Biofilms Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.01 Billion |

| Market Size (2031) | USD 4.28 Billion |

| Growth Rate (2026 - 2031) | 7.28% CAGR |

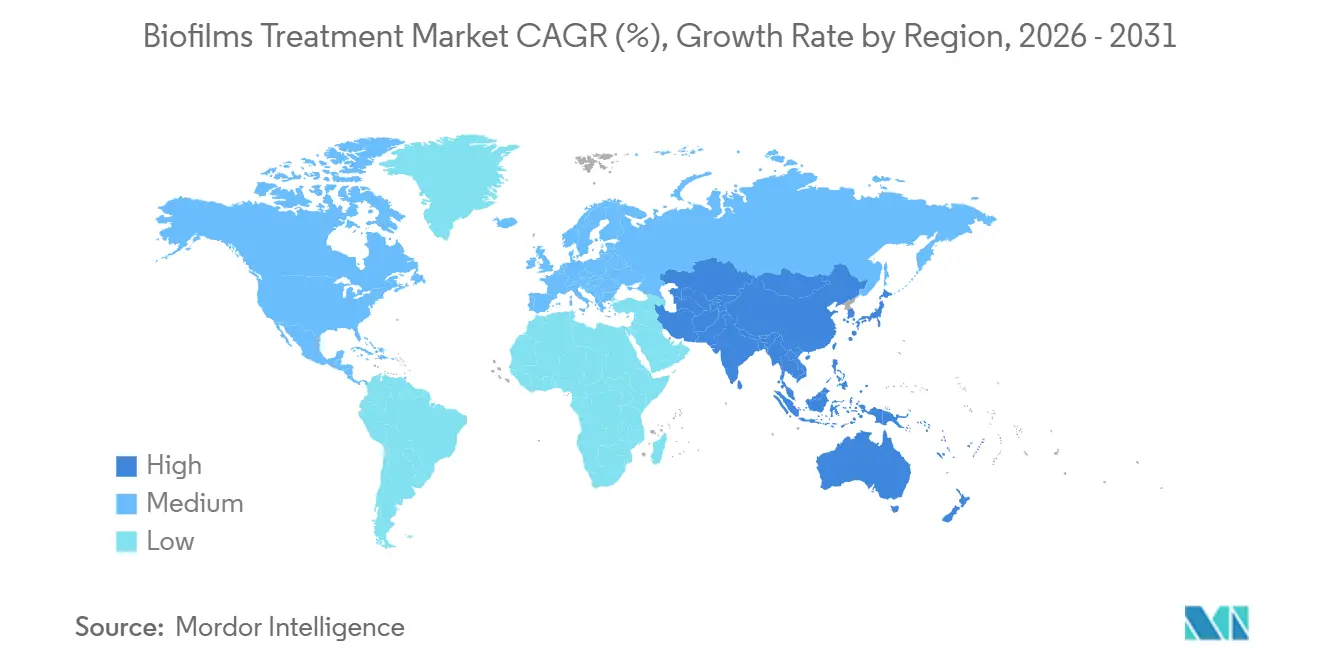

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

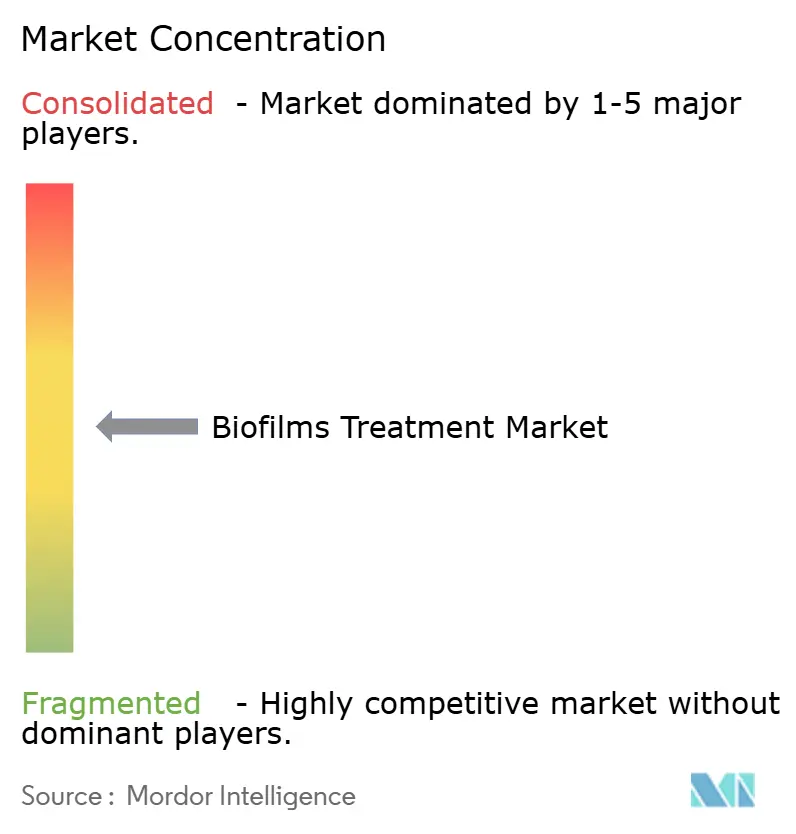

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biofilms Treatment Market Analysis by Mordor Intelligence

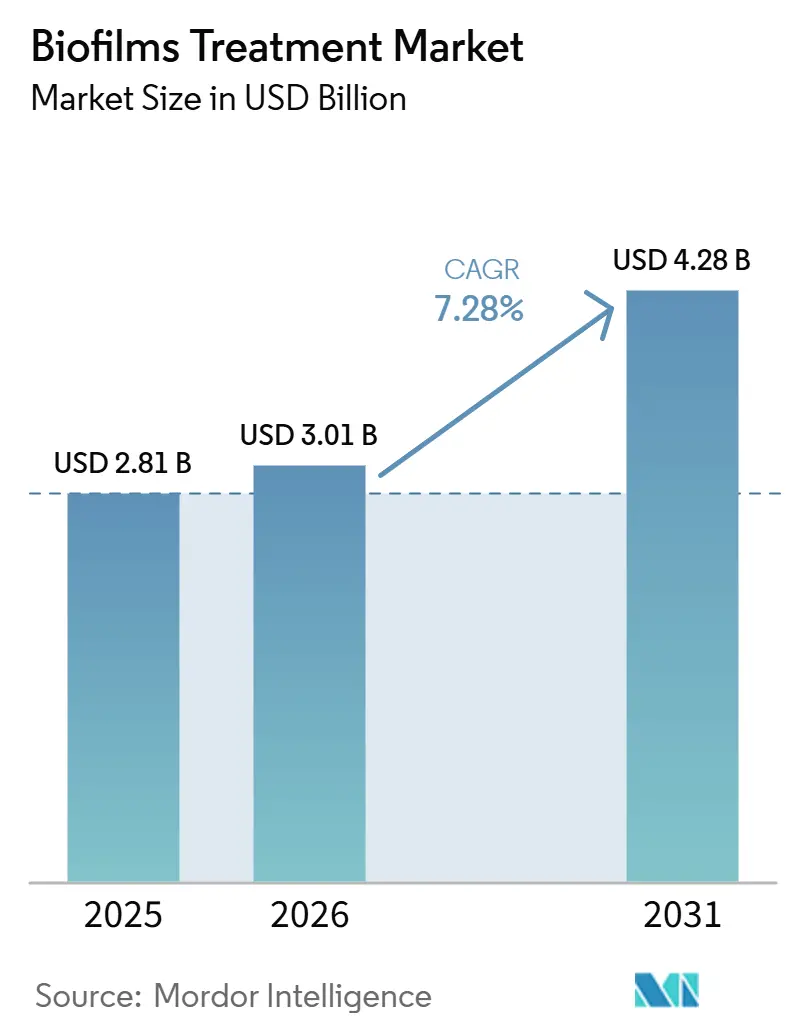

The Biofilms Treatment Market size is projected to expand from USD 2.81 billion in 2025 and USD 3.01 billion in 2026 to USD 4.28 billion by 2031, registering a CAGR of 7.28% between 2026 to 2031.

Chronic wound care continues to drive demand, as biofilms are associated with up to 60% of chronic wounds and more than half of burn wounds, sustaining treatment needs across hospitals and outpatient settings. Aging populations and the rising prevalence of diabetes are expanding the patient pool, particularly in diabetic foot ulcer care, where slow-healing wounds require repeated intervention. Updated antimicrobial stewardship guidance is shifting treatment toward topical and non-antibiotic approaches, supporting demand for anti-biofilm products that demonstrate clinical value without increasing resistance concerns. The biofilm treatment market is becoming more evidence-driven, as larger wound care companies use product launches, trial data, and broader portfolios to protect their positions, while specialist players advance targeted technologies into niche applications.

Key Report Takeaways

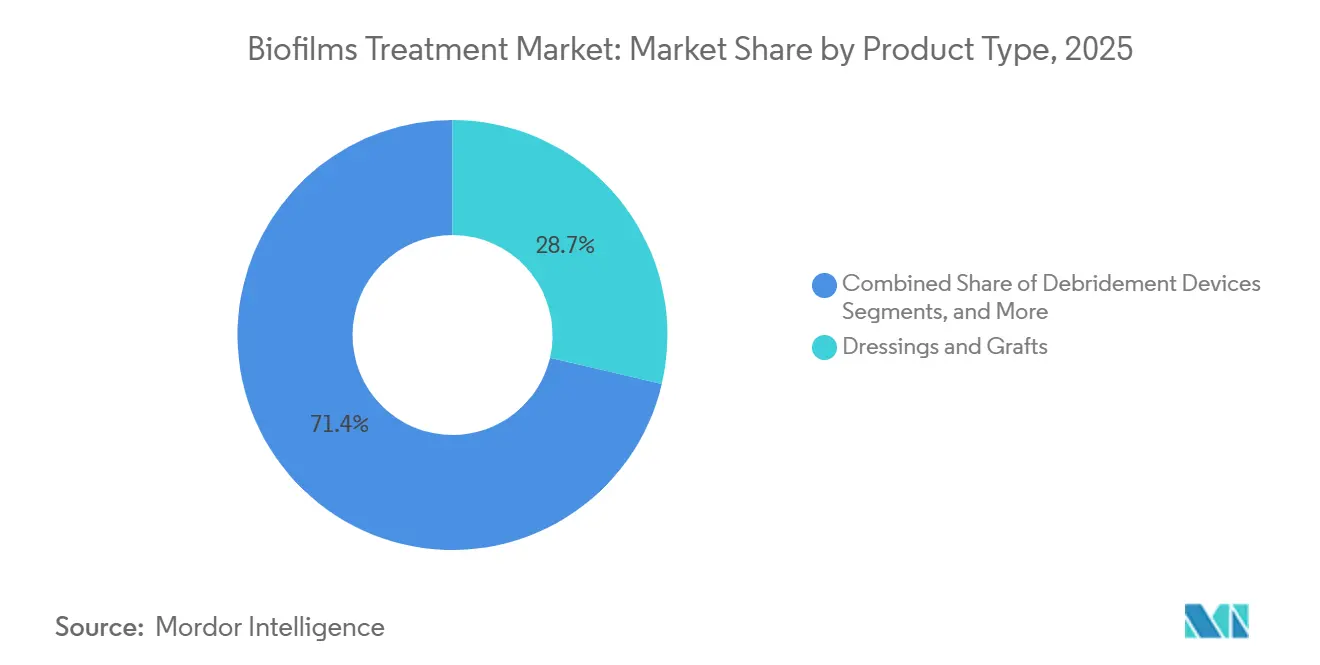

- By product type, dressings and grafts accounted for 28.65% of the biofilm treatment market size in 2025, while topical agents are projected to grow at an 8.93% CAGR through 2031.

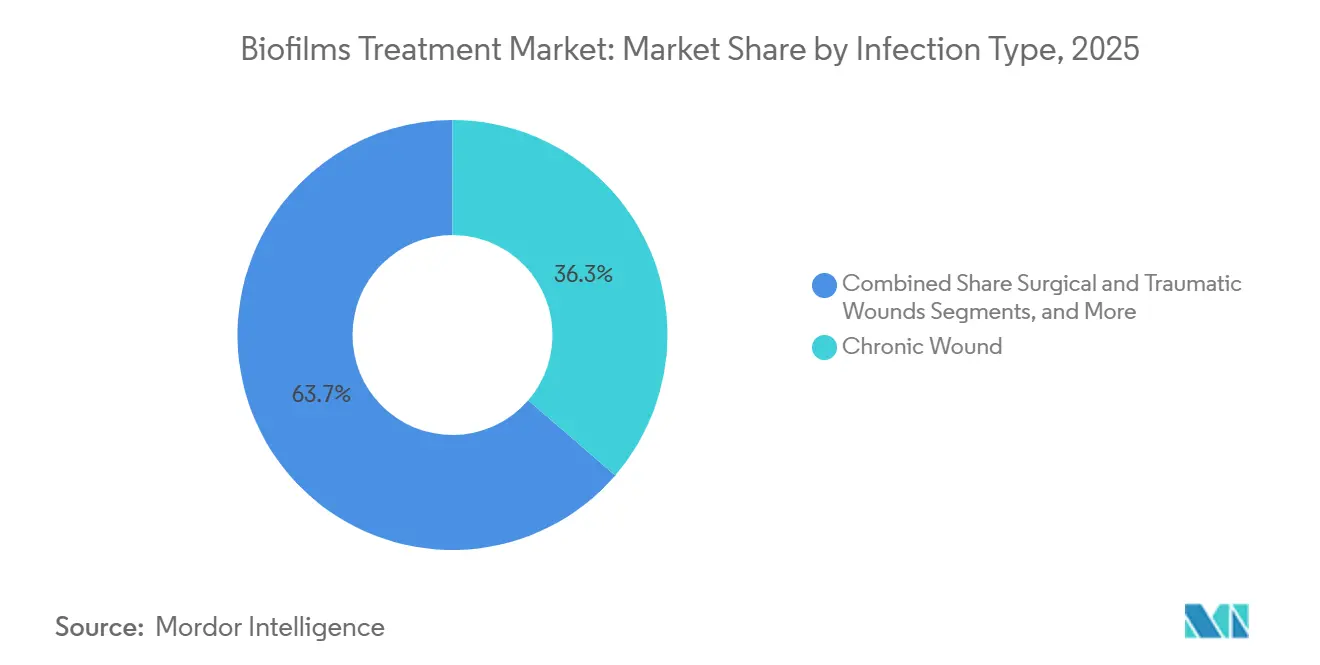

- By infection type, chronic wounds represented 36.34% of revenue in 2025, while surgical and traumatic wounds are forecast to advance at an 8.35% CAGR through 2031.

- By treatment method, physical debridement captured 35.23% of revenue in 2025, while chemical and antiseptic treatment is expected to grow at a 9.67% CAGR through 2031.

- By end user, hospitals held 52.88% of revenue in 2025, while specialty clinics and wound care centers are projected to expand at a 9.78% CAGR through 2031.

- By geography, North America held 38.56% of the biofilm treatment market share in 2025, while Asia-Pacific is projected to expand at an 8.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Biofilms Treatment Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increasing chronic wound prevalence and biofilm burden | +2.0% | Global, highest in North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Expanding advanced wound care adoption in hospitals and home healthcare | +1.5% | North America and Europe core, with spillover to Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Rising anti-biofilm product innovation in dressings, debridement, and topical therapies | +1.4% | Global, with innovation hubs in North America and Europe | Medium term (2-4 years) |

| Growing clinical emphasis on antimicrobial stewardship and non-antibiotic alternatives | +1.1% | Europe and North America primary, Asia-Pacific early adopters | Medium term (2-4 years) |

| Under-treated biofilm recolonization after standard debridement driving retreatment cycles | +0.7% | Global, concentrated in urban chronic wound care networks | Short term (≤ 2 years) |

| Increasing use in post-surgical and device-associated wound management | +0.8% | North America, Germany, the UK, and Japan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Chronic Wound Prevalence and Biofilm Burden

Chronic wounds affect an estimated 6.5 million patients each year in the United States, and treatment costs exceed USD 25 billion annually, with older adults and people with diabetes carrying a significant share of the burden. This trend supports demand in the biofilm treatment market, as biofilm slows healing, increases repeat treatment cycles, raises clinic visits, extends care duration, and adds to total spending. Diabetic foot ulcers affect 19% to 34% of people with diabetes over their lifetime, and 60% of these cases carry biofilm-forming bacterial isolates, with rates increasing in higher-grade ulcers. As diabetes prevalence is projected to reach 783 million people globally by 2045, the patient pool at risk of persistent wound infection is expected to expand, while evolving regulatory focus on antimicrobial risk in wound dressings supports products that disrupt biofilm and limit resistance concerns.[1]AZ Shen et al., “Biofilms and Chronic Wounds: Pathogenesis and Treatment,” Journal of Clinical Medicine, mdpi.com

Rising Anti-Biofilm Product Innovation in Dressings, Debridement, and Topical Therapies

Product development in the biofilm treatment market is shifting from single-mechanism antimicrobial products to platforms that disrupt biofilm, deliver active agents, and support the wound environment. A 2026 study in Scientific Reports validated a next-generation antimicrobial dermal matrix that eradicates polymicrobial biofilms and modulates inflammation in wound models, indicating broader treatment value than standard single-agent products. ConvaTec received European approval for ConvaNiox in April 2025 and launched it in France, Germany, Italy, Poland, Spain, and the UK. Trial data showed wound area reduction three times faster and 60% higher healing within 12 weeks compared to standard care. Kane Biotech’s Revyve platform also reflects this shift, with a 2026 Frontiers in Antibiotics publication showing a 3.5-5.5 log CFU reduction in antibiotic-tolerant biofilm cells of P. aeruginosa and S. aureus within three days, raising the need for stronger data and clearer clinical differentiation among market entrants.[2]G Theodorakopoulos et al., “Biofilm in Diabetic Foot Ulcers: A Systematic Narrative Review,” International Wound Journal, doi.org

Growing Clinical Emphasis on Antimicrobial Stewardship and Non-Antibiotic Alternatives

Antimicrobial stewardship in wound care is moving from a recommended practice to a more formal treatment framework across several health systems. EWMA updated guidance in November 2025 stating that clinicians should reserve systemic antibiotics for confirmed infection rather than biofilm colonization, supporting wider use of topical anti-biofilm products. A 2025 expert panel publication in Wounds identifies nitric oxide, topical oxygen, chelating agents, and PHMB as stronger non-antibiotic options for chronic wound biofilm management. For procurement teams, stewardship compliance is expected to influence purchasing decisions, while products without clear anti-biofilm evidence or low resistance risk may face challenges in securing formulary support, and DACC-coated dressings are expected to gain relevance by binding biofilm bacteria without driving resistance.

Expanding Advanced Wound Care Adoption in Hospitals and Home Healthcare

Advanced wound care adoption is expanding across institutional and non-institutional settings, broadening the channel base for the biofilm treatment market. Organogenesis reported USD 531.2 million in Advanced Wound Care net product revenue in 2025, up 17% year over year, supported by higher unit volume and new PHMB antimicrobial product lines that help prevent biofilm reformation after debridement. Growth varies by care setting, with home healthcare expanding faster than acute care in many systems as aging-in-place policies shift more wound management into community settings. Sanara MedTech launched its Tissue Health Plus program in July 2025 as a value-based wound care offering for payers and risk-bearing groups, linking payment more closely to outcomes than to product volume alone.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High cost and reimbursement variability for advanced biofilm therapies | -1.6% | Global, most acute in Asia-Pacific and Latin America | Long term (≥ 4 years) |

| Limited biofilm-specific clinical endpoints in routine practice | -1.0% | Global, acute in Europe and North America where HTA scrutiny is highest | Medium term (2-4 years) |

| Product performance variability across wound types and exudates | -0.8% | Global | Medium term (2-4 years) |

| Regulatory and claims substantiation burden for anti-biofilm labeling | -0.6% | North America and Europe primary | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost and Reimbursement Variability for Advanced Biofilm Therapies

Premium anti-biofilm dressings and debridement products often cost 3-10 times more than standard gauze or basic antimicrobial dressings, creating a major adoption barrier in the biofilm treatment market. In the United States, CMS reimbursement for advanced wound care products under HCPCS codes remains exposed to policy changes that may narrow eligible wound categories or impose stricter use thresholds. Across Europe, varied health technology assessment standards can delay routine formulary access in Italy or Spain, even when a product receives reimbursement in Germany. In many Asia-Pacific and Middle East markets, out-of-pocket payments outside major urban hospitals continue to limit premium product uptake, making real-world cost and healing evidence essential to support premium pricing.

Limited Biofilm-Specific Clinical Endpoints in Routine Practice

Biofilm detection and measurement remain poorly standardized outside specialist wound care centers, slowing wider adoption in the biofilm treatment market. Most hospital and community care settings rely on visible signs, such as slough, odor, or delayed healing, instead of validated approaches like fluorescence imaging or molecular diagnostics. This approach often pushes anti-biofilm products later in the care pathway after standard measures fail, reducing preventive use. Without point-of-care detection methods that align with routine nursing workflows, broader adoption in the biofilm treatment market is likely to remain slower than clinical need suggests.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dressings Lead, Topical Agents Poised for Outpaced Growth

Dressings and grafts held 28.65% of the biofilm treatment market size in 2025, supported by broad clinical use of silver-based, PHMB-containing, and hydrofiber formats across chronic wound care. These products remain central because they address a wide range of wound profiles and are well established across hospitals, clinics, and wound specialist practices. Smith+Nephew’s March 2026 launch of the ALLEVYN COMPLETE CARE Foam Dressing highlights innovation in premium dressings, with a 5-layer design that keeps over 99% of bacteria away from the wound bed and absorbs up to 93% of mechanical energy. Debridement devices also maintain a meaningful position because biofilm disruption typically starts with the removal of necrotic or nonviable tissue.

Wound cleansers and irrigation solutions remain important support products and are often used with primary dressings in wound hygiene protocols. Kane Biotech’s revyve Antimicrobial Skin and Wound Cleanser, which received FDA 510(k) clearance in February 2026, reflects a more structured investment focus in a product area that had often been fragmented and less innovation-driven. Topical agents are the fastest-growing product segment in the biofilm treatment market at an 8.93% CAGR from 2026 to 2031, as gel-phase and enzymatic formats can penetrate biofilm matrices more effectively than surface-acting products.

By Treatment Method: Chemical Approaches Gain Ground in Evidence-Based Protocols

Physical debridement represented 35.23% of revenue in 2025, reflecting its role as the standard first step in wound bed preparation for biofilm control. The biofilm treatment market continues to rely on debridement because advanced products cannot perform effectively when necrotic tissue remains in place. However, physical debridement alone does not prevent biofilm recurrence, and clinical guidance increasingly recognizes this limitation. This gap is driving chemical and antiseptic treatment toward the fastest growth rate among treatment methods, at 9.67% CAGR through 2031.

Nitric oxide, hypochlorous acid, PHMB, and silver-combination approaches are gaining commercial attention as evidence supporting their biofilm-disruption role strengthens. Enzymatic treatment retains a distinct position in the biofilm treatment industry because it is less traumatic for patients with fragile or ischemic wound margins, especially in pressure ulcer care among older adults. Combination therapy, which pairs debridement with antimicrobial dressings, is becoming a more common care model under stewardship-focused wound management.

By Infection Type: Chronic Wounds Anchor Demand, Surgical Wounds Emerge as a Growth Vector

Chronic wounds accounted for 36.34% of 2025 revenue and remain the largest infection category in the biofilm treatment market, as diabetic foot ulcers, venous leg ulcers, and pressure injuries create sustained treatment demand. The epidemiology of the underlying conditions, not only current product availability, supports this leadership. A 2026 cross-sectional study in Scientific Reports found biofilm-forming bacterial isolates in 60% of diabetic foot ulcer patients, with moderate-to-high biofilm formers concentrated in higher-grade ulcers where care becomes more complex and costly.

Surgical and traumatic wounds are the fastest-growing infection type in the biofilm treatment market, with an 8.35% CAGR through 2031. Procedure growth in many countries is increasing the number of post-operative wounds that can develop early biofilm before standard hygiene steps fully control the site. Device-associated wound care is also attracting more product attention, particularly around orthopedic implant interfaces and vascular access points, where infection prevention and wound management increasingly overlap.

By End User: Hospitals Remain Core, Specialty Clinics Reshape Growth Economics

Hospitals held 52.88% of the biofilm treatment market share in 2025, reflecting their role as the primary procurement center for inpatient wound care and the setting where product trials and formulary decisions usually begin. This leadership also reflects case complexity, as hospitals manage the largest share of severe, infected, and hard-to-heal wounds that require advanced care. Organogenesis reported 17% year-over-year growth in Advanced Wound Care net product revenue in 2025, supported by higher volume and PHMB-based antimicrobial lines that target biofilm after debridement. In the biofilm treatment market, hospital demand continues to set the pace for product validation and early revenue capture.

Specialty clinics and wound care centers are the fastest-growing end-user segment, expanding at a 9.78% CAGR from 2026 to 2031 as more complex wound care shifts out of acute inpatient settings. Their influence exceeds their current revenue base because wound specialists and podiatrists in these centers often shape care protocols later adopted by hospital procurement teams. Ambulatory surgical centers are also expanding their wound care role as same-day debridement volumes increase and follow-up pathways become more structured. Home healthcare remains smaller, but it is scaling steadily as products with longer wear time and easier application, such as Solventum’s V.A.C. Peel and Place Dressing designed for 7-day wear, support clinical-grade wound care outside institutional settings.

Geography Analysis

North America reported to account for 38.56% of the biofilm treatment market size in 2025, supported by a dense hospital network, a high chronic wound burden, and widespread adoption of advanced wound care products. The United States remains the regional core, as chronic wounds affect more than 8 million people, with biofilm persistence contributing to many non-healing cases. Canada is gaining traction in specialty wound care through newer product approvals and the expected return of commercial activity around Revyve across the United States and Canada in 2026. Mexico remains a smaller contributor, although rising diabetes prevalence and private hospital expansion continue to support early demand.

Europe maintains a significant position in the biofilm treatment market, driven by strict clinical standards, active HTA review, and the strong influence of EWMA guidance on prescribing behavior. Germany, the UK, France, Italy, Spain, and Poland are to be the first launch markets for ConvaTec’s ConvaNiox in 2025, reflecting a strategy focused on evidence generation in the region’s closely monitored health systems. EWMA 2026 in Bremen remains the key European clinical forum for wound management, where ConvaTec and Smith+Nephew plan to present new data and strengthen their commercial presence. Smaller markets across the rest of Europe are advancing as wound hygiene protocols become more closely linked to antimicrobial resistance planning.

Asia-Pacific is the fastest-growing regional segment in the biofilm treatment market, with a CAGR of 8.56% from 2026 to 2031. China and India remain the main growth engines, supported by a rising diabetes burden and continued healthcare infrastructure investment. India is expanding its medical device base and hospital capacity, while China is increasing the use of advanced wound care products across public and private settings. Japan’s aging population supports steady demand for advanced dressings, while GCC countries, Brazil, and Argentina are gradually improving access through private hospital expansion, procurement growth, insurance penetration, and public purchasing.

Competitive Landscape

The biofilm treatment market is moderately concentrated at the portfolio level, with ConvaTec, Smith+Nephew, Mölnlycke Health Care, and Solventum maintaining strong positions in global hospital procurement. Competition is increasing through broader portfolios from established wound care companies and targeted innovation from smaller specialists. Larger companies leverage scale, distributor reach, and evidence portfolios to protect hospital relationships, while Kane Biotech, Next Science, and Sanara MedTech are gaining traction through biofilm-specific solutions aligned with stewardship goals and unmet clinical needs.

Strategic activity indicates that evidence generation and product breadth will continue to shape the biofilm treatment market. ConvaTec reported to use EWMA 2026 to present 13 abstracts across foam, multimodal, and nitric oxide-generating dressings, strengthening its data-led portfolio strategy. Smith+Nephew reported to expand its premium dressing position with the March 2026 US launch of ALLEVYN COMPLETE CARE and highlight RENASYS EDGE tNPWT at EWMA 2026, linking advanced dressings with broader wound therapy capabilities. Kane Biotech is strengthening its specialist role through FDA 510(k) clearance for Revyve Antimicrobial Skin and Wound Cleanser and continued clinical evidence development for its wound gel platform.

Clinical evidence and regulatory filings are becoming key tools for building prescriber trust in the biofilm treatment market. Companies that publish randomized trial data, present findings at major wound care meetings, and obtain FDA or European clearances with clear product claims are raising entry standards. MiMedx reported record full-year 2025 net sales of USD 419 million, up 20% year over year, showing how evidence in wound tissue innovation can support commercial momentum. Technology convergence is also driving differentiation, as companies combine anti-biofilm products with negative pressure wound therapy, wound detection tools, or digital wound management. At the same time, the FDA’s updated Quality Management System Regulation, effective February 2026, may increase pressure on smaller manufacturers and support consolidation around mid-sized specialty platforms.

Biofilms Treatment Industry Leaders

Smith & Nephew plc

Mölnlycke Health Care AB

ConvaTec Group Plc

Coloplast A/S

B. Braun SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Kane Biotech expanded revyve commercialization in North America, appointed business development leaders, and scaled manufacturing after FDA 510(k) clearance, strengthening its biofilm-disrupting wound care platform in the United States and Canada.

- May 2026: Convatec showcased its Advanced Wound Care pipeline at EWMA 2026, presenting clinical and real-world evidence on dressings and Wound Hygiene outcomes to reinforce its biofilm management leadership.

- May 2026: Smith+Nephew presented ALLEVYN COMPLETE CARE Dressing and RENASYS EDGE tNPWT at EWMA 2026, expanding its advanced wound care portfolio for hard-to-heal wounds across hospital and home settings.

- February 2026: Kane Biotech received FDA 510(k) clearance for revyve Antimicrobial Skin and Wound Cleanser and restarted US and Canada commercialization for its FDA-cleared wound care platform.

- July 2025: Sanara MedTech launched the Tissue Health Plus Wound Care Provider Pilot Program, linking wound care payments to clinical outcomes and promoting advanced biofilm-targeting products.

Global Biofilms Treatment Market Report Scope

As per the scope of the report, biofilms are complex, self-protecting communities of microorganisms (like bacteria or fungi) that stick to surfaces and encase themselves in a slimy, sticky matrix. Because of this shield, bacteria in a biofilm can be up to 1,000 times more resistant to standard antibiotics than free-floating bacteria.

The biofilms treatment market is segmented by product type, treatment method, infection type, end user, and geography. By product type, the market includes dressings and grafts, debridement devices, topical agents, wound cleansers and irrigation solutions, and other product types. By treatment method, the market is segmented into physical debridement, chemical and antiseptic treatment, enzymatic treatment, and combination therapy. By infection type, the market is categorized into chronic wounds, surgical and traumatic wounds, diabetic foot ulcers, venous leg ulcers, pressure ulcers, and burns and other open wounds. By end user, the market is segmented into hospitals, specialty clinics and wound care centers, home healthcare settings, and ambulatory surgical centers. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Dressings and Grafts |

| Debridement Devices |

| Topical Agents |

| Wound Cleansers and Irrigation Solutions |

| Other Product Types |

| Physical Debridement |

| Chemical and Antiseptic Treatment |

| Enzymatic Treatment |

| Combination Therapy |

| Chronic Wound |

| Surgical and Traumatic Wounds |

| Diabetic Foot Ulcers |

| Venous Leg Ulcers |

| Pressure Ulcers |

| Burn and Other Open Wounds |

| Hospitals |

| Specialty Clinics and Wound Care Centers |

| Home Healthcare Settings |

| Ambulatory Surgical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Dressings and Grafts | |

| Debridement Devices | ||

| Topical Agents | ||

| Wound Cleansers and Irrigation Solutions | ||

| Other Product Types | ||

| By Treatment Method | Physical Debridement | |

| Chemical and Antiseptic Treatment | ||

| Enzymatic Treatment | ||

| Combination Therapy | ||

| By Infection Type | Chronic Wound | |

| Surgical and Traumatic Wounds | ||

| Diabetic Foot Ulcers | ||

| Venous Leg Ulcers | ||

| Pressure Ulcers | ||

| Burn and Other Open Wounds | ||

| By End User | Hospitals | |

| Specialty Clinics and Wound Care Centers | ||

| Home Healthcare Settings | ||

| Ambulatory Surgical Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the biofilm treatment market by 2031?

The biofilm treatment market is forecast to reach USD 4.28 billion by 2031 from USD 3.01 billion in 2026, growing at a 7.28% CAGR.

Which product category leads revenue in 2025?

Dressings and grafts lead with a 28.65% revenue share in 2025 because they are widely used across chronic wound settings.

Which treatment approach is growing the fastest?

Chemical and antiseptic treatment is the fastest-growing treatment method, with a 9.67% CAGR through 2031.

Why do chronic wounds matter so much in this space?

Chronic wounds account for 36.34% of 2025 revenue, and biofilms are heavily linked to diabetic foot ulcers, venous leg ulcers, pressure injuries, and burn wounds.

Which region leads today, and which one is growing the fastest?

North America leads with 38.56% share in 2025, while Asia-Pacific is the fastest-growing region at an 8.56% CAGR through 2031.

How are hospitals and specialty clinics shaping demand?

Hospitals remain the largest end user with 52.88% share in 2025, while specialty clinics and wound care centers are growing fastest at a 9.78% CAGR.

Page last updated on: