Biphasic External Defibrillator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.63 Billion |

| Market Size (2031) | USD 2.57 Billion |

| Growth Rate (2026 - 2031) | 9.45% CAGR |

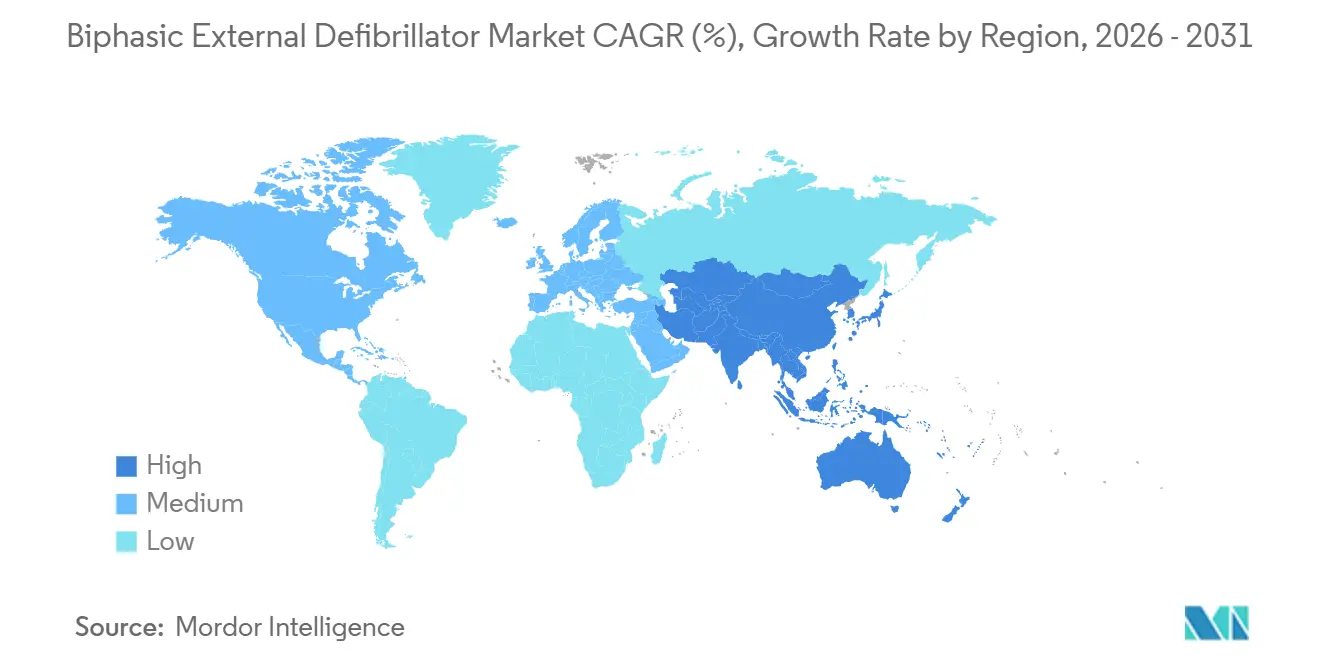

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

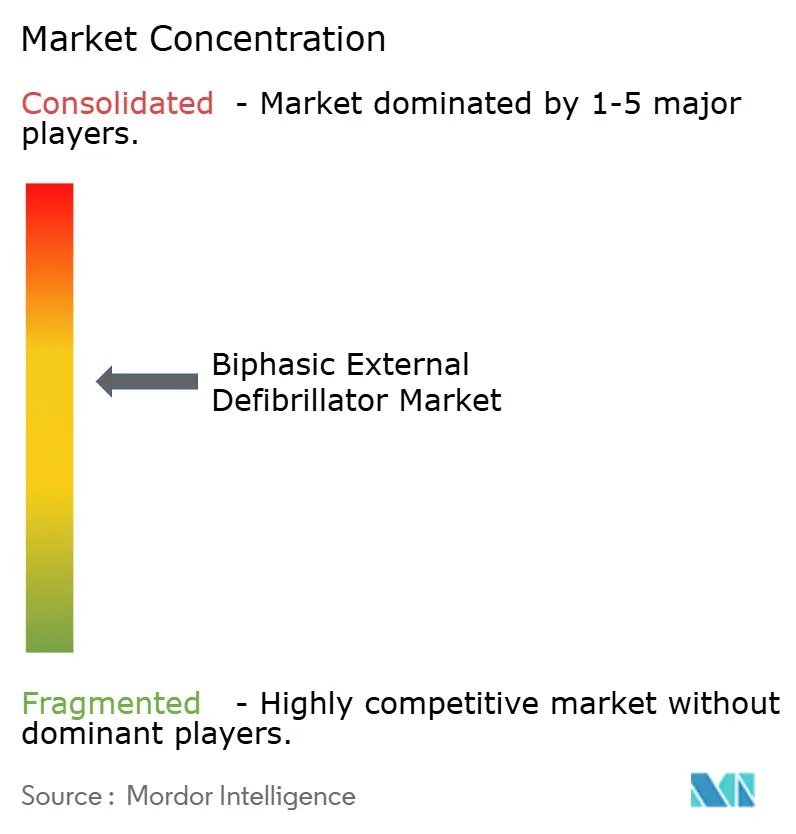

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biphasic External Defibrillator Market Analysis by Mordor Intelligence

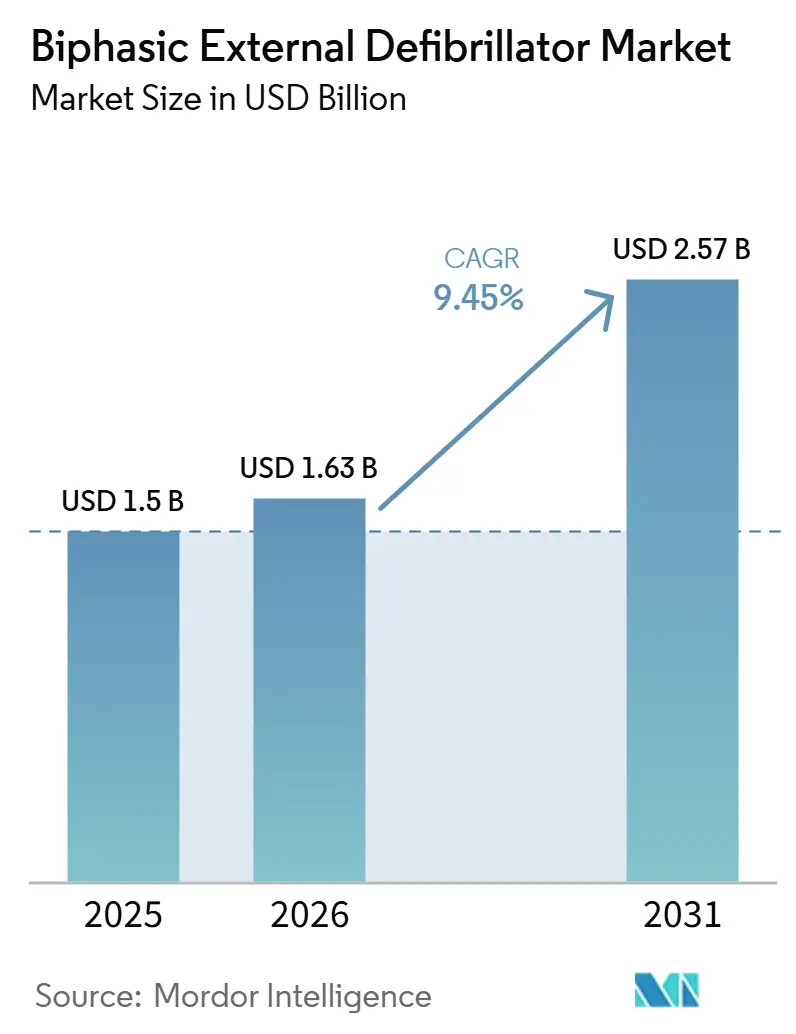

The biphasic external defibrillator market is expected to grow from USD 1.50 billion in 2025 to USD 1.63 billion in 2026 and is forecast to reach USD 2.57 billion by 2031 at 9.45% CAGR over 2026-2031. The biphasic external defibrillator market is expanding because survival after sudden cardiac arrest remains low in many settings, while public and workplace defibrillation is moving closer to a required safety standard in a wider set of venues. The biphasic external defibrillator market is also benefiting from a change in buyer mix, because more demand now comes from schools, workplaces, transit sites, and community facilities that are making first-time installations rather than waiting for hospital replacement cycles. In the biphasic external defibrillator market, competitive advantage is shifting toward device readiness, simple operation, and remote fleet oversight, which is pushing manufacturers to treat software and connectivity as core product features rather than add-ons. The biphasic external defibrillator market still faces friction from recall activity and uneven reimbursement, which can delay refresh cycles and make cost-sensitive institutions hold older units longer than planned. Even with those limits, the biphasic external defibrillator market has durable room for growth through 2031 because policy support, replacement demand, and broader acceptance of early defibrillation are reinforcing each other across clinical and non-clinical settings.

Key Report Takeaways

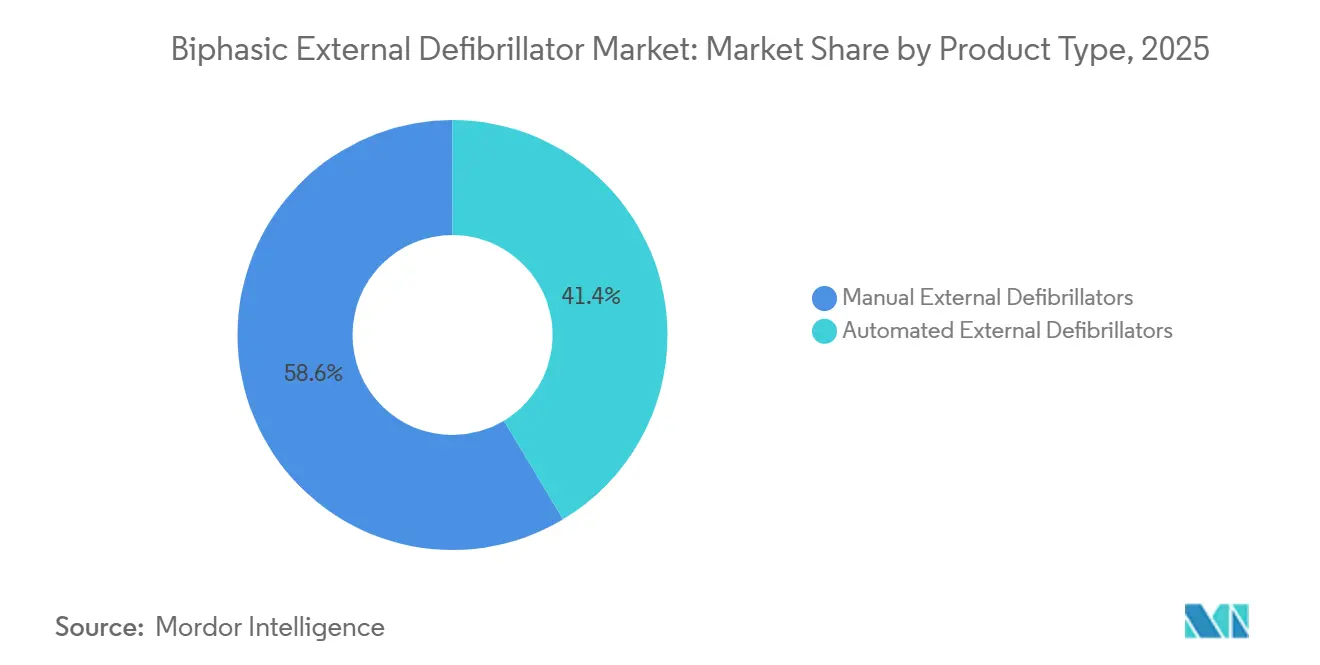

- By product type, automated external defibrillators led with 58.64% revenue share in 2025, and it is also expected to record a CAGR at 10.21% through 2031.

- By technology, the biphasic truncated exponential (BTE) waveform held 56.28% share in 2025, while the rectilinear biphasic waveform is expected to grow at a CAGR at 10.74% through 2031.

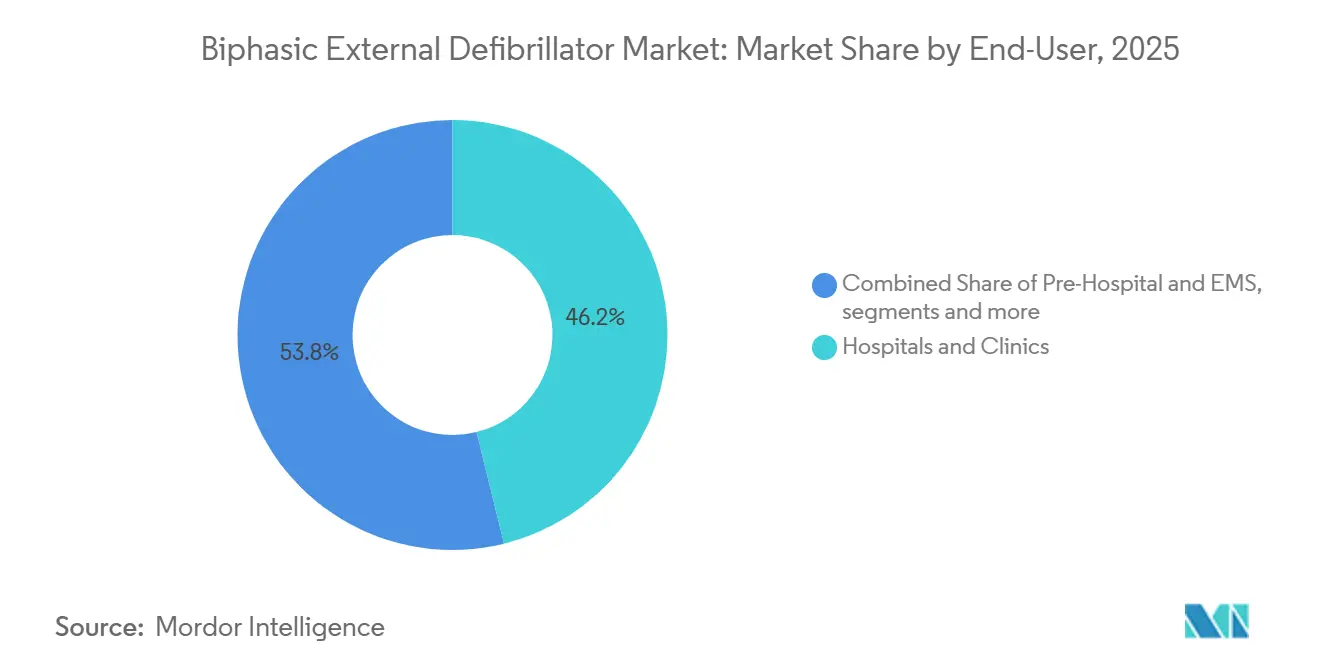

- By end-user, hospitals and clinics accounted for 46.15% share in 2025, while public access settings are anticipated to grow at a CAGR of 9.73% through 2031.

- By geography, North America held 41.83% of revenue in 2025, while Asia-Pacific is projected to have the highest CAGR at 11.87% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Biphasic External Defibrillator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Sudden Cardiac Arrest Burden | +2.2% | Global, concentrated in APAC and North America | Long term (≥ 4 years) |

| Expansion of Public Access Defibrillation Programs | +2.0% | North America and Europe, with early gains in China and Southeast Asia | Medium term (2-4 years) |

| Shift Toward Biphasic, Impedance-Compensated Waveforms | +1.5% | Global, with transition concentrated in APAC and MEA | Medium term (2-4 years) |

| Connected AED Adoption and Remote Compliance Monitoring | +1.3% | North America and Europe, expanding to APAC urban centers | Short term (≤ 2 years) |

| Corporate Workplace AED Mandates and ESG Safety KPIs | +1.0% | North America and Europe, expanding to Southeast Asia | Short term (≤ 2 years) |

| AED-as-a-Service Models Lowering Upfront Purchase Barriers | +0.8% | North America core, with spillover to the UK and Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Sudden Cardiac Arrest Burden

Sudden cardiac arrest remains one of the least resolved emergency conditions in acute care, which keeps the need for fast defibrillation high across both clinical and public settings. In the United States, more than 250,000 EMS-treated out-of-hospital cardiac arrest events were recorded in 2024, which shows the continuing scale of the care gap.[1]Sudden Cardiac Arrest Foundation, “Latest Statistics,” Sudden Cardiac Arrest Foundation, sca-aware.org In Europe, the 2025 resuscitation guidelines reported that EMS services treated 55 cases per 100,000 inhabitants each year, which confirms that the burden is not limited to one health system. Each minute of delayed defibrillation reduces survival probability by 7% to 10%, and only 37.9% of CARES-reported out-of-hospital cardiac arrest events in 2025 were witnessed by bystanders, which narrows the window for successful intervention. In the biphasic external defibrillator market, this burden keeps demand tied to a persistent clinical need rather than a short replacement cycle. The biphasic external defibrillator market is also supported by the fact that organizations face greater operational and legal exposure when no defibrillation option is available at the point of care or at the site of collapse.

Expansion of Public Access Defibrillation Programs

The biphasic external defibrillator market is gaining support from legislation that is steadily moving automated external defibrillator placement from optional practice to a more formal safety obligation. A 2024 analysis in JACC: Advances showed that public access defibrillation laws still vary widely across countries, which leaves room for more formal deployment mandates and program expansion.[2]G.D. Perkins et al., “Gaps in Public Access Defibrillation: Analysis of International Legislation,” JACC: Advances, jacc.org In the United States, the CDC continued to track state-level public access defibrillation laws in 2025, which reflects ongoing policy attention and uneven local adoption patterns. California Assembly Bill 365 expanded workplace AED availability expectations for electrical utility sites, while Maryland required AED placement in food service facilities and extended coverage to additional public venues on the timelines already set by law. The American Heart Association continues to frame workplace and community AED implementation as a practical survival measure rather than a niche intervention, which supports broader administrative buy-in. For the biphasic external defibrillator market, this shift matters because compliance-led purchases are usually less discretionary and less sensitive to short-term budget hesitation than purely elective capital spending.

Shift Toward Biphasic, Impedance-Compensated Waveforms

The biphasic external defibrillator market is also being shaped by a technology transition inside the biphasic category itself, rather than by a simple move away from monophasic systems. Biphasic truncated exponential platforms still account for the largest installed base, which gives them strong protocol familiarity and replacement inertia across hospitals, EMS fleets, and public access programs. A December 2025 medRxiv study that characterized commercial external defibrillator output found that biphasic truncated exponential remained the most prevalent waveform, while rectilinear biphasic designs showed more consistent current delivery across different patient impedance conditions.[3]F. Dörschner et al., “Characterization of External Defibrillator Output and Its Impact on Defibrillation Protection of Medical Equipment,” medRxiv, medrxiv.orgThat difference is important in high-use emergency environments because consistency across patient profiles can influence purchasing preference when organizations move from legacy units to newer systems. Japan added another layer to this transition when the Ministry of Health, Labor and Welfare lifted distribution restrictions on auto-shock AEDs, which opened a simpler operating model for non-clinical public locations. In the biphasic external defibrillator market, replacement decisions are therefore moving beyond basic biphasic adoption and toward a closer review of waveform performance, certification status, and ease of use for untrained responders.

Connected AED Adoption and Remote Compliance Monitoring

The biphasic external defibrillator market is increasingly moving toward connected AED systems that combine emergency response hardware with device monitoring and location management software. Mindray’s AED-Alert 2.0 platform provides remote checks on battery status, pad expiry, and device location through connected monitoring, which shows how fleet readiness is becoming part of the product value proposition. Avive Solutions also built its positioning around a GPS-enabled and 911-integrated connected AED model, supported by USD 56.5 million in growth funding announced in April 2024. As more organizations manage several units across multiple sites, remote compliance monitoring reduces the risk that a device is present but not ready for use at the critical moment. That shifts buying authority toward facility managers, risk officers, and corporate safety teams, which broadens the addressable customer base beyond hospital engineering departments. In the biphasic external defibrillator market, software-enabled oversight is now helping manufacturers defend pricing and service relationships even when basic hardware performance is increasingly standardized.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Acquisition and Lifecycle Maintenance Costs | -1.8% | Global, most acute in MEA, South America, and rural APAC | Long term (≥ 4 years) |

| Limited Reimbursement and Budget Constraints in Emerging Markets | -1.2% | North America and Europe, with fragmented payer coverage | Medium term (2-4 years) |

| Battery, Pad, and Consumable Waste Compliance Burden | -0.6% | APAC and MEA, where supply chain depth is limited | Short term (≤ 2 years) |

| Recalls, Documentation Burden, and Post-Market Surveillance Risk | -0.4% | Global, concentrated in FDA and EU MDR jurisdictions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Acquisition and Lifecycle Maintenance Costs

High unit cost remains one of the clearest limits on adoption in the biphasic external defibrillator market, especially outside large hospital systems and well-funded enterprise accounts. A standalone AED from established vendors typically ranges from USD 1,200 to USD 3,500, and total 10-year ownership cost can rise to USD 4,000 to USD 8,000 once pad replacements, battery changes, and compliance activities are included. That cost profile makes first-time placement harder for small institutions, local governments, and multi-site organizations that need broad coverage rather than a small number of premium units. The problem is not only the purchase price, because fragmented fleet oversight can also lead to missed pad expiry dates, uneven audit performance, and extra service spend. Subscription models help reduce the upfront burden, but the strongest uptake has been concentrated in markets with better service infrastructure and more mature managed-safety procurement models. For the biphasic external defibrillator market, cost remains a major reason why clinically justified deployment still does not always translate into timely purchasing.

Limited Reimbursement and Budget Constraints in Emerging Markets

The biphasic external defibrillator market is also constrained by the fact that most external AED purchases do not follow a clear third-party reimbursement path. Unlike implantable defibrillation systems, external units are commonly funded through capital budgets, public grants, employer spending, or direct institutional purchasing, which can slow buying decisions when budget cycles are tight. In the United States, there is no universal federal insurance coverage requirement for AED purchases, which keeps access dependent on local policy and organizational priorities. In Europe, the European Emergency Number Association has highlighted large disparities in public access defibrillation legislation and program structure, which reinforces an uneven funding and deployment landscape across countries. This matters most in home care, pre-hospital, and lower-income community settings, where earlier access could produce a strong clinical benefit but budget capacity is weakest. In the biphasic external defibrillator market, uneven reimbursement also slows replacement timing because providers often wait for device failure rather than upgrading to newer connected or waveform-enhanced platforms on schedule.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Automated AEDs Dominate on Both Volume and Growth Rate

Automated external defibrillators accounted for 58.64% of revenue in 2025, and this segment of the biphasic external defibrillator market size is projected to expand at 10.21% CAGR through 2031. The same segment is leading in both scale and growth because most new procurement outside hospitals is centered on devices that can be used by non-clinical responders. Schools, workplaces, retail sites, transit hubs, and community venues generally prefer automated models because those systems reduce the need for advanced operator training. That pattern is widening the commercial base of the biphasic external defibrillator industry beyond the traditional hospital buyer. It also makes first-install demand more important than replacement demand in this part of the market.

Manual external defibrillators still hold an essential role in clinical care because hospitals, intensive care units, operating rooms, and EMS teams require ECG visibility, synchronized cardioversion, and direct energy selection during treatment. The biphasic external defibrillator market, therefore, has a clear product split, where automated devices compete on usability, connectivity, and deployment breadth, while manual systems compete on clinical depth and workflow integration. That split is likely to remain stable because the two product types solve different operational problems even when they share the same core resuscitation purpose.

By Technology: BTE Holds the Floor While Rectilinear Biphasic Claims the Premium

Biphasic truncated exponential waveform held 56.28% of the biphasic external defibrillator market share in 2025, which reflects its broad installed base and long replacement cycle in hospitals, EMS fleets, and public access programs. That legacy presence gives BTE systems a durable floor because protocol familiarity, clinician training, and service history all support procurement continuity. At the same time, rectilinear biphasic waveform is the fastest-growing technology, and this part of the biphasic external defibrillator market size is projected to rise at 10.74% CAGR through 2031. The 2025 medRxiv waveform study supported the view that rectilinear designs can deliver more consistent current across changing patient impedance conditions. That performance distinction matters most in professional emergency settings, where variability in body profile and treatment environment is routine.

Advanced smart energy systems form the emerging third layer of the technology mix because they adjust delivered energy using real-time impedance measurement and are more common in premium clinical platforms. Across the biphasic external defibrillator industry, standards such as IEC 60601-2-4 and related risk management requirements create a technical floor that all new devices must meet, which limits purely low-cost entry strategies. Japan’s removal of restrictions on auto-shock AEDs added another technology shift inside automated biphasic devices by removing the shock-button step in selected settings. As a result, technology selection is no longer only about whether a device is biphasic, but also about how well the platform balances installed familiarity, current consistency, energy adaptation, and public-use simplicity.

By End-User: Hospitals Anchor Revenue as Public Settings Claim the Growth Premium

Hospitals and clinics accounted for 46.15% share in 2025, while public access settings are projected to record the fastest CAGR at 9.73% through 2031 in the biphasic external defibrillator market. Hospital demand remains large because crash carts, bedside defibrillators, and cath lab equipment require regular procurement and typically carry higher selling prices than basic public-access AEDs. Pre-hospital and EMS use also supports strong vendor stickiness because buyers in that segment require rugged construction, dependable operation, and protocol consistency across emergency fleets. Public access settings are growing faster because many sites are still making first-time purchases rather than routine replacements. That gives the biphasic external defibrillator market a strong expansion path outside traditional healthcare facilities.

Home care remains the smallest end-user segment, yet aging populations and simpler auto-shock device formats are making household ownership more realistic in select markets. The result is a wider end-user map for the biphasic external defibrillator market, with the highest momentum shifting toward decentralized and community-level coverage.

Geography Analysis

North America held 41.83% of global revenue in 2025, which made it the largest regional block in the biphasic external defibrillator market. The region benefits from an established installed base, stronger emergency care budgets, and a mature culture of workplace and community AED awareness. In 2025, the CDC continued to document state-level public access defibrillation laws, which shows that the legal framework remains active and still differs meaningfully across states. California’s Assembly Bill 365 added new support for AED availability at electrical utility worksites, which broadened the workplace use case further. The American Heart Association also reported that only 50% of workers can locate a workplace AED, which means awareness and placement gaps remain even in the most developed regional market.

Asia-Pacific is projected to post the fastest CAGR at 11.87% through 2031, which gives the region the strongest growth profile in the biphasic external defibrillator market. Regional demand is supported by large unmet need, wide differences in deployment density, and strong room for first-time installation in public and semi-public settings. In China, recent peer-reviewed research on sudden cardiac arrest mortality showed a continuing disease burden and reinforced the need for broader early-response capacity. Japan added an important regulatory catalyst when the Ministry of Health, Labor and Welfare lifted restrictions around auto-shock AED distribution, which lowered one operating barrier for public-space use. Across the Asia-Pacific, this means growth is likely to come more from widening access and first deployment than from mature replacement cycles alone.

Europe remains a significant revenue region in the biphasic external defibrillator market, supported by aging populations, established care systems, and continued reliance on regulated procurement pathways. The EU MDR compliance cycle is pushing healthcare providers to prioritize certified platforms and is encouraging portfolio rationalization among suppliers with broad professional offerings. The European Emergency Number Association has also highlighted wide legislative differences in public access defibrillation across countries, which keeps placement density uneven even within a relatively mature region. The Middle East and Africa and South America remain earlier-stage parts of the biphasic external defibrillator market, but rising cardiovascular burden and health infrastructure expansion are supporting gradual adoption in institutional settings.

Competitive Landscape

The biphasic external defibrillator market shows a moderately consolidated global structure, with major professional-grade revenue concentrated among Asahi Kasei through ZOLL, Stryker, Koninklijke Philips, Medtronic, Nihon Kohden, and others. At the same time, the public access AED segment is more open to new entrants because ease of use, connectivity, and service models can matter as much as legacy hospital relationships. This creates two overlapping competitive arenas inside the biphasic external defibrillator market, one centered on professional monitoring and defibrillation systems, and the other centered on scalable AED deployment. Compliance remains a major barrier for both groups, because FDA quality requirements and EU MDR obligations raise the cost of development, documentation, and post-market follow-up. That barrier protects large incumbents in clinical platforms even when price pressure is increasing in entry-level automated devices.

ZOLL strengthened its clinical position when the Zenix monitor and defibrillator received FDA approval in September 2025 and EU MDR approval in February 2026, which gave the company a fresh product for hospital and EMS workflows in both major regulatory regions. Philips expanded its partnership with Medtronic in August 2025 to deepen access to patient monitoring solutions, which supports broader account control in acute care settings where monitoring and resuscitation purchasing often intersect. Medtronic then received FDA approval in March 2026 for the OmniaSecure defibrillation lead, which helps strengthen its relationships across the wider cardiac care procurement chain. These moves show that leading vendors are defending share through product refresh, adjacent portfolio integration, and deeper health system relationships rather than relying on installed base alone.

The connected AED segment remains one of the clearest white spaces in the biphasic external defibrillator market because many schools, employers, and community organizations still do not manage their fleets through a centralized software layer. Mindray has addressed this through remote device oversight tools, while Avive has built a software-first and cellular-connected model for networked deployment. Overall, the biphasic external defibrillator market is rewarding manufacturers that can combine dependable hardware, regulatory discipline, and service-backed connectivity in one commercial model.

Biphasic External Defibrillator Industry Leaders

Koninklijke Philips N.V.

Stryker Corporation

Nihon Kohden Corporation

Asahi Kasei Corporation

CU Medical Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Medtronic received FDA approval for the OmniaSecure defibrillation lead, the world's first lumenless lead approved for conduction system pacing. The approval positions Medtronic's cardiac rhythm management portfolio as the most clinically versatile among defibrillation system providers and strengthens procurement relationships with hospitals managing both implantable and external defibrillation programs.

- February 2026: ZOLL Medical (Asahi Kasei) received EU Medical Device Regulation 2017/745 (EU MDR) approval for the Zenix monitor/defibrillator, enabling commercialization across European hospital and EMS markets. This followed FDA PMA clearance in September 2025 and completes the global commercial launch of ZOLL's most advanced professional defibrillator.

- January 2026: Ontario's OHSA AED mandate took effect, requiring all construction projects with 20 or more workers active for 3+ months to maintain an on-site AED. The Workplace Safety and Insurance Board (WSIB) simultaneously launched a rebate program of up to USD 2,500 per AED (for purchases through June 2027), directly stimulating first-install procurement across the Canadian construction sector.

Global Biphasic External Defibrillator Market Report Scope

According to the report’s scope, the biphasic external defibrillator market refers to the global market for external defibrillation devices that deliver controlled biphasic electrical shocks to restore normal heart rhythm during sudden cardiac arrest. These devices use advanced waveform technologies to improve efficacy, reduce energy requirements, and minimize myocardial damage compared to monophasic systems.

The biphasic external defibrillator market is segmented into product type, technology, end-user, and geography. By product type, the market is segmented into manual external defibrillators and automated external defibrillators. By technology, the market is segmented into biphasic truncated exponential (BTE) waveform, rectilinear biphasic waveform, and advanced smart energy optimization systems. By end-user, the market is segmented into hospitals and clinics, pre-hospital and EMS, public access settings, and home care settings. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Manual External Defibrillators |

| Automated External Defibrillators |

| Biphasic Truncated Exponential (BTE) Waveform |

| Rectilinear Biphasic Waveform |

| Advanced Smart Energy Optimization Systems |

| Hospitals and Clinics |

| Pre-Hospital and EMS |

| Public Access Settings |

| Home Care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Manual External Defibrillators | |

| Automated External Defibrillators | ||

| By Technology | Biphasic Truncated Exponential (BTE) Waveform | |

| Rectilinear Biphasic Waveform | ||

| Advanced Smart Energy Optimization Systems | ||

| By End-User | Hospitals and Clinics | |

| Pre-Hospital and EMS | ||

| Public Access Settings | ||

| Home Care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in biphasic external defibrillators market through 2031?

The market is projected to grow from USD 1.50 billion in 2025 to USD 1.63 billion in 2026 and reach USD 2.57 billion by 2031, registering a CAGR of 9.45% during the forecast period. Market growth is driven by low sudden cardiac arrest survival rates, expanding AED placement regulations, and rising adoption of connected AED management solutions.

Which product type is expanding the fastest?

Automated external defibrillators are both the largest and fastest-growing product type. They held 58.64% share in 2025 and are projected to grow at 10.21% through 2031.

Why are public access settings gaining importance?

Public access settings are benefiting from first-time installations in workplaces, schools, retail sites, and community venues. This end-user group is projected to grow at 9.73% CAGR through 2031.

Which region leads in revenue, and which region grows the fastest?

North America led with 41.83% revenue share in 2025, while Asia-Pacific is expected to grow the fastest at 11.87% CAGR through 2031.

Page last updated on: