Benchtop Laboratory Water Purifier Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

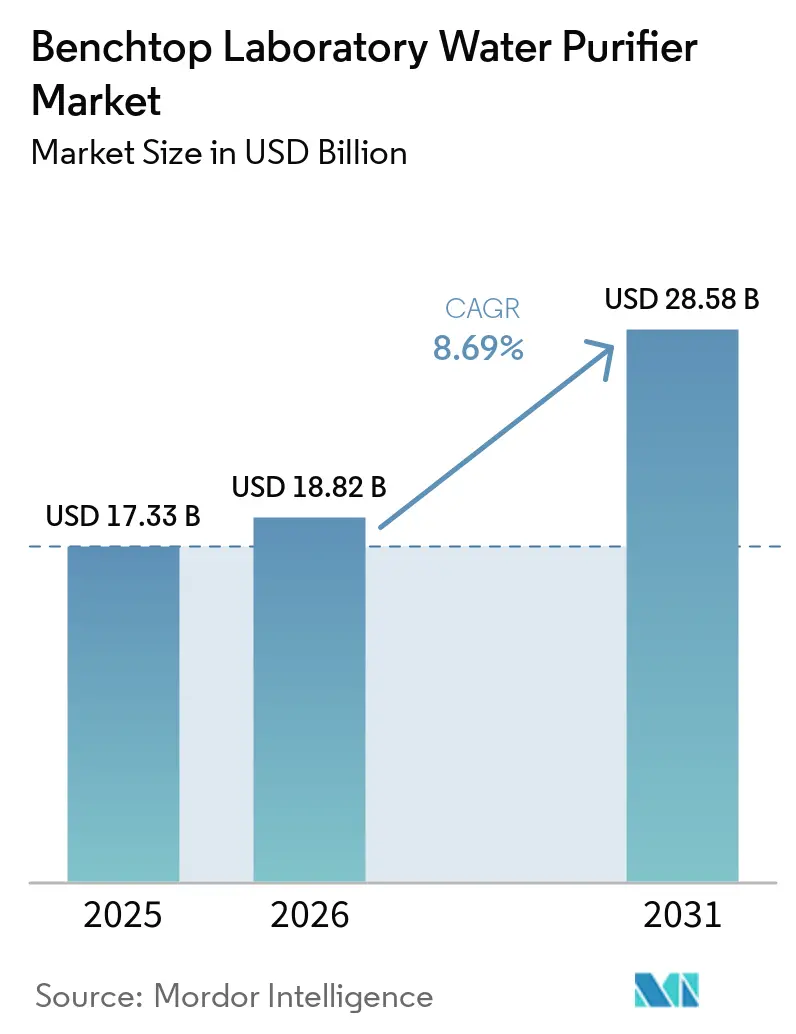

| Market Size (2026) | USD 18.82 Billion |

| Market Size (2031) | USD 28.58 Billion |

| Growth Rate (2026 - 2031) | 8.69% CAGR |

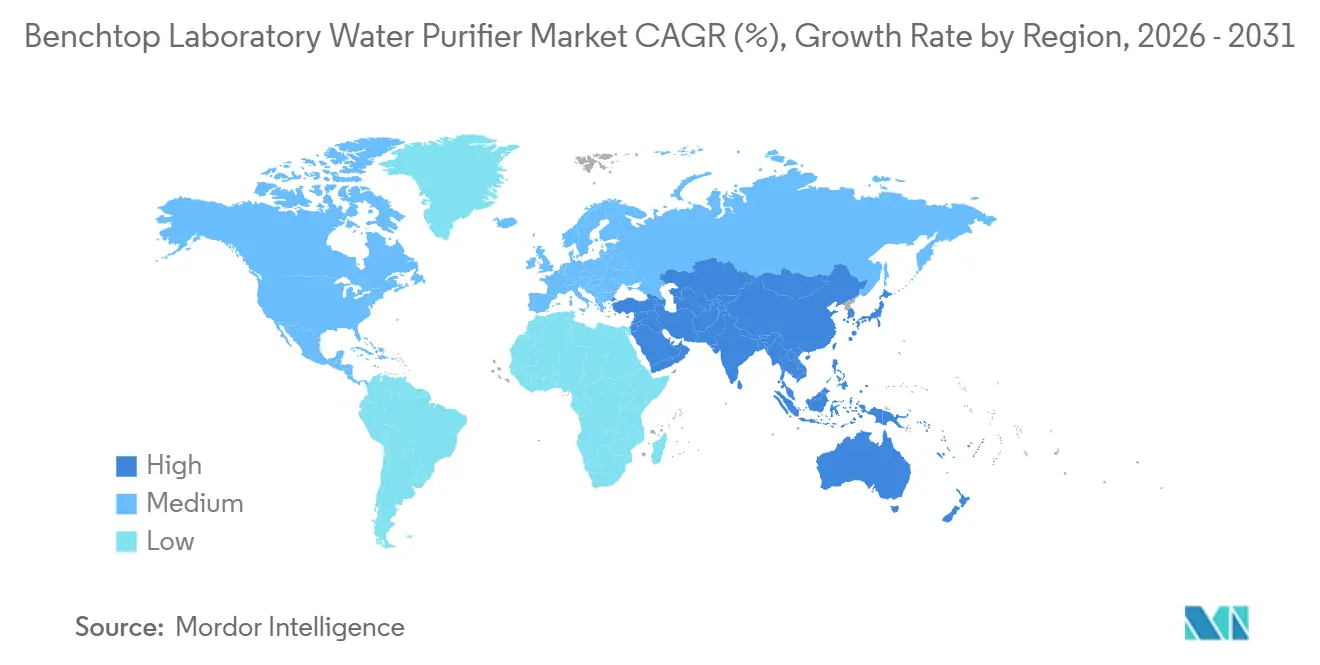

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

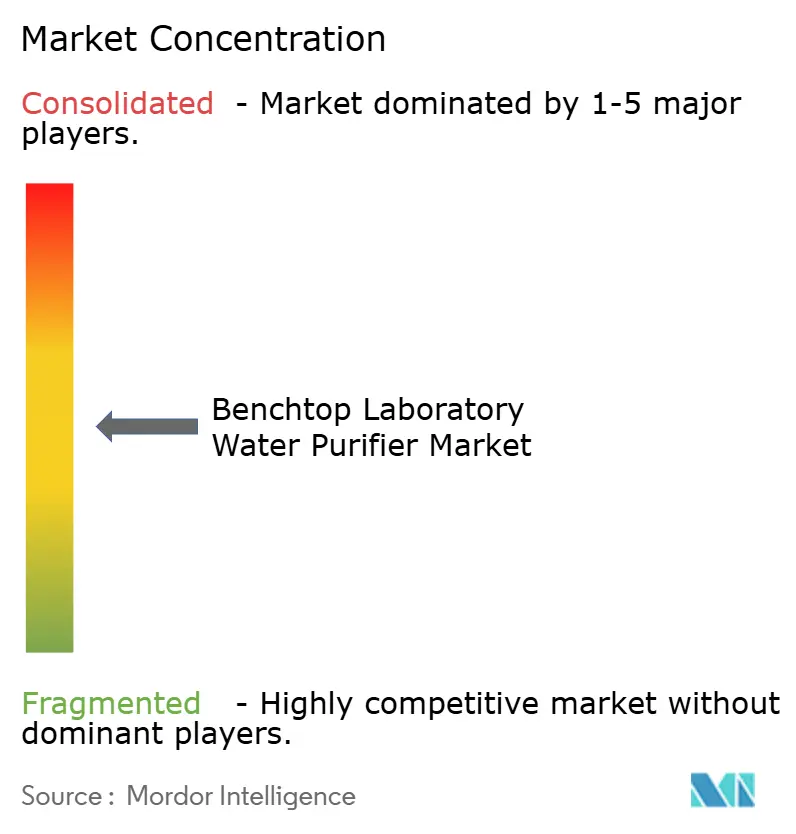

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Benchtop Laboratory Water Purifier Market Analysis by Mordor Intelligence

The Benchtop Laboratory Water Purifier Market size is expected to grow from USD 17.33 billion in 2025 to USD 18.82 billion in 2026 and is forecast to reach USD 28.58 billion by 2031 at 8.69% CAGR over 2026-2031.

In India, Brazil, and the U.S., pharmaceutical clean-room buildouts are incorporating benchtop systems into modular suites. At the same time, academic core facilities are replacing central reverse-osmosis loops with compact dispensers that reduce biofilm risks and minimize loop-sanitation downtime. Multinational drug manufacturers are adopting the 2025 shift in the Chinese Pharmacopoeia to membrane-based water-for-injection. This transition enables the standardization of global qualification procedures and the elimination of energy-intensive distillation skids. Semiconductor R&D centers in Taiwan, South Korea, Germany, and Arizona are setting strict requirements, demanding sub-0.055 µS/cm conductivity for extreme-ultraviolet lithography photoresist preparation. Meeting this standard has been challenging for legacy central plants, often requiring costly recirculation polishers. The industry is also moving toward smart, IoT-enabled dispensers with predictive maintenance dashboards. This trend is driving procurement decisions to focus on lifetime performance rather than upfront capital costs, strengthening the aftermarket cartridge revenue model for global vendors.

Key Report Takeaways

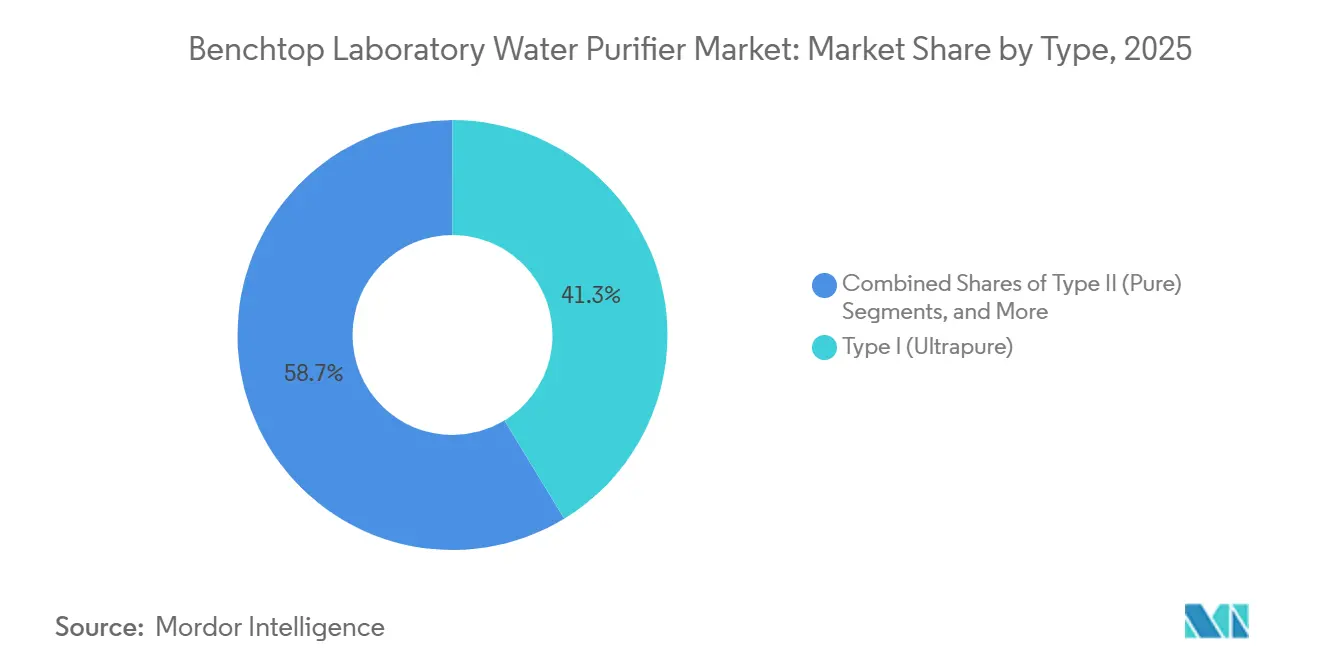

- By type, type I ultrapure systems led with 41.30% of the benchtop laboratory water purifier market size in 2025 and are on course for a 9.87% CAGR through 2031.

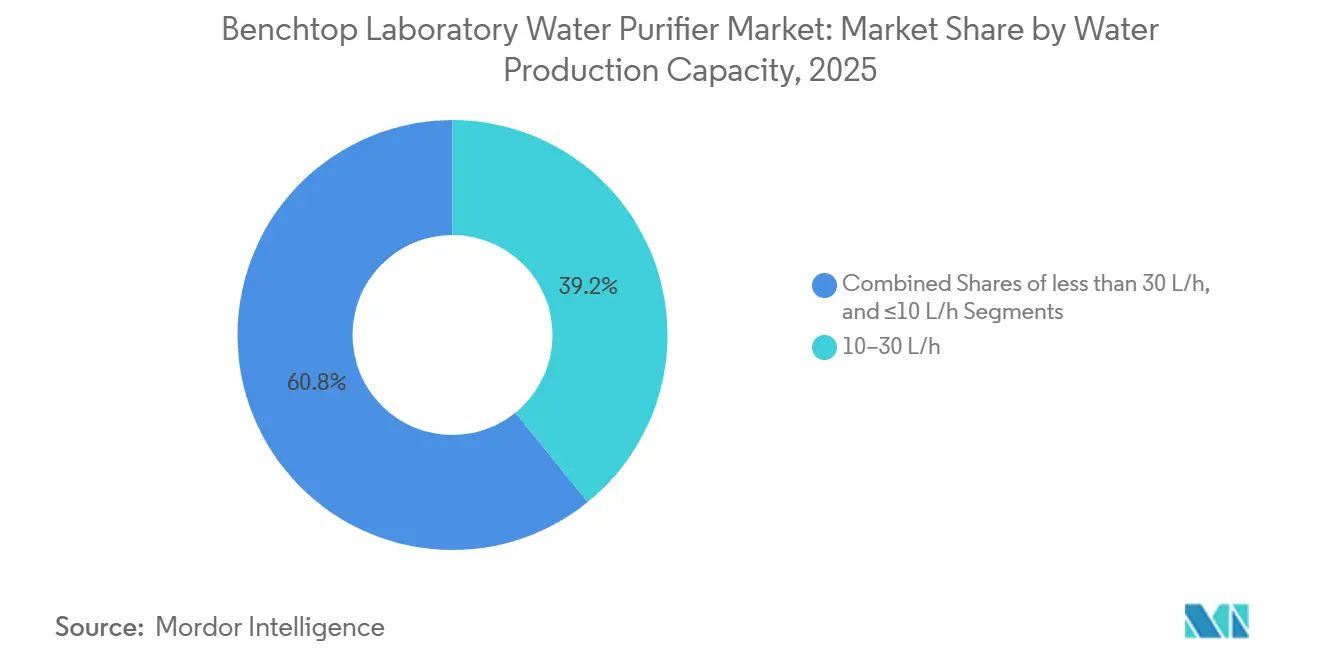

- By capacity, 10–30 liter-per-hour units represented 39.17% of 2025 revenue, while systems above 30 L/h are forecast to expand at 9.51% CAGR to 2031.

- By end-user industry, pharmaceuticals and biotechnology commanded 60.43% of the benchtop laboratory water purifier market share in 2025.

- By technology, ultrafiltration is the fastest-growing process, advancing at 9.66% CAGR between 2026 and 2031.

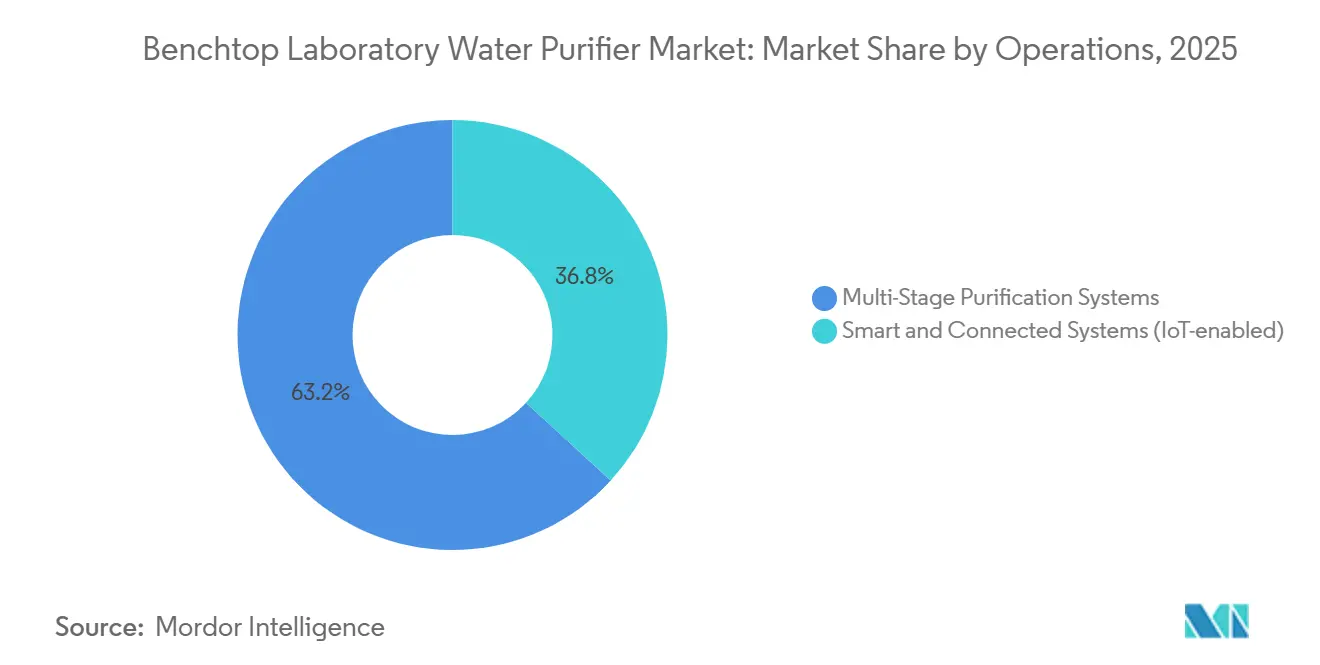

- By operations, the multi-stage purification system holds a 63.15% share in 2025.

- By geography, Asia-Pacific is the quickest-expanding region, set for a 7.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Benchtop Laboratory Water Purifier Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Capital-intensive pharmaceutical & biotech capacity additions | +2.1% | Global, with concentration in North America, Europe, and Asia-Pacific (China, India) | Medium term (2-4 years) |

| Tightening global pharmacopeia purity standards for lab water | +1.8% | Global (USP, EP, JP, ChP harmonization) | Long term (≥ 4 years) |

| Rapid expansion of cell-&-gene-therapy cleanrooms | +1.5% | North America & Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Boom in semiconductor R&D pilot fabs requiring ultrapure bench systems | +1.2% | Asia-Pacific (Taiwan, South Korea, Japan), North America (Arizona, Texas) | Short term (≤ 2 years) |

| Academic lab shift from central RO loops to point-of-use benchtop units | +0.9% | Global, led by North America and Europe | Medium term (2-4 years) |

| Decentralized micro-brewery QA labs adopting ASTM type-I systems | +0.6% | North America, Europe, Asia-Pacific (craft brewery hubs) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive Pharmaceutical & Biotech Capacity Additions

Biologic drug manufacturers are incorporating benchtop ultrapure modules into each clean-room suite to provide validated water on demand for media preparation, buffer pools, and sterile fill-finish steps, while preventing cross-suite contamination. Roquette’s São Paulo innovation center, which opened in 2025, follows this model by using multiple 20 L/h dispensers instead of a single central loop, significantly reducing downtime during sanitization cycles. This modular approach aligns with India’s Production Linked Incentive scheme and Brazil’s innovation tax credits, both of which encourage the rapid scale-up of single-use bioreactor lines. Point-of-use qualification simplifies validation processes, as each dispenser can be documented as an independent utility. Additionally, Kincell Bio’s 2026 gene-therapy expansion employs cartridge-based Type I systems in every Grade A isolator bay, eliminating 15 m of dead-leg piping per suite and reducing potential biofilm surface area by 42%.

Tightening Global Pharmacopeia Purity Standards for Lab Water

The 2025 Chinese Pharmacopoeia introduced significant updates by allowing water-for-injection through membrane separation, moving away from the distillation-only requirement and aligning with international standards. It also implemented multi-stage conductivity tests to detect sodium or ammonium breakthroughs in real time. Further, the NMPA’s March 2026 guidance mandated lifecycle microbial control and online total-organic-carbon monitoring for pharmaceutical water loops.[1]China Food and Drug Administration, cnpharm.com Source: “GP40 5th Edition,” Clinical and Laboratory Standards Institute, clsi.org ASTM raised its D1193 Type I criteria to ≥ 18.2 MΩ·cm resistivity and < 5 ppb TOC, a standard consistently met only by electrodeionization-plus-UV units. As a result, laboratories replacing glass stills are adopting advanced smart benchtop systems equipped with conductivity probes, TOC cells, and cloud logging capabilities, ensuring compliance with stringent regulatory audits.[2]IoT-Based Reverse Osmosis Monitoring System with LSTM,” Journal of Electrical Systems, journal.esrgroups.org

Rapid Expansion of Cell-&-Gene-Therapy Cleanrooms

Autologous CAR-T facilities require water with sub-0.001 EU/mL endotoxin levels and must eliminate nuclease carryover to protect viral vectors. The CLSI GP40 5th edition, released in December 2024, introduced a new special reagent water class to meet these requirements.[3]GP40 5th Edition,” Clinical and Laboratory Standards Institute, clsi.org To achieve these standards, clean-room builders are specifying 0.05 µm hollow-fiber ultrafiltration combined with dual-wavelength UV oxidation. Benchtop positioning eliminates the need for 10–20 m of stainless piping, which can accumulate biofilm, while modular cabinets allow for replacements without disrupting adjacent suites. Kincell Bio validated this configuration in 2026 and reported zero microbial excursions during six months of post-qualification monitoring.

Boom in Semiconductor R&D Pilot Fabs Requiring Ultrapure Bench Systems

Extreme-ultraviolet R&D lines for photoresist and GAA transistor steps require ultrapure water with 18.2 MΩ·cm resistivity and less than 1 ppb TOC. Pilot fabs in Arizona, Dresden, and Hsinchu have installed benchtop electrodeionization units directly in analytical metrology labs, as central UPW plants are not cost-effective for supplying the 30 L/day needed for research bays. TSMC’s Arizona Phase 2 and H+E Group’s 2025 German cleanroom projects included 15 L/h dispensers with inline ion-chromatography sensors, while GnG InTech’s Korean pilot line adopted similar systems. The point-of-use approach offers a payback period of under 18 months and allows engineers to reroute benches weekly without requiring loop extensions.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High service & cartridge-replacement OPEX | -1.4% | Global, acute in price-sensitive academic and small-lab segments | Long term (≥ 4 years) |

| Competition from refurbished / second-hand instruments | -0.8% | North America, Europe (mature markets with active secondary equipment channels) | Medium term (2-4 years) |

| Lab-on-chip devices reducing overall reagent-grade water demand | -0.9% | Europe and Asia | Long term (≥ 4 years) |

| PFAS disposal regulations raising waste-handling costs | -1.9% | North America, Europe and Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Service & Cartridge-Replacement OPEX

Consumables account for 18–22% of a benchtop unit’s purchase price annually. RO membranes are priced between USD 500–1,200 per pair, electrodeionization stacks cost USD 300–800, and UV lamps range from USD 150–400. OEMs incorporate electronic chips to restrict the use of third-party cartridges, significantly increasing the cost of ion-exchange resin by 200–300%. A 20 L/h dispenser in a mid-sized QC lab incurs annual expenses of USD 3,500–5,500, excluding emergency call-outs. Universities are now extending replacement intervals from 24 to 30 months, which raises the risk of out-of-spec runs.

Competition from Refurbished / Second-Hand Instruments

In 2024, American Laboratory Trading acquired FAMECO, enabling the sale of certified pre-owned Thermo Barnstead units at discounts of 40–60%. In 2025, LabX listed 47 used ELGA PureLab dispensers priced between USD 3,495–5,995, compared to new units costing USD 8,000–12,000. European resellers, such as Richmond Scientific, are offering six-month warranties with refurbished models, delaying new purchases across Western Europe. Although refurbished units lack features like IoT dashboards or cartridge authentication, cost-conscious customers are opting for manual logging to reduce expenses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Ultrapure Dominance Driven by Analytical Precision

In 2025, Type I ultrapure platforms accounted for 41.30% of the Benchtop laboratory water purifier market share and are projected to grow at a 9.87% CAGR through 2031. Laboratories utilizing high-performance liquid chromatography and ICP-MS require standards of ≥ 18.2 MΩ·cm resistivity and < 5 ppb TOC, which older Type II systems cannot meet. The market size for Type I units in the Benchtop laboratory water purifier sector is expected to reach USD 11.4 billion by 2031. The transition is further driven by PFAS-free construction mandates, replacing fluoropolymer tubing with PEEK or stainless alternatives to maintain undetectable fluoride levels. While Type II and Type III systems continue to serve autoclaves and glasswashers, they are losing market share as laboratory workflows become increasingly instrument-intensive.

By Technology: Ultrafiltration Gains on Endotoxin Control

Ultrafiltration revenue is growing at a 9.66% CAGR, outpacing the Benchtop laboratory water purifier industry average. This growth is attributed to the effectiveness of 0.05-µm hollow-fiber cassettes in reducing endotoxin levels to < 0.001 EU/mL. Reverse osmosis maintained a 35.8% revenue share in 2025 and remains the primary choice for dissolved salts. However, combined RO-E-DI-UF stacks are increasingly offered as single cabinets, eliminating the need for buyers to evaluate technologies separately. UV oxidation at 185 nm effectively breaks down organics, while 254 nm ensures microbial sterility. The integration of these four-stage processes meets the stringent reagent water standards required by CLSI GP40, particularly for molecular biology and cell-therapy laboratories.

By Water Production Capacity: Mid-Range Dominates, High-Capacity Accelerates

Units rated at 10–30 L/h contributed 39.17% of 2025 revenue, aligning with the water requirements of five to ten LC-MS or UHPLC instruments. These systems are widely used in quality-control labs at generics plants, academic flow-cytometry centers, and municipal environmental facilities. The market size for this capacity tier is projected to exceed USD 11 billion by 2031. Meanwhile, systems rated above 30 L/h are experiencing the fastest growth at a 9.51% CAGR, driven by contract research organizations consolidating analytics into centralized hubs with over 20 instruments operating continuously. Vendors are addressing this demand with modular racks that allow 40 L/h pods to be daisy-chained, enabling phased capacity expansion without disrupting floor plans. Smaller units, rated ≤ 10 L/h, remain relevant for research benches or DNA preparation stations requiring Type I water but consuming only 15 L/day.

By End-Use Application: Pharma Leads, F&B QC Surges

The pharmaceutical and biotech sectors accounted for 60.43% of 2025 revenue, driving growth through advancements in gene therapy and vaccine development. Their reliance on water-for-injection standards aligns with the capabilities of Type I systems. Meanwhile, quality-control labs in the food and beverage sector are experiencing the fastest growth at a 7.56% CAGR. Facilities such as craft breweries, bottled-water plants, and dairy processors are increasingly using ASTM Type I water for PFAS quantification and multi-element ICP-MS allergen screenings. The market size for Benchtop laboratory water purifiers in food and beverage labs is expected to double, growing from USD 0.9 billion in 2026 to nearly USD 1.8 billion by 2031. Clinical-diagnostic laboratories are also upgrading their systems, as high-sensitivity troponin assays detect organic contaminants that can affect photometric module performance.

By Operations: Smart Systems Gain on Predictive Maintenance

Modern multi-stage systems integrating RO, electrodeionization, UV, and UF technologies now feature edge-computing boards and connectivity options such as Bluetooth or Wi-Fi. Vendors are leveraging cloud dashboards to monitor conductivity and TOC levels, using anomaly detection to signal cartridge exhaustion before water quality is compromised. In 2026, predictive maintenance was implemented across fleets to achieve 99.9% uptime and significantly reduce manual testing. A prototype developed in 2025 demonstrated the potential of low-cost electronics in ensuring compliance, showcasing sub-1 µS/cm resolution. As laboratories increasingly automate reagent quality control, smart systems are capturing market share from traditional analog dispensers that lack audit-ready data export capabilities.

Geography Analysis

In 2025, North America secured a dominant 39.67% share of the benchtop laboratory water purifier market. The FDA's emphasis on quality-by-design mandates electronic logging of resistivity and TOC, prompting upgrade cycles for Barnstead and Milli-Q. In a strategic move, Thermo Fisher acquired Solventum's Purification & Filtration assets for USD 4.0 billion in 2025, integrating battery-grade and medical-device water lines into the expanded Barnstead portfolio. While university refurb channels moderate new sales, aftermarket cartridges flourish, especially as OEM firmware locks dispensers to proprietary packs. In Massachusetts and North Carolina, hubs for gene and cell therapy, every Grade B side room now features UF-equipped Type I stacks.

Asia-Pacific is set to lead with a robust 7.90% CAGR through 2031. China's March 2026 Guidelines for Inspection of Pharmaceutical Water, emphasizing online microbial trending, are pushing hospitals and CDMOs to transition from distillers to membrane stacks. In India, the second tranche of the Production Linked Incentive backs 70 new biologics plants, each integrating six to eight 20 L/h dispensers. Semiconductor hubs in Taiwan, South Korea, and Japan are procuring bench units that mimic central UPW chemistry for their R&D divisions. Meanwhile, as PFAS regulations tighten, craft-beer quality labs in Australia and Vietnam are retrofitting point-of-use Type I units.

Europe, led by Germany, the UK, and France, stands as the second-largest market by value. With the harmonization of EP Chapter 0169 streamlining validation, energy-conscious labs are gravitating towards RO-based dispensers boasting over 60% water recovery, aligning with corporate net-zero ambitions.

Competitive Landscape

Merck KGaA (Milli-Q), Thermo Fisher (Barnstead), Sartorius AG (Arium), and Veolia Water Technologies (ELGA LabWater) collectively dominate the benchtop laboratory water purifier market, holding a majority share. These industry giants are enhancing their offerings with IoT telemetry, electronic cartridge authentication, and extended service packages. In June 2024, Sartorius unveiled its Arium Mini Extend, featuring a handheld dispenser and a 5 L bag-tank, catering to space-constrained benches Pall Corporation's Cascada line, equipped with inline TOC, intelligent dispensing, and FDA validation packages, is positioning itself as a formidable competitor with its compliance-centric features. Purific Australia is disrupting the market by providing open-platform resin packs and AI diagnostics, successfully clinching contracts with local biobanks.

In a bid for vertical integration, global vendors are making strategic moves: Thermo Fisher has incorporated Solventum's filtration to cater to semiconductor UPW and battery electrodewashing needs. Merck is seamlessly integrating Milli-Q into M-Ventures' smart-lab cloud, creating a synergy between water data and chromatography instruments. Sartorius is bundling Arium with single-use bioreactor kits, crafting a comprehensive ecosystem for its clients. Meanwhile, regional players like Rephile Bioscience are carving a niche in Asia, thriving on competitive pricing and swift service. The rising demand for PFAS-free solutions has birthed niche startups, delivering specialized PEEK-tubed systems tailored for environmental labs.

Benchtop Laboratory Water Purifier Industry Leaders

Evoqua Water Technologies

Thermo Fisher Scientific Inc.

Merck KGaA (Milli-Q)

Sartorius AG (Arium)

Aqua Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: China’s NMPA unveiled its 2026 Medical Device Standards Revision Plan covering 80 standards, including purified water for IVD reagents and hemodialysis equipment, signaling new purity benchmarks.

- October 2025: Roquette inaugurated its São Paulo Pharmaceutical Innovation Center with modular clean-rooms equipped with benchtop water systems for excipient R&D.

- September 2025: Thermo Fisher finalized the USD 4.0 billion acquisition of Solventum’s Purification & Filtration business, adding battery-grade and semiconductor water lines to Barnstead.

Global Benchtop Laboratory Water Purifier Market Report Scope

As per the scope of the report, a benchtop laboratory water purifier is a compact, countertop device designed to produce high-purity water (Types I, II, or III) by removing contaminants like dissolved solids, organics, and microorganisms. These systems use technologies such as reverse osmosis, ion exchange, and UV light to supply purified water for applications ranging from glassware rinsing to sensitive molecular biology.

The benchtop laboratory water purifier market is segmented by type, technology, water production capacity, end-use application, operations, and geography. By type, the market includes Type I (Ultrapure), Type II (Pure), and Type III (RO/Primary). By technology, it is segmented into Reverse Osmosis (RO), Electrodeionization / Ion Exchange, UV Oxidation & UV Sterilization, and Ultrafiltration (UF). By water production capacity, the categories include ≤10 L/h, 10–30 L/h, and >30 L/h. By end-use application, the market is divided into pharmaceuticals & biotechnology, clinical & diagnostic laboratories, academic & research institutes, environmental & industrial testing, and food & beverage QC laboratories. By operations, it is segmented into multi-stage purification systems and smart & connected systems (IoT-enabled). By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Type I (Ultrapure) |

| Type II (Pure) |

| Type III (RO/Primary) |

| Reverse Osmosis (RO) |

| Electrodeionization / Ion Exchange |

| UV Oxidation & UV Sterilization |

| Ultrafiltration (UF) |

| ?10 L/h |

| 10-30 L/h |

| >30 L/h |

| Pharmaceuticals & Biotechnology |

| Clinical & Diagnostic Laboratories |

| Academic & Research Institutes |

| Environmental & Industrial Testing |

| Food & Beverage QC Laboratories |

| Multi-Stage Purification Systems |

| Smart & Connected Systems (IoT-enabled) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Type I (Ultrapure) | |

| Type II (Pure) | ||

| Type III (RO/Primary) | ||

| By Technology | Reverse Osmosis (RO) | |

| Electrodeionization / Ion Exchange | ||

| UV Oxidation & UV Sterilization | ||

| Ultrafiltration (UF) | ||

| By Water Production Capacity | ?10 L/h | |

| 10-30 L/h | ||

| >30 L/h | ||

| By End-use Application | Pharmaceuticals & Biotechnology | |

| Clinical & Diagnostic Laboratories | ||

| Academic & Research Institutes | ||

| Environmental & Industrial Testing | ||

| Food & Beverage QC Laboratories | ||

| By Operations | Multi-Stage Purification Systems | |

| Smart & Connected Systems (IoT-enabled) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the Benchtop laboratory water purifier market be by 2031?

The Benchtop laboratory water purifier market size is forecast to reach USD 28.58 billion by 2031, expanding at an 8.69% CAGR from 2027.

Which segment holds the largest Benchtop laboratory water purifier market share today?

Pharmaceutical and biotechnology laboratories account for 60.43% of global revenue because cell-and-gene therapy, HPLC, and sterile formulation workflows need Type I water.

Why is ultrafiltration gaining momentum in benchtop purifiers?

Ultrafiltration membranes remove endotoxin to < 0.001 EU/mL, matching new CLSI GP40 criteria for molecular-biology reagent water, which drives the fastest segment CAGR of 9.66%.

What drives Asia-Pacific demand for benchtop laboratory water purifiers?

China's 2025 pharmacopoeia harmonization, India's Production Linked Incentive plants, and semiconductor pilot fabs in Taiwan, South Korea, and Japan are boosting regional CAGR to 7.90% .

How are suppliers differentiating in a moderately concentrated market?

Leading vendors embed IoT telemetry, predictive maintenance, and cartridge authentication, while emerging players offer PFAS-free construction and open-platform consumables to cut total cost of ownership.

Page last updated on: