Biocompatible 3D Printing Materials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

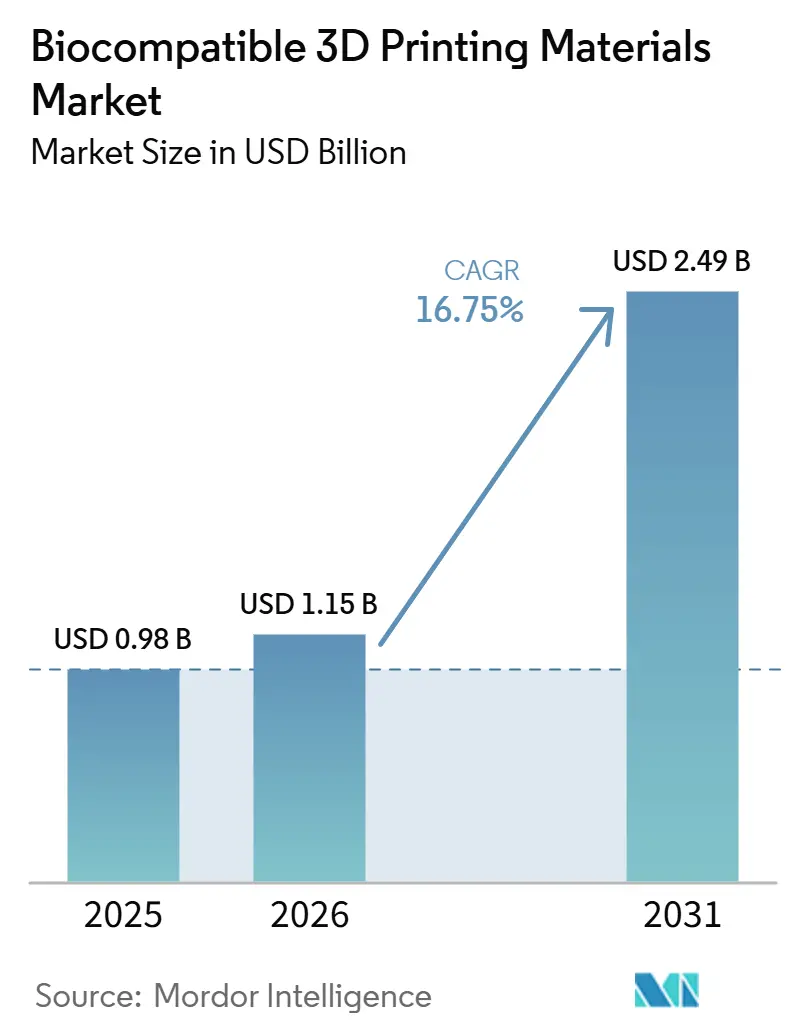

| Market Size (2026) | USD 1.15 Billion |

| Market Size (2031) | USD 2.49 Billion |

| Growth Rate (2026 - 2031) | 16.75% CAGR |

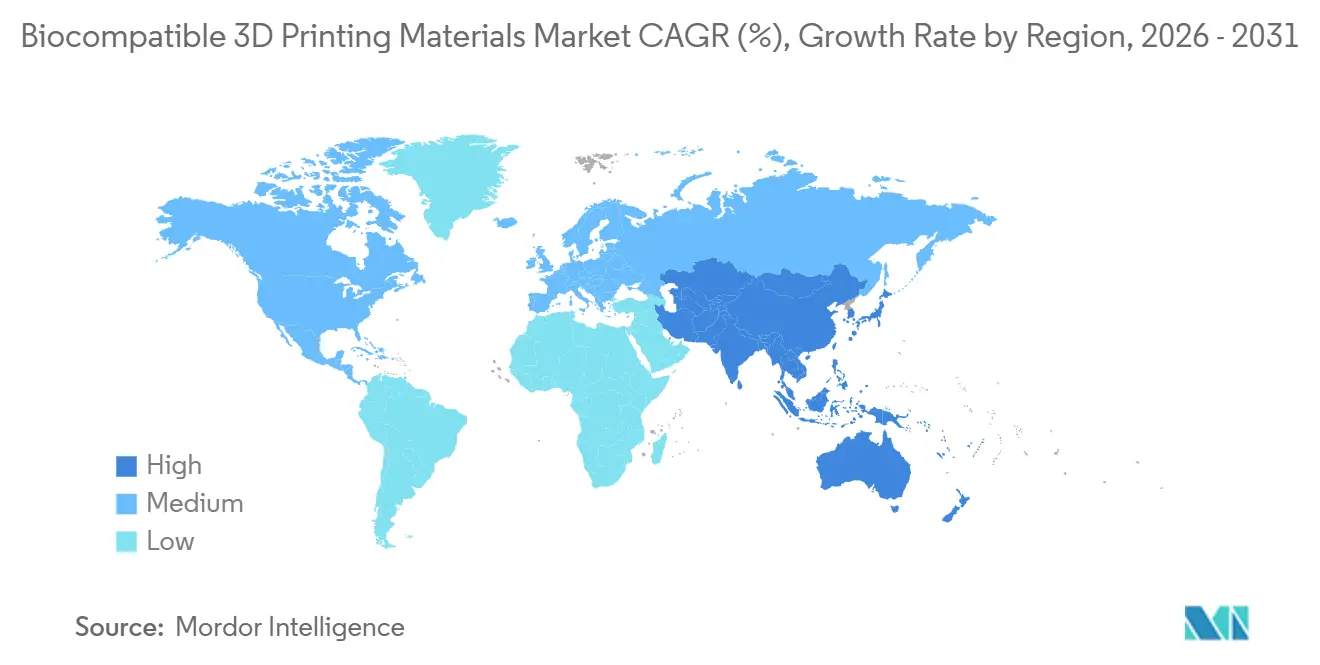

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biocompatible 3D Printing Materials Market Analysis by Mordor Intelligence

The Biocompatible 3D Printing Materials Market size is projected to expand from USD 0.98 billion in 2025 and USD 1.15 billion in 2026 to USD 2.49 billion by 2031, registering a CAGR of 16.75% between 2026 to 2031.

The market is expanding because hospitals, contract manufacturers, and specialty device OEMs are using validated in-house printing capabilities more widely and are also broadening their qualified material portfolios. The shift in the biocompatible 3D printing materials market is no longer limited to prototyping, because additive production is now moving into regulated use for implants, dental restorations, and tissue-related constructs. Demand in the biocompatible 3D printing materials market is also supported by the fact that patient-specific geometry directly affects clinical outcomes, which keeps this category closely tied to care delivery rather than general industrial spending cycles. Competitive activity in the biocompatible 3D printing materials market is centered on validated formulations, sterilizable workflows, and closer coordination between materials suppliers and downstream device makers. Opportunity in the biocompatible 3D printing materials market is strongest where suppliers can reduce qualification friction, support point-of-care manufacturing, and align materials with repeatable clinical workflows.

Key Report Takeaways

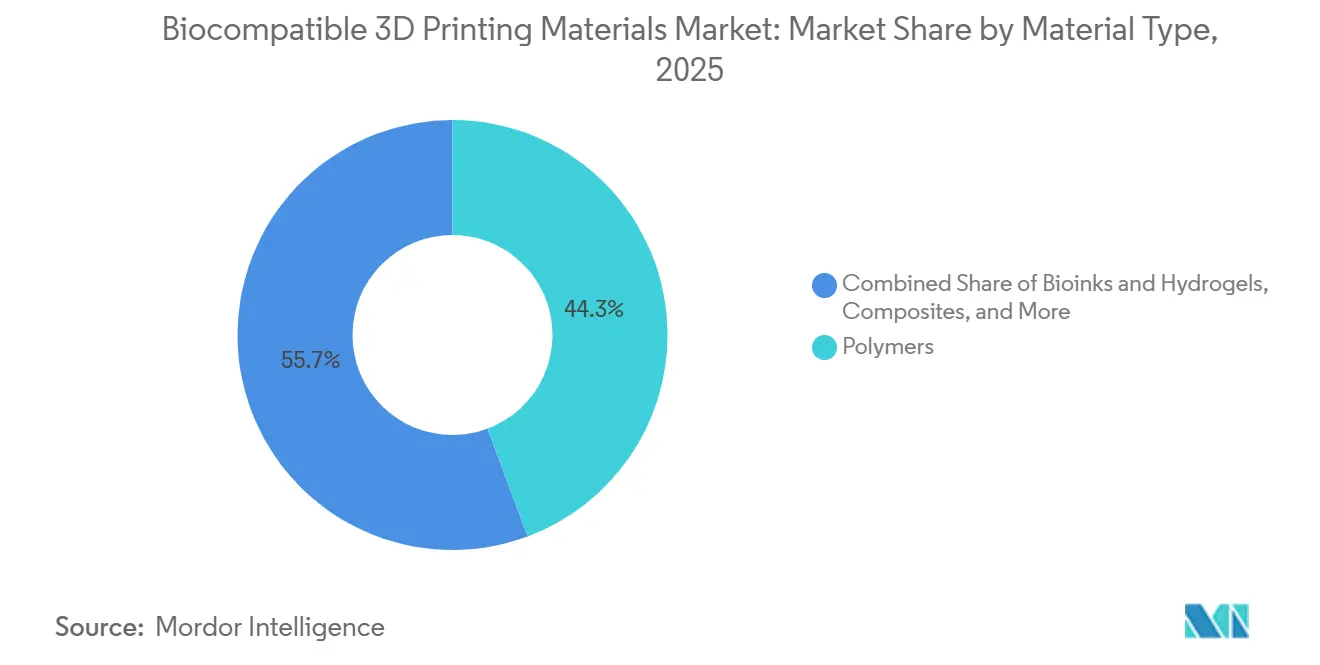

- By material type, polymers held 44.31% of revenue in 2025, while bioinks and hydrogels are projected to expand at an 18.38% CAGR through 2031.

- By form, filament accounted for 38.24% of revenue in 2025, while bioinks are forecast to grow at a 19.52% CAGR through 2031.

- By technology, fused deposition modeling captured 31.26% of revenue in 2025, while bioprinting is projected to advance at an 18.55% CAGR through 2031.

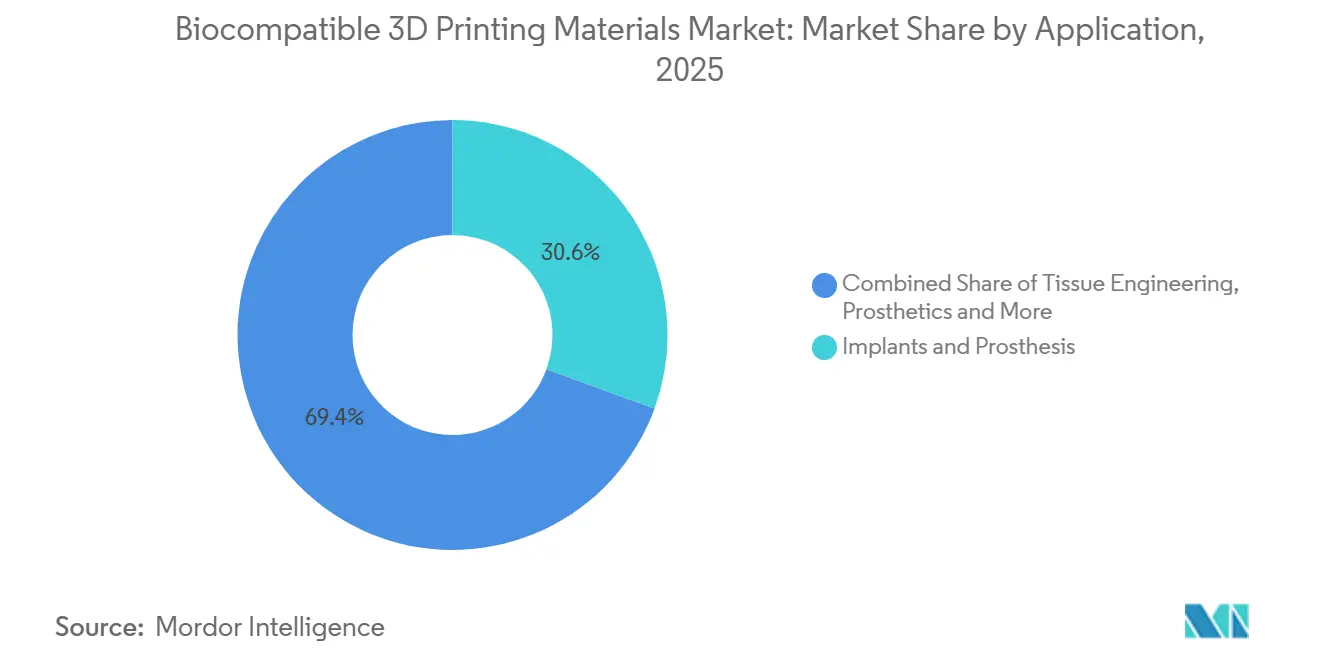

- By application, implants and prosthesis represented 30.56% of revenue in 2025, while tissue engineering is forecast to record a 17.65% CAGR through 2031.

- By end user, hospitals and clinics held 35.52% of revenue in 2025, while medical device manufacturers are projected to grow at an 18.25% CAGR through 2031.

- By geography, North America represented 36.22% share in 2025, while Asia-Pacific is expected to expand at 20.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Biocompatible 3D Printing Materials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Patient-Specific Medical Devices | +5.8% | Global, with early gains in North America, Germany, and Japan | Long term (≥ 4 years) |

| Expansion of Digital Dentistry and Chairside Manufacturing | +3.4% | North America, Western Europe, China, South Korea | Medium term (2-4 years) |

| Regulatory Clarification for Biocompatible Material Qualification | +2.7% | Global, led by U.S. and EU jurisdictions | Medium term (2-4 years) |

| Faster Validation of Sterilizable Print Workflows | +1.9% | North America and EU, with spillover to core APAC markets | Short term (≤ 2 years) |

| Growth in Point-of-Care Production Models | +2.1% | North America, EU, Australia, Thailand | Medium term (2-4 years) |

| Reimbursement Pressure Favoring Lower-Fit-Error Customization | +1.6% | North America initially, with follow-on in Western Europe | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Patient-Specific Medical Devices

The biocompatible 3D printing materials market is being pulled forward by orthopedic, craniofacial, and spinal procedures that need shapes conventional fabrication cannot match at the same turnaround. Titanium alloy, especially Ti-6Al-4V, remains central in load-bearing implants because its elastic modulus of 110 GPa is closer to cortical bone than cobalt-chrome or stainless steel alternatives, which lowers stress-shielding risk. A 2025 clinical study also showed that porous Ti-6Al-4V lumbar fusion implants produced through additive manufacturing delivered primary stability and favorable bone apposition in use. That is raising the value of suppliers that can pair material chemistry with pre-qualified porous print parameters and supporting clinical data. Materialise’s bioresorbable polycaprolactone tracheobronchial splint entered a U.S. FDA pivotal clinical trial in 2025, which shows that resorbable polymer formats are moving closer to active clinical use[1]Materialise, “Bioresorbable Implant 3D Printed by Materialise Enters Clinical Trial,” Materialise Press Release, materialise.com.

Expansion of Digital Dentistry and Chairside Manufacturing

The biocompatible 3D printing materials market is also gaining from dental workflows that are moving closer to the chairside and reducing multi-day restorative cycles. This shift changes how materials are packaged and used, because demand moves away from centralized laboratory batches and toward controlled, clinic-ready formats. It also lifts material consumption frequency, since chairside systems turn materials over at the pace of appointments rather than lab production schedules. Rapid Shape’s RS VIVO dental resin portfolio achieved FDA approval in February 2026, which strengthens the position of suppliers that can offer a full certified workflow across denture and splint applications[2]Rapid Shape, “Rapid Shape RS VIVO – New FDA Approved Dental Resins,” Rapid Shape, rapidshape3d.com. In the biocompatible 3D printing materials market, this makes regulatory-ready dental resins more important than simple formulation breadth alone.

Regulatory Clarification for Biocompatible Material Qualification

The biocompatible 3D printing materials market benefits when a cleared device creates a visible reference point for downstream users that are still deciding how much compliance risk to absorb. The July 2025 De Novo marketing authorization for TISSIUM’s COAPTIUM CONNECT, a fully bioabsorbable photopolymer nerve repair device developed with 3D Systems, marked the first vat-photopolymerized implant to achieve FDA clearance. That event matters beyond one device because it shows that resin-based implantable pathways can move through formal review and reach commercialization. Hospitals and contract manufacturers often use these reference cases as practical anchors when they evaluate their own in-house material adoption plans. In the biocompatible 3D printing materials market, this lowers perceived qualification risk for adjacent photopolymer applications.

Faster Validation of Sterilizable Print Workflows

Sterilization remains a practical checkpoint in the biocompatible 3D printing materials market because the same process that ensures microbiological safety can also alter material performance. A 2025 study on 3D-printed PEEK found that gamma sterilization at 25 kGy created nonlinear effects, with cross-linking and delayed oxidative chain scission varying with print conditions. This means buyers cannot treat sterilization as a routine final step and must validate each material-printer combination with care. Suppliers that ship materials with documented post-sterilization behavior reduce the internal burden on hospitals and device makers. That shortens time to clinical use and supports faster material qualification across the biocompatible 3D printing materials market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy Biocompatibility and Sterilization Validation Cycles | -3.2% | Global, more acute in emerging markets with limited testing infrastructure | Long term (≥ 4 years) |

| Limited Cross-Platform Material Interoperability | -1.8% | Global, particularly in hospital and CMO multi-vendor environments | Medium term (2-4 years) |

| High Cost of Qualified Medical-Grade Feedstocks | -2.1% | More severe in South America, MEA, and Southeast Asia | Medium term (2-4 years) |

| Process Drift Across Printer, Resin, and Post-Processing Steps | -1.4% | Global, amplified in distributed or multi-site manufacturing | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lengthy Biocompatibility and Sterilization Validation Cycles

The biocompatible 3D printing materials market still faces long qualification cycles when a supplier tries to bring a new medical-grade formulation into regulated use. A full ISO 10993-1-compliant evaluation can take 12 to 18 months when cytotoxicity, sensitization, implantation response, systemic toxicity, and other endpoints are required. That time burden is manageable for large suppliers with established regulatory teams, but it is harder for smaller developers working on novel bioinks or biodegradable polymers. The result is slower portfolio diversification, even in areas where clinical demand is moving faster than qualification capacity. This restraint keeps the biocompatible 3D printing materials market tilted toward suppliers that already have documentation depth and validation infrastructure.

Limited Cross-Platform Material Interoperability

Limited interoperability remains a practical drag on the biocompatible 3D printing materials market because many printer OEMs still validate materials only inside their own hardware ecosystems. In a multi-vendor hospital network, that forces buyers to either stay inside a locked platform or pay for new validation work each time they try to use an approved material elsewhere. The cost is not only financial, because procurement teams also face delays in sterilization review, quality documentation, and internal signoff. This slows materials trial activity and reduces the willingness of institutions to expand their qualified portfolios. A supplier that can validate one medical polymer or resin across multiple leading systems would have a clear structural advantage in the biocompatible 3D printing materials market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polymers Lead the Clinical Base, Bioinks Define the Growth Ceiling

Polymers accounted for 44.31% share of the biocompatible 3D printing materials market size in 2025, while bioinks and hydrogels are projected to grow at an 18.38% CAGR through 2031. In the biocompatible 3D printing materials industry, that split shows a market anchored by established polymers but pulled forward by living and semi-living formulations. PEEK and photopolymer resins remain central across dental, maxillofacial, and orthopedic workflows because they already sit inside validated care pathways. Evonik’s VESTAKEEP i4 3DF remains a key upstream reference point as the first ASTM F2026-compliant implant-grade PEEK filament for 3D printing[3]Evonik Industries AG, “VESTAKEEP i4 3DF – Product Specifications,” Evonik Industries AG, evonik.com.

Biodegradable polymer formats are advancing as clinical programs move closer to real-world use. Materialise’s bioresorbable tracheobronchial splint trial is important because it connects polymer development to a formal FDA pathway rather than a research-only setting. Metals, led by titanium and titanium alloys, remain indispensable in load-bearing orthopedic and spinal applications where long-term strength is non-negotiable. Ceramics are becoming more relevant in chairside dental use, while composites continue to serve targeted niches such as hearing aid shells and craniofacial models. The biocompatible 3D printing materials market therefore keeps its revenue base in proven polymers and metals even as future momentum shifts toward biologically active material classes.

By Form: Filament Anchors Clinical Production, Bioinks Enter the Clinical Corridor

Filament held 38.24% of form revenue in 2025, while bioinks are forecast to expand at a 19.52% CAGR through 2031. The biocompatible 3D printing materials market still leans heavily on filament because the installed base of FDM and FFF systems for medical PEEK remains broad in orthopedic, spinal, and maxillofacial workflows. Evonik’s VESTAKEEP range shows why this format stays relevant, because it covers different implantability grades within one product family. That flexibility helps buyers match form factor to contact duration and regulatory need without changing material family.

Bioinks are growing faster because they are moving beyond academic handling and into structured pre-clinical and early clinical programs. Work on GelMA and related hydrogel systems is relevant here, because published research shows these materials can create a supportive microenvironment for stromal keratocyte maintenance and corneal repair applications. That scientific base supports the idea that form is no longer just a packaging issue and is becoming part of biological function. The clinical corridor for bioinks is still narrower than for filament or liquid resins, but the direction of travel is clear. This keeps the biocompatible 3D printing materials market focused on both handling practicality and cell-supportive performance.

By Technology: FDM Holds Clinical Footprint, Bioprinting Leads the Forward Growth Curve

Fused deposition modeling held 31.26% of biocompatible 3D printing materials market share in 2025, while bioprinting is projected to advance at an 18.55% CAGR through 2031. FDM keeps its lead because it has a wide medical footprint in PEEK-based implant manufacturing and is already established in many hospital and CMO workflows. Selective laser sintering remains critical for porous titanium structures, especially where density control and lattice geometry matter in spinal and orthopedic applications. The biocompatible 3D printing materials market therefore still relies on conventional additive technologies for its main clinical throughput.

Bioprinting leads the growth curve because the underlying material logic is different from conventional thermoplastics or powders. It depends on bioinks, hydrogels, and cell-supportive systems that are being studied for predictive biofabrication and tissue-related constructs. That does not mean it will replace established technologies in the near term, because the qualification burden remains much higher. It does mean that more of the future value in the biocompatible 3D printing materials market will come from technologies able to process living or biologically active materials. Multi jet and material jetting will continue to matter in planning models and multi-material anatomical constructs, but they sit outside the main growth frontier.

By Application: Implants Set the Volume Base, Tissue Engineering Defines the Decade’s Growth Arc

Implants and prosthesis represented 30.56% of revenue in 2025, while tissue engineering is projected to grow at a 17.65% CAGR through 2031. That ranking shows the biocompatible 3D printing materials market still depends most on applications with regulatory depth, known materials, and established reimbursement pathways inside care delivery. A 2026 clinical study on microporous titanium prostheses for infected long-bone defects reported primary integration and no macroscopic infection through 12 months of follow-up. This supports the view that implantable metal applications remain the clearest volume center for the current market.

Tissue engineering is the faster-growth application because it sits where biological materials and patient-specific need intersect most clearly. Published work on predictive biofabrication and advanced bioink design shows why GelMA hydrogels, polysaccharide systems, and protein-responsive constructs are drawing more clinical attention. The application is still earlier than implants, but it expands the market into wound healing, scaffold fabrication, and regenerative use cases that conventional manufacturing cannot match. That is why the biocompatible 3D printing materials market sees tissue engineering as a growth arc rather than a present revenue base.

By End User: Hospitals Anchor Volume Demand, Device Manufacturers Capture the Growth Premium

Hospitals and clinics held 35.52% of revenue in 2025, while medical device manufacturers are projected to grow at an 18.25% CAGR through 2031. In the biocompatible 3D printing materials industry, hospitals remain the main institutional buyers because they run point-of-care programs, manage traceability requirements, and purchase validated portfolios for direct clinical use. Their procurement behavior tends to be sticky because requalifying a new material can trigger another cycle of documentation, sterilization review, and internal approval. The biocompatible 3D printing materials market therefore keeps a strong volume base in health systems that already have quality-managed additive capabilities.

Medical device manufacturers are the faster-growing end user because additive manufacturing is moving into primary production rather than staying limited to prototyping. That change pushes device makers to work more closely with upstream materials suppliers on lot traceability, qualification, and repeatable processing. It also tightens the connection between material selection and regulatory strategy. In the biocompatible 3D printing materials market, this end-user group is capturing the growth premium because it is actively redesigning supply chains around additive pathways.

Geography Analysis

North America accounted for 36.62% of biocompatible 3D printing materials market share in 2025, giving it the largest regional position in the current market. The region benefits from the deepest concentration of FDA-cleared material-printer ecosystems, mature hospital point-of-care programs, and close interaction between clinical buyers and suppliers. The VA Puget Sound bioprinting facility is especially important because it was built as a hospital-embedded, production-ready model with replication potential across the VA system. Canada contributes through research-linked bioprinting and dental digitalization activity, while Mexico is strengthening its position as a nearby manufacturing base for North American medical supply chains.

Europe held a meaningful share in 2025 and remains defined by regulatory rigor, strong materials science capability, and a dense clinical innovation base. Germany, the UK, and France lead regional development, with Germany holding a major upstream advantage in engineering polymers and medical-grade feedstocks. Materialise added custom-made PEEK implants to its CMF portfolio in February 2026 under EN ISO 13485-certified manufacturing conditions with a 72-hour delivery commitment. France also stands out because TISSIUM’s photopolymer nerve repair device, developed with 3D Systems, became the first vat-photopolymerized implant cleared by the FDA in July 2025.

Asia-Pacific is projected to grow at a 19.15% CAGR through 2031, making it the fastest-growing geography in the biocompatible 3D printing materials market. Growth is tied to rising bioprinting investment, faster dental digitization, and a widening base of orthopedic demand across aging populations. Japan and South Korea benefit from high-precision manufacturing ecosystems, while China remains important because of its scale and state-backed activity in advanced medical technologies. India is developing as a cost-focused production base for filament and pellet systems serving surgical guides and fracture fixation use cases. Thailand’s Siriraj Hospital showed that Southeast Asian institutions are moving from feasibility work into real clinical deployment when it completed surgery using a point-of-care 3D-printed titanium hip socket in April 2025. The Middle East and Africa remain split between premium GCC demand and infrastructure constraints elsewhere, while South America is still held back mainly by access to qualified medical-grade polymer and metal feedstocks. This means the biocompatible 3D printing materials market is expanding globally, but readiness still depends heavily on local validation infrastructure and supply access.

Competitive Landscape

The biocompatible 3D printing materials market shows moderate to high concentration across a core tier of integrated players, while the outer edge of formulation activity remains fragmented in bioinks, biodegradable polymers, and specialty ceramics. The leading companies compete by linking validated materials to hardware, workflow software, and regulatory support rather than selling chemistry alone. That model supports switching costs and recurring material revenue because the buyer is adopting an entire workflow, not only a feedstock. The biocompatible 3D printing materials market therefore rewards companies that can hold performance, documentation, and clinical usability together. Evonik’s VESTAKEEP i4 3DF illustrates this upstream leverage, because implant-grade PEEK supply remains strategically important for device makers that do not want to build polymer synthesis capabilities on their own.

A major gap still exists in cross-platform qualification. Hospitals and CMOs that run mixed printer fleets need validated materials that can move across systems without forcing a full requalification cycle every time. Few suppliers have solved that problem at scale, which leaves procurement teams stuck between locked ecosystems and extra validation cost. In the biocompatible 3D printing materials market, that white space remains one of the clearest areas for competitive differentiation.

Strategic execution is increasingly visible in targeted moves by established players. Materialise moved a bioresorbable printed implant into a U.S. FDA pivotal clinical trial in 2025, which shows a direct commitment to resorbable clinical formats. Materialise also expanded its CMF offering with custom-made PEEK implants in 2026, reinforcing speed and certified manufacturing as part of its competitive offer. 3D Systems helped establish a new regulatory reference point when TISSIUM’s photopolymer nerve repair device became the first vat-photopolymerized implantable device cleared by the FDA in 2025. These moves show that the biocompatible 3D printing materials market is being shaped less by raw material breadth and more by validation depth, regulatory execution, and integration into real clinical pathways.

Biocompatible 3D Printing Materials Industry Leaders

Formlabs Inc.

3D Systems, Inc.

Stratasys Ltd.

Evonik Industries AG

Henkel AG and Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: SHINING 3D Dental launched Ceramix-Nano in North America and Asia. The chairside capsule 3D printer uses patented Adaptive Pneumatic Stereolithography to make permanent ceramic crowns, veneers, and bridges in under 30 minutes per appointment. Its capsule-based material delivery system removes the need for laboratory turnaround for single-unit restorations and moves material economics toward closed-system, per-restoration pricing.

- July 2025: De Novo marketing authorization granted to TISSIUM's COAPTIUM CONNECT, a fully bioabsorbable photopolymer nerve repair device developed with 3D Systems, marked the first vat-photopolymerized implant to achieve FDA clearance, establishing a categorical precedent that expands the eligible application surface for resin-based biocompatible 3D printing materials substantially.

Global Biocompatible 3D Printing Materials Market Report Scope

As per the scope of the report, biocompatible 3D printing materials are materials specifically designed for use in medical or biological environments that do not produce adverse reactions when in contact with living tissues or fluids. These materials are safe for implantation, tissue engineering, or other biomedical applications, ensuring compatibility with the human body or biological systems while maintaining the necessary mechanical and chemical properties for effective 3D printing.

The biocompatible 3D printing materials market is segmented by material type into polymers (photopolymer resins, thermoplastic polymers, biodegradable polymers), metals (titanium and titanium alloys, stainless steel, cobalt-chrome alloys), ceramics (zirconia, alumina, other ceramics), composites, bioinks and hydrogels, and other material types; by form into powder, filament, liquid, resin, bioinks, and other forms; by technology into vat photopolymerization, fused deposition modeling, selective laser sintering, multi-jet modeling, material jetting, bioprinting, and other technologies; by application into implants and prostheses, prototyping and surgical guides, tissue engineering, scaffold fabrication, prosthetics, drug delivery systems, surgical instruments, hearing aids, dental appliances, and other applications; by end user into hospitals and clinics, dental laboratories, medical device manufacturers, contract manufacturing organizations, and other end users; and by geography into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Polymers | Photopolymer Resins |

| Thermoplastic Polymers | |

| Biodegradable Polymers | |

| Metals | Titanium and Titanium Alloys |

| Stainless Steel | |

| Cobalt-Chrome Alloys | |

| Ceramics | Zirconia |

| Alumina | |

| Other Ceramics | |

| Composites | |

| Bioinks and Hydrogels | |

| Other Material Types |

| Powder |

| Filament |

| Liquid |

| Resin |

| Bioinks |

| Other Forms |

| Vat Photopolymerization |

| Fused Deposition Modeling |

| Selective Laser Sintering |

| Multi Jet Modeling |

| Material Jetting |

| Bioprinting |

| Other Technologies |

| Implants and Prosthesis |

| Prototyping and Surgical Guides |

| Tissue Engineering |

| Scaffold Fabrication |

| Prosthetics |

| Drug Delivery Systems |

| Surgical Instruments |

| Hearing Aids |

| Dental Appliances |

| Other Applications |

| Hospitals and Clinics |

| Dental Laboratories |

| Medical Device Manufacturers |

| Contract Manufacturing Organizations |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material Type | Polymers | Photopolymer Resins |

| Thermoplastic Polymers | ||

| Biodegradable Polymers | ||

| Metals | Titanium and Titanium Alloys | |

| Stainless Steel | ||

| Cobalt-Chrome Alloys | ||

| Ceramics | Zirconia | |

| Alumina | ||

| Other Ceramics | ||

| Composites | ||

| Bioinks and Hydrogels | ||

| Other Material Types | ||

| By Form | Powder | |

| Filament | ||

| Liquid | ||

| Resin | ||

| Bioinks | ||

| Other Forms | ||

| By Technology | Vat Photopolymerization | |

| Fused Deposition Modeling | ||

| Selective Laser Sintering | ||

| Multi Jet Modeling | ||

| Material Jetting | ||

| Bioprinting | ||

| Other Technologies | ||

| By Application | Implants and Prosthesis | |

| Prototyping and Surgical Guides | ||

| Tissue Engineering | ||

| Scaffold Fabrication | ||

| Prosthetics | ||

| Drug Delivery Systems | ||

| Surgical Instruments | ||

| Hearing Aids | ||

| Dental Appliances | ||

| Other Applications | ||

| By End User | Hospitals and Clinics | |

| Dental Laboratories | ||

| Medical Device Manufacturers | ||

| Contract Manufacturing Organizations | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the biocompatible 3D printing materials market?

The market stands at USD 1.15 billion in 2026 and is forecast to reach USD 2.49 billion by 2031 at a 16.75% CAGR.

Which material type leads revenue in 2025?

Polymers led with 44.31% of revenue in 2025, supported by PEEK and photopolymer resin use across dental, maxillofacial, and orthopedic workflows.

Which form is growing the fastest?

Bioinks are the fastest-growing form, with a 19.52% CAGR projected through 2031, even though filament held the largest 2025 share at 38.24%.

Which technology has the largest installed clinical base?

Fused deposition modeling led with 31.26% of revenue in 2025 because it is widely used in PEEK-based implant and point-of-care workflows.

Which application is expanding the fastest through 2031?

Tissue engineering is projected to grow at a 17.65% CAGR through 2031, while implants and prosthesis remain the largest application segment with 30.56% of revenue in 2025.

Which region is growing the fastest?

Asia-Pacific is the fastest-growing region with a 19.15% CAGR through 2031, while North America held the largest regional share at 36.62% in 2025.

Page last updated on: