Biologics Contract Research Organization (CRO) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

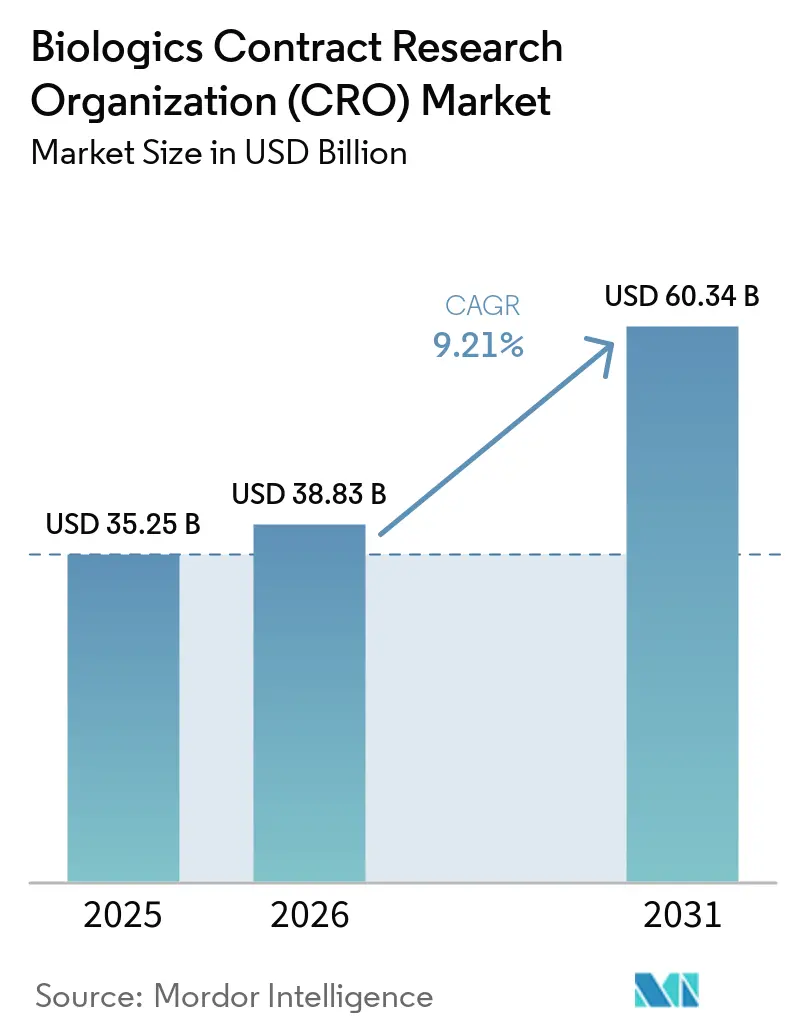

| Market Size (2026) | USD 38.83 Billion |

| Market Size (2031) | USD 60.34 Billion |

| Growth Rate (2026 - 2031) | 9.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

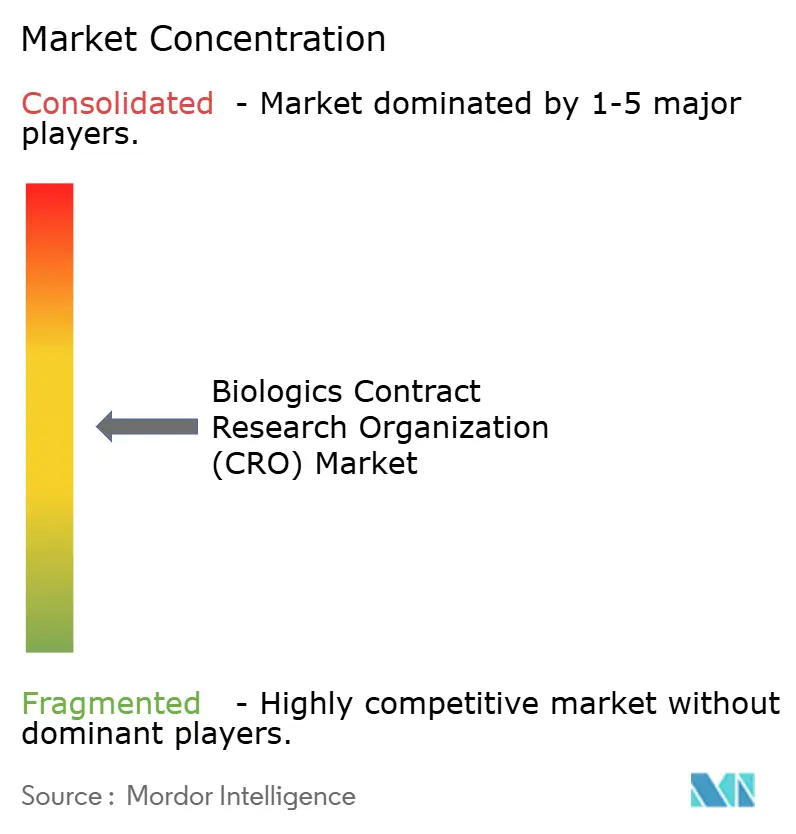

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biologics Contract Research Organization (CRO) Market Analysis by Mordor Intelligence

The Biologics Contract Research Organization Market size is expected to increase from USD 35.25 billion in 2025 to USD 38.83 billion in 2026 and reach USD 60.34 billion by 2031, growing at a CAGR of 9.21% over 2026-2031.

Strong outsourcing demand from sponsors working on biosimilars, cell therapies, and gene-editing candidates keeps the biologics contract research organization market on a steady growth path even as capital markets tighten. Much of the momentum comes from the need to front-load sophisticated analytics, glycan mapping, hydrogen–deuterium exchange mass spectrometry, and next-generation sequencing so that pivotal studies begin with fewer technical unknowns. Integrated discovery-through-manufacturing packages offered by large CDMOs have blurred traditional boundaries and helped smaller virtual biotechs reach the clinic faster, while regulatory harmonization across Asia-Pacific has opened new, cost-efficient trial hubs. At the same time, cybersecurity incidents and rising GMP compliance costs compel providers to upgrade data-integrity systems and aseptic infrastructures, actions that favor well-capitalized networks able to amortize capital expenditure across multiple global sites [1]U.S. Food and Drug Administration, “Biosimilar Product Information,” fda.gov.

Key Report Takeaways

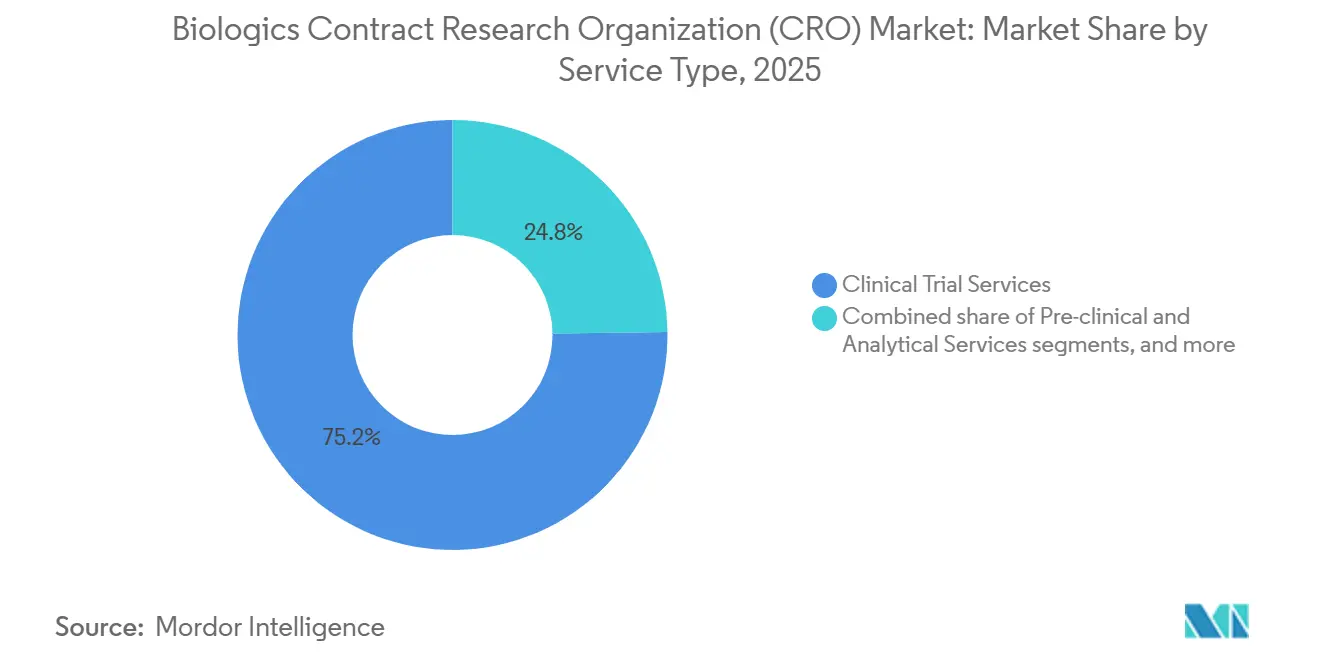

- By Service Type, clinical trial services captured 75.2% of the biologics contract research organization (CRO) market share in 2025, whereas Pre-clinical & Analytical Services are projected to expand at a 9.60 % CAGR to 2031.

- By Phase, phase III accounted for 75.1% of the biologics contract research organization (CRO) market size in 2025, yet pre-clinical work is advancing at 9.30 % CAGR through 2031.

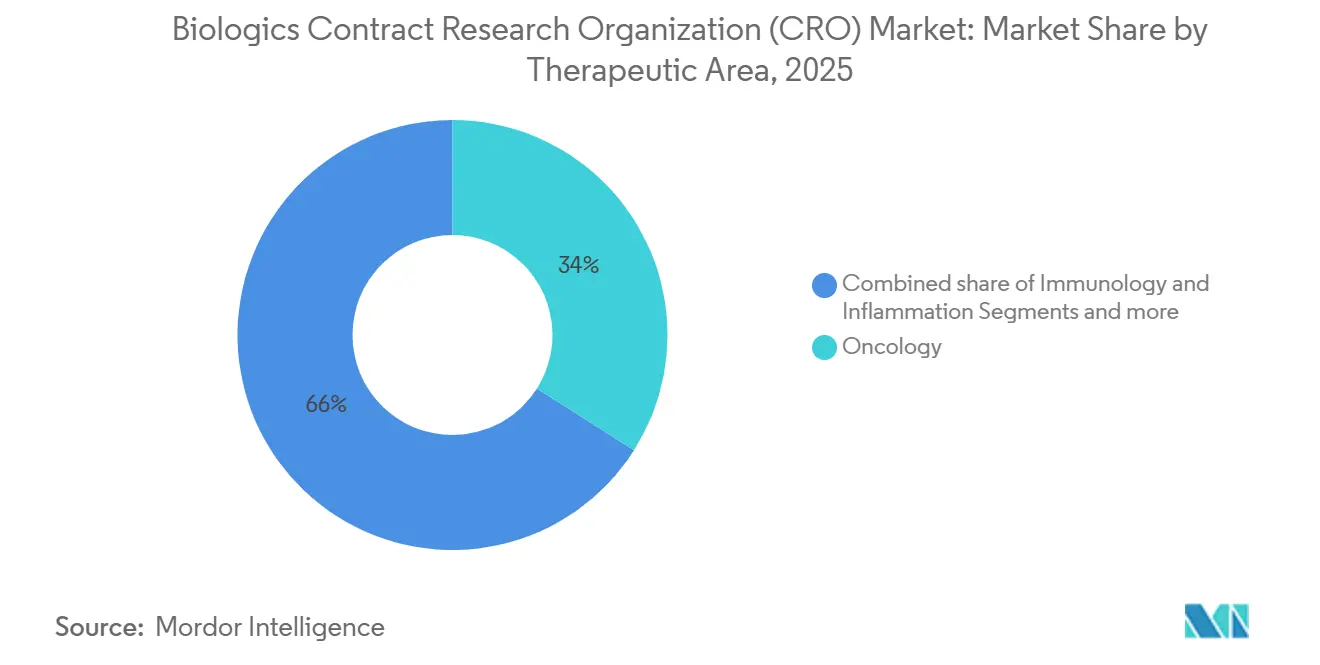

- By Therapeutic Area, oncology remained the top therapeutic driver with 34% of 2025 revenue, but Infectious Diseases are set to grow at 8.50 % CAGR to 2031.

- By End User, biopharma & biotech firms delivered 40.8% of 2025 sales and also hold the fastest growth outlook at 9.60 % CAGR.

- By Geography, North America owned 45.3% of 2025 revenue, whereas Asia-Pacific is forecast to post a 9.90 % CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Biologics Contract Research Organization (CRO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Adoption of Novel Biologics & Biosimilars | +1.6% | Global, with EU and North America leading biosimilar uptake | Medium term (2-4 years) |

| Growing Complexity of Biomolecules Necessitating Specialized Analytics | +1.1% | Global, acute in North America and EU for advanced characterization | Long term (≥4 years) |

| Cost-Pressure & Need for Faster Time-To-Market, Encouraging Outsourcing | +1.3% | Global, most pronounced in North America and APAC | Short term (≤2 years) |

| Cell & Gene Therapy Pipeline Expansion Boosting Demand for Advanced Bio-Analytics | +1.4% | APAC core (China, Japan), spill-over to North America | Long term (≥4 years) |

| AI/ML-Enabled In-Silico Biologics Design Services Offered by CROs | +1.0% | North America & EU, early adoption in Singapore, South Korea | Short term (≤2 years) |

| Regulatory Harmonization in APAC Facilitating Offshore Biologics Trials | +1.2% | APAC (China, India, Japan, South Korea), MEA emerging | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Adoption of Novel Biologics & Biosimilars

The FDA cleared sixteen biosimilars across 2024 and 2025, including interchangeable adalimumab and ustekinumab versions that together replace reference sales of roughly USD 20 billion. Sponsors outsource comparability analytics because internal labs generally lack validated high-throughput assays, which is why the biologics contract research organization market posts stronger growth in Pre-clinical & Analytical Services than overall revenue. Eurofins and SGS have expanded LC-MS fleets by more than fifteen units each since 2024 to manage the influx [2]Eurofins Scientific, “Global Biosimilar Testing Expansion,” eurofins.com. Interchangeability studies require multi-switch crossover designs that only experienced CROs can execute without protocol deviations, reinforcing the strategic value of seasoned providers.

Growing Complexity of Biomolecules Necessitating Specialized Analytics

Bispecific antibodies, ADCs, and fusion proteins demand orthogonal characterization hydrogen–deuterium exchange, analytical ultracentrifugation, and cryo-EM, which sits beyond most in-house quality-control budgets. FDA guidance issued in 2024 asks sponsors to use at least five analytic modalities to confirm lot-to-lot consistency for multispecific constructs. Charles River invested USD 80 million in 2025 for additional cryo-EM and HDX-MS capacity, reinforcing its leadership in the biologics contract research organization market. Glycosylation profiling has emerged as a gating factor for IND acceptance, pushing many sponsors to outsource glycan mapping to labs with validated LC-MS workflows.

Cost Pressure & Need for Faster Time-to-Market Encouraging Outsourcing

Virtual biotechs filed the majority of 2025 INDs and rely entirely on external partners for discovery, toxicology, and trial execution, significantly increasing outsourcing penetration in early-stage programs across the biotech contract research organization ecosystem. Running a Phase II oncology study in China or India costs significantly less than in the United States, yet data remain acceptable to FDA and EMA reviewers if studies meet ICH standards. WuXi AppTec reported that more than half of its 2025 bookings came from clients running parallel pre-clinical and Phase I projects, a strategy that compresses timelines by four to six months.

Cell & Gene Therapy Pipeline Expansion Boosting Demand for Advanced Bio-Analytics

More than 3,200 active cell and gene therapy trials were recorded in 2025, with China responsible for 38 % of new starts [3]American Society of Gene & Cell Therapy, “2025 Annual Meeting Highlights,” annualmeeting.asgct.org. Vendors such as Lonza and Charles River have each poured over USD 100 million into BSL-2+ vector-testing suites to meet demand for replication-competent lentivirus assays, NGS-based integration analysis, and potency testing. FDA guidance now mandates fifteen-year post-treatment surveillance for certain gene therapies, creating a long-tail services opportunity for patient-registry management.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Global GMP/GLP Compliance Raising Operating Costs | -0.9% | Global, acute in EU under Annex 1 revisions | Short term (≤2 years) |

| Scarcity of High-End Biologics Expertise in Emerging Regions | -0.6% | APAC emerging markets, MEA, South America | Medium term (2-4 years) |

| Shift Toward Integrated CDMO Models Cannibalizing Standalone CRO Revenue | -0.7% | North America & APAC, limited EU impact | Medium term (2-4 years) |

| Cyber-Security & Data-Integrity Risks in Distributed Biotesting | -0.5% | Global, heightened in decentralized trial models | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Cyber-Security & Data-Integrity Risks in Distributed Biotesting

Ransomware incidents against CRO trial databases shot up 42 % in 2024, prompting FDA warning letters and higher cyber-insurance premiums. Implementation of zero-trust architectures and blockchain audit trails adds USD 2-5 million to annual IT budgets, costs that small labs struggle to absorb.

Scarcity of High-End Biologics Expertise in Emerging Regions

Chinese and Indian CROs spend up to two years training staff for HDX-MS and analytical-ultracentrifugation, compared with nine months in North America, eroding cost advantages. Salary inflation now 70-80 % of U.S. equivalents compresses margins, while brain drain to Western labs slows capacity additions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Clinical Trials Dominate Yet Analytics Accelerate

Clinical Trial Services generated 75.23 % of the biologics contract research organization market revenue in 2025, reflecting the sheer cost of patient enrollment, global site monitoring, and real-time safety oversight. Sponsors routinely spend USD 50 million or more on a single late-stage oncology trial, cementing the clinical category’s dominance. However, Pre-clinical & Analytical Services are forecast to expand at 9.60 % CAGR as agencies demand orthogonal analytics, primary structure, higher-order structure, glycosylation, and bioactivity for biosimilar comparability packages. Pre-clinical clients value rapid turnaround on method validation and immunogenicity screening, so CROs with large LC-MS fleets and validated ELISA panels command premium fees. Quality & Regulatory Consulting remains a slim but profitable niche; top-tier providers bill USD 300-500 per hour for CMC dossier drafting and FDA pre-IND support.

Second-generation service lines are emerging as decentralized trials gain traction. Labcorp’s 2024 remote-monitoring platform streams cytokine readouts from participants’ homes, cutting site visits and speeding recruitment in immunology trials. Charles River booked a 25 % rise in non-human-primate toxicology studies in 2025, driven by bispecific and CAR-T programs. Parexel’s Regulatory Intelligence portal flags global CMC gaps in real time, trimming submission readiness by three to six months. Altogether, the biologics contract research organization market benefits from sponsors eager to de-risk clinical programs through better analytics, data visualization, and proactive regulatory strategy.

By Phase: Late-Stage Trials Drive Revenue While Early Work Gains Momentum

Clinical Trial phase activities captured 75.10 % of 2025 revenue, with Phase III studies alone often costing USD 40-80 million due to extensive site networks and multi-year follow-up. Adaptive first-in-human designs are making Phase I work more data-rich and expensive, especially when pharmacodynamic biomarkers or basket-trial cohorts are involved. Medpace’s 2025 hybrid design combines central infusion clinics with home pharmacokinetic sampling, trimming per-patient costs by 30 % while maintaining data quality. Meanwhile, Pre-clinical projects are accelerating at 9.30 % CAGR as sponsors invest in formulation optimization, developability screening, and immunogenicity risk assessment before filing an IND.

Discovery budgets also rise as AI tools flag aggregation or viscosity liabilities in silico, allowing chemists to prioritize high-probability candidates. NIH awarded USD 120 million in 2025 to university CRO consortia that bridge discovery and pre-clinical toxicology, feeding a pipeline of early-stage work to service providers. Regulatory pressure for long-term monitoring fifteen-year post-marketing follow-up for gene therapies, makes Phase IV an increasingly material revenue stream. Collectively, all stages contribute to the biologics contract research organization market, yet risk-conscious sponsors tilt funding toward early analytics to avoid costly late-phase failures.

By Therapeutic Area: Oncology Leads While Infectious Diseases Accelerate

Oncology delivered 34 % of 2025 turnover, driven by CAR-T, bispecific antibodies, and antibody-drug conjugates that generate large, complex data packages. A single pivotal CAR-T study can yield USD 15-25 million in CRO fees, dwarfing typical antibody programs. Infectious Diseases, however, are on track for 8.50 % CAGR as governments invest in broadly neutralizing antibodies and rapid-response platforms; BARDA set aside USD 500 million in 2025 for pandemic-preparedness biologics that require BSL-3 testing capacity. Immunology & Inflammation remains robust, with Syneos Health logging a 20 % rise in bookings for IL-17 and IL-23 programs.

Rare Diseases continue to attract venture capital and regulatory incentives. The FDA approved eight gene therapies in 2025, each demanding vector potency assays, biodistribution studies, and long-term safety registries. CEPI also committed USD 300 million to monoclonal antibodies targeting influenza, RSV, and novel coronaviruses, awards that mainly flow through experienced CROs. Combination therapies pairing checkpoint inhibitors with CAR-T or bispecifics further complicate analytical demands, deepening reliance on specialized providers within the biologics contract research organization market.

By End User: Biopharma Dominates and Leads Growth

Biopharma & Biotech Firms generated 40.80 % of 2025 revenue and share the highest growth outlook at 9.60 % CAGR as virtual biotechs proliferate, and big pharma divests internal clinical operations. Virtual companies with fewer than fifty employees made up 38 % of IND filers in 2025 and outsource essentially every function beyond corporate strategy. Academic & Research Institutes rely heavily on CRO expertise because most universities lack GMP suites and quality systems; the University of Pennsylvania’s Phase II glioblastoma CAR-T trial is fully outsourced to Parexel.

Government & Non-profit Organizations, though smaller in dollar terms, fund strategic initiatives: NIH distributed USD 4.2 billion in biologics grants in 2025, up 15 % year over year. Gates Foundation grants for neglected-disease biologics further expand the client base for CROs experienced in resource-constrained settings. As large pharmas embrace milestone-based fee schedules, CROs assume more development risk but secure upside through success fees, aligning incentives across the biologics contract research organization market.

Geography Analysis

North America captured 45.32 % of 2025 revenue thanks to a dense cluster of biopharma headquarters, high NIH funding, and FDA leadership in biosimilar and gene-therapy guidance. Nonetheless, the Asia-Pacific is projected to post a 9.90 % CAGR as streamlined regulations and cost arbitrage lure sponsors to China, India, Japan, and South Korea. China’s NMPA green-lit 27 biosimilars across 2024-2025 after adopting ICH Q5E, shortening local timelines by eighteen months. India’s CDSCO waiver of local trials for low-risk molecules, Japan’s alignment of extrapolation, and South Korea’s twelve-month fast-track review further solidify the region’s appeal.

Europe remains vital, with Germany, the United Kingdom, and France combining for a significant share of 2025 turnover. Germany’s Federal Ministry of Education and Research earmarked EUR 800 million in 2025 for translational biologics, often channeled through CRO-managed clinical networks. The Middle East & Africa and South America are smaller but growing, driven by fast-track pathways such as Brazil’s fifteen-month biosimilar review. Australia and South Korea benefit from ICH alignment and R&D tax credits; Canada and Mexico gain from USMCA provisions that simplify cross-border sample flow. South Africa and GCC states attract infectious-disease trials where patient prevalence supports larger cohorts, and WHO-backed regulatory capacity building improves data portability to U.S. and EU submissions.

Competitive Landscape

Five global heavyweights, IQVIA, Labcorp Drug Development, Charles River Laboratories, Syneos Health, and Parexel, command the majority of worldwide revenue, leaving ample space for regional specialists and tech-first entrants. Samsung Biologics and WuXi AppTec illustrate the power of vertical integration by wrapping discovery, CMC, GMP production, and clinical supply in one contract, locking clients into multi-year master service agreements that raise switching costs. Niche players such as BioAgilytix and Frontage Laboratories carve defensible territory in biomarker immunoassays and anti-drug antibody detection, where proprietary reagents create barriers to commoditization.

Technology provides a new competitive frontier. IQVIA’s AI-enabled antibody-design suite predicts aggregation and viscosity risks before synthesis, trimming lead-optimization timelines significantly. Charles River’s 2025 buyout of a German immunogenicity lab adds fifteen validated assays and expands its EMA-aligned footprint. FDA-inspected facilities and EMA-qualified oversight fetch 15-20% pricing premiums because sponsors prize regulatory assurance over headline cost. Academic spin-outs specializing in cryo-EM or high-resolution mass spectrometry remain attractive acquisition targets for incumbents seeking breadth in the biologics contract research organization market.

Biologics Contract Research Organization (CRO) Industry Leaders

IQVIA

Labcorp Drug Development

Charles River Laboratories

Syneos Health

Parexel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Avance Clinical, a global contract research organization, announced the acquisition of LumaBridge, a U.S.-based clinical CRO recognized for its oncology trial expertise. This strategic move highlights Avance's dedication to expediting clinical development for its biotech sponsors.

- March 2025: Samsung Biologics formally launched a CRO division leveraging its CDMO infrastructure to offer discovery-through-clinic packages.

Global Biologics Contract Research Organization (CRO) Market Report Scope

As per the scope of the report, Biologics Contract Research Organization (CRO) offers expert research and development services specifically for complex biologic therapies derived from living organisms.

The Biologics Contract Research Organization (CRO) Market is segmented by service type, phase, therapeutic area, end-users, and geography. By service type, the market is categorized into pre-clinical & analytical services, clinical trial services, quality & regulatory consulting, and bioinformatics & data management. By clinical phase, it is segmented into Pre-clinical, Phase I, Phase II, Phase III, and Phase IV. By therapeutic area, the market is divided into oncology, immunology & inflammation, infectious diseases, rare diseases, and others. By end-users, the segmentation includes biopharmaceutical & biotech firms, academic & research institutes, and government & non-profit organizations. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Pre-clinical & Analytical Services |

| Clinical Trial Services |

| Quality & Regulatory Consulting |

| Bio-informatics & Data Management |

| Pre-clinical |

| Phase I |

| Phase II |

| Phase III |

| Phase IV |

| Oncology |

| Immunology & Inflammation |

| Infectious Diseases |

| Rare Diseases |

| Others (Cardio-metabolic, Neurology) |

| Biopharmaceutical & Biotech Firms |

| Academic & Research Institutes |

| Government & Non-profit Organizations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Pre-clinical & Analytical Services | |

| Clinical Trial Services | ||

| Quality & Regulatory Consulting | ||

| Bio-informatics & Data Management | ||

| By Phase | Pre-clinical | |

| Phase I | ||

| Phase II | ||

| Phase III | ||

| Phase IV | ||

| By Therapeutic Area | Oncology | |

| Immunology & Inflammation | ||

| Infectious Diseases | ||

| Rare Diseases | ||

| Others (Cardio-metabolic, Neurology) | ||

| By End User | Biopharmaceutical & Biotech Firms | |

| Academic & Research Institutes | ||

| Government & Non-profit Organizations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the biologics contract research organization market.

The biologics contract research organization market size is expected to reach USD 38.83 billion in 2026.

What growth rate is expected through 2031?

Revenue is projected to rise at a 9.21 % CAGR through 2031.

Which service category is expanding fastest?

Pre-clinical & Analytical Services are growing at 9.60 % CAGR by meeting rising biosimilar comparability and immunogenicity demands.

Why is Asia-Pacific attracting more outsourced biologics trials?

Harmonized biosimilar guidelines, lower execution costs, and faster enrollment push Asia-Pacific growth to a 9.90 % CAGR.

Which therapeutic area shows the strongest growth potential?

Infectious-disease programs lead growth at 8.50 % CAGR as governments fund pandemic-preparedness antibodies.

Page last updated on: