Biotech Contract Research Organization (CRO) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 28.19 Billion |

| Market Size (2031) | USD 37.20 Billion |

| Growth Rate (2026 - 2031) | 5.71% CAGR |

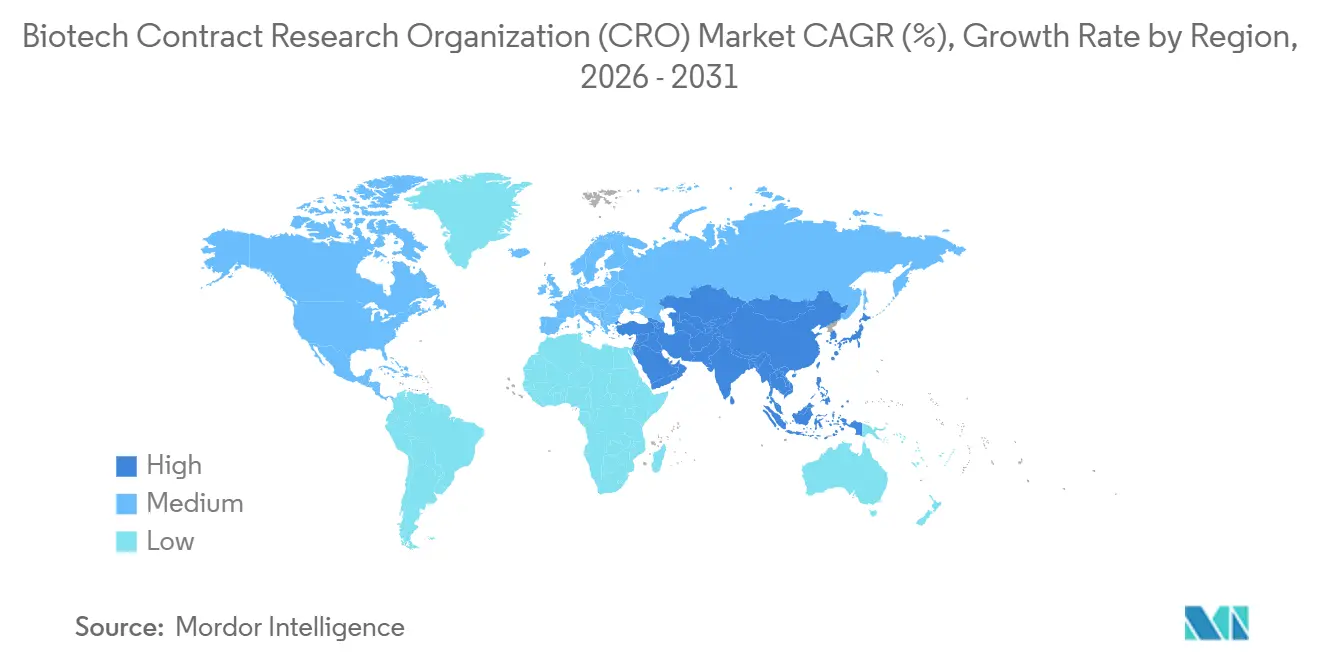

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biotech Contract Research Organization (CRO) Market Analysis by Mordor Intelligence

The Biotech Contract Research Organization Market size was valued at USD 25.44 billion in 2025 and is estimated to grow from USD 28.19 billion in 2026 to reach USD 37.20 billion by 2031, at a CAGR of 5.71% during the forecast period (2026-2031).

The shift toward variable-cost operating models, the BIOSECURE Act’s re-shoring of U.S.-funded work, and the steady rise in global R&D spending keep demand resilient. Clinical services remain the revenue anchor, while outcome-linked post-marketing work expands as real-world evidence gains regulatory weight. Oncology continues to attract the largest pool of protocols, yet infectious-disease programs are multiplying on the back of mpox, dengue, and antimicrobial-resistance initiatives. Capacity additions in North America and Europe reflect redirected demand from China, and India’s streamlined ethics approvals accelerate Asia-Pacific growth. A persistent talent shortage pushes CROs to apply artificial-intelligence tools for site selection and remote monitoring, cutting recruitment cycles and stabilizing margins.

Key Report Takeaways

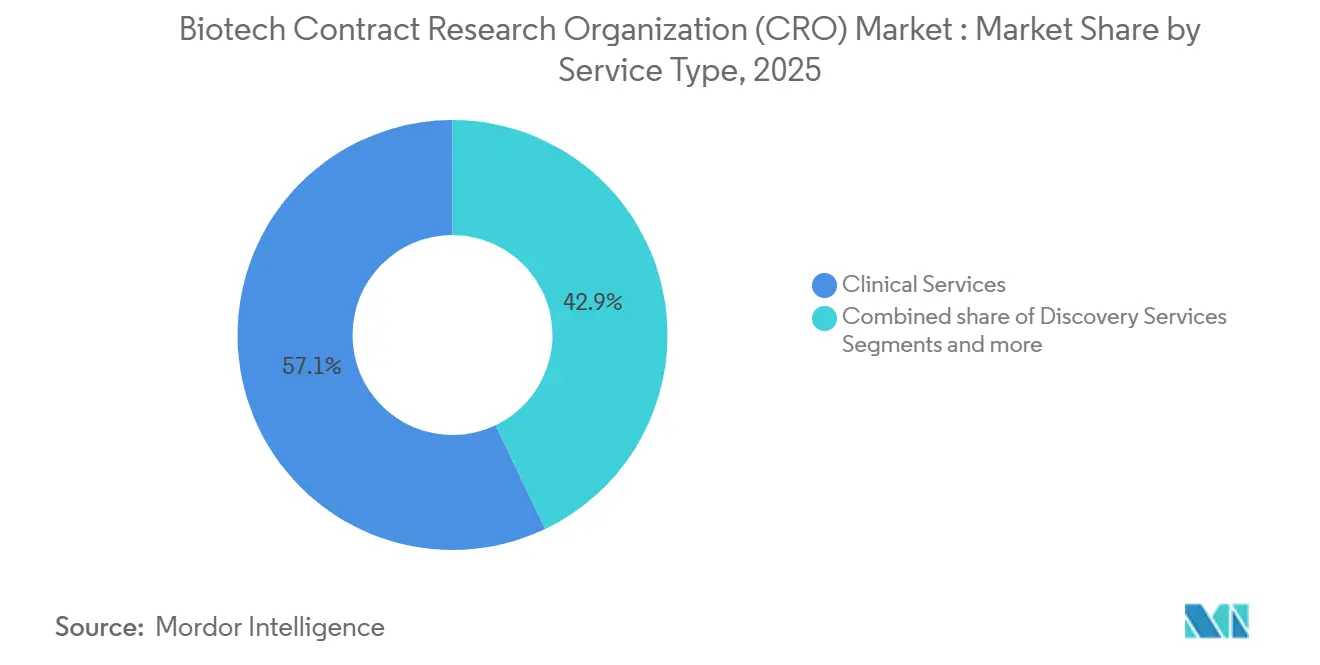

- By service type, clinical services led with 57.1% revenue share in 2025, while the Others segment is forecast to grow at a 6.00% CAGR through 2031.

- By therapeutic area, oncology captured 37.89% of spending in 2025; infectious diseases is poised to expand at a 5.90% CAGR between 2026 and 2031.

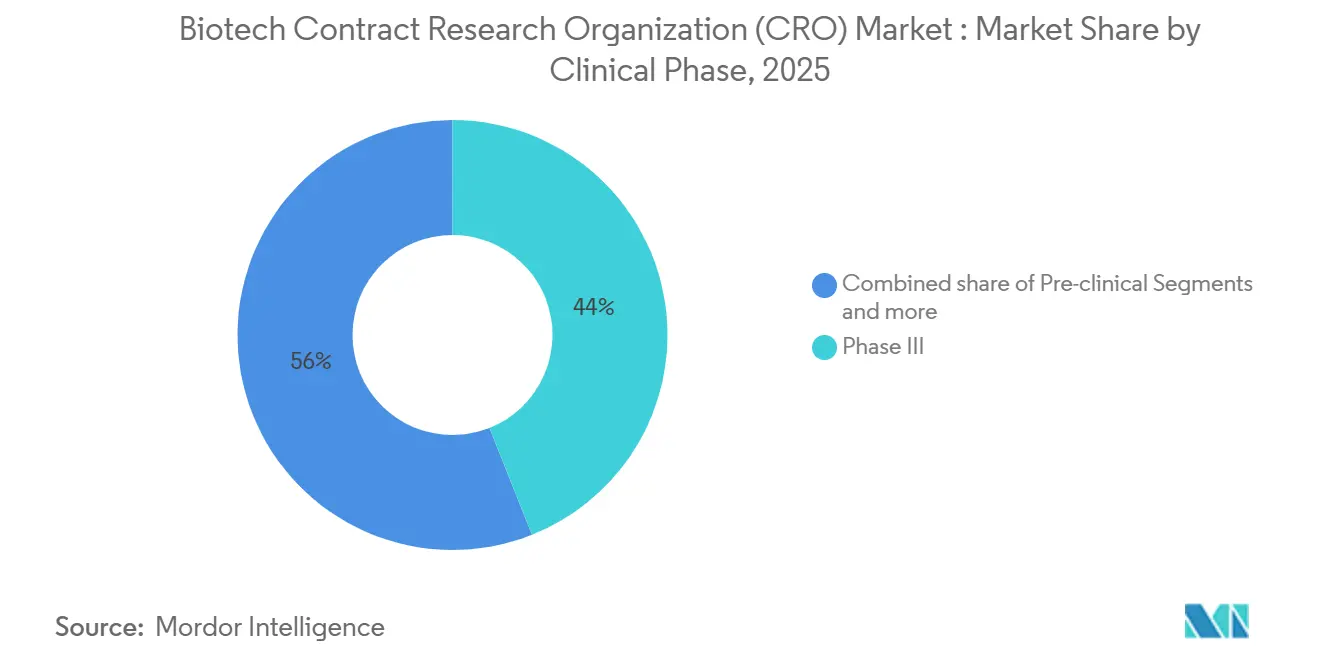

- By clinical phase, Phase III work accounted for 43.97% of spending in 2025 and is expected to grow at a 7.20% CAGR to 2031.

- By end user, pharmaceutical and biopharmaceutical companies held 56.3% of demand in 2025, whereas academic and research institutes are projected to advance at a 6.98% CAGR during the forecast window.

- By geography, North America dominated with a 44.9% share in 2025; Asia-Pacific is forecast to rise at a 7.10% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Biotech Contract Research Organization (CRO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising R&D outsourcing by biopharma | +1.2% | North America and Europe core, expanding globally | Medium term (2-4 years) |

| Growing complexity and volume of clinical trials | +1.0% | Global | Long term (≥ 4 years) |

| Expansion of cell and gene therapy pipelines | +0.8% | North America and Europe, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Outcome-based pricing and risk-sharing models | +0.5% | North America and Europe, early uptake in Japan | Medium term (2-4 years) |

| BIOSECURE Act re-shoring from Chinese vendors | +0.9% | North America, Europe, India, South Korea | Short term (≤ 2 years) |

| AI-enabled in-silico trial optimization | +0.7% | Global, led by North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising R&D Outsourcing by Biopharma

Flat internal productivity has encouraged sponsors to convert fixed laboratory and head-count expenses into variable CRO contracts. Public restructurings in 2024 pushed Pfizer, AstraZeneca, and other firms to outsource majority of their clinical activities. Venture-backed start-ups, which lack operational infrastructure, already route nearly all development work to external providers. Regulators such as the FDA and EMA have clarified that sponsors remain accountable for trial conduct even when execution rests with a CRO, removing a historic roadblock and deepening penetration [1]U.S. Food and Drug Administration, “Decentralized Clinical Trials Guidance for Industry,” fda.gov.

Growing Complexity and Volume of Clinical Trials

Global registries recorded 4,903 completed studies during 2024, up 14.2% year over year, while the average protocol contained 31 eligibility criteria. Oncology protocols frequently include genomic profiling and central imaging, adding millions of dollars to budgets. Decentralized elements appear in more than 90% of new protocols, creating logistical layers for home nursing, tele-visits, and direct-to-patient shipments that favor CROs with integrated technology [2]World Health Organization, “International Clinical Trials Registry Platform 2024 Annual Report,” who.int.

Expansion of Cell and Gene Therapy Pipelines

More than 1,900 advanced-therapy programs were active by late 2024. Each requires Good Manufacturing Practice capacity, non-human-primate toxicology, and cryogenic logistics, driving specialized CRO investment. The FDA expects 10-20 new approvals a year through 2027, ensuring a stream of early-phase engagements. Large providers have invested more than USD 500 million since 2023 to build dedicated analytics and viral-vector testing capability.

Outcome-Based Pricing and Risk-Sharing Models

Payers seek proof of long-term benefit before reimbursing high-cost therapies. Sponsors now embed milestone-linked fee schedules in CRO contracts, spreading risk and reinforcing the need for post-approval data capture. Early adopters report smoother cash flows and closer alignment between clinical-operations decisions and commercialization goals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-jurisdiction regulatory burdens | -0.6% | EU and multi-country Asia-Pacific trials | Long term (≥ 4 years) |

| Clinical-operations talent shortages | -0.5% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Non-human-primate and reagent supply shocks | -0.3% | North America preclinical hubs | Short term (≤ 2 years) |

| Data-sovereignty limits on genomic export | -0.2% | China, EU, India, Brazil | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Multi-Jurisdiction Regulatory Burdens

Running a single protocol across several regions can add six to 12 months to study start-up. The EU Clinical Trials Regulation unified submission portals but left ethics reviews to each member state, keeping 27 parallel approval paths in place. Japan’s 2024 revisions accelerated local reviews yet introduced rules that restrict real-time data transfer. Latin American jurisdictions often mandate duplicate ethics evaluations, pushing administrative costs 20-30% higher than single-country trials [3]European Medicines Agency, “EU Clinical Trials Regulation 2024 Implementation Detail,” ema.europa.eu.

Clinical-Operations Talent Shortages

Turnover among clinical research associates remains near 20% a year. Salary inflation of 15-20% since 2023 has narrowed operating margins for full-service providers. Remote-monitoring platforms help, yet they cannot entirely replace on-site oversight, leaving staffing as a medium-term drag on growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Clinical Services Anchor Revenue, Others Segment Gains Momentum

Clinical services generated 57.1% of 2025 revenue and are expected to preserve leadership as sponsors seek global site networks and data-management expertise. The Others segment, which includes regulatory consulting, pharmacovigilance, and real-world evidence generation, is projected to advance at a 6.00% CAGR through 2031, lifted by outcome-linked fee structures that extend CRO engagement beyond approval. Discovery and pre-clinical work together captured a significant share of revenue, but adoption is uneven because sponsors often insource early chemistry while outsourcing specialized toxicology. Still, the BIOSECURE Act redirected primate-intensive studies to U.S. vendors, helping pre-clinical bookings rise markedly at large providers.

Post-marketing surveillance revenue accelerates as regulators evaluate label expansions on real-world data, and the FDA’s 2024 guidance formally permits CROs to serve as long-term data custodians. Discovery services face margin compression from academic competition, while primate shortages continue to pinch capacity. Public funding for domestic breeding colonies should alleviate the constraint after 2027, yet interim slots remain scarce and high-priced.

By Therapeutic Area: Oncology Dominates, Infectious Diseases Accelerates

Oncology claimed 37.89% of 2025 spending, underpinned by precision-medicine programs and high trial costs that can exceed USD 19 million per Phase III study. Infectious-disease work is the fastest-growing niche, with a forecast 5.90% CAGR, supported by international initiatives targeting antimicrobial resistance and emerging viruses. CNS and cardiovascular protocols draw steady volumes but wrestle with reimbursement hurdles that slow new starts.

The oncology pipeline benefits from sustained regulatory momentum, with 10-20 cell or gene therapy approvals a year anticipated through 2027, each linked to multi-year CRO contracts for long-term follow-up. Infectious-disease trials attract public incentives worth up to USD 1 billion per novel antibiotic, de-risking sponsor spend, and elevating CRO bookings. CNS studies remain lengthier and more expensive, yet accelerated approvals for new Alzheimer’s drugs revived sponsor appetite.

By Clinical Phase: Phase III Captures Largest Share, Risk-Sharing Models Reshape Economics

Phase III work held 43.97% of 2025 revenue and should expand at a 7.2% CAGR through 2031, reflecting the pivotal role of efficacy trials in regulatory and payer decisions. Pre-clinical activity makes up a significant portion of revenue, limited by constrained animal supply. Phase I and Phase II together account for a little more than one-third of spending, while Phase IV post-marketing surveillance represents a smaller portion of revenue, yet is growing as real-world evidence becomes vital for market-access negotiations.

Outcome-linked contracts appear most often in Phase III engagements, aligning CRO compensation with regulatory milestones. The FDA’s 2024 decentralized-trial guidance allows remote visits and home nursing even for pivotal studies, trimming per-patient outlays and supporting wider patient cohorts.

By End User: Pharma Dominates, Academic Institutions Drive Fastest Growth

Pharmaceutical and biopharmaceutical companies generated 56.3% of demand in 2025 and retain scale advantages that favor large, end-to-end CRO partnerships. Academic and research institutes are the fastest-growing buyers, advancing at a 6.98% CAGR as universities monetize investigator-initiated trials and comply with grant-mandated quality oversight. Medical-device firms contribute a mid-teen share, with growth tied to AI-enabled diagnostics and minimally invasive tools.

Biotech start-ups, responsible for a rising share of new molecular approvals, outsource nearly all trial activity, reinforcing CRO order pipelines. Academic centers increasingly pair early-stage data packages with licensing objectives, which keeps CROs involved from planning through technology transfer.

Geography Analysis

North America generated 44.9% of global revenue in 2025, driven by a dense sponsor base, proximity to the FDA, and a mature trial infrastructure that enables study start within 60-90 days of protocol finalization. The BIOSECURE Act transferred more than USD 2 billion in annual pre-clinical and early-phase work from Chinese vendors to the United States and Canada. Yet a 20% turnover rate among clinical staff forces providers to raise wages, pressuring margins, and oncology trial fatigue challenges patient recruitment.

Asia-Pacific is the fastest-growing region at a projected 7.10% CAGR through 2031. India’s 30% rise in 2024 clinical-trial registrations, Japan’s expedited approvals, and South Korea’s strength in cell-therapy manufacturing draw sponsors seeking speed and cost efficiency. China remains a major market for domestic programs but faces data-sovereignty limits that complicate multinational protocols, prompting many foreign sponsors to pivot to compliant neighbors.

Europe holds a significant share of global revenue. Full implementation of the EU Clinical Trials Regulation in 2024 shaved several months off administrative timelines, and the United Kingdom’s 150-day accelerated review attracts first-in-human studies. Spain and Italy offer cost advantages, although longer ethics-committee reviews dilute the benefit. The Middle East, Africa, and South America together growing at notable rate, though Gulf Cooperation Council nations now invest in trial infrastructure as part of healthcare diversification.

Competitive Landscape

The biotech contract research organization (CRO) market remains moderately fragmented. The top five players, IQVIA, Labcorp Drug Development, Charles River Laboratories, ICON plc, and Syneos Health, collectively hold a significant revenue share, leaving meaningful share for mid-tier specialists. Full-service providers command premium pricing by bundling real-world data, site networks, and regulatory insight into single-vendor offerings. Niche firms such as Crown Bioscience and Champ Oncology defend high-margin translational-oncology niches. Capacity expansions announced after the BIOSECURE Act may lead to supply overhang by 2027 if volume moderates.

Technology is the key differentiator. AI-driven site-selection platforms deliver enrollment speeds up to 50% faster than manual methods, increasing win rates in competitive bids. Outcome-based contracts gain traction, yet only large providers possess the balance-sheet strength to absorb potential downside. Real-world evidence services create sticky, post-approval revenue streams but require advanced analytics that many mid-tier firms still lack. Private-equity groups continue to assemble regional roll-ups, aiming to bridge capability gaps and gain scale before an anticipated wave of sponsor consolidation.

Biotech Contract Research Organization (CRO) Industry Leaders

IQVIA

Labcorp Drug Development

Charles River Laboratories

ICON plc

Syneos Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: WEP Clinical completed the acquisition of Netherlands-based Siron Clinical, broadening European execution capacity.

- December 2025: Adicon Holdings purchased translational-oncology specialist Crown Bioscience for USD 204 million, enhancing pre-clinical discovery depth.

- October 2025: Thermo Fisher Scientific agreed to acquire Clario Holdings, adding digital endpoint-data capture that supports 70% of FDA approvals.

Global Biotech Contract Research Organization (CRO) Market Report Scope

As per the scope of the report, biotech contract research organization (CRO) is a specialized service provider that offers essential research and development support to biotechnology and pharmaceutical companies on a contractual basis. These organizations act as strategic partners, allowing biotech firms, especially smaller, resource-lean startups, to outsource complex and expensive tasks such as preclinical testing, clinical trial management, and regulatory affairs.

The biotech contract research organization (CRO) market is segmented by service type, therapeutic area, clinical phase, end-users, and geography. By service type, the market is categorized into discovery services, pre-clinical services, clinical services, and others. By therapeutic area, the market is divided into oncology, CNS / neurology, cardiovascular & metabolic, infectious diseases, immunology / inflammatory, respiratory, and others. By clinical phase, it is segmented into pre-clinical, phase I, phase II, phase III, and phase IV. By end-users, the segmentation includes pharmaceutical and biopharmaceutical companies, medical device companies, academic & research institutes, and government & non-profit organizations. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Discovery Services |

| Pre-clinical Services |

| Clinical Services |

| Others |

| Oncology |

| CNS / Neurology |

| Cardiovascular & Metabolic |

| Infectious Diseases |

| Immunology / Inflammatory |

| Respiratory |

| Others |

| Pre-clinical |

| Phase I |

| Phase II |

| Phase III |

| Phase IV |

| Pharmaceutical and Biopharmaceutical Companies |

| Medical Devices companies |

| Academic & Research Institutes |

| Government & Non-Profit Organisations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Discovery Services | |

| Pre-clinical Services | ||

| Clinical Services | ||

| Others | ||

| By Therapeutic Area | Oncology | |

| CNS / Neurology | ||

| Cardiovascular & Metabolic | ||

| Infectious Diseases | ||

| Immunology / Inflammatory | ||

| Respiratory | ||

| Others | ||

| By Clinical Phase | Pre-clinical | |

| Phase I | ||

| Phase II | ||

| Phase III | ||

| Phase IV | ||

| By End-user | Pharmaceutical and Biopharmaceutical Companies | |

| Medical Devices companies | ||

| Academic & Research Institutes | ||

| Government & Non-Profit Organisations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the biotech contract research organization market?

The biotech contract research organization market size is estimated to reach USD 28.19 billion in 2026.

What is the expected growth rate for CRO services over the next five years?

The market is projected to expand at a 5.71% CAGR between 2026 and 2031.

Which service type brings in the most revenue for CROs?

Clinical services, covering patient recruitment through database lock, generated 57.1% of revenue in 2025.

Which therapeutic area drives the highest spend with CROs?

Oncology accounted for 37.89% of sponsor spending in 2025.

Why is Asia-Pacific the fastest-growing CRO region?

Streamlined ethics approvals, cost advantages, and regulatory reforms in India and Japan push Asia-Pacific growth to a forecast 7.1% CAGR.

Page last updated on: