Automotive Exhaust System Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

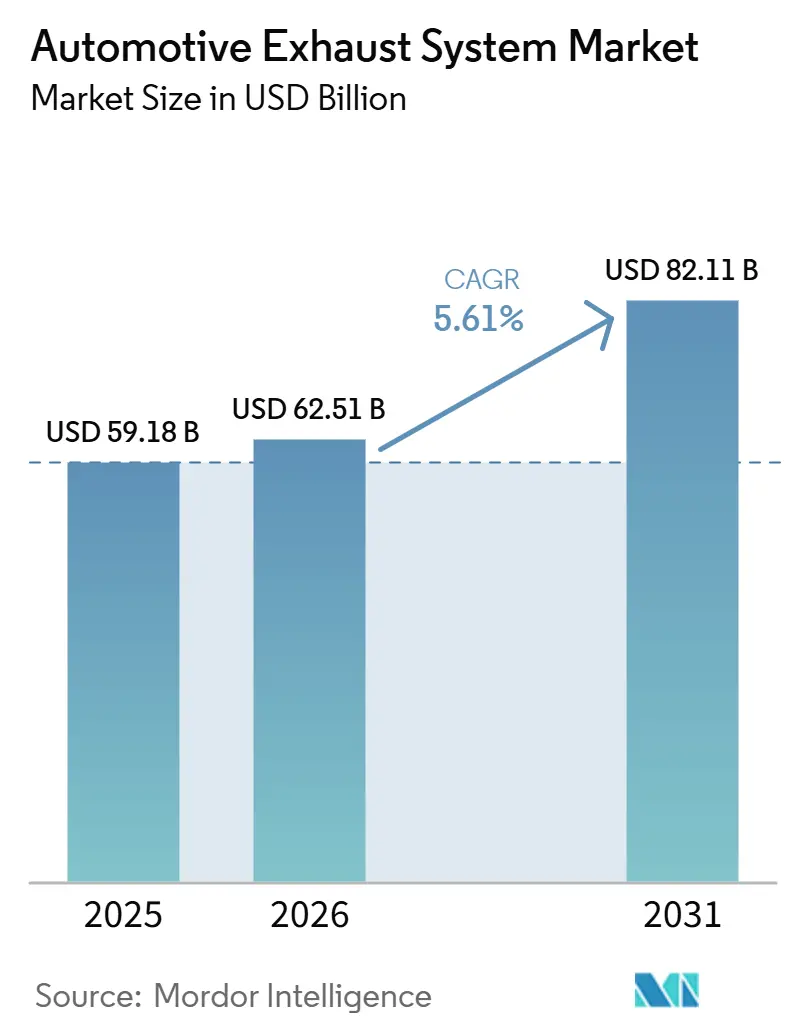

| Market Size (2026) | USD 62.51 Billion |

| Market Size (2031) | USD 82.11 Billion |

| Growth Rate (2026 - 2031) | 5.61% CAGR |

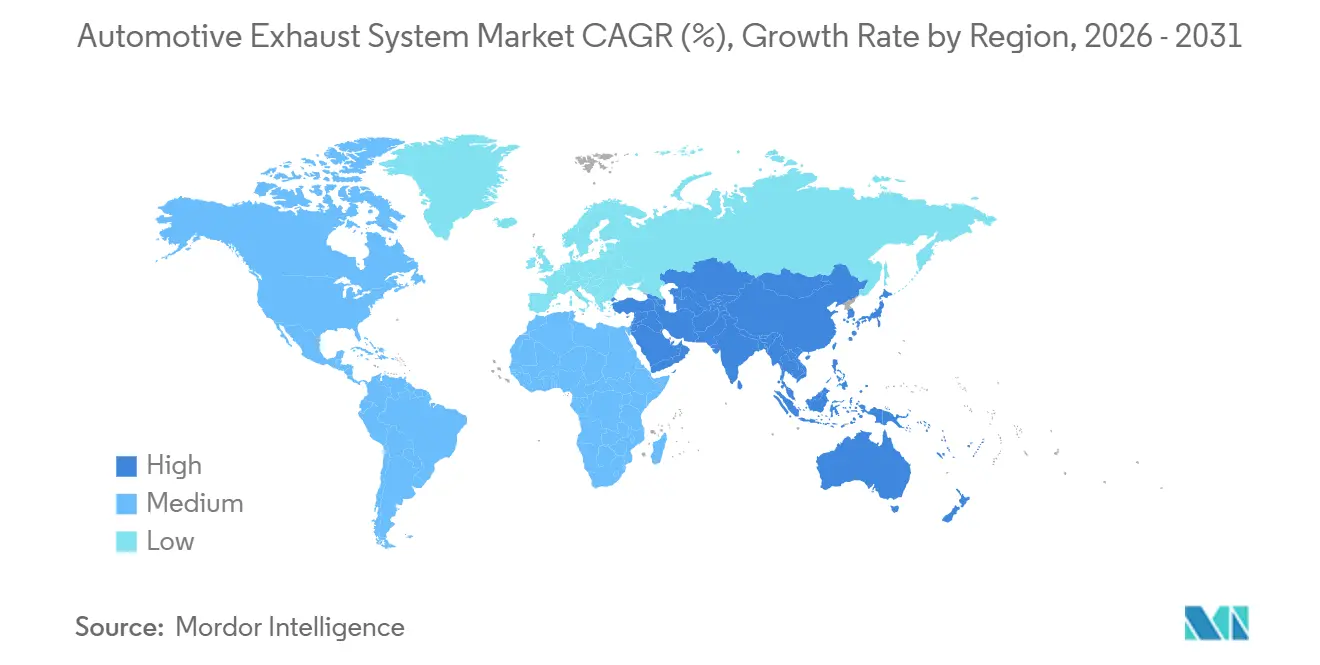

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

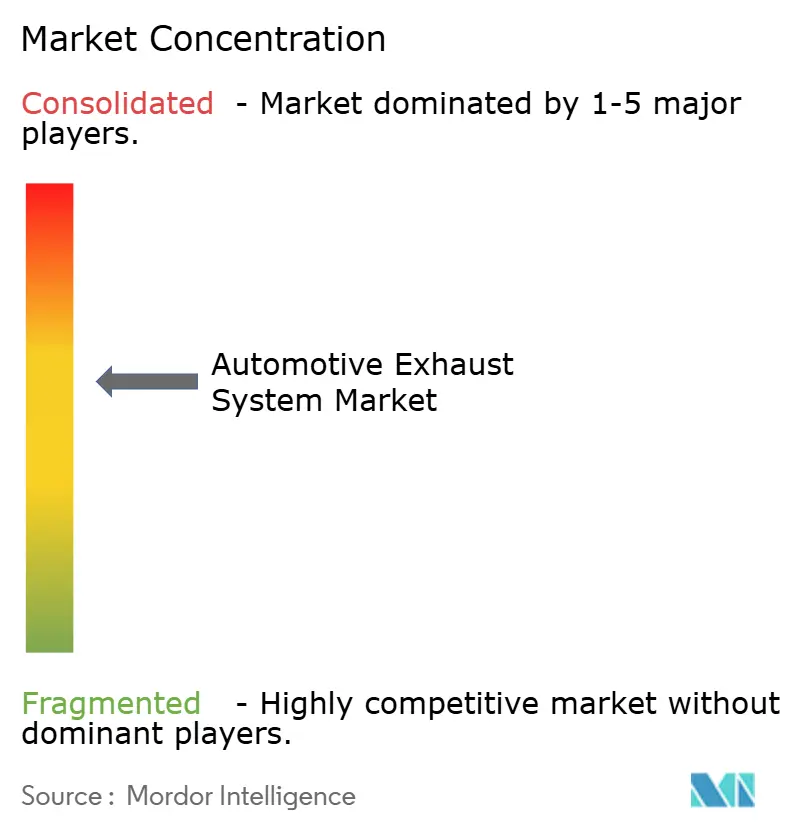

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Exhaust System Market Analysis by Mordor Intelligence

The Automotive Exhaust Systems Market size is expected to grow from USD 59.18 billion in 2025 to USD 62.51 billion in 2025 and is forecast to reach USD 82.11 billion by 2031 at 5.61% CAGR over 2025-2031. In Europe, China, India, and North America, heightened regulatory scrutiny is reshaping component architecture. This scrutiny is accelerating the shift toward high-efficiency catalytic converters, gasoline particulate filters, and wideband oxygen sensors. Concurrently, OEM cost-reduction mandates are guiding suppliers toward modular stainless-steel and titanium solutions. These solutions not only meet Euro 7 acoustic caps but also maintain durability. While rapid electrification poses challenges, the growth of hybrids and the expansion of low-emission zones bolster the near-term demand for Euro 7-ready systems. As a result, suppliers are diversifying their portfolios to include waste-heat recovery and battery-thermal solutions. They're also geographically rebalancing towards the Asia-Pacific region, which is expected to contribute significantly to future revenue. Competitive intensity is on the rise. Incumbent Tier 1s are divesting from low-margin diesel assets, while niche aftermarket players are leveraging titanium lightweighting and active valves to uphold price premiums.

Key Report Takeaways

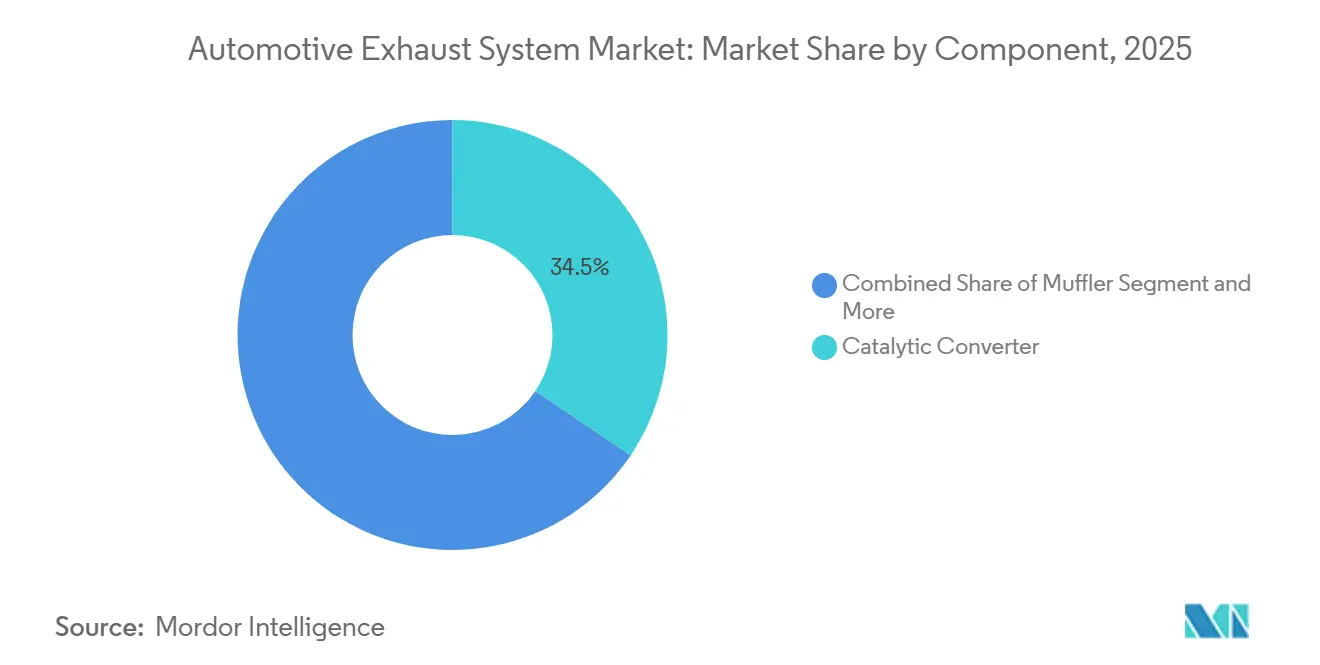

- By component, catalytic converters commanded 34.46% of the automotive exhaust systems market share in 2025, and oxygen sensors are projected to expand at a 5.63% CAGR between 2026 and 2031, the fastest pace among components.

- By fuel type, gasoline vehicles led with 58.71% revenue share in 2025, whereas alternate-fuel vehicles are forecast to grow at a 5.73% CAGR through 2031.

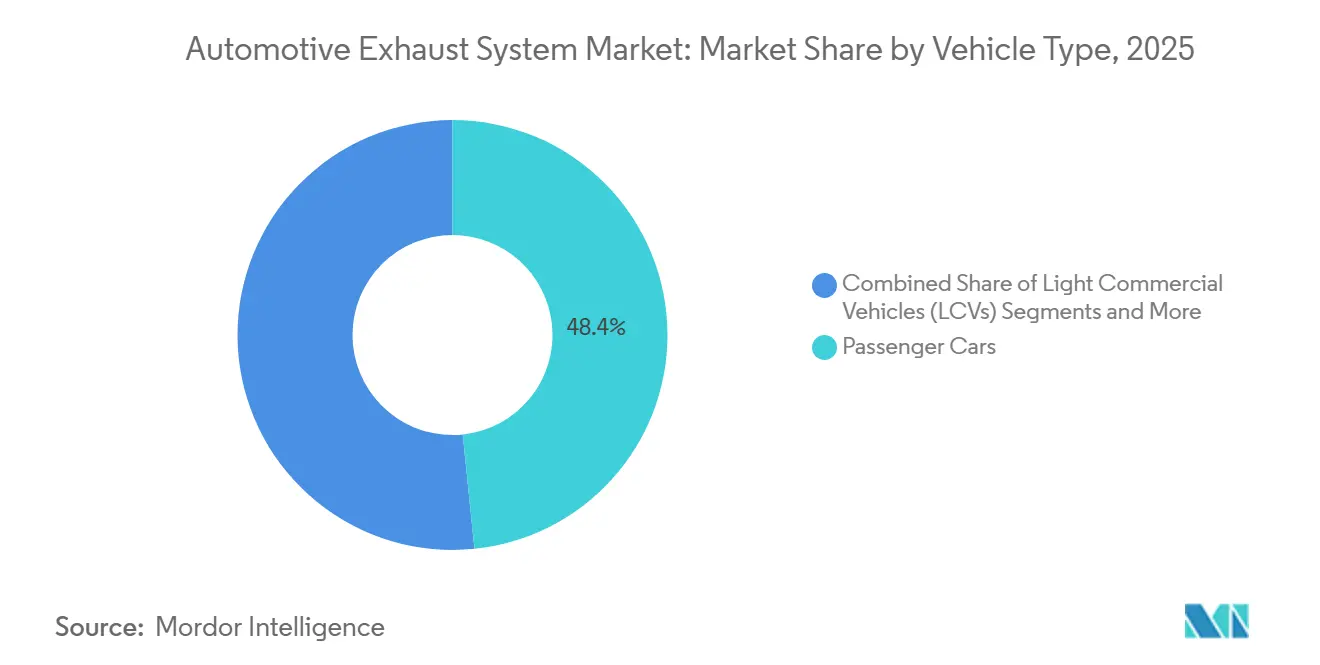

- By vehicle type, passenger cars accounted for 48.37% of the automotive exhaust systems market size in 2025, yet off-highway equipment is advancing at a 5.76% CAGR to 2031.

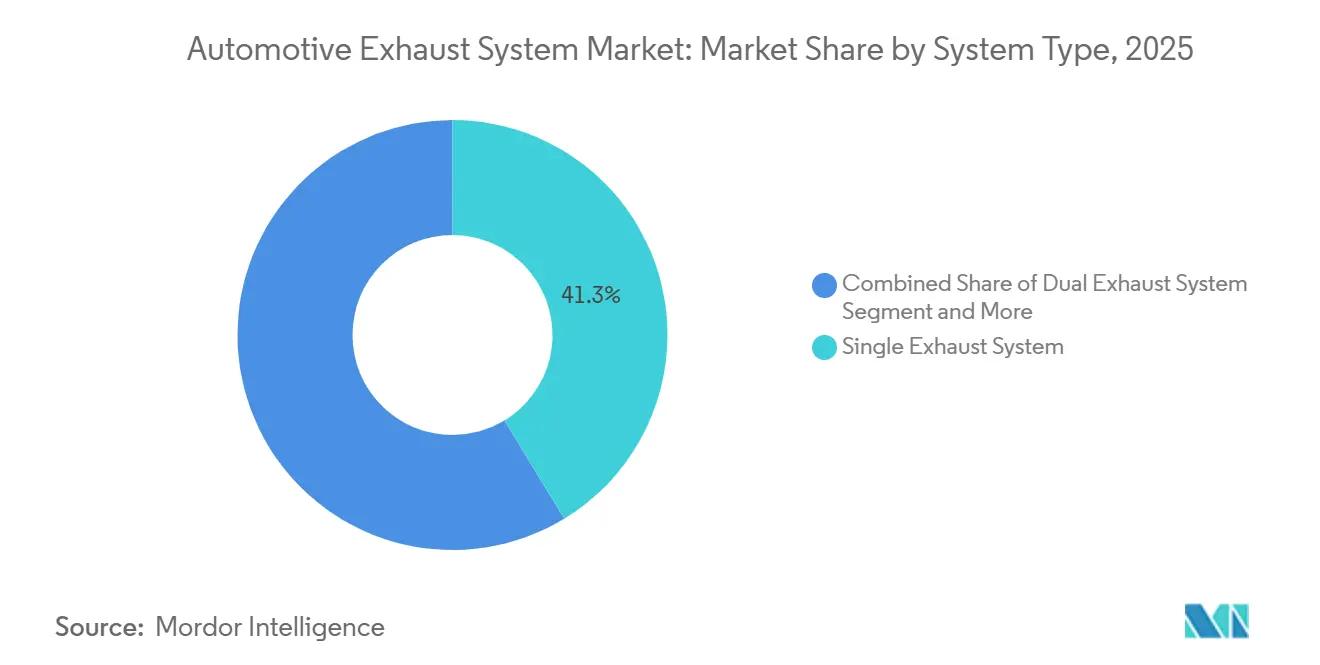

- By system type, single exhaust systems represented 41.25% of 2025 revenue, while header systems will expand at a 5.66% CAGR during 2026-2031.

- By sales channel, the OEM segment held 73.37% of the automotive exhaust systems market revenue in 2025, whereas the aftermarket is projected to grow the fastest at a 5.68% CAGR between 2026 and 2031.

- By geography, Asia-Pacific accounted for 36.75% of 2025 revenue and is forecast to expand at a 5.71% CAGR through 2031, the quickest rate among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Exhaust System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Euro 7 / China VII Emission Norms | +1.2% | Europe, China, with spillover to India (BS VII) and Southeast Asia | Medium term (2-4 years) |

| Rapid Growth in Turbo-Gasoline Passenger Cars | +0.9% | Global, with concentration in Europe, North America, and China | Short term (≤ 2 years) |

| Urban Low-Emission Zones (LEZ) Expansion | +0.7% | Europe (>500 LEZs by 2025), Asia (Bangkok, Hanoi pilot zones) | Short term (≤ 2 years) |

| OEM Shift to Lightweight Stainless and Titanium Alloys | +0.6% | North America, Europe, Japan (premium and performance segments) | Long term (≥ 4 years) |

| Rising Demand for Aftermarket Performance Kits | +0.5% | North America, Europe (enthusiast and tuner markets) | Medium term (2-4 years) |

| Heat-Energy Recovery Integration with Hybrids | +0.4% | Global, led by Japan, Europe, and China hybrid markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Euro 7 / China VII Emission Norms

Starting in mid-2027, Euro 7 will enforce light-duty regulations, followed by heavy-duty rules in mid-2029. These regulations introduce the PN10 measurement, targeting particles as small as nanometer-scale sizes. Additionally, they mandate continuous on-board monitoring. As a result, catalytic converters and particulate filters must now operate efficiently in a wide range of ambient conditions. Meanwhile, China's "China VII" standards, anticipated in the near future and set for a phased rollout over several years, aim to significantly tighten NOx limits. This shift is nudging OEMs towards adopting dual-SCR layouts and integrating multi-gas oxygen sensors[1]“Advanced Oxygen Sensors,” China Ministry of Ecology and Environment, mee.gov.cn.

Rapid Growth in Turbo-Gasoline Passenger Cars

In recent years, a significant majority of vehicles with combustion engines have been equipped with turbocharged direct-injection gasoline engines. These engines, with their heightened exhaust enthalpy, necessitate the use of stainless manifolds, ceramic coatings, and catalysts that activate in a very short time. Recently, Futaba commenced mass production of stainless manifolds specifically for Toyota and Lexus. Concurrently, NGK secured a contract to supply cordierite Gasoline Particulate Filters (GPF) in India, aligning with the country's upcoming emission regulations[2]“VI Stage 3 transition and future BS VII requirements,” NGK Insulators, ngk.co.jp. Additionally, wideband lambda sensors, now standard for transient air-fuel control, can withstand extremely high temperatures.

Urban Low-Emission Zones Expansion

Europe is set to establish numerous Low Emission Zones (LEZs) in the near future, while pilot programs in Bangkok and Hanoi are taking shape in Asia. These initiatives are hastening the retirement of older vehicles that do not meet current emission standards. As a result, there's a growing demand for retrofit SCR-on-filter solutions, notably from industry players like Tenneco and Eberspächer. Meanwhile, Oxford's proposed zero-emission zone for the long term hints at a potential decline in vehicle volumes over time. However, opportunities for retrofitting remain robust during this transitional phase.

OEM Shift to Lightweight Stainless & Titanium Alloys

By utilizing stainless steel 409/304 and titanium, system mass is significantly reduced, aiding OEMs in achieving their fleet-CO₂ targets. Akrapovič offers titanium cat-back kits for Lamborghini and Ferrari, achieving notable weight reductions, but at a considerable premium. With battery demand driving an increase in Class 1 nickel usage, suppliers are investing in low-nickel ferritic R&D. Futaba has significantly increased its alloy R&D investments over recent years. However, the company grapples with Euro 7 acoustic regulations, necessitating additional resonators to stay within the required sound limits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating BEV Power-Train Penetration | -1.8% | Global, led by China (50% NEV share in 2025), Europe, and California | Long term (≥ 4 years) |

| Raw-Material Price Volatility | -0.6% | Global, with acute exposure in stainless-steel supply chains | Medium term (2-4 years) |

| Catalytic-Metals Theft Risk | -0.3% | North America, Europe (declining but residual insurance and replacement costs) | Short term (≤ 2 years) |

| Euro-7 Acoustic Caps Limiting Sport Exhausts | -0.2% | Europe, with spillover to markets adopting Euro 7-equivalent noise standards | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating BEV Power-Train Penetration

In recent years, battery electric vehicles (BEVs) have gained significant traction in global light-vehicle sales, with China leading the market in new-energy vehicle adoption. While demand for BEVs in the U.S. experienced a slight decline following the expiration of a federal tax credit, California remains committed to its ambitious zero-tailpipe emissions target for the future. Suppliers, such as Futaba, are anticipating a substantial revenue shortfall in the coming years. In response, they are shifting their investments towards battery cooling plates and thermal modules for electric vehicles.

Raw-Material Price Volatility (Ni, Mo)

In the forecast period, surcharges for stainless steel experienced a significant increase on a monthly basis, driven by tightening Class 1 nickel supplies due to battery growth. While ferritic and 200-series alloys are becoming more popular, the concentration of molybdenum supply in China introduces geopolitical risks. Magna's filings during this period highlighted an incomplete cost pass-through, prompting the company to pursue vertical recycling and selectively substitute with aluminum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Catalysts and Sensors Drive Compliance

In 2025, catalytic converters accounted for 34.46% of total revenue, highlighting their dominance in emissions control. Driven by Euro 7 and China VII mandates emphasizing continuous lambda and NOx monitoring, oxygen sensors are projected to spearhead growth with a 5.63% CAGR. Bosch's wideband units, designed to endure extreme temperatures, achieve ignition in mere seconds. As dual-SCR layouts expand their sensing points, the demand for oxygen sensors in automotive exhaust systems is on a steady rise. Stricter limits on particulate numbers are paving the way for wider adoption of gasoline particulate filters in turbo-gasoline fleets. While mufflers and pipes trend towards commoditization, premium brands are distinguishing themselves with titanium tailpipes.

Stainless manifolds are now taking the place of cast iron to meet the thermal demands of turbo-gasoline. In a significant development, Futaba's latest launches for Toyota and Lexus are realizing notable weight reductions per vehicle. Although modular mufflers under development promise tooling savings, their durability remains unproven. Tailpipes, often viewed as low-value, are being upgraded to titanium for supercar trims, commanding impressive premiums. With a regulatory shift towards real-time compliance, catalysts and sensors stand to gain added value, while stamped components face shrinking margins.

By Fuel Type: Gasoline Dominance, Alternate Fuels Rising

Gasoline vehicles delivered 58.71% of 2025 revenue, aided by 70% turbo-DI adoption. Mandatory gasoline particulate filters reinforce catalyst pull-through. Alternate fuels—CNG, LPG, and biomethane—will post the highest CAGR of 5.73%. India's CNG fleet is experiencing significant annual growth, driving the market forward. Key enablers include three-way catalysts fine-tuned for methane oxidation and adaptive lambda sensors.

While diesel's share in the automotive exhaust systems market is declining due to LEZ bans, it still holds a notable position in off-highway and heavy vehicles. These vehicles require advanced architectures, specifically the dual-dosing SCR combined with DPF. As hybrids are expected to account for a substantial portion of global sales in the near future, the relevance of combustion persists. This trend bolsters the demand for solutions that are low in heat mass and quick to light off, effectively mitigating cold-start spikes.

By Vehicle Type: Passenger Cars Lead, Off-Highway Accelerates

In 2025, passenger cars accounted for 48.37% of the market. Under PN10 regulations, close-coupled catalysts and GPFs are becoming the norm. Off-highway equipment is set to grow at a 5.76% CAGR, driven by the enforcement of DPF+SCR on 56-560 kW diesels under EU Stage V and US Tier 4 Final regulations. These regulations are expected to drive advancements in emission control technologies, further influencing market dynamics.

Equipment sales have surged recently, fueled by rising infrastructure investments in the Asia-Pacific. This uptick has spurred a demand for heavy stainless assemblies, prized for their high soot loading capacity. Commercial vans, medium trucks, and buses are increasingly opting for robust stainless systems, drawn by the promise of a lower total cost of ownership (TCO) and longer warranties. Additionally, the growing focus on sustainability and emission reduction is pushing manufacturers to innovate in material design and system efficiency. At the same time, pilot initiatives for CNG and hydrogen are unveiling fresh prospects for lean-burn catalyst formulations, which are expected to play a pivotal role in the transition to cleaner energy solutions.

By System Type: Single Exhaust Prevails, Headers Gain Traction

Front-drive packaging efficiency allowed single exhausts to capture 41.25% of the 2025 turnover. This dominance is attributed to their ability to optimize space and reduce complexity in front-drive vehicles. Meanwhile, header systems are set to grow at a 5.66% CAGR, driven by enthusiasts and OEM performance divisions favoring tubular stainless or titanium manifolds for enhanced flow efficiency. These materials not only improve performance but also offer durability and resistance to high temperatures. With Euro 7 noise regulations in play, there's a push to integrate resonators and active valves within header assemblies, increasing the content per vehicle and meeting stringent noise emission standards.

In the aftermarket, cat-back kits are flourishing, providing upgrades that ensure compliance without tampering with catalysts. These kits are particularly popular among consumers seeking performance enhancements while adhering to regulatory requirements. Futaba's modular concept aims for platform sharing to reduce tooling costs, but it faces challenges in acoustic tuning adjustments, which are critical for maintaining sound quality and performance consistency across different platforms.

By Sales Channel: OEM Dominance, Aftermarket Resilience

OEM supply captured 73.37% of 2025 revenue, anchored by long-term contracts and IATF 16949 compliance. Yet the aftermarket’s projected 5.68% CAGR reflects aging fleets and enthusiast demand. Euro 7 OBD functions will trim gray-market parts as fault codes emerge, advantaging branded suppliers with compliant sensor integration.

As catalytic-converter thefts decline, insurance companies feel some relief, yet the volume of replacements stays significant. Performance buyers continue to show price sensitivity, thanks to the substantial weight savings offered by titanium and stainless cat-back kits.

Geography Analysis

Asia-Pacific generated 36.75% of 2025 revenue and will post a 5.71% regional CAGR to 2031. China's significant light-vehicle production, India's growing adoption of CNG, and strong off-highway sales indicate positive near-term growth. The introduction of China's new emission standards will increase the need for catalysts and sensors, while India's upcoming regulations will expand pollutant coverage to include ammonia and nitrous oxide. Japan's strong presence in the hybrid vehicle market ensures steady demand for intermittent-duty exhaust systems. In South Korea, the alignment with European emission standards and the hybrid vehicle initiatives by Hyundai and Kia support regional market stability.

Europe continues to play a pivotal role in global sales. The forthcoming Euro 7 standards, set to roll out later this decade, will enforce stricter measures like advanced particulate counting and continuous monitoring. This shift is poised to boost the demand for cutting-edge catalysts and particulate filters. With the rise of numerous low-emission zones, there's a swift push to replace older vehicles, opening doors for retrofitting opportunities. While battery electric vehicles are on the rise, hybrids still hold a crucial position as manufacturers navigate challenges like range limitations and profitability. Germany's prominence is further highlighted by its hosting of major suppliers like Eberspächer, Benteler, and Faurecia, showcasing the region's robust integration capabilities.

North America stands out as a major revenue source, even as production sees a slight dip. Federal policy shifts have led to fluctuations in the demand for battery electric vehicles. Yet, California's steadfast zero-emission mandate charts a clear long-term course. Noteworthy investments, including Tenneco's valve production expansion in Mexico and Benteler's exhaust manufacturing upgrades in South Carolina, underscore manufacturers' dedication to internal combustion engine platforms. While there's been a decline in catalytic-converter thefts, the financial outlay on replacements remains significant.

Competitive Landscape

Faurecia, Tenneco, Eberspächer, and Benteler collectively hold a notable share of the global market, suggesting a moderate concentration. In a strategic pivot towards electrification and a focus on higher-margin modules, Faurecia has sold its commercial-vehicle exhaust plants to Cummins, aligning with its long-term IGNITE plan. This move reflects Faurecia's broader strategy to adapt to the evolving automotive landscape, where electrification and sustainability are becoming critical drivers of growth. Yutaka Giken's projected revenue decline highlights the risks of depending on a single OEM, particularly as Honda speeds up its electrification push. The company's reliance on Honda underscores the challenges faced by suppliers in diversifying their customer base amidst the industry's transition to electric vehicles. On a similar note, Futaba foresees a significant revenue decline from internal combustion engine (ICE) sales in the coming decade and is shifting its R&D focus to battery cooling plates. This strategic redirection indicates Futaba's proactive approach to align with the growing demand for electric vehicle components.

Driving technological advancements are innovations in catalyst chemistry and sensing. Umicore has unveiled a bi-metallic formulation to lessen platinum dependence, while Bosch has developed a triple-gas NOx sensor that adheres to the rigorous Euro 7 diagnostic standards. These advancements highlight the industry's commitment to meeting stringent environmental regulations while optimizing performance. Corning is advancing with its hierarchical-pore GPFs, tailored for superior filtration and reduced backpressure. Such innovations are critical in addressing the dual challenges of improving efficiency and reducing emissions.

Aftermarket specialists Akrapovič and Scorpion are adopting titanium lightweighting and active valves, aligning with Euro 7 noise regulations to safeguard their profit margins. These companies are leveraging advanced materials and technologies to maintain competitiveness in a highly regulated market. Established players are increasingly benefiting from challenges like the ISO 16183 test standards and WLTP Phase 3 durability benchmarks. With the capability to back global validation efforts, these incumbents are pivoting. As ICE volumes decline, they're strategically redirecting their focus to thermal management solutions for hybrids, fuel cells, and batteries. This shift underscores the industry's broader transition towards sustainable and energy-efficient technologies, ensuring long-term growth opportunities for market leaders.

Automotive Exhaust System Industry Leaders

Faurecia (FORVIA)

Tenneco

Eberspächer Group

Benteler International

Futaba Industrial

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: BorgWarner won wastegate gasoline turbocharger contracts for 1.0-liter engines destined for next-generation European and North American compact cars and hybrids, underscoring continuing ICE investment by global OEMs.

- July 2025: BorgWarner secured multi-year supply deals with a major North American OEM covering midsize and large SUV turbocharger platforms that integrate cast-in exhaust manifolds for tighter boost control.

Global Automotive Exhaust System Market Report Scope

The scope of the report includes Component (Exhaust Manifold and More), Fuel Type (Gasoline and More), Vehicle Type (Two-Wheeler and More), System Type (Single and More), Sales Channel (OEM and Aftermarket), and Geography.

| Exhaust Manifold |

| Muffler |

| Catalytic Converter |

| Exhaust Pipes |

| Oxygen Sensor |

| Tailpipe |

| Gasoline |

| Diesel |

| Alternate Fuels (Biofuels, CNG, LPG) |

| Two-Wheeler |

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Medium and Heavy Commercial Vehicles (HCVs) |

| Buses and Coaches |

| Off-highway Vehicles |

| Single Exhaust System |

| Dual Exhaust System |

| Cat-Back Exhaust System |

| Header Exhaust System |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Component | Exhaust Manifold | |

| Muffler | ||

| Catalytic Converter | ||

| Exhaust Pipes | ||

| Oxygen Sensor | ||

| Tailpipe | ||

| By Fuel Type | Gasoline | |

| Diesel | ||

| Alternate Fuels (Biofuels, CNG, LPG) | ||

| By Vehicle Type | Two-Wheeler | |

| Passenger Cars | ||

| Light Commercial Vehicles (LCVs) | ||

| Medium and Heavy Commercial Vehicles (HCVs) | ||

| Buses and Coaches | ||

| Off-highway Vehicles | ||

| By System Type | Single Exhaust System | |

| Dual Exhaust System | ||

| Cat-Back Exhaust System | ||

| Header Exhaust System | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big will the automotive exhaust systems market be by 2031?

The automotive exhaust systems market size is projected to reach USD 82.11 billion by 2031, expanding at a 5.61% CAGR from 2026 to 2031.

Which component category is growing the fastest through 2031?

Oxygen sensors are forecast to post the fastest 5.63% CAGR as Euro 7, and China VII requires continuous NOx and lambda monitoring.

What share of demand did catalytic converters capture in 2025?

Catalytic converters accounted for 34.46% of the automotive exhaust systems market share in 2025.

Which region offers the highest growth potential?

Asia-Pacific is set to record the highest 5.71% regional CAGR thanks to China’s tightening standards and India’s CNG fleet expansion.

How is electrification affecting exhaust suppliers?

Battery-electric penetration is a –1.8% drag on market CAGR, prompting suppliers like Futaba and Faurecia to pivot toward hybrid-optimized exhausts and battery-thermal products.

What is driving aftermarket demand despite tougher regulations?

Vehicle fleets aging beyond 12 years and enthusiast interest in performance upgrades sustain a 5.68% aftermarket CAGR, though Euro 7 OBD rules favor compliant premium brands.

Page last updated on: