Autonomous Vehicle Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

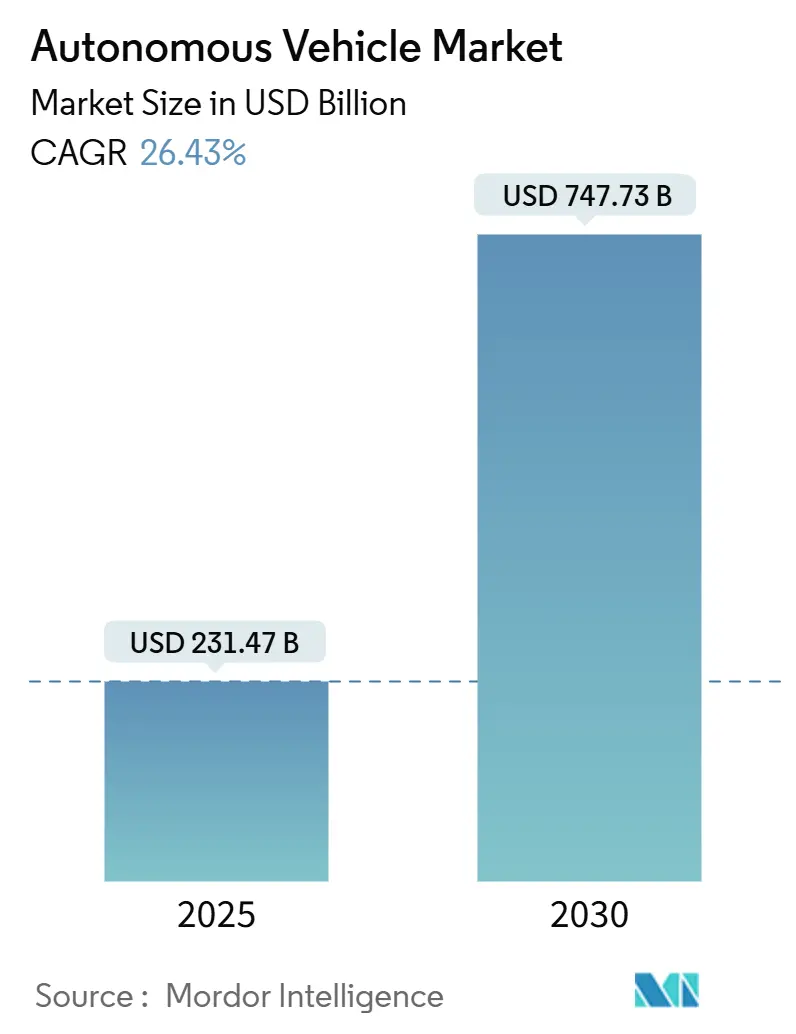

| Market Size (2025) | USD 231.47 Billion |

| Market Size (2030) | USD 747.73 Billion |

| Growth Rate (2025 - 2030) | 26.43% CAGR |

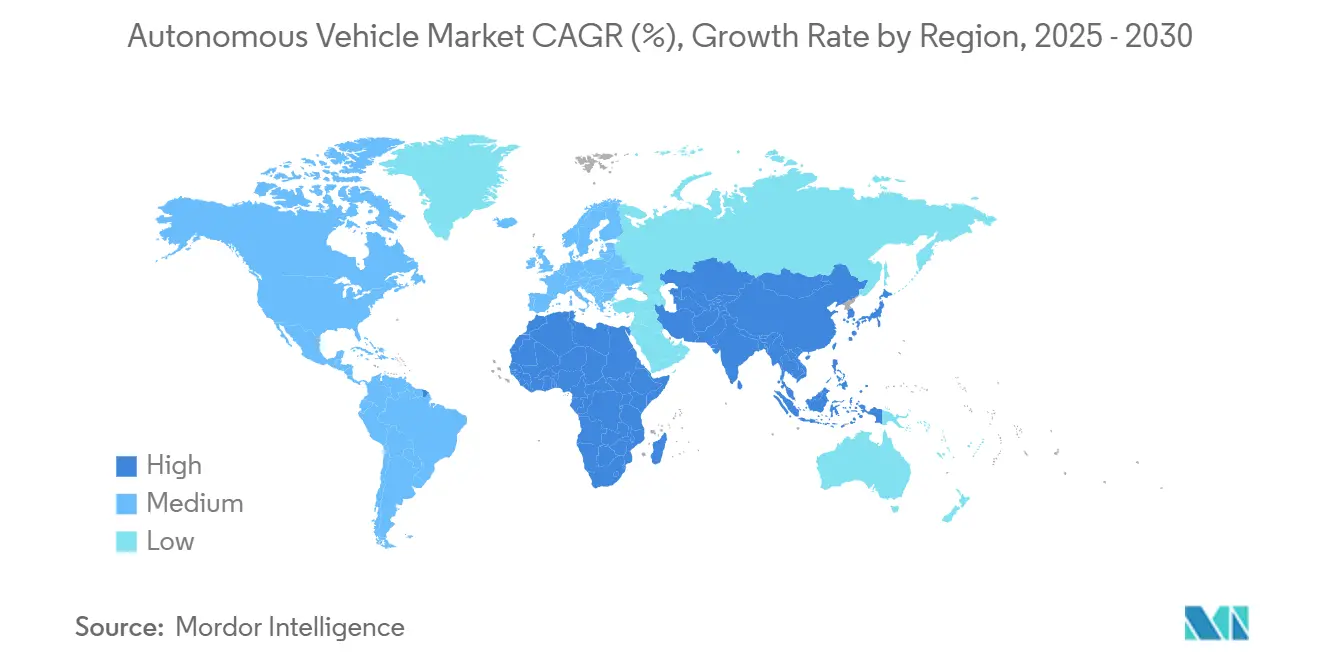

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

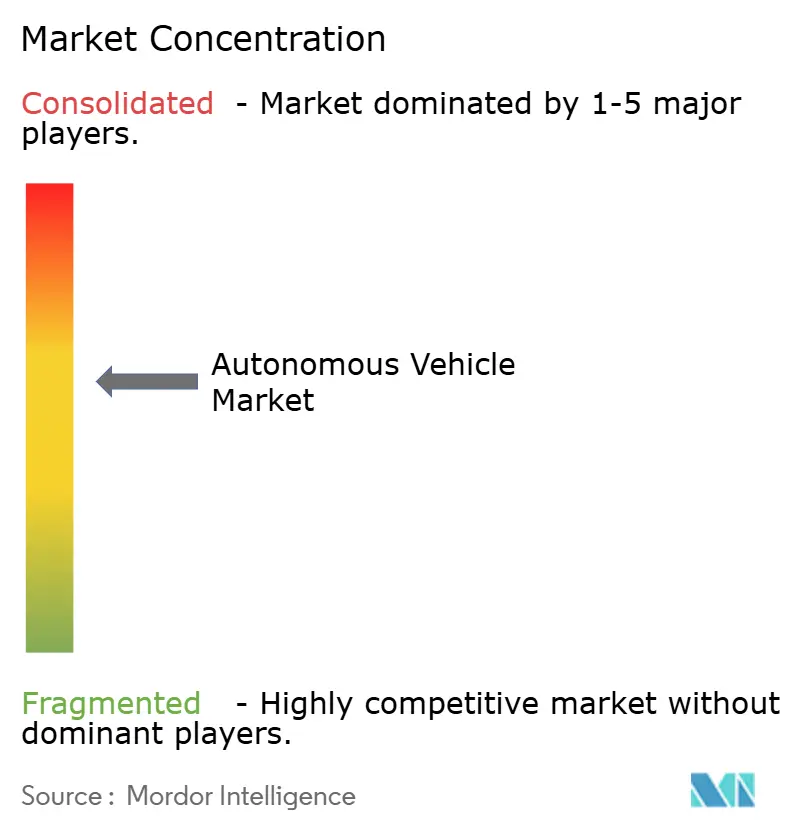

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Autonomous Vehicle Market Analysis by Mordor Intelligence

The autonomous vehicle market size is valued at USD 231.47 billion in 2025 and is projected to reach USD 747.73 billion by 2030, expanding at a compound annual growth rate (CAGR) of 26.43% during 2025-2030. The autonomous vehicle market is evolving quickly, driven by advances in AI, smarter sensors, and powerful simulation tools that help bring safer and more efficient transport options to life, especially in ride-sharing and logistics. More people are warming up to self-driving cars, and tech giants like Waymo and Tesla are already testing robo taxi services in cities like Phoenix, Austin, and even the United Kingdom. At the same time, Chinese players like BYD and Pony.ai are moving fast, rolling out cost-effective autonomous fleets with strong government backing and access to massive data pools. Big opportunities are emerging in commercial robo taxis, self-driving trucks, and autonomous driving software platforms supporting AV development. With new laws on the horizon in the United Kingdom and the EU and rising investments in next-gen connectivity like V2X and 6G, the path is paved for a much smarter and more scalable mobility future.

Key Report Takeaways

- By level of automation, Level 1 (driver assistance) dominated the market with a 45.21% share in 2024, whereas Level 5 (full automation) is projected to expand at a 27.23% CAGR between 2025 and 2030.

- By vehicle type, passenger cars held 78.92% of the autonomous vehicle market share in 2024, while commercial vehicles are anticipated to grow at a 25.72% CAGR by 2030.

- By propulsion type, internal combustion engine (ICE) vehicles led with a 62.35% share in 2024, while battery electric vehicles (BEVs) are set to grow at a 35.21% CAGR through 2030.

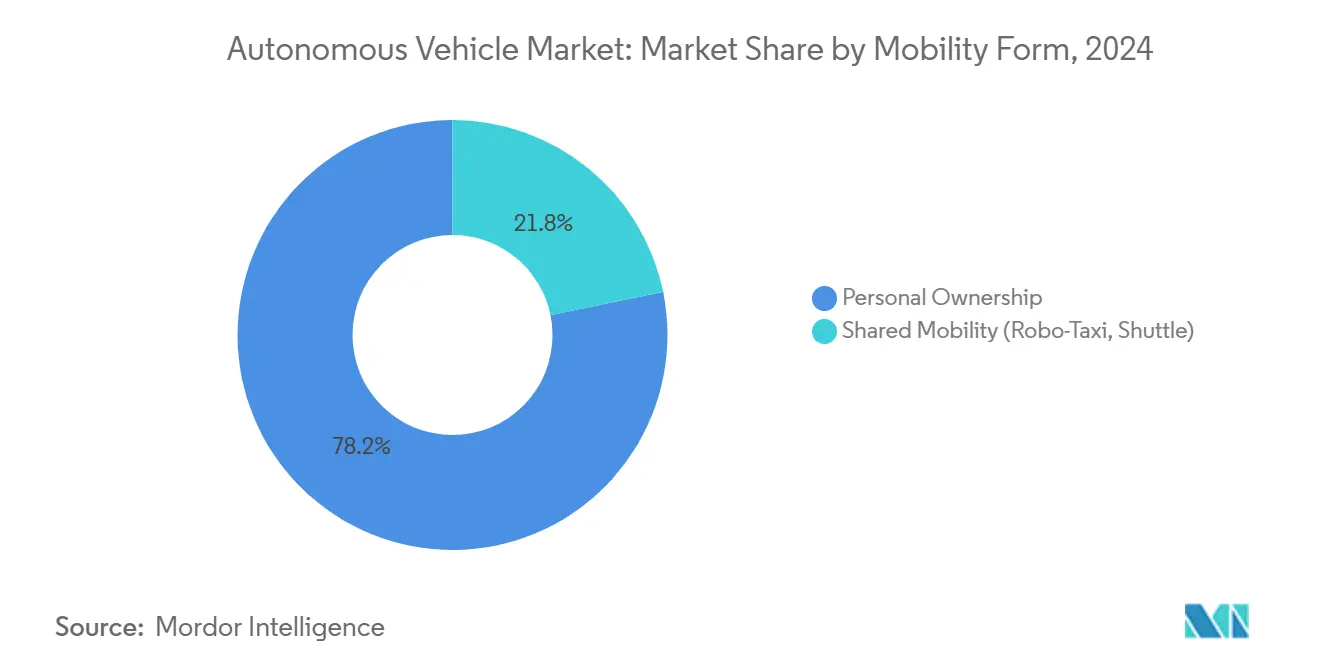

- By mobility form, personal ownership made up 78.21% of the autonomous vehicle market size in 2024, whereas shared mobility services are forecast to grow at a 30.32% CAGR over the 2025–2030 period.

- By component, hardware contributed 57.36% of the autonomous vehicle market size in 2024, while software components are expected to see faster growth with a 26.82% CAGR through 2030.

- By geography, Asia-Pacific led the global autonomous vehicle market with a 46.52% share in 2024, while the Middle East and Africa region is projected to be the fastest-growing with a 28.11% CAGR by 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Autonomous Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ADAS Safety Mandates in EU and China | +5.2% | EU, China, Global | Medium term (2-4 years) |

| Robo Taxi Pilots Expand in Asian Megacities | +4.8% | Asia, North America | Short term (≤ 2 years) |

| Cheaper LiDAR Fuels Mass-Market L3 | +4.5% | Global | Medium term (2-4 years) |

| Power-Efficient SoCs for Vehicle Edge AI | +3.2% | Global | Medium term (2-4 years) |

| 5G-V2X Freight Corridors in North America | +2.8% | North America | Medium term (2-4 years) |

| Fleet Targets Drive Autonomous Logistics | +2.5% | Europe, North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Mandates for ADAS-Centric Safety Regulations in the EU and China

Stringent ADAS safety rules in both regions are pushing the autonomous car industry to accelerate software validation cycles, which in turn drives earlier supplier revenue. The European Commission’s cross-border testbed program and China’s multi-city robo taxi permits are effectively giving vendors clear roadmaps for approval gates, encouraging higher R&D outlays in 2025. An observable consequence is that leading developers are partitioning their codebases to meet region-specific requirements, creating overlapping but not identical feature sets. This segregation subtly increases total software volume, which later influences maintenance costs and talent needs.

Rapid Expansion of Robo Taxi Pilots Across Asian Megacities

Robo taxi fares in cities like Wuhan and Shanghai are now lower than those of traditional ride-hailing services. This trend underscores the potential of autonomous shared mobility to outpace human-driven alternatives, even prior to the complete removal of drivers in all districts. The cost gap is mainly achieved through depot-style fleet management and lower off-peak idle time, an approach that is difficult for traditional taxis to replicate. A notable inference is that lower-income commuters, often overlooked in early AV narratives, are becoming target customers due to these cheaper fares, potentially widening public acceptance faster than anticipated.

Falling LiDAR and AI Compute Costs Are Unlocking Mass-Market Level 3 Launches

Average prices for automotive LiDAR units have significantly decreased over time, while new automotive-grade system-on-chip delivers higher TOPS per watt, permitting automakers to profitably package Level 3 features into premium and select mid-range trims. Automakers now bundle LiDAR with radar-camera fusion as an optional “Level 3 plus” suite, signaling a gradual shift away from single-sensor architectures. Because the incremental bill-of-materials delta is shrinking, finance teams inside OEMs are more willing to green-light broader trims for new geographies, further growing the autonomous vehicle market forecast share of Level 3 vehicles.

Power-Efficient Automotive SoCs Enabling In-Vehicle Edge AI

Next-generation 5 nm and 3 nm automotive chips now process 200-800 TOPS at sub-30 W thermal envelopes, allowing real-time perception without compromising EV range. Suppliers integrating dedicated neural-network accelerators provide deterministic latency, which helps certify safety functions, thereby shortening validation timelines. The quiet implication is that lower energy draw frees battery capacity for cabin features, meaning consumers may see longer range or richer infotainment rather than trade-offs.

Restraints Impact Analysis*

| Restraint | (~) % Point Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented AV Rules Across United States | -3.6% | United States | Short term (≤ 2 years) |

| Public Mistrust Follows Robotaxi Incidents | -3.2% | Global, highest in China | Short term (≤ 2 years) |

| AI Chip Shortages and Fab Constraints | -2.4% | Global | Short term (≤ 2 years) |

| High-Definition Map Maintenance Costs | -2.1% | Southeast Asia, Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Patchwork State-Level AV Regulations in the United States Delay Commercial Scale

With 29 states legislating unique autonomous rules, multi-state service providers must maintain varied reporting, driver-monitoring, and insurance structures, inflating overhead and thereby limiting the autonomous vehicles market share they can capture quickly.[1]"Autonomous Vehicles | Self-Driving Vehicles Enacted Legislation," National Conference of State Legislatures (NCSL), ncsl.org Evidence shows that some developers now pick launch corridors strictly within permissive clusters, which unintentionally sidelines certain high-demand freight lanes. An emerging takeaway is that the lack of a unified framework indirectly channels investment toward simulation rather than on-road testing, potentially stretching development timelines.

Public Mistrust Intensified by High-Profile Robo Taxi Incidents in China

High media visibility of isolated safety mishaps has fueled survey responses that underline discomfort driving near autonomous vehicles, yet willingness to purchase remains sizable. This split indicates that perceived risk can be outweighed by perceived personal safety once inside the vehicle. Manufacturers are therefore investing in transparent incident-report dashboards to build trust, a step that may become a de facto prerequisite for city permits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Level of Automation: L4 Deployment Accelerates Despite L1 Dominance

Level 1 (Driver Assistance) features held 45.21% of the autonomous vehicle market share in 2024, but Level 5 (Full Automation) is projected to grow at a 27.23% CAGR through 2030, meaning higher automation will narrow the gap quickly. Legislative clarity for conditional and high-automation functions encourages suppliers to certify redundant steering and braking subsystems, raising immediate hardware revenue. A subtle effect is that insurers are revising actuarial tables to shift liability to manufacturers for specific modes, hinting at future premium reductions for end users.

Growing interest in Level 3 from luxury buyers brings down development amortization per unit, indirectly funding Level 4 autonomous car research. Models such as the BMW 7-Series with Personal Pilot Level 3 illustrate that early adopters pay premium prices, a margin that helps offset ongoing mapping costs. Additionally, pilot-mode data harvested from Level 3 vehicles is feeding machine-learning models used in Level 4 trucks, shortening data-collection loops across segments.

By Vehicle Type: Commercial Segment Outpaces Passenger Cars

Passenger cars commanded 78.92% of the autonomous vehicle market share during 2024. Yet, many OEMs now view autonomy as a recurring software subscription opportunity rather than a one-time hardware upgrade, shifting the business model toward long-term revenue streams. Over-the-air updates extend feature life cycles, which could lengthen average ownership as buyers anticipate new capabilities mid-cycle. As more households subscribe to partial autonomy, aftermarket suppliers may see declining demand for traditional navigation hardware, suggesting a reshaping of accessory markets.

Commercial vehicles are projected to grow at a 25.72% CAGR through 2030, outpacing passenger cars in market size expansion as autonomy adoption accelerates in logistics and freight segments. Labor shortages and mandated driving-hour limits make autonomy economically compelling for fleet operators, especially in long-haul corridors. An unexpected by-product is that depots invest in robotic maintenance tools to match truck autonomy, thereby modernizing entire yard operations.

By Propulsion Type: BEVs Lead Autonomous Innovation Curve

Internal combustion engines (ICEs) still hold a 62.35% share in 2024, but efficiency-focused hybrid configurations are increasingly chosen for retrofit autonomy in emerging markets where charging infrastructure lags. This pragmatic approach allows fleet owners to benefit from partial autonomy sooner, suggesting a prolonged coexistence phase rather than an abrupt EV takeover.

Battery electric vehicles (BEVs) are forecast to expand at a 35.21% CAGR through 2030, outstripping internal-combustion growth. Because autonomous driving software-defined vehicle platforms sit naturally atop electric architectures, OEMs leverage common high-voltage buses to power sensor suites without extra alternators. An inference here is that battery-swap strategies may gain traction for autonomous taxis, as downtime translates directly into lost fare revenue.

By Mobility Form: Shared Platforms Accelerate AV Commercialization

Personal ownership accounted for 78.21% share of the autonomous vehicle market in 2024, but rising urban congestion fees may push more city dwellers toward flexible subscription-based robo taxi services. Automakers preparing for this shift are piloting flexible ownership models, such as fractional subscriptions, allowing households to alternate between private and shared autonomous access, blending convenience with lower total cost of mobility.

Shared mobility is poised for a 30.32% CAGR, driven by robo taxi economics that enable higher seat utilization compared to privately owned vehicles. Platform operators increasingly optimize routing to match peak demand with fleet availability, cutting vehicle-kilometer costs. Interestingly, data shows that lower evening fares encourage non-commute trips, expanding total urban mobility rather than cannibalizing existing transport.

By Component: Software Growth Outpaces Hardware Despite Lower Share

Hardware components dominated the autonomous vehicle market in 2024 with a 57.36% share, but the autonomous driving software segment is projected to grow faster at a 26.82% CAGR through 2030, as OEMs increasingly shift focus to over-the-air (OTA) feature updates and driving logic modules. The rise of AI-based perception and decision-making stacks is turning the software layer into a major revenue driver. Moreover, partnerships between automakers and cloud platforms are accelerating the rollout of real-time fleet management and safety updates, blurring the lines between mobility and digital services.

Even as sensor prices fall, innovation in perception algorithms drives recurring software-license streams, altering revenue recognition from up-front hardware sales to multi-year contracts. This shift encourages automotive suppliers to adopt DevOps practices common in the tech sector, signaling further cultural convergence between the two industries.

Geography Analysis

Asia-Pacific led the autonomous vehicle market in 2024 with a 46.52% share, driven largely by China’s expansive multi-city robo taxi deployments and widespread 5G infrastructure. Coordinated government support across ministries enables streamlined testing, insurance, and cybersecurity approvals, significantly reducing project timelines. An emerging trend is that second-tier cities are bypassing traditional public transport upgrades by adopting autonomous shuttles directly, signaling market diffusion beyond major urban hubs. Meanwhile, countries like Japan and Singapore leverage consortium-led models combining academic and autonomous industry expertise, allowing efficient R&D scaling despite smaller budgets.

The Middle East and Africa are the fastest-growing regions, projected to grow at a 28.11% CAGR from 2025 to 2030. National strategies, particularly in the United Arab Emirates, place autonomous vehicles at the heart of smart-city goals, with Dubai aiming for 25% of all trips to be autonomous by 2030. Purpose-built infrastructure with autonomous vehicle lanes gives the region an edge over retrofitted systems in legacy urban layouts. A surprising benefit is that the region’s clear-weather desert conditions deliver high-fidelity sensor data, accelerating vision system validation.

North America remains pivotal because of its deep capital markets and technology clusters, despite holding a smaller autonomous vehicle market share than Asia. Federal grants for 5G-V2X corridors and a vibrant startup pipeline sustain innovation momentum, even as fragmented state rules slow nationwide scaling. The presence of large ride-hailing platforms offers immediate commercial distribution once regulatory clarity emerges. An underlying shift is that trucking-focused states are coalescing around common guidelines, hinting at a bottom-up path to de facto national standards.

Competitive Landscape

The competitive landscape is led by a handful of scale players, most prominently Waymo, Tesla, and Baidu, each executing distinctive vertical-integration approaches. Waymo’s multi-city robo taxi service crossed 4 million paid rides in 2024, validating consumer-ready operations at fleet scale.[2]“Waymo One Surpasses 4 Million Rider Trips,” Waymo, blog.waymo.com Tesla’s on-vehicle, camera-first strategy continues to differentiate by relying on large-scale shadow data rather than expensive LiDAR arrays. A key inference is that the two divergent sensor philosophies will likely coexist, catering to different cost tolerances and redundancy expectations.

Strategic partnerships accelerate technology diffusion, as traditional automakers pair with chip vendors or mapping specialists to quickly close capability gaps. For instance, alliances between European truck manufacturers and the United States' autonomy software firms reveal that geographic expertise is becoming less relevant than complementary assets. The result is a cross-border blend of hardware manufacturing strength and Silicon Valley algorithmic leadership, which may raise antitrust scrutiny if market concentration intensifies.

White-space opportunities persist in niche segments such as airport shuttles and mining vehicles, where limited-access environments simplify deployment. Smaller specialists are therefore carving defensible positions by focusing on domain-specific software tuned to repeatable routes. Because these niches produce earlier positive cash flow, they may incubate future multipurpose autonomy platforms able to scale outward.

Autonomous Vehicle Industry Leaders

-

Waymo LLC

-

Tesla, Inc.

-

General Motors Co. (Cruise LLC)

-

Baidu Inc. (Apollo)

-

Volkswagen AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Waymo secured approval from the California Public Utilities Commission to expand its autonomous ride-hailing service across the wider San Francisco Bay Area. The decision follows the company’s March safety plan filing and signals regulatory confidence in existing operational safeguards.

- May 2025: Uber and WeRide announced plans to extend joint autonomous operations to 15 cities within two years. The expansion underlines rising strategic alignment between ride-hailing and dedicated AV software providers.

- January 2025: Amazon-owned Zoox started an Early Rider Program in Las Vegas to pave the way for a commercial robo taxi service later in the year. The initiative will deploy vehicles without manual controls in multiple U.S. cities.

Global Autonomous Vehicle Market Report Scope

The autonomous vehicle market report is segmented by Level of Automation (Level 1- Driver Assistance, Level 2 - Partial Automation, Level 3 - Conditional Automation, Level 4 - High Automation, and Level 5 - Full Automation), Vehicle Type (Passenger Cars and Commercial Vehicles), Propulsion Type (Internal Combustion Engine (ICE), Battery Electric Vehicles (BEV), and Hybrid Electric Vehicles (HEV)), Mobility Form (Personal Ownership and Shared Mobility), Component (Hardware (Sensors, Computing Platforms and Actuators and Control Systems), Software (Perception and Planning Suites, Mapping and Localization Engines, and Driver Monitoring and HMI), and Services (Integration and Validation and Remote Operation and Tele-operation)), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

| Level 1- Driver Assistance |

| Level 2 - Partial Automation |

| Level 3 - Conditional Automation |

| Level 4 - High Automation |

| Level 5 - Full Automation |

| Passenger Cars |

| Commercial Vehicles |

| Internal Combustion Engine (ICE) |

| Battery Electric Vehicles (BEV) |

| Hybrid Electric Vehicles (HEV) |

| Personal Ownership |

| Shared Mobility (Robo-Taxi, Shuttle) |

| Hardware | Sensors (LiDAR, RADAR, Cameras, Ultrasonic, IMU) |

| Computing Platforms (SoCs, GPUs) | |

| Actuators and Control Systems | |

| Software | Perception and Planning Suites |

| Mapping and Localization Engines | |

| Driver Monitoring and HMI | |

| Services | Integration and Validation |

| Remote Operation and Tele-operation |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Egypt | |

| United Arab Emirates | |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East and Africa |

| By Level of Automation | Level 1- Driver Assistance | |

| Level 2 - Partial Automation | ||

| Level 3 - Conditional Automation | ||

| Level 4 - High Automation | ||

| Level 5 - Full Automation | ||

| By Vehicle Type | Passenger Cars | |

| Commercial Vehicles | ||

| By Propulsion Type | Internal Combustion Engine (ICE) | |

| Battery Electric Vehicles (BEV) | ||

| Hybrid Electric Vehicles (HEV) | ||

| By Mobility Form | Personal Ownership | |

| Shared Mobility (Robo-Taxi, Shuttle) | ||

| By Component | Hardware | Sensors (LiDAR, RADAR, Cameras, Ultrasonic, IMU) |

| Computing Platforms (SoCs, GPUs) | ||

| Actuators and Control Systems | ||

| Software | Perception and Planning Suites | |

| Mapping and Localization Engines | ||

| Driver Monitoring and HMI | ||

| Services | Integration and Validation | |

| Remote Operation and Tele-operation | ||

| Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Egypt | ||

| United Arab Emirates | ||

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the autonomous vehicle market size in 2025?

The autonomous vehicle market size is valued at USD 42.87 billion.

How fast is the autonomous vehicle market expected to grow?

Between 2025 and 2030, the autonomous vehicle market is forecast to grow at a 23.27% CAGR.

Which region holds the largest autonomous vehicle market share?

Asia-Pacific commanded 46.52% of the autonomous vehicle market share owing to supportive regulations and large-scale robotaxi deployments.

Why are commercial vehicles important for autonomous adoption?

Commercial fleets face acute driver shortages and benefit financially from continuous vehicle utilization, making them early adopters of autonomous technology.

Page last updated on: