Automotive Backup Camera Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 3.04 Billion |

| Market Size (2030) | USD 4.21 Billion |

| Growth Rate (2025 - 2030) | 6.73% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Backup Camera Market Analysis by Mordor Intelligence

The Automotive Backup Camera market size reached USD 3.04 billion in 2025 and is projected to advance to USD 4.21 billion by 2030, reflecting a 6.73% CAGR during the forecast period. The measured expansion signals a transition from purely regulatory fitment toward value-added feature competition, as automakers now package reversing cameras with surround-view arrays and automated-parking software rather than optioning them as standalone compliance items. This shift compresses average selling prices for single-function modules yet opens incremental revenue in software, display integration, and data-analytics services. North America remains the largest revenue contributor, while the Middle East and Africa record the fastest gains as Gulf Cooperation Council states adopt Euro-style rear-visibility mandates. Technology preferences are changing too: wired systems still dominate on cost, but wireless architectures advance rapidly on electric-vehicle platforms that favor modular cockpits[1]“Bosch Media Service,” Robert Bosch GmbH, bosch-presse.de. Meanwhile, Tier-1 suppliers look to soften hardware margin pressure by embedding perception software and enabling over-the-air feature activation.

Key Report Takeaways

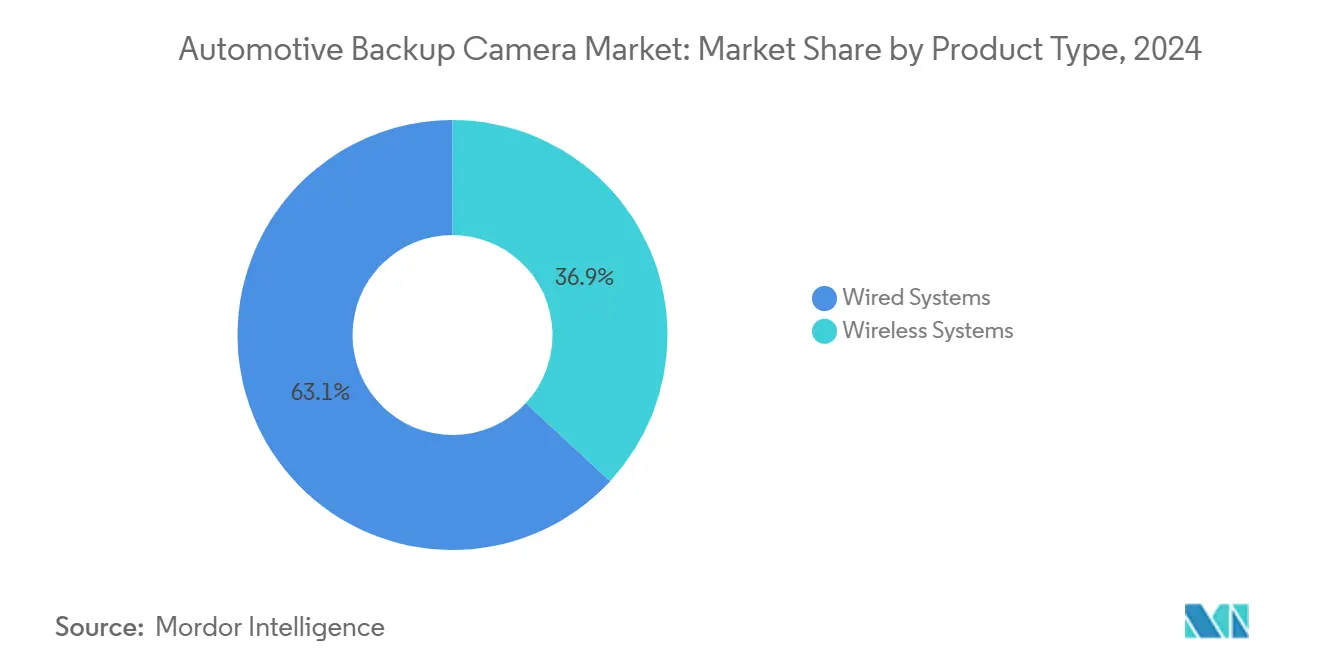

- By product type, wired systems led with 63.10% Automotive Backup Camera market share in 2024, whereas wireless systems are forecast to grow at a 9.80% CAGR through 2030, the fastest clip within the category.

- By vehicle type, passenger cars held 71.40% of volume in 2024, while heavy commercial vehicles are expanding at an 8.60% CAGR between 2025 and 2030, topping segment growth charts.

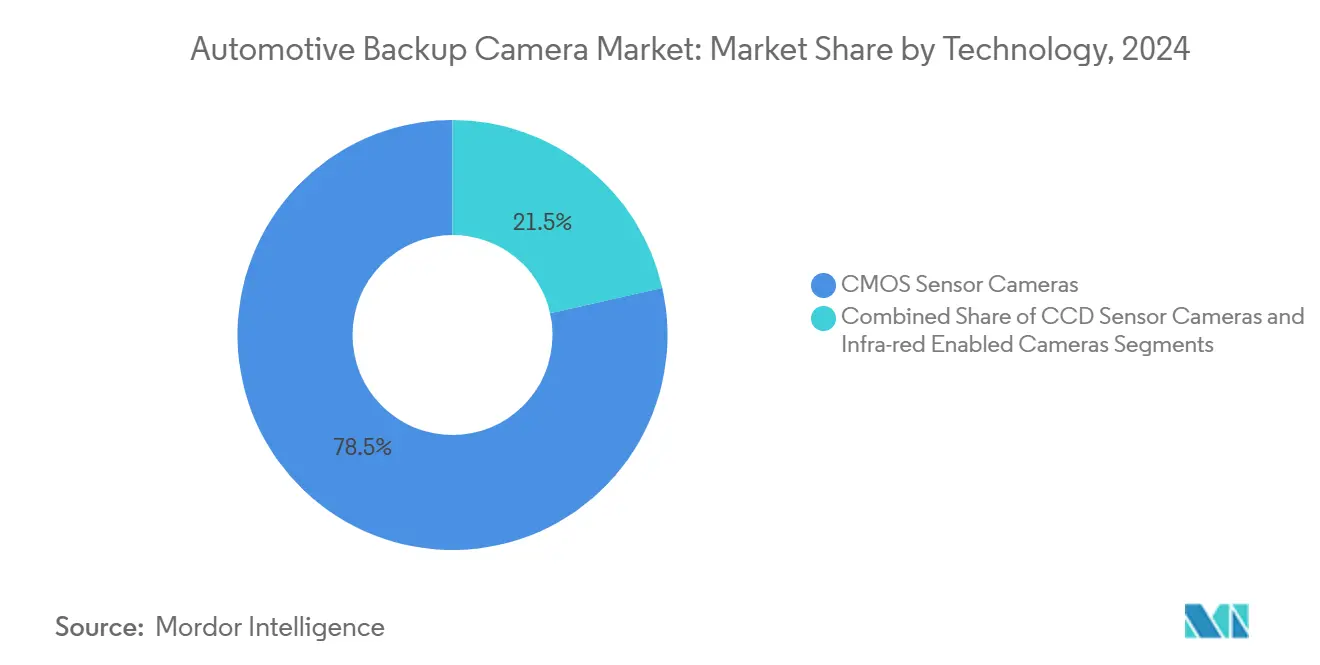

- By technology, CMOS sensors accounted for 78.50% of shipments in 2024; infrared and night-vision variants register the highest projected CAGR at 10.40% to 2030.

- By sales channel, OEM fit represented 68.90% of revenue in 2024, yet the aftermarket is advancing at an 11.30% CAGR on the back of an aging vehicle parc and insurance-premium incentives.

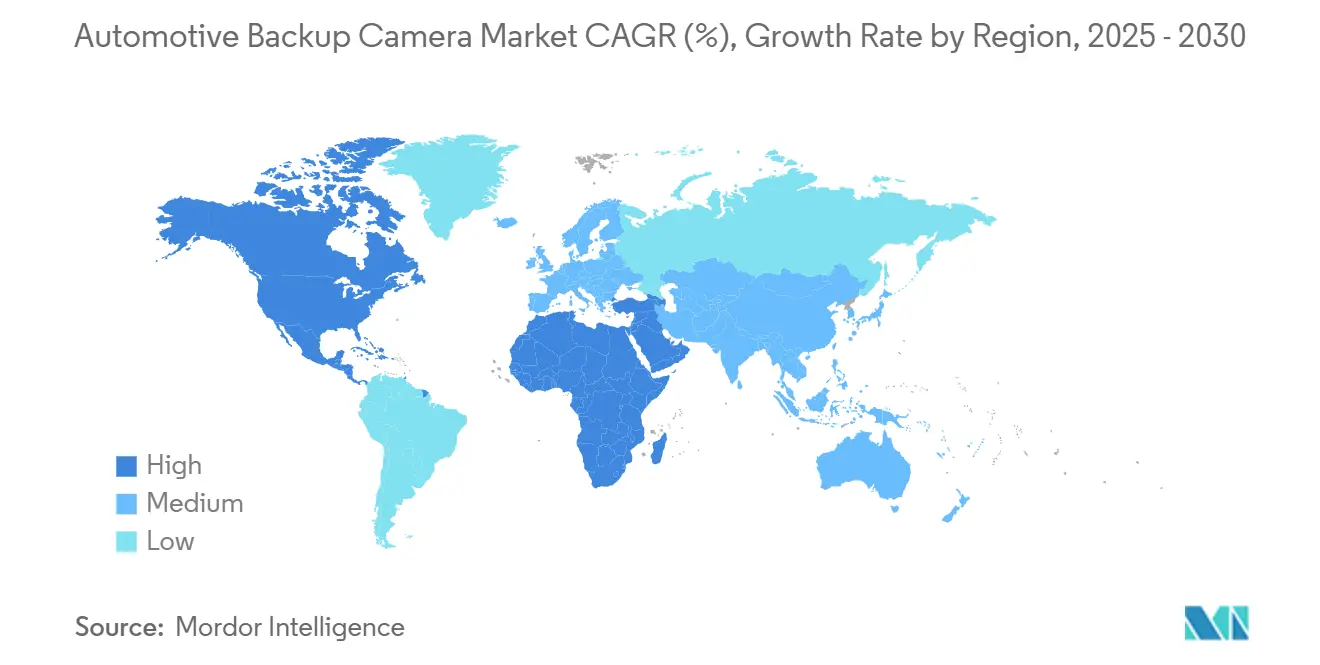

- By geography, North America contributed 34.20% of revenue during 2024; the Middle East and Africa bloc is expected to record a 7.90% CAGR, the swiftest regional pace.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Backup Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| U.S. FMVSS 111 compliance deadlines in LCVs | +0.8% | North America | Short term (≤ 2 years) |

| Euro NCAP star-rating weightage | +1.1% | Europe; spillover Middle East | Medium term (2-4 years) |

| Insurance-premium discounts | +0.9% | North America, EU | Medium term (2-4 years) |

| Rapid electrification with larger cockpits | +1.3% | China, EU, global | Long term (≥ 4 years) |

| Aftermarket digital-mirror retrofits | +0.7% | North America, Europe | Short term (≤ 2 years) |

| Falling CMOS sensor ASPs | +1.0% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

U.S. FMVSS 111 Compliance Deadlines in LCVs

Federal Motor Vehicle Safety Standard 111 enters its final phase-in for light commercial vans and chassis-cab trucks in 2026, triggering a second wave of OEM camera integration that features higher-resolution sensors and rugged housings, resulting in average selling prices that can increase by up to 20%. The regulation aligns with FMCSA rules that expand windshield-mount zones, allowing larger displays that enhance driver acceptance and reduce liability. The tailwind is temporary, but fleet retrofits of pre-2026 units extend demand as insurers reward compliant vehicles with premium reductions. Suppliers are expected to enjoy near-term margin buoyancy, although volumes are expected to plateau once the mandate achieves full coverage.

Euro NCAP Star-Rating Weightage for Reverse-Visibility Tech

Euro NCAP’s 2023 protocol assigns up to 10% of a vehicle’s safety score to reversing-detection performance, forcing automakers to certify sub-500-millisecond object detection at five-meter ranges[2]“Euro NCAP Assessment Protocols,” European New Car Assessment Programme, euroncap.com . High-dynamic-range imaging and edge-processing algorithms costing an extra USD 3–5 per module are now essential for 5-star ratings. Gulf Cooperation Council nations and South Korea intend to mirror the protocol by 2027, creating a de facto global benchmark. Suppliers incapable of meeting the latency threshold risk exclusion from premium programs despite hardware compliance with baseline rules.

Insurance-Premium Discounts Linked to Rear-Collision Reduction

North American and European insurers began offering 5–10% discounts in 2024 for vehicles equipped with backup cameras and rear automatic emergency braking after IIHS data showed 17% fewer backing crashes. Retrofit kits costing USD 300–500 deliver a two- to three-year payback for high-mileage fleets. Some carriers bundle discounts with telematics programs, transforming cameras into data sources for risk scoring. This evolution positions software and analytics, rather than hardware, as the long-run value driver.

Rapid Electrification Driving Larger Display-Enabled Cockpits

Battery-electric architectures liberate cabin space for 15-inch to 17-inch displays that integrate backup-camera feeds with infotainment, elevating cameras from compliance accessories to core UX elements. Automakers monetize the hardware through software-unlockable surround-view and 3-D guidance. Valeo’s shipment of 20 million camera systems with embedded Mobileye processors exemplifies how shared sensors underpin multiple ADAS functions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-vulnerability of connected camera ECUs | -0.6% | North America, EU, global | Medium term (2-4 years) |

| Margin squeeze from automaker cost-down | -0.9% | Global | Short term (≤ 2 years) |

| Fogging & low-temperature limitations | -0.4% | Northern Europe, Canada, northern U.S. | Long term (≥ 4 years) |

| Consumer privacy legislation (EU AI Act) | -0.5% | EU; spillover California and others | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyber-Vulnerability of Connected Camera ECUs

ISO/SAE 21434, contractual from 2024, mandates secure boot loaders and encrypted firmware, adding USD 2–4 per module and straining commodity-priced cameras. Upstream Security logged a 50% rise in vehicle cyber incidents in 2024, with cameras implicated in 8%. Suppliers unable to maintain cybersecurity management systems face exclusion from OEM programs.

Margin Squeeze from Automaker Cost-Down Mandates

OEMs demand 3–5% annual price reductions, compressing camera-module margins by 200–300 basis points and pushing suppliers to offshore assembly or exit the segment. Warranty costs for units failing after five-year freeze-thaw cycles aggravate the squeeze. Large suppliers cross-subsidize losses with higher-margin radar and lidar lines, widening the gap over independent specialists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wireless Gains Despite Wired Dominance

The Automotive Backup Camera market size for wired systems reached USD 1.92 billion in 2024, translating to a 63.10% share, yet wireless units post the fastest 9.80% CAGR as EV platforms eliminate heavy harnesses. OEM engineers resist architectural changes mid-cycle, cementing wired leadership through 2030. Nonetheless, aftermarket technicians value the 60% labor saving from wireless kits, driving adoption in retrofit fleets.

Wireless uptake accelerates as 5 GHz and 60 GHz links achieve sub-50-millisecond latency that meets Euro NCAP reversibility thresholds. Magna’s dual-mode Gen.5 camera illustrates supplier hedging, shipping the same hardware with wired or wireless interfaces[3]“Magna Thermal Camera Gen.5 Launch,” Magna International, magna.com . Competition will favor firms that flexibly support both architectures without fresh tooling.

By Vehicle Type: HCVs Accelerate as Passenger Cars Mature

Passenger cars commanded 71.40% of Automotive Backup Camera market volume in 2024, but HCVs expand 8.60% annually through 2030 as fleet insurers reward reduced backing collisions. Modules for Class 8 trucks cost 20–30% more owing to ruggedized housings and extended-temperature electronics.

The passenger-car segment, entering saturation in developed markets, sees pricing pressure as cameras commoditize into wider ADAS suites. Conversely, HCV penetration sits below 40%, providing runway for volume. Premium fleets also adopt infrared night-vision, where Magna owns 98% share, preserving margin amid CMOS commoditization.

By Technology: Infrared Advances as CMOS Commoditizes

CMOS remains the workhorse at 78.50% Automotive Backup Camera market share, benefiting from sub-USD 1 sensor cost and on-chip processing that lowers ECU load. CCD retreats to niches, while infrared modules climb at a 10.40% CAGR, finding demand in 24-hour logistics and harsh-weather routes.

The cost gap narrows as uncooled microbolometers scale. Magna’s 640 × 480 thermal unit now integrates edge AI in a USD 150–200 package, fetching 5–7 times CMOS prices yet paying back fleets within two years via fewer incidents. Pending EU studies on night-vision mandates for commercial vehicles could accelerate uptake.

By Sales Channel: Aftermarket Outpaces OEM Fit

OEM fit accounted for 68.90% of Automotive Backup Camera market revenue in 2024, but the aftermarket grows at 11.30% as the median vehicle age rises and insurers incentivize retrofits. Wireless kits selling for USD 150–300 slash installation time to under an hour, appealing to DIY owners.

OEM channels focus on software-unlockable features, turning cameras into recurring-revenue nodes; Valeo’s Mobileye-equipped systems exemplify this trend. The aftermarket remains hardware-centric yet faces warranty-exposure risks from low-quality imports lacking ingress-protection certifications.

Geography Analysis

North America held 34.20% Automotive Backup Camera market share in 2024, underpinned by FMVSS 111 mandates. Growth now arises from aftermarket retrofits and the final LCV compliance wave concluding in 2026. Insurance discounts of 5–10% and harsh Canadian winters, which necessitate higher-spec heaters and coatings, shape supplier specification strategies.Europe ranks second, driven by Regulation 2019/2144 and Euro NCAP’s visibility weighting . Germany, the United Kingdom, France, and Italy supply over 60% of regional demand. The EU AI Act imposes high-risk classification on object-recognition cameras, hiking compliance outlays and pushing smaller vendors toward consolidation.

Asia-Pacific leads by volume as China eyes a 2026 rear-visibility mandate that could add 20–25 million units annually. Japan and South Korea leverage domestic sensor and module capacity, securing cost advantages. India’s price-sensitive market adopts sub-USD 20 cameras to meet BNVSAP goals.The Middle East and Africa log a 7.90% CAGR, fastest globally, as GCC states embed Euro-style rules and offer tax breaks for fleet retrofits. Israel’s perception-software ecosystem drives high-resolution demand, while South African retrofits echo North American patterns.

South America remains the smallest region. Brazil debates commercial-vehicle mandates amid fiscal constraints, and Argentina’s volatility dampens near-term purchases, though mining fleets present ruggedized-camera opportunities.

Competitive Landscape

Top-five suppliers—Bosch, Valeo, Continental, Magna, and DENSO—capture roughly 60-65% of Automotive Backup Camera market revenue, leaving space for niche players. Bosch partnered with Cariad in April 2025 to decouple perception software from proprietary ECUs, letting automakers source commodity hardware while retaining software control. Valeo embeds Mobileye processors for over-the-air upgrades, surpassing 20 million shipments in March 2025. Magna focuses on thermal imaging, owning 98% of that premium sub-segment after surpassing 1 million units shipped by January 2025.

ISO/SAE 21434 cybersecurity compliance is now a gating factor. Suppliers able to amortize secure-boot loaders and penetration testing across multi-million-unit programs gain bid advantages, accelerating consolidation. Cost-driven challengers from China, such as OmniVision, undercut pricing by up to 30% but struggle to meet functional-safety and cybersecurity thresholds, limiting penetration into premium OE programs.

Emerging business models include camera-as-a-service contracts that shift capital expense to operating expense and lock in long-term software revenue. While hardware margins tighten, companies that bundle algorithms, analytics, and compliance certification preserve profitability.

Automotive Backup Camera Industry Leaders

Robert Bosch GmbH

Valeo SE

Continental AG

Magna International Inc.

Gentex Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Bosch and Cariad agreed to co-develop standalone video-perception software that separates intelligence from hardware, challenging vertically integrated rivals.

- March 2025: Valeo produced its 20 millionth front-facing camera system with Mobileye EyeQ processors, reinforcing its strategy to monetize software updates beyond initial sales.

- January 2025: Magna launched its Gen.5 thermal camera, having shipped more than 1 million night-vision units and holding 98% share of the premium infrared space.

- August 2024: The EU AI Act (Regulation 2024/1689) entered into force, classifying object-recognition cameras as high-risk AI systems and inflating compliance costs.

Global Automotive Backup Camera Market Report Scope

The Automotive Backup Camera Market is segmented by Product Type (Wired Systems, and Wireless Systems), Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), and Heavy Commercial Vehicles (HCVs)), Technology (CMOS Sensor Cameras, CCD Sensor Cameras, and Infra-red Cameras), Sales Channel (Original Equipment Manufacturer (OEM) Fit, and Aftermarket), and Geography (North America, Europe, Asia-Pacific, and more).

| Wired Systems |

| Wireless Systems |

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Heavy Commercial Vehicles (HCVs) |

| CMOS Sensor Cameras |

| CCD Sensor Cameras |

| Infra-red / Night-Vision Enabled Cameras |

| Original Equipment Manufacturer (OEM) Fit |

| Aftermarket |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Wired Systems | |

| Wireless Systems | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCVs) | ||

| Heavy Commercial Vehicles (HCVs) | ||

| By Technology | CMOS Sensor Cameras | |

| CCD Sensor Cameras | ||

| Infra-red / Night-Vision Enabled Cameras | ||

| By Sales Channel | Original Equipment Manufacturer (OEM) Fit | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Automotive Backup Camera market in 2025?

It stands at USD 3.04 billion with a 6.73% forecast CAGR toward USD 4.21 billion by 2030.

Which product architecture grows fastest through 2030?

Wireless systems advance at a 9.80% CAGR as electric-vehicle platforms and retrofit demand favor reduced cabling.

Why are heavy commercial vehicles attracting attention?

Insurance-premium discounts and updated FMCSA windshield rules drive an 8.60% CAGR for camera adoption in trucks.

What technology segment offers premium pricing?

Infrared night-vision modules, though only a minor share today, grow 10.40% annually and command 5–7 times CMOS prices.

How do insurers influence retrofit demand?

Discounts of 5–10% for vehicles with cameras shorten aftermarket payback periods to about two to three years.

Which region shows the fastest growth rate?

The Middle East and Africa record a 7.90% CAGR as GCC nations roll out Euro-style rear-visibility rules.

Page last updated on: