Behavioral Health Care Software and Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

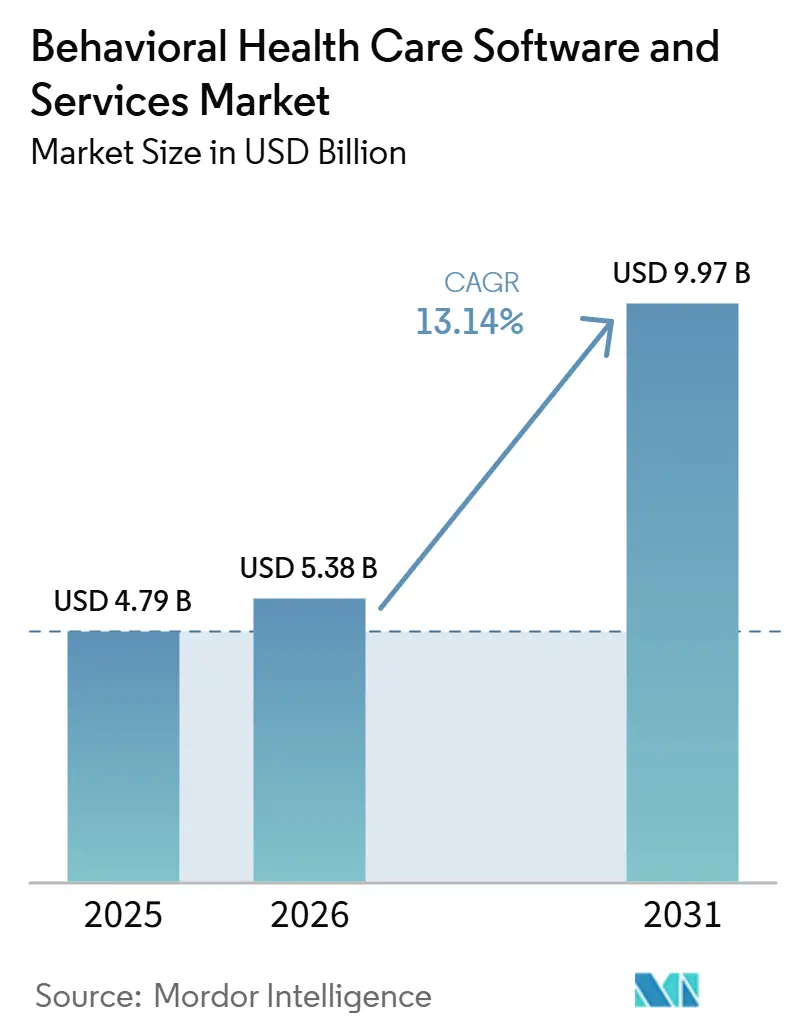

| Market Size (2026) | USD 5.38 Billion |

| Market Size (2031) | USD 9.97 Billion |

| Growth Rate (2026 - 2031) | 13.14% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Behavioral Health Care Software and Services Market Analysis by Mordor Intelligence

The behavioral health care software and services market was valued at USD 4.79 billion in 2025 and is expected to reach USD 5.38 billion in 2026. It is forecast to reach USD 9.97 billion by 2031, registering a CAGR of 13.14% during 2026-2031. Persistent unmet demand is still a core growth force, as 137 million people in the United States, or 40% of the population, lived in a federally designated Mental Health Professional Shortage Area in December 2025. This gap between patient need and clinician supply keeps the behavioral health care software and services market tied to access expansion, not only to operational efficiency. Sustained telehealth use, wider adoption of AI-supported documentation, and the spread of reporting needs under structured payment models are reinforcing demand for both clinical workflow tools and revenue cycle platforms. Competitive positioning is also strengthening around embedded billing logic, consent management, and reporting depth, which raises switching friction and supports retention for specialized vendors in the behavioral health care software and services market. Even so, delayed federal enforcement of the 2024 MHPAEA Final Rule and thin operating margins at community providers are still slowing some renewals and expansion plans.

Key Report Takeaways

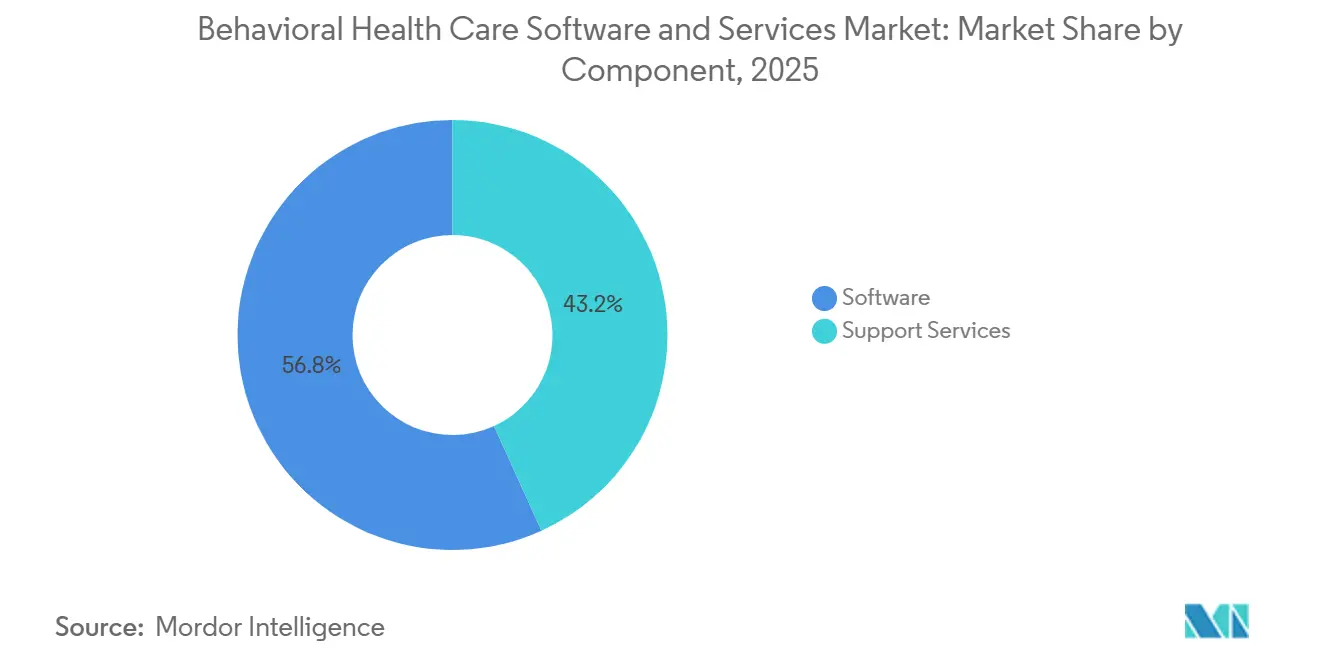

- By component, software accounted for 56.84% of the behavioral health care software and services market size in 2025 and is forecast to grow at 14.28% CAGR through 2031.

- By delivery model, the subscription model held 61.37% share in 2025, while the ownership model is projected to record the highest CAGR at 13.89% through 2031.

- By functionality, clinical functionality represented 51.92% share in 2025, while financial functionality is projected to advance at 14.07% CAGR through 2031.

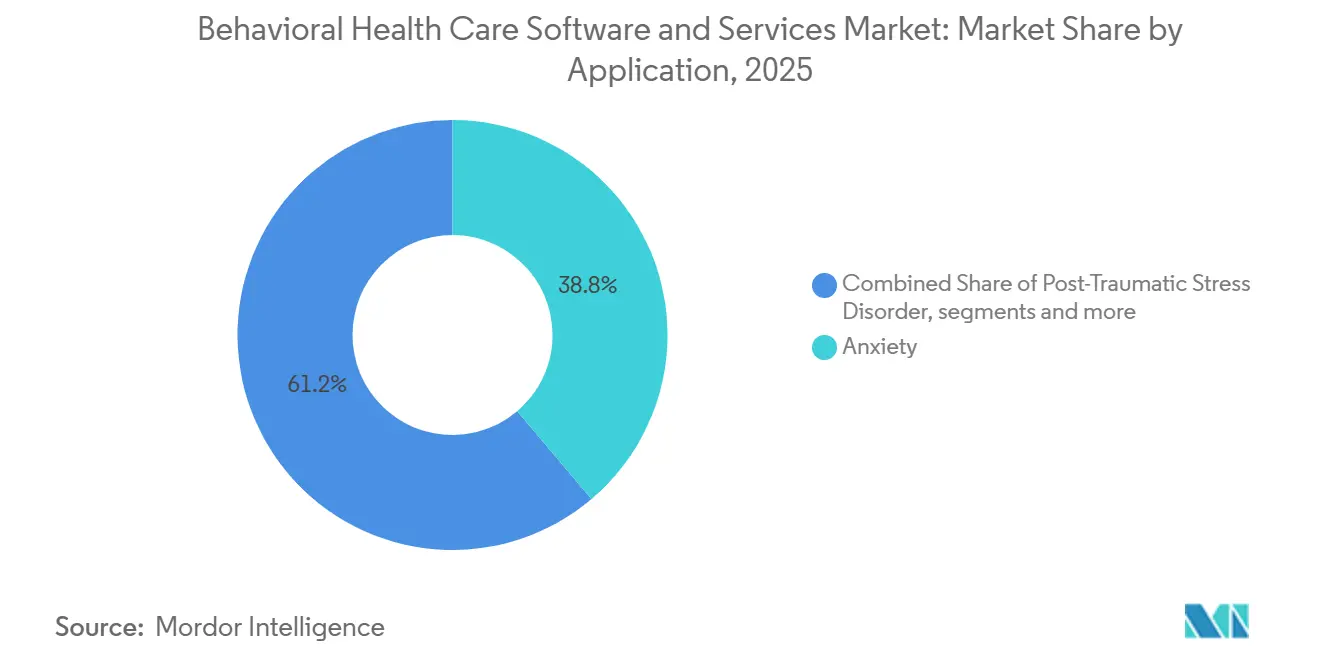

- By application, anxiety disorders led with 38.76% share in 2025, while post-traumatic stress disorder is projected to grow at 15.21% CAGR through 2031.

- By end-user, healthcare providers held 47.58% share in 2025, while healthcare payers are projected to expand at 13.76% CAGR through 2031.

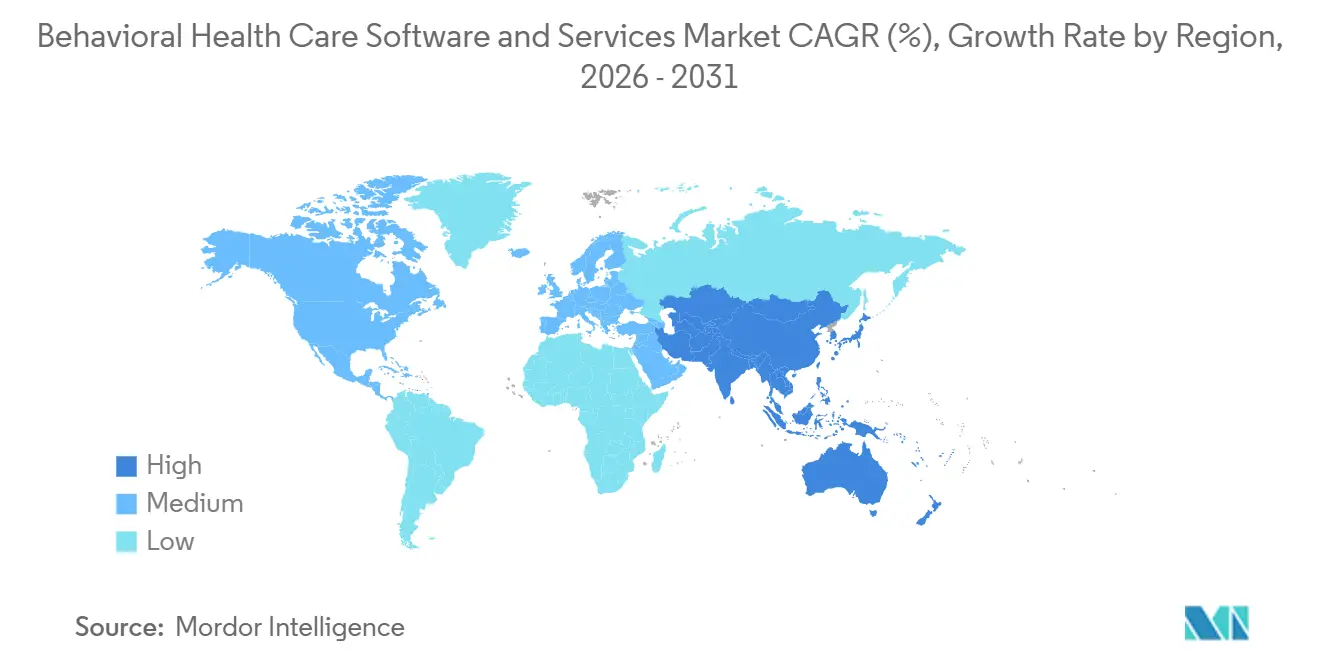

- By geography, North America held 41.63% of the behavioral health care software and services market share in 2025, while Asia-Pacific is projected to expand at 15.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Behavioral Health Care Software and Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Telehealth Adoption in Behavioral Care | +3.2% | Global, concentrated in North America and Australia | Short term (≤ 2 years) |

| Expansion of Behavioral Health EHR and Care Coordination Workflows | +2.4% | North America and Europe, with spillover to Asia-Pacific | Medium term (2-4 years) |

| AI-Enabled Documentation and Clinical Productivity | +2.8% | North America, with early gains in the United Kingdom and Australia | Short term (≤ 2 years) |

| Insurance Parity and Digital Reimbursement Tailwinds | +1.5% | North America | Medium term (2-4 years) |

| Security-First, Consent-Aware Interoperability Demand | +0.9% | North America and Europe, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Value-Based Contracting for Community and Outpatient Behavioral Care | +1.8% | North America, with early gains in urban European markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Telehealth Adoption in Behavioral Care

Behavioral health remains one of the most durable telehealth use cases, which keeps virtual care central to the behavioral health care software and services market. The American Medical Association reported that 85.9% of U.S. psychiatrists were providing weekly virtual video visits in 2024. HHS has also kept Medicare behavioral telehealth available from the patient’s home, without geographic restrictions and without a prior in-person visit requirement, through December 31, 2027. That policy structure removes a long-standing access barrier for rural and lower-income populations and keeps hybrid care models relevant in routine delivery. It also favors vendors that embed virtual visits directly into the record, because note capture, clinical workflow, and billing can remain in one system during and after the session. As a result, the behavioral health care software and services market continues to benefit when telehealth is treated as a standard care pathway instead of a temporary extension channel.

AI-Enabled Documentation and Clinical Productivity

AI-assisted documentation has moved beyond pilot activity and is becoming a practical workflow layer inside the behavioral health care software and services market. A 2025 study in the Journal of Technology in Behavioral Science found that AI documentation tools cut administrative time by up to 42% and saved 886 documentation hours per organization each year.[1]Springer Nature, “AI Integration in Behavioral Healthcare: A Practical Framework for Clinicians,” Journal of Technology in Behavioral Science, link.springer.com The same study reported that progress notes were submitted 55 hours earlier when note automation was in use. A 2026 JMIR Formative Research study that evaluated Talkspace Smart Notes across 1,528 mental health providers found 94% weekly adoption and 97.7% positive note-quality ratings.[2]JMIR Formative Research, “AI-Powered Documentation for Mental Health Providers: Retrospective Observational Mixed Methods Study,” JMIR Formative Research, formative.jmir.orgThat study also found statistically significant gains in completed sessions and client caseload per provider, which links documentation improvement to revenue capacity rather than to convenience alone. As vendors such as Qualifacts expand multilingual AI documentation support, the behavioral health care software and services market is moving toward a point where AI note assistance is expected in mainstream platform evaluations.

Expansion of Behavioral Health EHR and Care Coordination Workflows

Coverage expansion and care coordination requirements are widening the need for connected data infrastructure across the behavioral health care software and services market. CMS launched the Innovation in Behavioral Health Model in January 2025 in Michigan, New York, and South Carolina. The model ties funding to interoperability, EHR adoption, and quality reporting, which gives specialty behavioral health providers a direct operational reason to invest in more structured systems. These requirements also pull payers toward platforms that can track utilization, support audit readiness, and surface quality signals across networks. The shift matters because benefit expansion becomes harder to administer when clinical, claims, and outcomes data remain in separate tools. For that reason, the behavioral health care software and services market is seeing stronger demand for platforms that support coordination and reporting rather than documentation alone.

Value-Based Contracting for Community and Outpatient Behavioral Care

Value-based reimbursement is still developing unevenly, yet it is clearly shaping technology priorities across the behavioral health care software and services market. Providers need measurement-based care workflows, patient-reported outcome capture, and payer-ready reporting before they can participate in outcomes-linked contracts at scale. That makes software adoption a prerequisite for alternative payment readiness rather than a later operational upgrade. It also changes procurement, because organizations increasingly look for platforms that can prove clinical activity, quality performance, and financial accountability in one workflow. This is especially relevant in community and outpatient settings, where contract terms depend on visible outcomes and credible reporting. As a result, the behavioral health care software and services market is gaining from the view that outcomes tracking infrastructure is now part of financial access, not just part of compliance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Behavioral Health Staff and IT Administrators | -1.4% | Global, most acute in North America and rural Asia-Pacific | Long term (≥ 4 years) |

| 42 CFR Part 2 and Fragmented Consent Workflows | -0.9% | North America | Short term (≤ 2 years) |

| Thin Operating Margins in Small Practices and Community Clinics | -0.6% | Global, concentrated in community-based providers | Medium term (2-4 years) |

| Vendor Switching Friction from Legacy EHR and Billing Dependencies | -0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Behavioral Health Staff and IT Administrators

Clinician and IT staffing shortages still limit how much care volume the behavioral health care software and services market can process. HRSA reported that 137 million Americans, or 40% of the population, lived in a Mental Health Professional Shortage Area as of December 2025.[3]U.S. Department of Health & Human Services, “Behavioral Health Workforce Brief 2025,” Health Resources & Services Administration, bhw.hrsa.gov Under status quo supply assumptions, HRSA also projected shortfalls of 77,050 addiction counselors, 99,780 mental health counselors, and 36,780 adult psychiatrists by 2038. Even when software improves billing speed and note completion, billable activity still depends on the number of available clinicians. In California, all 58 counties faced behavioral health workforce shortages in 2025, and the state was projected to need more than 6,200 additional psychiatrists by 2033. Telehealth and AI tools can raise throughput, but the behavioral health care software and services market cannot fully escape the structural supply ceiling created by workforce shortages.

42 CFR Part 2 and Fragmented Consent Workflows

The 2026 compliance transition for 42 CFR Part 2 is creating a near-term implementation burden across the behavioral health care software and services market. HHS said the 2024 Final Rule aligns Part 2 more closely with HIPAA and introduces civil monetary penalties through the Office for Civil Rights. Vendors now need updated consent workflows for substance use disorder records, revised notice templates, and stronger disclosure audit trails. Larger platforms are better positioned to absorb this engineering and compliance work because they already maintain dedicated infrastructure for regulatory updates. Smaller vendors and margin-constrained community providers face a heavier short-term burden because system redesign and user training rise at the same time. Over a longer horizon, the rule should support better coordination, but for now it keeps the behavioral health care software and services market under added implementation pressure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platforms Outpace Services as Automation Raises Margin per Clinician

Software accounted for 56.84% of behavioral health care software and services market size in 2025 and is projected to expand at 14.28% CAGR through 2031, making it both the largest and fastest-growing component. This lead reflects the way AI-enabled EHRs can automate documentation, billing pre-population, and outcome tracking in one operating layer. When those tasks move into the platform, revenue per clinician can improve without a matching increase in implementation staff or internal IT headcount. That operating logic is especially important for outpatient providers that need productivity gains but have limited room to add administrative labor.

Support services still retain a meaningful role, especially for enterprise providers and publicly funded behavioral health organizations that lack deep internal IT capacity. Implementation, training, managed billing, analytics support, and ongoing configuration work remain important when organizations must meet state reporting rules and payer documentation standards. These services also strengthen retention because deployment work becomes embedded in local workflows over time. The behavioral health care software and services market therefore shows a layered structure in this segment, with software driving growth while services reinforce adoption durability and raise switching friction.

By Delivery Model: Ownership Accelerates as Enterprises Trade Flexibility for Control

The subscription model held 61.37% share in 2025, which reflects the purchasing reality of smaller practices that prefer recurring operating expense over large upfront capital commitments. For many independent and community-based providers, subscription deployment is the simplest route into digital workflows because it reduces infrastructure demands and shortens implementation time. It also fits lean staffing models where practices need regular updates without maintaining a large internal technology function. That makes subscription the default entry point for a broad base of buyers and supports continued SaaS expansion in the behavioral health care software and services market. Even when providers later expand functionality, many first adopt through cloud-based subscription tools because the initial barrier is lower.

The ownership model is projected to grow at 13.89% CAGR through 2031, which shows that enterprise demand is moving in a different direction from small-practice demand. Large health systems, multistate provider groups, and Certified Community Behavioral Health Clinics often need deeper configurability, custom reporting, and tighter control over state-specific compliance workflows. For that reason, the behavioral health care software and services market continues to support strong ownership demand wherever enterprise scale, regulatory variation, and workflow control carry more weight than lighter deployment.

By Functionality: Financial Modules Close the Revenue Intelligence Gap

Clinical functionality captured 51.92% share in 2025, which confirms that EHR, clinical documentation, and telehealth remain the foundation of system purchasing. Without compliant clinical records, providers cannot reliably submit claims, track outcomes, or sustain structured reimbursement relationships. Clinical documentation is still the anchor workflow because it links the care encounter to quality tracking, scheduling, and reimbursement follow-through. Telehealth has also become part of this same core layer, since video visits now need to connect directly to records, notes, and billing logic in daily operations.

Financial functionality is projected to record the fastest CAGR at 14.07% through 2031, which reflects rising attention on reimbursement precision and denial reduction. Behavioral health billing is unusually complex because providers work across multiple payer types, prior authorization rules, substance use disorder coding needs, and extra consent requirements. The behavioral health care software and services market is therefore moving beyond documentation alone and placing greater value on financial intelligence that can connect clinical activity to reimbursement accuracy.

By Application: PTSD Growth Outpaces the Broader Market as Screening and Recognition Improve

Anxiety disorders led demand with 38.76% share in 2025, which is consistent with the large volume of outpatient and teletherapy encounters associated with anxiety treatment. This segment benefits from repeat care patterns, standardized treatment pathways, and broad use of session documentation templates. Digital CBT support, symptom tracking, and measurement-based care workflows also fit anxiety treatment well because they can be repeated across large patient populations.

Post-traumatic stress disorder is projected to grow at 15.21% CAGR through 2031, making it the fastest-growing application segment. Growth is tied to stronger screening activity and greater recognition of PTSD among veterans, first responders, and survivors of violence. PTSD also appears more often alongside substance use and mood disorders, which increases demand for workflows that can manage complex care paths across diagnoses. The behavioral health care software and services market is therefore expanding its application focus beyond high-volume anxiety workflows and toward more specialized conditions that require deeper coordination, screening support, and integrated documentation.

By End-User: Payers Emerge as the Fastest-Growing Buyer Segment

Healthcare providers held 47.58% of end-user demand in 2025 and remained the largest buying group for clinical EHR and practice management tools. Community mental health centers, private practices, and residential facilities still shape the core of purchasing because they own day-to-day documentation and billing workflows. Their technology choices are increasingly influenced by whether a platform can support outcomes reporting and value-based readiness, not only by whether it can record encounters. That keeps provider demand at the center of the behavioral health care software and services market because clinical operations are still the first point of system use.

Healthcare payers are projected to grow at 13.76% CAGR through 2031, which makes them the fastest-growing end-user group in the forecast period. Their demand differs from provider demand because it centers on utilization management, network adequacy, population risk identification, and quality reporting rather than session-level charting. The patient segment remains the smallest today, but self-scheduling, digital intake, asynchronous messaging, and digital therapeutics are making patient-facing functionality more important in platform design. As these layers expand, the behavioral health care software and services market is adding a stronger analytics and engagement dimension around the clinical systems that originally defined it.

Geography Analysis

North America held 41.63% of the behavioral health care software and services market share in 2025, led by the United States. Permanent Medicare telehealth provisions for behavioral health, expansion of the CCBHC model, and the CMS Innovation in Behavioral Health Model are all supporting structured software adoption in the region. The United States also remains the densest competitive arena for specialized vendors, which raises the standard for AI documentation, interoperability, and compliance depth. Canada and Mexico contribute smaller but growing shares as mental health digitization and telehealth infrastructure continue to develop. Compliance requirements such as HIPAA, ONC-related interoperability expectations, and 42 CFR Part 2 also create higher switching costs, which helps anchor established suppliers in the behavioral health care software and services market.

Europe was the second-largest region and drew meaningful demand from Germany, the United Kingdom, France, and Scandinavia. Adoption is being supported by national mental health plans, digital health frameworks, and broader use of teleconsultation across clinical settings. Markets with clearer reimbursement and certification structures tend to move faster because providers can justify investment with fewer policy ambiguities. Italy, Spain, and the rest of Europe remain earlier in the curve, but the base for the behavioral health care software and services market is widening as digital mental health support becomes more formalized in care delivery.

Asia-Pacific is projected to expand at 15.04% CAGR through 2031, which makes it the fastest-growing regional segment. Large untreated patient populations, rising smartphone penetration, and government-backed digitization programs are helping demand build across China, India, Japan, Australia, and South Korea. Some countries are moving directly toward digital-first behavioral support because specialist capacity remains limited and traditional infrastructure is uneven. Japan is also seeing stronger behavioral health app adoption alongside an aging population and greater attention to workplace mental health reporting. South America, the Middle East, and Africa remain smaller contributors, but public digital health investment is gradually broadening the reach of the behavioral health care software and services market.

Competitive Landscape

The competitive field remains moderately fragmented, with more than 20 purpose-built vendors serving enterprise, community, and independent practice buyers. Netsmart, Qualifacts, Credible Behavioral Health, TherapyNotes, and SimplePractice hold differentiated positions across key user tiers, while broader EHR vendors compete through integration breadth and adjacent care capabilities. This structure means vendors are no longer competing on basic recordkeeping alone. Billing workflows, consent architecture, reporting depth, and workflow fit now matter more in procurement because those elements are harder to replace after implementation. As a result, switching costs are rising and established specialists continue to defend their positions in the behavioral health care software and services market.

Strategic moves are increasingly centered on interoperability, AI governance, and workflow expansion. Qualifacts stated that it became the first EHR provider certified to ISO 42001 for AI management systems, which strengthens its position in compliance-sensitive AI deployments. Netsmart also expanded its enterprise footprint in March 2026 through the broader myAvatar deployment at Pyramid Healthcare, which reinforced its strength in large multistate behavioral organizations.

Competition is also increasing around ambient documentation and payer analytics, where point solutions and core platforms both see room to grow. General EHR vendors still have openings in the segment, but specialized behavioral health platforms remain better positioned where reimbursement rules, consent workflows, and community-care reporting are central. The behavioral health care software and services market therefore remains open to consolidation, yet the strongest near-term edge still sits with vendors that are built specifically around behavioral care workflows.

Behavioral Health Care Software and Services Industry Leaders

Netsmart Technologies, Inc.

Qualifacts Systems, Inc.

Oracle

Epic Systems Corporation

Core Solutions, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Spring Health completed its acquisition of Alma, a membership platform connecting over 10,000 independent mental health clinicians with insurance payer networks, creating an end-to-end behavioral health platform covering both employer-sponsored care and independent practice management.

- April 2026: Qualifacts acquired MethodOne by Computalogic, a controlled-medication dispensing software purpose-built for opioid treatment programs, integrating medication-assisted treatment (MAT) workflows directly into the Credible, CareLogic, and InSync EHR platforms to create a unified SUD clinical and dispensing solution.

- April 2026: Streamline Healthcare Solutions launched SMARTscribe and SMARTcomply, AI-enabled ambient documentation and compliance tools embedded in the SmartCare EHR, powered by Eleos, with over 40 joint customer deployments at time of launch.the

Global Behavioral Health Care Software and Services Market Report Scope

According to the report’s scope, the behavioral health care software and services market refers to digital platforms and professional services that support the management, monitoring, and delivery of mental health and substance use treatment.

The behavioral health care software and services market is segmented into component, delivery model, functionality, application, end-user, and geography. By component, the market is segmented into software and support services. By delivery model, the market is segmented into subscription model and ownership model. By functionality, the market is segmented into clinical functionality, administrative functionality, and financial functionality. By clinical functionality, the market is further segmented into electronic health records, clinical decision support, and telehealth integration. By administrative functionality, the market is further segmented into patient and client scheduling, workforce management, and document management. By financial functionality, the market is further segmented into revenue cycle management, managed care, and general ledger and payroll. By application, the market is segmented into anxiety, post-traumatic stress disorder, substance abuse, bipolar disorders, schizophrenia, and other applications. By end-user, the market is segmented into healthcare providers, healthcare payers, and patients. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Software |

| Support Services |

| Subscription Model |

| Ownership Model |

| Clinical Functionality | Electronic Health Records |

| Clinical Decision Support | |

| Telehealth Integration | |

| Administrative Functionality | Patient and Client Scheduling |

| Workforce Management | |

| Document Management | |

| Financial Functionality | Revenue Cycle Management |

| Managed Care | |

| General Ledger and Payroll |

| Anxiety |

| Post-Traumatic Stress Disorder |

| Substance Abuse |

| Bipolar Disorders |

| Schizophrenia |

| Other Applications |

| Healthcare Providers |

| Healthcare Payers |

| Patients |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Support Services | ||

| By Delivery Model | Subscription Model | |

| Ownership Model | ||

| By Functionality | Clinical Functionality | Electronic Health Records |

| Clinical Decision Support | ||

| Telehealth Integration | ||

| Administrative Functionality | Patient and Client Scheduling | |

| Workforce Management | ||

| Document Management | ||

| Financial Functionality | Revenue Cycle Management | |

| Managed Care | ||

| General Ledger and Payroll | ||

| By Application | Anxiety | |

| Post-Traumatic Stress Disorder | ||

| Substance Abuse | ||

| Bipolar Disorders | ||

| Schizophrenia | ||

| Other Applications | ||

| By End-User | Healthcare Providers | |

| Healthcare Payers | ||

| Patients | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is behavioral health care software expected to grow through 2031?

The category is projected to rise from USD 4.79 billion in 2025 to USD 5.38 billion in 2026 to reach USD 9.97 billion by 2031 at a 13.14% CAGR.

Which region leads global demand for behavioral health platforms?

North America led with 41.63% share in 2025, supported by U.S. telehealth policy, structured reimbursement programs, and dense vendor presence.

What is the biggest component in behavioral health technology spending?

Software was the largest component with 56.84% share in 2025 and also the fastest-growing component at 14.28% CAGR through 2031.

Why are financial modules growing faster than clinical modules?

Financial functionality is projected to grow at 14.07% CAGR through 2031 because providers need better claims control, reimbursement precision, and workflow support for complex behavioral billing.

Page last updated on: