Bahrain Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

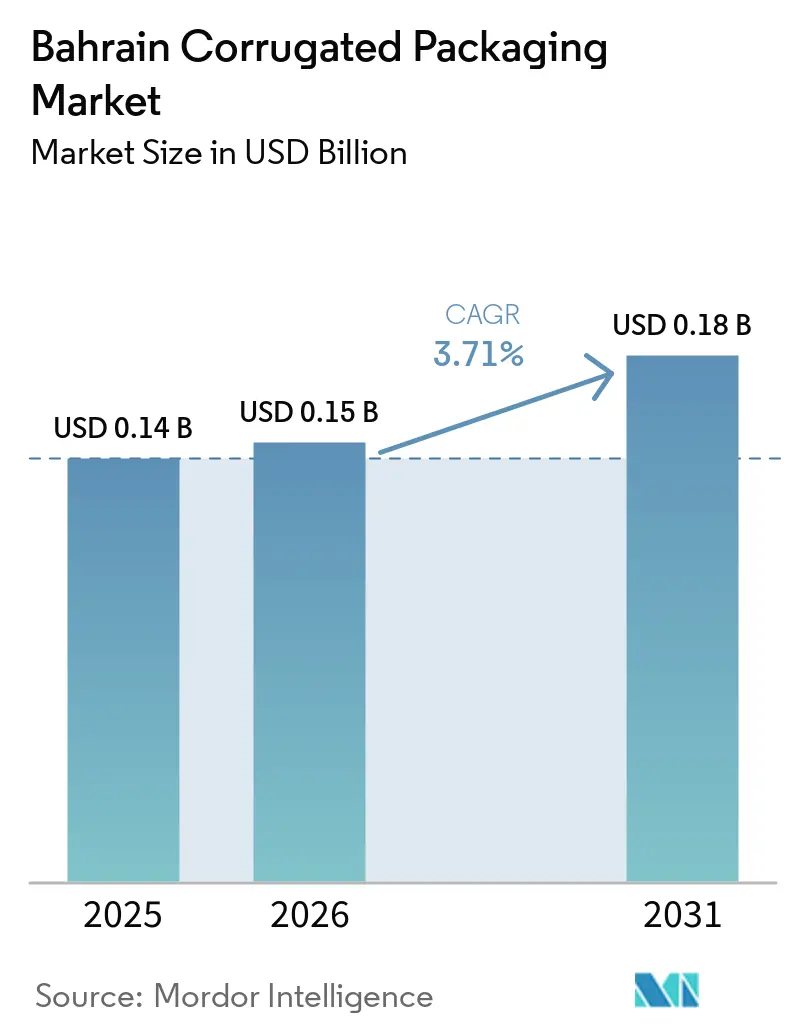

| Base Year Market Size (2025) | USD 0.14 Billion |

| Market Size (2026) | USD 0.15 Billion |

| Market Size (2031) | USD 0.18 Billion |

| Growth Rate (2026 - 2031) | 3.71% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bahrain Corrugated Packaging Market Analysis by Mordor Intelligence

The Bahrain corrugated packaging market size is expected to grow from USD 0.14 billion in 2025 to USD 0.15 billion in 2026 and is forecast to reach USD 0.18 billion by 2031, expanding at a 3.71% CAGR over 2026-2031. Local demand remains closely linked to food imports, which supply more than 90% of domestic consumption, while the Industrial Sector Strategy 2022-2026 channels investment into downstream aluminum, petrochemical, and FMCG production, thereby multiplying box requirements. Converters capitalize on Tamkeen subsidies that cover up to half of automation or digital-printing costs, yet their profitability stays vulnerable to ocean-freight surcharges and kraftliner spot-price swings because every containerboard tonne must still cross a border. GCC mills that will add roughly 250,000 tonnes of recycled liner and fluting capacity by 2027 strengthen regional supply security, but they also sharpen price competition as new entrants court Bahraini accounts. Corporate sustainability targets and Bahrain’s Green Factory Seal incentives accelerate spending on energy-efficient corrugators, closed-loop water systems, and FSC-certified sourcing, reinforcing the long-term shift away from plastic and toward lightweight recycled grades.

Key Report Takeaways

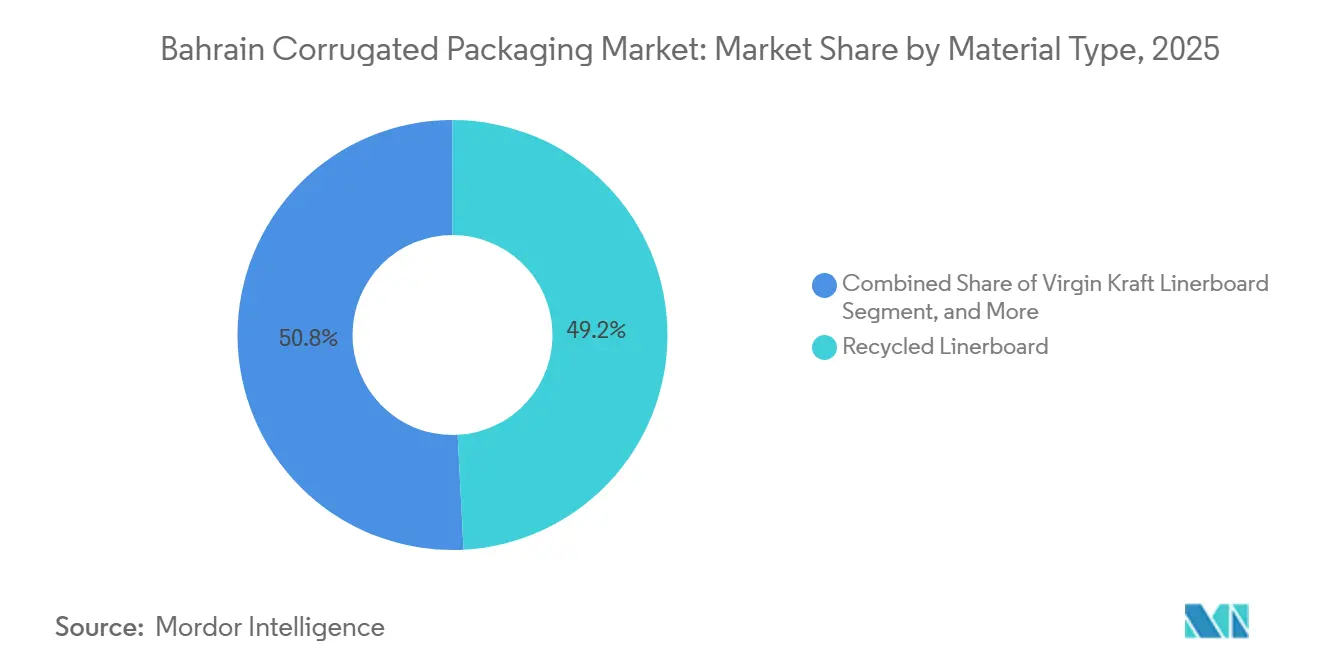

- By material type, the recycled linerboard segment captured 49.18% of the Bahrain corrugated packaging market share in 2025.

- By flute type, the Bahrain corrugated packaging market size for f flute is projected to grow at an 4.71% CAGR through 2031.

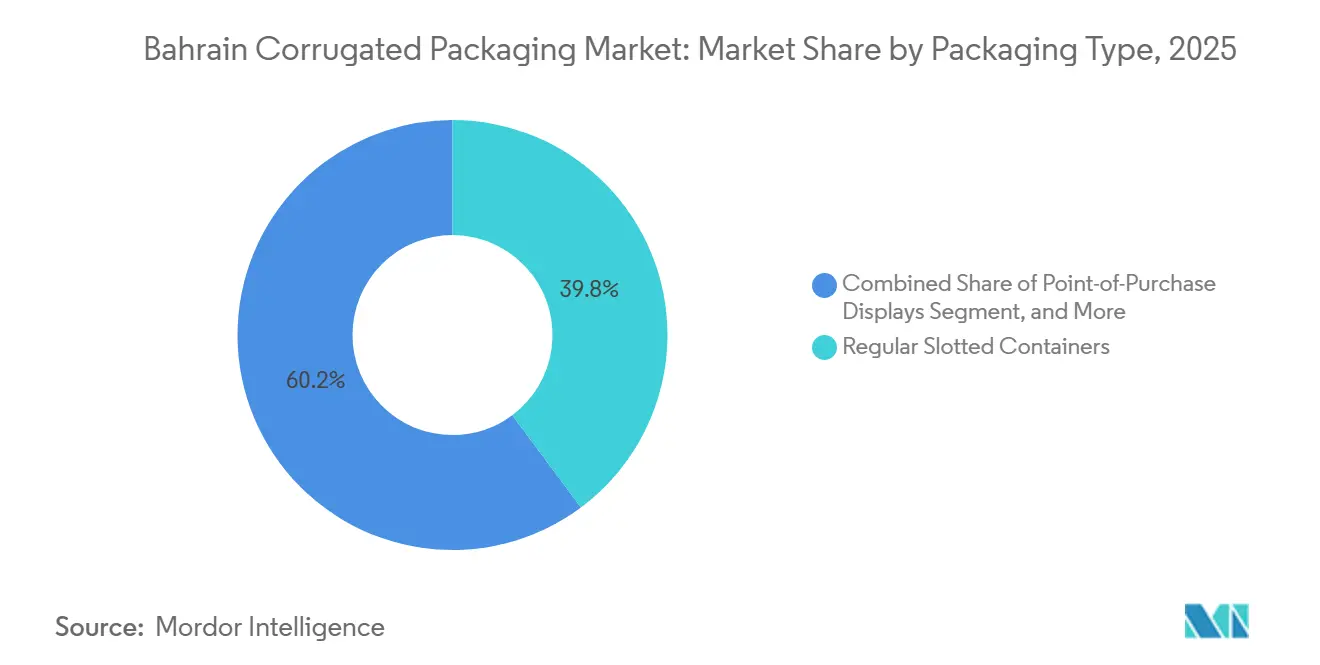

- By packaging type, the regular slotted containers segment captured 39.81% of the Bahrain corrugated packaging market share in 2025.

- By wall type, the Bahrain corrugated packaging market size for triple-wall is projected to grow at an 4.63% CAGR through 2031.

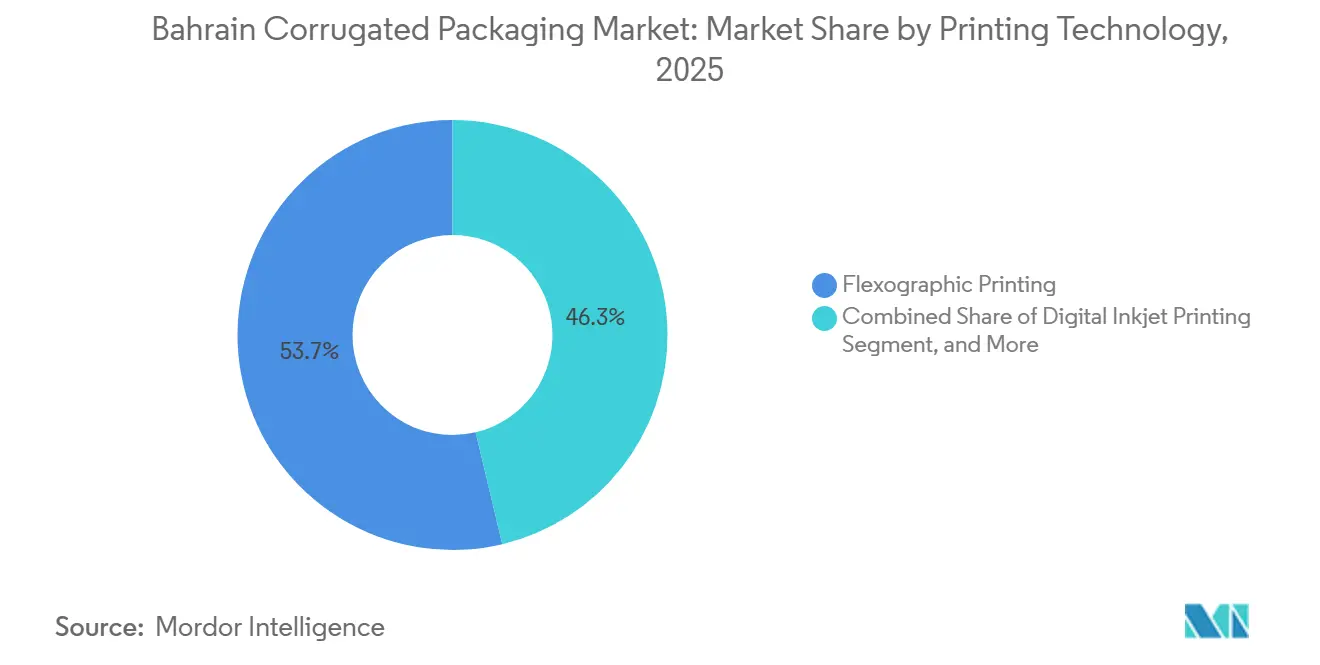

- By printing technology, the flexographic printing segment captured 53.72% of the Bahrain corrugated packaging market share in 2025.

- By end-user industry, the Bahrain corrugated packaging market size for e-commerce fulfillment centers is projected to grow at an 4.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Bahrain Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated E-Commerce Penetration Post-COVID-19 | +1.2% | National, focused on Manama and Sitra hubs | Medium term (2-4 years) |

| Mandatory Country-of-Origin Labeling for Imported Food | +0.8% | National, aligned with GSO rules | Short term (≤ 2 years) |

| Rising Demand for Sustainable, Plastic-Free Packaging | +0.7% | National, spillover to GCC exports | Long term (≥ 4 years) |

| Integration of IoT-Enabled Smart Labels | +0.4% | National, early pharma and electronics use | Long term (≥ 4 years) |

| GCC Trade Corridors Boost Export Needs | +0.5% | Regional, Bahrain as logistics node | Medium term (2-4 years) |

| Government Incentives for Local Conversion | +0.3% | National, via Tamkeen and EDB grants | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated E-Commerce Penetration Post-COVID-19

Bahrain’s online retail volumes have maintained double-digit growth since 2021, and fulfillment operators now manage temperature-controlled warehouses that serve Saudi and Emirati shoppers within forty-eight hours. Those operators request lightweight die-cut cartons that minimize volumetric shipping costs while protecting fragile cosmetics, snacks, and electronics during multiple hand-offs. Digital inkjet equipment capable of profitable runs of fewer than 50 units helps converters tailor Arabic branding, promotion codes, and country-of-origin marks without storing pre-printed inventory. Bahrain’s duty-free access under the U.S. trade agreement further encourages American brands to ship bulk products to Manama, relabel them locally, and forward them across the Gulf via This convergence of cross-border logistics, rapid artwork changeovers, and small-batch economics keeps e-commerce the single strongest volume catalyst through the medium term.

Mandatory Country-of-Origin Labeling for Imported Food

GSO-aligned rules obligate every imported food carton to carry Arabic text, net weight in metric units, and explicit pork or halal declarations. The Ministry of Health’s licensing cap of six labels per factory per month forces importers to coordinate packaging artwork with government approval windows that last up to six weeks. Converters holding in-house prepress and Arabic typography expertise win contracts because they can cycle new graphics quickly without plate charges. QR codes and serialized barcodes that meet pharma-grade traceability standards are increasingly being applied to high-value dairy and infant formula shipments, raising the technological bar for box makers. Compliance pressure, therefore, converts regulatory overhead into commercial advantage for plants that have already invested in digital workflows.

Rising Demand for Sustainable, Plastic-Free Packaging

Global FMCG groups operating Bahraini plants have pledged to cut virgin plastic use, prompting a switch from laminated rigid boxes to micro-flute corrugated formats with up to 50% lower basis weight and 59% lower cradle-to-gate carbon footprint. Hotpack Global leverages FSC and PEFC chain-of-custody, along with an EcoVadis Gold rating, to meet procurement scorecards published by Mondelēz and Arla plants in Bahrain. The government’s Green Factory Seal offers loan discounts and subsidized solar panels to converters that install energy-efficient corrugators or closed-loop water systems, tipping the return-on-investment math in favor of sustainability projects. Retailers label eco-friendly packaging on the shelf, reinforcing consumer pull for boxes that are curbside recyclable and plastic-free. These combined corporate and policy forces keep sustainability a structural rather than cyclical growth lever.

Integration of IoT-Enabled Smart Labels

Tamkeen’s iFactories program covers half the cost of robotics, sensors, and data platforms, enabling early adopters to embed NFC chips or RFID tags into corrugated cartons to monitor temperature, humidity, and tamper events. Pharmaceutical distributors moving insulin and vaccines through Bahrain International Airport demand proof that cold-chain breaks never occurred, and smart labels now provide that audit trail. Electronics exporters add shock and tilt indicators to cartons of semiconductors bound for Singapore, cutting insurance claims and accelerating customs clearance. Converters capable of integrating data carriers during the box-making stage command price premiums that offset chip costs. While penetration remains low, early success stories signal an irreversible march toward data-rich corrugated packaging across high-value verticals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Domestic Recovered Paper Feedstock | -0.9% | National, import dependent | Short term (≤ 2 years) |

| High Volatility in Kraftliner Import Prices | -0.7% | Regional, tied to global markets | Medium term (2-4 years) |

| Limited Availability of Water for Pulping | -0.3% | National, desalination costs | Long term (≥ 4 years) |

| High Capital Intensity for Digital Upgrades | -0.2% | National, especially SMEs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Domestic Recovered Paper Feedstock

Bahrain lacks a nationwide curbside collection scheme, so mills must import old corrugated containers from Europe, North America, and increasingly Southeast Asia. The Strait of Hormuz security flare-up in early 2026 raised marine insurance and delayed feedstock vessels, obliging converters to carry up to eight weeks of buffer inventory.[1]The Pulp and Paper Times, “US-Iran Tensions Strain GCC Recycled Paper Mills,” thepulpandpapertimes.com Elevated working-capital needs squeeze smaller plants that cannot secure long supplier credit lines. Attempts to source locally collide with limited post-consumer collection volumes and competition from tissue mills. Without domestic pulping capacity, the industry remains structurally exposed to distant market shocks that it cannot hedge through futures or swaps.

High Volatility in Kraftliner Import Prices

PIX Testliner GCC quotations swung from USD 454 per tonne in May 2024 to USD 478 one year later as global energy spikes, freight reroutes, and weather-related outages destabilized supply. Converters locked into net-60 payment terms with FMCG customers struggled to quickly pass through surcharges, eroding gross margins during upward price cycles. Some buyers switched partial volumes to recycled fluting, but premium food and beverage accounts still insist on virgin linerboard for moisture resistance, limiting substitution. Saudi diesel price hikes of nearly 8% in January 2026 further inflated inland haulage costs for board-trucked across the King Fahd Causeway. The lack of containerboard hedging tools in GCC markets leaves Bahraini plants managing risk mainly through multi-year supply contracts and diversified sourcing across Saudi, Kuwaiti, and Emirati mills.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Grades Dominate, Lightweight Semi-Chemical Builds Momentum

Recycled linerboard maintained a 49.18% share of the Bahrain corrugated packaging market in 2025, as its lower mill gate price offsets freight surcharges and currency shifts when importers land European kraft. Continuous output from Gulf Paper Manufacturing Company’s Dubai machine and Al Jawdah Paper’s new Qassim mill assures Bahraini converters of shorter lead times and reduced moisture-damage risk during sea transit. Semi-chemical fluting, although currently smaller, is forecast to grow at a 4.47% CAGR through 2031 as box designers shave weight to cut dimensional shipping fees and meet retail chain sustainability scorecards without sacrificing edge-crush strength.[2]Gulf Paper Manufacturing Company, “About,” gulfpaper.com

Lightweighting pressure will intensify as Bahrain’s e-commerce warehouses negotiate volumetric tariffs with regional couriers, making gram savings translate directly into logistics savings that brands can quantify. Retailers are already mandating minimum recycled-content thresholds that only GCC mills with robust quality certifications can consistently meet, pulling procurement away from ad-hoc Asian spot buys. The Bahrain corrugated packaging market size is tied to recycled linerboard, therefore expands in absolute terms even as its percentage share plateaus, because total box volume grows with food imports and online fulfillment parcels.

By Flute Type: B Flute Anchors Transit, Thin Flutes Target Luxury Graphics

B flute captured 46.17% of revenue in 2025 because its 2.5-3.0 millimeter profile balances cushioning and pallet cube efficiency for processed food and beverage shippers that replenish shelves weekly across the GCC. E and F flutes appeal to cosmetics and personal-care brands investing in shelf-ready packaging where crisp offset graphics and tactile varnishes command aisle attention at pharmacy chains. F flute is forecast for the fastest 4.71% CAGR as luxury chocolate and electronics launches choose its sub-one-millimeter thickness to achieve rigid-box aesthetics without the carbon footprint of chipboard.

Converters that install servo-driven die-cutters and high-speed folding-gluers achieve registration precision essential for micro-flute performance, capturing business from premium gift segments previously outsourced to East Asia. Bahrain’s Green Factory Seal encourages investments in new corrugators capable of fine-flute changeovers in under 10 minutes, cutting scrap and energy use per square meter. The Bahrain corrugated packaging market size, attributed to thin flutes, will expand in tandem with duty-free tourist retail, airport confectionery, and e-commerce subscription boxes that privilege the unboxing experience. Brand owners also note sustainability gains, because thinner flutes reduce truckloads per million boxes and lower cradle-to-gate emissions, aligning with Science Based Targets Initiative pledges.

By Packaging Type: Custom Die-Cut Formats Outpace Commodity Cartons

Regular slotted containers accounted for 39.81% of 2025 demand because automated erecting equipment in Bahrain’s food and beverage plants is calibrated for this long-standing standard. However, rising direct-to-consumer shipments and premium gifting trends are prompting brand owners to seek structural differentiation that a plain RSC cannot provide. Die-cut custom boxes therefore register a projected 4.87% CAGR, supported by digital plotting tables that shorten design cycles and reduce sample costs for converters embracing rapid prototyping. Folding cartons remain important for pharmaceuticals and personal care items that require secondary retail packs carrying dosage or ingredient information in both Arabic and English, though their overall tonnage is modest compared with corrugated shipping cases.

Brand marketers view unboxing as a shareable social media moment, and Bahraini converters now integrate interior print, tear strips, and tamper-evident tabs to elevate that experience. Micro-fulfillment centers serving Manama and Dammam request right-sized die-cuts that maximize courier van density and minimize air voids, reinforcing the shift away from generic cartons. Retail chains demand self-locking shelf-ready units that move directly from pallet to aisle, cutting labor costs while boosting speed to shelf during festival periods. Converters able to run small batches without plate changeovers capture those contracts, and their margin uplift offsets the incremental design expense.

By Wall Type: Triple-Wall Boards Capture Export and Industrial Upside

Single-wall boards accounted for 61.32% of shipments in 2025 because they meet everyday transit requirements for domestically consumed processed foods, beverages, and e-commerce parcels that move mainly within the GCC and experience limited stacking stress. Nonetheless, Bahrain’s aluminum downstream and petrochemical exporters increasingly specify double-wall or triple-wall cartons to safeguard heavy or high-value components traveling by sea to Europe or South Asia, where multi-modal handling heightens crush risk. Triple-wall configurations, combining ACA or BCA flutes, are consequently forecast to post a 4.63% CAGR as export-oriented heavy industry expands under the Industrial Sector Strategy.

Investments in wider corrugators allow converters to laminate three webs in one pass, lowering per-square-meter cost and making triple-wall accessible to mid-volume customers. Automated compression testers on the shop floor now validate that each heavy-duty batch meets specified edge-crush and box compression values before dispatch, reducing claims and reinforcing buyer confidence. Freight savings accrue because exporters can sometimes replace wooden crates with lighter, triple-wall cartons that still meet insurance criteria, thereby boosting demand even when commodity volumes plateau.

By Printing Technology: Digital Inkjet Narrows the Flexographic Cost Gap

Flexographic presses captured 53.72% of the market share in 2025 due to their high throughput on medium- and long-run jobs typical of beverage trays, detergent cases, and fast-moving consumer goods with stable graphics. However, SKU proliferation in snacks, cosmetics, and online subscription boxes means average order length continues to shrink, exposing the cost of flexographic plates and changeover downtime. Digital inkjet machines capable of 600-dpi six-color output at seventy-plus meters per minute enable profitable runs as low as twenty-five boxes, a threshold impossible for legacy flexo lines without heavy mark-up.

Adoption of end-to-end digital workflows, including cloud-based artwork portals and automatic nesting software, compresses lead time from artwork sign-off to ship-ready cartons to less than forty-eight hours in many cases. This agility attracts fast-fashion e-retailers and seasonal confectionery launches that cannot forecast exact volumes months in advance. Digital presses also print serialized barcodes, expiry dates, and localized regulatory panels in a single pass, reducing downstream label application costs and alignment errors. As machine acquisition costs fall and ink chemistries improve, the cost crossover point will shift further in favor of digital for ever-larger batch sizes, accelerating displacement of mid-range flexographic orders.

By End-User Industry: Online Fulfillment Sets the Fastest Growth Pace

Processed foods accounted for 31.19% of total sales in 2025, as Bahrain hosts regional plants for biscuit, chocolate, and dairy brands that ship finished goods across six GCC markets on a weekly schedule. These facilities value reliable single-wall transit cases with tear-tape openings and display panels suited for hypermarket aisles, ensuring a steady baseline demand even when other sectors fluctuate seasonally. E-commerce fulfillment centers are poised for a 4.55% CAGR, as third-party logistics companies continue to add chilled and ambient storage nodes that require short-run branded boxes, thermal liners, and returns-ready resealable strips.

Electronics distributors increasingly ask for E or F flute cartons fitted with anti-static coatings and embedded shock sensors to protect smartphones and circuit boards during multi-modal transfers. Pharmaceutical importers require serialized outer shipper cartons that align with GCC track-and-trace mandates, pushing converters toward on-press data printing and camera-based verification. Cosmetics and personal-care brands invest in high-definition micro-flute packs that double as shelf-display units, reinforcing brand storytelling while reducing plastic use. Industrial sectors, notably aluminum extrusions and petrochemical equipment, adopt triple-wall boxes lined with VCI paper to prevent corrosion during ocean voyages, thereby boosting the share of heavy-duty tonnage.

Geography Analysis

Bahrain’s location astride the King Fahd Causeway makes it a natural consolidation hub for shipments feeding Saudi Arabia’s Eastern Province, which accounts for a large share of GCC retail spending. Duty-free movement within the Gulf Customs Union means boxes produced in Manama can cross into Dammam overnight without additional tariffs, giving Bahraini converters a cost and speed advantage over Asian imports, which face 20-day transit times. Khalifa Bin Salman Port handles most inbound containerboard, and its recent berth expansion enables gearless vessels to discharge reels directly onto covered yards, minimizing moisture exposure before slitting.

Regional supply dynamics are shifting as Saudi Arabia and the UAE commission a combined 250,000 tonnes of new recycled containerboard capacity between 2025 and 2027, thereby reducing dependency on European and Indian imports and lowering landed-cost volatility. Bahraini converters will benefit from shorter lead times and lower safety-stock requirements, but they will also face fiercer price competition as surplus tonnage seeks outlets beyond domestic Saudi consumption. Political flashpoints in the Red Sea and the Strait of Hormuz periodically disrupt shipping lanes, forcing mills to reroute via the Cape of Good Hope and inflating freight surcharges, although container index declines in early 2026 offered temporary relief from pandemic-era highs.

Trade agreements amplify Bahrain’s geographic leverage, because tariff-free access to the United States under the FTA encourages exporters to ship U.S. origin goods in Bahraini-printed cartons labeled Made in USA, thereby unlocking duty rebates across GCC markets.[3]Oxford Business Group, “Smart Industry Initiatives in Bahrain,” oxfordbusinessgroup.com Free trade with Singapore and EFTA nations widens sourcing flexibility for specialty chemicals and starches used in corrugating adhesives, helping plants hedge single-country supply risks. Government customs-duty exemptions announced in 2025 for raw materials not produced locally reduce the cash tied up in inbound kraftliner and digital-inkjet inks, supporting converters’ working-capital cycles.

Competitive Landscape

United Paper Industries, trading as Bahrain Pack, retains more than 70% domestic market share following a Tamkeen-backed expansion that increased capacity by 7,000 tonnes and funded a high-speed folder-gluer capable of complex die-cutting. Hotpack Global, operating twenty facilities across the Middle East, challenges this dominance by bundling corrugated with food-service disposables under FSC and PEFC chain-of-custody, appealing to retailers seeking one-stop sustainable solutions.[4]Hotpack Global, “About Us,” hotpackglobal.com INDEVCO Paper Containers differentiates by licensing Arcwise curved cartons, enabling perfume and gift brands to gain shelf impact without plastic windows, and by marketing multi-award-winning designs that command premium margins. Napco National’s 2025 purchase of Arabian Flexible Packaging signals intent to cross-sell flexibles and corrugated, raising the bar on total packaging programs offered to Gulf FMCG groups.

Technology adoption shapes competitive boundaries because converters installing Domino X630i or AstroNova AJ-1300 presses can turn artwork revisions within twenty-four hours, winning time-sensitive e-commerce campaigns that traditional flexo houses must decline. Plants participating in Bahrain’s iFactories initiative receive subsidized robotics and IoT upgrades, enabling them to run predictive maintenance routines that raise uptime and reduce scrap, which directly feeds into pricing flexibility during tender rounds. Season International leverages local manufacture of edge-protectors, air-bubble sheets, and EPS inserts to bundle protective materials with cartons, reducing buyers’ vendor count and securing loyalty through convenience.

Price pressure will intensify as Saudi and Emirati mills flood the region with new board, causing converters to pivot from volume to value architectures that emphasize structural design, smart labels, or consumer-engaging graphics. Government procurement policies give local manufacturers a ten percent preference under the Takamul value-added scheme, encouraging foreign brands to co-pack inside Bahrain or partner with domestic plants to secure state contracts. Strategic control of recovered-paper supply chains becomes another battleground, with some players exploring joint ventures in waste-management to lock in feedstock and capture ESG credits.

Bahrain Corrugated Packaging Industry Leaders

Season International Trading & Industries Co.

United Paper Industries Co. W.L.L.

Hotpack Packaging Industries LLC

Big Boxers Co. W.L.L.

Napco National

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: US-Iran tensions lifted Gulf shipping insurance premiums and delayed recovered-paper deliveries, inflating mill costs and threatening board price hikes for Bahraini converters.

- March 2026: Maersk and CMA CGM suspended Suez routes and rerouted via the Cape of Good Hope, adding transit days for containerboard bound for GCC markets, although spot freight rates briefly softened.

- August 2025: Napco National acquired Arabian Flexible Packaging, doubling its UAE gravure capacity and signaling a move to bundle flexible and corrugated solutions across the Gulf.

- March 2025: MEPCO broke ground on its PM5 line, which will double Saudi containerboard capacity by 2027, reshaping GCC supply balances.

Bahrain Corrugated Packaging Market Report Scope

The Bahrain corrugated packaging market is defined as the industrial sector focused on the design, manufacturing, and distribution of fiber-based containers, comprising a fluted medium bonded between flat linerboards. This industry is a critical enabler of the Kingdom’s logistics and retail sectors, providing diverse board constructions such as single-wall, double-wall, and triple-wall formats. The scope of this report provides a comprehensive evaluation of the Bahraini market from 2026 to 2031, featuring detailed value forecasts and trends across key commercial hubs, including Manama, Sitra, and Salman Industrial City.

The Bahrain Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material Type | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current value of the Bahrain corrugated packaging market and how fast is it growing?

The market stands at USD 0.15 billion in 2026 and is projected to reach USD 0.18 billion by 2031 at a 3.71% CAGR.

Which material type dominates corrugated board demand in Bahrain?

Recycled linerboard leads with 49.18% share because regional mills supply it more economically than virgin kraft.

Why is digital printing gaining traction among Bahraini box makers?

Digital inkjet presses eliminate plate costs, enable profitable runs under fifty boxes, and simplify compliance updates on Arabic labeling.

How will new Saudi and UAE containerboard capacity influence Bahraini converters?

Roughly 250,000 tonnes of extra GCC supply by 2027 should shorten lead times and temper price spikes, yet it will also intensify regional price competition.

What sustainability certifications help packaging suppliers win contracts in Bahrain?

FSC, PEFC, ISO 14001, and EcoVadis Gold scores are increasingly required by multinational FMCG and pharmaceutical buyers operating in the kingdom.

Which end-user segment is expected to grow fastest through 2031?

E-commerce fulfillment centers are forecast for a 4.55% CAGR, driven by expanding temperature-controlled warehouses and same-day delivery models.

Page last updated on: