Balloon Inflation Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

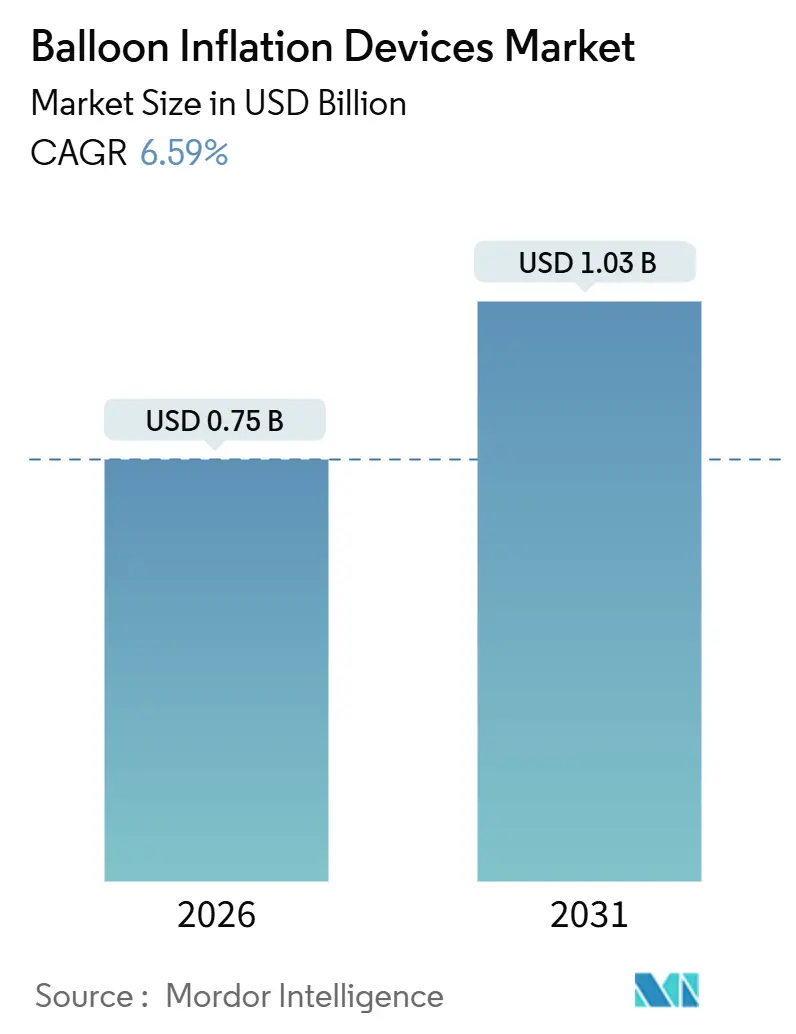

| Market Size (2026) | USD 0.75 Billion |

| Market Size (2031) | USD 1.03 Billion |

| Growth Rate (2026 - 2031) | 6.59% CAGR |

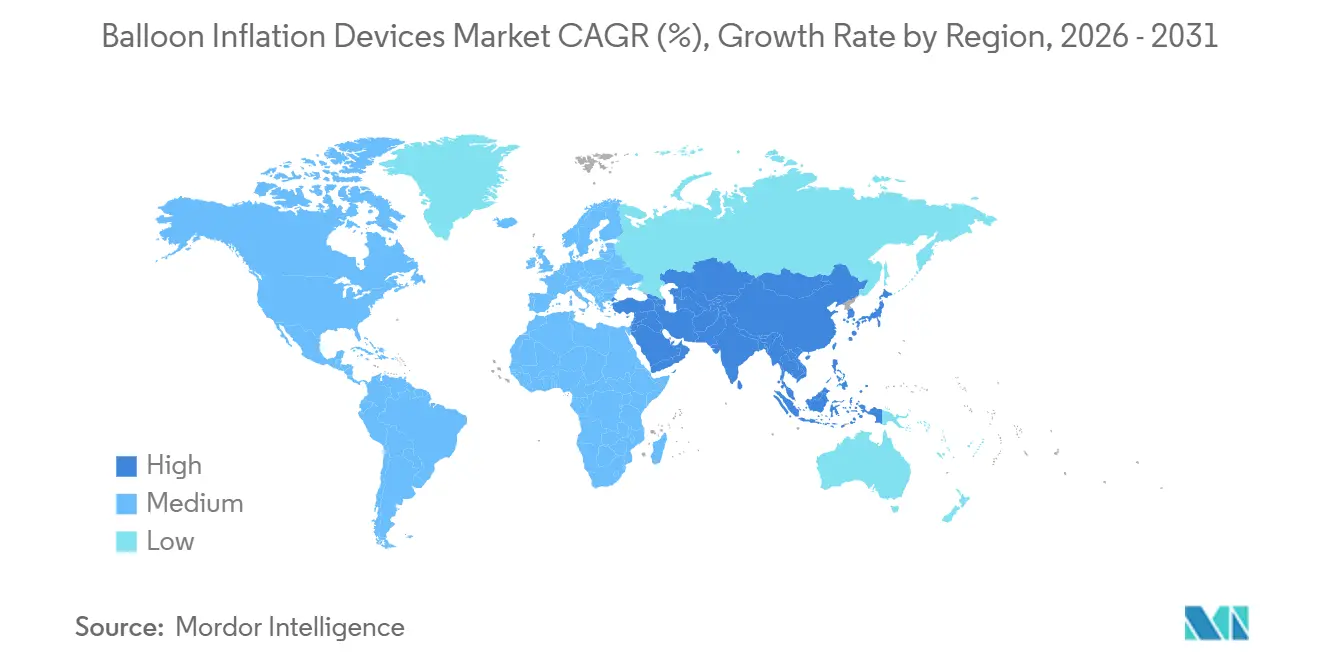

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Balloon Inflation Devices Market Analysis by Mordor Intelligence

The Balloon Inflation Devices Market size is estimated at USD 0.75 billion in 2026, and is expected to reach USD 1.03 billion by 2031, at a CAGR of 6.59% during the forecast period (2026-2031).

Demand is anchored by the global rise in cardiovascular disease and the steady shift from open surgery to minimally invasive interventions, both of which sustain procedure volumes that rely on precise pressure delivery. Rapid analog-to-digital migration is reshaping procurement priorities as hospitals value real-time data capture and integration with cath-lab informatics. Regulatory pressure for single-use sterility is enlarging disposable volumes, while Asia-Pacific infrastructure expansion is tilting growth momentum toward high-volume emerging markets. Competitive dynamics increasingly reward vendors that add software value, optimize supply chains for PFAS-free polymers, and localize production to manage currency and tariff risks.

Key Report Takeaways

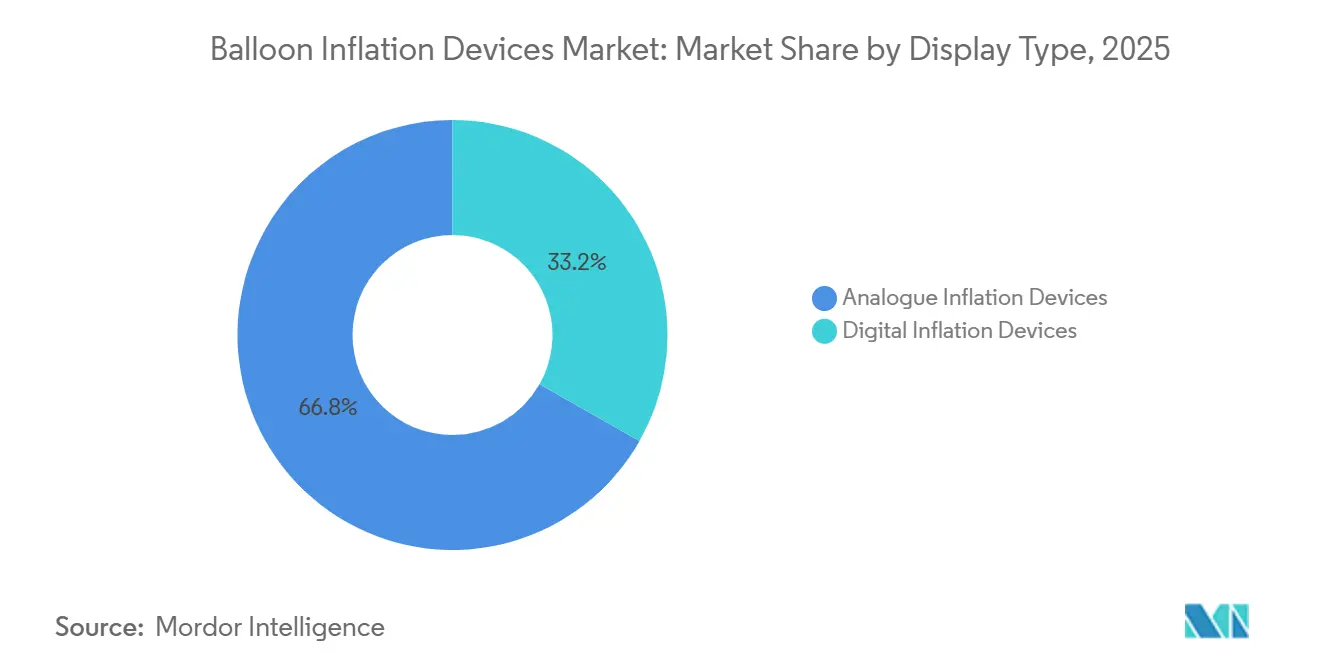

- By display type, analogue inflation devices captured 66.81% of the balloon inflation devices market share in 2025, whereas digital systems are forecast to expand at a 7.09% CAGR through 2031.

- By capacity, the 60 mL capacity segment led with 41.57% of the balloon inflation devices market size in 2025, while 30 mL units are projected to post the fastest 7.78% CAGR between 2026 and 2031.

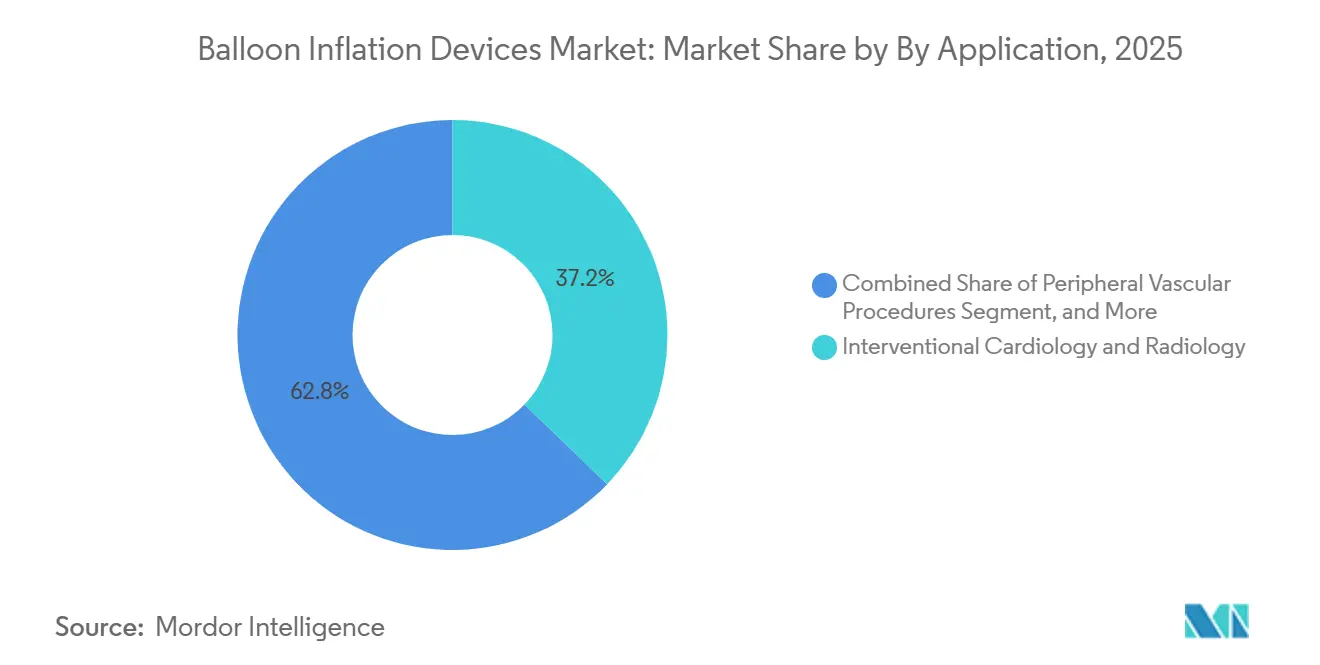

- By application, interventional cardiology and radiology accounted for 37.22% of the balloon inflation devices market in 2025, but peripheral vascular procedures are set to record a 9.69% CAGR through 2031.

- By end user, hospitals and clinics dominated the balloon inflation device market with 68.93% of the market share in 2025, yet ambulatory surgical centers are expected to grow at an 8.27% CAGR through 2031.

- By geography, North America commanded 41.83% balloon inflation devices market share in 2025, while Asia-Pacific is on track for the highest 10.27% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Balloon Inflation Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden of Cardiovascular Diseases | 1.8% | Global, with highest impact in North America, Europe, and APAC urban centers | Long term (≥ 4 years) |

| Growing Adoption of Minimally-Invasive Procedures | 1.5% | Global, led by North America and Western Europe, expanding in APAC | Medium term (2-4 years) |

| Technological Shift to Digital Pressure-Monitor Systems | 1.2% | North America and EU, with spillover to APAC tier-1 hospitals | Short term (≤ 2 years) |

| Surging Demand for 60 mL Devices in Complex Peripheral Cases | 0.9% | North America, Europe, and APAC interventional centers | Medium term (2-4 years) |

| Integration of Inflation Data Into Cath-Lab AI Analytics | 0.7% | North America and select EU markets | Short term (≤ 2 years) |

| Regulatory Push Toward Single-Use Sterile Disposables | 0.6% | Global, with strongest enforcement in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Cardiovascular Diseases

Cardiovascular disease causes 17.9 million deaths each year, and the Global Burden of Disease Study reported 523 million prevalent cases in 2019. The clinical workload translates directly into balloon angioplasty, stent, and valvuloplasty procedures, each of which requires an inflation device. Hospitals in high-income economies sustain baseline demand, while in emerging markets, procedure growth is double-digit as catheter laboratories open outside capital cities. Procurement teams in lower-middle-income countries remain price sensitive, which preserves share for analog devices in early adoption stages vendors with broad geographic footprints hedge against localized reimbursement volatility and currency swings. Over the long term, rising obesity and diabetes prevalence will keep the interventional pipeline active, cementing a durable need for both disposable and reusable inflation devices.

Growing Adoption of Minimally Invasive Procedures

Catheter-based techniques now dominate first-line therapy for coronary and peripheral artery disease because they shorten hospital stays and speed patient recovery. A multicenter series covering 4,243 transseptal mitral valve-in-valve procedures achieved a 97.1% device success rate, underscoring the maturity of balloon‐expandable technology.[1]Brian Whisenant et al., “Outcomes of Transseptal Mitral Valve-in-Valve and Valve-in-Ring Procedures,” JACC: Cardiovascular Interventions, JACC.ORG Each minimally invasive step relies on precise inflation control for lesion preparation, stent deployment, or valve expansion. High-volume hybrid operating rooms tend to use digital inflation devices that feed data directly into electronic health records and quality dashboards. Community hospitals and resource-constrained facilities keep analog units in service to manage upfront costs, but capital budget cycles increasingly include digital upgrades as case complexity grows. The cumulative effect is volume expansion across acuity tiers that sustains growth even as per-case device counts plateau.

Technological Shift to Digital Pressure-Monitor Systems

Digital inflation devices incorporate pressure sensors, automated inflation and deflation protocols, and data-logging functions that align with value-based care metrics. The U.S. FDA lists ISO 10555-4 as a recognized consensus standard, reinforcing demand for traceable pressure data.[2]U.S. Food and Drug Administration, “Recognized Consensus Standards: ISO 10555-4,” FDA.GOV Leading hospitals link inflation consoles to cath-lab analytics, using pressure curves to audit procedural quality and operator technique. Premium pricing is offset by workflow gains, reduced operator variability, and stronger documentation during accreditation audits. For manufacturers, digital migration raises R&D outlays and lengthens regulatory submissions, but it also elevates margins and erects feature-based barriers against low-cost analog competitors. Modular upgrade kits that retrofit existing analog handles mitigate switching costs for budget-constrained centers and accelerate installed-base conversion.

Surging Demand for 60 mL Devices in Complex Peripheral Cases

Long-segment femoropopliteal lesions and large-diameter iliac arteries require high inflation volumes to achieve uniform vessel wall contact. Drug-coated balloons and scaffolds often specify 60 mL syringes to maintain target pressure during therapeutic dwell times. The 60 mL class secured 41.57% market share in 2025, reflecting entrenched use among interventional radiologists and vascular surgeons. Despite the headline share, operators increasingly select 30 mL devices for mid-distal tibial work to reduce contrast load, radiation exposure, and consumable cost. Device makers respond with modular barrel designs that allow chair-side exchange from 20 mL to 60 mL without replacing the inflation handle, trimming inventory, and aligning capacity with lesion anatomy. As peripheral interventions climb in emerging economies, the 60 mL category will remain the workhorse for long-lesion therapy, sustaining a meaningful contribution to overall market expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Per-Unit Cost & Reimbursement Gaps | -1.1% | Global, with acute impact in emerging markets and rural North America | Medium term (2-4 years) |

| Stringent Global Regulatory Approvals & Re-Approvals | -0.8% | Global, with highest friction in EU (MDR) and North America (FDA 510(k) updates) | Long term (≥ 4 years) |

| Drug-Eluting Stents Shortening Balloon Dwell Times | -0.6% | North America and EU, where DES penetration exceeds 80% | Medium term (2-4 years) |

| PFAS-Related Polymer Supply Disruptions | -0.5% | Global, with supply-chain concentration in North America and Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Per-Unit Cost & Reimbursement Gaps

Digital inflation devices list between USD 200 and USD 800, a burden for hospitals paid under bundled or capitated models. In several Asian and Latin American markets, out-of-pocket payments remain common, steering clinicians toward reusable analog units rather than single-use digital options. Medicare annual updates can either buoy or depress U.S. demand depending on whether inflation devices receive separate reimbursement or fall inside a procedure bundle. To bridge affordability, vendors deploy tiered product lines, leasing plans, and consignment inventory. These tools soften capital shocks but compress gross margins, particularly when component costs rise due to polymer supply constraints. Unless payers increase device-specific allowances, price sensitivity will temper penetration of premium digital consoles in mid-tier facilities.

Stringent Global Regulatory Approvals & Re-Approvals

The FDA Quality Management System Regulation, effective in February 2026, tightens design control, clinical evidence, and post-market reporting for Class II devices, including balloon inflators.[3]U.S. Food and Drug Administration, “Class II Special Controls Guidance Documents,” FDA.GOV In Europe, the Medical Device Regulation extends certification timelines and expands documentation demands, straining small manufacturers. Compliance costs lengthen development cycles, elevate submission fees, and redirect engineering resources toward validation tasks. Market incumbents spread these costs across larger revenue bases, while startups face prohibitive entry barriers. Hospitals benefit from reduced recall risk, yet fewer fresh models reach the shelf, trimming competitive variety. Over the long term, harmonization efforts could streamline dual filings, but in the short term, regulatory friction hinders rapid portfolio refreshes and swift geographic expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Display Type: Digital Gains Ground

Analogue devices held 66.81% of the balloon inflation devices market share in 2025, securing their position in cost-sensitive community hospitals that value mechanical durability and zero power dependence. These bourdon-gauge units require limited maintenance and support reuse policies where sterilization infrastructure is robust. In parallel, digital inflation devices are forecast to climb at a 7.09% CAGR from 2026 to 2031. Digital consoles log every pressure increment, integrate with electronic medical records, and satisfy audit requirements for procedural traceability, traits that appeal to high-volume cardiovascular centers. Developed markets such as the United States, Germany, and Japan lead digital adoption because value-based payment models reward efficiency and outcome documentation. In emerging economies, hybrid upgrades, analog handles fitted with clip-on digital modules, enable gradual conversion within tight capital budgets. Competitive positioning rests on offering seamless user interfaces, long-lasting battery endurance, and software updates that extend the console's lifespan.

Second, the uptake of digital systems correlates with the spread of advanced imaging platforms such as intravascular ultrasound and optical coherence tomography. Physicians favor synchronized displays that overlay pressure readouts with live imaging to refine stent or valve positioning. Vendors that deliver plug-and-play interoperability with cath-lab monitors forge stickier customer relationships. Analog providers defend their share by emphasizing cost per use and straightforward service requirements. Long term, the digital share will continue its climb as refurbished units seep into secondary markets, yet analog devices will maintain relevance where electricity supply is unreliable, or procurement budgets remain constrained.

By Capacity: Mid-Range Devices Accelerate

The 60 mL segment accounted for 41.57% of the balloon inflation devices market in 2025, driven by widespread use in femoropopliteal and iliac artery procedures, where extensive lesion lengths demand large inflation reservoirs. Nevertheless, 30 mL devices are anticipated to lead growth with a 7.78% CAGR through 2031 as operators tailor capacity to lesion anatomy and procedural goals. Evidence from complex structural heart cases, including transseptal mitral valve-in-valve implants with 97.1% success rates, highlights the need for precise pressure modulation rather than sheer volume. Mid-range syringes reduce contrast usage, lower radiation exposure, and shorten case duration, outcomes that align with hospital efficiency metrics. Modular systems that allow clinicians to swap 20 mL, 30 mL, or 60 mL barrels onto a standard handle minimize SKU proliferation and lower inventory carrying costs.

Clinically, drug-coated balloon protocols in peripheral artery disease specify inflation times that are easier to control with mid-range syringes, aiding consistent drug diffusion across vessel walls. Operationally, supply chain managers favor capacity consolidation to streamline ordering and prevent stockouts. Manufacturers that deliver quick-release barrel locks and ergonomic plungers enhance staff satisfaction among those who handle multiple peripheral cases daily. While 20 mL devices remain critical in pediatrics and coronary segments, the market narrative through 2031 centers on balancing 30 mL versatility against 60 mL dominance in large-diameter vascular repairs.

By Application: Peripheral Vascular Surges

Interventional cardiology and radiology accounted for 37.22% of the balloon inflation devices market in 2025, as coronary artery disease remains the single most significant indication cohort. Yet peripheral vascular procedures will expand at a 9.69% CAGR from 2026 to 2031, lifted by rising diabetes prevalence, aging populations, and improved reimbursement for endovascular therapies. Peripheral artery disease is estimated to affect 200 million people globally, often remaining undiagnosed until critical limb ischemia, thus presenting a sizable intervention backlog. As hospital systems launch limb-salvage programs, demand for long-balloon catheters and corresponding large-capacity inflators intensifies. Vendors that bundle peripheral balloons, guidewires, and inflators under a volume-discount contract can lock in share and simplify procurement for newly established vascular centers.

Growth in peripheral work also reduces the historical dependency on coronary volumes, insulating suppliers from cyclical stent pricing swings. Structural heart innovations, including balloon-expandable aortic and mitral valves, layer incremental demand by requiring high-pressure deliveries. Gastro-enterological, urological, and assorted niche applications collectively account for a smaller share, yet they reward device makers that customize inflation tips or pressure profiles for unique anatomical pathways. This breadth of indications spreads regulatory risk and smooths quarterly revenue fluctuations.

By End User: ASCs Gain Momentum

Hospitals and clinics accounted for 68.93% of the balloon inflation device market in 2025, as they house the imaging suites and acute-care capacity needed for complex cardiovascular interventions. Nonetheless, ambulatory surgical centers (ASCs) are forecast to grow at an 8.27% CAGR through 2031, following recent reimbursement policy updates that moved several diagnostic angiography and low-risk peripheral angioplasty procedures to the outpatient list. ASCs favor single-use disposable inflators that eliminate reprocessing overhead and simplify accreditation audits. Disposable demand is reinforced by the FDA Quality Management System Regulation of 2026, which elevates documentation for sterilization validation.

Procurement patterns differ between the channels. Hospital purchasing committees emphasize interoperability with existing cath-lab networks and demand enterprise-level pricing. ASC chains and office-based labs focus on procedural throughput, preferring inflators packaged with catheters and guidewires in a cost-per-case kit. Specialty centers such as cardiac day hospitals and mobile cath units round out end-user diversity, each with tailored preferences for device footprint, portability, and battery life. Vendors that field dedicated ASC sales teams and align packaging sizes with outpatient inventory constraints are well-positioned to capitalize on this fastest-growing channel.

Geography Analysis

North America accounted for 41.83% of global revenue in 2025, supported by dense catheter-laboratory networks, widespread insurance coverage, and early adoption of digital inflators that interface with electronic health records. The United States drives regional value, while Canada and Mexico contribute steady incremental growth as they expand cardiovascular infrastructure in secondary cities. FDA rule updates arriving in 2026 may lengthen approval timelines for new entrants, reinforcing incumbent advantages and compressing small-firm participation. Growth will moderate as hospital price pressure intensifies, yet replacement demand and procedural complexity will sustain revenue stability.

Asia-Pacific is projected to post a 10.27% CAGR as China’s Healthy China 2030 plan and India’s Ayushman Bharat initiative scale tertiary cardiovascular care across provincial hubs. Public funding for stroke and chest-pain centers increases cath-lab installs, escalating inflator demand from a low installed base. Urban hospitals in China and South Korea rapidly adopt digital consoles, while rural facilities rely on analog imports or local assembly. Vendors that establish local manufacturing through joint ventures qualify for favorable tariffs and meet localization quotas, improving price competitiveness. Eventual analog-to-digital migration in tier-2 cities promises a second growth wave beyond the forecast horizon.

Europe, the Middle East and Africa, and South America supply the remainder of global revenue. Europe wrestles with lengthy MDR certification queues that slow portfolio refreshes but reward enterprises with strong regulatory teams. Germany, France, and the United Kingdom anchor volume, although price caps under national health systems restrain premium device penetration. Gulf Cooperation Council states invest heavily in cardiovascular capacity, creating pockets of high-margin demand within the Middle East. South Africa and Nigeria show latent potential yet move gradually due to budget limitations. In South America, Brazil and Argentina benefit from public-private financing models that co-fund cath-lab expansions, though currency volatility adds ordering uncertainty.

Competitive Landscape

The balloon inflation devices industry is moderately concentrated, with Boston Scientific, Medtronic, B. Braun, Terumo, and Teleflex accounting for the majority of global revenue. Their competitive advantage stems from vertically integrated portfolios that couple inflators with balloons, guidewires, and imaging systems, simplifying procurement under single-source contracts. Incumbents refresh products incrementally by adding ergonomic plungers, more responsive pressure sensors, and Bluetooth data offloads that feed hospital analytics. Smaller challengers exploit niche openings by offering cloud-based pressure dashboards, AI-driven inflation protocols, and PFAS-free polymer barrels that anticipate regulatory shifts. Subscription pricing models that bundle hardware, disposables, and software aim to lower acquisition barriers for mid-tier facilities.

Strategic differentiation now leans heavily on software. Vendors that deliver firmware updates and analytics modules without hardware swap-outs prolong console lifecycles and secure maintenance revenue. Regulatory tightening by the FDA and EU favors companies with mature quality systems, creating acquisition targets among niche innovators who lack global compliance breadth. Supply chain resilience is rising in strategic priority, with manufacturers dual-sourcing critical O-rings and syringe-barrel resins to hedge against potential PFAS curbs. Enterprises that blueprint regional assembly in Asia and Latin America gain tariff advantages and shorten lead times for rapidly growing markets. As hospital groups renegotiate purchasing agreements every two to three years, brand loyalty hinges on a mix of device performance, software upgrade cadence, and post-sale training quality.

The landscape remains dynamic. In 2025, Terumo demonstrated high-pressure balloon dilatation performance in complex coronary lesions, reinforcing its reputation as a leader in next-generation coronary tools. Teleflex faced a 2024 inflation-related recall that prompted process audits yet underscored its commitment to transparent field-corrective action. Boston Scientific and Medtronic continue to cross-sell inflators during drug-coated balloon adoption campaigns, leveraging broad call-points across cardiology, radiology, and peripheral vascular surgery. Meanwhile, startups equipped with remote-update dashboards court data-driven hospitals willing to pilot AI-adjusted pressure algorithms that could standardize procedural quality across operator skill levels.

Balloon Inflation Devices Industry Leaders

Ambu A/S

Becton, Dickinson and Company

Boston Scientific Corporation

Olympus Corporation

Teleflex Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Terumo highlighted clinical experience with Takeru PTCA Balloon Dilatation Catheters across complex coronary lesions, advancing next-generation coronary therapy.

- March 2025: Fujifilm commercialized a new double-balloon enteroscopy scope that enables advanced small-bowel diagnostics in gastroenterology suites.

- February 2025: Cagent Vascular introduced the Serranator SL-PRO PTA Serration Balloon Catheter to improve linear scoring along vessel walls and enhance drug transfer efficiencies.

- June 2024: Teleflex and Arrow International issued a recall for selected intra-aortic balloon catheter kits after manufacturing inspections revealed incomplete inflation performance.

Global Balloon Inflation Devices Market Report Scope

The Balloon Inflation Devices Market Report is Segmented by Display Type (Analogue Inflation Devices, Digital Inflation Devices), Capacity (20 mL, 30 mL, 60 mL), Application (Interventional Cardiology & Radiology, Peripheral Vascular Procedures, Gastro-enterological Procedures, Urological Procedures, Others), End User (Hospitals & Clinics, Ambulatory Surgical Centers, Specialty Centres, Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Analogue Inflation Devices |

| Digital Inflation Devices |

| 20 mL |

| 30 mL |

| 60 mL |

| Interventional Cardiology & Radiology |

| Peripheral Vascular Procedures |

| Gastro-enterological Procedures |

| Urological Procedures |

| Others |

| Hospitals & Clinics |

| Ambulatory Surgical Centers |

| Specialty Centres |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Display Type | Analogue Inflation Devices | |

| Digital Inflation Devices | ||

| By Capacity | 20 mL | |

| 30 mL | ||

| 60 mL | ||

| By Application | Interventional Cardiology & Radiology | |

| Peripheral Vascular Procedures | ||

| Gastro-enterological Procedures | ||

| Urological Procedures | ||

| Others | ||

| By End User | Hospitals & Clinics | |

| Ambulatory Surgical Centers | ||

| Specialty Centres | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the balloon inflation devices market by 2031?

The balloon inflation devices market size is expected to reach USD 1.03 billion by 2031.

Which display technology is growing the fastest?

Digital inflation devices are forecast to grow at a 7.09% CAGR as hospitals seek real-time data integration.

Why are ambulatory surgical centers important for future demand?

ASCs are shifting lower-acuity angiography and angioplasty procedures to the outpatient setting, driving an 8.27% CAGR in device adoption.

Which geographic region offers the highest growth rate?

Asia-Pacific leads with a 10.27% CAGR, driven by significant public investments in cardiovascular infrastructure.

How are regulations influencing product development?

Stricter FDA and EU rules raise documentation and traceability requirements, nudging vendors toward single-use, digitally traceable inflation devices.

Page last updated on: