Bangladesh Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

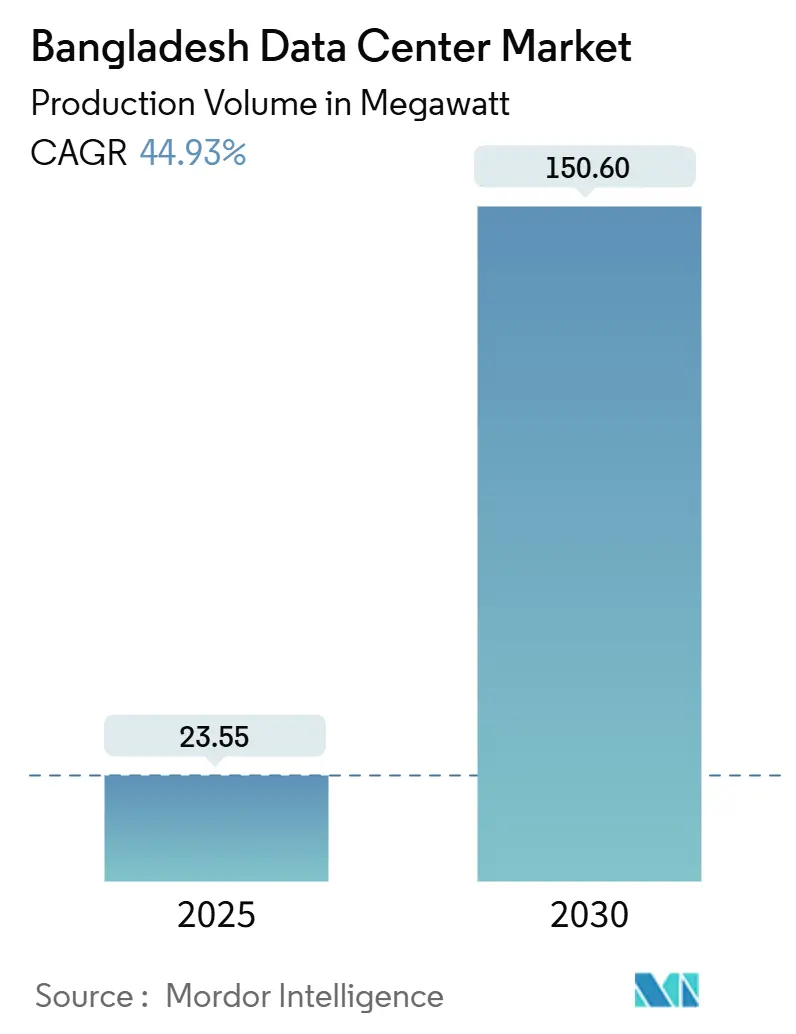

| Base Year Market Size (2025) | 23.55 megawatt |

| Market Volume (2025) | 23.55 megawatt |

| Market Volume (2030) | 150.60 megawatt |

| Growth Rate (2025 - 2030) | 44.93% CAGR |

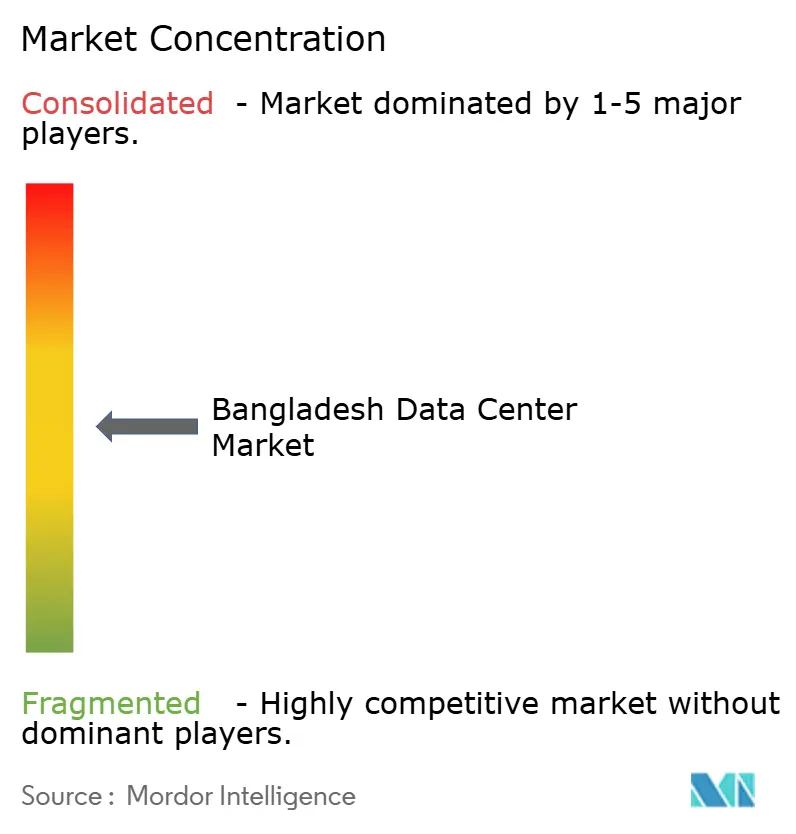

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bangladesh Data Center Market Analysis by Mordor Intelligence

The Bangladesh data center market size reached an installed IT load of 23.55 MW in 2025 and is forecast to hit 150.6 MW by 2030, translating into a 44.93% CAGR. The outlook is propelled by submarine-cable upgrades, public-sector digitization projects and cloud-localization mandates that collectively position the country as a regional interconnection node. Substantial new capacity is clustering around Dhaka while secondary cities accelerate as edge locations that reduce latency for 5G, e-commerce and fintech workloads. Global cloud platforms preparing Local Zone and Edge deployments view Bangladesh as the logical bridge between South and Southeast Asia, and their entry signals sustained hyperscale demand. At the same time, grid instability and high electricity tariffs compel operators to deploy sophisticated power-management schemes and to lobby for renewable power purchase agreements as the next competitive differentiator. Strategic investors now treat compliant Tier III and Tier IV capacity as prerequisite infrastructure for everything from public-sector digital health to private-sector OTT streaming.

Key Report Takeaways

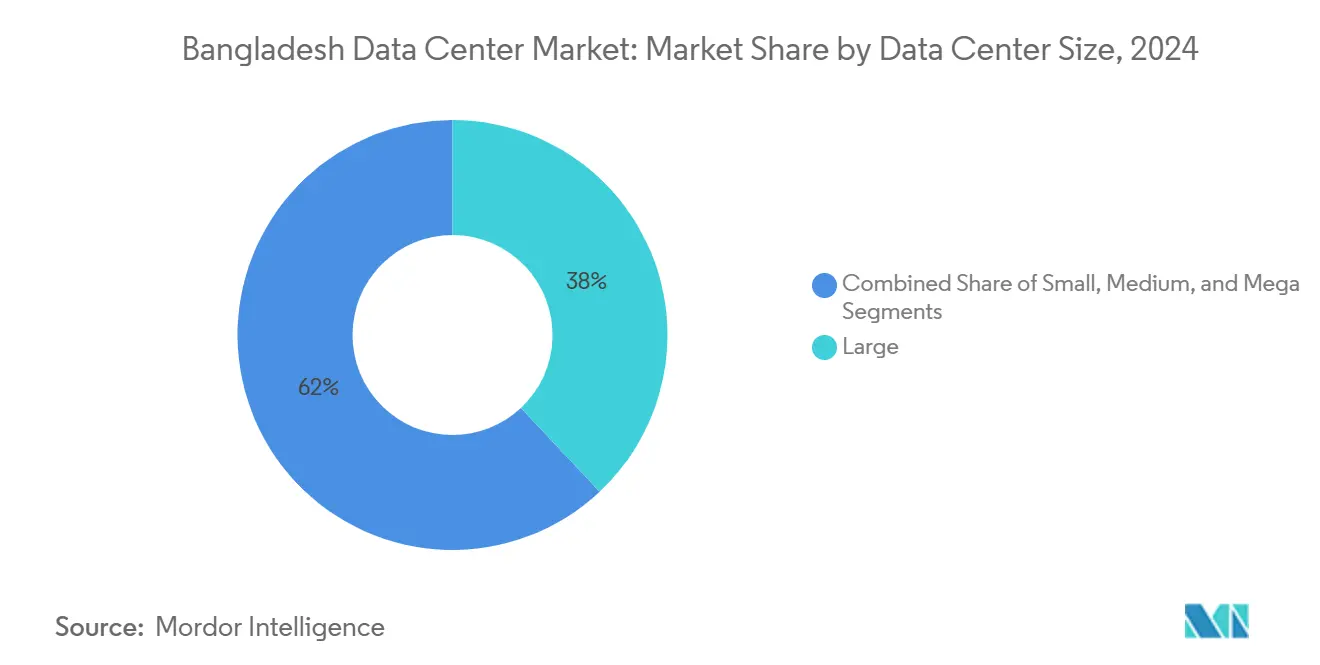

- By data-center size, large facilities held 38% of Bangladesh data center market share in 2024 while the mega-scale category is projected to expand at an 18.30% CAGR through 2030.

- By tier standard, Tier III captured 56% of the Bangladesh data center market size in 2024; Tier IV is advancing at a 16.40% CAGR through 2030.

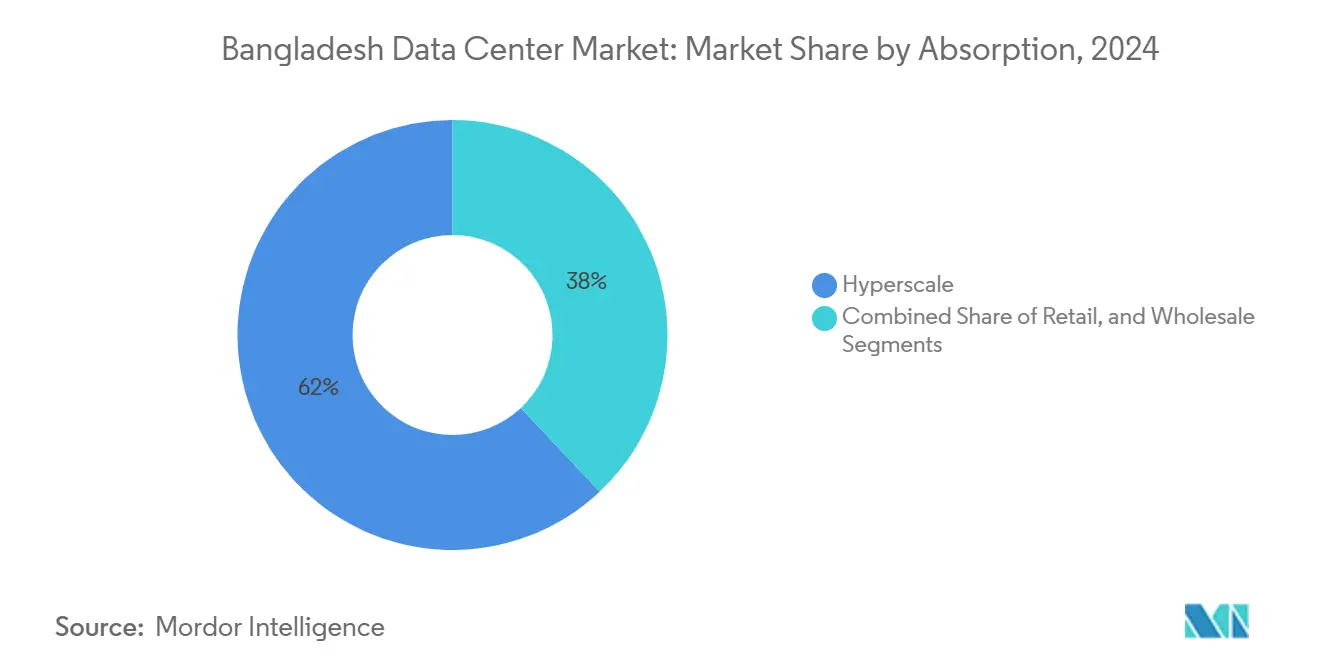

- By absorption, hyperscale colocation accounted for 62% share of the Bangladesh data center market in 2024, with cloud-service-provider utilization growing at a 17.80% CAGR to 2030.

- By hotspot, dhaka accounted for 49.00% share of the Bangladesh data center market in 2024, with sylhet and other cities utilization growing at a 18.70% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Bangladesh Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mobile-data boom and 5G rollout | +12.50% | National, early gains in Dhaka and Chattogram | Medium term (2-4 years) |

| Smart Bangladesh 2041 digital agenda | +10.80% | National, Dhaka core, spreading to tier-2 cities | Long term (≥ 4 years) |

| E-commerce, fintech & OTT traffic localization | +8.70% | Dhaka core, spill-over to Chattogram and Khulna | Short term (≤ 2 years) |

| Entry of global cloud platforms | +7.20% | Dhaka primary, selective tier-2 expansion | Medium term (2-4 years) |

| Dual landing of SEA-ME-WE 6 and IAX cables | +3.80% | National, primary benefits in Dhaka and Cox’s Bazar | Short term (≤ 2 years) |

| Data-sovereignty push from regulators | +2.30% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mobile-data boom and 5G rollout

Telecom subscriptions now exceed 190 million, yet only a fraction of devices are 5G-enabled, meaning network operators must densify their edge nodes before full consumer adoption. Grameenphone’s 2024 launch of a Super Core Data Center marks a significant step toward local traffic termination, which helps keep latency below 10 milliseconds.[1]Grameenphone, “Super Core Data Center Launch,” telecomtalk.info The Rural Connectivity Improvement Project further extends fiber backhaul across 64 districts, opening demand for micro-edge sites that complement Dhaka’s hyperscale footprint.

Smart Bangladesh 2041 digital agenda

More than 5,400 Union Digital Centers already deliver 150+ public and private digital services, cutting citizen transaction times by 85% and annual costs by 63%. The forthcoming National Blockchain Strategy requires geographically distributed ledger nodes, prompting ministries to reserve rack space in Tier III facilities. A USD 7.5 million startup fund earmarked for digital-governance infrastructure makes domestic colocation the default choice for e-government workloads.

Dual landing of SEA-ME-WE 6 and IAX cables improves latency

Bangladesh Submarine Cable Company Limited invested USD 80 million in the SEA-ME-WE 6 project, adding 7,200 Gbps of capacity that directly feeds Dhaka and Cox’s Bazar gateways. Lower round-trip times can shave 30 milliseconds off Singapore-Dhaka traffic, a critical threshold for high-frequency trading and real-time gaming platforms.

Data-sovereignty push from regulators

The Personal Data Protection Act classifies personally identifiable data as “Critical,” mandating that such data remain onshore. Regulators permit other categories to be mirrored abroad only when they are mapped back to a domestic primary node.[2]Government of Bangladesh, “National Blockchain Strategy,” bcc.portal.gov.bdThis framework locks in long-term demand for certified local capacity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid instability and high electricity tariffs | -8.20% | National, acute in industrial zones | Short term (≤ 2 years) |

| Limited domestic Tier III/IV talent | -4.50% | National, concentrated in technical roles | Medium term (2-4 years) |

| Scarcity of renewable PPAs | -2.80% | National | Long term (≥ 4 years) |

| Political-risk premium on financing | -1.70% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid instability and high electricity tariffs

Installed capacity exceeds 28 GW, yet distribution losses result in only 12–13 GW reaching end-users. Operators therefore oversize diesel backup, driving opex up by as much as 60% when global fuel prices spike.[3] Institute for Energy Economics and Financial Analysis, “Bangladesh Power Development Board reforms,” ieefa.orgData center CFOs are now approaching renewable developers for behind-the-meter solar arrangements, but policy hurdles are delaying utility-scale PPAs.

Limited domestic talent in Tier III/IV operations

Uptime-certified facilities require specialists in concurrent-maintainability protocols, yet local curricula seldom include data-center-specific modules. Operators often import expertise from Singapore or India at a 25–30% wage premium. Industry associations are lobbying universities to add modular courses that blend electrical engineering with facility management.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Size: Mega-Scale Facilities Drive Consolidation

The mega-scale category is on track for an 18.30% CAGR to 2030, outpacing all other sizes. The country’s National Data Center exemplifies economies of scale, operating with Tier IV redundancy and serving multiple ministries and foreign clients alike. Gennext Technologies has earmarked USD 500 million over five years for the Meghna Cloud complex, reinforcing that investors envision Bangladesh as an export-oriented digital hub. Large facilities continue to command 38% of Bangladesh data center market share thanks to integrated service portfolios suited to BFSI and telecom tenants. Medium-scale facilities feed regional government workloads, and small facilities remain relevant for local disaster-recovery nodes.

Demand for mega-scale builds dovetails with the incoming SEA-ME-WE 6 capacity, making Bangladesh an attractive gateway for content traversing India to Southeast Asia. To accommodate this traffic, operators design power shells that can host 100-kW racks and liquid-cooling loops. That design philosophy primes the Bangladesh data center market size for workstreams such as GPU-based inference clusters and high-density video transcoding.

By Tier Standard: Tier III Dominance Reflects Reliability Needs

Tier III sites satisfy mainstream enterprise appetites for 99.982% uptime, and they captured 56% of Bangladesh data center market share in 2024. Uptime Institute certification is frequently embedded in request-for-proposal checklists, especially among telecom operators rolling out 5G core and mobile-edge computing. Banking regulators likewise expect concurrent-maintainability for payment-switch infrastructure.

Tier IV builds grow at a 16.40% CAGR because certain banks and government agencies want fault-tolerant architectures that promise 99.995% availability. The National Data Center’s Tier IV status sets a public benchmark. Colocation providers such as CoLoCity Limited market dual-bus power and compartmentalized fire suppression to win premium tenants. Tier I and Tier II facilities linger in secondary towns where cost sensitivity trumps strict redundancy.

By Absorption: Hyperscale Colocation Leads Utilization

Hyperscale tenants occupied 62% of commissioned capacity in 2024. Their presence underpins the Bangladesh data center market size because they contract multi-megawatt halls on ten-year terms. In return, they demand low-latency connectivity to submarine cables and BDIX, plus expansion clauses for GPU-dense zones. Cloud-service-provider utilization rises at a 17.80% CAGR as Microsoft and Amazon populate Local Zones that keep regulated workloads domestic.

Retail colocation remains vital for SMEs that prefer opex-based models yet cannot comply with data-sovereignty rules if they host abroad. Wholesale colocation appeals to fintech and OTT firms needing cage-level segregation. Non-utilized capacity is deliberately built ahead of demand so that operators can offer immediate rack availability, which has become a differentiator whenever global cloud tenants execute rapid regional expansions.

By End-User: BFSI Sector Drives Premium Infrastructure

Banks, insurers and micro-finance providers anchor the premium end of the Bangladesh data center industry. IFIC Bank’s centralized security program reduced manual log review by three hours per day once it migrated to a Dhaka Tier III site. Cloud-native startups also expand aggressively, mirroring the capital influx into local fintech and e-commerce sectors.

Telecom operators position edge nodes as competitive assets that shave latency for 5G slices and IoT telemetry. Their internal workloads are migrating off aging on-premises facilities into purpose-built colocation halls that supply cross-connects to multiple subsea cable systems. Manufacturing-sector adoption remains early-stage, yet automation pilots in garment factories hint at future demand for private-cloud footprints hosted onshore.

Geography Analysis

Dhaka retains 49% of the Bangladesh data center market share on the strength of carrier-neutral meet-me rooms, proximity to the capital’s financial district and a talent pool of certified electrical and mechanical engineers. The National Data Center in nearby Kaliakoir adds Tier IV capacity that houses everything from electronic-government workloads to foreign customer disaster-recovery nodes.

Chattogram emerges as the alternate hub because its port connects maritime logistics, and its location provides direct access to coastal submarine cable landings. Lower real-estate costs make contiguous land parcels feasible here, so operators plot campuses that can scale beyond 50 MW. Khulna leverages agricultural supply-chain digitization programs, drawing e-commerce platforms that seek regional fulfillment centers.

Sylhet and other cities record the fastest growth at an 18.70% CAGR through 2030. Government initiatives such as Rural Connectivity Improvement seed fiber backhaul into every district, making edge node deployment economically viable. These distributed facilities improve national disaster-recovery postures by providing geographic diversity beyond Dhaka’s seismic zone and political concentration.

Competitive Landscape

Local incumbents such as Dhaka Colo and XeonBD remain influential because they understand the regulatory maze and cultivate relationships that accelerate permitting. Newer entrants including CoLoCity Limited and BDPEER differentiate on network density and automation. Foreign investors bring specialized design expertise and bigger balance sheets. Gennext Technologies’ USD 500 million commitment to Meghna Cloud is the largest foreign pledge yet and signals confidence in Bangladesh’s trajectory as a sub-regional traffic exchange point.

Competitive intensity rises as clients view Tier III redundancy and PUE below 1.5 as baseline expectations rather than differentiators. Operators therefore experiment with indirect evaporative cooling and lithium-ion battery strings to trim electricity bills and to meet evolving sustainability scorecards. BDx Data Centers’ accreditation under NVIDIA’s DGX-Ready program shows how AI-specific readiness now influences site selection.

Consolidation is likely because smaller firms struggle to finance successive capacity phases under stringent Tier standards. Those with sub-10 MW portfolios become acquisition targets for pan-Asian platforms seeking to establish a quick beachhead that complies with data-sovereignty rules.

Bangladesh Data Center Industry Leaders

Dhaka Colo

XeonBD

Coloasia Ltd (Global Fair Communications)

Nusratech Pte Ltd. (Gotipath)

Felicity IDC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Bangladesh issues a data-classification framework under the Personal Data Protection Act that mandates onshore storage of personally identifiable information, triggering fresh colocation demand.

- April 2025: BDx Data Centers secures NVIDIA DGX-Ready certification, positioning Bangladesh to host enterprise AI training clusters.

- March 2025: Starlink receives regulatory clearance for a local gateway under NGSO guidelines, expanding satellite backhaul options.

- March 2025: Meghna Cloud switches on phase 1 of Bangladesh’s first dedicated cloud data center, backed by USD 500 million over five years.

Bangladesh Data Center Market Report Scope

The Bangladesh Data Center Market Report is Segmented by Data Center Size (Small, Medium, Large, Mega, Massive), Tier Standard (Tier I and II, Tier III, and Tier IV), Absorption (Non-Utilized, Utilized (Colocation Type (Hyperscale, Retail, Wholesale), End-User (BFSI, Cloud Service Providers, E-Commerce, Government, Manufacturing, Media and Entertainment, Telecom, and Other End-Users)), and Hotspot (Dhaka, Chattogram, and Rest of Bangladesh). The Market Forecasts are Provided in Terms of Volume (MW Capacity).

| Small |

| Medium |

| Large |

| Mega |

| Massive |

| Tier I and II |

| Tier III |

| Tier IV |

| Non-Utilized | ||

| Utilized | By Colocation Type | Hyperscale |

| Retail | ||

| Wholesale | ||

| By End-User | BFSI | |

| Cloud Service Providers | ||

| E-Commerce | ||

| Government | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Telecom | ||

| Other End-Users | ||

| Dhaka |

| Chattogram |

| Rest of Bangladesh |

| By Data-Center Size | Small | ||

| Medium | |||

| Large | |||

| Mega | |||

| Massive | |||

| By Tier Standard | Tier I and II | ||

| Tier III | |||

| Tier IV | |||

| By Absorption | Non-Utilized | ||

| Utilized | By Colocation Type | Hyperscale | |

| Retail | |||

| Wholesale | |||

| By End-User | BFSI | ||

| Cloud Service Providers | |||

| E-Commerce | |||

| Government | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Telecom | |||

| Other End-Users | |||

| By Hotspot | Dhaka | ||

| Chattogram | |||

| Rest of Bangladesh | |||

Key Questions Answered in the Report

What is the projected IT-load capacity for Bangladesh data centers by 2030?

Installed capacity is forecast to reach 150.6 MW by 2030, reflecting a 44.93% CAGR.

Which segment currently dominates capacity absorption?

Hyperscale colocation holds 62% of utilized capacity, driven by global cloud entrants.

How does the Personal Data Protection Act influence infrastructure demand?

It mandates onshore storage for personally identifiable data, locking in domestic colocation requirements and accelerating capacity growth.

Why is power pricing a critical issue for operators?

Distribution losses and reliance on imported fuels raise electricity tariffs, adding up to 60% to operational expenditure for diesel-backed resiliency.

Which city offers the highest growth potential outside Dhaka?

Sylhet and other tier-2 cities are expanding at an 18.70% CAGR as edge nodes roll out alongside nationwide 5G coverage.

Page last updated on: