Automotive Steering Wheel Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 36.41 Billion |

| Market Size (2031) | USD 44.47 Billion |

| Growth Rate (2026 - 2031) | 4.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Steering Wheel Market Analysis by Mordor Intelligence

The automotive steering wheel market size is expected to grow from USD 34.98 billion in 2025 to USD 36.41 billion in 2026 and is forecast to reach USD 44.47 billion by 2031 at 4.08% CAGR over 2026-2031. Growth is propelled by electrification, Level 3+ autonomous vehicle development, and expanding safety mandates pushing airbag integration and biometric driver-monitoring into the wheel. Electric Power Steering (EPS) remains the volume backbone, yet steer-by-wire (SbW) platforms are scaling fastest as premium EV programs validate column-less cockpits. Lightweight metals and natural-fiber composites limit mass while supporting OEM sustainability targets. Asia-Pacific commands production share thanks to China’s battery-electric boom and semiconductor localisation, whereas North America and Europe pull demand for premium interfaces with haptic controls. Competitive intensity is moderate: legacy leaders Autoliv, ZF Friedrichshafen, and Joyson extend vertical integration. However, software-defined vehicle specialists and chipmakers are carving out white-space in steering control and cybersecurity stacks.

Key Report Takeaways

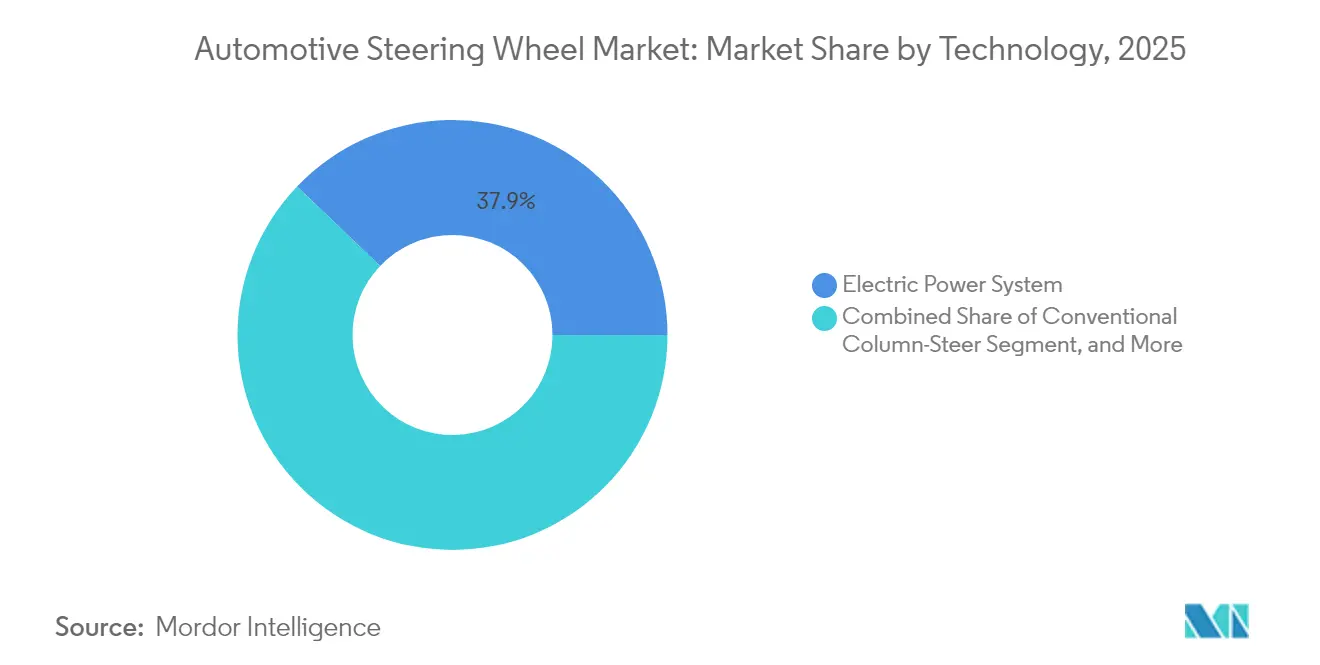

- By technology, electric power steering held 37.86% of the automotive steering wheel market share in 2025, while steer-by-wire is projected to expand at a 7.66% CAGR by 2031.

- By material, aluminium captured 37.12% of the automotive steering wheel market revenue share in 2025; natural-fiber composites are advancing at a 7.42% CAGR through 2031.

- By vehicle type, passenger cars accounted for 75.05% of the automotive steering wheel market size in 2025; light commercial vehicles are poised for an 8.06% CAGR to 2031.

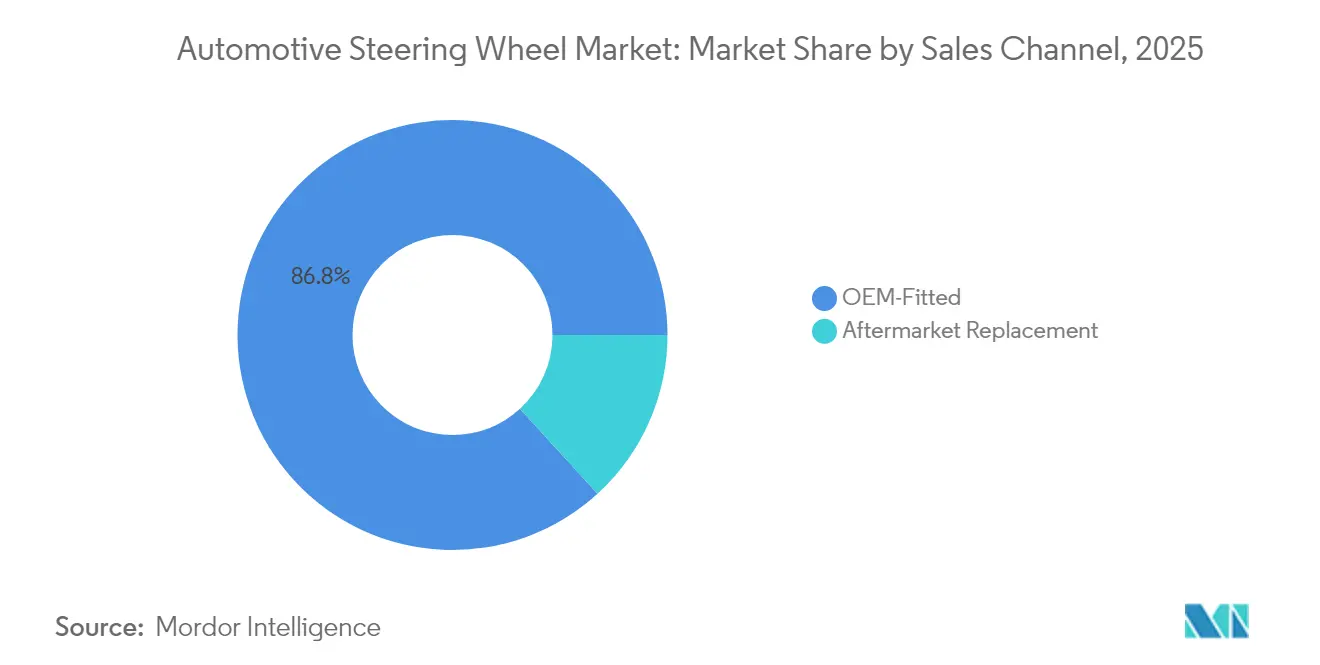

- By sales channel, OEM-fitted wheels dominated with 86.78% of the automotive steering wheel market in 2025, whereas the aftermarket is forecast to climb at 7.94% CAGR between 2026-2031.

- By propulsion, internal-combustion engines still represented 73.96% of the automotive steering wheel market 2025 demand, yet battery-electric models are growing at 9.88% CAGR toward 2031.

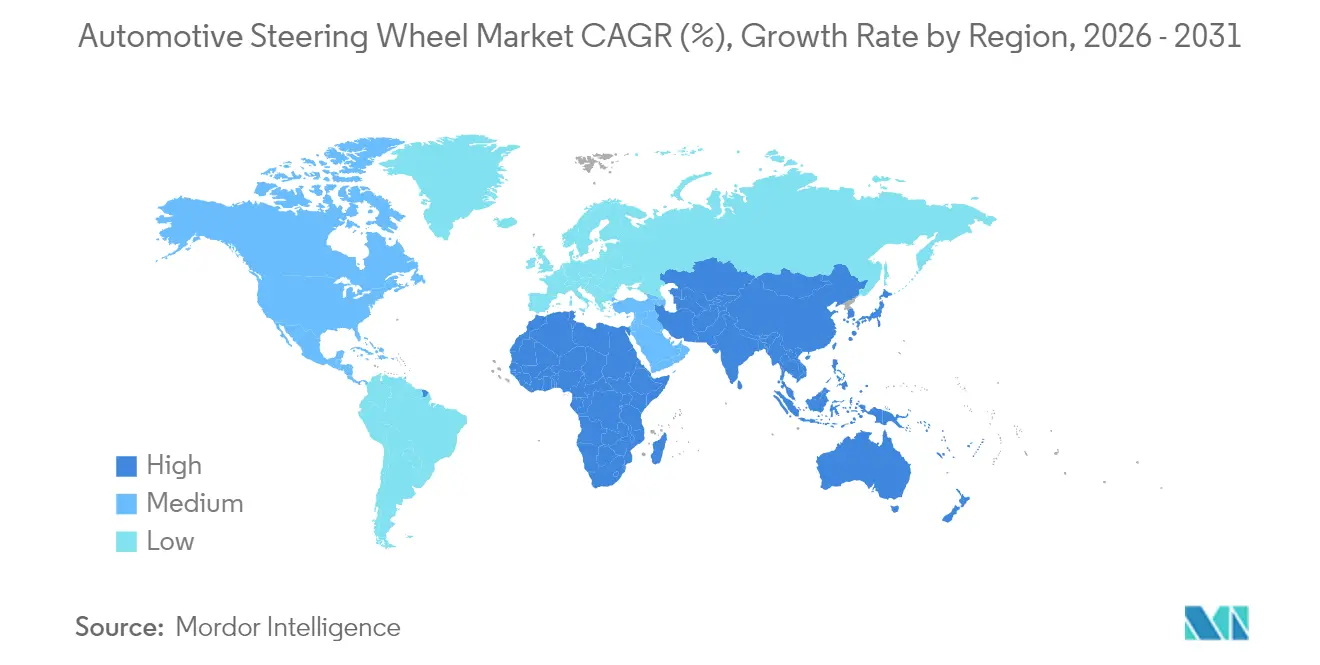

- By geography, Asia-Pacific led with 48.21% of the automotive steering wheel market revenue share in 2025, and is projected to post the fastest 6.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Steering Wheel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Adoption of Steer-By-Wire (SBW) Platforms | +1.8% | Global, with early gains in China, Europe | Medium term (2-4 years) |

| Mandatory Frontal-Airbag Integration In Steering Wheels | +0.9% | Global, EU GSR II compliance driving adoption | Short term (≤ 2 years) |

| Light-Weighting Push From EV OEMs | +1.2% | Global, concentrated in EV-leading markets | Medium term (2-4 years) |

| Premiumisation and In-Cabin UX Upgrades | +0.7% | North America & EU, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Legislative Drive-Impairment Monitoring Via Wheel Sensors | +0.5% | North America, with EU following | Long term (≥ 4 years) |

| Demand For Stowable/Column-Less Cockpits In L3+ Vehicles | +0.3% | Premium segments globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Adoption of Steer-By-Wire (SBW) Platforms

Mercedes-Benz will roll out full SbW on the 2026 EQS, following NIO’s 2025 launch of the ET9 that features ZF’s column-less architecture. The technology removes mechanical links, enabling variable ratios and software-tuned feedback for urban manoeuvrability and high-speed stability. ZF has secured multi-OEM contracts that underpin a 7.90% CAGR for SbW hardware through 2030[1] “Steer-By-Wire Orders Accelerate,” ZF Press Office, zf.com. The shift allows software-defined chassis control while challenging traditional suppliers to build electronic and cybersecurity competencies. Early wins in China illustrate regulators’ willingness to homologate the architecture, accelerating global uptake.

Mandatory Frontal-Airbag Integration in Steering Wheels

EU General Safety Regulation II, effective July 2024, compels enhanced emergency braking and drowsiness-warning functions that re-shape steering design[2] “GSR II Safety Requirements,” Continental Automotive, continental.com. In the United States, NHTSA research into driver-impairment detection uses tactile sensors embedded in the rim under the DADSS program. ZF LIFETEC has engineered top-deployment airbags that blend aesthetics with crash performance, meeting stricter packaging limits. Convergence of mandates raises system complexity and integration cost but standardises global requirements, creating volume leverage for tier-ones.

Light-Weighting Push From EV OEMs

Aluminium use in EVs is 30% higher than in ICE vehicles, trimming steering-wheel rim mass by 40% versus steel[3]“Aluminum Use in EVs,” Constellium Technical Team, constellium.com. Secondary aluminium saves 95% of energy, supporting cost and ESG targets. Natural-fibre composites, led by hemp, are growing at 7.65% CAGR; Ford already applies bio-based fibres in 300 parts across its lineup. Strength-to-weight gains align with OEM decarbonisation, although moisture ingress and end-of-life sorting remain engineering hurdles.

Legislative Drive-Impairment Monitoring Via Wheel Sensors

The US Infrastructure Law calls for impaired-driver detection in new models, with steering-wheel touch sensors viewed as a primary path[4]“Driver Alcohol Detection System for Safety Update,” SAE International, sae.org. Joyson and Forciot are co-developing printed sensor foils that cheaply capture grip strength and biometrics. UN ECE’s new DCAS regulation for SAE L2 systems mandates grip monitoring, anchoring long-term demand for sensor-rich rims[5]“Driver Control Assistance Systems Regulation,” UNECE Secretariat, unece.org.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Aluminium and Magnesium Prices | -0.6% | Global, particularly affecting cost-sensitive segments | Short term (≤ 2 years) |

| Global SbW Homologation and Cybersecurity Compliance Lag | -0.8% | Global, with varying regulatory timelines | Medium term (2-4 years) |

| Chip-Level Shortages For Haptic/Driver-Sense Modules | -0.7% | Global, acute in semiconductor-dependent regions | Short term (≤ 2 years) |

| Share-Shift Risk From Joystick/Voice HMI In Robo-Taxis | -0.4% | Urban centers in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Aluminum and Magnesium Prices

Spot prices for aluminium and magnesium have swung more than 20% in 2024-2025, squeezing margins on lightweight rims and spokes. Suppliers hedge through long-term supply contracts and alloy substitution, yet cost spikes deter adoption in cost-sensitive segments. OEMs explore recycled feedstock to offset volatility, but tier-two casting shops remain exposed to raw-material risk.

Global SbW Homologation and Cyber-Security Compliance Lag

The universal rollout of SbW (Safety by Wire) technology faces challenges due to the need for stringent ASIL-D redundancy, secure boot mechanism implementations, and compliance with over-the-air (OTA) update protocols, which vary significantly across regions. Furthermore, high certification costs place a substantial burden on smaller manufacturers, potentially limiting their competitiveness and ability to adopt these advancements, particularly outside premium market segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: EPS Dominates While SbW Scales Quickly

EPS controlled 37.86% of the automotive steering wheel market in 2025 as OEMs upgraded hydraulic systems to electric assist for efficiency and ADAS readiness. Conventional column-steer persists in markets prioritising low cost and mechanical simplicity. Steer-by-wire remains niche but is forecast at 7.66% CAGR to 2031 thanks to premium EV launches and autonomous drive programs.

The EPS-heavy portion of the steering wheel market size supports today’s electrification, while SbW prepares the ground for Level 3+ hands-free modes. ZF’s ET9 contract showcases commercial viability, delivering a variable ratio and software-defined feel without hydraulic fluid. In commercial trucks, EPS units provide up to 8,000 Nm torque yet trim energy draw compared with hydraulic pumps, underlining the efficiency case.

Second-order effects shape supplier positioning. EPS units rely on integrated torque sensors that feed lane-keep and auto-park functions, raising entry barriers for low-cost players. SbW architectures create fresh real estate for retractable columns, enabling living-room cabin concepts. Integration of high-bandwidth CAN-FD or Ethernet-based domain controllers further blurs lines between chassis and infotainment domains, offering white-space for software integrators rather than classic column specialists.

By Material Type: Natural Fibers Gain Momentum

Aluminium remained the leader with 37.12% of the automotive steering wheel market share in 2025, credited to 40% mass savings and endless recyclability. Steel endures for heavy-duty fleets where durability trumps weight. Magnesium rims serve high-performance niches but face processing and corrosion cost hurdles. Natural-fibre composites, notably hemp and flax, are set to grow 7.42% CAGR through 2031, propelled by automakers’ cradle-to-gate CO2 targets. Cupra’s ampliTex seatbacks cut 49% CO2 versus carbon fibre, signalling scalability for interior parts.

The steering wheel market benefits from bio-composite skins over aluminium skeletons, marrying structural integrity with tactile sustainability cues. Challenges persist: moisture absorption demands advanced resin systems, and bio-fibre parts cannot exceed 200 °C bake cycles common in EV paint lines. Nevertheless, European directives urging 25% recycled or bio-based content in interiors post-2028 strengthen the pull for natural fibres.

By Vehicle Type: Passenger Car Dominates while LCV Electrification Accelerates

Passenger cars contributed 75.05% to the automotive steering wheel market size in 2025. Heavy commercial vehicles keep a stable demand for robust wheel assemblies as fleet operators pursue operational uptime. Light commercial vehicles (LCVs) are the fastest-growing slice at 8.06% CAGR to 2031, fuelled by e-commerce delivery electrification. ZF’s EPS truck unit reduces maintenance and meets ADAS rollout, appealing to fleet total cost of ownership.

LCV growth reshapes specification, heated wheels, and capacitive touch sensors migrate from premium cars to delivery vans, where drivers spend extended shifts. Fleet managers prioritise energy efficiency gains from EPS plus regenerative braking harmony, reinforcing demand for integrated steering-brake control packages.

By Sales Channel: Aftermarket Sees Customization Upside

OEM-installed wheels owned 86.78% of the automotive steering wheel market share in 2025 due to mandatory safety validation of airbag modules and driver-monitoring electronics. Safety regulations restrict aftermarket freedom, yet replacement and customisation drive an 7.94% CAGR forecast for independent channels. Ageing vehicle parc in emerging economies and interest in sport-styled rims support volume. Indian suppliers aim to triple their exports as US tariffs squeeze Chinese shipments, catalysing capacity build-out.

Digital storefronts improve component traceability, while 3D-printed custom grips personalise rides within regulatory limits. However, advanced sensor integration complicates DIY installation, tilting aftermarket growth toward certified workshops.

By Propulsion Type: BEV Momentum Reshapes Specifications

ICE vehicles still held 73.96% of the automotive steering wheel market in 2025 demand, but their share erodes as battery-electric vehicles (BEVs) rise 9.88% CAGR to 2031. BEV wheels focus on mass reduction and thermal management to offset battery payload, increasing aluminium and bio-composite uptake. Software-centric E/E architectures create fertile ground for steer-by-wire adoption, which removes mechanical columns and complements the skateboard chassis. Hybrid vehicles serve as an interim bridge, demanding dual-voltage compatibility in torque sensors and heaters.

Beyond hardware, BEVs leverage over-the-air updates to refine steering feel post-sale, prompting suppliers to embed flashable micro-controllers in rim modules. Cyber-security stacks certified under UNECE R155 become the baseline, compelling steering ECUs to support encrypted diagnostics and secure boot.

Geography Analysis

Asia-Pacific led the automotive steering wheel market with 48.21% share in 2025 and is growing at 6.56% CAGR on the strength of China’s EV surge and policy-backed chip localisation. Beijing targets 25% local semiconductor content by 2025, anchoring supply for wheel-integrated sensors and ECUs. Large-scale production and cost efficiencies permit rapidly migrating premium features such as haptic feedback into mid-segment vehicles. However, export restrictions on rare-earth magnets have disrupted OEM production schedules, as seen in temporary shutdowns at Suzuki and Ford plants.

North America remains a technology adopter rather than a cost leader. US infrastructure legislation mandates driver-impairment detection, spurring demand for sensor-rich wheels, while Canadian and Mexican plants scale EPS output to serve Detroit Three EV programs. Nexteer’s new technical centre in Mexico adds 350 roles by 2026 to hone column-type EPS and SbW validation, exploiting near-shoring trends. Trade-policy uncertainty around potential US tariffs on Mexican assemblies could shift sourcing back to Asia despite freight premiums.

Europe balances premiumisation with strict safety mandates. EU GSR II and Euro NCAP 2026 physical-button requirements anchor demand for integrated wheel controls and grip sensors. Bosch’s Hungarian plant now produces EPS racks for regional OEMs, evidencing capacity expansion nearer to premium customers. On the supply side, German tier-ones push SbW validation through TÜV and KBA authorities, setting performance benchmarks that ripple through global homologation.

Emerging regions - South America, the Middle East, and Africa - show double-digit unit growth off low bases. India’s component makers pursue a USD 100 billion export ambition, with steering wheel assemblies viewed as tariff-friendly volume cargo. ZF Rane’s acquisition of TRW Sun Steering Wheels adds Gurugram and Pune plants, enhancing domestic content for localised airbags and sensors. Gulf states accelerate EV adoption for fleet decarbonisation, yet infrastructure gaps delay large-scale SbW rollout.

Competitive Landscape

The steering wheel market is moderately concentrated. Autoliv leads with integrated safety portfolios; Q1 2024 sales hit USD 2.6 billion, outpacing global vehicle production by 5 points[6]“Q1 2024 Results,” Autoliv Investor Relations, autoliv.com. Its BASF tie-up delivers recyclable polyurethane foam rims yet trims material costs amid inflation. The ZF–Foxconn joint venture, valued at EUR 1 billion, broadens access to consumer-electronics-grade PCBA manufacturing and accelerates vertical integration.

Joyson Electronics logged RMB 27.1 billion H1 2024 revenue, with 60% of new orders tied to new-energy vehicles and a four million-unit annual steering-wheel capacity at its Hefei hub. The firm’s folding hidden wheels for autonomous cabins illustrate rapid design iteration. Continental and Bosch remain strong in mechatronics, but software-first entrants such as HARMAN leverage AI-driven UX platforms; its 2025 CES unveil showcased cloud-based personalisation layered over central compute units.

Cross-disciplinary alliances intensify. Semiconductor giants co-develop secure microcontrollers targeting ISO 21434 compliance, while start-ups supply edge AI driver-monitoring algorithms licensed into wheel ECUs. The pivot toward cybersecurity and OTA support diminishes barriers between hardware tiers and software integrators, handing an advantage to suppliers that marry mechatronics with cloud expertise.

Automotive Steering Wheel Industry Leaders

Autoliv Inc.

ZF Friedrichshafen AG

Joyson Safety Systems

TOYODA GOSEI CO., LTD.

Nexteer Automotive Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Nexteer Automotive introduced its High-Output Column-Assist Electric Power Steering (HO CEPS). This new addition enhances Nexteer's leading steering portfolio and offers OEMs exceptional flexibility.

- February 2025: ZF started series production of steer-by-wire systems for the NIO ET9, the market’s first full-SbW deployment. These systems enable variable ratio control without mechanical linkage.

- January 2025: ZF booked brake-by-wire contracts for nearly 5 million vehicles, bundling electro-mechanical braking with electric recirculating ball steering gear valued at USD 2 billion.

Global Automotive Steering Wheel Market Report Scope

A steering wheel and the mechanism it is connected to are principally responsible for controlling a vehicle's direction. It converts the driver's rotational commands into swiveling motions of the car's front wheels. The steering system's joints and hydraulic lines allow the driver's movement to eventually reach the tires as it contacts the road.

The automotive steering wheel market report has been segmented by technology type, vehicle type, material type, sales channel, and geography. By technology type (conventional and control embedded), material type (aluminum, steel, magnesium, and others), vehicle type (passenger cars and commercial vehicles), sales channel (OEMs and aftermarket), and geography (North America, Europe, Asia-Pacific, South America, and Middle-East and Africa).

The report offers market size and forecast for Automotive Steering Wheel Market in value (USD) for all the above segments.

| Conventional Column-Steer |

| Electric Power-Assist (EPS) |

| Steer-by-Wire (SbW) |

| Aluminium Rim |

| Magnesium Rim |

| Steel Rim |

| Natural-fibre Composite Rim |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Bus and Coahes |

| OEM Fitted |

| Aftermarket Replacement |

| Internal-Combustion Engine |

| Battery-Electric Vehicle |

| Hybrid Electric Vehicle |

| Plug-In Hybrid Electric Vehicles |

| Fuel Cell Electric Vehicles |

| Alternative Fuels |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Philippines | |

| Indonesia | |

| Vietnam | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Technology | Conventional Column-Steer | |

| Electric Power-Assist (EPS) | ||

| Steer-by-Wire (SbW) | ||

| By Material Type | Aluminium Rim | |

| Magnesium Rim | ||

| Steel Rim | ||

| Natural-fibre Composite Rim | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Heavy Commercial Vehicles | ||

| Bus and Coahes | ||

| By Sales Channel | OEM Fitted | |

| Aftermarket Replacement | ||

| By Propulsion Type | Internal-Combustion Engine | |

| Battery-Electric Vehicle | ||

| Hybrid Electric Vehicle | ||

| Plug-In Hybrid Electric Vehicles | ||

| Fuel Cell Electric Vehicles | ||

| Alternative Fuels | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Philippines | ||

| Indonesia | ||

| Vietnam | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the steering wheel market?

The steering wheel market was valued at USD 36.41 billion in 2026 and is projected to reach USD 44.47 billion by 2031.

Which technology segment is growing fastest?

Steer-by-wire systems are growing at 7.66% CAGR through 2031 as premium EVs and autonomous vehicles adopt column-less architectures.

Why does Asia-Pacific dominate steering wheel production?

Asia-Pacific holds 48.21% share thanks to China’s EV scale, semiconductor localization goals and well-established tier-one supply chains.

What regulations are shaping future steering wheels?

EU GSR II, US impaired-driver legislation and UNECE’s DCAS rules mandate airbags and driver-monitoring sensors, pushing electronic integration into the wheel.

Is the aftermarket opportunity significant?

Yes, despite OEM dominance, the aftermarket is set to expand at 7.94% CAGR due to ageing fleets and customization demand, especially in emerging markets.

Page last updated on: