Basketball Streaming Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

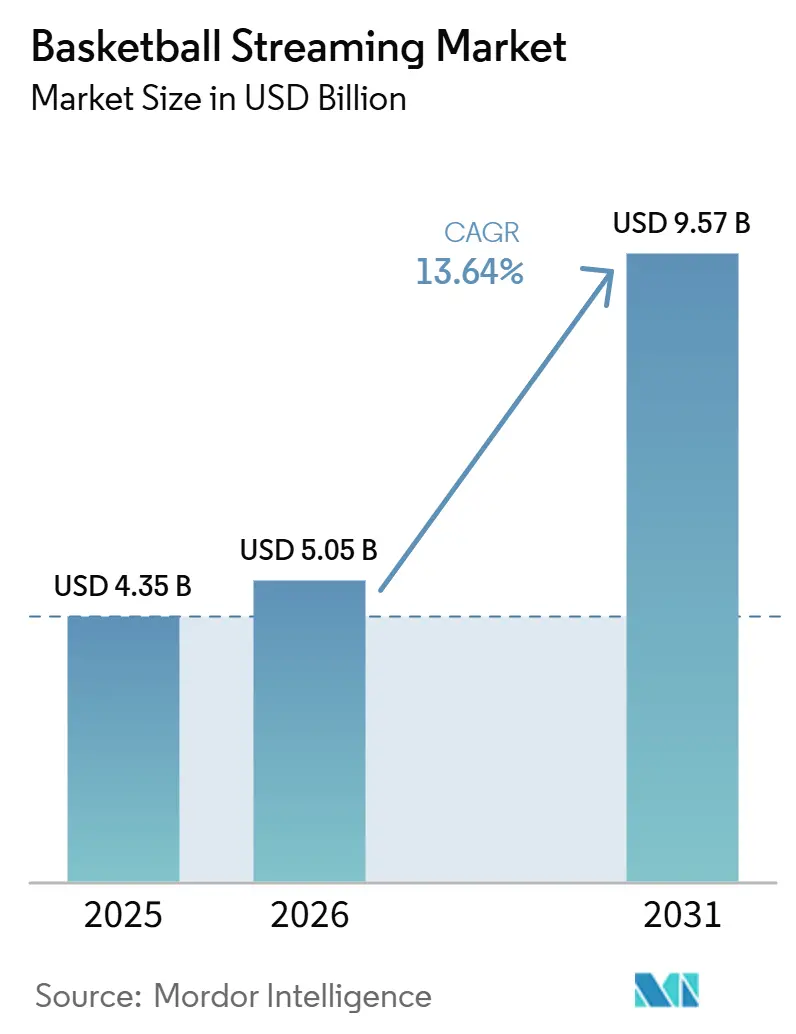

| Market Size (2026) | USD 5.05 Billion |

| Market Size (2031) | USD 9.57 Billion |

| Growth Rate (2026 - 2031) | 13.64% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Basketball Streaming Market Analysis by Mordor Intelligence

The basketball streaming market size stood at USD 4.35 billion in 2025 and is projected to reach USD 9.57 billion by 2031, at a CAGR of 13.64% from 2026 to 2031. The basketball streaming market entered a more mature phase after the NBA shifted national distribution across ABC, ESPN, NBC, Peacock, and Prime Video under its new long-term rights structure, which made streaming a primary route for premium basketball access rather than a side product. Record regular-season viewership in 2026 and higher usage on the NBA App also show that direct distribution is now supporting both audience reach and repeat engagement at the same time. The basketball streaming market is also gaining from wider international rights activity, stronger mobile viewing habits, and a larger pool of fans who move between full games, highlights, and social video in the same session. Telecom-linked bundling is improving discovery in several regions, while automated highlights and personalized video are helping platforms keep younger viewers active even when they do not watch complete games. At the same time, the basketball streaming market is rewarding platforms that can manage expensive rights, keep access simple across fragmented packages, and build revenue from both subscriptions and advertising.

Key Report Takeaways

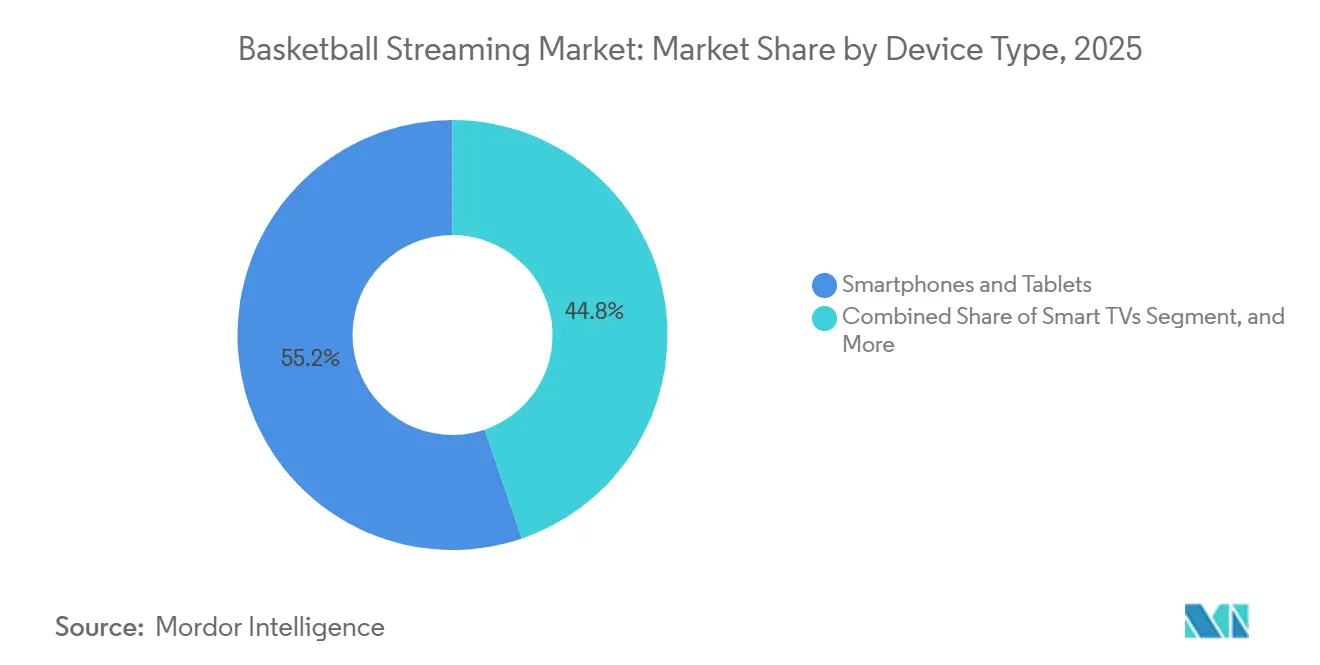

- By device type, smartphones and tablets held 55.23% share of the basketball streaming market in 2025, while smart TVs are projected to expand at a 13.86% CAGR through 2031.

- By content type, domestic matches accounted for 60.36% share of the basketball streaming market in 2025, while international matches are projected to expand at a 13.91% CAGR through 2031.

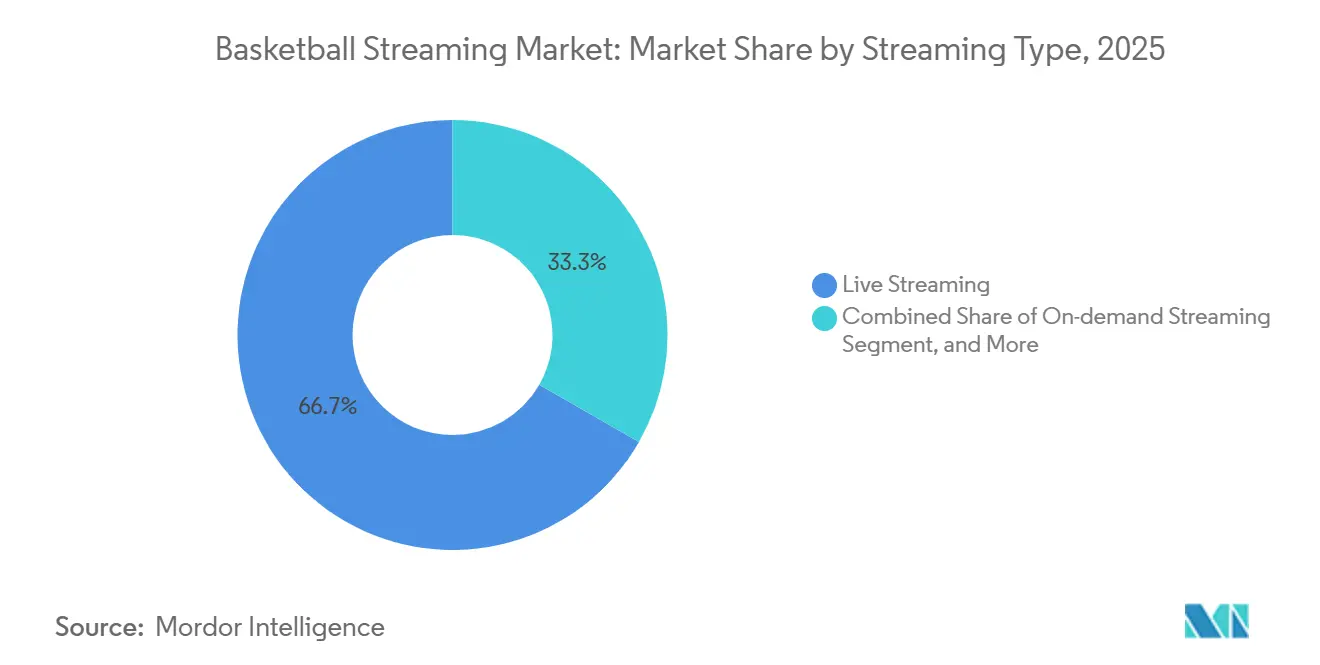

- By streaming type, live streaming held 66.72% share in 2025, while on-demand streaming remained the fastest-growing format through 2031.

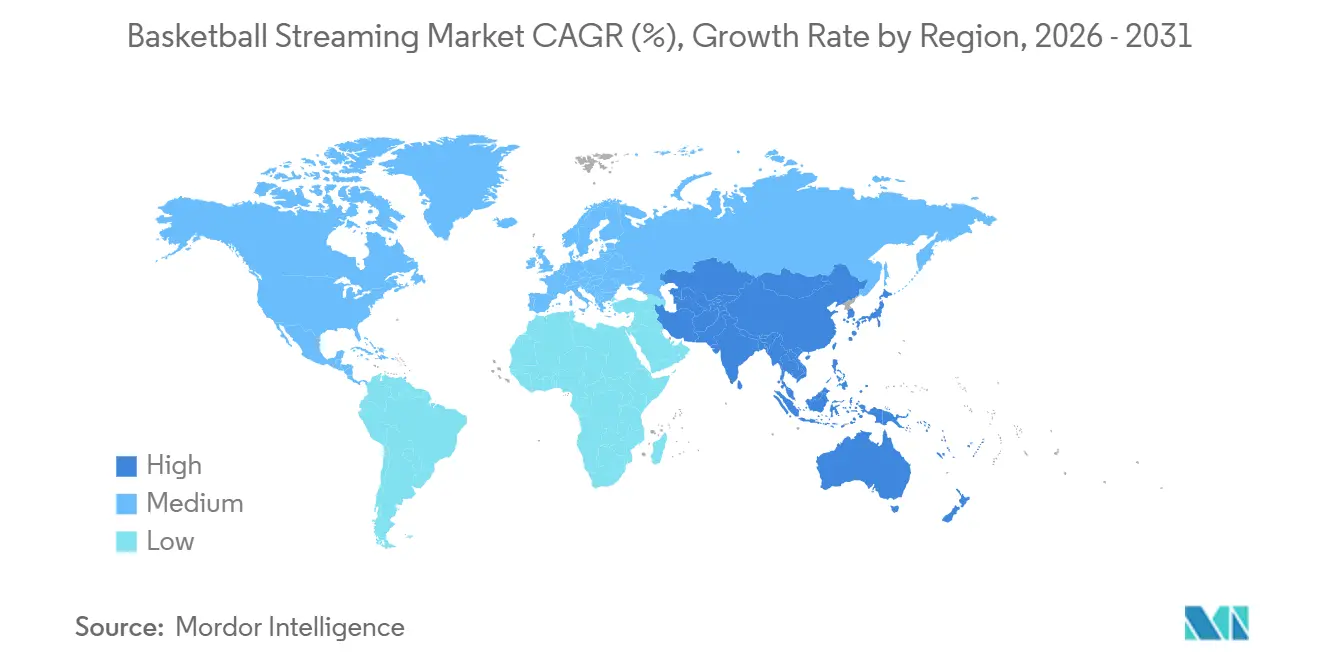

- By geography, North America held 56.66% share in 2025, while Asia-Pacific is projected to expand at a 14.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Basketball Streaming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Direct-To-Consumer League Pass Ecosystems | +2.5% | North America core, expanding to Asia-Pacific and South America | Short term (≤ 2 years) |

| Rising Live-Sports Ad Inventory Premiums on Connected Screens | +2.2% | Global, highest in North America and Asia-Pacific core | Medium term (2-4 years) |

| Mobile-First Consumption Among Younger Basketball Fans | +1.8% | Asia-Pacific core, South America, Middle East | Short term (≤ 2 years) |

| Subscription Bundling With Telecom and Pay-TV Offers | +1.5% | Global, early gains in India, Middle East, and Scandinavia | Medium term (2-4 years) |

| AI-Powered Personalization and Highlights Improve Retention | +1.2% | Global | Medium term (2-4 years) |

| Monetization of Youth, College, and International Basketball Rights | +1.0% | Global, spill-over to Africa and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Direct-to-Consumer League Pass Ecosystems

The NBA’s July 2024 media agreement placed Prime Video and Peacock beside ABC and ESPN, which shifted premium basketball into a lasting hybrid system where streaming sits at the center of national access rather than beside it.[1]NBA Communications, “NBA Signs New 11-Year Media Agreements with The Walt Disney Company, NBCUniversal and Amazon Prime Video through 2035-36 Season,” NBA, nba.com By the close of the upcoming regular season, total U.S. viewership is expected to reach a significant level, while global live coverage is projected to expand substantially. This trend shows that digital distribution can expand audience scale without diluting the value of premium rights. Watch hours per user on the NBA App are also expected to increase meaningfully, indicating that owned league platforms are becoming meaningful audience engagement and retention channels rather than support layers for broadcast partners. This model gives rights holders greater direct control over pricing, packaging, and first-party audience behavior, which is important as subscriber decisions can now be tracked closer to the point of purchase and renewal. For the basketball streaming market, this creates a more durable revenue loop in which distribution control, customer data, and content value reinforce each other over time.

Rising Live-Sports Ad Inventory Premiums on Connected Screens

Live basketball continues to deliver appointment viewing at scale, making it one of the few streaming content types that can consistently support premium connected-screen advertising. Standard live sports CTV placements commonly command high CPMs, while interactive or event-triggered units can exceed that range, raising the revenue ceiling for platforms with premium game inventory. Premion reported that most advertisers already active in live sports CTV planned to increase spending over the next 12 months, while many nonbuyers also expected to enter the category.[2]Premion, “How Live Sports on CTV Is Reshaping Opportunity for Local Advertisers,” Premion, premion.com Basketball is particularly well-positioned because the regular season provides platforms with a large volume of premium inventory across many nights, unlike sports that rely primarily on a few tentpole events. In the basketball streaming market, this advertising depth matters because it supports a two-engine model in which subscription revenue and premium advertising both contribute to rights monetization.

Mobile-First Consumption Among Younger Basketball Fans

Basketball skews younger than many competing sports, and that matters because younger viewers already treat streaming as their default sports destination rather than an occasional replacement for pay television. WSC Sports found in its Generational Fan Study that Millennials and Gen Z increasingly select streaming platforms as their primary sports destination.[3]WSC Sports, “The 2025-2026 Generational Fan Study,” WSC Sports, wsc-sports.com Disney Advertising also reported that Gen Z and Millennials spend a larger share of their sports viewing time on devices other than television, confirming that mobile and adjacent screens already carry most of the engagement load for younger cohorts. These usage patterns fit basketball particularly well because fans often follow live scores, clips, commentary, and social discussion at the same time across phones and tablets. For the basketball streaming market, that creates favorable conditions for flexible access products, mobile-led discovery, and shorter viewing windows that still generate meaningful engagement.

Subscription Bundling with Telecom and Pay-TV Offers

Subscription bundling is becoming a practical response to access friction because basketball rights are now spread across several paid services in many regions. In June 2026, Turkcell partnered with Bango to launch streaming super-bundles that combined major global and local entertainment services inside mobile-billed plans, which showed how telecom operators are moving into the aggregator role. In May 2026, Ooredoo and beIN renewed their strategic partnership in Qatar, which reinforced telecom-led distribution as a workable route for premium sports access across the Middle East. These arrangements matter because fans can absorb basketball within a broader connectivity or entertainment bill instead of making a separate purchase each time rights move to a new platform. In the basketball streaming market, bundling supports discovery, lowers payment friction, and gives distributors another tool for reducing churn in price-sensitive households.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Rights Ownership Across Leagues, Teams, And Territories | -1.50% | Global, most acute in Europe and Asia-Pacific | Medium term (2-4 years) |

| High Sports Rights Inflation Compresses Margins | -1.20% | North America highest cost base, expanding globally | Long term (≥ 4 years) |

| Piracy And Unauthorized Restreaming Reduce Monetizable Reach | -0.90% | Global, most severe in Europe and South America | Short term (≤ 2 years) |

| Variable Broadband Quality And Latency Hurts Premium Live Viewing | -0.60% | Africa, South Asia, parts of South America and Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Rights Ownership Across Leagues, Teams, and Territories

Rights fragmentation remains one of the clearest structural limits on scale because basketball content is divided across national league packages, local team packages, and territory-specific international agreements. FIBA’s distribution setup shows this clearly, with separate arrangements across markets such as Germany and China rather than one unified worldwide digital access model. The NBA’s ongoing local rights transition adds another layer because fans may still need different services depending on team location, national package, and competition type. When viewers cannot predict where a game will appear, the discovery burden rises, and the value of each individual subscription weakens. For the basketball streaming market, that means a large share of underlying fan demand still does not convert cleanly into stable recurring revenue.

High Sports Rights Inflation Compresses Margins

Rights inflation is also pressuring platform economics because premium basketball packages now require far larger commitments than in earlier contract cycles. The NBA’s long-term media agreement announced in recent years carried a record value, setting a new benchmark for national basketball distribution costs across the streaming and broadcast ecosystem. Those commitments can be justified by audience scale, but they still raise the performance threshold for subscriber conversion, advertising yield, and long-term retention. Platforms that do not pair basketball with broader sports portfolios or strong audience data capabilities face a much narrower path to profitable monetization. In the basketball streaming market, the cost side is therefore rising faster than many mid-tier operators can comfortably absorb, especially when they lack national scale or broad bundling power.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Smartphones Hold the Largest Share While Smart TVs Improve Monetization

Smartphones and tablets held 55.23% of the basketball streaming market share in 2025, which made mobile the leading access point for both live viewing and short-form basketball consumption across regions. That lead reflects more than convenience because league apps, regional services, and international basketball products are increasingly designed around fast sign-in, short-form discovery, and portable viewing behavior from the first user touchpoint. Disney Advertising reported in 2025 that younger sports audiences already spent most of their viewing time on devices other than television, which helps explain why basketball aligns so well with the mobile environment. WSC Sports also found strong streaming preference among Gen Z and Millennial fans, which reinforces the link between basketball fandom and mobile-native behavior in the basketball streaming industry.

Mobile leadership also fits the rhythm of basketball viewing because fans often check in repeatedly across a game rather than committing only to a single uninterrupted long session. The NBA’s 2026 regular-season results showed nearly 20 million live game streams from Tap to Watch, which supports the view that fast, low-friction mobile access is now central to engagement growth. Smart TVs are projected to grow at a 13.86% CAGR through 2031, which shows that living-room streaming is becoming more important as households expect premium sports inside connected home entertainment setups. This shift improves monetization because premium live sports inventory on connected televisions is priced well above open web video, giving rights holders a better revenue mix as screen time migrates upward. Laptops, desktops, consoles, and emerging interactive devices remain smaller in revenue terms, but they still matter because the basketball streaming market increasingly rewards flexible access across every screen type rather than a single dominant device.

By Content Type: Domestic Games Lead Revenue While International Rights Expand Reach

Domestic matches accounted for 60.36% of the basketball streaming market size in 2025, which kept home-market loyalty and regular-season volume at the center of revenue generation for most distributors. That lead is tied to habitual viewing patterns because local fans follow teams across long schedules, pregame and postgame coverage, and repeat weekly windows that keep subscription value visible through the season. The NBA’s 1,230-game regular season also gives domestic packages a depth of inventory that few sports properties can match, which helps stabilize both subscription models and ad sales. In practical terms, domestic programming still provides the most dependable commercial base for the basketball streaming industry because it combines frequency, familiarity, and team-specific engagement.

International matches are projected to expand at a 13.91% CAGR through 2031, supported by broader territorial rights distribution and stronger monetization efforts outside mature NBA home markets. FIBA’s 2024 agreement with Migu made the platform the exclusive digital rights holder for major international basketball events in China through 2029, which strengthened long-run visibility for cross-border viewing and tournament-led audience growth. DAZN also expanded its women’s European basketball coverage in 2025 through the inaugural EuroLeague Women Final Six, which showed that international rights growth is not limited to men’s competitions or only to the largest leagues. Other content, including automated highlights, documentaries, and shoulder programming, is gaining relevance because WSC Sports showed in 2026 how AI-driven clips can extend engagement without requiring new premium live rights spending.

By Streaming Type: Live Games Drive Revenue While On-Demand Extends Usage

Live streaming held 66.72% of the basketball streaming market share in 2025, which confirms that real-time access remains the main reason fans pay for premium basketball services across both mature and developing regions. Viewers place a higher value on live games because the outcome loses urgency once scores are known, and that time sensitivity supports heavier subscription spending, more predictable usage, and better ad pricing. StreamLayer reported that live sports CTV inventory typically commands USD 30 to USD 65 CPMs, which helps explain why live coverage continues to anchor revenue even as viewing behavior spreads across more formats. This keeps live distribution at the center of the basketball streaming market because no other content layer matches its combined effect on acquisition, retention, and advertiser demand.

On-demand streaming was the fastest-growing format through 2031, which reflects the rising role of short clips, replay packages, and personalized post-game viewing within everyday basketball use. Spiideo launched AI Highlights in May 2026, which demonstrated how automated production can turn game footage, event data, and commentary into ready-to-distribute basketball clips at scale without a large manual editing workflow. WSC Sports said its work with the NBA produced 67,000 personalized playoff highlights in a single year, which shows how on-demand viewing has moved beyond catch-up and into a dedicated retention tool. Other formats, such as multiview streams, audio-led experiences, and early interactive overlays, remain smaller today, but they point to how the basketball streaming industry is widening beyond one standard full-game viewing journey.

Geography Analysis

North America held 56.66% of the basketball streaming market size in 2025, which kept the region far ahead of every other geography in monetized basketball viewing. The lead rests on the NBA’s deep media infrastructure and on the 2025-26 rights reset that placed ABC and ESPN, Peacock, Prime Video, and NBA TV inside one broader national streaming cycle. In June 2026, the NBA said the regular season reached 170 million total U.S. viewers and more than 1.3 billion hours of global live coverage, which underlined the scale advantage of the North American ecosystem. Canada followed a similar path through strong sports network distribution and direct-to-consumer access, which kept basketball discoverable across both bundled and stand-alone products. South America remains smaller in revenue terms, but the basketball streaming market is broadening there as regional platforms and imported league packages extend access to more cross-border competitions.

Europe remains a rights mosaic rather than a single unified basketball zone, with different broadcasters and streamers controlling FIBA, EuroLeague, and domestic league access by country. Movistar Plus+ and EuroLeague extended their Spanish partnership through the 2030-31 season, which shows how incumbent subscription platforms still matter in established European markets. This setup supports recurring revenue, but it also slows greenfield direct-to-consumer expansion because many viewers already receive basketball inside broader pay television or multi-sport bundles. Asia-Pacific is projected to grow at a 14.23% CAGR through 2031, making it the fastest-growing region in the basketball streaming market. FIBA’s exclusive digital partnership with Migu in China and strong NBA audience momentum across key Asia-Pacific territories give the region a long runway for both premium and mobile-led viewing.

Africa is moving from limited availability toward multi-tier access, with the NBA returning to SuperSport channels and debuting on Showmax across more than 50 sub-Saharan countries in November 2025. In May 2026, ESPN Africa secured exclusive pay television rights to the NBA Finals across sub-Saharan Africa, which added a premium layer to the regional distribution model. The Middle East is advancing through a mix of dedicated sports services and telecom-linked distribution, which helps premium basketball content reach viewers through familiar billing relationship. Across both regions, the biggest opening in the basketball streaming market is still a unified direct platform that combines local payments, localized commentary, and strong on-demand discovery.

Competitive Landscape

The basketball streaming market is moderately concentrated at the top of national rights, but it remains fragmented across local team packages, secondary competitions, and international territories. Amazon Prime Video, Disney through ESPN, and NBCUniversal sit at the center of the NBA’s national U.S. distribution structure after the league’s 11-year deal announced in 2024. That arrangement gave Amazon a major strategic step forward because Prime Video moved from a complementary sports outlet into a primary home for premium basketball under a long-duration rights cycle. The competitive split in the basketball streaming market is therefore less about raw subscriber scale alone and more about which platforms can combine rights depth, ad sales strength, retention tools, and broad device reach.

DAZN has taken an expansion path that mixes rights acquisition with platform development, which keeps it relevant in both international basketball and wider streaming bundle discussions. In April 2025, DAZN expanded its partnership with EuroLeague Women to become the exclusive broadcaster for the inaugural Final Six and the exclusive global English-language partner. In 2025, fuboTV and DAZN also entered a multi-year integrated partnership that combined virtual MVPD distribution with DAZN’s international sports content portfolio. These moves show that mid-tier operators are trying to stay competitive by linking basketball with wider sports bundles instead of relying on a single property or one narrow rights window. They also show why the basketball streaming market remains open to specialized platforms that can serve fans across several leagues, territories, and viewing models at once.

Data and personalization are becoming a second front of competition because platforms need stronger engagement without matching every rival on rights spend. WSC Sports said its NBA partnership generated 67,000 personalized playoff highlights in one year, which shows how automated content can keep fans active between live games and across multiple digital touchpoints. Spiideo’s AI Highlights launch in May 2026, along with similar automation moves in lower tiers, indicates that this capability is spreading down the value chain rather than remaining limited to the biggest leagues. In the basketball streaming market, the likely winners are the services that pair premium rights with efficient personalization, workable bundling, and a simple viewing path across fragmented content sources.

Basketball Streaming Industry Leaders

ESPN

Amazon.com, Inc.

Warner Bros. Discovery, Inc.

NBCUniversal Media, LLC

YouTube, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: ESPN Africa secured exclusive multi-year English-language pay-TV rights to the NBA Finals across sub-Saharan Africa, including Conference Finals coverage and NBA Sunday Night regular-season games. All games air on ESPN linear channels and stream on Disney+ in South Africa, marking the first time NBA Finals content carries dedicated pay-TV exclusivity across the continent.

- May 2026: Spiideo launched AI Highlights inside Spiideo Play with initial support for basketball, soccer, ice hockey, and handball. The platform combines video data, event feeds, audio commentary, and contextual AI to generate story-driven highlight clips without manual editorial intervention, enabling leagues at all tiers to compete for digital engagement without broadcast production budgets.

- March 2026: TNT Sports acquired exclusive multi-year U.S. English-language broadcast rights to major FIBA competitions, including the FIBA Women’s Basketball World Cup 2026, the FIBA Basketball World Cup 2027, and EuroBasket 2029. The deal displaced FIBA’s prior ESPN arrangement and represented Warner Bros. Discovery’s most consequential basketball rights acquisition after its exit from the NBA national deal in 2024.

- November 2025: The NBA returned to SuperSport channels and debuted on Showmax across more than 50 sub-Saharan African countries, marking the league’s first regional linear broadcast presence since the 2015-16 season. Distribution through DStv Compact packages and GOtv Supa Plus significantly expanded basketball’s addressable audience across English-speaking and French-speaking Africa.

Global Basketball Streaming Market Report Scope

Basketball Streaming Market refers to the digital distribution of live and on-demand basketball games through OTT platforms, sports apps, broadcaster websites, and connected TV services. It allows fans to watch leagues, tournaments, highlights, and related content on smartphones, tablets, PCs, and smart TVs.

The Basketball Streaming Market Report is Segmented by Device Type (Smartphones and Tablets, Smart TVs, and Laptops and Desktops), Content Type (International Matches, and Domestic Matches), Streaming Type (Live Streaming, and On-demand Streaming), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Smartphones and Tablets |

| Smart TVs |

| Laptops and Desktops |

| Other Device Type |

| International Matches |

| Domestic Matches |

| Other Content Type |

| Live Streaming |

| On-demand Streaming |

| Other Streaming Type |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Device Type | Smartphones and Tablets | |

| Smart TVs | ||

| Laptops and Desktops | ||

| Other Device Type | ||

| By Content Type | International Matches | |

| Domestic Matches | ||

| Other Content Type | ||

| By Streaming Type | Live Streaming | |

| On-demand Streaming | ||

| Other Streaming Type | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the basketball streaming market size in 2026 and how fast is it growing?

The basketball streaming market stood at USD 4.35 billion in 2025 and is projected to reach USD 9.57 billion by 2031, growing at a 13.64% CAGR from 2026 to 2031.

Which region leads basketball streaming revenues today?

North America led with 56.66% share in 2025, supported by the NBA's deep media infrastructure and strong direct-to-consumer and national streaming distribution.

Which device category is most important for basketball viewing?

Smartphones and tablets held 55.23% share in 2025, which shows that mobile remains the main access point for live games, clips, and repeat viewing.

Why does live viewing still matter more than highlights and replays?

Live streaming held 66.72% share in 2025 because real-time access remains the primary reason fans pay for premium basketball services and advertisers value that urgency.

What is driving the strongest future growth by content category?

International matches are projected to expand at a 13.91% CAGR through 2031, supported by broader territorial rights activity and deeper monetization outside mature home markets.

What are the biggest strategic risks for streaming platforms in basketball?

The main risks are fragmented rights ownership and rising rights costs, which make discovery harder for fans and raise the revenue threshold platforms must meet to stay profitable.

Page last updated on: