Biliary Catheters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.23 Billion |

| Market Size (2031) | USD 4.59 Billion |

| Growth Rate (2026 - 2031) | 7.28% CAGR |

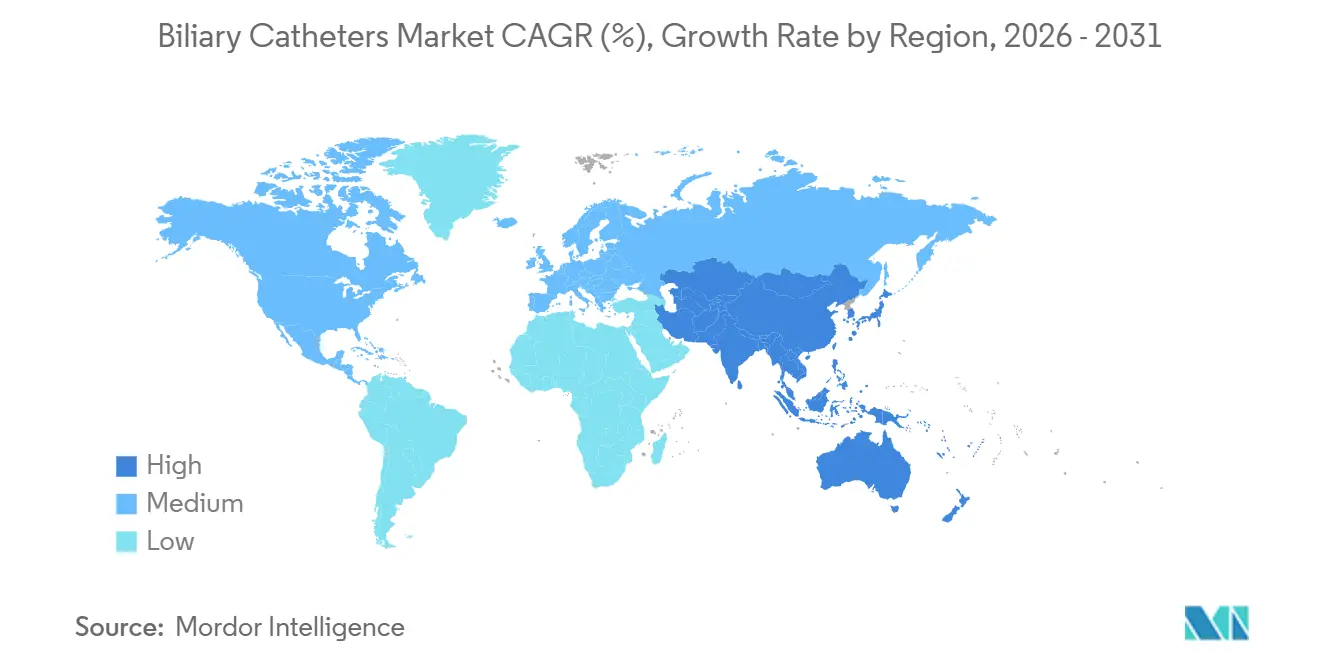

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

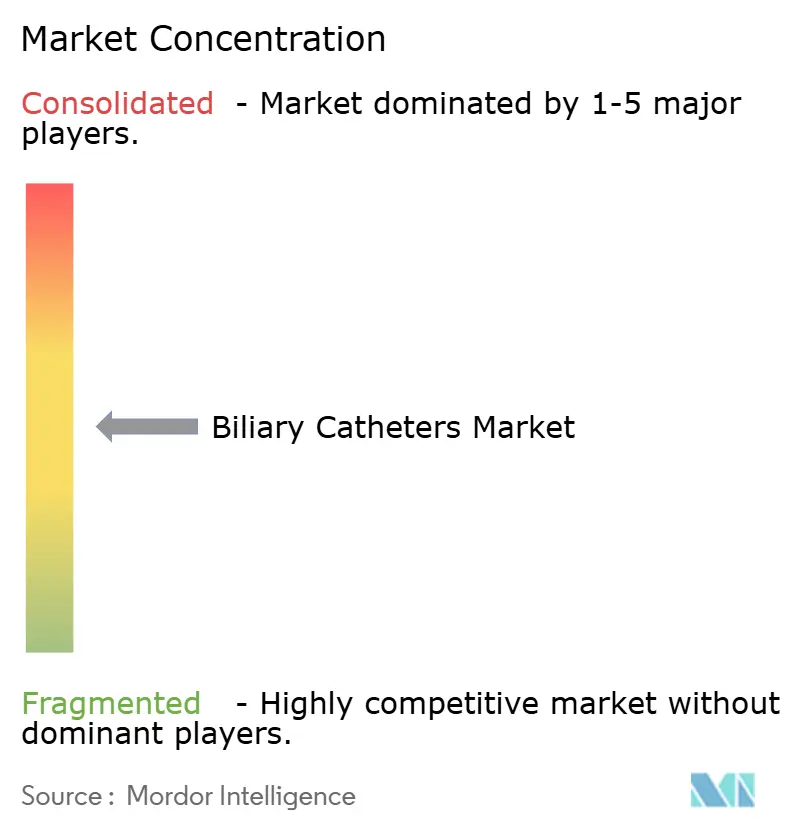

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biliary Catheters Market Analysis by Mordor Intelligence

The Biliary Catheters Market size is expected to grow from USD 3.01 billion in 2025 to USD 3.23 billion in 2026 and is forecast to reach USD 4.59 billion by 2031 at 7.28% CAGR over 2026-2031.

Growth in the biliary catheters market remains linked to the broader adoption of ERCP and PTBD, as both procedures are standard interventions for biliary obstruction across benign and malignant conditions. The transition from reusable to single-use duodenoscope platforms is reshaping demand, as hospitals require compatible accessories that support infection-control standards and established workflows. Purchasing consolidation across health systems favors suppliers with integrated portfolios covering access devices, cannulas, drainage tools, and stent-delivery support. Rising palliative drainage demand in oncology, outpatient migration of suitable GI procedures, and innovation in anti-fouling coatings, slim delivery systems, and EUS-guided access accessories continue to support market value growth despite pricing pressure.

Key Report Takeaways

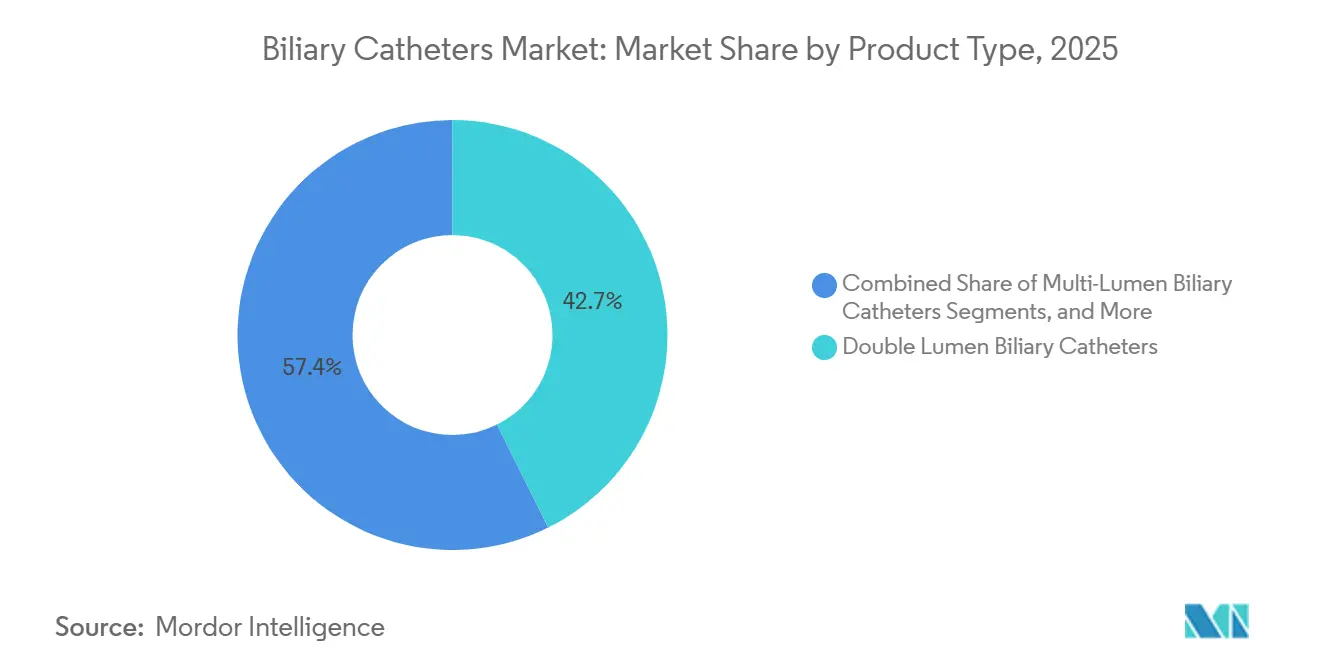

- By product type, double lumen biliary catheters led with 42.65% share in 2025, while single lumen biliary catheters are projected to grow at 8.93% CAGR through 2031.

- By material, Polyurethane held 43.45% share in 2025, while polyvinyl chloride recorded the fastest projected growth at 9.67% CAGR through 2031.

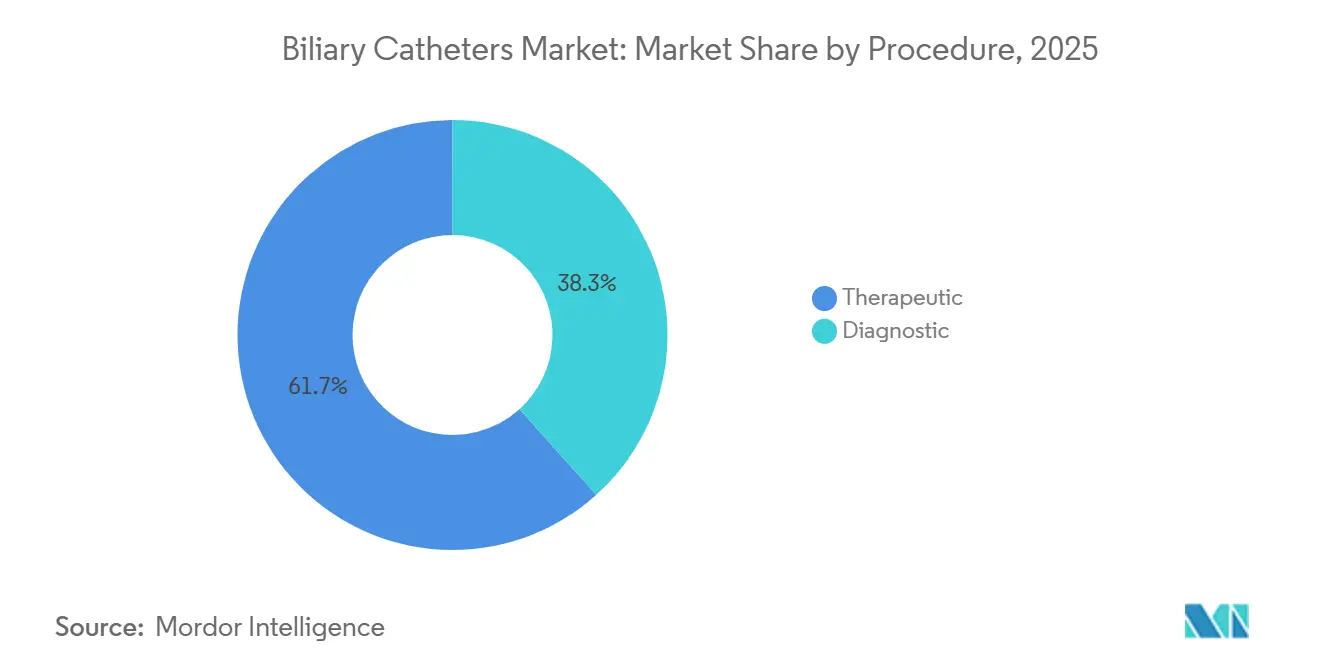

- By procedure, therapeutic procedures accounted for 61.66% of the biliary catheters market size in 2025, while diagnostic procedures are forecast to expand at 8.35% CAGR through 2031.

- By functionality, drainage captured 42.34% share in 2025, while stone removal is expected to advance at 9.78% CAGR through 2031.

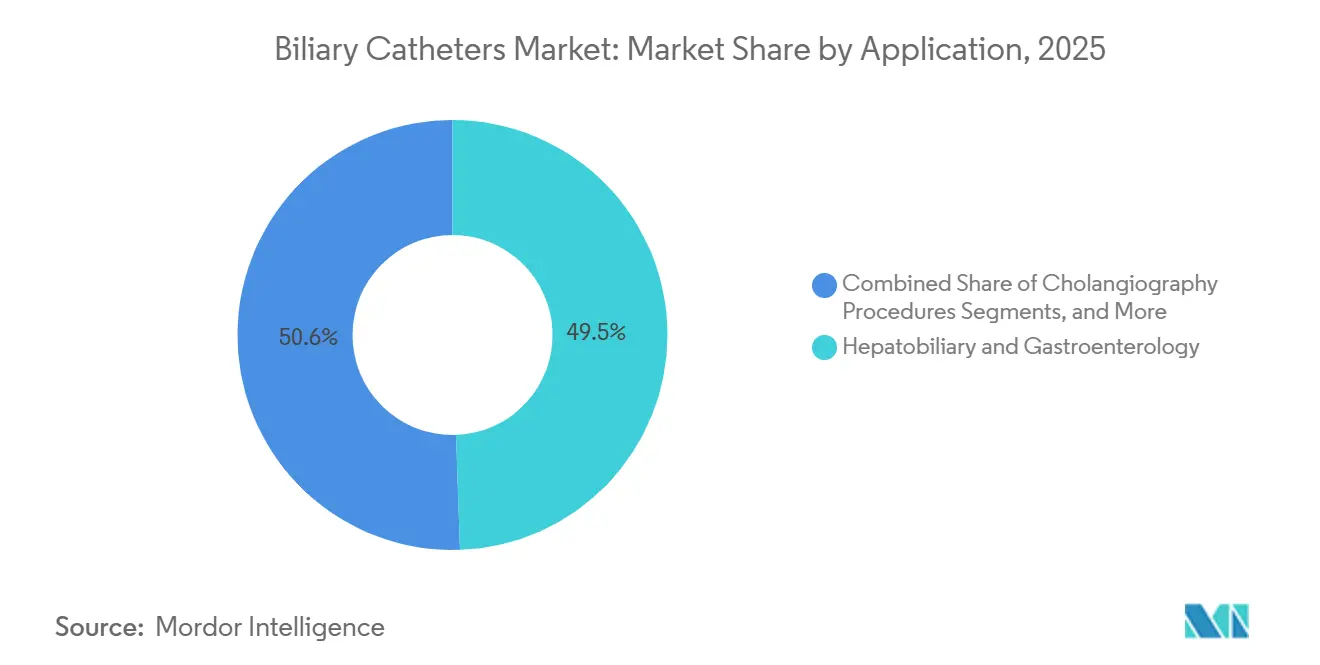

- By application, hepatobiliary and gastroenterology held 49.45% share in 2025, while oncology is projected to grow at 8.24% CAGR through 2031.

- By end user, hospitals represented 61.65% share in 2025, while ambulatory surgical centers are expected to rise at 9.22% CAGR through 2031.

- By geography, North America held 41.88% of the biliary catheters market share in 2025, while Asia-Pacific is projected to expand at 8.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Biliary Catheters Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising ERCP and PTBD procedure volumes | +2.0% | Global, concentrated in North America, Europe, and China | Medium term (2-4 years) |

| Rising need for minimally invasive biliary decompression | +1.5% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Wider adoption of hydrophilic and radiopaque catheter designs | +1.1% | North America and EU, with spillover to Asia-Pacific | Long term (≥ 4 years) |

| Higher biliary cancer and stricture workup rates | +1.0% | Asia-Pacific core, with spillover to North America | Long term (≥ 4 years) |

| Expansion of ambulatory and same-day interventional care | +0.8% | North America, with early gains in Germany, the United Kingdom, and Australia | Short term (≤ 2 years) |

| Device standardization in integrated health systems | +0.6% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising ERCP and PTBD Procedure Volumes

Rising ERCP and PTBD procedure volumes remain the clearest demand base for the biliary catheters market, as most obstruction pathways continue to rely on these two interventions across routine and complex care settings. ERCP supports stent placement, stone extraction, stricture dilation, and nasobiliary drainage, while PTBD adds demand when endoscopic access fails or hilar anatomy favors percutaneous drainage. MedPAC reported a 5.7% increase in ASC surgical procedures per FFS Medicare beneficiary in 2024, showing that GI and related interventions continue to shift to lower-cost outpatient settings.[1]Medicare Payment Advisory Commission, “March 2025 Report to the Congress, Chapter 10, Ambulatory Surgical Center Services Status Report,” MedPAC, medpac.gov As volumes expand across hospitals, day-care centers, and specialized outpatient facilities, the market benefits from a broader installed base that favors ready-to-use, workflow-friendly, and increasingly disposable catheter formats.

Rising Need for Minimally Invasive Biliary Decompression

The shift toward minimally invasive decompression is expanding the clinical relevance of the biliary catheters market, as surgery is no longer the preferred first-line option for many biliary obstruction cases. Endoscopic and percutaneous approaches reduce patient burden, shorten recovery, and align with care pathways that prioritize faster stabilization and fewer inpatient days. EUS-guided biliary drainage is also strengthening demand for slimmer delivery systems and specialized access tools. A 2025 Endoscopy paper described hepaticogastrostomy using a catheter-like delivery system that omitted the fistula dilation step, highlighting the business value of simpler access designs that shorten workflows and reduce exchange steps.

Wider Adoption of Hydrophilic and Radiopaque Catheter Designs

Hydrophilic coatings and radiopaque design elements are becoming standard purchasing requirements in the biliary catheters market, not optional upgrades for premium hospital accounts. Hospitals and procedural teams increasingly expect easier trackability, lower insertion resistance, and clearer fluoroscopic visibility in complex anatomies. A 2026 Bioactive Materials study reported that a lubricant-infused anti-fouling coating sharply reduced early neutrophil adhesion, preserved stent patency for more than six months in murine models, and prevented complete biliary occlusion seen in non-coated controls within two months.[2]“Endoscopic Ultrasonography-Guided Hepaticogastrostomy with Antegrade Stenting Using a Catheter-Like Delivery System: A Novel Technique Completely Omitting the Fistula Dilation Step,” Endoscopy, pmc.ncbi.nlm.nih.gov This supports higher-value positioning based on coating chemistry, visibility, and consistent performance rather than only lumen count or size.

Higher Biliary Cancer and Stricture Workup Rates

Higher cancer and stricture workup rates are creating durable demand for the biliary catheters market, as patients often require repeated drainage, imaging, exchange, and palliative support across multiple care episodes. A 2025 Chinese Medical Journal study reported 216,770 global biliary tract cancer cases in 2023, representing a 101.09% absolute increase from 1990 levels. IARC and WHO reported in 2026 that liver cancer accounted for 7.5% of all global cancer deaths, or nearly 735,000 fatalities annually.[3]Disease Burden of Biliary Tract Cancer in 204 Countries and Territories, 1990-2021: A Comprehensive Demographic Analysis of the Global Burden of Disease Study 2021,” Chinese Medical Journal, journals.lww.com This disease burden sustains demand across palliative drainage, malignant stricture management, and imaging-led workup, especially in East and Southeast Asia, where PTBD remains important alongside ERCP.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Reprocessing and infection-control burden for reusable ancillary equipment | -0.8% | Global, acute in North America and EU | Short term (≤ 2 years) |

| Procedure-specific reimbursement pressure in cost-managed settings | -0.6% | North America, with spillover to Western Europe | Medium term (2-4 years) |

| Complication risk from cannulation, migration, and occlusion events | -0.7% | Global, acute in North America and EU | Short term (≤ 2 years) |

| Narrow differentiation in core catheter designs and price compression | -0.6% | North America, with spillover to Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Reprocessing and Infection-Control Burden for Reusable Ancillary Equipment

Infection-control requirements continue to restrain the biliary catheters market, as reusable ancillary equipment increases costs, documentation needs, and operational pressure for endoscopy programs. Infection events linked to duodenoscope use have led hospitals and regulators to strengthen reprocessing standards and oversight of contaminated-device risk. Boston Scientific noted the broader impact of these changes in its 2025 Form 10-K, linking demand for single-use platforms and related accessories to hospital efforts to manage contamination risk and improve workflow control.

In the near term, higher compliance spending may delay upgrades to premium catheter systems, especially in facilities with moderate procedure volumes compared to large tertiary centers. Smaller hospitals and emerging-market providers face greater pressure because they have less capacity to absorb sterilization burdens and device premium costs at the same time. As a result, the market benefits from the long-term shift toward disposables but continues to face short-term budget constraints as providers balance infection-control needs with procedure budgets.

Procedure-Specific Reimbursement Pressure in Cost-Managed Settings

Reimbursement pressure limits growth potential in the biliary catheters market because device costs do not always translate directly into procedure payments, particularly under strict cost-managed contracts. In these settings, procurement teams often select the lowest-cost catheter that meets clinical expectations, limiting premium pricing unless a product clearly improves workflow, reduces exchanges, or supports higher-acuity cases. This pressure is most evident in the ERCP segment, where case volumes remain high, but per-procedure device allocations stay tightly managed.

MedPAC’s 2025 report showed continued ASC volume expansion, supporting procedure growth while highlighting a payment environment where operational efficiency is as important as product performance. Providers may continue increasing volumes while resisting broad premium-device adoption across standard cases. Consequently, innovation can succeed in the biliary catheters market only when it aligns with reimbursement logic and demonstrates value within tightly controlled procedural budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Double Lumen Dominates, Single Lumen Accelerates

Double lumen biliary catheters accounted for 42.65% of the biliary catheters market share in 2025, maintaining the leading product position as they support drainage and contrast delivery in a single device session. Their adoption remains strong in hospital ERCP suites, where physicians often move from visualization to therapy without a device change. Hospitals continue to prefer these products because they reduce exchanges, save time, and support predictable workflows in high-acuity settings.

Single lumen biliary catheters are projected to grow at a CAGR of 8.93% through 2031, supported by simpler diagnostic use, lower-cost configurations, and alignment with outpatient standardization goals. Their growth also reflects the shift toward single-use accessory ecosystems that reduce contamination risks and simplify inventory planning. Olympus Medical Systems received FDA 510(k) clearance in May 2025 for the Single Use Cannula V, K250573, supporting the broader move toward single-use ERCP accessory sets in regulated markets. Multi-lumen biliary catheters remain specialized for complex hilar obstruction cases that require multi-drain planning and command higher average selling prices.

By Material: Polyurethane Anchors Volume, PVC Posts Fastest Growth

Polyurethane acccounted 43.45% of the 2025 material segment, keeping it central to the biliary catheters market because it balances flexibility, kink resistance, and handling control in difficult anatomy. Hospitals rely on polyurethane for cases that require dimensional stability during guidewire support, fluoroscopic navigation, and manipulation through tortuous biliary pathways. Its clinical familiarity supports purchasing preference in tertiary care environments where reliability is a key procurement factor.

Polyvinyl chloride is the fastest-growing material segment, with a projected CAGR of 9.67% through 2031, supported by lower cost and suitability for disposable device formats preferred by outpatient centers. The biliary catheters industry continues to monitor formulation changes, as DEHP-related concerns and regulatory scrutiny could affect PVC’s compliance and cost position. Surface engineering may narrow material performance differences, while silicone continues to serve a smaller niche in longer-dwell percutaneous drainage where sustained biocompatibility is important.

By Procedure: Therapeutic Volume Leads, Diagnostic Broadens Its Base

Therapeutic procedures held 61.66% of the biliary catheters market size in 2025, as drainage, stone extraction, stent placement, and stricture dilation generate the highest device use. These procedures often require multiple device passes, more accessory combinations, and higher clinical urgency than diagnostic work. As a result, therapeutic procedures continue to deliver a larger revenue contribution within the biliary catheters market.

Diagnostic procedures are projected to expand at a CAGR of 8.35% through 2031, driven by broader use of cholangiography and related assessment tools in surveillance, early malignancy workup, and post-surgical follow-up. The boundary between diagnostic and therapeutic procedures is narrowing as clinicians increasingly move from evaluation to intervention in one session. A 2025 pilot study in Digestive Diseases and Sciences described a non-slip banded balloon catheter for common bile duct stone extraction used with minimal endoscopic sphincterotomy plus papillary balloon dilation, supporting the feasibility of combined procedural pathways.

By Functionality: Drainage Leads Volume, Stone Removal Posts Highest CAGR

Drainage accounded 42.34% of the 2025 functional segment, keeping it central to the biliary catheters market because decompression remains the first clinical priority in benign and malignant obstruction. External and internal-external drainage configurations support long-dwell palliative use when standard endoscopic pathways fail or durable decompression becomes the main objective. Drainage demand remains broad across oncology, post-surgical complications, and inflammatory obstruction.

Stone removal is projected to grow at a CAGR of 9.78% through 2031, making it the fastest-rising functionality as choledocholithiasis remains common in older populations and single-use retrieval balloons gain regulatory traction. Zhejiang Soudon Medical Technology received FDA 510(k) clearance in May 2026 for a Disposable Stone Retrieval Balloon Catheter, K253013, and Zhejiang Chuangxiang Medical Technology received clearance in March 2026 for Single Use Stone Retrieval Balloons, K253132. These approvals can increase recurring unit consumption as single-use balloons replace formats constrained by reprocessing cycles and reuse protocols.

By Application: Hepatobiliary & GI Core, Oncology Grows Fastest

Hepatobiliary and gastroenterology captured 49.45% of the 2025 application segment, keeping them the main demand center for the biliary catheters market across ERCP and PTBD use. Cholangiography procedures remain the second-largest application area, and together, these two uses show that demand remains anchored in core obstruction workup and intervention. Established reimbursement pathways and expertise in high-volume centers support stability in these mainstream application areas.

Oncology is projected to expand at a CAGR of 8.24% through 2031, as malignant obstruction becomes a stronger long-term growth driver for the biliary catheters market. IARC and WHO reported that liver cancer accounted for 7.5% of all global cancer deaths in 2024 estimates, or nearly 735,000 deaths each year. A 2025 multicenter prospective observational study in Digestive Diseases and Sciences showed the feasibility of using an ultra-thin delivery sheath for uncovered self-expanding metallic stents in unresectable malignant hilar biliary obstruction, indicating demand for thinner-profile palliative delivery systems.

By End User: Hospitals Dominant, ASCs Post Fastest Expansion

Hospitals accounted for 61.65% of the 2025 end-user segment, reflecting the concentration of high-acuity procedures in tertiary and quaternary settings across the biliary catheters market. Complex hilar obstruction management, EUS-guided drainage, advanced stone extraction, and post-surgical stricture repair depend on specialist teams, imaging support, and inpatient backup that hospitals provide more consistently than smaller outpatient facilities. This concentration supports hospital leadership and demand for premium catheter formats.

Ambulatory surgical centers are projected to grow at a CAGR of 9.22% through 2031, making them the fastest-growing end-user channel in the biliary catheters market. Continued outpatient volume growth supports this shift, and MedPAC confirmed a 5.7% rise in ASC surgical procedures per FFS Medicare beneficiary in 2023, with GI services contributing to that expansion. This migration favors simpler, standardized, and disposable product choices because outpatient centers prioritize efficiency, lower setup burden, and predictable case turnover.

Geography Analysis

North America held 41.88% of the biliary catheters market share in 2025, maintaining its position as the largest regional contributor. Mature reimbursement structures, strong procedural infrastructure, and a broad installed base support faster adoption of single-use and premium accessory formats. Infection-control policies continue to drive recurring demand as disposable scopes and accessories gain adoption. Boston Scientific reported USD 2.916 billion in Endoscopy segment net sales in 2025, with 7.7% organic growth, supported by its WallFlex Biliary RX Stent Systems, SpyGlass DS II platform, and EXALT Model D single-use duodenoscope.

Europe remains the second-largest geography in the biliary catheters market, with Germany, France, the United Kingdom, and Italy serving as major procedural anchors. Tighter regulatory oversight and clinical evidence requirements favor manufacturers with strong post-market surveillance and documentation capabilities. The expansion of interventional endoscopy across Southern and Central Europe is also broadening the addressable procedural base. Medi-Globe GmbH received FDA 510(k) clearance in April 2026 for the Endoflux Biliary & Pancreatic Stent Sets, K251658, after a 321-day extended review, highlighting its focus on regulated market expansion.

Asia-Pacific is the fastest-growing region in the biliary catheters market, with a projected CAGR of 8.56% through 2031, supported by rising age-related stone burden, higher oncology-linked biliary demand, and expanding interventional capacity. The 2024 Chinese Medical Journal study showed continued long-term growth in biliary tract cancer burden, supporting sustained procedural demand. China and India remain key growth engines as infrastructure investment expands access to advanced biliary interventions, while South Korea is gaining visibility through FDA 510(k) clearances for Taewoong Medical’s Niti-S Biliary Stent, K251123, in December 2025 and S&G Biotech’s EGIS Biliary Double Bare Stent, K242845, in 2025. The Middle East and Africa and South America remain smaller but emerging parts of the market, supported by infrastructure expansion and private healthcare investment despite current constraints in specialist access and fluoroscopy-equipped facilities.

Competitive Landscape

The biliary catheters market is moderately consolidated, with Boston Scientific, Cook Medical, and Olympus forming the most visible ERCP-centered leadership group across major regulated markets. The competitive landscape also includes Medtronic, Teleflex, Merit Medical, AngioDynamics, B. Braun Melsungen, Micro-Tech, Taewoong Medical, Zhejiang Soudon, and other regional manufacturers, which prevents tight control by a limited group of players. Pricing pressure remains highest in standard access and commodity-like catheter formats, while differentiation is stronger in stone retrieval, drainage performance, coating science, visualization-linked platforms, and advanced delivery systems.

Companies in the biliary catheters market are increasingly building full procedural ecosystems rather than offering stand-alone products. Boston Scientific has positioned its EXALT Model D single-use duodenoscope within a broader biliary access and visualization portfolio that includes WallFlex and SpyGlass DS II, strengthening procedural alignment and reducing mixed-vendor use during ERCP workflows. Medtronic also expanded its platform strategy through its 2025 distribution agreement with Dragonfly Endoscopy, increasing its reach in pancreaticobiliary visualization and procedural support.

Innovation in the biliary catheters market is focused on anti-fouling performance, thinner-profile access systems, and digitally assisted intervention. Research published in Surgical Endoscopy in 2026 described augmented reality-assisted cholangioscopy using Apple Vision Pro with the SpyGlass DS system, reporting technical success in 4 of 4 complex cases and no complications. Taewoong Medical’s push into slim-delivery EUS-related systems and the growing number of Chinese FDA clearances show that Asian manufacturers are competing on both price and relevance to newer procedure styles.

Biliary Catheters Industry Leaders

Boston Scientific Corporation

Cook Medical Incorporated

Medtronic plc

B. Braun SE

Teleflex Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Zhejiang Soudon Medical Technology received FDA 510(k) clearance K253013 for its Disposable Stone Retrieval Balloon Catheter under product code GCA after a 231-day extended review.

- April 2026: Micro-Tech (Nanjing) Co., Ltd. received FDA 510(k) clearance K253832 for its Dilation Balloon Catheter under biliary product code FGE.

- April 2026: Medi-Globe GmbH received FDA 510(k) clearance K251658 for the Endoflux Biliary & Pancreatic Stent Sets after a 321-day extended review.

- December 2025: Taewoong Medical Co., Ltd. received FDA 510(k) clearance K251123 for the Niti-S Biliary Stent after a 262-day extended review, supporting its expansion into advanced biliary access and EUS-related procedures.

Global Biliary Catheters Market Report Scope

As per the scope of the report, a biliary catheter is a thin, flexible tube used to restore the flow of bile from the liver or gallbladder. It is inserted when the normal drainage pathway is blocked by conditions like tumors, gallstones, or strictures, which prevents painful symptoms like jaundice and infections.

The biliary catheters market is segmented by product type, material, procedure, functionality, application, end user, and geography. By product type, the market includes single-lumen biliary catheters, double-lumen biliary catheters, and multi-lumen biliary catheters. By material, the market is segmented into polyurethane, polyvinyl chloride, and silicone. By procedure, the market is categorized into diagnostic and therapeutic. By functionality, the market is segmented into drainage, stent placement, and stone removal. By application, the market includes cholangiography procedures, hepatobiliary and gastroenterology, and oncology. By end user, the market is segmented into hospitals, ambulatory surgical centers, and specialized clinics. By geography, the market is analyzed across major regions globally. The report also covers the estimated market sizes and trends for countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Single Lumen Biliary Catheters |

| Double Lumen Biliary Catheters |

| Multi-Lumen Biliary Catheters |

| Polyurethane |

| Polyvinyl Chloride |

| Silicone |

| Diagnostic |

| Therapeutic |

| Drainage |

| Stent Placement |

| Stone Removal |

| Cholangiography Procedures |

| Hepatobiliary and Gastroenterology |

| Oncology |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialized Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Single Lumen Biliary Catheters | |

| Double Lumen Biliary Catheters | ||

| Multi-Lumen Biliary Catheters | ||

| By Material | Polyurethane | |

| Polyvinyl Chloride | ||

| Silicone | ||

| By Procedure | Diagnostic | |

| Therapeutic | ||

| By Functionality | Drainage | |

| Stent Placement | ||

| Stone Removal | ||

| By Application | Cholangiography Procedures | |

| Hepatobiliary and Gastroenterology | ||

| Oncology | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialized Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the biliary catheters market in 2026?

The biliary catheters market stands at USD 3.23 billion in 2026 and is forecast to reach USD 4.59 billion by 2031 at a 7.28% CAGR.

Which product type leads biliary catheter demand?

Double Lumen Biliary Catheters led in 2025 with 42.65% share because they support both drainage and contrast delivery during the same procedure.

Which functionality is growing the fastest in biliary care devices?

Stone Removal is the fastest-growing functionality, with a projected 9.78% CAGR through 2031, supported by rising stone burden and growing adoption of single-use retrieval balloons.

Why is oncology becoming more important for biliary catheter use?

Oncology is projected to grow at 8.24% CAGR through 2031 because malignant obstruction often requires repeated drainage, stent support, and palliative intervention.

Which end-user setting is expanding the quickest for biliary procedures?

Ambulatory Surgical Centers are the fastest-growing end-user segment, advancing at 9.22% CAGR through 2031 as more GI procedures move into lower-cost outpatient settings.

Which region offers the strongest growth outlook through 2031?

Asia-Pacific is the fastest-growing regional segment, with an expected 8.56% CAGR, supported by rising disease burden, aging populations, and expanding interventional care capacity.

Page last updated on: