Bacteriostatic Water For Injection Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

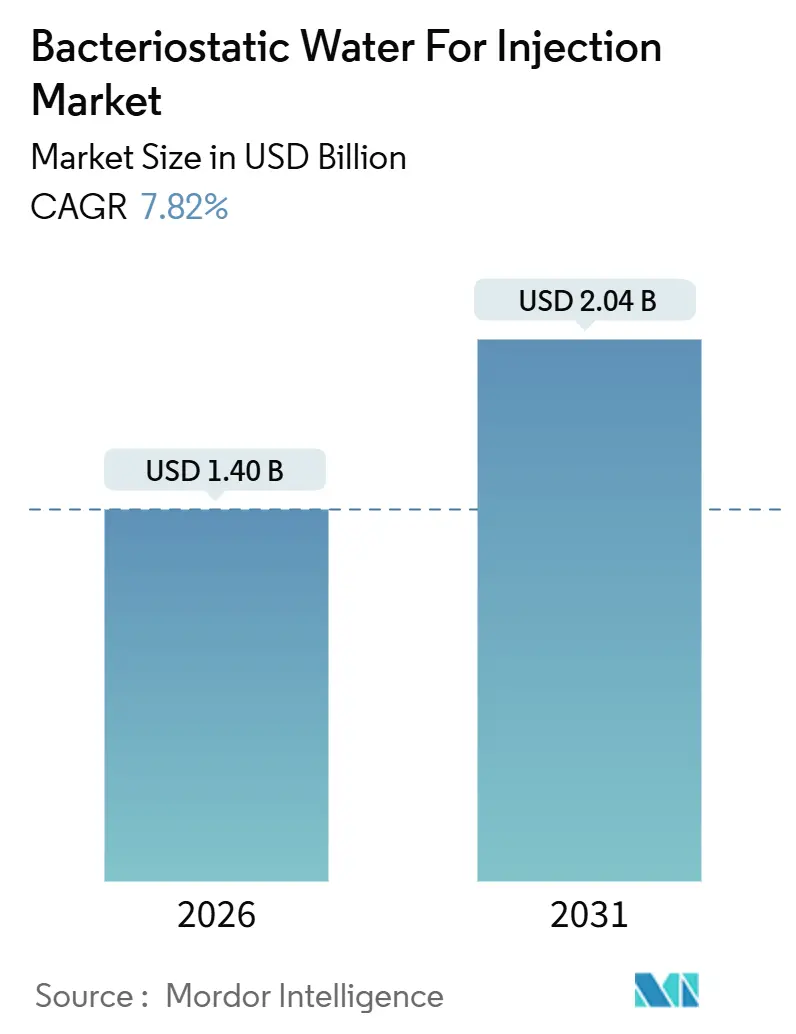

| Market Size (2026) | USD 1.40 Billion |

| Market Size (2031) | USD 2.04 Billion |

| Growth Rate (2026 - 2031) | 7.82% CAGR |

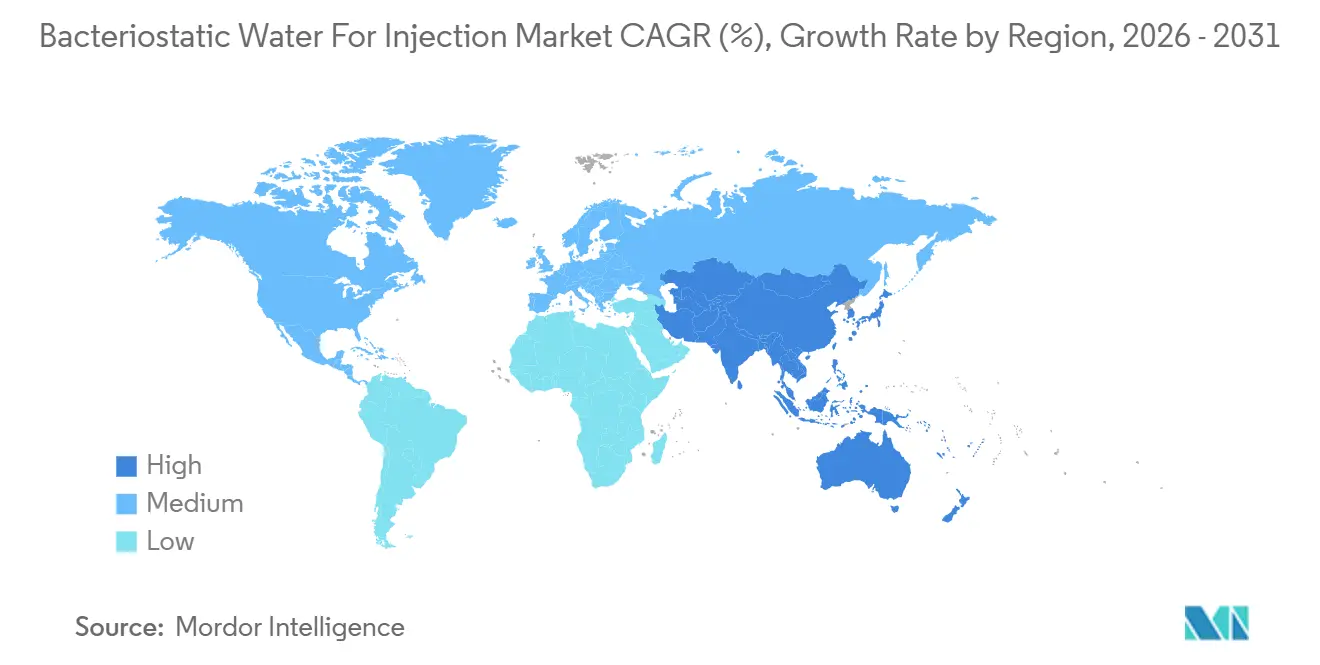

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bacteriostatic Water For Injection Market Analysis by Mordor Intelligence

The Bacteriostatic Water For Injection Market size is estimated at USD 1.40 billion in 2026, and is expected to reach USD 2.04 billion by 2031, at a CAGR of 7.82% during the forecast period (2026-2031).

The industry's shift from oral drugs to sterile, lyophilized biologics and vaccines has heightened the demand for reliable reconstitution media. Benzyl alcohol-preserved formats play a pivotal role in connecting pharmaceutical manufacturers, contract fill-finish facilities, and healthcare providers, with care settings now extending from hospital wards to home-based infusion treatments. Capital investments are being directed toward isolator-equipped production lines, low-extractable polymer containers, and advanced track-and-trace labeling systems to meet stringent quality standards. However, market dynamics pose challenges, including cost-containment pressures from group purchasing organizations, raw material shortages—particularly of Type I borosilicate glass—and regulatory warnings about benzyl alcohol use in pediatric care. These factors collectively constrain margin growth, with vertically integrated producers better positioned to navigate these headwinds.

Key Report Takeaways

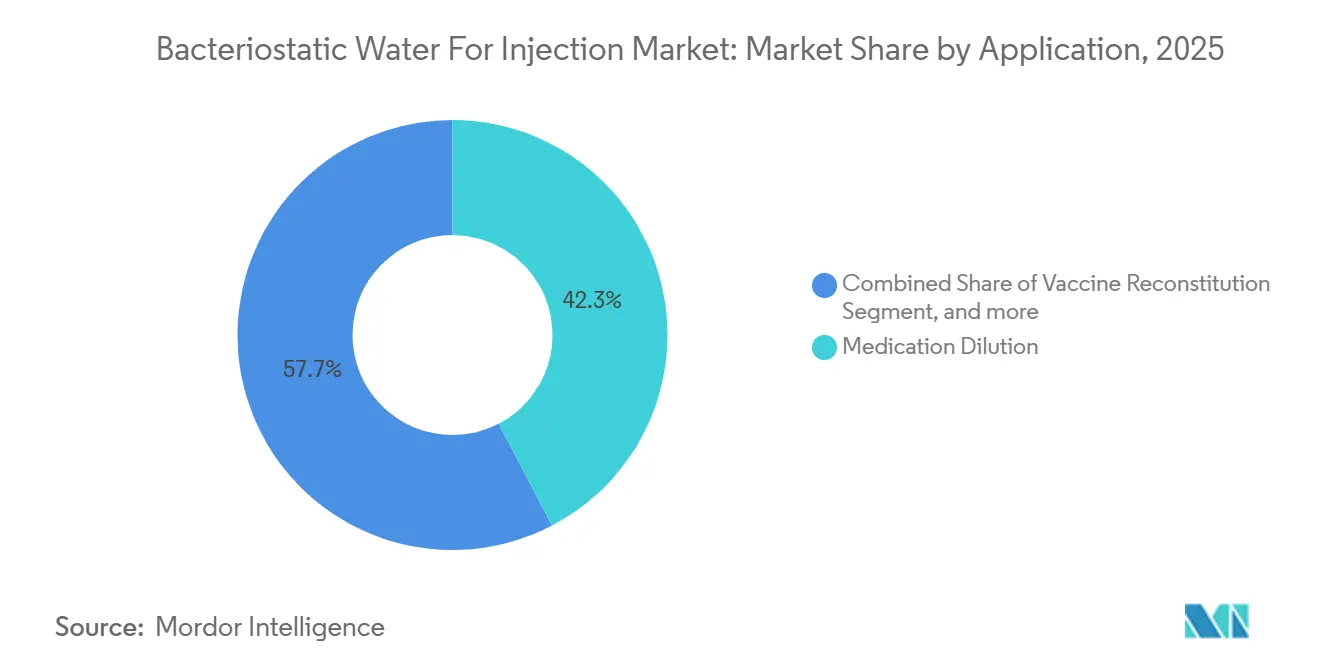

- By application, medication dilution led with 42.34 % revenue share in 2025, while vaccine reconstitution is advancing at a 9.54 % CAGR to 2031.

- By container type, multi-dose vials held 53.45 % of 2025 revenue; prefilled syringes record the fastest 9.88 % CAGR through 2031.

- By packaging material, plastics commanded 49.76 % of 2025 revenue, yet glass is expanding at a 9.76 % CAGR to 2031.

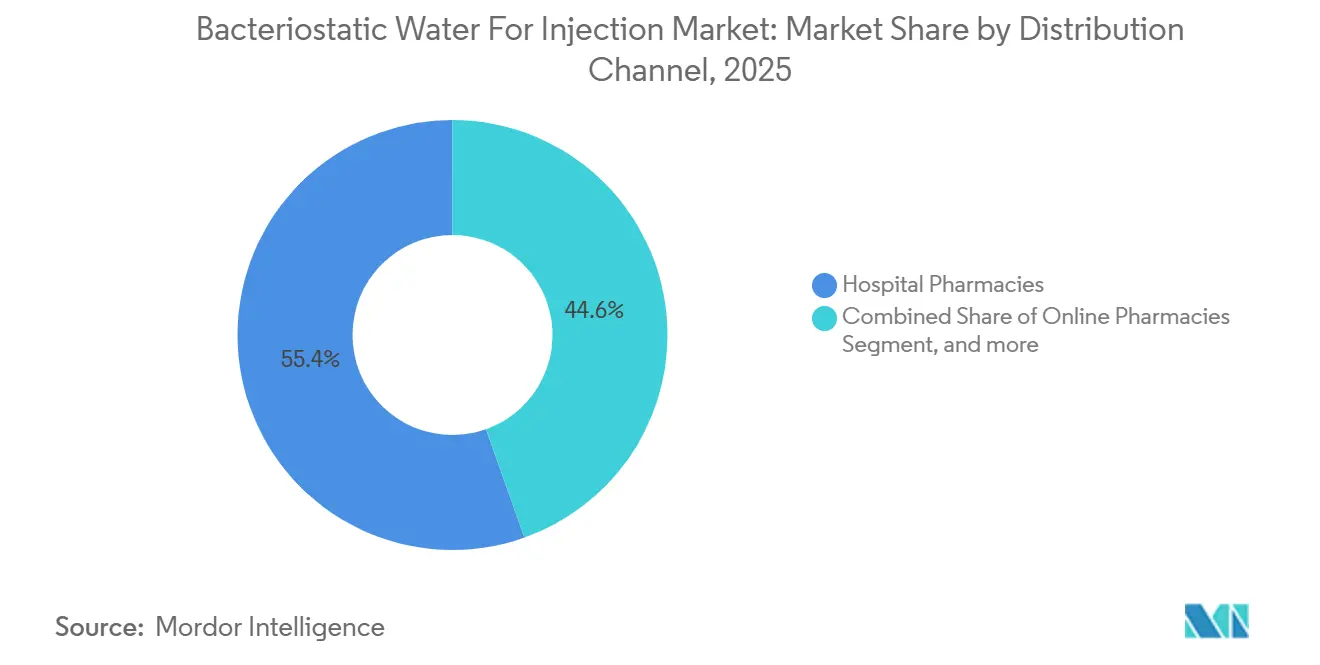

- By distribution channel, hospital pharmacies controlled 55.43 % of 2025 volume; online pharmacies are growing at a 10.34 % pace to 2031.

- By end user, hospitals accounted for a 58.65 % share in 2025, whereas home healthcare is rising at a 10.21 % CAGR through 2031.

- By geography, North America captured 43.67 % of 2025 revenue; Asia-Pacific posts the highest 8.43 % CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bacteriostatic Water For Injection Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Demand For Injectable Therapeutics | +1.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Expansion Of Parenteral Manufacturing Capacities Worldwide | +1.5% | APAC core, spill-over to North America & Europe | Long term (≥ 4 years) |

| Stringent Regulatory Standards For Sterility And Quality Assurance | +1.2% | North America & EU, cascading to APAC | Short term (≤ 2 years) |

| Growth Of Home-And Ambulatory-Based Drug Administration | +1.4% | North America & Europe, emerging in APAC | Medium term (2-4 years) |

| Increasing Adoption Of Multi-Dose Packaging And Reconstitution Systems | +0.9% | Global | Medium term (2-4 years) |

| Integration Of Advanced Purification And Monitoring Technologies | +0.7% | North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Demand for Injectable Therapeutics

Biologics and lyophilized vaccines dominate late-stage pipelines, and each dose needs a sterile diluent. The World Health Organization cleared 15 new lyophilized vaccines in 2024, a record that directly lifts demand for bacteriostatic water for injection market products. Gavi pledged USD 8.8 billion for routine immunization in 2026-2030, channeling large volumes of multi-dose diluent into low-income nations[1]Gavi Secretariat, “2026–2030 Investment Opportunity,” gavi.org. Beyond public health, prescribing of GLP-1 receptor agonists such as semaglutide has surged; Novo Nordisk responded with a USD 6.1 billion Danish capacity build that includes dedicated diluent lines. New conjugate vaccines, illustrated by Merck’s 21-valent V116 approval in June 2024, reinforce the upward trajectory for benzyl alcohol-preserved vials in outpatient clinics. Collectively, these dynamics turn the bacteriostatic water for injection market into a growth lever tied to every expansion in parenteral therapy.

Expansion of Parenteral Manufacturing Capacities Worldwide

A wave of site expansions is rewriting supply geography. Pharmascience reserved USD 88 million for aseptic lines in Montreal in 2024. Lonza earmarked USD 560 million for its Swiss Visp campus the same year. In the Asia-Pacific region, Samsung Biologics allocated more than USD 2 billion for additional bioreactor and co-packaging capacity, confirming the region’s role as a biosimilar hub. PCI Pharma Services invested over USD 365 million across two continents to add isolator platforms that handle benzyl alcohol and preservative-free formats within one cleanroom train. These outlays demonstrate that market stakeholders expect the bacteriostatic water for injection market to scale in parallel with biologics output, rather than merely as an auxiliary service.

Stringent Regulatory Standards for Sterility and Quality Assurance

Quality rules tightened quickly. The FDA’s Q3E guidance, finalized in 2024, requires extractables and leachables studies for every container that contacts injectables. The European Medicines Agency now allows reverse-osmosis-based water production but mandates endotoxin limits of ≤ 0.25 EU/mL, driving adoption of real-time monitoring. USP Chapter 1207 updated deterministic leak testing protocols, adding helium mass spectrometry as the benchmark for vial integrity. ISO 13485 certification has become the standard for prefilled diluent syringes entering home settings. These layered requirements create high entry barriers and confer pricing power on incumbents in the bacteriostatic water for injection market.

Growth of Home and Ambulatory-Based Drug Administration

The global home-healthcare sector exceeded USD 110 billion in 2025 and continues to expand as payers shift reimbursement from acute to ambulatory care. Prefilled diluent syringes reduce the risk of manipulation; BD doubled Nebraska capacity with a USD 300 million outlay in 2024. Gerresheimer followed up with a EUR 500 million expansion in the Czech Republic for ready-to-use glass syringes. West Pharmaceutical Services invested USD 1.2 billion to scale its Crystal Zenith polymer platform, which is prized for its low extractables in high-concentration biologics. Ambulatory surgery centers, performing 28 million U.S. procedures in 2024, stock multi-dose vials because the 28-day sterility window curbs waste. These data points affirm the link between care-setting migration and the opportunity pipeline for the bacteriostatic water for injection market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital And Operating Costs Of Aseptic Production | -0.8% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Regulatory Restrictions On Benzyl Alcohol Use In Vulnerable Populations | -0.6% | North America & Europe, cascading to APAC | Short term (≤ 2 years) |

| Availability Of Alternative Preservative-Free Diluent Formats | -0.5% | North America & Europe | Medium term (2-4 years) |

| Supply-Chain Vulnerabilities For Critical Raw Materials And Components | -0.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Operating Costs of Aseptic Production

Building a single aseptic line costs USD 50–100 million and yearly operating expenses exceed USD 10 million. Energy prices climbed 15% after 2024 carbon-pricing rules in the EU and California, pushing utilities to the second-largest cost line for fill-finish firms[2]European Commission, “EU Emissions Trading System Revision 2024,” ec.europa.eu. Emerging-market producers lack access to validation engineers and face longer lead times for isolator imports that can add USD 5 million per line. Contract manufacturers must choose between stainless-steel assets that offer scale yet require week-long cleaning cycles, or single-use systems that raise disposables cost but hasten changeover. These economic hurdles temper capacity additions and slow competitive entry into the bacteriostatic water-injection market.

Regulatory Restrictions on Benzyl Alcohol Use in Vulnerable Populations

The FDA strengthened benzyl-alcohol warnings in 2024, prohibiting use in neonates and mandating boxed cautions for pregnant women. The EMA now requires exposure risk assessments for hepatically or renally impaired adults. Hospitals must stock parallel preservative-free sterile water in single-dose vials for pediatric floors, elevating inventory complexity and carrying costs by 10-15%. Compounding pharmacies under 503B rules cannot repackage multidose bacteriostatic water for injection, shrinking the addressable volume of a USD 12 billion segment. These limitations cap overall uptake for benzyl alcohol formats and divert some growth toward preservative-free alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application, Vaccine Reconstitution Drives Fastest Expansion

Application revenue totaled USD x in 2025, and vaccine reconstitution posted the steepest 9.54% CAGR, exceeding the bacteriostatic water for injection market benchmark. The bacteriostatic water for injection market, led by medication dilution with a 42.34% share in 2025, is expanding more slowly than the vaccine and biologic segments. Second-order effects include pediatric catch-up programs in low-income countries and routine adult boosters in high-income regions, both of which drive recurring vial pull-through. The bacteriostatic water for injection market share for laboratory use is minor yet rising as cell-culture outsourcing adopts longer shelf-life diluents. Pipeline attrition in oral GLP-1 candidates, notably Pfizer’s phase-2 setback, is redirecting capital toward injectable formats that require reliable diluent co-packaging. Vaccine developer Merck validated this path when its V116 approval mandated a 0.7 mL benzyl alcohol diluent per outpatient dose, a small volume that scales rapidly across national immunization plans.

Downstream, antibiotic reconstitution remains entrenched in inpatient protocols, especially for cephalosporins and carbapenems that must be administered immediately after preparation. Veterinary, diagnostic, and biotech applications cumulatively contribute mid-single digits while reinforcing the universality of bacteriostatic water in sterile workflows. Suppliers that can flex between commodity antibiotic volumes and high-purity biologic lots stand to optimize asset utilization and profit pools throughout the forecast horizon.

By Container Type, Prefilled Syringes Gain Share Despite Multi-Dose Dominance

Container-type revenues underline a cost-versus-safety trade-off. Multi-dose vials delivered over half of 2025 sales, but growth is lagging because home-care biologics lean toward ready-to-use devices. The bacteriostatic water for injection market for prefilled syringes is pegged to a 9.88% CAGR, driven by investments from BD, Gerresheimer, and West that collectively exceed USD 2 billion. Hospitals still champion multi-dose economics but must train staff to properly disinfect vial septa to avoid contamination. The bacteriostatic water for injection market share for single-dose vials is rising in neonatal units that cannot tolerate benzyl alcohol, and DSCSA serialization deadlines make bar-coded, unit-level tracking mandatory by 2027. Hybrid IV bags remain niche but grow in oncology as continuous infusions become commonplace for targeted therapies.

Capex allocation reflects the directional bet: polymer syringe lines offer faster changeovers and lower breakage, while glass vial lines retain unbeatable inertness for chemical stability. CDMOs that offer flexible filling suites capable of switching between vials, syringes, and cartridges will capture program-level contracts from innovators who demand redundancy across container formats.

By Packaging Material, Glass Rebounds Amid Extractables Scrutiny

Plastic dominated 2025 revenue through weight and breakage savings, yet regulatory headwinds on leachables are driving a glass renaissance. The bacteriostatic water for injection market size for glass packaging is on a 9.76% rate to 2031, surpassing plastics growth. FDA Q3E rules intensify scrutiny of cyclic-olefin polymers, giving Type I borosilicate an inertness halo. SCHOTT Pharma and Corning Valor Glass offer reinforced chemistries that solve historical fracture issues, positioning glass as the default for high-value biologics. Plastic retains utility through West’s Crystal Zenith, which tolerates gamma sterilization and handles ultra-high concentration mAbs that precipitate in alkali glass. Hybrid or coated vials are experimental but may achieve rapid adoption if they combine glass inertness with polymer toughness.

Substitution economics will hinge on the total cost of failure: a single biologic dose can exceed USD 10,000 street price, meaning one cracked glass ampule outweighs higher unit costs in polymer alternatives. For lower-cost antibiotics, polymer keeps its edge. Suppliers with dual material portfolios hedge against regulatory and pricing swings in the bacteriostatic water for injection market.

By Distribution Channel, Online Pharmacies Disrupt Traditional Hospital Procurement

Group purchasing organizations preserved hospital pharmacy dominance in 2025, but e-commerce flips the last-mile script for chronic patients. The bacteriostatic water for injection market size flowing through online pharmacies is positioned for double-digit expansion as Amazon Pharmacy and CVS digital portals integrate same-day logistics. Careful temperature control and anti-counterfeit serialization underpin patient trust. Retail chains meet walk-in demand but lack the direct insurance integration that drives mail-order repeat fills. Direct wholesaling into 503B outsourcing facilities remains strategic because compounding volumes require pallet deliveries rather than parcel shipments. Contract terms increasingly include supply-continuity clauses that penalize stockouts, rewarding manufacturers with geographically diversified fill-finish footprints.

In parallel, telehealth platforms prescribe self-administered biologics and send diluent starter kits alongside drug pens. As more payers reimburse home infusion, online channels will continue to erode hospital-centered share volumes. Manufacturers must align pack sizes, labeling, and ancillary supply kits to consumer-grade usability standards.

By End User, Home Healthcare Outpaces Hospitals in Growth Trajectory

Hospitals remain the largest absolute consumer, consuming multi-dose vials every shift. Yet the bacteriostatic water for injection market size tied to home healthcare posts the swiftest 10.21% CAGR as payers push costs out of inpatient settings. Prefilled syringes minimize mixing errors and fit mail-order packaging constraints. Ambulatory surgery centers keep multi-dose stock due to the 28-day window, but clinics' ordering patterns skew towards smaller cartons. Research labs and CROs enlarge their demand incrementally; they value 28-day sterility because reagent prep spans multi-week experiments. Compounding pharmacies’ reliance on preservative-free alternatives limits their benzyl alcohol uptake, yet they still consume substantial volumes of sterile water.

Equipment innovations further nudge volumes to the home. Autoinjector kits now ship with diluent cartridges that snap into pen devices. As patient self-training apps embed barcode checks, dosing errors decline, and adherence improves, home healthcare solidifies as the fastest-rising pillar within the bacteriostatic water for injection market.

Geography Analysis

North America accounted for 43.67 of revenue in 2025, driven by large biopharma pipelines, robust CDMO ecosystems, and dollar-denominated procurement budgets. FDA Q3E extractables guidance forced container upgrades, benefiting domestic vendors with Type I borosilicate mastery. Canada’s Pharmascience plant expansion underscores the region’s status as a sterile injectables nearshoring hub. Mexico’s maquiladora clusters attract fill-finish investments seeking tariff-free access into U.S. distribution networks.

Europe ranks second in share, aided by EMA water-for-injection monograph changes that legitimize lower-energy purification routes. German engineering depth supplies a skilled technician pipeline that stabilizes cost. Post-Brexit dual-release testing complicates U.K. compliance, nudging some throughput to continental facilities. Lonza’s Visp expansion and SCHOTT Pharma’s IPO signal continued capital confidence in European capacity.

Asia-Pacific registers the fastest CAGR of 8.43%, led by Indian and Chinese biosimilar plants seeking to export under ICH Q7 compliance. Samsung Biologics’ multi-billion-dollar projects make South Korea the anchor CDMO hub for U.S. and EU sponsors[3]Samsung Biologics Co. Ltd., “Incheon Facility Overview,” samsungbiologics.com. Biocon Biologics and WuXi Biologics add regional redundancy, while Japan and Australia optimize clinical-trial supply chains. Africa and South America remain volume-light due to supply-chain fragilities, but gain momentum as local immunization programs localize fill-finish to improve resilience.

Competitive Landscape

Market concentration sits in a moderate band; the top five players control roughly half of global turnover. Pfizer Hospira, Baxter International, Fresenius Kabi, B. Braun, and Lonza use vertically integrated production and locked-in contracts with innovators to defend share. The bacteriostatic water for injection market welcomes new entrants, yet regulatory validations and capital costs block rapid scaling. Device makers like BD and Gerresheimer are absorbing packaging upstream, chasing the white-space in prefilled syringes for home use. Polymer specialists, notably West’s Crystal Zenith, leverage the advantages of their extractables profiles to win high-value biologic programs. Technology suppliers such as Cytiva, FUJIFILM Diosynth, and Syntegon feed an automation arms race that raises baseline quality expectations.

Supply risk around borosilicate glass and pharmaceutical-grade benzyl alcohol motivates dual sourcing. Multinationals, therefore, value CDMOs that co-locate diluent and drug filling on the same campus to curb freight and contamination risk. As DSCSA serialization goes global, companies that offer integrated RFID and 2D barcoding in every carton strengthen anti-counterfeit arguments that resonate in tender bids.

Bacteriostatic Water For Injection Industry Leaders

Pfizer Inc.

B. Braun SE

Fresenius SE & Co. KGaA

Baxter International Inc.

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Fagron Sterile Services US (FSS) was selected by Angels for Change for the "Project PROTECT" grant to proactively manufacture and supply Sterile Water for Injection, a product that has frequently been on the FDA’s drug shortage list due to disruptions from natural disasters.

- April 2024: Asahi Kasei began selling a new membrane system to produce WFI (water for injection), a sterile water used for injection preparation, as a more cost-effective and energy-efficient alternative to conventional distillation, specifically targeting pharmaceutical and biotech applications.

Global Bacteriostatic Water For Injection Market Report Scope

| Medication Dilution |

| Biologic & Peptide Reconstitution |

| Vaccine Reconstitution |

| Antibiotic Reconstitution |

| Laboratory & Diagnostic Usage |

| Other Applications |

| Multi-Dose Vials |

| Single-Dose Vials |

| Prefilled Diluent Syringes |

| IV Bags |

| Glass |

| Plastic (COP, Polyolefin) |

| Others |

| Hospital Pharmacies |

| Retail & Community Pharmacies |

| Online Pharmacies |

| Direct / Wholesale |

| Hospitals |

| Clinics |

| Ambulatory Surgical Centres |

| Home Healthcare |

| Research Laboratories |

| Compounding Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Application | Medication Dilution | |

| Biologic & Peptide Reconstitution | ||

| Vaccine Reconstitution | ||

| Antibiotic Reconstitution | ||

| Laboratory & Diagnostic Usage | ||

| Other Applications | ||

| By Container Type | Multi-Dose Vials | |

| Single-Dose Vials | ||

| Prefilled Diluent Syringes | ||

| IV Bags | ||

| By Packaging Material | Glass | |

| Plastic (COP, Polyolefin) | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail & Community Pharmacies | ||

| Online Pharmacies | ||

| Direct / Wholesale | ||

| By End User | Hospitals | |

| Clinics | ||

| Ambulatory Surgical Centres | ||

| Home Healthcare | ||

| Research Laboratories | ||

| Compounding Pharmacies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

What CAGR is projected for the bacteriostatic water for injection market between 2026 and 2031?

The market is forecast to grow at 7.82% per year during the 2026Ð2031 period.

Which application area is expanding fastest within bacteriostatic water usage?

Vaccine reconstitution leads the pack, registering a 9.54% CAGR through 2031.

Why are prefilled diluent syringes seeing growing demand?

They minimize medication-error risk, support home-based biologic administration, and benefit from sizeable capacity additions by BD and Gerresheimer scheduled through 2027.

How do new regulatory standards influence packaging-material preferences?

FDA Q3E and EMA extractables guidance push high-value biologics toward Type I borosilicate glass, spurring a 9.76% CAGR for glass containers.

Which geographic region shows the strongest growth outlook?

Asia-Pacific posts the highest 8.43% CAGR, powered by Indian, Chinese, and South Korean biosimilar manufacturing expansions.

What primary factor limits benzyl alcoholÐpreserved formats?

FDA and EMA warnings against neonatal and vulnerable-patient exposure restrict benzyl alcohol penetration to roughly 60% of total sterile-water demand.

Page last updated on: