Avascular Necrosis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

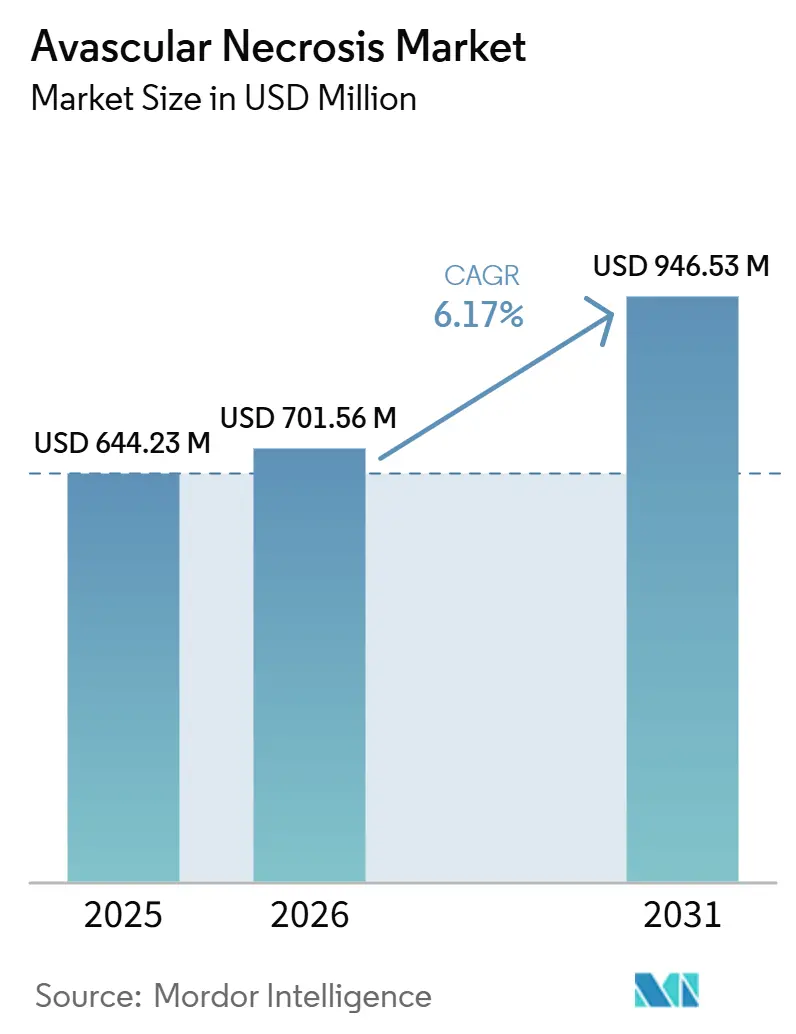

| Market Size (2026) | USD 701.56 Million |

| Market Size (2031) | USD 946.53 Million |

| Growth Rate (2026 - 2031) | 6.17% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Avascular Necrosis Market Analysis by Mordor Intelligence

The Avascular Necrosis Market size is expected to grow from USD 644.23 million in 2025 to USD 701.56 million in 2026 and is forecast to reach USD 946.53 million by 2031 at 6.17% CAGR over 2026-2031.

The avascular necrosis market is being shaped by the rising burden of non-traumatic disease, broader use of joint-preserving care in earlier stages, and steady procedure demand in later-stage hip damage. Steroid-linked disease continues to expand the treated pool, with published evidence showing wide incidence variation in high-dose corticosteroid users and an added wave of post-COVID cases in younger adults who are more likely to seek preservation options before replacement. The avascular necrosis market is also benefiting from stronger MRI-led detection pathways, because earlier recognition shifts more patients into decompression, drug-based management, and regenerative procedures instead of immediate arthroplasty. Asia-Pacific remains the clearest expansion opportunity for the avascular necrosis market, supported by a large diagnosed base in China and continued hospital capacity growth across major Asian care systems. Competitive activity in the avascular necrosis market remains firm among large orthopedic manufacturers, while reimbursement limits, uneven clinical evidence for cell therapies, and specialist shortages continue to slow the pace of adoption in several care settings.

Key Report Takeaways

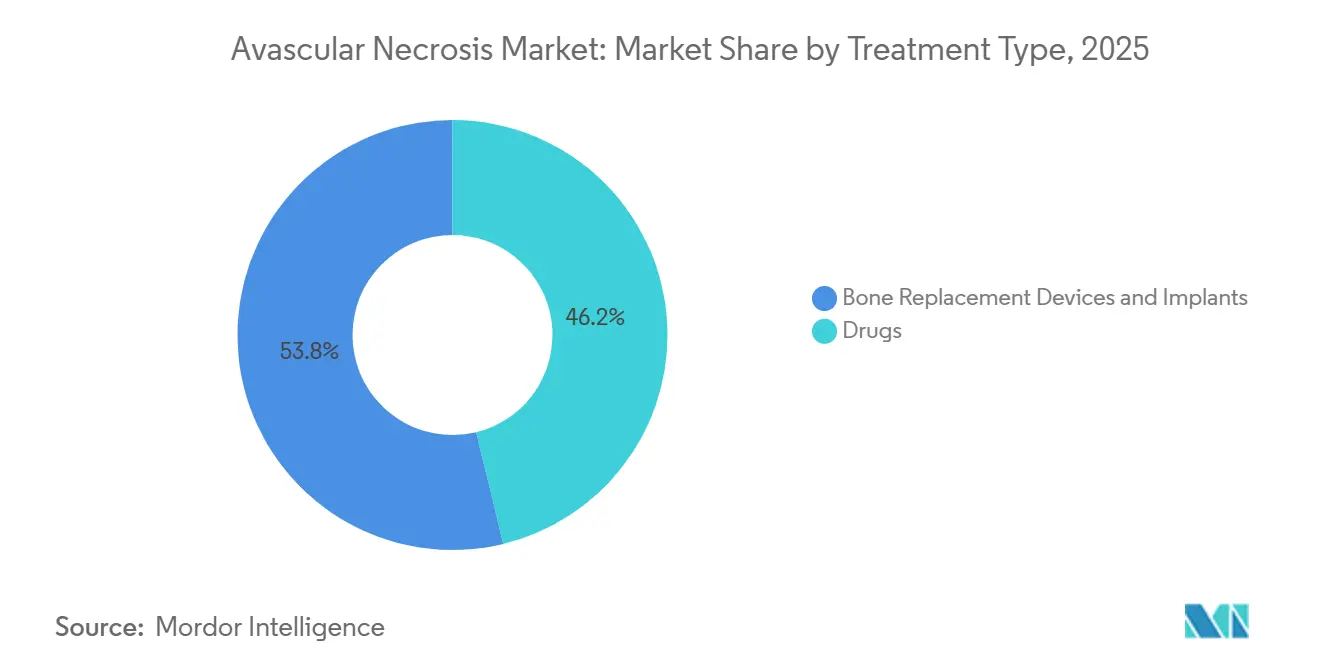

- By treatment type, bone replacement devices and implants accounted for 53.83% of the avascular necrosis market size in 2025, while the same segment is projected to expand at a 7.15% CAGR through 2031.

- By disease type, non-traumatic AVN held 60.38% of the avascular necrosis market share in 2025, while non-traumatic AVN also recorded the highest projected CAGR at 6.76% through 2031.

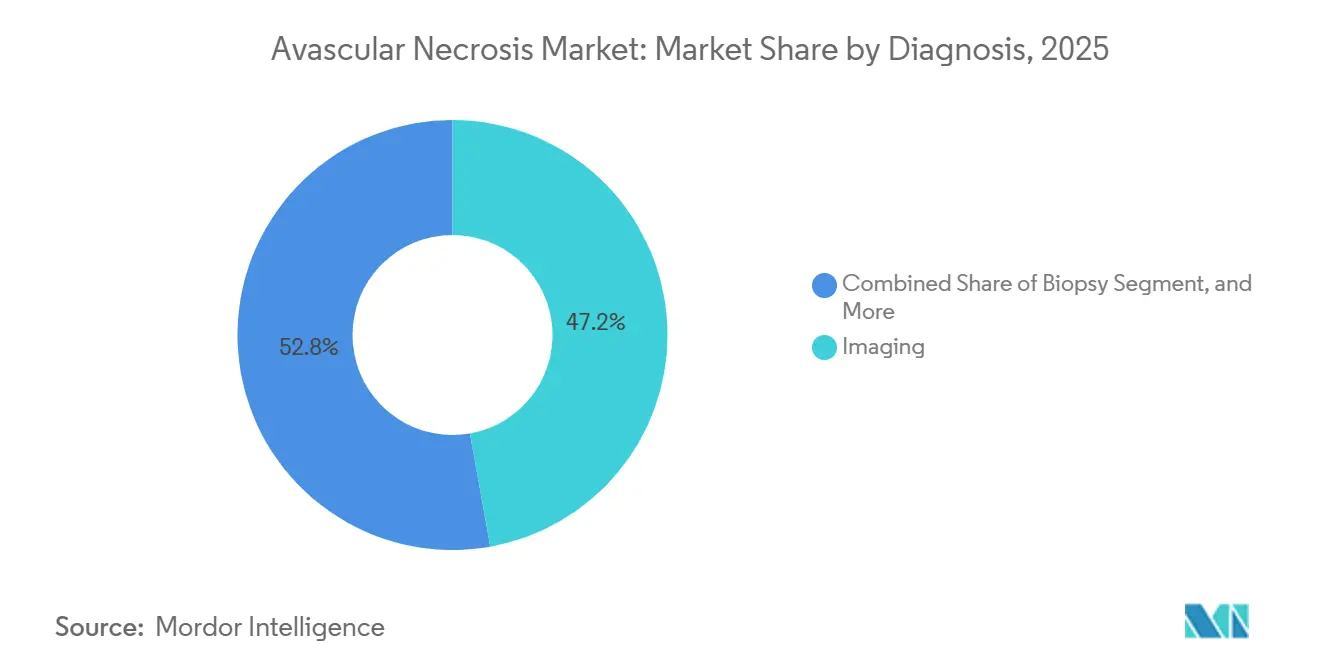

- By diagnosis, imaging represented 47.16% of the avascular necrosis market size in 2025, while imaging is forecast to advance at a 7.57% CAGR through 2031.

- By end user, hospitals held 44.63% share in 2025, while specialty clinics are projected to grow at the fastest CAGR of 6.94% through 2031.

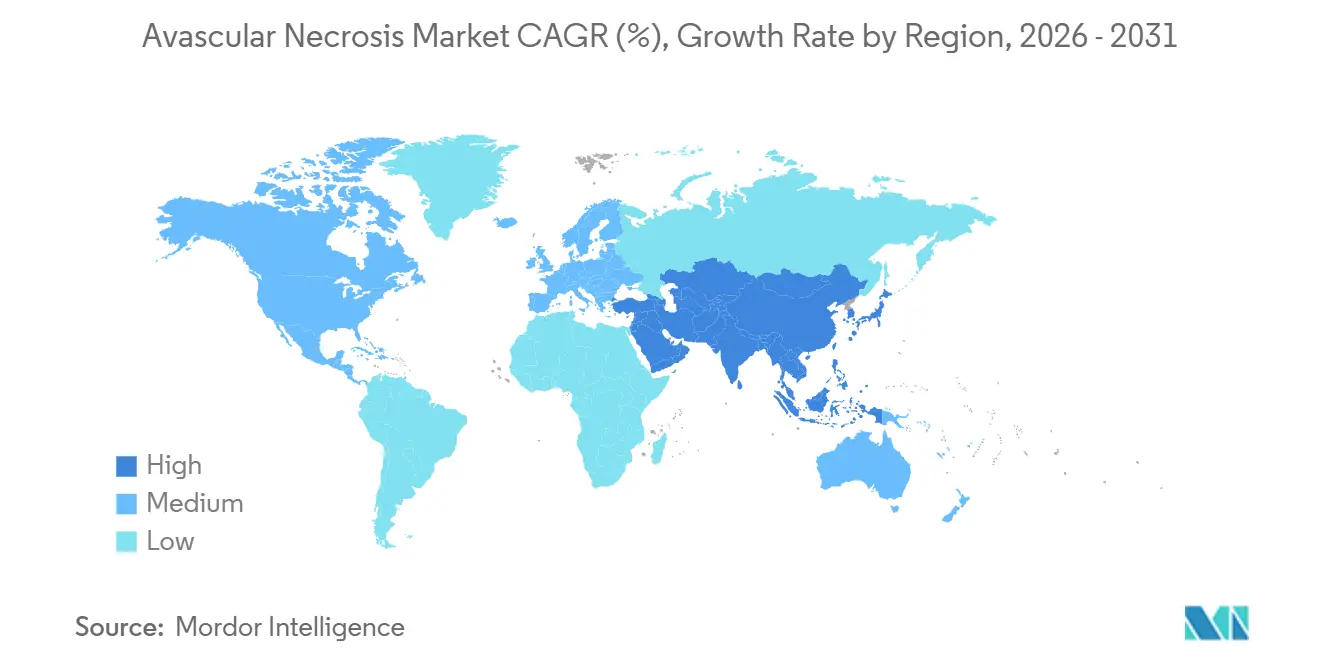

- By geography, North America held 38.63% share in 2025, while Asia-Pacific is projected to expand at a 7.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Avascular Necrosis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Steroid-Induced And Trauma-Related Bone Ischemia | +1.8% | Global, strongest in North America and Asia-Pacific | Short term (≤ 2 years) |

| Expanding Joint Replacement And Bone Preservation Volumes | +1.5% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rising MRI-Based Early Diagnosis And Risk Screening | +0.9% | North America and Europe, expanding into Asia-Pacific | Short term (≤ 2 years) |

| Growing Regenerative And Cell-Based Therapy Pipeline | +0.8% | Global, with early gains in North America and Asia-Pacific | Long term (≥ 4 years) |

| Increasing Use Of Specialty Orthopedic Referral Pathways | +0.5% | North America and Western Europe | Medium term (2-4 years) |

| Expanding Medical Tourism For Advanced Orthopedic Care | +0.4% | Asia-Pacific core, with spillover into Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Steroid-Induced and Trauma-Related Bone Ischemia

Corticosteroid exposure remains the strongest modifiable demand driver in the avascular necrosis market. A 2024 review in Diagnostics reported incidence ranging from 3% to 37% in patients receiving high-dose corticosteroids, and it noted a 21% rate even in high-dose users without added risk factors. A 2025 review in the Journal of Orthopaedic Research linked post-COVID AVN onset to a mean latency of 126 days and cumulative steroid exposure of 1,198 mg prednisolone equivalent. This pattern matters because many of these patients are in the 30-45 age group, which increases demand for joint preservation instead of immediate replacement. Trauma-related AVN is also supporting the avascular necrosis market, because fractures, dislocations, and crush injuries still create a durable surgical pool in high-volume orthopedic systems. The combined effect is a wider treatment funnel that supports drugs, decompression, implants, and regenerative care across the avascular necrosis market.

Expanding Joint-Replacement and Bone-Preservation Procedure Volumes

Procedure expansion remains one of the clearest growth supports for the avascular necrosis market. The American Joint Replacement Registry recorded more than 4.4 million hip and knee arthroplasty procedures through 2024, and its 2025 annual report showed an 8.8% year-over-year increase in procedure count.[1]American Academy of Orthopaedic Surgeons, “American Joint Replacement Registry 2025 Annual Report,” AAOS That trend confirms that late-stage intervention demand remains elevated, even after pandemic-related disruption has passed. The avascular necrosis market benefits directly because total hip arthroplasty still absorbs a large share of advanced femoral head collapse cases. Bone-preserving surgeries also remain relevant in earlier disease, especially when patients are diagnosed before structural collapse. Wider approval for same-day arthroplasty and continued device launches should keep procedure volume growth central to the avascular necrosis market over the forecast period.

Rising Adoption of Early MRI-Based Diagnosis and Risk-Stratified Screening

MRI-led diagnosis is widening the addressable treatment base in the avascular necrosis market. A 2024 study in Cureus reported that plain radiography detected only 41% of Stage I cases, while MRI identified marrow and subchondral changes that X-ray could not capture at the same point.[2]Cureus Editorial Team, “Early-Stage AVN Detection Performance of Plain Radiography and MRI,” Cureus A 2025 multicenter study in Frontiers in Surgery validated a 3D deep-learning framework for automated staging of early femoral head osteonecrosis on MRI. Earlier and more consistent staging moves patients into decompression, drug therapy, and regenerative options sooner. That shift supports a broader revenue mix across the avascular necrosis market instead of concentrating value only in late-stage replacement. It also improves planning efficiency for surgeons and hospitals that are building dedicated AVN pathways.

Growing Pipeline for Regenerative and Cell-Based Joint-Preservation Therapies

Regenerative platforms are adding a longer-term expansion layer to the avascular necrosis market. A 2025 meta-analysis in PLOS ONE found lower femoral head collapse rates and lower arthroplasty conversion in bone marrow stem cell-treated groups, with hip preservation reaching 90% in early to mid-stage disease. A 2025 systematic review in Frontiers in Pharmacology also found that bone marrow aspirate concentrate combined with core decompression outperformed decompression alone in slowing progression.[3]Frontiers in Surgery Editorial Team, “Deep Learning Framework for Early Femoral Head Osteonecrosis Staging,” Frontiers in Surgery Commercial rollout is still limited by dosing variability, manufacturing complexity, and reimbursement policy. Even so, the avascular necrosis market is gaining a more layered treatment structure, where high-cost autologous options may sit beside future off-the-shelf allogeneic or vesicle-based products. That pipeline depth is important because it keeps the avascular necrosis market from relying only on mature implant categories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure costs and reimbursement friction | -1.2% | North America & EU; most acute in the United States | Short to medium term (≤ 4 years) |

| Late presentation and low primary-care recognition | -0.8% | Global; most severe in MEA and South America | Long term (≥ 4 years) |

| Limited long-term evidence for regenerative interventions | -0.5% | Global; regulatory impact concentrated in North America and EU | Long term (≥ 4 years) |

| Shortage of skilled orthopedic surgeons in emerging markets | -0.4% | MEA, South America, APAC periphery (excluding China, Japan, South Korea) | Medium to long term (2–4+ years) |

| Source: Mordor Intelligence | |||

High Procedure Costs and Reimbursement Friction

Reimbursement remains one of the clearest brakes on the avascular necrosis market. Aetna updated coverage policy CPB 0753 in November 2025 and tightened the distinction between covered core decompression use and experimental adjunctive cell-based procedures billed under newer CPT codes. That keeps many regenerative approaches outside routine reimbursement, even as clinical evidence becomes stronger. The avascular necrosis market, therefore shows a mismatch between medical promise and commercial access. In China, price compression in hip implants has also reduced conventional device margins, after reported prices moved from CNY 35,000 (USD 4,900) to CNY 7,000 (USD 980) under national procurement pressure. This pushes manufacturers toward premium systems and leaves parts of the avascular necrosis market exposed to pricing pressure even when unit demand is rising.

Late Presentation and Low Primary-Care Recognition

Delayed diagnosis still limits the avascular necrosis market in many settings. A 2025 diagnostic lag survey in Japan identified avascular necrosis of the femoral head as a condition where delay worsened outcomes because collapse progressed beyond the window for joint-preserving surgery. The problem is amplified when symptoms are mistaken for routine osteoarthritis or non-specific hip pain in primary care. In lower-resource systems, limited orthopedic coverage and weaker MRI access slow referral even more. That reduces the share of patients who can enter higher-value early intervention pathways in the avascular necrosis market. It also shifts care toward costly replacement procedures and narrows the growth runway for conservative and regenerative segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Devices Drive Revenue While Drugs Sustain Adoption

Bone replacement devices and implants held 53.83% share in 2025, and this category is also projected to grow at the fastest 7.15% CAGR through 2031. This leadership shows how much of the avascular necrosis market still depends on late-stage surgical intervention after structural collapse has occurred. Total hip arthroplasty, revision procedures, and cementless fixation systems remain the main revenue base in this segment. The category also benefits from surgeon familiarity, strong registry support, and a steady launch cycle in robotic and navigation-linked platforms. That has kept the avascular necrosis market anchored to devices even as earlier-stage treatment pathways expand.

The Australian registry evidence cited in the source draft points to strong commercial traction for cementless systems, with Stryker's Trident acetabular shell identified as the most implanted cementless acetabular system in that registry. This matters because bone ingrowth fixation is well aligned with the needs of many AVN patients who progress to total hip arthroplasty. Bone grafts and vascularized graft techniques remain relevant, but their uptake depends more heavily on specialist skill and center capability. Drugs still play a durable supporting role in the avascular necrosis market by addressing pain, inflammation, and vascular risk factors in earlier disease stages. A 2026 Scientific Reports study also linked pravastatin plus fibrin sealant-embedded bone marrow stem cells with better repair outcomes and stronger VEGF expression in a steroid-induced model, which suggests that drug and biologic boundaries may keep narrowing. That crossover could gradually broaden the treatment mix inside the avascular necrosis market without displacing the central role of implants in advanced disease.

By Disease Type: Non-Traumatic AVN Shapes Market Priority Across the Value Chain

Non-traumatic AVN accounted for 60.38% of the avascular necrosis market share in 2025, and it is also the fastest-growing disease segment with a 6.76% CAGR through 2031. This pattern places steroid exposure, systemic disease, and vascular compromise at the center of the avascular necrosis market. The segment is especially important because it often creates multifocal disease and repeated imaging, treatment, and follow-up needs across several joints. A 2025 report cited in the source draft described rising multifocal osteonecrosis in corticosteroid-treated patients, which lifts the average burden per case. That dynamic gives the avascular necrosis market a broader service and product requirement than a single-joint procedural model would suggest.

Steroid-induced disease remains the largest subtype within non-traumatic AVN, while idiopathic and radiation-related cases add smaller but harder-to-predict patient pools. Sickle cell disease-associated and lupus-related presentations also shape demand in selected regions where those underlying disorders are more visible in clinical practice. Traumatic AVN still represents a large secondary pool, near 40% of the segment in the source draft, and it often reaches care through fracture, dislocation, and post-surgical pathways. A 2026 network meta-analysis in Frontiers in Endocrinology found that high-dose autologous stem cell therapy combined with core decompression lowered the risk of hip failure and femoral head collapse relative to decompression alone. That finding is commercially relevant because traumatic cases can be well-suited to hip-preserving strategies when they are identified early enough. Together, these patterns keep the avascular necrosis market focused on both complex systemic disease management and surgically defined injury-related care.

By Diagnosis: Imaging Consolidates Share as AI Accelerates Adoption

Imaging represented 47.16% of the avascular necrosis market size in 2025, and imaging is also projected to grow at the fastest 7.57% CAGR through 2031. This dual lead shows that the avascular necrosis market is increasingly organized around earlier and more precise staging. MRI remains the most important modality because it detects marrow edema and subchondral change before plain films become clearly abnormal. A 2024 European Journal of Radiology study showed that multi-sequence MRI combined with radiomics-based classifiers improved separation between early and late-stage disease. That gives the avascular necrosis market a better route into stage-appropriate treatment instead of delayed escalation.

AI-supported interpretation can also extend specialist-level staging support to tier-2 and tier-3 hospitals that lack the same academic imaging depth. CT continues to hold value in procedural planning, especially when surgeons need better definition of lesion geometry before decompression or reconstruction. X-ray remains part of serial monitoring and still matters where cost limits MRI frequency. Biopsy is becoming less central as image resolution and structured interpretation improve. PET and PET-CT remain niche tools in the avascular necrosis market, but they may gain selective use in multifocal disease or complex research settings if the evidence base expands further. Overall, diagnosis in the avascular necrosis market is shifting from simple confirmation toward more detailed triage and treatment selection.

By End User: Hospitals Anchor Volume While Specialty Clinics Gain Strategic Ground

Hospitals held 44.63% share in 2025, which keeps them at the center of procedural volume in the avascular necrosis market. Their lead reflects the concentration of total hip arthroplasty, vascularized graft work, complex imaging, inpatient recovery, and robot-assisted surgery in larger care systems. Hospitals also remain the main setting for advanced trials and structured evaluation of regenerative therapies. This gives them a dual role as both the largest revenue channel and the main innovation gateway in the avascular necrosis market. Rehabilitation centers and ambulatory surgical centers contribute important support capacity, but they remain secondary to hospitals in overall revenue contribution.

Specialty clinics are projected to expand at the fastest 6.94% CAGR through 2031, which shows how the avascular necrosis market is decentralizing some earlier-stage care. Outpatient assessment, MRI review, decompression planning, injections, and pharmacologic management fit well within these settings. The shift is helped by lower outpatient treatment costs and a wider acceptance of ambulatory delivery for selected Stage I and Stage II patients. Specialty regenerative medicine clinics also play a meaningful role in countries where cell-based care is commercially available outside large hospitals. Home care remains a small but emerging channel, tied mainly to post-operative rehabilitation, adherence support, and remote monitoring. Taken together, the avascular necrosis market is keeping hospitals as the procedural core while allowing clinics to capture more of the early and follow-up pathway.

Geography Analysis

North America held 38.63% of the avascular necrosis market share in 2025, which kept it as the largest regional contributor. The United States drives this position through broad implant availability, dense MRI capacity, mature orthopedic referral networks, and reimbursement support for major joint replacement procedures. The 2025 American Joint Replacement Registry report documented more than 4.4 million cumulative hip and knee arthroplasty procedures through 2024, which reflects the depth of the regional procedural base. This infrastructure gives the avascular necrosis market a strong platform for both advanced-stage surgery and earlier imaging-led intervention. Canada and Mexico add to regional volume, with Canada offering stable public coverage and Mexico supporting cross-border orthopedic care in selected centers.

Europe remains a stable part of the avascular necrosis market because large health systems in Germany, France, and the United Kingdom support access to imaging, surgery, and follow-up care. Aging populations in Italy and Spain also keep disease management demand active. Western Europe is moving faster in robotic hip arthroplasty and AI-enabled guidance, which strengthens the premium device layer of the avascular necrosis market. The European Medicines Agency framework for advanced therapy medicinal products will remain important for cell-based commercialization across the region. Eastern European markets remain more cost sensitive, which favors generic drug use and mid-tier implant adoption.

Asia-Pacific is the fastest-growing region in the avascular necrosis market, with a projected 7.04% CAGR through 2031. China dominates the regional opportunity, and the source draft cited more than 8 million cumulative non-traumatic femoral head necrosis cases with 150,000 to 200,000 new diagnoses each year. China also shows how procurement pressure can expand procedure access while reducing conventional implant pricing, which is pushing suppliers toward premium robot-compatible systems. Japan is advancing novel implant technology, and Zimmer Biomet received PMDA approval in September 2025 for an iodine-treated total hip system that directly matters for infection-conscious orthopedic care. South Korea supports a smaller but premium regenerative segment, while Middle East and Africa and South America remain earlier-stage opportunities because of reimbursement gaps, workforce shortages, and lower MRI penetration outside major cities.

Competitive Landscape

The avascular necrosis market is moderately consolidated in orthopedic devices, where Stryker, Zimmer Biomet, Smith and Nephew, and Johnson and Johnson hold strong positions in hip reconstruction platforms. Their strength comes from implant portfolios, surgeon familiarity, distribution reach, and the ability to pair hardware with robotics or digital planning tools. This has made the device layer of the avascular necrosis market more structured than the pharmaceutical and regenerative layers. At the same time, the broader avascular necrosis market remains less concentrated because drug categories are mature and regenerative programs are still scattered across smaller developers. That split explains why competition looks tighter in replacement procedures than in earlier-stage preservation care.

A major strategy in the avascular necrosis market is platform lock-in through robotics and navigation. Stryker launched the Trident II Acetabular System in India in April 2026 with compatibility for Mako SmartRobotics, which strengthens the link between implant choice and surgical software environment. Zimmer Biomet also deepened this model after acquiring OrthoGrid Systems and integrating AI-powered fluoroscopic guidance into the Z1 Femoral Hip System, which it commercialized in November 2024. Smith and Nephew has followed a similar path by linking hip system development with its broader technology and robotics capabilities. These moves raise switching costs for hospitals and surgeons, which helps leading firms protect their position inside the avascular necrosis market.

The early-stage preservation segment remains more open because no single company has built dominant scale there. Regenerative developers such as Mesoblast, Regrow Biosciences, and Vericel are competing more on clinical progress and manufacturing readiness than on installed commercial power. Vericel's March 2026 FDA manufacturing approval is relevant because it expands advanced therapy production capacity and signals how process scale may become a competitive factor in the avascular necrosis market. Price pressure remains stronger in China, where procurement has narrowed the margin pool for conventional implants and shifted competition toward premium add-ons and technology-linked systems. Overall, the avascular necrosis market is likely to remain mixed, with established leaders in implants and a wider field of challengers in biologics and joint-preservation therapies.

Avascular Necrosis Industry Leaders

Johnson and Johnson

Bayer AG

Pfizer Inc.

Sanofi SA

Teva Pharmaceutical Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Stryker launched the Trident II Acetabular System in India, a total hip arthroplasty solution compatible with Mako SmartRobotics and featuring Tritanium In-Growth and X3 crosslinked polyethylene technology, positioning the company to capitalise on India's rapidly expanding joint-replacement volumes driven by AVN and osteoarthritis.

- March 2026: Vericel Corporation received FDA approval for commercial manufacturing at its advanced-therapy cell manufacturing facility in Burlington, Massachusetts, enabling commercial production scale-up of MACI (autologous cultured chondrocytes on porcine collagen membrane) from Q2 2026 and laying infrastructure for potential international expansion into bone-repair applications.

- January 2026: Scientific Reports published findings confirming that pravastatin combined with fibrin sealant-embedded BMSCs produced superior bone-repair outcomes versus core decompression alone in a steroid-induced AVN model, significantly elevating local VEGF expression, evidence that strengthens the rationale for pharmaceutical-biologic combination strategies entering early-phase clinical trials.

Global Avascular Necrosis Market Report Scope

The Avascular Necrosis (AVN) market refers to the global market for the diagnosis, treatment, and management of avascular necrosis (osteonecrosis), a progressive musculoskeletal disorder characterized by the death of bone tissue due to an interruption in blood supply, which can lead to bone collapse, chronic pain, and joint dysfunction if left untreated.

The Avascular Necrosis (AVN) market is segmented by treatment type, disease type, diagnosis, end user, and geography. Based on treatment type, the market is divided into Drugs and Bone Replacement Devices and Implants. The Drugs segment includes Nonsteroidal Anti-Inflammatory Drugs (NSAIDs), Cholesterol-Lowering Drugs, Blood Thinners, and Other Drugs, while the Bone Replacement Devices and Implants segment comprises Bone Grafts, Joint Replacement Surgery, and Cementless Prosthesis. Based on disease type, the market is categorized into Traumatic Avascular Necrosis and Non-Traumatic Avascular Necrosis. The Traumatic segment includes Fracture-Induced, Dislocation-Induced, Post-Surgical, Crush Injury-Related, and Sports Injury-Associated AVN, whereas the Non-Traumatic segment includes Steroid-Induced, Alcohol-Induced, Sickle Cell Disease-Associated, Lupus-Related, Radiation Therapy-Induced, and Idiopathic AVN. Based on diagnosis, the market is segmented into Imaging, Biopsy, Computed Tomography (CT) Scan, Positron Emission Tomography (PET), and X-Ray. Based on end user, the market comprises Hospitals, Specialty Clinics, Rehabilitation Centers, Ambulatory Surgical Centers, and Home Care Settings. Geographically, the market is analyzed across North America (United States, Canada, and Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, and Rest of Asia-Pacific), Middle East & Africa (GCC, South Africa, and Rest of the Middle East & Africa), and South America (Brazil, Argentina, and Rest of South America).

| Drugs | Nonsteroidal Anti-Inflammatory Drugs |

| Cholesterol-Lowering Drugs | |

| Blood Thinners | |

| Other Drugs | |

| Bone Replacement Devices and Implants | Bone Grafts |

| Joint Replacement Surgery | |

| Cementless Prosthesis |

| Traumatic Avascular Necrosis |

| Fracture-Induced |

| Dislocation-Induced |

| Post-Surgical |

| Crush Injury-Related |

| Sports Injury-Associated |

| Non-Traumatic Avascular Necrosis |

| Steroid-Induced |

| Alcohol-Induced |

| Sickle Cell Disease-Associated |

| Lupus-Related |

| Radiation Therapy-Induced |

| Idiopathic |

| Imaging |

| Biopsy |

| Computed Tomography Scan |

| Positron Emission Tomography |

| X-Ray |

| Hospitals |

| Specialty Clinics |

| Rehabilitation Centers |

| Ambulatory Surgical Centers |

| Home Care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Drugs | Nonsteroidal Anti-Inflammatory Drugs |

| Cholesterol-Lowering Drugs | ||

| Blood Thinners | ||

| Other Drugs | ||

| Bone Replacement Devices and Implants | Bone Grafts | |

| Joint Replacement Surgery | ||

| Cementless Prosthesis | ||

| By Disease Type | Traumatic Avascular Necrosis | |

| Fracture-Induced | ||

| Dislocation-Induced | ||

| Post-Surgical | ||

| Crush Injury-Related | ||

| Sports Injury-Associated | ||

| Non-Traumatic Avascular Necrosis | ||

| Steroid-Induced | ||

| Alcohol-Induced | ||

| Sickle Cell Disease-Associated | ||

| Lupus-Related | ||

| Radiation Therapy-Induced | ||

| Idiopathic | ||

| By Diagnosis | Imaging | |

| Biopsy | ||

| Computed Tomography Scan | ||

| Positron Emission Tomography | ||

| X-Ray | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Rehabilitation Centers | ||

| Ambulatory Surgical Centers | ||

| Home Care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the avascular necrosis market?

The avascular necrosis market stands at USD 701.56 million in 2026 and is forecast to reach USD 946.53 million by 2031 at a 6.17% CAGR.

Which treatment segment leads revenue in avascular necrosis care?

Bone replacement devices and implants lead with 53.83% share in 2025, reflecting the heavy role of total hip arthroplasty and related reconstruction in advanced disease.

Which region is growing fastest in avascular necrosis treatment demand?

Asia-Pacific is the fastest-growing region with a projected 7.04% CAGR through 2031, supported by large patient volumes and expanding orthopedic capacity.

Why is MRI becoming more important in avascular necrosis diagnosis?

MRI detects early structural change far better than plain radiography, which helps move more patients into decompression, drug therapy, and regenerative care before collapse.

What is the main restraint on wider uptake of regenerative therapies for avascular necrosis?

Reimbursement remains the biggest barrier because payer policies still limit coverage for many cell-based adjunctive procedures even when clinical evidence improves.

Page last updated on: