Ayurveda Stomach Care Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

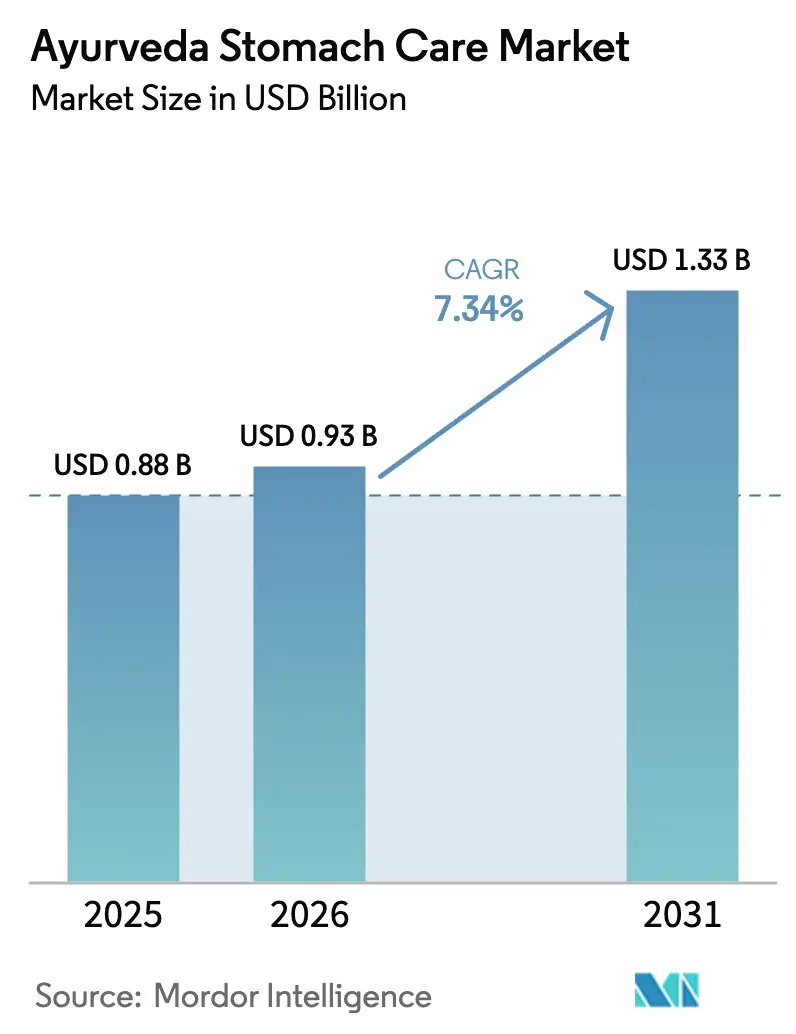

| Market Size (2026) | USD 0.93 Billion |

| Market Size (2031) | USD 1.33 Billion |

| Growth Rate (2026 - 2031) | 7.34% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ayurveda Stomach Care Market Analysis by Mordor Intelligence

The Ayurveda Stomach Care Market size is projected to be USD 0.88 billion in 2025, USD 0.93 billion in 2026, and reach USD 1.33 billion by 2031, growing at a CAGR of 7.34% from 2026 to 2031.

Rising gastrointestinal disease prevalence, government funding for traditional medicine, and consumer migration to herbal solutions drive momentum, while digital commerce compresses distribution costs and widens geographic reach. Policy endorsements from the World Health Organization strengthen global confidence, and bioavailability technologies let brands back efficacy with pharmacokinetic data. Mature incumbents are defending share through vertical integration that shields margins from raw-material volatility, even as climate shifts tighten herb supply. Meanwhile, convenience-led formats speak to younger urban buyers who want fast, portable relief.

Key Report Takeaways

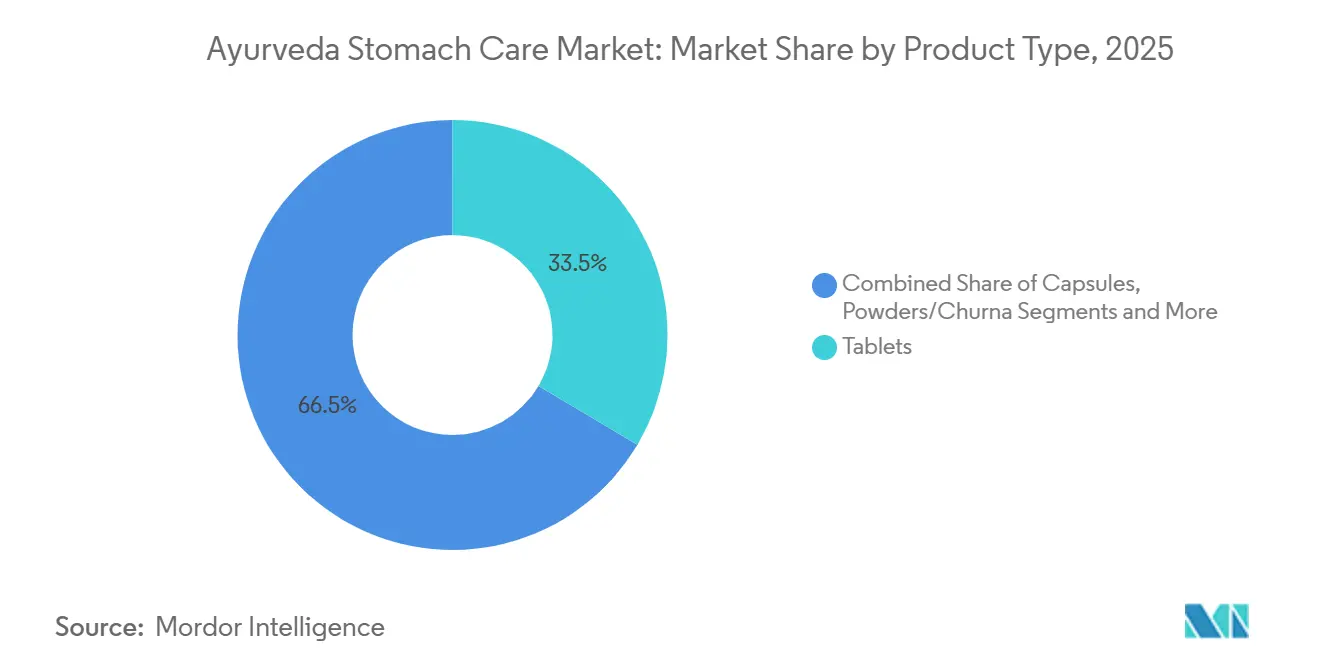

- By product type, tablets led with 33.52% Ayurveda stomach care market share in 2025. Ready-to-drink herbal shots are expanding at an 11.24% CAGR to 2031, the fastest pace among all product formats.

- By distribution channel, OTC retail pharmacies held 35.23% of the Ayurveda stomach care market size in 2025. E-commerce is set to register a 10.35% CAGR through 2031, outpacing every other channel.

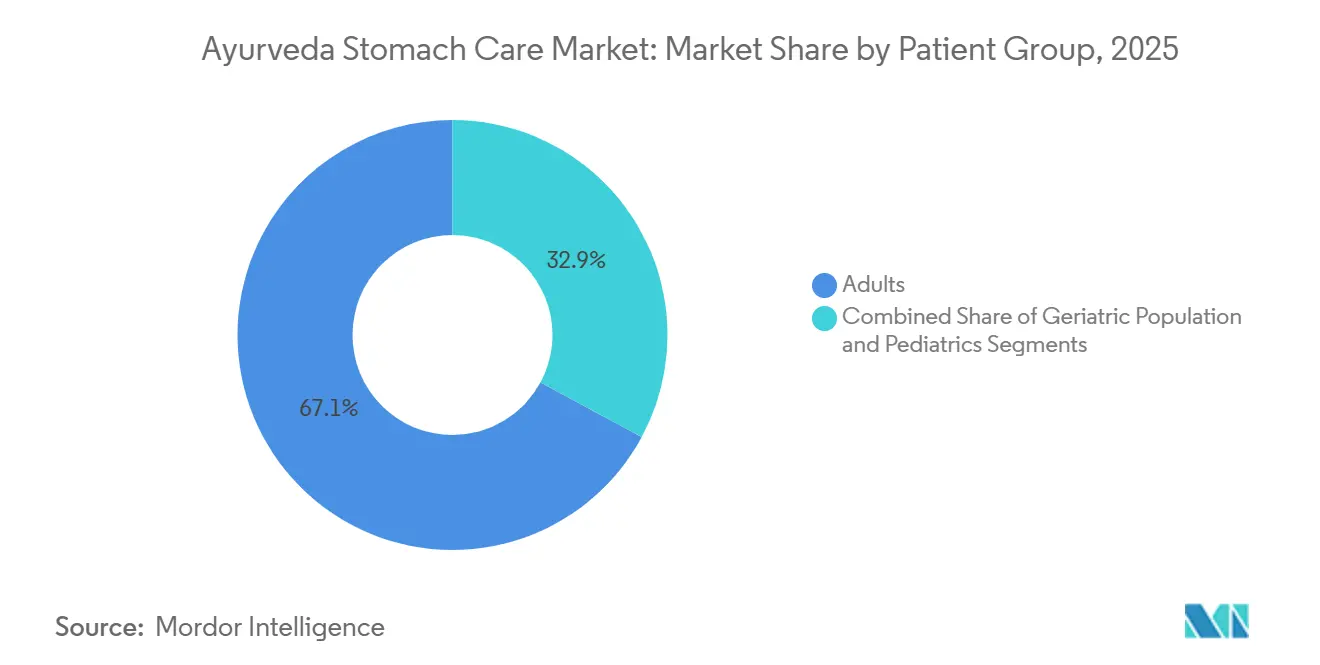

- By patient group, adults accounted for 67.13% of user value in 2025, while pediatric formulations are forecast to rise at a 9.23% CAGR to 2031.

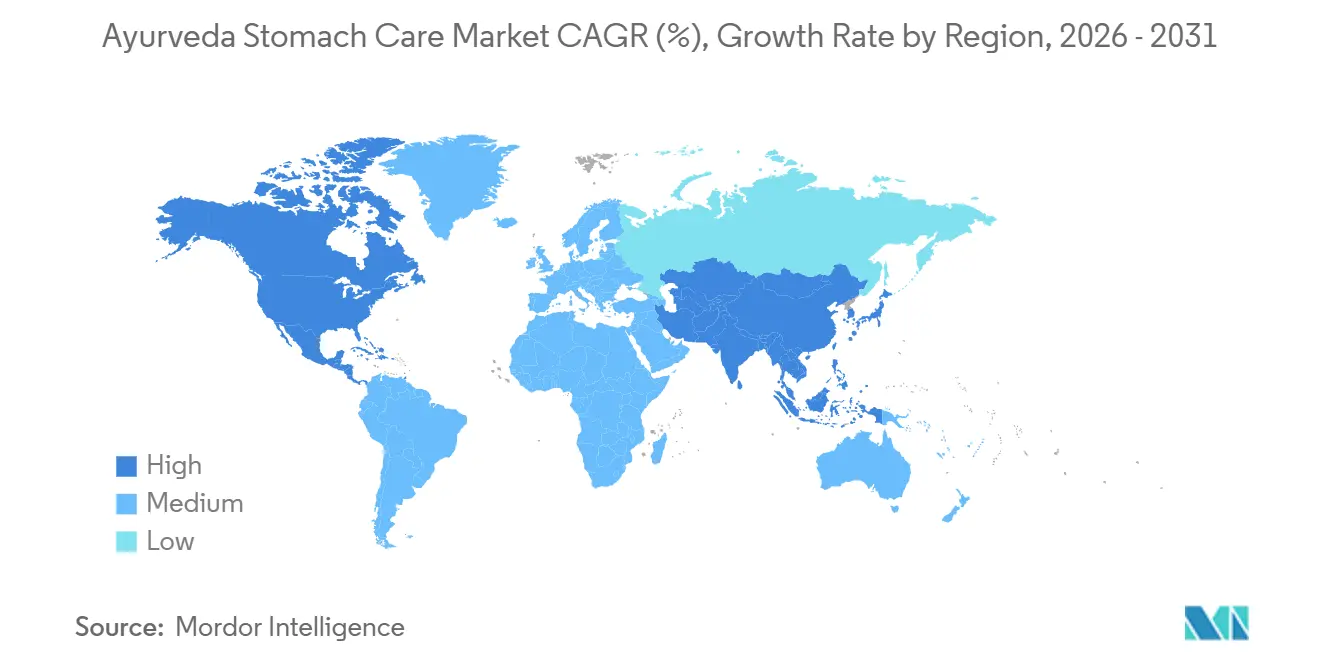

- Asia-Pacific commanded 42.32% share of the Ayurveda stomach care market size in 2025, yet North America is advancing at a 9.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ayurveda Stomach Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of gastrointestinal disorders | +1.2% | Global with focus on South Asia and Sub-Saharan Africa | Long term (≥ 4 years) |

| Growing consumer preference for herbal and natural remedies | +1.5% | North America, Europe, Urban Asia-Pacific | Medium term (2-4 years) |

| Government promotion and integration of Ayurveda in public healthcare | +1.3% | India with regional spill-over | Long term (≥ 4 years) |

| Tele-consultation enabling personalized digestive therapies | +0.8% | India, United States, United Kingdom | Short term (≤ 2 years) |

| Botanical bioavailability enhancers improving formulation efficacy | +0.9% | North America, Europe, Premium Asia-Pacific | Medium term (2-4 years) |

| Cross-border diaspora e-commerce demand | +0.7% | United States, Canada, United Kingdom, Australia, GCC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Gastrointestinal Disorders

World Health Organization data show that diarrheal diseases caused 1.2 million deaths in 2019, underscoring a massive unmet clinical need.[1]World Health Organization, “WHO Traditional Medicine Global Summit 2024,” who.int Chronic cases such as irritable bowel syndrome and reflux linger despite conventional drugs, which often create side effects or rebound symptoms. Ayurvedic stomach care formulas use multi-herb blends that soothe mucosa, regulate motility, and balance microbiota in one regimen. Urbanization and processed diets enlarge the addressable pool every year, especially where healthcare access remains fragmented. India’s National Ayurveda Morbidity Survey logged higher digestive visits at 12,500 co-located units in 2024, proving patients are embracing herbal first-line care.[2]Press Information Bureau, “Press Release: Budget 2024-25 Highlights for Ministry of AYUSH,” Government of India, pib.gov.in

Growing Consumer Preference for Herbal and Natural Remedies

U.S. herbal supplement sales climbed in 2024, led by Ashwagandha and turmeric, both Ayurvedic staples. Consumers, disappointed by proton pump inhibitors, seek plant-based options that address root causes rather than mask symptoms. Ayurvedic narratives around dosha balance and Agni cultivation resonate with wellness seekers who value agency. Certifications such as USDA Organic and B Corp status give brands a price premium in Western outlets. In emerging Asia, affordability and cultural familiarity keep adoption rates high among middle-income households.

Government Promotion and Integration of Ayurveda in Public Healthcare

India allocated INR 3,050.38 crore (USD 366 million) for Ayurveda infrastructure in the 2024-25 budget, embedding 12,500 co-located units in public hospitals. The WHO Traditional Medicine Summit in 2024 gathered 88 member states that endorsed Ayurveda for universal coverage.[3]World Health Organization, “Diarrhoeal Disease Fact Sheet,” who.int Neighboring Nepal, Sri Lanka, and Bangladesh now replicate India’s model, giving regional producers predictable procurement contracts. Insurance schemes that reimburse herbal consultations lower out-of-pocket costs, broadening access.

Tele-consultation Enabling Personalized Digestive Therapies

Platforms such as JIVA Ayurveda enable video assessments that match constitutional types to bespoke herb plans without in-clinic visits. Frequent virtual follow-ups improve symptom tracking and diet coaching, delivering outcomes that brick-and-mortar clinics struggle to match. Diaspora users connect with India-based doctors, sidestepping local practitioner shortages and high fees. Data integration with AI symptom checkers raises diagnostic precision, yet cross-border regulation remains unsettled in the United States and Europe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of standardized clinical evidence for efficacy and safety | -0.9% | North America, Europe, Urban Asia-Pacific | Long term (≥ 4 years) |

| Heterogeneous regulatory frameworks across countries | -0.7% | Global with acute friction in North America and EU | Medium term (2-4 years) |

| Climate-linked supply-chain vulnerability for key herbs | -0.6% | India, Nepal, Sri Lanka with global downstream effect | Medium term (2-4 years) |

| Adulteration scandals undermining consumer trust | -0.8% | Global with high reputational risk in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lack of Standardized Clinical Evidence for Efficacy and Safety

A 2024 Cochrane review found only 73 randomized trials suitable for meta-analysis on herbal dyspepsia treatments, too heterogeneous to support firm conclusions. The U.S. FDA botanical guidance demands Phase III trials and detailed toxicology, costs that few Ayurvedic firms can shoulder. India’s research council is sponsoring multicenter trials on Triphala, yet publication cycles trail commercial needs, limiting physician confidence in the interim.

Heterogeneous Regulatory Frameworks Across Countries

The FDA treats Ayurvedic products as supplements that cannot claim to cure disease, while the EU’s directive requires 30 years of documented use and quality dossiers priced beyond many exporters. Maintaining multiple label sets and formulations inflates overhead, pushing smaller firms out of high-value regions and concentrating share among conglomerates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Convenience Formats Challenge Tablet Leadership

Tablets held 33.52% Ayurveda stomach care market share in 2025 on the strength of low cost, pharmacy compatibility, and dosing familiarity. Ready-to-drink herbal shots are forecast to expand at an 11.24% CAGR, reflecting a consumer pivot toward grab-and-go wellness. Powders retain authenticity for domestic buyers yet face friction abroad where preparation rituals feel foreign. Syrups satisfy pediatric palatability but demand cold-chain logistics. Bioavailability enhancers such as piperine permit dose reduction, lowering raw material spend and stabilizing margins. The functional beverage subset is drawing venture capital as brands like Health-Ade graft Ayurvedic botanicals onto kombucha and tonic lines, blurring categories and expanding shelf presence.

Tablets still enjoy pharmacopeial standards that streamline quality control, and incumbents such as Dabur cushion share with hybrids like Hajmola, which merges digestive herbs with contemporary flavors. Ready-to-drink players must solve stability hurdles around pH drift and microbial growth, often requiring aseptic lines that raise capital needs. Capsules appeal to Western users who value standardized dosing, though higher unit costs temper speed. Oils and pastes remain niche topical formats for massage-based relief, limiting scale but delivering margin due to premium pricing.

By Distribution Channel: Digital Commerce Redraws the Path-to-Patient

OTC pharmacies captured 35.23% of Ayurveda stomach care market size in 2025, a function of trust and location. Pharmacists frequently co-recommend Ayurvedic products alongside allopathic scripts, ensuring visibility at the moment of purchase. Yet e-commerce is projected to post a 10.35% CAGR through 2031, riding subscription models and cross-border fulfillment. Digital channels now contribute 35% of Dabur’s India revenue, a landmark illustrating the speed at which online sales cannibalize shelf-space reliance.

Marketplace regulation is tightening, with the FDA directing platforms to verify seller legitimacy, weeding out non-compliant listings and gifting share to brands that invest in documentation. Specialty clinics and hospitals, while authoritative, lack geographic spread outside metros, limiting unit sales. Hypermarkets impose slotting fees that only high-volume SKUs can absorb, further nudging smaller labels into direct-to-consumer tactics.

By Patient Group: Pediatric Demand Outpaces the Adult Core

Adults accounted for 67.13% of user volume in 2025 due to higher incidence of chronic digestive issues. Pediatric formulations, however, are growing at 9.23% CAGR as parents steer clear of antibiotics and seek milder relief for colic or constipation. Himalaya’s kid-centric syrups and gummies show that flavor masking and dose adjustments can unlock uptake. Geriatric users, while fewer in number, display high per-capita spend as polypharmacy burdens push them toward gentler adjunctives.

Regulators scrutinize pediatric claims more closely. The FDA asks for age-specific safety data, a hurdle that raises trial costs. Palatability remains a barrier; sugar content invites scrutiny from clean-label guardians. Brands resolve the conflict by switching to non-nutritive natural sweeteners. In the elderly cohort, modified-release profiles and lower pill counts improve adherence but require pharma-grade capability, raising entry barriers for small firms.

Geography Analysis

Asia-Pacific maintained 42.32% of Ayurveda stomach care market size in 2025, driven by India’s vast domestic base and export pipelines. New budget allocations and 12,500 co-located hospital units give Ayurveda systemic legitimacy, stimulating prescription volumes. China and Japan trial Ayurveda under cross-cultural wellness pilots, while Australia’s regulator classifies products as complementary medicines, demanding proof of traditional use. Supply risk remains as climate volatility disrupts Himalayan herb yields.

North America is projected to register the fastest 9.64% CAGR through 2031. Herbal supplement sales passed USD 13 billion in 2024, with Ashwagandha and turmeric ranking top sellers. Diaspora consumers seed initial demand, and mainstream wellness circles amplify adoption through social proof. Import alerts tied to heavy metals heighten quality scrutiny, steering volume to firms that hold NSF or USP seals.

Europe advances at a slower pace owing to the high cost of registering products under the EU Traditional Herbal Medicinal Products Directive. Germany and the United Kingdom remain bright spots due to naturopathic networks and integrative clinics. Middle East and Africa gain share through expatriate inflows and government exploration of cost-effective traditional modalities. South America is nascent yet promising as wellness tourism opens channels in Brazil and Argentina.

Competitive Landscape

The Ayurveda stomach care market revenue indicates a moderately concentrated field. Dabur leverages scale and a wide SKU portfolio, reporting 6.8% healthcare growth and 35% domestic online sales share in Q2 FY25. Patanjali posted INR 33,000 crore (USD 4 billion) in FY24 revenue, yet overseas income remains under 15%, signaling room for export scale-up. Himalaya, Kerala Ayurveda, and Arya Vaidya Pharmacy differentiate through clinic networks and heritage branding that command higher unit margins.

Competitive strategies split between cost leadership and science-backed differentiation. Natreon’s standardized ingredients help downstream brands meet Western regulatory proof thresholds. Bioavailability patents around phytosome delivery erect technical barriers that may lock out copycats. Heavy metal recalls spur consolidation as smaller firms lacking quality budgets accept acquisition offers from larger peers who need brand diversity. White-space growth lies in pediatric, geriatric, and ready-to-drink niches where incumbents hold limited mindshare.

Climate risk pushes leaders to contract farming or own estates for critical herbs, reducing exposure to raw-material swings. Digital marketing funnels and influencer partnerships give direct-to-consumer brands lower acquisition costs versus legacy TV spots. Certifications such as USDA Organic and B Corp allow emerging labels like Organic India to charge premiums in Whole Foods and similar chains, proving that value gets unlocked when heritage meets modern governance.

Ayurveda Stomach Care Industry Leaders

Baidyanath Ayurved Bhawan Pvt Ltd

Patanjali Ayurved Ltd

Zandu (Emami)

Himalaya Wellness Company

Dabur India Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: OneVeda entered India with clinically validated Ayurvedic lines targeting consumer trust gaps.

- October 2025: Jeena Sikho Lifecare rolled out a national Pet-Yakrit-Pleeha Shuddhi Kit and inked a five-year diagnostic pact with Chandan Healthcare to deepen preventive services.

- August 2025: FSSAI published an official Ayurveda Aahara list to standardize acceptable food preparations and resolve labeling ambiguities.

Global Ayurveda Stomach Care Market Report Scope

Ayurveda stomach care is a holistic practice that balances doshas (body energies), strengthens Agni (digestive fire), and eliminates toxins (ama) through herbs, and detoxification to address digestive issues like indigestion, bloating, and acidity.

The Ayurveda Stomach Care Market Report is segmented by Product Type, Distribution Channel, Patient Group, and Geography. By Product Type, the market is segmented into Powders/Churna, Tablets, Syrups & Tonics, Capsules, Oils & Pastes, Ready-to-drink Herbal Shots, and Other Product Types. By Distribution Channel, the market is segmented into OTC Retail Pharmacies, Ayurvedic Speciality Clinics & Hospitals, Hypermarkets & Supermarkets, E-commerce, and Other Channels. By Patient Group, the market is segmented into Adults, Geriatric Population, and Pediatrics. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Powders / Churna |

| Tablets |

| Syrups & Tonics |

| Capsules |

| Oils & Pastes |

| Ready-to-drink Herbal Shots |

| Other Product Types |

| OTC Retail Pharmacies |

| Ayurvedic Speciality Clinics & Hospitals |

| Hypermarkets & Supermarkets |

| E-commerce |

| Other Channels |

| Adults |

| Geriatric Population |

| Pediatrics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Powders / Churna | |

| Tablets | ||

| Syrups & Tonics | ||

| Capsules | ||

| Oils & Pastes | ||

| Ready-to-drink Herbal Shots | ||

| Other Product Types | ||

| By Distribution Channel | OTC Retail Pharmacies | |

| Ayurvedic Speciality Clinics & Hospitals | ||

| Hypermarkets & Supermarkets | ||

| E-commerce | ||

| Other Channels | ||

| By Patient Group | Adults | |

| Geriatric Population | ||

| Pediatrics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the Ayurveda stomach care market?

The market stands at USD 933 million in 2026.

How fast is global demand expected to grow?

Forecasts show a 7.34% CAGR through 2031.

Which product format is expanding the quickest?

Ready-to-drink herbal shots are rising at an 11.24% CAGR.

Why is North America the fastest growing region?

Diaspora demand, clean-label trends, and e-commerce push the region to a 9.64% CAGR.

What limits Ayurvedic brands from entering Europe?

The EU directive demands costly registrations and 30 years of traditional use evidence.

How are companies improving herbal efficacy?

Bioavailability enhancers such as piperine and phytosome complexes increase absorption, supporting clinical validation.

Page last updated on: