Benelux Frontline Worker Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

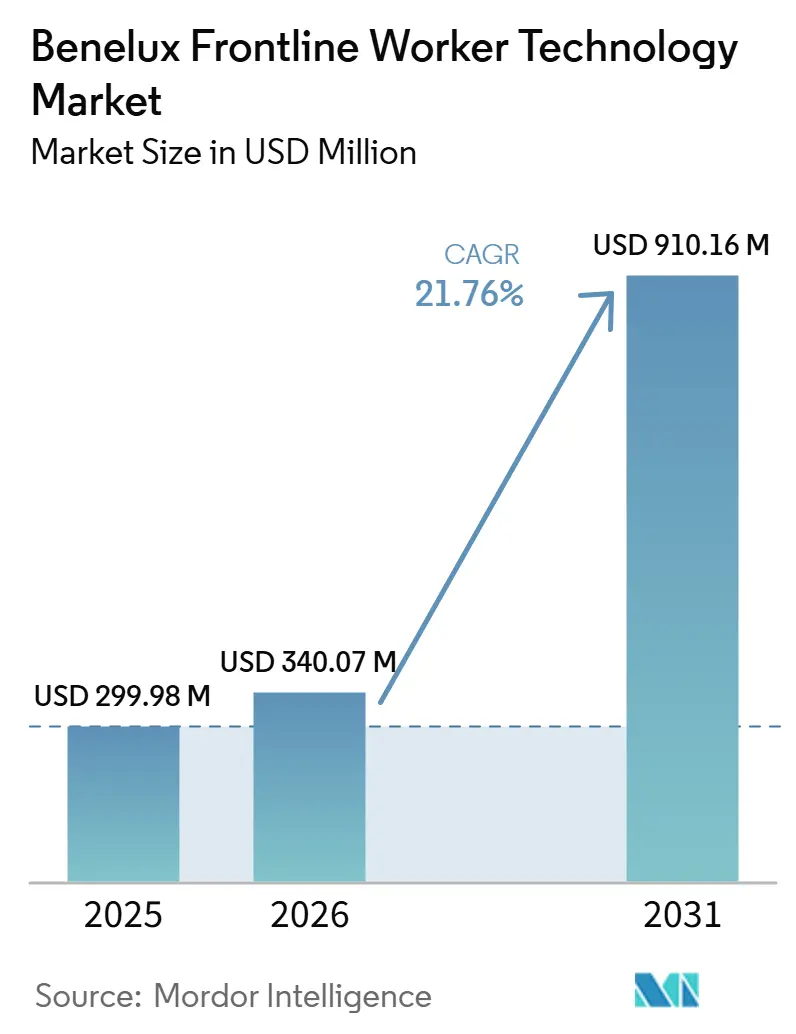

| Base Year Market Size (2025) | USD 299.98 Million |

| Market Size (2026) | USD 340.07 Million |

| Market Size (2031) | USD 910.16 Million |

| Growth Rate (2026 - 2031) | 21.76% CAGR |

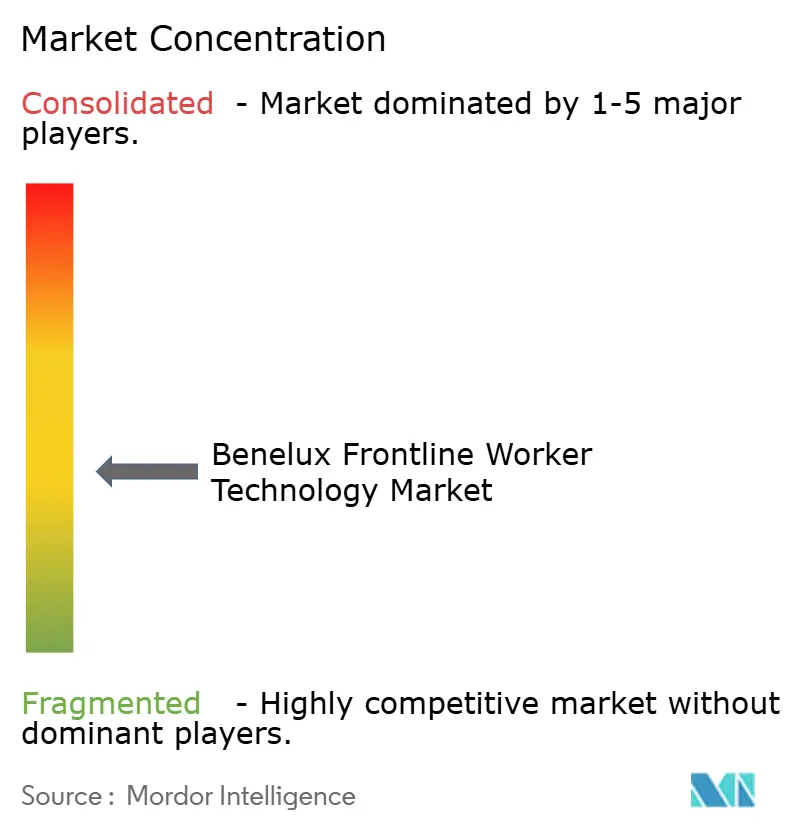

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Benelux Frontline Worker Technology Market Analysis by Mordor Intelligence

The Benelux frontline worker technology market size was USD 300 million in 2025 and is forecast to reach USD 910 million by 2031 at a CAGR of 21.76% during 2026-2031. The market is moving forward as employers replace manual scheduling, paper records, and spreadsheet-led shift planning with cloud platforms that can support distributed frontline teams with less administrative effort. Labor shortages across the region are also pushing employers to spend more on productivity tools because adding headcount is becoming harder in manufacturing, logistics, healthcare, retail, and public services. Strong digital readiness in the Netherlands and the cross-border workforce complexity seen in Luxembourg are keeping adoption conditions favorable across the region. Competition in the Benelux frontline worker technology market is increasingly centered on AI-enabled orchestration, compliance support, and the ability to connect workforce tools with existing HR, ERP, payroll, warehouse, and operations systems. Integration work and stricter AI governance are still slow some large deployments, but they also create a clearer advantage for vendors that can offer auditability, easier implementation, and local compliance support.

Key Report Takeaways

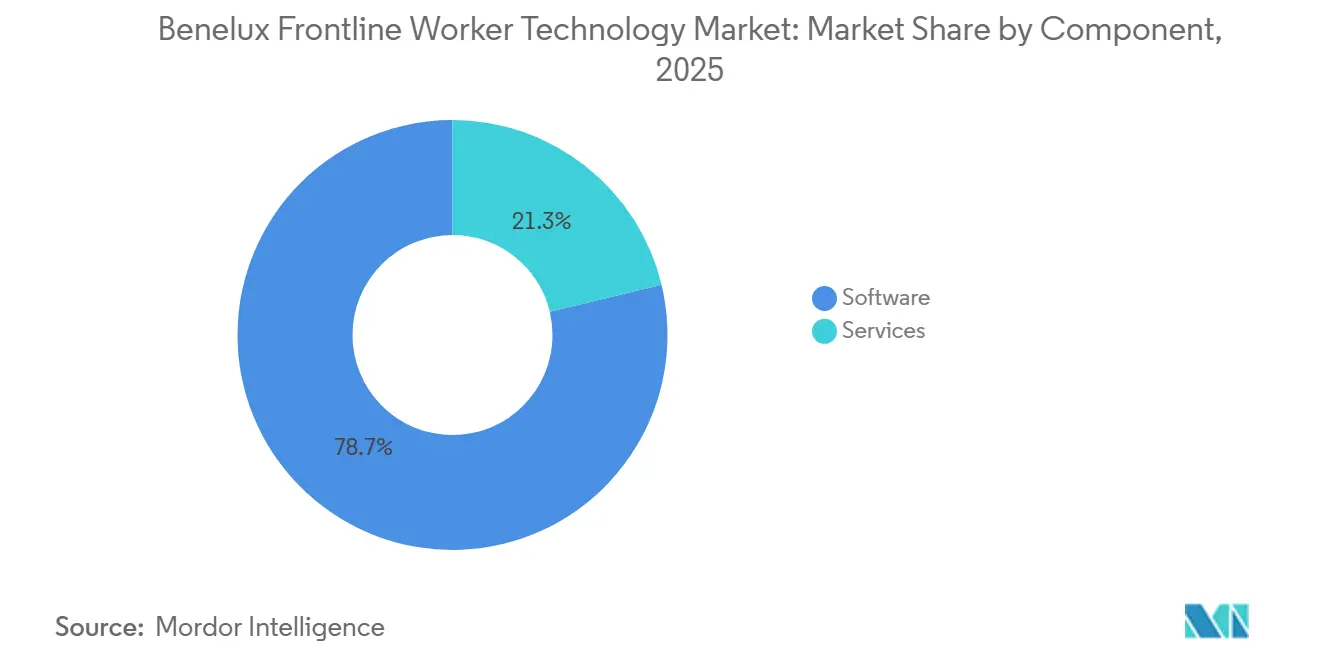

- By component, software accounted for 82.22% of revenue in the Benelux frontline worker technology market in 2025, while services are projected to expand at a 22.19% CAGR through 2031.

- By deployment mode, cloud-based deployment accounted for 81.11% of the Benelux frontline worker technology market size in 2025 and is projected to record the fastest CAGR of 23.84% through 2031.

- By organization size, large enterprises held 71.66% of demand in 2025, while SMEs are expected to expand at a 24.61% CAGR through 2031.

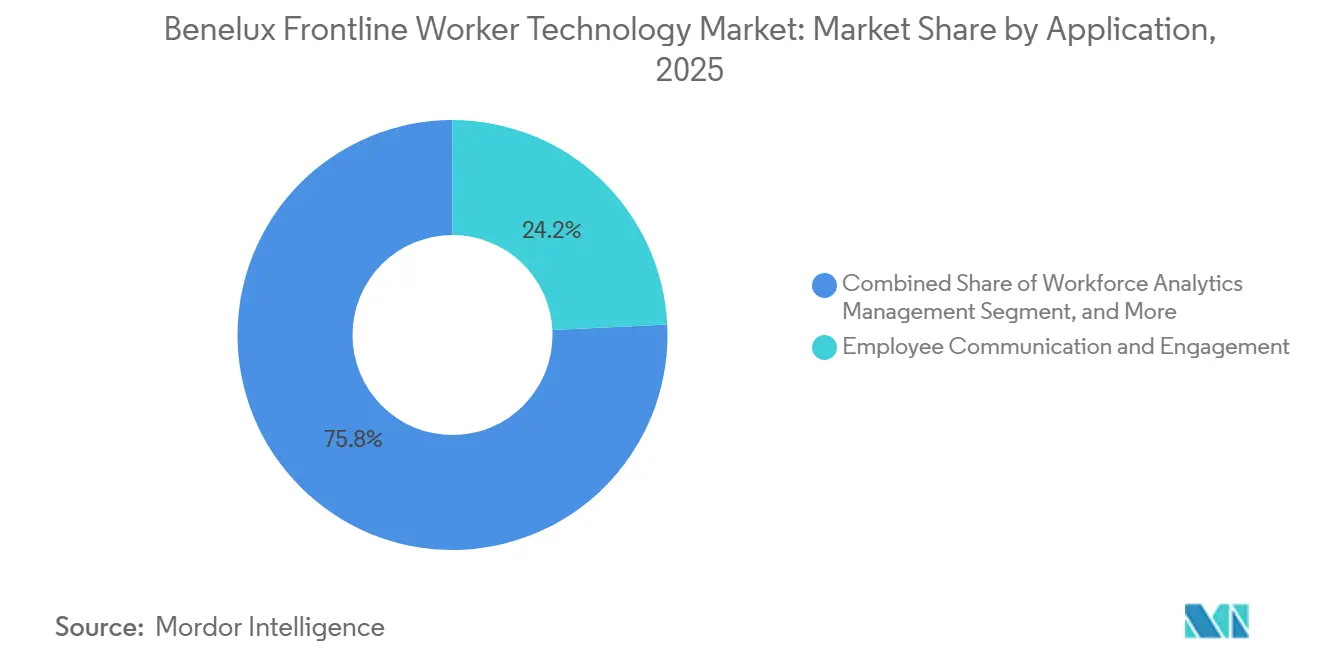

- By application, employee communication and engagement held 24.22% of revenue in 2025, while workforce analytics and performance management are projected to grow at a 26.33% CAGR through 2031.

- By end-user industry, industrial manufacturing accounted for 31.11% of revenue in 2025, while transportation and logistics is projected to advance at a 28.99% CAGR through 2031.

- By geography, the Netherlands held 49.66% of the Benelux frontline worker technology market share in 2025, while Luxembourg is projected to grow at a 29.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Benelux Frontline Worker Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Real-Time Task Orchestration for Distributed Frontline Teams | +4.8% | Global, concentrated in Benelux logistics corridors and multi-site manufacturing operations | Short term (≤ 2 years) |

| Worker Safety and Compliance Digitization Requirements | +3.9% | EU-wide, with peak compliance pressure in Belgium and the Netherlands | Medium term (2-4 years) |

| Replacement of Paper and Spreadsheet Shift Operations | +3.5% | Global, with advanced adoption in the Netherlands and Belgium | Short term (≤ 2 years) |

| Adoption of Rugged Mobile Devices and Smart Wearables | +3.2% | Global, with strong uptake in Benelux warehousing, transport, and field service | Medium term (2-4 years) |

| Labor Shortages and Need for Productivity Uplift | +2.9% | Benelux, with spillover into EU cross-border labor markets | Short term (≤ 2 years) |

| Privacy-First Workforce Analytics and Consent-Based Mobile Management | +1.4% | EU-wide, strongest in the Netherlands and Belgium | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Real-Time Task Orchestration across Distributed Frontline Teams

The Benelux frontline worker technology market is benefiting from the simple fact that legacy task boards and email chains do not work well across multi-site frontline operations. Employers in logistics, manufacturing, field service, and public operations now need live visibility into who is available, what work is pending, and how quickly shift changes can be absorbed. SD Worx reported in 2026 that 44.6% of European organizations were redesigning work and workflows in response to AI and automation, which supports the move toward integrated orchestration tools instead of isolated point solutions.[1]SD Worx, “Pulse 2026, AI In The Workplace, Expert Insights And Future Of AI In HR,” SD Worx, sdworx.com UKG reinforced this shift in June 2026 by adding an agentic orchestration layer to its Workforce Operating Platform, including the Workforce Intelligence Hub and Dynamic Workforce Operations, which connected real-time data to frontline execution in a single interface. This matters in the Benelux frontline worker technology market because many buyers now prefer suites that connect scheduling, pay, performance, and coverage decisions on a shared database. It also raises the bar for smaller vendors, as buyers in the region increasingly expect a single system to manage execution across multiple sites, languages, and shift structures.

Stricter Worker Safety and Compliance Digitization Requirements

The Benelux frontline worker technology market is also gaining support from the shift toward digital compliance records in frontline settings. Paper logs and local spreadsheets are becoming less practical because employers need timestamped records that can be reviewed quickly and stored consistently across sites. The European Commission confirmed that the EU AI Act entered into force on August 1, 2024, and that high-risk obligations will become fully applicable from August 2, 2026, thereby increasing the governance burden for automated scheduling and workforce analytics tools.[2]European Commission, “Regulation (EU) 2024/1689, Artificial Intelligence Act,” European Commission, europa.eu This is pushing employers toward platforms that can document model behavior, store audit trails, and support cleaner oversight of workplace automation. The result for the Benelux frontline worker technology market is that compliance has become part of the product value rather than a separate administrative layer. It also helps explain why service work remains important because each policy update, workflow change, or audit requirement can trigger configuration, training, and support work after the first deployment.

Accelerating Replacement of Paper-Based and Spreadsheet-Based Shift Operations

A large share of the near-term opportunity in the Benelux frontline worker technology market still comes from replacing manual shift administration. Many mid-sized operators in hospitality, construction, retail, and manufacturing still run scheduling, attendance checks, and task assignments through paper files or spreadsheet templates. Statistics Netherlands reported in June 2026 that 64% of Dutch firms faced staff shortages in April 2026, and close to half of the affected firms were investing in automation as a response.[3]Honeywell, “CK67 Ultra-Rugged 5G Mobile Device Datasheet,” Honeywell, honeywellenterprisemobility.com That type of pressure supports cloud scheduling and task management platforms because companies want to increase output from existing teams rather than rely solely on recruitment. The business case is even stronger in Belgium and the Netherlands because working-time rules, break rules, and overtime-monitoring requirements make manual scheduling more error-prone. Vendors that keep onboarding simple, support mobile use from day 1, and connect easily to payroll systems are therefore in a stronger position as the paper-to-digital shift continues.

Rising Adoption of Rugged Mobile Devices And Smart Wearables

The Benelux frontline worker technology market is also supported by the broader adoption of rugged mobile hardware in warehouses, field operations, and industrial sites. The region has dense logistics, strong manufacturing clusters, and demanding frontline environments, which keep demand high for devices that can handle long shifts and harsh operating conditions. Honeywell highlighted this direction with its CK67 ultra-rugged 5G mobile device, which was released in 2025 for warehouse and distribution settings and designed with long Android lifecycle support and operational intelligence capabilities.[4]Statistics Netherlands, “Staff Shortages Mean Business Is Turning To Automation,” CBS, cbs.nl As more sites standardize on rugged and wearable hardware, software design becomes more important because frontline users need interfaces that work quickly on smaller screens and in hands-busy settings. This favors mobile-first platforms over solutions that were extended later from desktop HR or ERP systems. It also broadens the addressable scope of the Benelux frontline worker technology market because hardware readiness makes digital task execution more practical across more use cases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Friction With Legacy HR, ERP, POS, And WMS Stacks | -3.1% | Global, particularly acute in legacy-heavy Belgian manufacturing and Dutch logistics | Medium term (2-4 years) |

| Frontline User Resistance To Complex Or Opaque AI Scheduling | -2.4% | EU-wide, amplified in Belgium and the Netherlands by worker consultation expectations | Short term (≤ 2 years) |

| Limited ROI Visibility In Small Multi-Site Deployments | -1.8% | Global, concentrated among Benelux SMEs operating 5-50 frontline employees per site | Medium term (2-4 years) |

| Data Residency And Mobile Cybersecurity Compliance Burden | -1.3% | EU and Benelux, driven by GDPR enforcement expectations and EU AI Act obligations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Friction with Legacy HR, ERP, POS, and WMS Stacks

Integration remains one of the clearest brakes on the Benelux frontline worker technology market, especially in large manufacturing and logistics accounts. Many employers still run core HR, inventory, warehouse, payroll, and production functions on older systems that were not built for fast two-way data exchange with modern workforce tools. Belgium's Federal Public Service Economy reported in 2025 that only 5.7% of the country's active workforce worked in ICT-related roles, indicating a capacity gap that can slow implementation within buying organizations. When internal technical capacity is limited, even a well-scoped deployment can take longer, as buyers rely more on external integrators and staged rollouts. That raises perceived risk for mid-market buyers and can delay full adoption beyond the initial pilot stage. For the Benelux frontline worker technology market, this means vendors with pre-built connectors and lower implementation effort can defend pricing better than vendors that still rely on custom integration work.

Frontline User Resistance to Complex or Opaque AI Scheduling

User trust is another real restraint in the Benelux frontline worker technology market because optimized schedules still fail when employees do not understand or accept the logic behind them. Scheduling tools may improve coverage, but they can create frustration when workers feel their preferences, fairness, or preferred shift patterns are not reflected in the outcome. SD Worx reported in 2026 that only 29.3% of European employees regularly used AI tools, and only 52.1% trusted their organizations to use AI ethically, indicating that adoption remains uneven even as employer interest rises. In the Benelux frontline worker technology market, this makes explainability, self-service controls, and employee-facing transparency more important than a narrow focus on algorithmic optimization. Platforms that let employees view schedule rules, manage swaps, and interact with supervisors through clear workflows are better placed to move beyond pilot use. Vendors that ignore that trust layer risk slower rollouts, even when the technical product is strong.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Ground As Deployments Become More Involved

Software accounted for 82.22% of revenue in 2025, which shows that subscriptions remain the economic core of the Benelux frontline worker technology market. Cloud applications still dominate buyer budgets because they can be rolled out faster across distributed sites and usually need less upfront infrastructure than older enterprise systems. The software lead also reflects the practical buying pattern seen across the region, where employers often start with communication, scheduling, or task management and then add more workflows over time. This keeps the Benelux frontline worker technology market centered on platforms that can support repeat use across daily operations rather than on one-time technology projects. It also means vendors are judged heavily on usability, mobile access, and how quickly supervisors can begin using the tools at the site level.

Services are still the fastest-growing component, with a projected CAGR of 22.19% through 2031, because larger deployments now involve more integration, training, change support, and ongoing configuration work. This part of the Benelux frontline worker technology industry is expanding as employers buy broader suites instead of single modules and need help aligning them with payroll, ERP, and operational systems. Compliance changes add another layer, as policy updates can require workflow redesign, reporting changes, and additional user training after the original rollout. Belgium's Federal Public Service Economy has already identified the region's digital skills gap, which supports external service demand when internal IT teams are stretched. In effect, the software layer keeps scale high, while the services layer is gaining importance because buyers in the Benelux frontline worker technology market want faster deployment and stronger local support once the platform is live.

By Deployment Mode: Cloud Adoption Deepens While Hybrid Stays Relevant

Cloud-based deployment accounted for 81.11% of spending in 2025, which makes it the clear default model in the Benelux frontline worker technology market. That share reflects a strong preference for faster rollout, subscription pricing, automatic updates, and easier management across multiple frontline locations. Cloud also suits the regional operating model because many employers need to manage shift communication, tasks, and compliance across sites in multiple countries or languages. In practical terms, cloud has become the easiest path for employers seeking quick onboarding and central oversight without rebuilding their entire IT stack. Cloud-based deployment also has the strongest growth outlook, with a 23.84% CAGR through 2031, indicating the market is still in an expansion phase rather than a maturity phase.

Hybrid deployment remains strategically relevant because many large employers still depend on on-premises systems for plant operations, point-of-sale workflows, or regulated records that cannot be replaced at the same pace as frontline applications. That need is evident in manufacturing and logistics, where companies often want cloud workflows at the user level but still need stable links to legacy back-end systems. As a result, buyers in the Benelux frontline worker technology market often view hybrid as a transition model rather than a legacy holdout. On-premises tools, therefore, remain in use in parts of government and critical infrastructure where network control and data handling remain sensitive. This structure means the cloud continues to lead the Benelux frontline worker technology market, while hybrid still matters because it reduces disruption for large employers that cannot move every system at once.

By Organization Size: SMEs Narrow The Gap With Large Enterprises

Large enterprises accounted for 71.66% of demand in 2025, reflecting the spending power and site complexity of major employers in the Benelux frontline worker technology market. These companies often manage broad frontline populations across factories, logistics networks, healthcare settings, retail chains, or municipal operations, so the cost of poor coordination is higher for them. They also tend to have established relationships with large software providers and more formal digital transformation budgets. That combination kept large organizations ahead in 2025 and gave them a bigger role in early multi-module deployments. Their scale also means they often set the first wave of demand for analytics, AI orchestration, and connected workflows.

SMEs are the fastest-growing segment by organization size, with a projected CAGR of 24.61% through 2031, as cloud pricing and easier onboarding are reducing the access gap. This is an important shift in the Benelux frontline worker technology market because many regional employers fall into the mid-market and have relied on manual tools longer than large enterprises have. Statistics Netherlands reported in June 2026 that staff shortages were pushing firms toward automation, which supports adoption even among buyers with smaller internal teams. Vendors are responding with template-led deployments, mobile-first interfaces, and lighter integration paths that suit leaner operating structures. That is why the Benelux frontline worker technology industry is broadening beyond flagship enterprise accounts and reaching a wider base of smaller operators with clear daily workflow needs.

By Application: Analytics Accelerate As Communication Tools Mature

Employee communication and engagement held 24.22% of application revenue in 2025, making it the largest application area in the Benelux frontline worker technology market. That position is logical because many frontline employees do not have regular access to corporate email, while mobile communication is the most direct way to connect teams across shifts and sites. Employers usually begin by addressing basic communication gaps before moving to more advanced automation layers. Once mobile communication is in place, tasking, scheduling, and knowledge sharing become easier to standardize because there is already a live connection to the workforce. This is why communication remained the foundation layer across many deployments in 2025.

Workforce analytics and performance management are projected to grow at a 26.33% CAGR through 2031, which makes it the fastest-growing application in the Benelux frontline worker technology market. Buyers that already digitized communication and scheduling are now moving toward forecasting, performance visibility, and more proactive labor planning. This shift is especially relevant in a region where labor shortages and compliance demands make workforce efficiency more valuable at the site level. The Benelux frontline worker technology market for analytics-related tools is benefiting from this next-step investment pattern, as companies seek better labor visibility without adding more management overhead. Learning and knowledge enablement, safety and compliance management, and task execution are also gaining relevance as employers try to preserve know-how, reduce operational errors, and keep frontline processes more consistent. Taken together, these patterns show a market moving from foundational communication needs to more connected decision support and performance management over time.

By End-User Industry: Manufacturing Leads While Logistics Expands Fastest

Industrial manufacturing accounted for 31.11% of revenue in 2025, giving it the largest vertical position in the Benelux frontline worker technology market. Manufacturers in Belgium and the Netherlands are using frontline tools to digitize quality checks, shift handovers, maintenance coordination, and safety reporting because paper processes no longer scale well across busy facilities. That keeps manufacturing central to demand because frontline work in this segment depends on consistency, auditability, and rapid response to production issues. The segment also benefits from the region's strong industrial base and the need to connect shop floor activity with broader enterprise systems. Industrial manufacturing, therefore, accounted for a leading share of the Benelux frontline worker technology market in 2025 and remains a reference point for vendor positioning.

Transportation and logistics are projected to grow at a 28.99% CAGR through 2031, which makes it the fastest-growing vertical in the Benelux frontline worker technology market. This follows the region's role as a major European freight and warehousing hub, where real-time dispatch, driver coordination, proof-of-delivery workflows, and cross-site execution all matter. Healthcare and life sciences are also becoming increasingly important, as the Netherlands is pushing hybrid care delivery, with the Dutch National Institute for Public Health and the Environment tracking a target of 70% hybrid care services by the end of 2026. The World Economic Forum also noted in its 2025 Future of Jobs Report that roles such as delivery drivers, construction workers, and care economy workers are among the fastest-growing jobs in absolute terms through 2030, which supports demand across several frontline-heavy sectors. As a result, the Benelux frontline worker technology market share is still led by manufacturing today, but the strongest forward momentum is coming from logistics and other labor-intensive service environments.

Geography Analysis

The Netherlands accounted for 49.66% of spending in 2025, making it the largest geography in the Benelux frontline worker technology market. Its lead reflects strong digital readiness, a large logistics base, and a business environment that is already comfortable with software-led process change. Statistics Netherlands reported in March 2026 that Dutch firms ranked among the top 3 in the EU for digitalization in 2025 and that 84% of the population had at least basic digital skills, which was the highest rate in the EU. That level of readiness matters because frontline platforms depend on manager adoption, worker access, and confidence in digital workflows. The Netherlands also benefits from large freight, warehousing, airport cargo, and industrial activity, which keeps demand strong for task management, mobile workforce tools, and operational analytics.

Belgium remains a core part of the Benelux frontline worker technology market, even though it did not lead in terms of share in 2025. Its growth case is tied to labor shortages, operational digitization, and a rising need for more structured frontline coordination. ManpowerGroup reported in March 2026 that Belgium had a 3.8% job vacancy rate, compared with a 2.0% EU average, and that 73% of Belgian employers were having difficulty filling roles. Belgium's Federal Public Service Economy also showed in its 2025 digital economy review that AI use was advancing in operational automation and HR-adjacent workflows, which supports the case for broader frontline system adoption. That combination makes Belgium attractive to vendors that can tie communication, scheduling, analytics, and compliance into a single product structure. It also means local-language coverage and smooth deployment matter, because employers are trying to improve productivity without adding process complexity.

Luxembourg is projected to grow at a 29.16% CAGR through 2031, which makes it the fastest-growing geography in the Benelux frontline worker technology market. Its small absolute size is offset by its concentration of multinational employers and its daily cross-border workforce patterns. The Luxembourg government set out a national AI strategy in 2024 that supports trusted, human-centered workplace AI, helping create a positive policy climate for compliant workforce tools. The rest of the region contributes a smaller but expanding share as cross-border facilities and pan-European rollouts gradually extend the Benelux frontline worker technology market's footprint beyond the main national demand centers.

Competitive Landscape

The Benelux frontline worker technology market remains moderately fragmented, with no single vendor controlling demand across all application areas. Large enterprise software providers such as Microsoft, SAP SE, ServiceNow, and Workday compete on integration depth, product breadth, and their ability to fit inside existing HR and ERP environments. Specialist vendors such as Quinyx, WorkJam, Legion Technologies, Augmentir, and Tulip Interfaces compete more on mobile usability, quicker deployment, and sharper frontline focus. This creates a market where buyers often choose between ecosystem breadth and execution speed rather than between strong and weak products. It also means the competitive center of gravity is moving from stand-alone communication or scheduling tools toward broader workforce operating platforms.

Recent product moves show how this shift is playing out inside the Benelux frontline worker technology market. UKG added an agentic orchestration layer to its Workforce Operating Platform in June 2026, linking real-time intelligence with frontline execution and making orchestration a more visible part of vendor differentiation. ServiceNow launched Autonomous Workforce in February 2026, following the acquisition of Moveworks, which strengthened its position in conversational support and workflow automation for employees. Workday also expanded its frontline proposition in January 2026 with Paradox Conversational ATS, available through Workday, and the Workday Frontline Agent, both aimed at high-volume frontline hiring and workforce management tasks. These moves suggest that vendors are trying to own more of the frontline workflow stack rather than stay in narrow categories.

Competition is also tightening because platform breadth alone is no longer enough in the Benelux frontline worker technology market. SAP, Nokia, and Microsoft announced a multi-year partnership in June 2026 to advance cloud and AI-led business transformation, including deeper links between SAP Joule and Microsoft 365 Copilot for both frontline and knowledge workers. Tulip secured USD 120 million in January 2026 and paired the funding with a strategic alliance with Mitsubishi Electric, which strengthens its ability to deepen its presence in industrial accounts. In the same direction, Legion Technologies and WorkJam announced a strategic partnership in March 2025 that combined labor optimization with digital workplace tools on a more integrated model. The implication is clear: buyers in the Benelux frontline worker technology market are consolidating around vendors that can cover multiple workflows on a shared architecture while still keeping deployment practical for frontline teams.

Benelux Frontline Worker Technology Industry Leaders

UKG Inc.

Infor Inc.

WorkJam Inc.

Quinyx AB

Zebra Technologies Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Nokia, SAP, and Microsoft announced a strategic multi-year partnership to advance cloud and AI-driven enterprise business transformation, including deeper integration between SAP Joule AI and Microsoft 365 Copilot to unify AI assistance across frontline and knowledge worker populations within common enterprise environments.

- June 2026: UKG introduced an agentic orchestration layer to its Workforce Operating Platform, including the Workforce Intelligence Hub and Dynamic Workforce Operations, enabling managers to shift from reactive to predictive frontline operations management.

- May 2026: UKG unveiled UKG Pro Pay with Workforce AI at Payroll Congress 2026, introducing agentic and generative AI to detect, analyze, and resolve payroll discrepancies in real time, with direct relevance for frontline and hourly workers whose variable schedules make payroll accuracy a recurring operational risk.

- February 2026: ServiceNow launched Autonomous Workforce after the Moveworks acquisition close, combining Moveworks' conversational AI with ServiceNow's workflow capabilities to automate employee support processes.

Benelux Frontline Worker Technology Market Report Scope

The Benelux frontline worker technology market refers to the ecosystem of software and services designed to empower non-desk employees who primarily perform their duties outside a traditional office setting. This includes tools that facilitate communication, task management, scheduling, knowledge sharing, and performance tracking for workers in sectors such as retail, manufacturing, healthcare, and logistics across the Benelux region. The market encompasses cloud-based, on-premises, and hybrid deployment models tailored to the operational and security needs of organizations of varying sizes, from small and medium enterprises to large corporations. Key applications include workforce scheduling and coordination, safety and compliance management, and learning enablement, all aimed at improving operational efficiency, employee engagement, and real-time decision-making at the edge of business operations. The market scope is defined by the revenues generated by technology vendors and service providers across the Benelux countries, specifically Belgium, the Netherlands, and Luxembourg.

The Benelux Frontline Worker Technology Market Report is Segmented by Component (Software, and Services), Deployment (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Employee Communication and Engagement, Workforce Execution and Task Management, Workforce Scheduling and Coordination, Learning and Knowledge Enablement, Workforce Analytics and Performance Management, Safety and Compliance Management, and Other Applications), End-User Industry (Retail and E-Commerce, Industrial Manufacturing, Healthcare and Life Sciences, Transportation and Logistics, Hospitality, Construction, Government and Public Administration, and Other Industries), and Geography (Belgium, Netherlands, Luxembourg, and Rest of Benelux). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Employee Communication and Engagement |

| Workforce Execution and Task Management |

| Workforce Scheduling and Coordination |

| Learning and Knowledge Enablement |

| Workforce Analytics and Performance Management |

| Safety and Compliance Management |

| Other Applications |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Hospitality |

| Construction |

| Government and Public Administration |

| Other Industries |

| Belgium |

| Netherlands |

| Luxembourg |

| Rest of Benelux |

| By Component | Software |

| Services | |

| By Deployment | Cloud-Based |

| Hybrid | |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Employee Communication and Engagement |

| Workforce Execution and Task Management | |

| Workforce Scheduling and Coordination | |

| Learning and Knowledge Enablement | |

| Workforce Analytics and Performance Management | |

| Safety and Compliance Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Industrial Manufacturing | |

| Healthcare and Life Sciences | |

| Transportation and Logistics | |

| Hospitality | |

| Construction | |

| Government and Public Administration | |

| Other Industries | |

| By Geography | Belgium |

| Netherlands | |

| Luxembourg | |

| Rest of Benelux |

Key Questions Answered in the Report

What is the current and forecast value of the Benelux frontline worker technology market?

The Benelux frontline worker technology market was valued at USD 299.98 million in 2025 and is forecast to reach USD 910.16 million by 2031 at a CAGR of 21.76% during 2026-2031.

Which deployment model leads demand in Benelux frontline worker technology?

Cloud-based deployment led with 81.11% of spending in 2025 and is also projected to grow the fastest at a 23.84% CAGR through 2031.

Which application area is expanding the fastest across frontline workforce platforms in Benelux?

Workforce analytics and performance management is the fastest-growing application, with a projected CAGR of 26.33% through 2031, as employers move beyond communication into labor visibility and optimization.

Which end-user sector creates the largest revenue base in this regional market?

Industrial manufacturing held the largest share at 31.11% in 2025 because factories are digitizing shift handovers, quality checks, maintenance coordination, and safety workflows.

Why is logistics becoming such a strong growth engine for frontline technology vendors?

Transportation and logistics is projected to grow at a 28.99% CAGR through 2031 because the region's freight, warehousing, and delivery networks need real-time task dispatch, worker communication, and execution tracking.

Which country offers the strongest near-term growth opportunity in Benelux?

Luxembourg is projected to grow the fastest at a 29.16% CAGR through 2031, supported by its multinational employer base and complex cross-border workforce management needs.

Page last updated on: