Barium Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

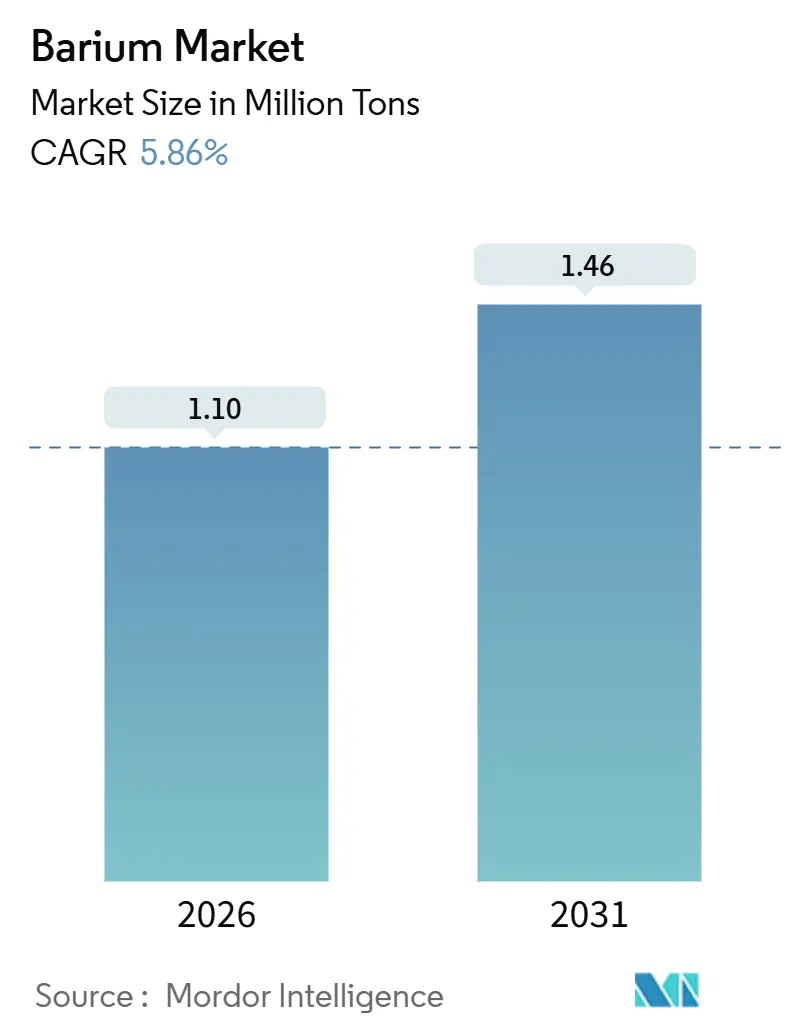

| Market Volume (2026) | 1.10 Million tons |

| Market Volume (2031) | 1.46 Million tons |

| Growth Rate (2026 - 2031) | 5.86% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

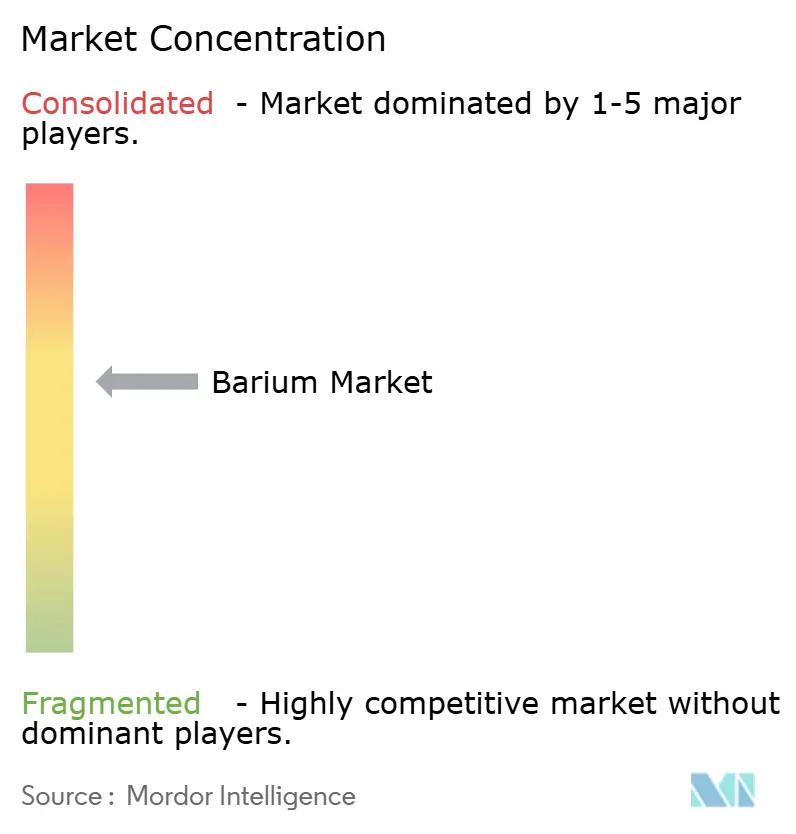

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Barium Market Analysis by Mordor Intelligence

The Barium Market size is estimated at 1.10 million tons in 2026 and is expected to reach 1.46 million tons by 2031, at a CAGR of 5.86% during the forecast period (2026-2031). Structural shifts, not commodity cycles, fuel this growth trajectory. Key drivers include rapid electronics miniaturization, stricter environmental regulations favoring lead-free fluxes, and consistent upstream drilling programs. Demand for drilling-grade barite aligns with rig counts. Concurrently, demand for multilayer ceramic capacitors (MLCCs) is on the rise. Each NVIDIA GB300 AI server needs significantly more MLCC units compared to a smartphone. Barium sulfate pigments are pivotal in creating zero-energy "cool-paint" coatings. These coatings can reflect nearly all incoming solar radiation. Academic models suggest that if applied to a portion of the world's surface, this technology could counteract current warming trends. The Asia-Pacific region accounts for a majority of global consumption, anchored by significant output from China and India. Together, they supply a substantial portion of U.S. imports.

Key Report Takeaways

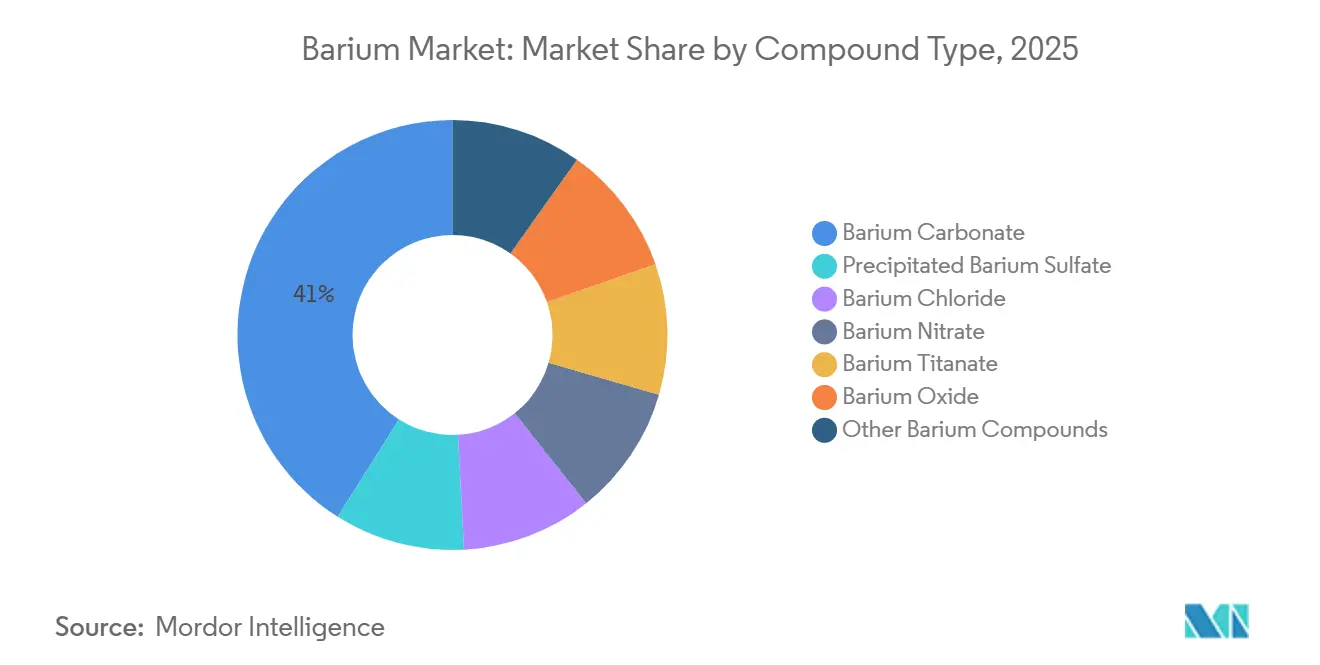

- By compound type, barium carbonate held 41.04% of 2025 volume and is forecast to grow at a 6.74% CAGR through 2031.

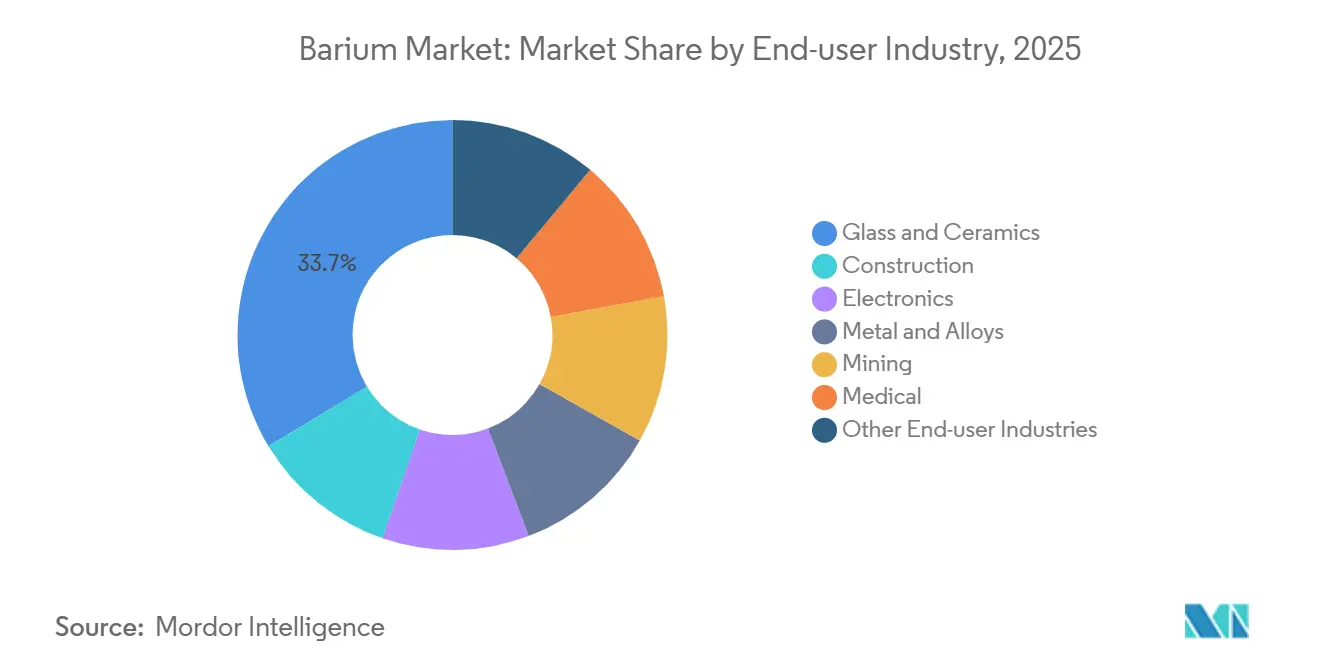

- By end-user industry, glass and ceramics held 33.67% of the 2025 volume, and electronics are projected to advance at a 7.85% CAGR to 2031, outpacing the overall Barium market.

- By geography, Asia-Pacific commanded 67.61% of 2025 consumption, while North America records the fastest regional growth at a 6.90% CAGR till 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Barium Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding use of barium compounds in construction materials and specialty coatings | +0.8% | Global, with concentration in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Structural growth in electronics and advanced ceramics (barium titanate) | +1.4% | Global, led by Asia-Pacific manufacturing hubs and North America data-center corridors | Long term (≥ 4 years) |

| Rising oil and gas drilling activity boosting demand for drilling-grade barite | +1.2% | North America (Permian Basin, Bakken), Middle East, Latin America offshore | Short term (≤ 2 years) |

| Emerging adoption of barium-based cool-paint technologies for urban heat mitigation | +0.6% | Global, early adoption in Middle East, Southern Europe, U.S. Sun Belt | Long term (≥ 4 years) |

| Nano-barium fillers for lightweight EV battery casings and radiation shielding | +0.5% | Asia-Pacific (China, Japan, South Korea), North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Use of Barium Compounds in Construction Materials and Specialty Coatings

In a bid to adhere to sulfate-resistant and low-toxicity standards, construction specifications are increasingly replacing lead additives with barium carbonate and barium sulfate. Research published in 2024 highlighted that barium carbonate nanoparticles can improve mortar compressive strength while simultaneously reducing water absorption[1]MDPI Editorial Board, “Barium Carbonate Nanoparticles for Sulfate-Resistant Concrete,” Buildings, mdpi.com. These high-performance concretes, tailored for extreme heat conditions, are being utilized in megaprojects under Saudi Vision 2030 and the UAE’s Expo City expansions. Additionally, precipitated barium sulfate has been found to diminish titanium dioxide loading in anticorrosive coatings. This reduction not only cuts formulation costs but also maintains opacity. As the industry shifts its focus from raw minerals to engineered fillers with precise particle-size control, producers investing in surface-modification technologies stand to gain significantly.

Structural Growth in Electronics and Advanced Ceramics (Barium Titanate)

Ferroelectric barium titanate plays a pivotal role in MLCC dielectrics, ensuring stable power delivery for AI servers, 5G base stations, and electric vehicles[2]Murata Manufacturing, “Investor Relations Briefing: MLCC Demand for AI Infrastructure,” Murata, murata.com. Murata forecasts a surge in MLCC demand for AI infrastructure in the coming years. In a significant move, Samsung clinched a U.S. patent in April 2025 for a groundbreaking formula that maintains capacitance beyond 150 °C, effectively addressing thermal throttling challenges in compact server racks. Hosokawa Micron boasts milling lines adept at producing 100-nanometer powders, essential for crafting ultrathin dielectric layers. Moreover, beyond its capacitor applications, this compound enhances ionic conductivity in solid-state batteries. As computing and energy storage evolve, the barium market is outpacing the growth of conventional ceramics.

Rising Oil and Gas Drilling Activity Boosting Demand for Drilling-Grade Barite

Drilling-grade barite, the primary weighting agent, plays a crucial role in maintaining hydrostatic pressure in well fluids. Baker Hughes reported active rigs in the U.S., marking a modest decline from the previous year. The Permian Basin, with numerous operating rigs, is now averaging laterals that lead to increased mud consumption per well. Demand surges from offshore projects in Latin America and the Middle East, where deepwater wells can require more barite volume compared to onshore horizontals. With the U.S. relying on imports for a significant portion of its barite, there's heightened vulnerability to fluctuations in Asian supply and freight rates. Furthermore, consolidation among shale operators is stabilizing procurement cycles, mitigating the boom-bust dynamics that once unsettled the Barium market.

Emerging Adoption of Barium-Based Cool-Paint Technologies for Urban Heat Mitigation

Ultrawhite paints, powered by barium sulfate pigments, reflect solar radiation and emit infrared heat. This innovation can reduce roof temperatures compared to traditional coatings (30331-1). Policy pilots in Saudi Arabia and U.S. cities like Phoenix reference solar-reflectance thresholds, which only barium sulfate formulations can meet in a cost-effective manner. The adoption of this technology is expected to drive significant growth in the barium market, expanding it beyond its traditional industrial confines.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concentrated barite supply base and raw-material disruption risk | -0.9% | Global, acute in North America and Europe dependent on Asian imports | Short term (≤ 2 years) |

| Stringent environmental and toxic-emission regulations on barium processing | -0.6% | Europe (REACH), North America (EPA), Asia-Pacific (emerging standards) | Medium term (2-4 years) |

| Escalating bulk-freight and container costs inflating delivered barite prices | -0.7% | Import-dependent markets: North America, Europe, parts of Middle East | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Concentrated Barite Supply Base and Raw-Material Disruption Risk

In 2024, China and India accounted for the majority of global barite production. Starting July 2025, China's revamped Mineral Resources Law will impose export quotas on strategic minerals. An earlier embargo on antimony led to a significant drop in U.S. supplies, causing prices to rise sharply. Given that the U.S. imports most of its barite, a similar embargo could either halt operations on rigs or necessitate expensive alternatives. While Morocco and Mexico contribute to the market, they fall short of matching the tonnage from Asia. This concentration of supply stands out as the most significant challenge for the barium market.

Stringent Environmental and Toxic-Emission Regulations on Barium Processing

Due to cardiovascular and renal risks associated with water-soluble barium salts, the U.S. EPA has established a reference dose. An EU anti-dumping investigation in August 2025, targeting Chinese and Indian barium carbonate, revealed emission non-compliance issues. These violations now necessitate expensive scrubbers and wastewater systems. In pursuit of ISO 14001 certification, Hebei Xinji invested significantly in a closed-loop water recycling system. As smaller producers contemplate exiting the market, the resulting supply constraints and heightened compliance costs are poised to depress the global barium market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Compound Type: Carbonate Dominance Anchors Glass and Ceramics Demand

Barium carbonate captured 41.04% of the barium market share in 2025 and is forecast to post 6.74% growth to 2031, comfortably outpacing the broader 5.86% trajectory. Producers are reaping the rewards of regulatory shifts that phase out lead fluxes in glass and ceramic glazes, leading to a pivot towards barium-based alternatives. This trend is also driving heightened interest in barium carbonate for optical glass, where its enhanced refractive index justifies a premium price. While barium titanate commands a smaller tonnage, its growth is swift; a rise in MLCC unit density translates to a surge in demand. Notably, Samsung's 2025 patent on high-temperature formulations highlights the sector's ongoing research and development commitment.

Precipitated barium sulfate finds its niche in coatings, plastics, and medical imaging, where its brightness and inertness command a price premium. Venator's establishment of additive plants underscores the scale needed to thrive in the engineered filler market. Meanwhile, barium chloride and barium nitrate play minor roles in heat treatment and pyrotechnics. Although barium oxide has seen a downturn in cathode-ray tubes, this decline is somewhat balanced by its use in catalysts and ferrite magnets. Other compounds, like barium hydroxide, serve as specialty intermediates with limited capacity expansions. This fragmentation among compound types is prompting integrated miners to ascend the value chain, bolstering their position in the Barium market.

By End-User Industry: Electronics Acceleration Outpaces Mature Glass and Ceramics

Electronics delivered a 7.85% CAGR, driven by AI servers demanding significant MLCC units per chassis. Dominating this sector, Nippon Chemical Industrial and Sakai Chemical utilize patented milling and calcination techniques to produce 100-nanometer powders with precise compositional tolerances. While glass and ceramics captured 33.67% of the barium market share in 2025, their growth is aligning more closely with the Barium market average. This shift comes as sanitary ware and container glass markets saturate in developed nations. Mining applications, often linked to drilling mud, are closely tied to rig-count health.

Construction demand is bolstered by the use of sulfate-resistant concrete and anticorrosive coatings, especially in the Middle East and coastal regions of Asia. While medical imaging remains a niche player, Bracco Diagnostics made headlines in December 2024 by introducing eco-friendly packaging to its VARIBAR line. Barium finds its way into metal and alloy applications for degassing and grain refining, both closely monitored by industrial production indices. This divergence in end-use highlights the need for producers to shift focus towards electronics and engineered fillers, maximizing their value in the Barium market.

Geography Analysis

Asia-Pacific accounted for 67.61% of the 2025 volume, driven by significant output from China and India, catering to both domestic industries and U.S. imports. China's updated Mineral Resources Law promotes stockpiling and capacity growth, pushing for added domestic value before exports. Guizhou Redstar pivoted from commodity chemicals to electronics-grade salts, achieving notable revenue in 2024. Hebei Xinji Chemical, with its plants and numerous patents, underscores the rising capital demands for environmental standards. Meanwhile, Japan's Nippon Chemical Industrial and Sakai Chemical are supplying high-purity titanate, solidifying Asia's lead from raw minerals to precision powders.

North America, while smaller, posts the fastest regional CAGR at 6.90%. Operators are actively maintaining Permian rigs and lengthening laterals, boosting barite usage per well. The U.S. leans heavily on imports, making buyers vulnerable to freight fluctuations and geopolitical tensions. Europe, while growing at a slower pace, holds strategic significance. Kandelium Group dominates, accounting for the entirety of the EU's barium carbonate output. However, even with anti-dumping duties on imports from China, the EU's dependence on this supply remains intact. In the Middle East and Africa, as well as South America, demand is closely linked to oil-field advancements and infrastructure initiatives, notably Saudi Vision 2030.

Competitive Landscape

The Barium market is moderately concentrated. Chinese state-owned producers integrate mining and processing to maintain cost leadership, while Japanese specialty companies command high-purity niches. Indian exporters hold ISO-accredited plants but face EU duties that compress margins. Consolidation in U.S. shale stabilizes demand, while EU tariffs push glassmakers to diversify sourcing away from high-duty Chinese carbonate. White-space opportunities appear in radiative-cooling paints and solid-state batteries, where current supply chains are thin and margins high, offering a route to diversify the Barium market beyond traditional industrial uses.

Barium Industry Leaders

Solvay

Hebei Xinji Chemical Group Co., Ltd.

Nippon Chemical Industrial Co., Ltd.

Guizhou Redstar Co., Ltd.

Vishnu Chemicals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Guizhou Redstar Co., Ltd announced a high-purity barium carbonate environmental-impact assessment for a 6,000 t/y line.

- November 2024: Cimbar Resources set a 3%–15% price increase on specialty minerals effective January 2025, covering industrial barium sulfate and other fillers.

Global Barium Market Report Scope

Primarily utilized in medical imaging, pyrotechnics, and oil drilling, barium, a versatile alkaline earth metal, also plays a crucial role in glass production and various industrial processes.

The barium market is segmented by compound type, end-user industry, and geography. By compound type, the market is segmented into precipitated barium sulfate, barium chloride, barium nitrate, barium titanate, barium oxide, barium carbonate, and other barium compounds. By end-user industry, the market is segmented into construction, electronics, metal and alloys, mining, medical, glass and ceramics, and other end-user industries. The report also covers the market size and forecasts in 16 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (Tons).

| Precipitated Barium Sulfate |

| Barium Chloride |

| Barium Nitrate |

| Barium Titanate |

| Barium Oxide |

| Barium Carbonate |

| Other Barium Compounds |

| Construction |

| Electronics |

| Metal and Alloys |

| Mining |

| Medical |

| Glass and Ceramics |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Compound Type | Precipitated Barium Sulfate | |

| Barium Chloride | ||

| Barium Nitrate | ||

| Barium Titanate | ||

| Barium Oxide | ||

| Barium Carbonate | ||

| Other Barium Compounds | ||

| By End-user Industry | Construction | |

| Electronics | ||

| Metal and Alloys | ||

| Mining | ||

| Medical | ||

| Glass and Ceramics | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the Barium market in 2026, and what is its CAGR?

The Barium market size reached 1.10 million tons in 2026 and is advancing at a 5.86% CAGR toward 2031, reaching 1.46 million tons.

Which compound holds the largest volume share?

Barium carbonate led with 41.04% volume share in 2025 and is on track for a 6.74% CAGR through 2031.

Why is electronics the fastest-growing end user for barium?

AI servers, 5G gear, and EV powertrains need more MLCC units exponentially, each relying on barium titanate dielectrics.

Which region grows fastest through 2031?

North America posts the quickest regional growth at a 6.90% CAGR, driven by resilient shale drilling and reshoring trends.

What is the main supply-side risk facing buyers?

High reliance on Chinese and Indian barite exposes importers to potential export quotas or freight disruptions that can spike prices.

Page last updated on: