Biliary Tumor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.85 Billion |

| Market Size (2031) | USD 1.16 Billion |

| Growth Rate (2026 - 2031) | 6.40% CAGR |

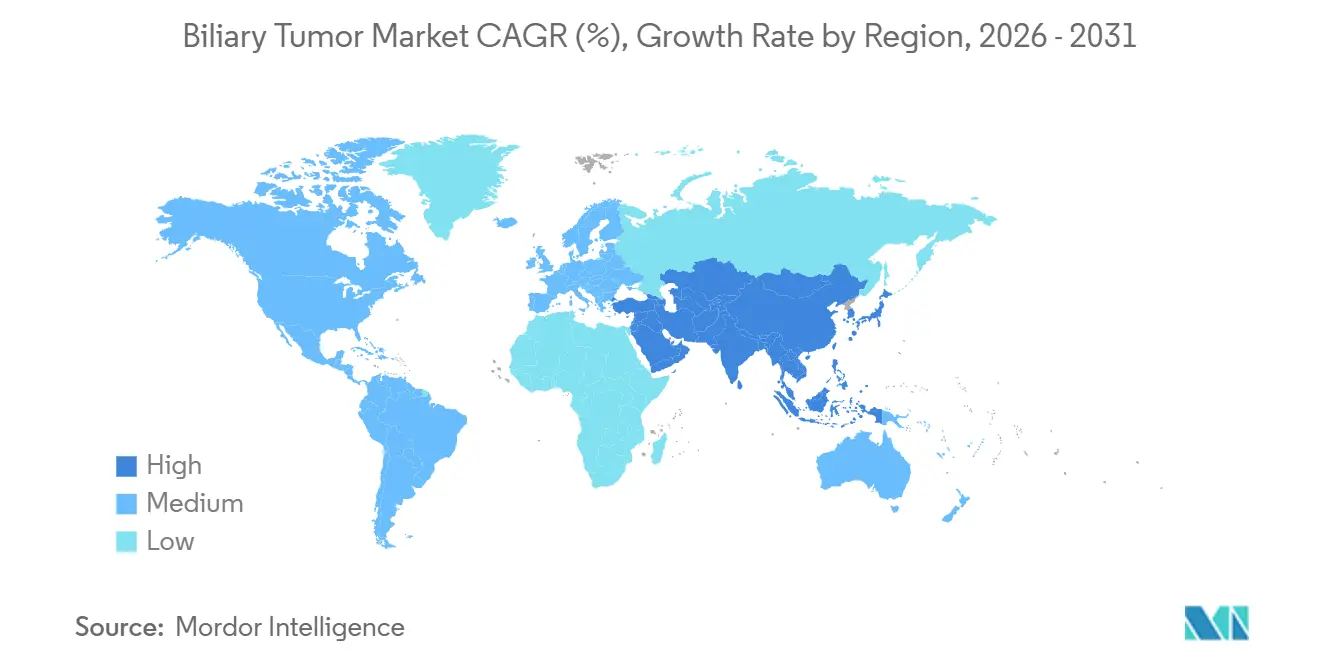

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

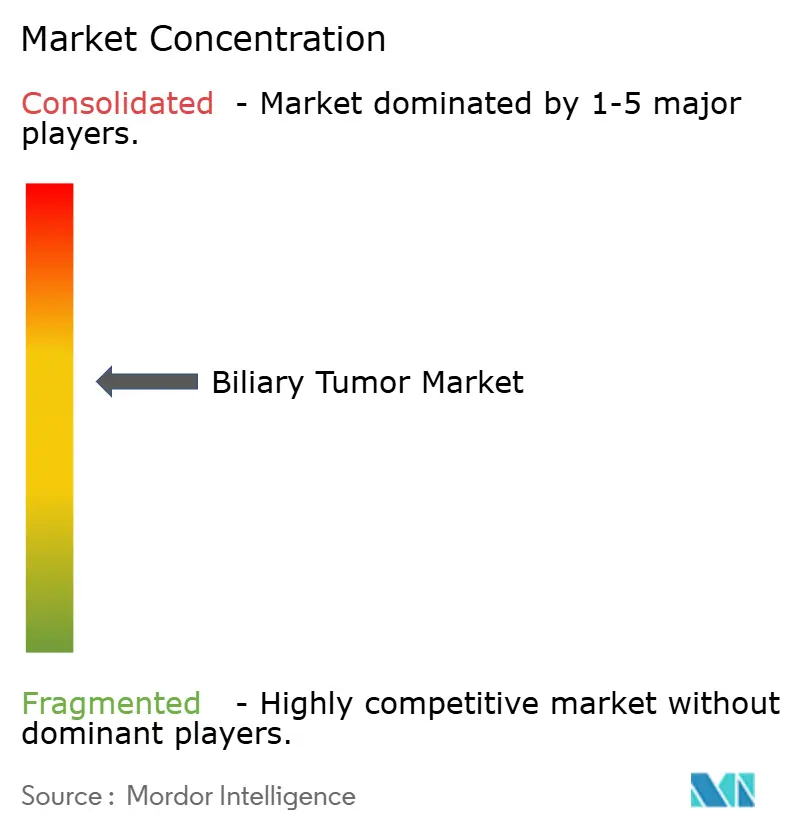

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biliary Tumor Market Analysis by Mordor Intelligence

The Biliary Tumor Market size is estimated at USD 0.85 billion in 2026, and is expected to reach USD 1.16 billion by 2031, at a CAGR of 6.40% during the forecast period (2026-2031).

The current growth trajectory masks a structural shift that began when durvalumab plus gemcitabine-cisplatin became the global first-line standard, quickly followed by pembrolizumab combinations and the HER2-directed antibody zanidatamab. Only patients whose tumors harbor FGFR2, IDH1, or HER2 alterations qualify for targeted agents, so the Biliary Tumor market is expanding in direct proportion to the penetration of biomarker testing. Hospitals remain the dominant treatment setting because they control infusion suites and interventional radiology capacity, yet diagnostic laboratories are capturing more value as comprehensive genomic profiling becomes mandatory for therapy selection. Regionally, North America still contributes the largest revenue pool, but incidence-driven volume growth in Asia Pacific is pushing the Biliary Tumor market toward a more balanced geographic mix.

Key Report Takeaways

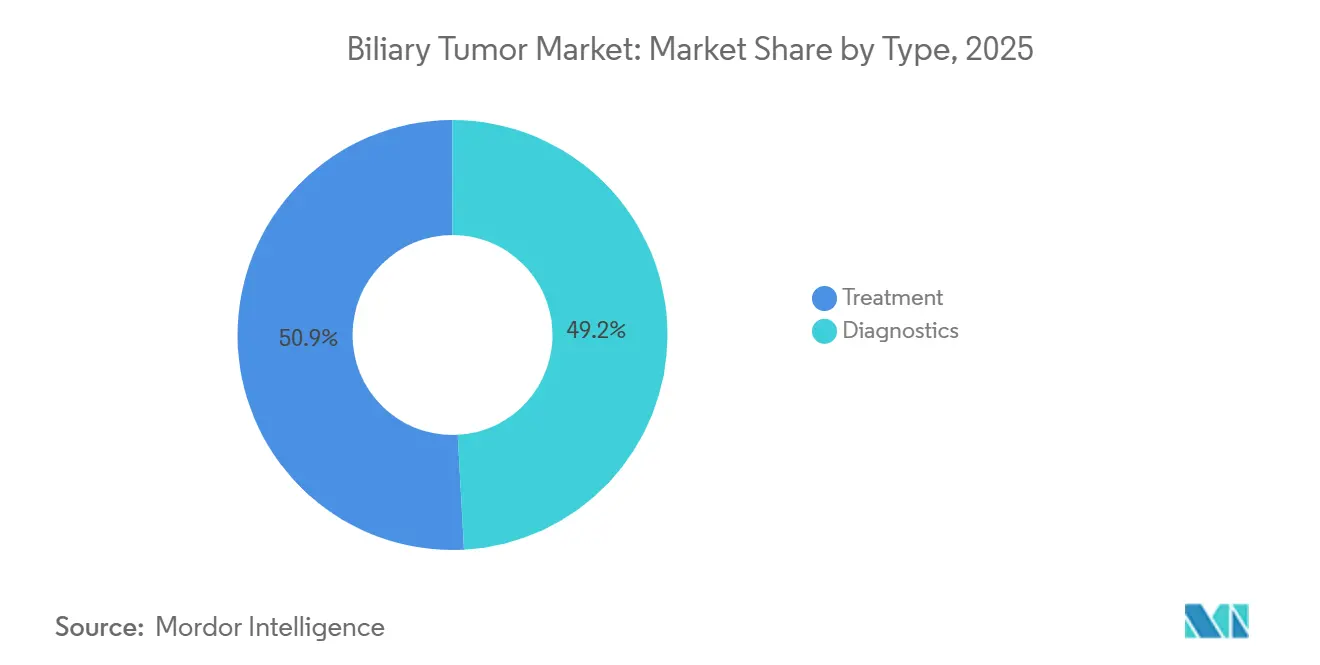

- By type, treatment accounted for 50.85% of revenue in 2025, whereas Diagnostics is advancing at a 7.30% CAGR through 2031.

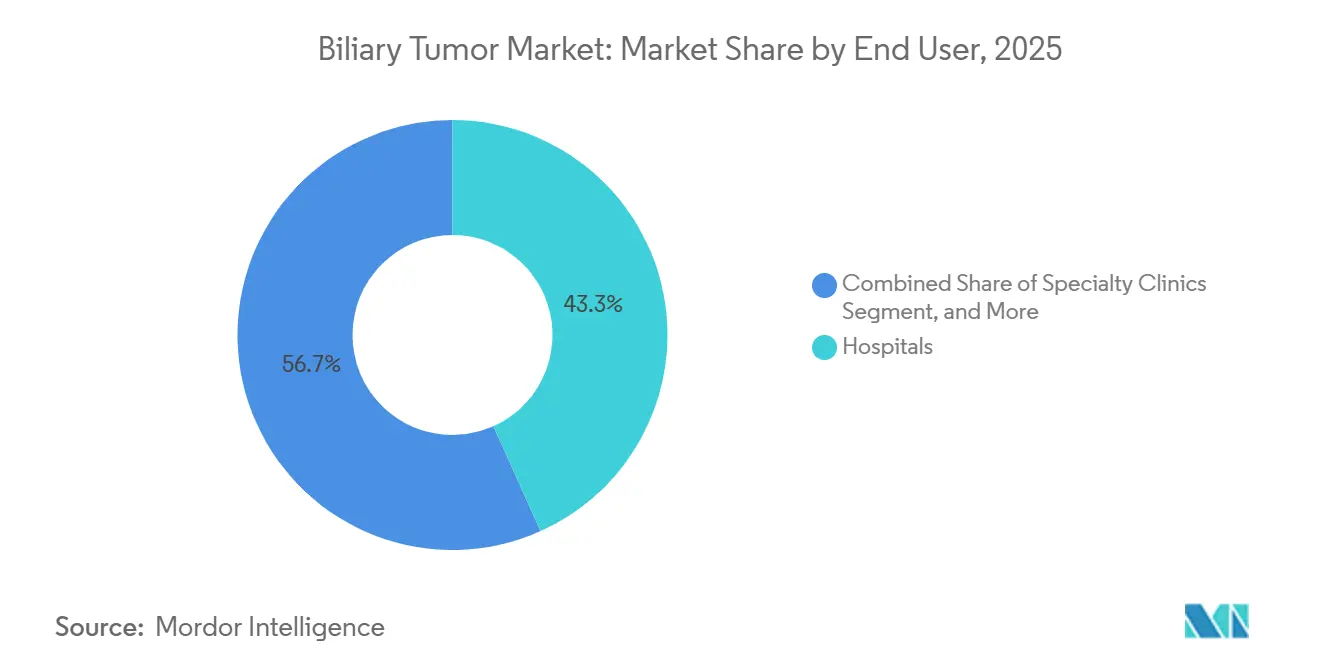

- By end user, hospitals accounted for 43.28% of the 2025 total, while Diagnostics Centers recorded the fastest CAGR of 6.90%.

- By geography, North America captured 44.25% share in 2025, but Asia Pacific is the most dynamic territory with an 8.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Biliary Tumor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| First-line shift to IO + gemcitabine/cisplatin as global standard of care | +1.2% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Expanding biomarker testing enabling FGFR2/IDH1/HER2 targeted uptake | +1.0% | North America, Europe, urban APAC hubs | Medium term (2-4 years) |

| HER2-positive segment unlocked by zanidatamab approval | +0.6% | North America, Europe, Japan | Medium term (2-4 years) |

| Rising incidence and awareness in high-burden APAC markets | +1.4% | Thailand, China, Japan, South Korea | Long term (≥ 4 years) |

| Liver-directed therapies gaining adoption for intrahepatic cholangiocarcinoma | +0.8% | North America, Europe, select APAC centers | Medium term (2-4 years) |

| Select-center transplant protocols expanding eligibility | +0.4% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

First-Line Shift to Immunotherapy Plus Gemcitabine-Cisplatin as Global Standard of Care

Durvalumab added to gemcitabine-cisplatin extended median overall survival to 12.8 months, compared with 11.5 months with chemotherapy alone, a result that secured global regulatory approvals and immediate guideline endorsements.[1]Dy Oh, “Durvalumab plus Gemcitabine and Cisplatin in Advanced Biliary Tract Cancer,” New England Journal of Medicine, nejm.org Uptake is brisk in the United States and Western Europe, where 60-70% of eligible patients now begin combination therapy, although Latin America and parts of Asia still face reimbursement delays. Pharmacy budgets are feeling pressure because durvalumab’s annual cost surpasses USD 150,000, dwarfing the generic backbone’s outlay. The October 2023 approval of pembrolizumab plus chemotherapy created a competing regimen and fragmented prescribing patterns. Health systems are therefore negotiating outcomes-based agreements to contain rising spend.

Expanding Biomarker Testing Enabling FGFR2, IDH1, and HER2 Targeted Uptake

Next-generation sequencing is now recommended for all advanced cases to detect FGFR2 fusions, IDH1 mutations, HER2 amplification, BRAF alterations, and mismatch-repair deficiency.[2]National Comprehensive Cancer Network, “Hepatobiliary Cancers, Version 1.2025,” nccn.org FGFR2-positive tumors respond to futibatinib, which delivered a 42% objective response rate in the FOENIX-CCA2 trial and gained accelerated approval in 2022. IDH1-mutant disease is treatable with ivosidenib, although clinical benefit is modest. Tissue-based panels still require roughly two weeks, driving interest in liquid biopsy assays that can return results in under a week, yet payer coverage for blood-based testing is inconsistent. Asia Pacific illustrates both promise and constraint: major urban hubs offer broad NGS access, but rural patients often remain untested and thus ineligible for precision therapy.

HER2-Positive Segment Unlocked by Zanidatamab Approval

Zanidatamab became the first HER2-directed drug approved for biliary tumors in November 2024, following a 41.3% response rate and a median overall survival of 12.5 months in the HERIZON-BTC-01 study. Roughly 15-20% of patients harbor HER2 amplification, creating a new addressable niche of several thousand cases annually in the United States alone. Companion diagnostics using immunohistochemistry and fluorescence in situ hybridization have become routine, though inter-lab variability in scoring is a recognized challenge. Jazz Pharmaceuticals acquired the originator of zanidatamab for USD 1.5 billion in 2024, underscoring big pharma's demand for differentiated rare-oncology assets.

Rising Incidence and Awareness in High-Burden APAC Markets

Cholangiocarcinoma incidence exceeds 85 per 100,000 in Northeast Thailand due to endemic liver-fluke infection, the highest rate worldwide. China is logging 3-5% yearly increases in urban intrahepatic cases, linked to hepatitis B and aflatoxin exposure, while Japan reports stable but elevated incidence reflecting better imaging. Public-health campaigns promoting cooked-fish consumption are lowering pediatric infection rates in Thailand, yet legacy adult cohorts will sustain high volumes through 2035. Screening pilots using ultrasound and CA19-9 testing are under way in Thai villages, but cost-effectiveness analyses remain inconclusive. Urban centers across Asia are adopting Western treatment algorithms, though rural–urban disparities in diagnostic turnaround and therapy initiation persist.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low prevalence of actionable biomarkers limits addressable pool | -0.9% | Global | Medium term (2-4 years) |

| Late diagnosis and poor ECOG reduce time on therapy | -1.1% | Global, acute in APAC rural regions | Short term (≤ 2 years) |

| High cost and reimbursement hurdles for immunotherapy and targeted agents | -0.7% | Latin America, MEA, parts of APAC | Medium term (2-4 years) |

| Limited interventional radiology capacity for Y-90 | -0.5% | Global, pronounced in MEA and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low Prevalence of Actionable Biomarkers Limits Addressable Pool

FGFR2 fusions appear in only 10-15% of intrahepatic cases and are rare elsewhere, while IDH1 mutations occur in 13-20% of tumors, leaving the majority without a druggable target. HER2 amplification offers another 15-20% niche, but not all HER2-positive patients respond because resistance mechanisms remain unclear. Intratumoral heterogeneity complicates therapy: metastatic sites may lack the FGFR2 fusion seen in the primary lesion, reducing systemic efficacy. Circulating-tumor-DNA assays track clonal evolution, yet their sensitivity in biliary tumors is only 60-70%. Pharmaceutical firms therefore weigh the commercial viability of drugs targeting alterations present in fewer than 1,000 U.S. patients per year.

Late Diagnosis and Poor ECOG Reduce Time on Therapy and Continuation Rates

Roughly two-thirds of patients present with unresectable or metastatic disease, and many already have an ECOG performance status of 2 or worse, limiting tolerance for intensive regimens.[3]Jorge Bridgewater, “Quality of Life in Advanced Biliary Cancer,” Journal of Gastrointestinal Oncology, jgo.amegroups.com In real-world settings, ECOG 2 patients discontinue treatment within 3-4 months, compared with 6-8 months in fitter cohorts. Up to half require biliary stent placement before systemic therapy can begin, and stent occlusion interrupts treatment in about 20-30% of cases. Rural Asia illustrates the problem: median ECOG at diagnosis in Northeast Thailand is 2–3, compared with 1–2 in Bangkok, reflecting delayed imaging access. The lack of effective population-level screening perpetuates late-stage presentation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Diagnostics Outpace Treatment Growth

Diagnostics achieved a 7.30% CAGR, topping Treatment’s growth and signaling the central role of biomarker discovery. Gemcitabine-cisplatin remains the backbone of care, but immunotherapy is the fastest-expanding sub-segment as new combinations shift first-line paradigms. Targeted therapy generates high revenue per patient, although its reach is constrained by the frequency of biomarkers. Locoregional interventions such as Y-90 radioembolization and SBRT are used for unresectable intrahepatic disease, with TheraSphere usage up 12% year over year.

Diagnostics revenues stem chiefly from next-generation sequencing panels that detect FGFR2 fusions, IDH1 mutations, and HER2 amplification. Liquid biopsy adoption is rising because blood-based testing trims turnaround to a single week, an advantage when tissue is scarce. Companion diagnostics for zanidatamab and futibatinib generate predictable recurring demand. These trends ensure that the Diagnostics slice of the biliary tumor market continues to outpace the broader biliary tumor market.

By End User: Diagnostics Centers Capture Decentralized Testing

Hospitals held 43.28% of 2025 value because they host infusion suites and interventional radiology services. Even so, specialized Diagnostics Centers are repeating a pattern seen in other solid tumors, posting a 6.90% CAGR thanks to economies of scale, automated workflows, and shorter assay cycles. Outpatient Y-90 radioembolization is migrating to ambulatory sites, reinforcing a gradual shift of complex procedures outside traditional inpatient walls.

Reference laboratories process thousands of panels monthly, lowering the unit price to USD 2,500-3,500 and shrinking results time to 7-10 days. Specialty Clinics linked to academic centers receive disproportionate shares of zanidatamab prescriptions because they offer access to clinical trials. Community oncologists increasingly outsource genomic testing, accelerating the diagnostics' entry into the biliary tumor market.

Geography Analysis

North America accounted for 44.25% of revenue in 2025, driven by rapid FDA approvals and broad payer coverage that deliver timely access to new immunotherapies and HER2-targeted agents. The United States alone accounts for 85% of regional spend, with incidence creeping upward due to non-alcoholic steatohepatitis and obesity. Canada joined the durvalumab cohort only at the end of 2024, while Mexico limits first-line immunotherapy to privately insured patients.

Asia Pacific is the fastest-expanding region, with an 8.48% CAGR. Thailand remains the global epicenter because of liver-fluke infection rates above 85 per 100,000, whereas China’s urban incidence surge is tied to hepatitis B and aflatoxin exposure. Japan’s supportive reimbursement and prompt PMDA approvals shorten therapy roll-outs, and South Korea’s NHIS added futibatinib in 2025, sharply improving access for FGFR2-positive patients.

EMA approvals are universal, but individual HTA bodies apply varying cost-effectiveness thresholds, leading to reimbursement delays. Germany, France, and the United Kingdom collectively shape regional uptake, yet Southern and Eastern nations lag. Middle East, Africa, and South America remain small slices of the biliary tumor market because diagnostic infrastructure is sparse and payer budgets are tight.

Competitive Landscape

Competition is moderate because systemic therapies and locoregional devices rarely overlap. AstraZeneca’s durvalumab and Merck’s pembrolizumab dominate immunotherapy revenue streams, whereas Incyte, Taiho, and Servier focus on FGFR2 and IDH1 inhibitors. Jazz Pharmaceuticals entered the field through the USD 1.5 billion acquisition of the developer of zanidatamab, illustrating continued asset consolidation.

Boston Scientific’s glass-based TheraSphere owns roughly 60% of the Y-90 market because outpatient administration reduces facility cost. Sirtex remains strong in Europe and Asia, supported by existing distributor ties. Diagnostic firms Foundation Medicine, Guardant Health, SYNLAB, and Sonic Healthcare are in a race to compress turnaround times and secure national payer contracts. Forward-looking programs pursue antibody-drug conjugates against HER2 and TROP2, KRAS G12C inhibitors, and artificial-intelligence tools that predict biomarker status directly from pathology images.

Biliary Tumor Industry Leaders

Becton, Dickinson and Company

AstraZeneca

Incyte Corporation

Johnson & Johnson

Merck & Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: FDA cleared zanidatamab-gkkz (Ziihera) for previously untreated HER2-positive biliary tract cancer, based on a 41.3% response and 12.5-month median overall survival.

- May 2024: Jazz Pharmaceuticals announced a USD 1.5 billion acquisition of zanidatamab’s originator to strengthen its precision-oncology portfolio.

- January 2024: NICE reversed its July 2023 ruling and endorsed durvalumab plus gemcitabine-cisplatin for first-line therapy after AstraZeneca submitted new cost-effectiveness data.

Global Biliary Tumor Market Report Scope

The Biliary Tumor Market is the global healthcare segment focused on the diagnosis, treatment, and management of malignant and benign tumors arising in the biliary tract, including cholangiocarcinomas (intrahepatic and extrahepatic), gallbladder cancers, and other rare biliary neoplasms. It encompasses pharmaceuticals, surgical interventions, radiation therapies, diagnostics, and supportive care solutions.

The Biliary Tumor Market Report is Segmented by Type (Treatment [Chemotherapy, Immunotherapy, Targeted Therapy, Locoregional Therapy], Diagnostics), End User (Hospitals, Specialty Clinics, Diagnostics Centers, Others), and Geography (North America, Europe, Asia Pacific, Middle East and Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

| Treatment | Chemotherapy (e.g., GemCis, GemOx, FOLFOX, capecitabine/5-FU) |

| Immunotherapy | |

| Targeted therapy | |

| Locoregional therapy | |

| Diagnostics |

| Hospitals |

| Specialty Clinics |

| Diagnostics Centers |

| Others (Ambulatory Surgical Centers, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Treatment | Chemotherapy (e.g., GemCis, GemOx, FOLFOX, capecitabine/5-FU) |

| Immunotherapy | ||

| Targeted therapy | ||

| Locoregional therapy | ||

| Diagnostics | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Diagnostics Centers | ||

| Others (Ambulatory Surgical Centers, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the size of the biliary tumor market in 2026?

The biliary tumor market size stood at USD 0.85 billion in 2026.

Which therapy type is growing fastest?

Immunotherapy combinations are the fastest-expanding treatment modality, driven by approvals for durvalumab and pembrolizumab.

What share did North America hold in 2025?

North America accounted for 44.25% of global revenue in 2025.

Why is diagnostics outpacing treatment growth?

Mandatory next-generation sequencing for FGFR2, IDH1, and HER2 markers is moving testing volumes to centralized labs and lifting diagnostic revenue above the overall market growth rate.

Which new drug opened the HER2-positive segment?

Zanidatamab, approved in November 2024, unlocked the HER2-positive niche.

Page last updated on: