Basal Insulin Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

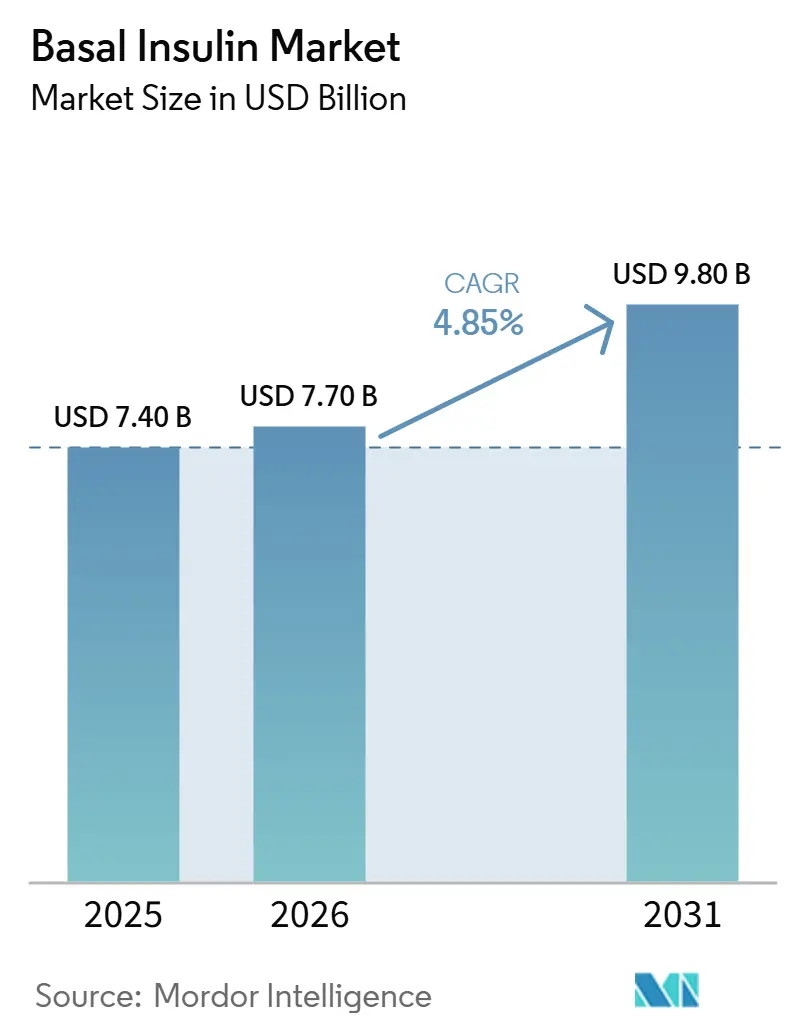

| Market Size (2026) | USD 7.70 Billion |

| Market Size (2031) | USD 9.80 Billion |

| Growth Rate (2026 - 2031) | 4.85% CAGR |

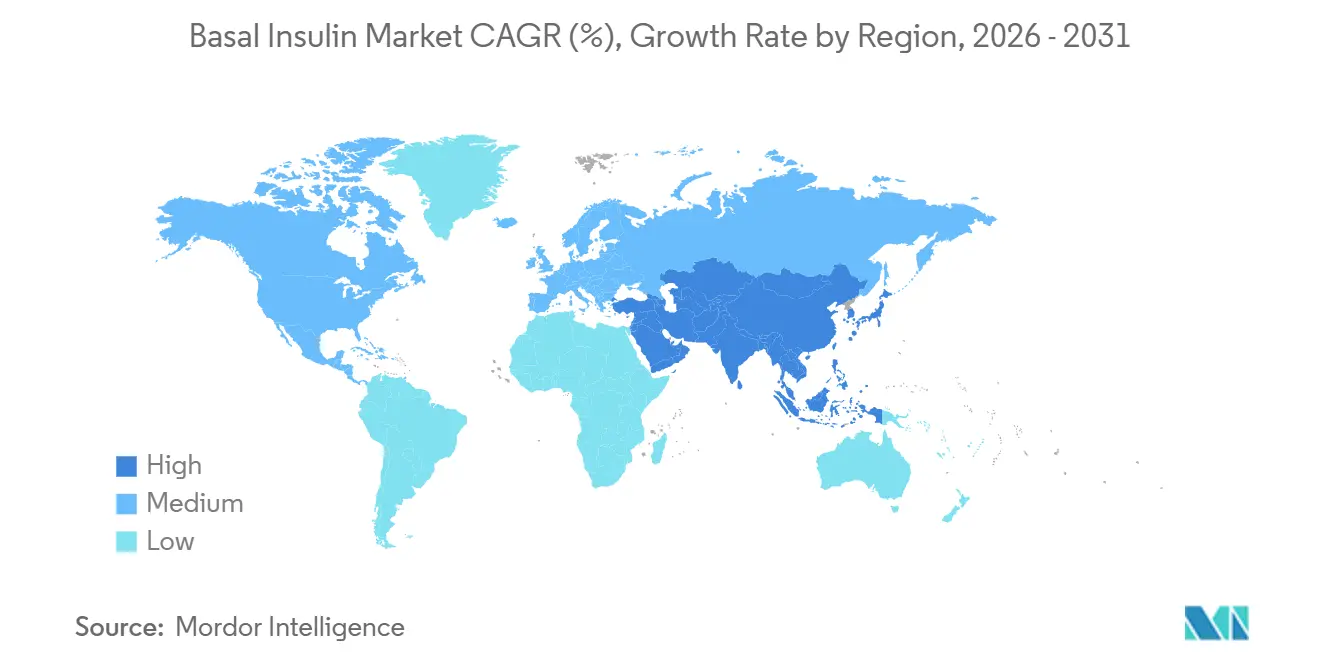

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

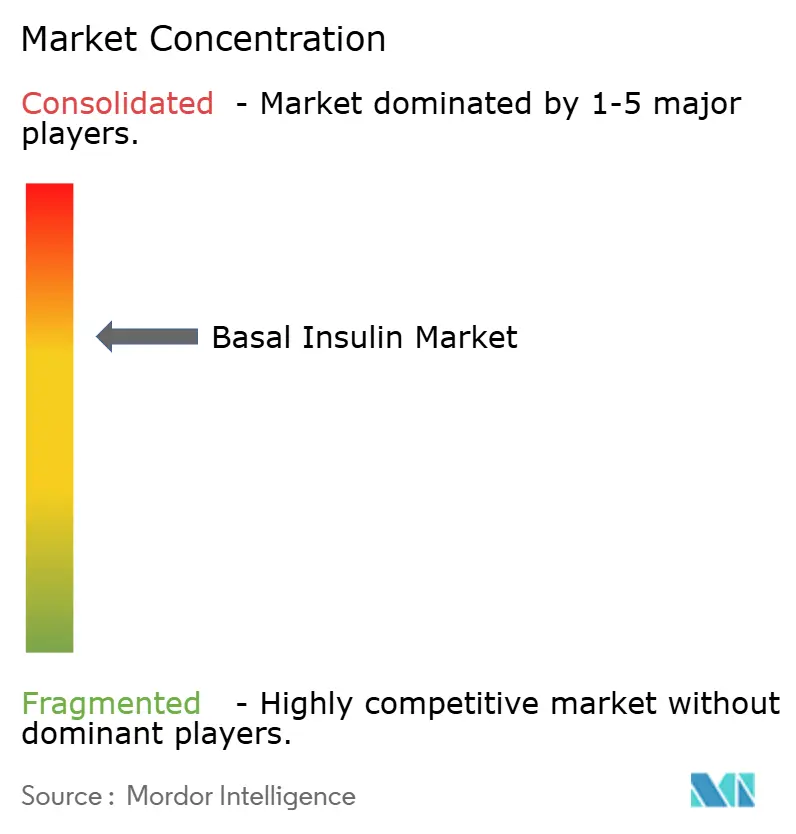

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Basal Insulin Market Analysis by Mordor Intelligence

The Basal Insulin Market size is expected to increase from USD 7.40 billion in 2025 to USD 7.70 billion in 2026 and reach USD 9.80 billion by 2031, growing at a CAGR of 4.85% over 2026-2031.

Widening diabetes prevalence continues to enlarge the eligible patient pool, yet payers and clinicians increasingly shift first-line injectable therapy toward GLP-1 receptor agonists, tempering overall volume growth. FDA clearance of Novo Nordisk’s once-weekly Awiqli (insulin icodec) in March 2026 curtails daily injections to 52 per year, improving adherence and differentiating the class [1]FDA, “Approval of Awiqli Once-Weekly Basal Insulin,” lelezard.com. At the same time, Medicare’s negotiated significant price cut for semaglutide effective January 2027 reinforces health-plan preference for GLP-1s as the initial add-on to oral agents. Smart-pen integration with continuous glucose monitors (CGMs) accelerates device stickiness by automating dose titration, while expanding online-pharmacy fulfillment compresses legacy retail margins and redistributes channel economics.

Key Report Takeaways

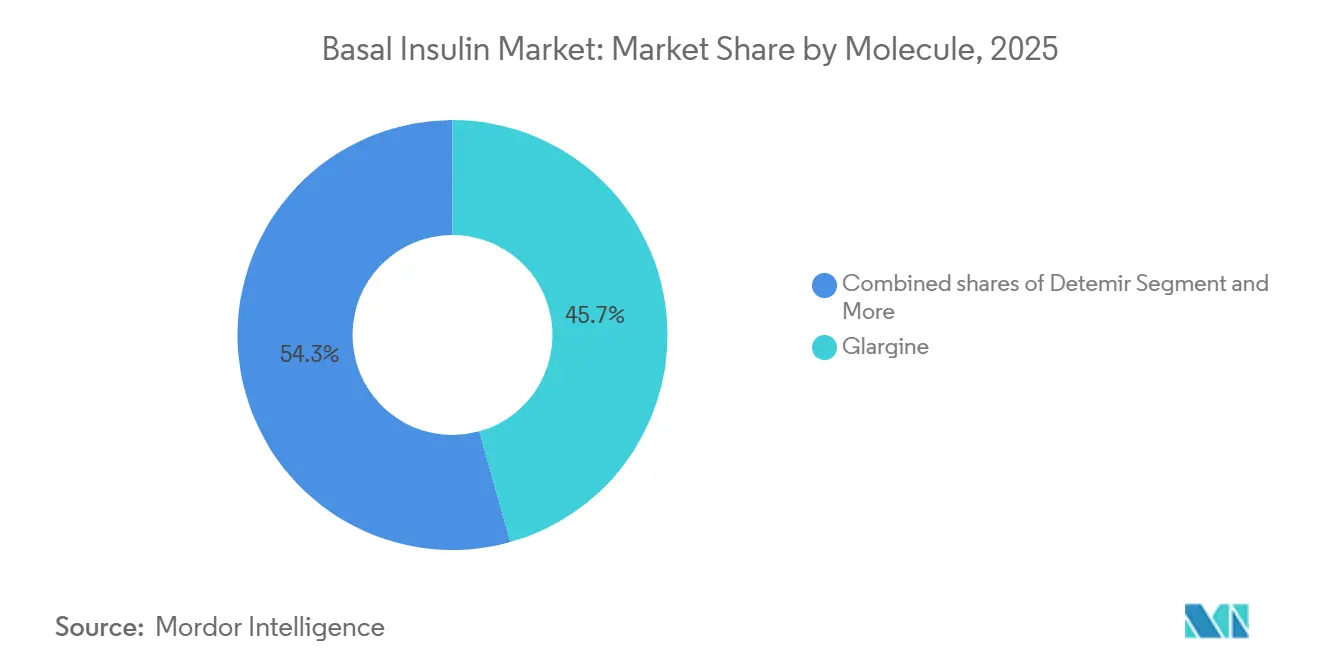

- By molecule, glargine led with 45.67% of basal insulin market share in 2025, whereas the detemir class is forecast to grow at a 5.67% CAGR through 2031.

- By delivery device, pre-filled disposable pens captured 58.34% of basal insulin market size in 2025; reusable and smart pens are advancing at a 6.12% CAGR over 2026-2031.

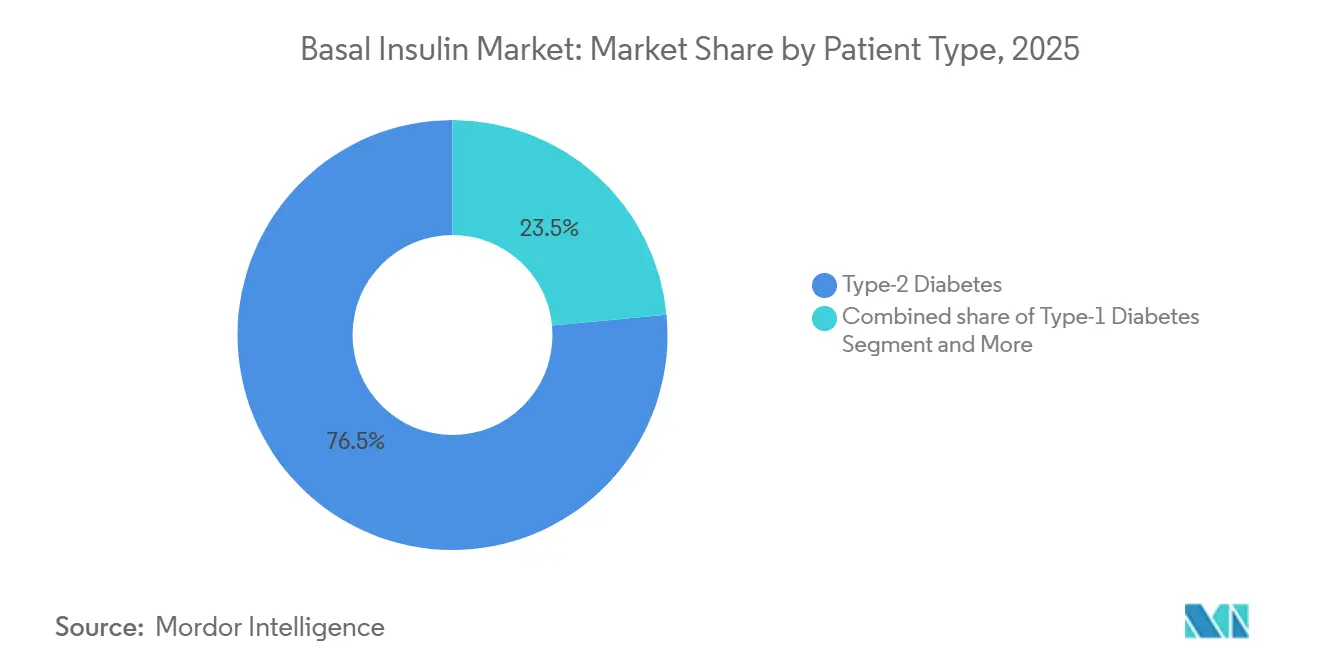

- By patient type, type-2 diabetes accounted for 76.50% of volume in 2025 and is progressing at a 5.23% CAGR, while type-1 diabetes remains the most stable revenue contributor.

- By distribution channel, retail pharmacies held 46.82% share in 2025, yet online pharmacies are scaling at a 5.9% CAGR on the back of Amazon Pharmacy and CVS digital bundles.

- By geography, North America retained 43.89% share in 2025; Asia-Pacific is projected to post the fastest 6.32% CAGR through 2031 as India’s semaglutide patent expiry floods the region with low-cost GLP-1s.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Basal Insulin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global diabetes prevalence | +1.5% | Global, with highest absolute growth in Asia-Pacific and Middle East & Africa | Long term (≥ 4 years) |

| Biosimilar insulin market expansion | +1.4% | North America & Europe lead; Asia-Pacific accelerating via domestic manufacturing | Medium term (2-4 years) |

| Adoption of long-acting insulin analogues | +1.2% | North America & Europe mature markets; Asia-Pacific and Latin America growth frontiers | Medium term (2-4 years) |

| Once-weekly basal insulin pipeline momentum | +0.9% | North America & Europe initial launch markets; Asia-Pacific follow-on approvals by 2028-2030 | Medium term (2-4 years) |

| Shift from vials to pre-filled pens | +0.8% | Global, with fastest adoption in urban centers and higher-income cohorts | Medium term (2-4 years) |

| Integration with CGM-enabled smart pens | +0.7% | North America & Western Europe; limited penetration in price-sensitive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Diabetes Prevalence

According to NCD Alliance over one in nine adults worldwide now live with diabetes, with projections indicating a rise to 853 million by 2045. Low- and middle-income nations now account for most new diagnoses, but therapeutic access lags epidemiologic need. Aggressive local-pricing strategies such as Novo Nordisk’s USD 24-per-week Ozempic launch in India in December 2025 unlock volume yet compress margins. In the United States, the CDC estimates 38 million people have diabetes; A modest share of Medicare beneficiaries gained GLP-1 coverage under 2026 pilots, redirecting many prospective insulin starts to incretin therapy. The basal insulin market therefore expands in absolute terms while facing a shrinking eligible numerator as treatment algorithms evolve.

Adoption of Long-Acting Insulin Analogues

Glargine, degludec, and detemir displaced NPH insulin on safety grounds, but biosimilar competition now erodes the analogue premium. Semglee launched at 64% below Lantus list price and delivered equivalent glycemic control in real-world evidence from UC Health [2]UC Health, “Semglee Cost-Effectiveness,” reuters.com. Sanofi’s Merilog became the first rapid-acting biosimilar approved in the United States in February 2026, establishing precedent that accelerates basal-analogue follow-ons. Updated 2026 Diabetes Canada guidelines caution about hypoglycemia risk for icodec in type-1 diabetes, indicating analogue uptake will plateau in developed markets but rise in emerging regions where biosimilars bridge affordability gaps.

Once-Weekly Basal Insulin Pipeline Momentum

Novo Nordisk’s Awiqli secured U.S. approval in March 2026 after a 2024 Complete Response Letter, showing superior HbA1c reduction over daily glargine but 1.6-fold higher hypoglycemia incidence in trials. Patient-preference studies revealed 93.7% favor weekly over daily injections, supporting rapid uptake if payers grant coverage. Eli Lilly’s efsitora alfa demonstrated non-inferiority to degludec in Phase 2, positioning a duopoly beyond 2028. Yet Medicare’s cost-effectiveness thresholds suggest access will hinge on pricing parity with daily biosimilars rather than convenience alone.

Integration with CGM-Enabled Smart Pens

Medtronic’s InPen now links with Simplera CGM, while Dexcom’s G7 pairs with Novo smart pens, creating a data loop that cuts HbA1c an extra points. The American Diabetes Association’s 2026 Standards of Care eliminated prior authorization barriers for CGM bundles, effectively making reimbursement mandatory in the United States. High sensor costs of USD 100-200 per month restrict penetration in many Asia-Pacific and Latin American markets, segmenting the basal insulin market into high-tech and low-tech adoption tiers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GLP-1 uptake delaying basal starts | -1.1% | North America & Europe; rising in Asia-Pacific with oral GLP-1s | Short term (≤ 2 years) |

| High analogue pricing and reimbursement gaps | -0.6% | Global, acute pressure in U.S. commercial payers and emerging markets | Medium term (2-4 years) |

| Regulatory complexity for biosimilars | -0.3% | North America & Europe | Long term (≥ 4 years) |

| Manufacturing scale-up bottlenecks | -0.2% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

GLP-1 Uptake Delaying Basal Starts

SURPASS-4 showed tirzepatide reduced insulin initiation by 71% versus glargine, pushing basal insulin deeper into treatment lines [3]SURPASS-4 Investigators, “Tirzepatide Insulin Sparing Study,” reuters.com. SUSTAIN-4 and subsequent trials confirm semaglutide’s dual benefit of HbA1c lowering and 10-15% body-weight reduction, making GLP-1s the preferred injectable for type-2 diabetes. Oral formulations—Novo’s semaglutide (approved December 2025) and Lilly’s orforglipron (approved April 2026) at USD 149 per month—remove injection barriers and equalize cost with basal insulin starter packs. Medicare’s negotiated USD 274 monthly semaglutide price effective 2027 cements payer bias toward GLP-1s, compressing basal starts in developed markets.

High Analogue Pricing & Reimbursement Gaps

U.S. legislation capped Medicare insulin copays at USD 35 in 2023, cutting average spending to USD 15 in 2024 and eroding manufacturer margins. Biosimilar glargine entries such as Semglee and Rezvoglar list significantly below Lantus, creating three-tier pricing that fragments share and limits volume scale. WHO’s insulin prequalification seeks broader biosimilar access, but local manufacturing constraints slow uptake, keeping out-of-pocket costs above household income in many emerging economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Molecule: Icodec Pipeline Reshapes Long-Acting Landscape

Detemir is projected to grow at a 5.67% CAGR through 2031, the fastest rate among basal insulin molecules. Three factors explain the rebound. First, emerging-market biosimilars launch at prices significantly below branded analogues, making twice-daily detemir attractive where drug budgets are tight. Second, payers in cost-sensitive regions steer formularies toward these lower-priced options rather than premium once-daily products. Third, clinicians see value in detemir’s weight-neutral profile for obese type-2 patients who cannot afford GLP-1 combinations.

Glargine still led with 45.67% of molecule share in 2025, supported by Sanofi’s Lantus and Toujeo, but biosimilars such as Semglee and Rezvoglar are eroding that position with price discounts. Degludec, marketed as Tresiba, retains a dosing-flexibility edge yet faces U.S. price pressure and biosimilar competition that limits its growth to low-single digits. The Others group—once-weekly icodec and Lilly’s pipeline efsitora alfa—secured a toehold after Awiqli won FDA approval in March 2026 for type-2 diabetes, though exclusion from type-1 indications confines uptake to majority of insulin users.

By Delivery Device: Smart Pens Gain Share as CGM Integration Becomes Standard

Pre-filled pens led with 58.34% share in 2025; however, reusable and smart pens outpace overall basal insulin market growth at 6.12% CAGR through 2031. The basal insulin market share commanded by traditional vials has fallen in North America, whereas India and sub-Saharan Africa still rely on them for significant portion of doses. Smart-pen-CGM bundles are rapidly gaining preferred-drug-list placement among U.S. payers following ADA guideline changes. Insulet’s Omnipod GO basal-only tubeless pump—positioned between pens and full-loop pumps—could capture notable share by 2030.

Ypsomed-BD autoinjector development targets high-viscosity biologics, anticipating concentrated insulin growth. Vendor lock-in strengthens as data platforms pair proprietary pens with branded CGMs, raising patient switching costs and reinforcing manufacturer share.

By Patient Type: Type-2 Diabetes Sustains Volume but GLP-1s Compress Growth

Type-2 patients accounted for 76.50% of basal insulin market share in 2025, and their segment is forecast to expand at a 5.23% CAGR through 2031 despite mounting GLP-1 substitution pressure. Type-1 diabetes users contribute roughly modest share of basal insulin market size and generate higher per-capita revenue because lifelong dependence and the absence of GLP-1 alternatives stabilizes demand. Gestational diabetes regestered nominal share of prescriptions, yet the EXPECT trial’s validation of degludec in pregnancy should lift its small but critical share over the forecast horizon. Clinical evidence from SURPASS-4 shows tirzepatide cut insulin starts by 71%, effectively demoting basal insulin to third- or fourth-line status in many algorithms, especially across North America and Europe. Novo Nordisk’s Awiqli approval covers only type-2 diabetes, further bifurcating the pool of potential weekly-dose adopters.

By Distribution Channel: Online Pharmacies Scale Amid Telehealth Integration

Retail outlets held 46.82% of basal insulin market share in 2025 on the strength of in-person counseling and same-day pickup, but growth slows as copay caps squeeze pharmacy margins. Online pharmacies are projected to post a robust 5.9% CAGR through 2031, expanding basal insulin market size by bundling home delivery with subscription pricing and virtual consults; Amazon Pharmacy’s RxPass and CVS’s digital refills exemplify this migration. Hospital pharmacies capture about significant share of initial inpatient volume, yet majority of transitions to retail or digital channels within 90 days, limiting their sustained influence. Manufacturer-direct portals such as LillyDirect and TrumpRx signal a pivot toward disintermediation, allowing drug makers to reclaim rebates and real-time data while maintaining price competitiveness.

In emerging markets, limited cold-chain logistics and low credit-card penetration delay e-pharmacy adoption, but smartphone growth and regional fulfillment centers point to gradual uptake from 2027 onward. Altogether, distribution is bifurcating into a high-touch retail tier and a low-cost digital tier, with online channels expected to command notable share of basal insulin market share by 2031 as telehealth integration matures

Geography Analysis

North America retained 43.89% of basal insulin market size in 2025, buoyed by Medicare copay caps but constrained by rapid GLP-1 substitution and biosimilar price pressure. Federal negotiation reducing semaglutide pricing significantly from 2027 will likely further shift formularies away from insulin. Capacity expansions Novo’s USD 4.1 billion North Carolina fill-finish plant and Lilly’s USD 3 billion Wisconsin site—hedge demand across insulin and incretin portfolios.

Asia-Pacific is projected to grow at a 6.32% CAGR, outpacing all regions. India’s March 2026 semaglutide patent lapse opened a flood of more than 50 branded generics, compressing GLP-1 prices and reshaping therapeutic sequencing. China’s regulatory reforms accelerate local biosimilar approvals; Sihuan’s degludec filing underlines domestic challengers to multinationals. Manufacturers invest more than USD 2 billion in regional plants to secure “local-for-local” supply and tariff advantages.

Europe and Middle East & Africa register mid-single-digit growth. Stringent interchangeability rules slow biosimilar penetration, while heterogeneous reimbursement frameworks fragment market access for novel formulations. Sanofi’s EUR 1.3 billion Frankfurt expansion (completion 2029) aims to support regional demand once Lantus and Toujeo biosimilars proliferate.

Competitive Landscape

Novo Nordisk, Eli Lilly, and Sanofi together command roughly majority of the basal insulin market, yet face dual threats: biosimilar price erosion and internal cannibalization by their own GLP-1 franchises. Novo’s insulin revenues now fund capacity expansions prioritizing Wegovy and Ozempic, relegating older insulins to cash-generation roles. Lilly’s USD 50 billion U.S. manufacturing build-out supports cross-subsidization, exploiting obesity-drug margins to defend insulin pricing. Sanofi, while growing double digits in emerging markets, cedes North American share to interchangeable biosimilars such as Semglee. Strategic advantage is migrating toward device ecosystems, vertical supply integration, and direct-to-consumer distribution. Medtronic’s InPen-Simplera loop and Dexcom-Novo smart-pen pairing create data-driven lock-ins. Online portals—Amazon Pharmacy, LillyDirect, and TrumpRx—bypass traditional pharmacy benefit managers, enabling full-margin capture and real-time demand insights.

Basal Insulin Industry Leaders

Eli Lilly and Company

Sanofi S.A.

Biocon Biologics Ltd

Wockhardt Ltd.

Novo Nordisk A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: FDA approved Novo Nordisk’s Awiqli, the first once-weekly basal insulin for adults with type-2 diabetes, after resolving manufacturing concerns.

- February 2026: FDA cleared Sanofi’s Merilog, the first rapid-acting insulin biosimilar in the United States, paving the way for basal-analogue biosimilars.

Global Basal Insulin Market Report Scope

As per the scope of the report, basal insulin, also known as background insulin, is a long-acting form of insulin designed to mimic the natural, steady trickle of the hormone that the pancreas releases throughout the day and night. Its primary purpose is to keep blood glucose levels stable during periods of fasting, such as while you are sleeping or between meals, by regulating the amount of sugar the liver releases into the bloodstream.

The basal insulin market is segmented by molecules, delivery devices, patient type, distribution channel, and geography. Based on molecules, the market is segmented into glargine, detemir, degludec, and others. By delivery devices, vials & syringes, pre-filled disposable pens, re-usable / smart pens, and pump-based basal delivery. Based on patient type, the market is segmented into type-1 diabetes, type-2 diabetes, and gestational diabetes. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies.

Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Glargine |

| Detemir |

| Degludec |

| Others |

| Vials & Syringes |

| Pre-filled Disposable Pens |

| Re-usable / Smart Pens |

| Pump-based Basal Delivery |

| Type-1 Diabetes |

| Type-2 Diabetes |

| Gestational Diabetes |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Molecule | Glargine | |

| Detemir | ||

| Degludec | ||

| Others | ||

| By Delivery Device | Vials & Syringes | |

| Pre-filled Disposable Pens | ||

| Re-usable / Smart Pens | ||

| Pump-based Basal Delivery | ||

| By Patient Type | Type-1 Diabetes | |

| Type-2 Diabetes | ||

| Gestational Diabetes | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast will the basal insulin market grow from 2026 to 2031?

It is forecast to expand at a 4.85% CAGR, rising from USD 7.7 billion in 2026 to USD 9.8 billion by 2031.

Which molecule currently leads global sales?

Glargine remains the largest contributor, accounting for 45.67% of value in 2025.

Why is Asia-Pacific the fastest-growing region?

Surging diabetes prevalence, rapid biosimilar approvals, and falling GLP-1 prices underpin a 6.32% CAGR to 2031.

How will once-weekly insulins affect future competition?

Awiqli’s approval and pipeline candidates like efsitora alfa are expected to capture up to notable share of volume by 2031, mainly among type-2 patients seeking simpler regimens.

Page last updated on: