Benelux Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

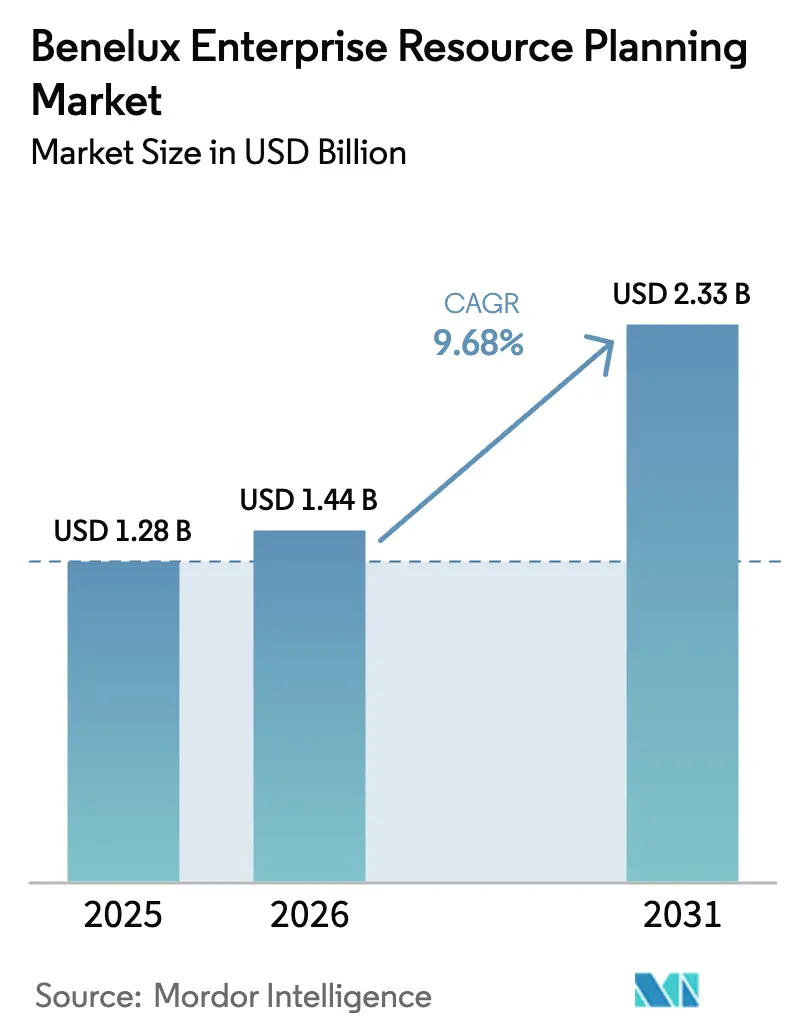

| Base Year Market Size (2025) | USD 1.28 Billion |

| Market Size (2026) | USD 1.44 Billion |

| Market Size (2031) | USD 2.33 Billion |

| Growth Rate (2026 - 2031) | 9.68% CAGR |

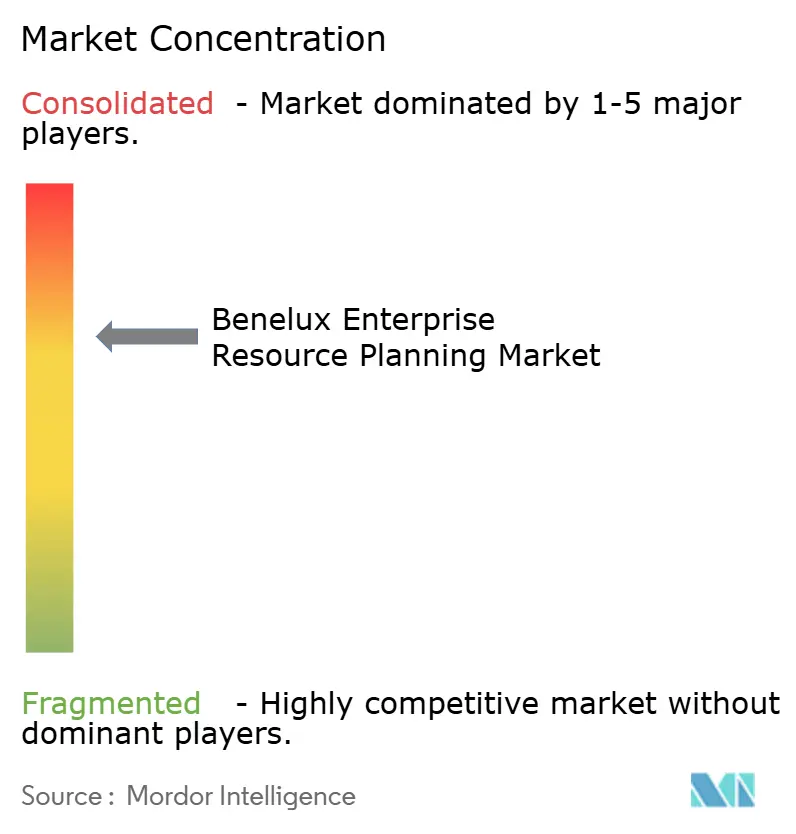

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Benelux Enterprise Resource Planning Market Analysis by Mordor Intelligence

The Benelux enterprise resource planning market size was valued at USD 1.28 billion in 2025 and is estimated to grow from USD 1.44 billion in 2026 to reach USD 2.33 billion by 2031, at a CAGR of 9.68% during the forecast period (2026-2031). Demand is accelerating as e-invoicing mandates, EU recovery-fund grants, and embedded generative-AI copilots shorten replacement cycles and shift budgets toward cloud subscriptions. Belgium's Peppol e-invoicing mandate took effect on January 1, 2026, forcing thousands of suppliers to upgrade legacy accounting modules or risk losing public-sector contracts, while the Corporate Sustainability Reporting Directive (CSRD) is pushing enterprises to instrument ESG data flows directly within ERP backbones rather than relying on spreadsheet reconciliations.[1]First-name Last-name, “Peppol E-Invoicing Mandate Belgium,” EUR-Lex, eur-lex.europa.euMid-market manufacturers are adopting cloud suites to reduce total cost of ownership, while banks in Luxembourg prioritize cyber-resilient deployments that comply with the Digital Operational Resilience Act. Vendors are retiring on-premise support, widening the value gap between SaaS and perpetual licenses, and spurring two-tier architectures that link edge factories to central finance cores. Competitive intensity is highest in the Netherlands, where local champions Exact and Visma jostle with SAP and Microsoft, and lowest in Luxembourg, where regulatory complexity favors incumbents with deep financial-services templates.

Key Report Takeaways

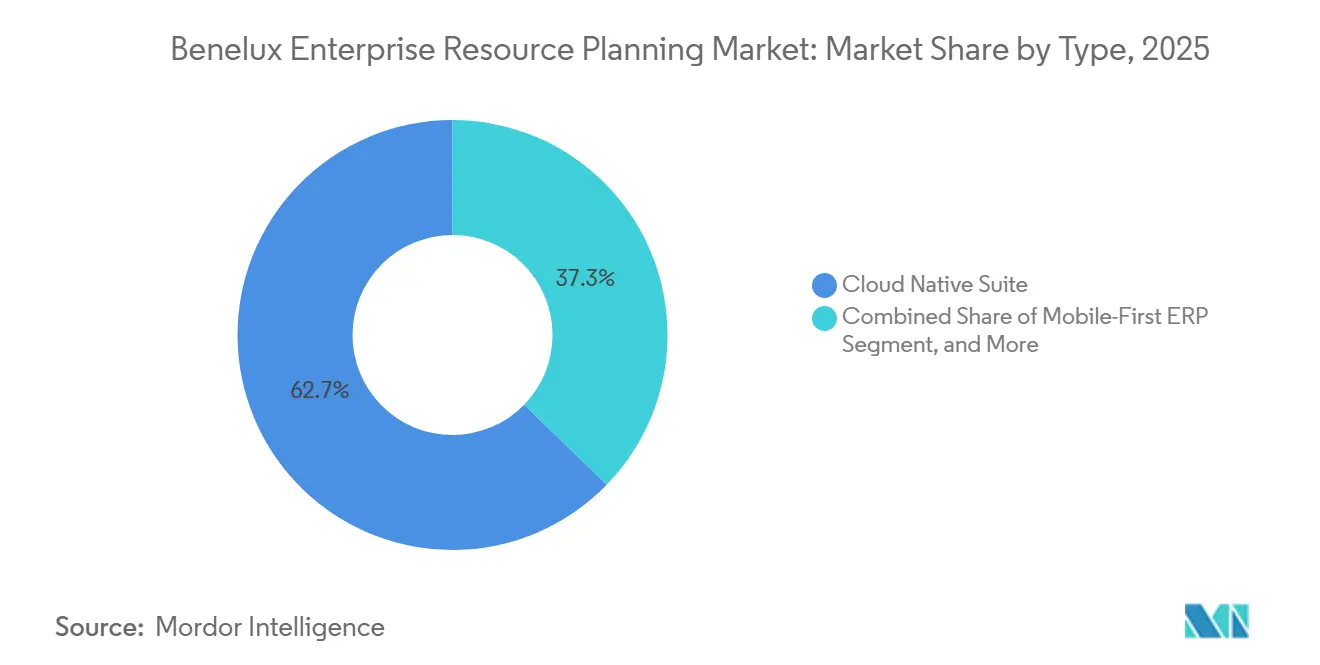

- By type, cloud-native suites held 62.73% of 2025 revenue and IS on track for a 10.48% CAGR through 2031.

- By business function, finance and accounting led with 53.47% of 2025 revenue, while manufacturing execution is projected to grow at a 10.68% CAGR through 2031.

- By deployment model, cloud captured 34.60% of 2025 revenue and is expanding at a 11.08% CAGR.

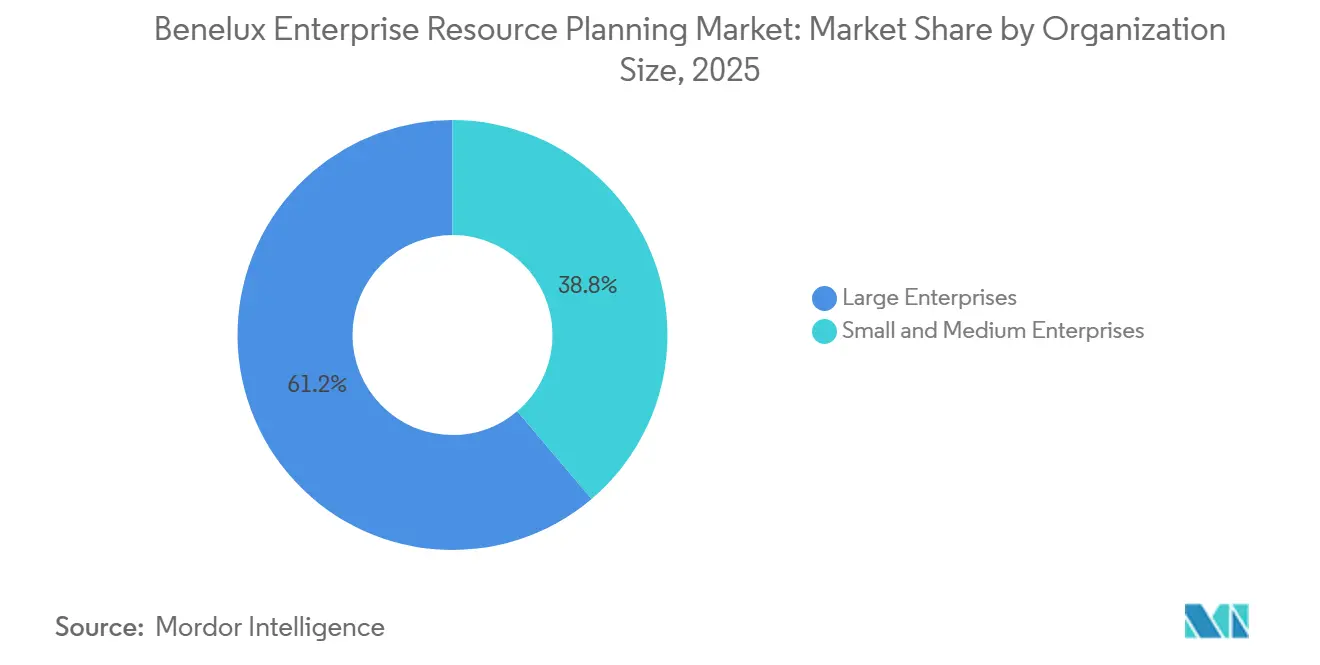

- By organization size, small and medium enterprises accounted for 38.8% of 2025 revenue and is forecasted to rise at a 11.78% CAGR.

- By industry vertical, manufacturing accounted for 37.50% of 2025 revenue and is set to post the fastest CAGR of 11.68% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Benelux Enterprise Resource Planning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-Native Adoption Among Mid-Market Firms | +2.1% | Netherlands and Belgium with spillover to Luxembourg financial services | Medium term (2-4 years) |

| Growing Compliance Pressure on E-Invoicing and ESG Reporting | +1.9% | Belgium, Netherlands, Luxembourg | Short term (≤ 2 years) |

| Accelerated Digitalization Incentives from EU Recovery Funds | +1.5% | Belgium and Netherlands | Medium term (2-4 years) |

| Rising Integration of AI Copilots into ERP Suites | +1.3% | Early adoption in Dutch technology hubs and Belgian multinationals | Long term (≥ 4 years) |

| Vendor Push Toward Subscription Renewals and Upsell | +1.1% | Installed bases of SAP, Oracle and Microsoft | Short term (≤ 2 years) |

| Demographic Talent Crunch Driving Automation | +0.9% | Flanders manufacturing and Noord-Brabant industrial clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-Native Adoption Among Mid-Market Firms

SaaS total cost of ownership now undercuts perpetual licenses by roughly 20%, prompting firms with 100-999 full-time employees to replace decade-old systems rather than patch them. Faster patch cycles, predictable operating expense models, and easier integration with acquired subsidiaries have cut selection timetables from 18 months to 9 months. Vendors able to document payback in less than a year are winning against rivals still focused on bespoke customization. The market therefore tilts toward providers offering modular, API-first suites that enable rapid scale-up without infrastructure refreshes.

Growing Compliance Pressure on E-Invoicing and ESG Reporting

Belgium’s Peppol framework obliges public-sector suppliers to transmit structured invoices, eliminating PDF workflows and forcing thousands of SMEs to modernize accounting modules. The Corporate Sustainability Reporting Directive adds a mandatory layer of emissions and labor-practice disclosure, making real-time data capture in finance and supply-chain ledgers a non-negotiable requirement. Early movers that embed sustainability metrics directly inside general-ledger structures reduce manual reconciliation by about 40% and lock in competitive advantage as audit deadlines near. The Benelux enterprise resource planning market is therefore expanding fastest where compliance risk is highest.

Accelerated Digitalization Incentives from EU Recovery Funds

Belgium earmarked EUR 5.299 billion (USD 5.83 billion) for digital public administration, with up to 50% reimbursement for eligible ERP deployments. Dutch grants back municipal cloud migrations, shortening decision cycles and creating a consultant bottleneck that favors vendors with certified partner ecosystems. The subsidy window front-loads demand into 2026-2028, giving suppliers experienced in EU procurement frameworks a first-mover edge. As funds taper after 2028, vendors with a larger installed base will benefit from sticky subscription renewals.

Rising Integration of AI Copilots Into ERP Suites

Generative-AI assistants draft journal entries, surface procurement anomalies, and automate cash flow forecasts, trimming the month-end close by about 3 days.[2]Source: First-name Last-name, “Copilot for Finance General Availability,” Microsoft Corporation, microsoft.comCFOs view these copilots less as cost savers and more as insurance against staff turnover because they institutionalize tacit knowledge and reduce manual error. Incumbents that can host large language models within multi-tenant ERP stacks gain scale economies and regulatory control that open-source challengers cannot easily match. Consequently, the Benelux enterprise resource planning market rewards platforms that bundle AI without relying on external APIs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Switching Costs From Legacy Custom Solutions | -1.4% | Belgium and Netherlands multinational subsidiaries | Medium term (2-4 years) |

| Shortage of Skilled ERP Consultants | -1.2% | Acute in Netherlands, moderate in Belgium, limited pool in Luxembourg | Short term (≤ 2 years) |

| Cyber-Sovereignty Concerns Over Public Cloud | -0.8% | Government agencies in Belgium and Netherlands, Luxembourg finance | Long term (≥ 4 years) |

| Inflation-Driven IT Budget Caution Among SMEs | -0.7% | Manufacturing SMEs in Belgium and Netherlands | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Switching Costs from Legacy Custom Solutions

Localization investments in Belgian social security filings, Dutch payroll tax logic, and Luxembourg fund accounting rules often exceed USD 2 million per subsidiary. Enterprises face a dilemma between costly re-implementation and accepting functionality gaps that invite manual workarounds. Roughly half of ICT projects in the region report delays due to legacy complexity, so vendors offering automated code conversion and data migration tools accelerate deal velocity. Firms lacking such tooling lose momentum in the market because buyers now insist on capped migration risk.

Shortage of Skilled ERP Consultants in The Region

Nearly half of active projects report skills gaps, inflating timelines by up to 40% and pushing total cost above CFO approval thresholds. Scarcity is most severe in niche verticals such as Luxembourg fund administration, where domain and platform expertise must coincide. Vendors counter the labor crunch by shipping low-code configuration studios and pre-built industry templates that reduce the need for consultants. Platforms that still rely on extensive bespoke development encounter lengthening sales cycles, restraining overall Benelux enterprise resource planning market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Cloud-Native Suites Dominate, Edge Instances Gain Speed

Cloud-native suites accounted for 62.73% of 2025 revenue and will expand at a 10.48% CAGR, underpinned by vendor roadmaps that bundle finance, supply chain, and HCM into a single contract. The Benelux enterprise resource planning market for two-tier or edge ERP is currently smaller; however, it is experiencing rapid growth, as manufacturers increasingly deploy edge nodes on factory floors for latency-sensitive execution. Vendors re-platforming legacy code to multi-tenant architectures are racing to protect installed bases, while API-first challengers integrate easily with warehouse automation and e-commerce add-ons. Two-tier growth therefore enlarges, rather than cannibalizes, overall market share by unlocking new shop-floor and remote-site use cases.

Mobile-first ERP and social or collaborative suites add further momentum by extending workflows to frontline workers and project teams that operate outside the traditional back office. Field technicians in utilities and telecom companies now approve work orders and update inventory from smartphones, eliminating the lag that once plagued paper-based processes. Collaborative suites embed chat, document sharing, and workflow orchestration inside the ERP screen, shrinking email volume and reducing cycle time on proposal approvals, design reviews, and procurement exceptions. Because these user-experience upgrades raise daily engagement, they limit shelf-ware risk and improve renewal rates, which in turn supports the premium pricing that SaaS vendors command.

By Business Function: Finance Leads, Manufacturing Execution Accelerates

Finance and accounting modules delivered 53.47% of 2025 revenue, driven by real-time statutory reporting and cross-border VAT automation across three jurisdictions. Manufacturing execution applications add IoT sensor data and quality traceability, posting a 10.68% CAGR that outstrips every other function. Omnichannel retail strategies maintain a significant share for customer relationship and commerce, while human capital management is experiencing steady growth due to complex labor laws and the adoption of self-service workforce portals. Pre-integrated data models covering finance, supply chain, and HCM improve upsell velocity and expand the Benelux enterprise resource planning market for full-suite providers.

Supply-chain and operations modules are becoming the focal point of AI pilot projects that optimize safety-stock targets and reschedule transport in real time when ports experience congestion or strikes. Human capital teams are layering skills-taxonomy engines onto core HR data, building internal talent marketplaces that match open roles with employees trained on new production systems. Customer-facing teams, meanwhile, use unified product, inventory, and credit data to quote accurate delivery dates during live sales calls, reducing order cancellations.

By Deployment Model: Cloud Climbs, On-Premise Slows

Cloud captured 34.60% of 2025 revenue and will grow at a 11.08% CAGR as vendors retire on-premises support and bundle regulatory updates into subscription fees. Consultant shortages and longer hardware refresh cycles raise project costs for on-prem replacements by a moderate share, curbing demand despite the still-large installed base. Hybrid strategies that retain on-premises statutory ledgers while spinning up cloud modules for analytics address compliance and sovereignty concerns. The Benelux enterprise resource planning market share of on-premise models will therefore erode steadily but not disappear in heavily regulated verticals.

In the cloud, customers are experimenting with regional sovereign-cloud zones that store encryption keys locally and allow auditors to conduct on-site inspections, satisfying DORA and Schrems II requirements without reverting to full on-premises systems. Some enterprises adopt a multi-cloud pattern, running finance on one hyperscaler and manufacturing analytics on another, to spread vendor risk and exploit specialized GPU capacity for AI co-pilots. Subscription contracts now include uptime rebates tied to business-hour service-level agreements rather than generic monthly availability, reflecting the mission-critical nature of invoice clearance under Peppol.

By Organization Size: SMEs Outpace, Enterprises Consolidate

Small and medium enterprises accounted for 38.8% of 2025 revenue and will expand at a 11.78% CAGR as open-source and low-code suites eliminate upfront license costs. Funding of EUR 500 million (USD 550 million) in 2024 enabled a Belgian challenger to scale billings to EUR 1 billion by 2027, underscoring the appetite among cost-sensitive buyers. Large enterprises continue to have complex consolidation needs, and their growth rates are slower than those of small and medium-sized enterprises due to longer decision cycles and the extensive customization required, which delays deployment. Two-tier rollouts let headquarters protect core platforms while subsidiaries adopt lighter cloud solutions, increasing overall Benelux enterprise resource planning market penetration without cannibalizing incumbent revenue.

SMEs are also driving innovation in payment models, favoring month-to-month subscriptions with usage-based tiers for seasonal industries such as horticulture and tourism. Vendors cater to this preference by launching click-to-configure marketplaces where buyers activate payroll or e-commerce extensions with a single toggle, bypassing lengthy statement-of-work negotiations. Meanwhile, large enterprises intensify focus on data governance and master-data management as they merge newly acquired subsidiaries, a task complicated by divergent local tax codes and sustainability metrics.

By Industry Vertical: Manufacturing Leads, Healthcare Surges

Manufacturing accounted for 37.50% of 2025 revenue and will post an 11.68% CAGR as aging workforces drive automation of production scheduling and predictive maintenance. Healthcare and life sciences are expected to grow significantly as hospitals digitize supply chains and integrate patient records. Retail and e-commerce are also expanding steadily as omnichannel strategies require unified inventory views. Public-sector grants are driving growth in this area, while adoption in the banking, financial services, and insurance sector is progressing more slowly due to stringent data-sovereignty rules. Vertical templates that reduce implementation risks are therefore crucial to the development of the Benelux enterprise resource planning market.

The IT and telecom sector is piloting edge-enabled ERP nodes that synchronize billing events with 5G network slices, creating reference architectures that later migrate to manufacturing and logistics. Construction firms increasingly embed progress-billing milestones into project accounting modules to manage cash flow on multi-year infrastructure programs funded by the EU Recovery Facility. In government, the spread of smart-city initiatives is tying traffic data and utility consumption directly into ERP procurement ledgers to trigger demand-based replenishment of spare parts.

Geography Analysis

The Netherlands delivered 49.3% of 2025 revenue and will expand at a 9.7% CAGR as pervasive broadband, M&A activity, and a deep reseller network keep cloud pipelines full. Belgium accounted for a significant share of revenue but experienced slower growth due to linguistic fragmentation and high legacy-system inertia, which slowed migration. Luxembourg contributed a smaller share of the revenue but is expected to grow at the fastest rate as banks and fund administrators prepare for DORA-mandated incident reporting and third-party risk management. Visma, a Norwegian software conglomerate, acquired WeFact, a Dutch invoicing and subscription-management platform, in February 2026, and had previously acquired TimeChimp and Bizzcontrol in late 2024, consolidating its position in the Dutch SME market and cross-selling payroll, time-tracking, and financial-planning modules into unified SaaS bundles.[3]Source: First-name Last-name, “WeFact Acquisition February 2026,” Visma A/S, visma.com

Dutch buyers also benefit from a competitive fintech ecosystem that plugs open banking APIs into ERP cash management dashboards, shortening the cash conversion cycle for exporters handling multi-currency flows. Regional airports in Eindhoven and Rotterdam are digitizing maintenance and ground-handling contracts inside project-accounting modules, showcasing how transportation investments spill into ERP modernization. In addition, Dutch universities act as testbeds for AI copilots that recommend grant-budget reallocations, feeding a steady stream of analytics talent into the vendor partner channel and reinforcing the Netherlands

Belgium’s tri-lingual governance adds cost and complexity, yet it also creates a service niche for vendors that pre-package Flemish, French and German language packs alongside localized chart-of-account templates. Municipalities leveraging Recovery Facility grants must choose platforms certified for Peppol and CSRD out of the box, effectively narrowing the vendor shortlist and raising win ratios for suppliers with reference sites in the public sector. The mining of lithium in Belgian Congo subsidiaries further complicates supply-chain traceability, driving manufacturers headquartered in Antwerp and Ghent to roll out ESG-ready modules that map upstream emissions and labor practices.

Competitive Landscape

The Benelux enterprise resource planning market remains moderately concentrated: SAP, Microsoft, Oracle, Unit4, and Infor together held 75% of 2025 revenue. Incumbents benefit from local-language support, vertical templates, and dense partner ecosystems, yet face pricing pressure from open-source and low-code rivals. A Belgian challenger raised EUR 500 million (USD 550 million) in late 2024 and targets EUR 1 billion revenue by 2027, signaling investor confidence in modular SaaS that minimizes consultant dependency.[4]Source: First-name Last-name, “Odoo Secures EUR 500 Million Funding Round,” TechCrunch, techcrunch.com

Visma’s February 2026 purchase of Dutch invoicing vendor WeFact, following earlier buys of TimeChimp and Bizzcontrol, shows a roll-up model aimed at bundling payroll, time tracking, and accounting into a unified suite. Competitive white space exists in AI-powered financial planning tools for mid-market CFOs and industry-specific bundles for healthcare providers needing pharmaceutical traceability. Buyer priorities emphasize the containment of implementation risk over feature novelty, maintaining an advantage for platforms with proven delivery records.

SAP defends its share by deepening industry editions that bundle MES, PLM, and sustainability calculators into S/4HANA Cloud, framing migrations as regulatory risk mitigation rather than an optional refresh. Microsoft expands through partner co-sell motions that blend Dynamics 365 with Azure confidential-compute regions, using joint reference architectures to calm soverits industry editions, bundling MES, PLM, and sustainability calculators into S/4HANA Cloud, and eignty concerns in public sector tenders. Oracle targets CFO pain points with Autonomous Database features that patch and tune without downtime, reducing reliance on scarce DBAs and tilting total cost comparisons in its favor. These strategic pivots underscore a broader trend: vendors compete as much on deployment assurance and managed services as on pure feature count in the market.

Benelux Enterprise Resource Planning Industry Leaders

SAP SE

Microsoft Corporation

Oracle Corporation

Unit4 N.V.

Infor Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Visma acquired WeFact, a Dutch invoicing and subscription management platform, strengthening cross-sell potential in the Netherlands' SME segment.

- January 2026: Microsoft released Copilot for Finance at general availability, automating variance analysis and cash flow forecasting while trimming month-end close cycles by about 3 days.

- January 2026: Oracle upgraded Fusion Cloud ERP with agentic AI that reclassifies expense reports and flags duplicate vendor invoices before payment processing.

- September 2025: Aptean launched its Foundation Bundle for Benelux food and beverage manufacturers, integrating ERP, MES, and quality modules into a single subscription aligned with HACCP rules.

Benelux Enterprise Resource Planning Market Report Scope

The Benelux enterprise resource planning (ERP) market encompasses the adoption and implementation of ERP systems across various industries in Belgium, the Netherlands, and Luxembourg. These systems integrate core business processes, including finance, supply chain, human resources, and customer relationship management, to enhance operational efficiency and decision-making.

The Benelux Enterprise Resource Planning Market Report is Segmented by Type (Cloud-Native Suite, Mobile-First ERP, Social/Collaborative ERP, and Two-Tier/Edge ERP), Business Function (Finance and Accounting, Supply Chain and Operations, Human Capital Management, Customer Relationship and Commerce, and Manufacturing Execution and Quality), Deployment Model (On-Premise, and Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (Manufacturing, Retail and E-commerce, BFSI, Government and Public Sector, IT and Telecom, Healthcare and Life Sciences, Other Industry Verticals), and Geography (Belgium, Netherlands, Luxembourg). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Native Suite |

| Mobile-First ERP |

| Social / Collaborative ERP |

| Two-Tier / Edge ERP |

| Finance and Accounting |

| Supply-Chain and Operations |

| Human Capital Management |

| Customer Relationship and Commerce |

| Manufacturing Execution and Quality |

| On-Premise |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| Manufacturing |

| Retail and E-commerce |

| BFSI |

| Government and Public Sector |

| IT and Telecom |

| Healthcare and Life Sciences |

| Others Industry Vertical |

| By Type | Cloud-Native Suite |

| Mobile-First ERP | |

| Social / Collaborative ERP | |

| Two-Tier / Edge ERP | |

| By Business Function | Finance and Accounting |

| Supply-Chain and Operations | |

| Human Capital Management | |

| Customer Relationship and Commerce | |

| Manufacturing Execution and Quality | |

| By Deployment Model | On-Premise |

| Cloud | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Industry Vertical | Manufacturing |

| Retail and E-commerce | |

| BFSI | |

| Government and Public Sector | |

| IT and Telecom | |

| Healthcare and Life Sciences | |

| Others Industry Vertical |

Key Questions Answered in the Report

How large is the Benelux Enterprise Resource Planning market in 2026?

The market is projected to reach USD 1.44 billion in 2026.

What is the expected CAGR for Benelux ERP spending from 2026 to 2031?

Spending is forecast to grow at 9.68% over the 2026-2031 period.

Which deployment model is growing fastest in Benelux?

Cloud subscriptions are expanding at a 11.08% CAGR, outpacing on-premise replacements.

Why are SMEs accelerating ERP adoption in Benelux?

Subscription pricing removes upfront license costs and EU grants cover up to 50% of project spend, driving a 12.9% CAGR among SMEs.

Which industry vertical leads ERP demand across the region?

Manufacturing commands the largest 37.50% share and posts an 11.68% CAGR through 2031.

How concentrated is vendor competition in Benelux?

The five largest providers together hold 75% share, resulting in a moderate concentration score of 7.

Page last updated on: