year, and the company exports more than 95% of its total borate production to international markets, highlighting the boric acid market's dependence on Turkish supply reaching global customers. The U.S. Geological Survey (USGS) recorded Eti Maden's 2024 refined borate production at 3 million metric tons, reflecting a 20% increase over 2023, indicating that the company is actively managing capacity ramp-up and output alongside its large reserve base. This scale, combined with reserve control and export reach, strengthens Eti Maden's position across the boric acid market and raises the bar for competitors seeking volume-based business in glass, construction, and other industrial channels.

Competition becomes more technical in higher-purity and regulated segments of the boric acid market, where customer approval cycles and documentation carry more weight than capacity alone. Merck KGaA illustrates this through its EMPROVE API boric acid, which is supported by ICH Q7-compliant manufacturing standards along with CEP and US-DMF documentation, enabling it to maintain positioning in pharmaceutical supply. This approach demonstrates how qualification depth can be a competitive factor in premium niches, even for suppliers that do not control upstream reserves at the scale of major borate miners. Quiborax identifies itself as the world's third-largest boric acid producer, confirming that the supply base broadens beyond the two leading players even as overall concentration remains high. Mid-tier participants such as Gujarat Boron Derivatives, Inkabor, and Etimine USA compete primarily through regional access and application-focused capability. Opportunities remain in under-served agricultural micronutrient markets and specialized high-purity or isotope-related applications, where certification and service depth can be as important as tonnage.

Boric Acid Industry Leaders

Eti Maden

Rio Tinto (U.S. Borax)

Quiborax S.A.

Minera Santa Rita S.R.L.

Gujarat Boron Derivatives Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The European Commission adopted Commission Implementing Decision (EU) 2026/1128, extending boric acid's approval as an active substance for product type 8 biocides (wood protection) under Regulation (EU) No 528/2012. The decision ensures regulatory continuity for wood treatment manufacturers, construction-sector operators, and biocide distributors across the EU.

- November 2025: Rio Tinto announced the initiation of a formal sale process for its US Borax California assets, comprising the Boron mine and processing facility in the Mojave Desert, the Port of Los Angeles refinery and shipping terminal, and the Owens Lake mining operation. The company engaged UBS and JPMorgan Chase as advisors on a divestiture estimated at up to USD 2 billion. The California operations supply approximately 30% of global boron demand.

Global Boric Acid Market Report Scope

Boric acid, with the chemical formula H₃BO₃, is a weak, naturally occurring Lewis acid commonly found as a white, odorless powder or crystalline solid. It is widely used in household pest control, as a mild antiseptic, and in industrial manufacturing.

The boric acid market is segmented by grade, end-use industry, and geography. By type, the market is segmented into pharmaceutical-grade, industrial-grade, and other grades. By end-use industry, the market is segmented into glass and fiberglass, electronics, construction, wood preservation, pharmaceuticals, cosmetics & personal care, agriculture, and others. The report also covers market size and forecasts for boric acid across 16 countries in major regions. The market sizes and forecasts are provided in terms of value (USD).

| Pharmaceutical Grade |

| Industrial Grade |

| Other Grades |

| Glass and Fiberglass |

| Electronics |

| Construction |

| Wood Preservation |

| Pharmaceuticals |

| Cosmetics & Personal Care |

| Agriculture |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Grade | Pharmaceutical Grade | |

| Industrial Grade | ||

| Other Grades | ||

| By End-User Industry | Glass and Fiberglass | |

| Electronics | ||

| Construction | ||

| Wood Preservation | ||

| Pharmaceuticals | ||

| Cosmetics & Personal Care | ||

| Agriculture | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Boric Acid Market?

The Boric Acid Market size was valued at USD 1.15 billion in 2025 and is estimated to grow from USD 1.26 billion in 2026 to reach USD 1.63 billion by 2031, at a CAGR of 5.27% during the forecast period (2026-2031).

Which grade leads to current demand?

Industrial-grade LED with a 72.33% share in 2025 because it serves fiberglass, ceramics, construction, flame-retardant applications, wood preservation, and agriculture at scale.

Which end-user group is growing the fastest?

Electronics is the fastest-growing end-user segment, with a 6.51% CAGR through 2031, as semiconductor and precision electronics applications require cleaner, more tightly controlled inputs.

Why is Asia-Pacific so important in this space?

Asia-Pacific held 43.15% of demand in 2025 and is forecast to grow at 7.66% CAGR, supported by China’s manufacturing scale, India’s pharmaceutical expansion, and Japan and South Korea’s electronics base.

Page last updated on: