Big Data In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 79.86 Billion |

| Market Size (2031) | USD 193.49 Billion |

| Growth Rate (2026 - 2031) | 19.35% CAGR |

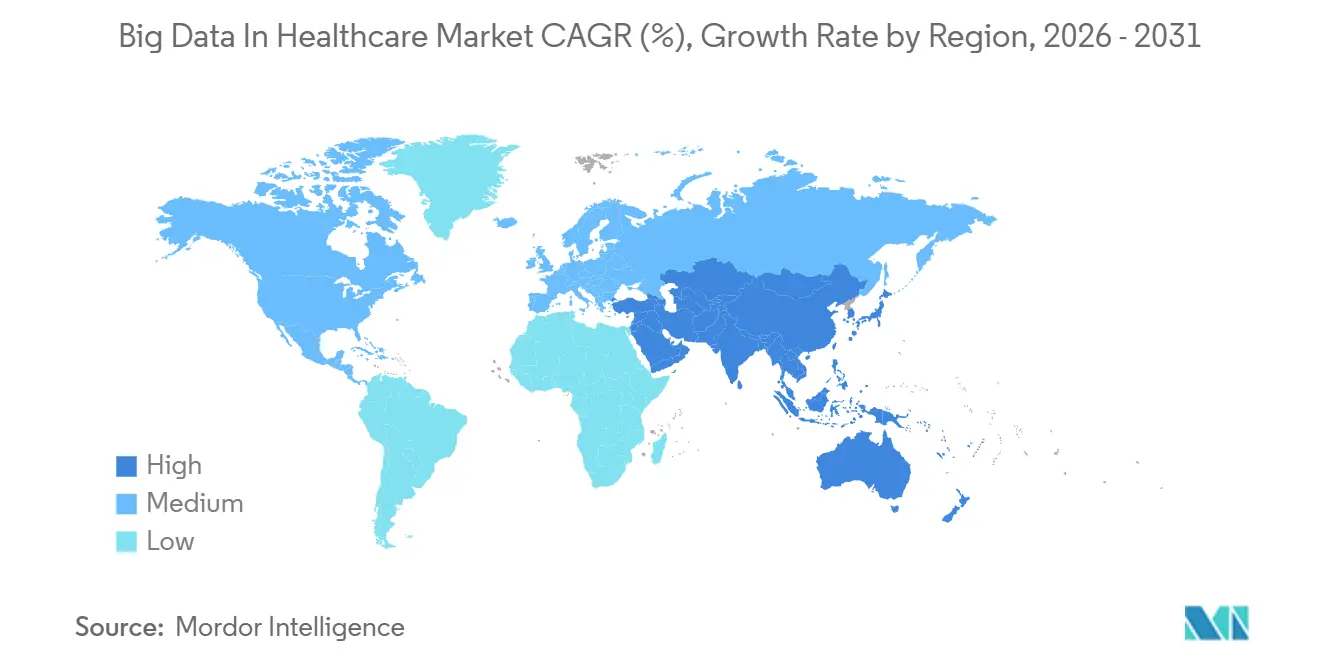

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

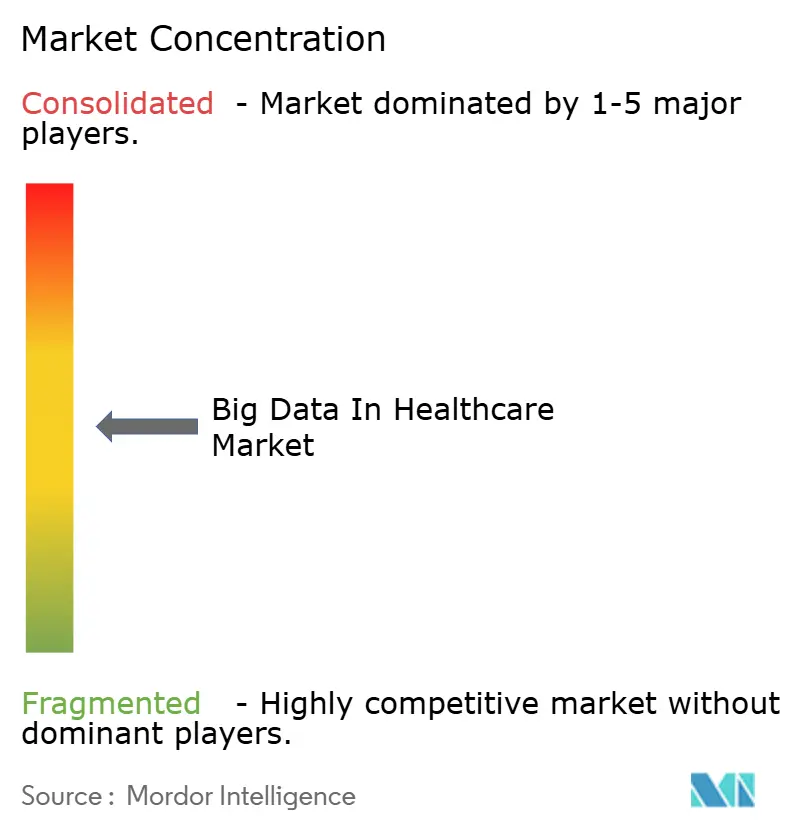

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Big Data In Healthcare Market Analysis by Mordor Intelligence

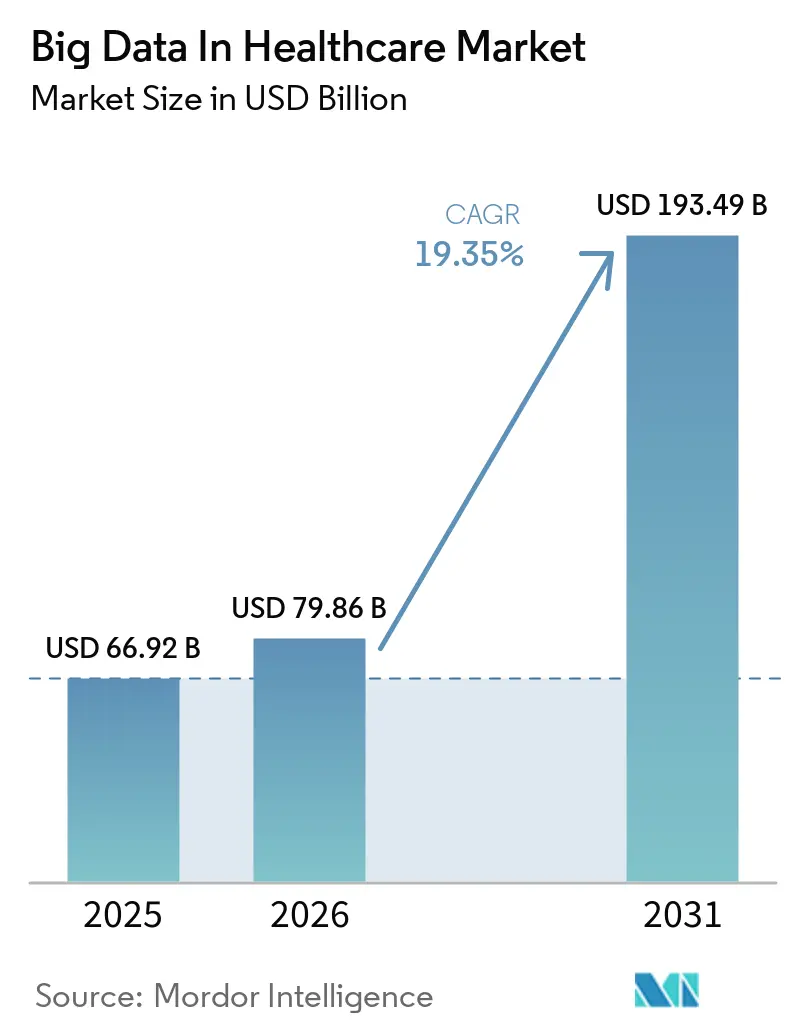

The Big Data In Healthcare Market size is projected to expand from USD 66.92 billion in 2025 and USD 79.86 billion in 2026 to USD 193.49 billion by 2031, registering a CAGR of 19.35% between 2026 to 2031.

Growth is propelled by providers’ move toward data-driven care delivery, the rise of real-time analytics, and policy initiatives that favor interoperable data exchange. Value-based care agreements are accelerating demand for advanced analytics that prove measurable outcomes to payers, while the European Health Data Space shows how regulation can unlock secondary data use across an entire region. Multi-omics integration is pushing precision medicine into everyday practice, with AI models now processing genomic and clinical data from 57 million National Health Service patient records. North America leads adoption thanks to FHIR-based interoperability infrastructure, yet Asia-Pacific is growing fastest as large public–private digitization programs scale across China and India. Services dominate spending because most healthcare organizations lack internal expertise for complex deployments, and cloud migration outpaces on-premise upgrades as AI workloads intensify.

Key Report Takeaways

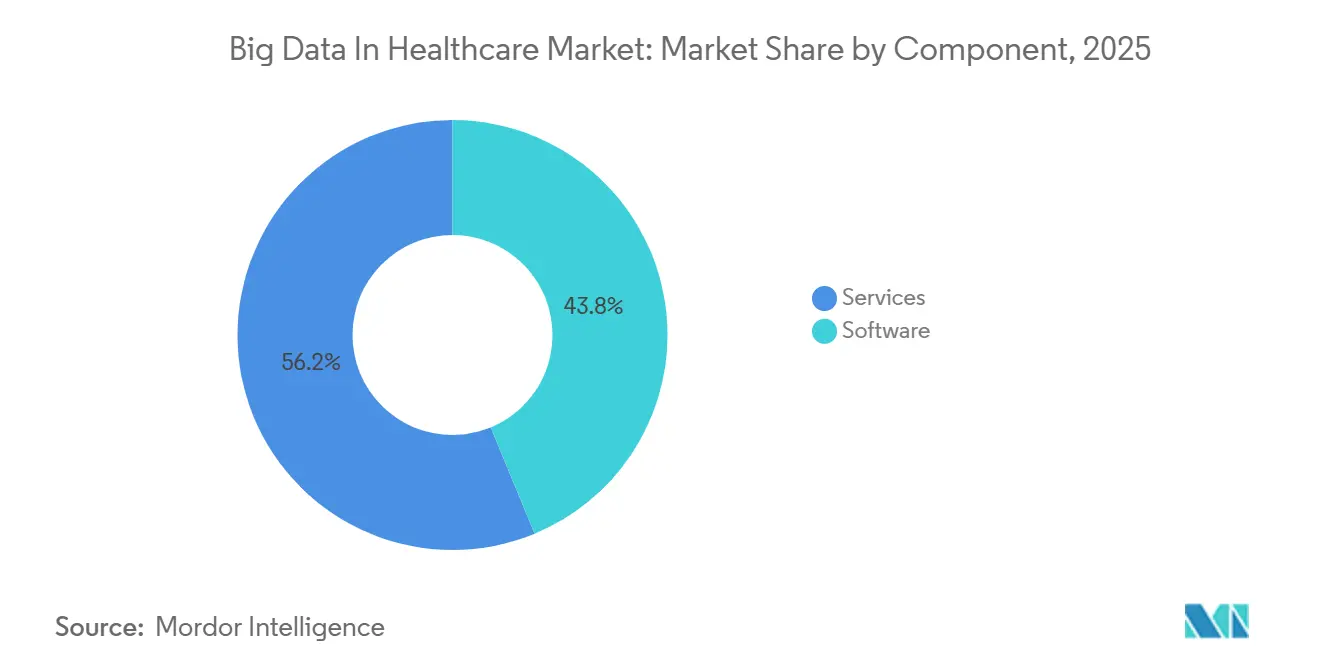

- By component, services held 56.25% of big data in healthcare market share in 2025 and are advancing at a 21.45% CAGR through 2031.

- By deployment, on-premise accounted for 60.95% share of the big data in healthcare market size in 2025, while cloud is projected to expand at 23.95% CAGR to 2031.

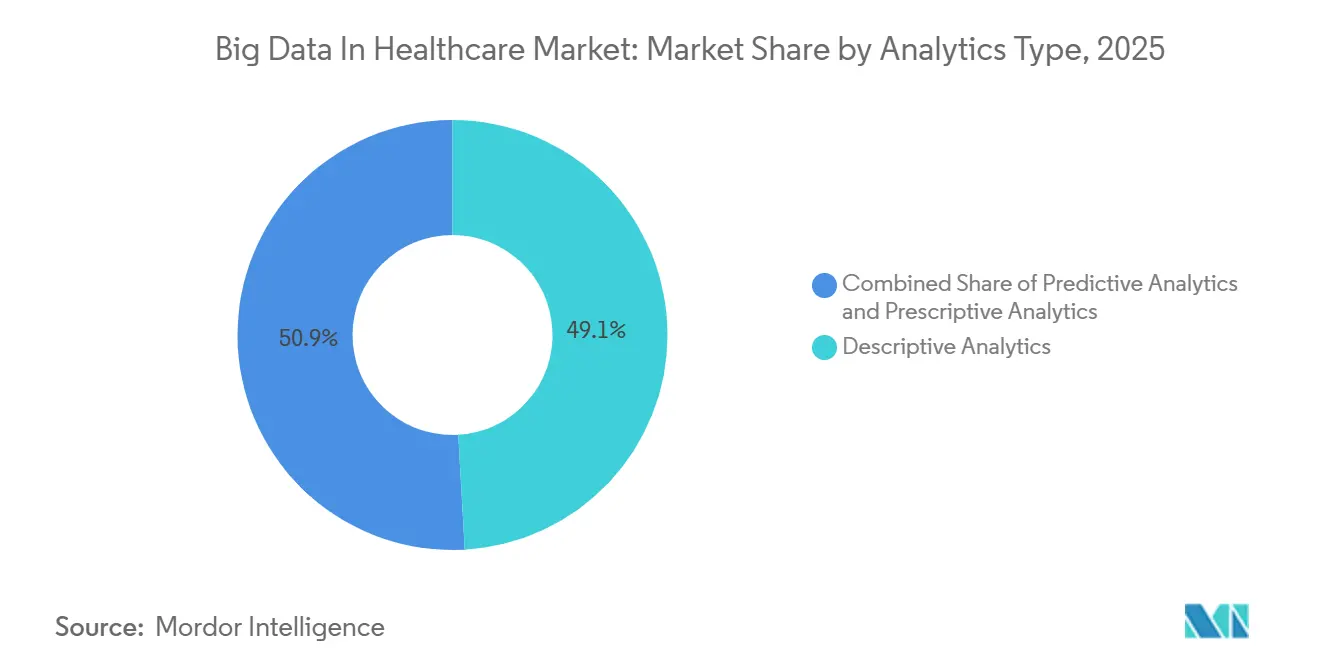

- By analytics type, descriptive analytics led with 49.10% revenue share in 2025; prescriptive analytics is forecast to grow at 25.10% CAGR to 2031.

- By application, financial analytics commanded 29.20% of big data in healthcare market share in 2025, whereas population health analytics is set to climb at 20.85% CAGR by 2031.

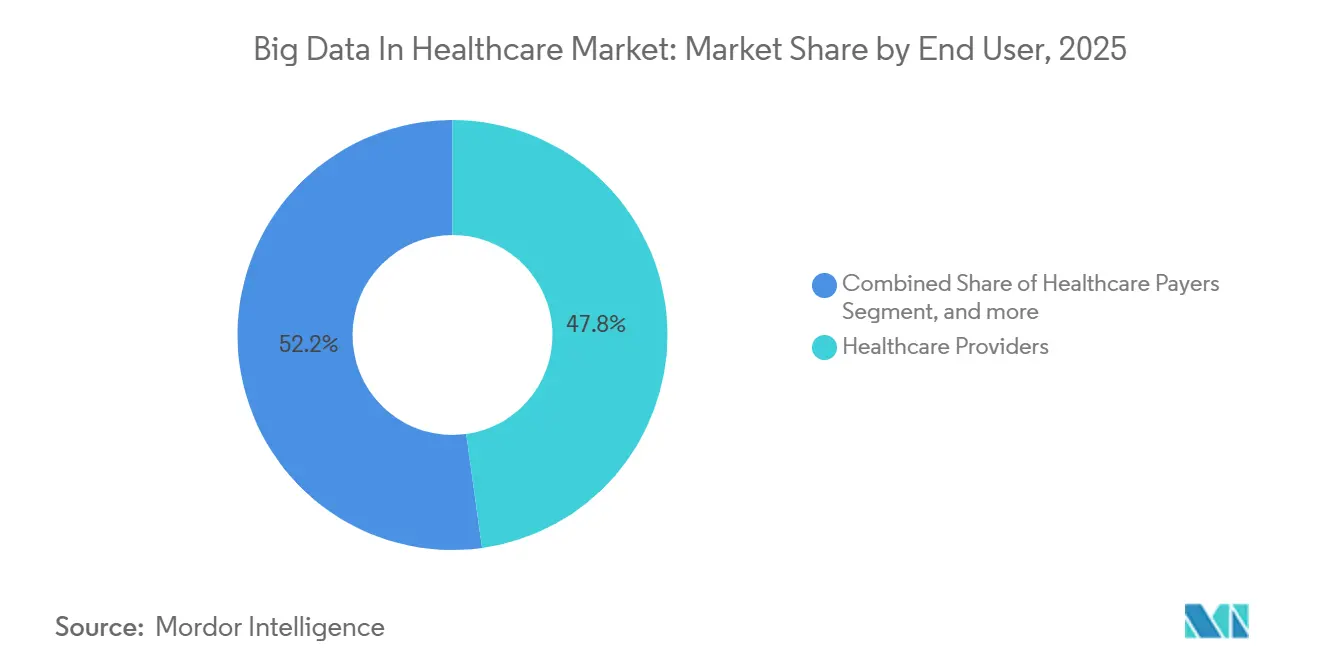

- By end user, healthcare providers controlled 47.80% of the big data in healthcare market in 2025; pharma and biotechnology companies lead growth with a 21.05% CAGR through 2031.

- By geography, North America commanded 45.10% share in 2025; Asia-Pacific is growing fastest at a 20.10% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Big Data In Healthcare Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increase in demand for analytics solutions for population health management | +4.2% | Global, early adoption in North America and EU | Medium term (2-4 years) |

| Rising need for business intelligence to optimise health administration and strategy | +3.8% | Global, mature healthcare markets | Short term (≤ 2 years) |

| Mandates for value-based care reimbursement | +3.1% | Primarily North America, secondary EU | Medium term (2-4 years) |

| Expanding adoption of real-time remote-patient-monitoring data streams | +2.9% | Global, accelerated in Asia-Pacific and Middle East & Africa | Short term (≤ 2 years) |

| Integration of multi-omics datasets into clinical decision support | +2.4% | North America and EU core, Asia-Pacific emerging | Long term (≥ 4 years) |

| Emergence of hospital-at-home models generating rich home-based data | +2.1% | North America and EU primary, selective Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increase in Demand for Analytics Solutions for Population Health Management

Population health strategies increasingly combine social determinants with clinical data to predict risk and allocate resources. Providers deploying advanced analytics have lowered readmission rates and demonstrated material cost savings, aligning with the Centers for Medicare & Medicaid Services' target that all fee-for-service beneficiaries join value-based arrangements by 2030[1]Centers for Medicare & Medicaid Services, “Innovation Center Strategy Refresh,” cms.gov. Real-world evidence platforms merge claims, electronic health records, and genomic profiles to create individualized risk scores that guide early interventions. Uptake is widespread across integrated delivery networks in the United States, while European payers use similar tools to meet EHDS objectives.

Rising Need for Business Intelligence to Optimise Health Administration & Strategy

Hospitals face tight margins and growing administrative complexity. Modern business intelligence suites integrate revenue-cycle metrics with operational and clinical indicators to highlight performance gaps in real time. AI-based denial management modules automate claim edits and have shortened average payment windows for large US systems, freeing cash for patient care investments[2]Guidehouse, “AI-enabled revenue cycle performance,” guidehouse.com. Rolling forecasts and scenario modeling help executives navigate shifting reimbursement rates, workforce constraints, and supply chain disruptions. Multi-facility systems benefit the most because enterprise dashboards surface best practices that can be standardized across locations.

Mandates for Value-Based Care Reimbursement

Payment models that reward outcomes over volume require robust analytics to track longitudinal patient journeys and quantify quality metrics. Health systems now integrate clinical data with social factors to build holistic patient profiles that enable targeted interventions. Sophisticated contract analytics automatically apply risk adjustments and shared-savings logic, reducing manual reporting burdens. Early adopters report higher care gap closure rates and payer collaboration improvements, with documented savings such as USD 2.7 million annually through seamless data exchange. Regulatory momentum points to broader adoption in Europe as EHDS operationalizes secondary data use.

Expanding Adoption of Real-Time Remote-Patient-Monitoring Data Streams

Wearables and Internet-of-Medical-Things sensors generate continuous data that predictive models translate into actionable alerts. Machine learning algorithms developed with cloud-based toolchains forecast health deterioration up to three months ahead with 85% accuracy[3]Accenture, “Predictive analytics in remote monitoring,” accenture.com. In the United States 320 hospitals across 37 states have hospital-at-home waivers, accelerating demand for streaming analytics that support acute-level care outside traditional facilities. Asia-Pacific governments promote similar services to extend specialist oversight into rural regions, fuelling rapid platform rollouts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Security concerns related to sensitive patient medical data | -2.8% | Global, heightened in EU and North America | Short term (≤ 2 years) |

| High cost of implementation and deployment | -2.1% | Global, acute in emerging markets | Medium term (2-4 years) |

| Fragmented data standards hindering interoperability | -1.9% | Global, regional variations | Long term (≥ 4 years) |

| Limited AI explainability raising clinical liability risk | -1.4% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Security Concerns Related to Sensitive Patient Medical Data

More than 31 million Americans were affected by healthcare breaches in 2024. Proposed 2025 HIPAA security updates mandate rigorous asset inventories and incident response plans, adding complexity to analytics rollouts. Homomorphic encryption allows computation on encrypted data but introduces latency and integration hurdles that slow projects. Cross-institution research collaborations struggle to reconcile data-sharing benefits with legal exposure, leading some partners to narrow the scope of joint analytics initiatives.

High Cost of Implementation and Deployment

First-year compliance with new HIPAA security rules may cost providers USD 9 billion, straining capital budgets for analytics programs. Legacy infrastructure upgrades, data-quality cleanups, and staff training consume resources before analytic returns materialize. Digital maturity assessments average USD 3,000 per hospital and reveal gaps that demand specialist consulting and managed services. Smaller hospitals and clinics often defer advanced analytics or rely on regional health information exchanges to share the financial burden.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Drive Implementation Complexity

The services segment held 56.25% of the big data in healthcare market share in 2025 and is forecast to grow at 21.45% CAGR as organizations outsource consulting, integration, and managed operations. Many health systems lack internal skill sets in data governance and security, so they contract specialized vendors to design cloud architectures, map data flows, and ensure regulatory compliance. The services segment also benefits from multi-year managed analytics contracts that bundle platform maintenance with performance optimization.

Despite software’s smaller share, platform vendors collaborate with service partners to accelerate deployments, improving time to value for providers. Growth in services underscores the big data in healthcare market's need for multidisciplinary teams that combine clinical insight with data science and cybersecurity. Providers negotiate outcome-based service level agreements that align consulting fees with readmission reductions or revenue-cycle improvements. As advanced use cases emerge, such as federated learning across multiple hospitals, demand for specialized algorithm-curation services is rising.

By Deployment: Cloud Transformation Accelerates

On-premise deployments accounted for 60.95% of the big data in healthcare market size in 2025 because many institutions retained physical control over protected health information. However, cloud deployments are projected to grow at 23.95% CAGR through 2031 as hyperscalers invest in healthcare-specific security tooling and compliance attestations. Providers increasingly migrate AI and high-performance computing workloads to cloud clusters where elastic scaling supports computationally intensive genomics and imaging analyses.

Cloud uptake also reflects the shift to subscription models that convert capital outlays into operating expenses, a feature attractive to budget-constrained hospitals. Microsoft and NVIDIA collaborate on turnkey AI stacks optimized for healthcare, encouraging health systems to offload model training to secure data centers. Hybrid models persist in cardiology and radiology departments where large imaging archives still reside on local picture archiving systems, yet data-tiering policies push older studies to cheaper cloud object storage.

By Analytics Type: Prescriptive Analytics Leads Innovation

Descriptive analytics held 49.10% of revenue in 2025, providing routine dashboards for finance and quality reporting. Predictive analytics occupies a growing middle ground, but prescriptive analytics is set to expand at 25.10% CAGR, reflecting advances in optimization algorithms and decision-support engines. Early prescriptive deployments recommend antibiotic stewardship adjustments and operating room scheduling changes, driving measurable efficiency gains.

Healthcare organizations integrate prescriptive engines with workflow systems to surface recommendations inside electronic health records. Some platforms incorporate reinforcement learning to iteratively improve treatment guidelines based on outcomes data. A study published in PubMed Central reported that prescriptive analytics reduced intensive care unit length of stay by 1.4 days on average. As cloud costs fall, smaller hospitals can afford prescriptive modules on a subscription basis, broadening adoption beyond academic centers.

By Application: Financial Analytics Dominates Current Market

Financial analytics captured 29.20% of big data in healthcare market share in 2025 because revenue-cycle optimization delivers immediate bottom-line benefits. Automated claims coding, denial management, and cash-flow forecasting modules shorten payment cycles and flag anomalies for audit teams. Guidehouse reports that machine learning-augmented revenue cycle tools cut manual touchpoints by 30% for multi-hospital systems.

Population health analytics is forecast to grow at 20.85% CAGR as value-based contracts require holistic risk stratification and outcome tracking. Clinical analytics remains essential for quality improvement initiatives, while operational analytics monitors staffing, bed turnover, and supply chain utilization. Vendors increasingly offer unified platforms that merge financial and clinical datasets to support enterprise performance dashboards, blurring application boundaries.

By End User: Healthcare Providers Lead Adoption

Healthcare providers controlled 47.80% of the big data in healthcare market in 2025 because they generate the bulk of clinical data and face direct accountability for patient outcomes. Hospitals, integrated delivery networks, and outpatient clinics deploy analytics to reduce readmissions, optimize staffing, and improve diagnostic accuracy. Providers also partner with payers on shared-savings contracts, elevating data-sharing requirements and analytics sophistication.

Pharma and biotechnology companies represent the fastest growing end-user group with a 21.05% CAGR, leveraging real-world evidence to supplement clinical trials and accelerate drug discovery. AstraZeneca’s generative AI assistants mine radiology scans and trial documents to streamline R&D processes, supporting its ambition to bring 20 new medicines to market by 2030. Payers use analytics for fraud detection and risk adjustment, while research institutes harness de-identified clinical data to explore new disease pathways.

Geography Analysis

North America remained the largest regional market with 45.10% share in 2025, supported by mature EHR adoption and federal interoperability policies. The 2024 Draft Federal FHIR Action Plan aims to standardize implementation guides across agencies, encouraging seamless data flow among providers, payers, and public health bodies. US health systems engage cloud vendors to modernize analytics while balancing HIPAA obligations. Canada advances national health data integration through its Infoway initiatives, and Mexico invests in digital epidemiology to manage chronic disease burdens.

Europe follows closely, energized by the European Health Data Space that is expected to save the bloc EUR 11 (USD 12.9) billion over ten years by enabling secure secondary data use. Germany’s Hospital Future Act allocates EUR 4 (USD 4.7) billion to modernize hospital IT systems, including analytics readiness. The United Kingdom scales its NHS Federated Data Platform to unify datasets across trusts. France, Italy, and Spain implement national electronic health record expansion, emphasizing AI readiness. By 2028 the EHDS will create cross-border data-sharing pathways that accelerate research and population health programs.

Asia-Pacific is the fastest growing big data in healthcare market region, projected at a 20.10% CAGR through 2031. China integrates provincial health information exchanges into a national backbone that supports predictive modeling for public health emergencies. India’s Ayushman Bharat Digital Mission establishes a unique health identifier that links patient data across public and private facilities. Japan pilots AI-driven eldercare monitoring as it contends with a rapidly aging population. Australia publishes My Health Record APIs to encourage third-party analytics innovations, and South Korea funds cloud-based genomic analysis under its Bio-Vision 2030 roadmap. Diverse demographics and disease profiles create demand for flexible analytics frameworks that can scale from megacities to remote islands.

Competitive Landscape

The big data in healthcare market is moderately concentrated, with electronic health record vendors, cloud hyperscalers, specialized analytics firms, and emerging AI-native platforms all competing. Epic Systems expanded its installed base by 176 facilities in 2024, adding 29,399 beds, while Oracle Health lost 74 sites and 17,232 beds, illustrating how customer support and interoperability drive switching decisions. Intermountain Health and Mayo Clinic publicly endorse Epic’s open APIs that facilitate third-party analytics integration.

Cloud leaders differentiate through sector-specific security and AI accelerators. Microsoft’s partnership with NVIDIA provides optimized GPU infrastructure and reference architectures for healthcare workloads. Amazon Web Services signed a multi-year agreement with Datavant to streamline de-identified data discovery, positioning AWS as a preferred environment for cross-provider analytics collaborations. Google Cloud continues to invest in Healthcare Data Engine integrations that simplify FHIR mapping for hospitals adopting real-time analytics pipelines.

Mergers and acquisitions reshape the vendor landscape. HEALWELL acquired Orion Health in 2025 to form a global interoperability leader capable of supporting EHDS deployments. Oracle is reportedly evaluating the purchase of Veradigm to bolster real-world evidence capabilities in its analytics suite, reflecting a strategy to align EHR data with payer and life sciences use cases. IBM and Cleveland Clinic installed an industry-first healthcare-dedicated quantum computer to explore next-generation drug discovery and optimization algorithms.

Big Data In Healthcare Industry Leaders

Epic Systems Corporation

GE HealthCare

Oracle Corporation

International Business Machines Corporation

Veradigm Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Infosys acquired Optimum Healthcare IT to strengthen its AI-led cloud and data initiatives specifically for healthcare providers.

- June 2025: Epic Systems partnered with Mayo Clinic and Abridge to create generative AI tools that summarize nurse–patient conversations and embed them directly in electronic health records.

- May 2025: Saudi Arabia announced plans to integrate AI across its healthcare sector by 2030, covering diagnostics, robot-assisted surgery, and genomics.

Global Big Data In Healthcare Market Report Scope

As per the scope of the report, big data in healthcare refers to examining big data to discover health information. The data is amassed from numerous sources, including Electronic Health Records (EHRs), medical imaging, genomic sequencing, pharmaceutical research, wearables, and medical devices.

The big data in healthcare market is segmented by component, which includes software and services; deployment, categorized as on-premise and cloud-based. By analytics type, the market segmentation includes, descriptive analytics, predictive analytics, and prescriptive analytics. The application covers financial analytics, clinical data analytics, operational analytics, and population health analytics. By end user, the market is segmented into healthcare providers, healthcare payers, pharma & biotechnology companies, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. Additionally, the report provides insights into market sizes and trends for 17 countries across major global regions, presenting values in USD for each segment.

| Software |

| Services |

| On-premise |

| Cloud |

| Descriptive Analytics |

| Predictive Analytics |

| Prescriptive Analytics |

| Financial Analytics |

| Clinical Data Analytics |

| Operational Analytics |

| Population Health Analytics |

| Healthcare Providers |

| Healthcare Payers |

| Pharma & Biotechnology Companies |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Deployment | On-premise | |

| Cloud | ||

| By Analytics Type | Descriptive Analytics | |

| Predictive Analytics | ||

| Prescriptive Analytics | ||

| By Application | Financial Analytics | |

| Clinical Data Analytics | ||

| Operational Analytics | ||

| Population Health Analytics | ||

| By End User | Healthcare Providers | |

| Healthcare Payers | ||

| Pharma & Biotechnology Companies | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the Big Data in Healthcare market size in 2026?

The market is valued at USD 79.86 billion in 2026.

How fast is the Big Data in Healthcare market expected to grow?

It is projected to expand at a 19.35% CAGR to reach USD 193.49 billion by 2031.

Which component contributes the most revenue today?

Services account for 56.25% of 2025 revenue and remain the fastest-growing segment at a 21.45% CAGR through 2031.

Which region will see the highest growth through 2031?

Asia-Pacific leads regional growth with a forecast 20.10% CAGR through 2031, driven by large-scale digitization across China, India, and Southeast Asia.

Why do healthcare providers dominate adoption?

Providers hold 47.80% market share in 2025 because they generate the bulk of clinical data and must demonstrate measurable care improvements under value-based contracts.

Page last updated on: