Automated CPR Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 246.40 Million |

| Market Size (2031) | USD 367.60 Million |

| Growth Rate (2026 - 2031) | 8.33% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automated CPR Devices Market Analysis by Mordor Intelligence

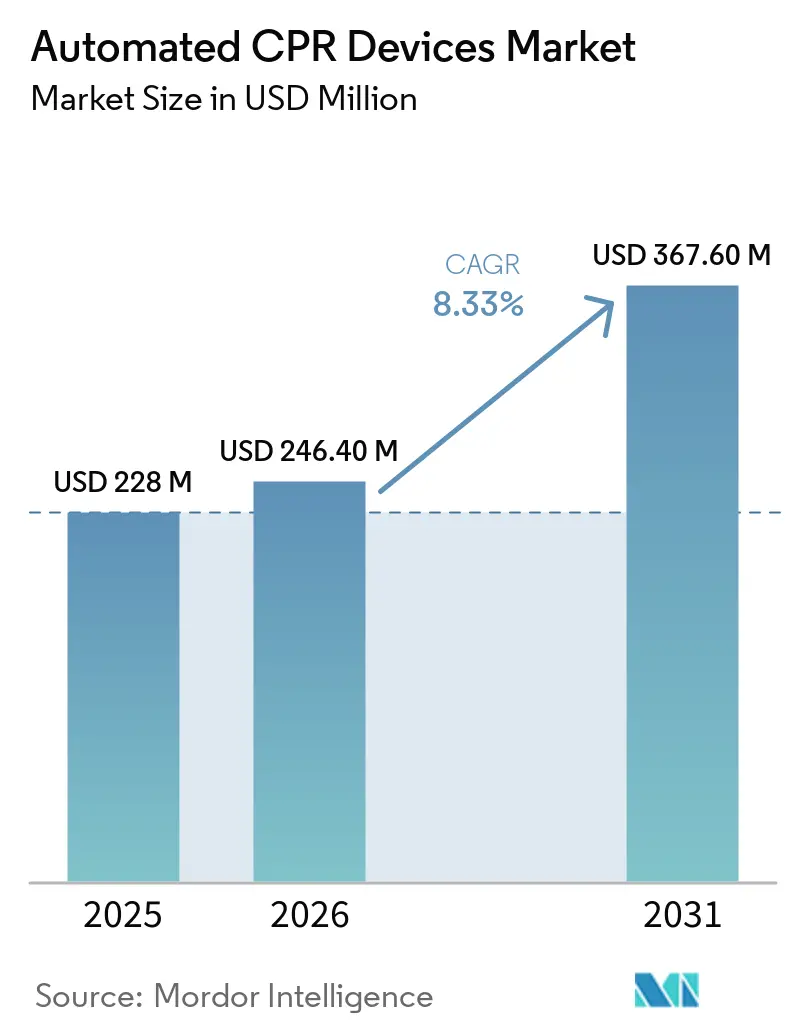

The Automated CPR Devices Market size is expected to grow from USD 228 million in 2025 to USD 246.40 million in 2026 and is forecast to reach USD 367.60 million by 2031 at 8.33% CAGR over 2026-2031.

Rising reliance on uninterrupted chest compressions during transport, the advantages of battery-electric platforms, and expanding deployment in catheterization laboratories underpin this growth trajectory. Demand concentrates where manual cardiopulmonary resuscitation (CPR) cannot be sustained—air-medical missions, rural long-haul transfers, and prolonged in-hospital codes—driving recurring sales of consumables and maintenance contracts. At the same time, guideline caution from the International Liaison Committee on Resuscitation (ILCOR) and the American Heart Association (AHA) channels adoption toward selective high-acuity indications rather than blanket equipping of every ambulance, creating a bifurcated Automated CPR devices market marked by premium purchasing from tertiary centers and constrained budgets in low-volume services. Competitive intensity remains moderate because Stryker and Zoll leverage multi-year service agreements that embed training, software, and disposables, raising switching costs and stabilizing the Automated CPR devices market through predictable revenue streams.

Key Report Takeaways

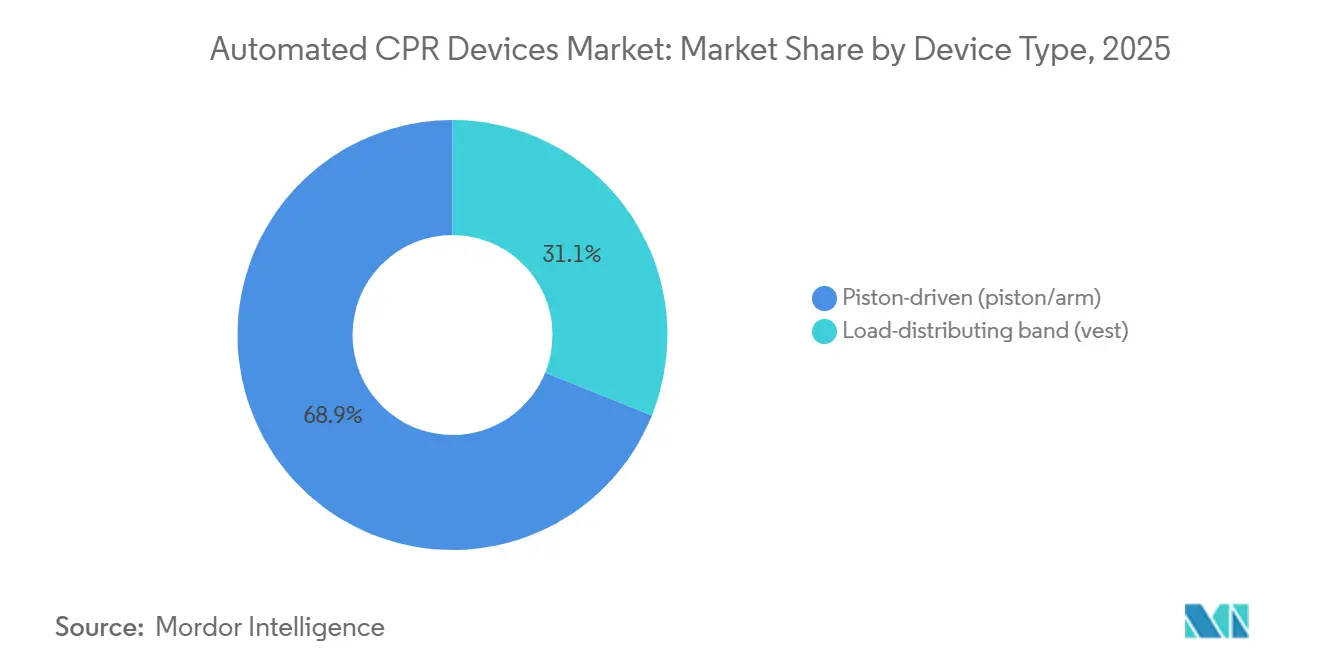

- By device type, piston-driven systems led with 68.90% of the Automated CPR devices market share in 2025, while load-distributing band units recorded the fastest 8.93% CAGR through 2031.

- By power source, battery-electric configurations accounted for 61.30% of the Automated CPR devices market in 2025 and are advancing at 8.56% CAGR through 2031.

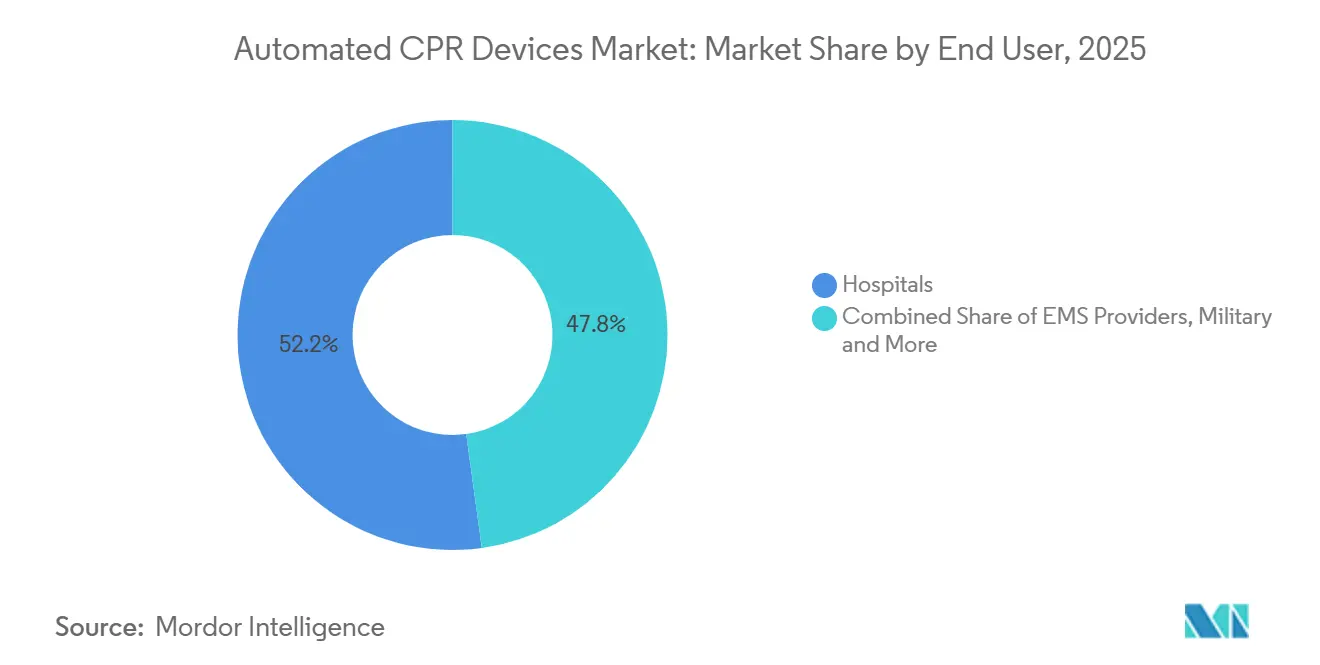

- By end user, hospitals captured 52.18% revenue in 2025, whereas emergency medical services providers are projected to expand at a 9.05% CAGR during 2026-2031.

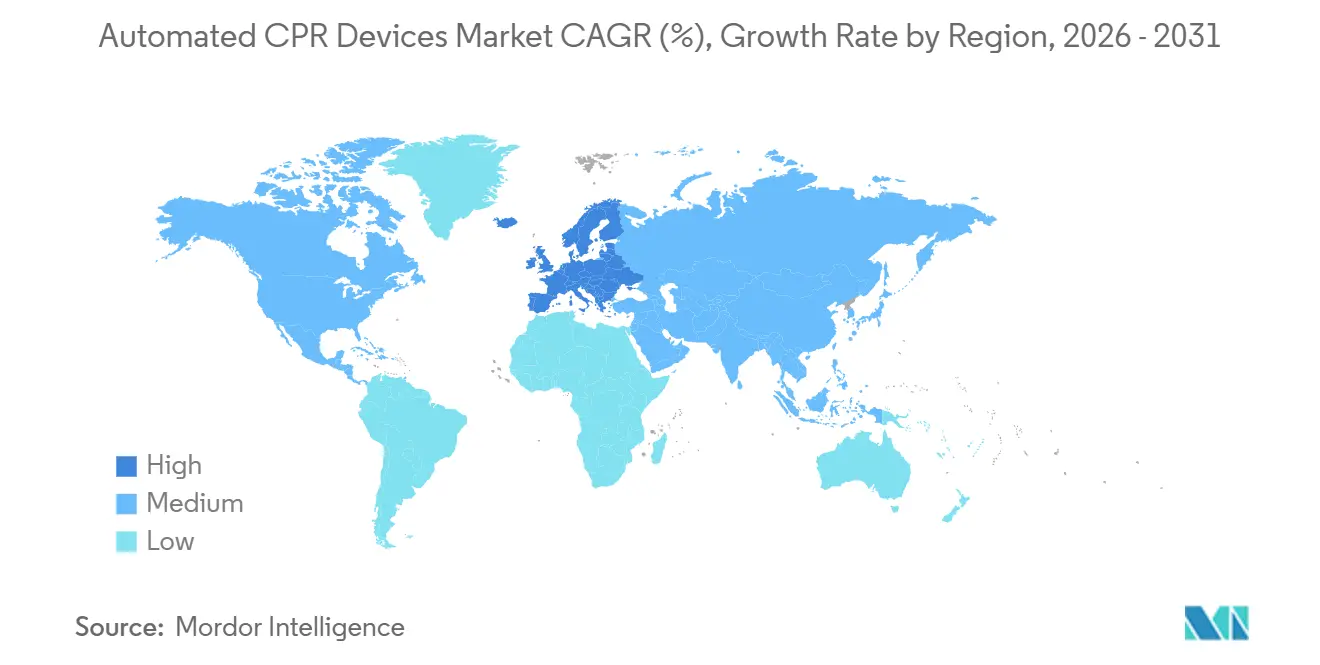

- By geography, North America held 41.90% share in 2025, yet Europe is forecast to post the strongest 8.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automated CPR Devices Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising OHCA incidence and persistently low survival rates drive adoption of CPR adjuncts | +2.1% | Global, with highest absolute case volumes in North America, Europe, and urban Asia-Pacific | Long term (≥ 4 years) |

| Shift to battery-powered mechanical CPR for transport consistency and crew safety | +1.8% | North America (air medical and rural ground), Europe (interfacility transfer), Australia | Medium term (2-4 years) |

| Growing EMS and hospital use for transport, cath lab PCI, and prolonged resuscitation codes | +2.4% | North America, Europe, select tertiary centers in China, Japan, South Korea | Medium term (2-4 years) |

| Product refresh cycles and new launches expand installed base and feature sets | +1.2% | Global, with concentration in North America and Europe replacement markets | Medium term (2-4 years) |

| Air medical transport standardization for uninterrupted CPR during flight operations | +1.0% | North America (dominant air-medical market), Australia, Northern Europe | Short term (≤ 2 years) |

| Rural EMS staffing gaps and aging volunteer workforce elevate device adoption need | +1.5% | North America rural counties, Northern Europe, Australia regional services | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising OHCA Incidence and Persistently Low Survival Rates Drive Adoption of CPR Adjuncts

Global out-of-hospital cardiac arrest (OHCA) survival to discharge remained below 10% through 2025, prompting care systems to test adjuncts that minimize pauses during airway management, vascular access, or defibrillation. In the United States, the CARES registry reported 9.1% survival for all-rhythm arrests, while Ireland documented 8.0% survival across 2,746 cases, 53% of which used mechanical CPR [1]CARES, “2025 Annual Report,” mycares.net. A Vienna dataset echoed the challenge with 9.3% survival, reinforcing the need for devices that sustain perfusion during inevitable hands-off periods. Tehran University researchers demonstrated a 14.1-percentage-point absolute improvement in return of spontaneous circulation when LUCAS-3 replaced manual technique, underscoring why tertiary centers embed mechanical CPR in refractory-arrest algorithms.

Collectively, these findings point to a durable demand driver for the Automated CPR devices market among systems seeking incremental gains in neurologically intact survival.

Growing EMS and Hospital Use for Transport, Cath Lab PCI, and Prolonged Resuscitation Codes

Catheterization laboratories now treat ongoing arrest with simultaneous percutaneous coronary intervention, a practice linked to 51% return of spontaneous circulation and 26% good neurological outcome in a Swedish cohort [2]Lund University, “PCI During Cardiac Arrest Outcomes,” lunduniversity.lu.se. Mechanical devices maintain diastolic pressures above 30 mmHg, safeguarding cerebral perfusion while guidewires advance. Air-medical fleets logged over 600 CPR transports in 2025, compelling Air Methods to standardize AutoPulse NXT across its aircraft to keep crew members restrained during turbulence.

Ground agencies facing 30-mile interfacility transfers followed suit. Such operational realities cement the Automated CPR devices market as a transport-critical technology rather than a mere in-station convenience.

Shift to Battery-Powered Mechanical CPR for Transport Consistency and Crew Safety

Battery-electric architectures eliminate dependence on compressed oxygen, trimming setup time to under 5 seconds and extending runtime to 45 minutes per charge enough for the longest rotor-wing missions. Bluetooth-enabled LUCAS 3.1 exports compression metrics to electronic patient-care records, a feature prized by quality-improvement programs. Pneumatic devices persist in operating rooms yet lose relevance in pre-hospital spaces where cylinder logistics and hose entanglement are liabilities. Mercy Air cited turbulence-related injury risk as a primary reason for installing AutoPulse in June 2025, spotlighting how crew-safety mandates accelerate battery adoption.

Rural EMS Staffing Gaps and Aging Volunteer Workforce Elevate Device Adoption Need

Median volunteer crew size in U.S. rural counties fell to 2-3 responders in 2025, down from 4-5 ten years earlier, straining manual-CPR continuity during 20- to 40-mile transports. Cotton Fire Department, Fayette County EMS, and others purchased mechanical devices specifically to offset shrinking rosters.

The Buhl Rural Fire District reported successful 35-mile transports with just two personnel after integrating LUCAS, a scenario impossible under manual protocols. While individual order volumes remain small, cumulative demand across thousands of rural agencies lifts the Automated CPR devices market over the long term.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clinical guidelines discourage routine use; selective indications only | -1.2% | Global, particularly influencing public-sector procurement in Europe, Canada, and Australia | Short term (≤ 2 years) |

| High total cost of ownership (device, consumables, training, maintenance) | -0.9% | Low-volume rural services in North America, resource-constrained Asia-Pacific, Middle East & Africa, South America | Medium term (2-4 years) |

| Reliability and recall risks disrupt service continuity and erode clinical confidence | -0.4% | Global, with heightened sensitivity in North America and Europe due to regulatory scrutiny | Short term (≤ 2 years) |

| Improper deployment can delay first shock and medication administration in EMS protocols | -0.3% | North America and Europe EMS systems with rapid response times (<8 minutes) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Clinical Guidelines Discourage Routine Use; Selective Indications Only

ILCOR’s 2025 Consensus issued a weak recommendation against routine mechanical CPR after six randomized trials showed no survival benefit in unselected arrests, a conclusion echoed by AHA and the European Resuscitation Council [3]ILCOR, “2025 Advanced Life Support CoSTR,” ilcor.org. Canada’s technology-assessment agency added concerns over fracture risk and absent cost-effectiveness data, prompting budget committees to delay large-scale procurement. Consequently, many purchasers now restrict devices to transport, catheterization labs, or limited-personnel cases, trimming near-term volumes in the Automated CPR devices market even as niche demand persists.

High Total Cost of Ownership (Device, Consumables, Training, Maintenance)

A five-year life-cycle outlay approaches USD 45,000 for agencies performing 100 resuscitations, once acquisition, training, service, and single-use bands are included. In departments with fewer than 20 annual arrests, per-case costs exceed USD 2,000—hard to justify when manual CPR is “free.” A 2026 JAMA model pegged home AED programs at USD 4.48 million per QALY, illustrating how expensive resuscitation adjuncts struggle for cost-utility in low-incidence settings. The same calculus tempers Automated CPR devices market penetration across Asia-Pacific and Africa, where budgets prioritize basic life-support gear.

Segment Analysis

By Device Type: Piston-Driven Architectures Sustain Dominance Amid Installed-Base Inertia

Piston systems commanded 68.90% of Automated CPR devices market share in 2025 and are projected to expand at an 8.93% CAGR through 2031. The architecture’s motorized plunger consistently delivers 102 compressions per minute at 5.0-5.5 cm depth, a standard difficult to maintain manually for more than 3 minutes. Multi-year service contracts lock hospitals and emergency medical services (EMS) providers into proprietary suction cups and software, creating annuity streams that underpin the Automated CPR devices market size for Stryker and its distributors. Load-distributing band rivals such as Zoll’s AutoPulse apply circumferential thoracic pressure and claim better perfusion indexes for bariatric patients; nonetheless, trained crews favor piston units’ faster setup when seconds matter.

Emerging Chinese manufacturers price comparable piston devices 30-40% below Western incumbents yet face regulatory delays in the United States and Europe, limiting near-term share gain. Corpuls’ Bluetooth synchronization, which trims peri-shock pause to 2.00 seconds, illustrates how incremental feature gains can win tenders in highly scrutinized European markets.

By Power Source: Battery-Electric Platforms Capture Transport and Air-Medical Use-Cases

Battery-electric units held 61.30% share in 2025 and are growing at 8.56% CAGR through 2031, reflecting the operational imperative to avoid oxygen cylinders during helicopter lift-offs and stair-chair extrications. The Automated CPR devices market size expansion for this segment is reinforced by fleet-wide adoptions such as Air Methods’ 2025 rollout and Mercy Air’s June 2025 integration.

Pneumatic alternatives, significant share, remain entrenched in fixed clinical settings where compressed gas is plentiful, but they are forecast to trail at high CAGR as pre-hospital buyers migrate to cordless simplicity.

By End User: EMS Providers Set the Pace as Transport Protocols Normalize Continuous Compressions

Hospitals represented 52.18% revenue in 2025, underpinned by catheterization-lab use during coronary intervention and by extracorporeal CPR programs that require stable perfusion during cannulation. EMS providers, however, are slated for 9.05% CAGR, overtaking institutions by 2031 as national protocols mandate uninterrupted compressions during scene-to-hospital transfers. This dynamism underscores how evolving field guidelines recalibrate spending priorities within the Automated CPR devices market.

Geography Analysis

North America retains the largest installed base, translating to 41.90% of 2025 revenue, yet guideline restraint and cost-effectiveness debates temper growth in forecasted period. High-profile contracts—such as Los Angeles Fire Department’s USD 9.4 million monitor procurement that deliberately excluded mechanical devices—illustrate selective spending. In contrast, Europe is posting the fastest 8.78% CAGR on the back of protocol harmonization across 24 of 27 member states and rising cross-border funding for cardiology centers.

Asia-Pacific lags in penetration but not ambition, with China’s 2023 clinician survey revealing transition from manual to mechanical CPR during prolonged codes despite limited device availability. Domestic innovation, typified by Korea’s ROSCER prototype, could localize supply and accelerate Automated CPR devices market diffusion in the region. Middle East and Africa, along with South America, accounted for less than modest share of revenue in 2025; however, Qatar’s registry-reported mechanical CPR rate demonstrates niche pockets of high uptake, albeit with mixed survival outcomes.

Competitive Landscape

The automated CPR devices market is moderately concentrated. Stryker’s LUCAS surpassed 50,000 global units by December 2024, while Zoll Medical’s AutoPulse NXT won the entire Air Methods fleet, signifying control of the air-medical vertical. Asahi Kasei’s fiscal 2025 earnings dipped because of delayed defibrillator launches, yet the company counters by bundling AutoPulse with monitor-defibrillator packages. Mid-tier firms such as Corpuls differentiate on connectivity, evidenced by its Cosinuss acquisition for in-ear sensor integration.

Chinese entrants tempt cost-sensitive buyers but remain absent from U.S. Food and Drug Administration clearances, curbing their influence on high-value tenders. A May 2025 Class 2 recall covering five refurbished LUCAS demonstration units highlights reputational risks in a market already moderated by cautious guidelines.

Automated CPR Devices Industry Leaders

-

Stryker Corporation

-

ZOLL Medical Corporation

-

CU Medical Systems, Inc

-

Codex Healthcare

-

SCHILLER AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Zoll Medical launched the LifeVest wearable cardioverter-defibrillator, leveraging cardiology relationships to broaden beyond the Automated CPR devices market.

- June 2025: Corpuls acquired Cosinuss for in-ear vital-sign sensors, aiming to embed physiologic feedback into corpuls cpr workflows.

- May 2025: Air Methods finished a nationwide AutoPulse NXT deployment, standardizing mechanical CPR across 600-plus annual transports.

Global Automated CPR Devices Market Report Scope

As per the scope of the report, automated CPR devices, also known as mechanical chest compression devices, are portable machines designed to deliver high-quality, consistent chest compressions to victims of sudden cardiac arrest. These devices serve as an adjunct to manual CPR, addressing human limitations such as rescuer fatigue, which typically sets in after just two minutes and leads to a decrease in compression depth and rate.

The automated CPR devices market is segmented by device type, power source, end users, and geography. By device type, the market is segmented into piston-driven and load-distributing band. By power source, the market is segmented into battery-electric, and pneumatic/oxygen-driven. By end users, the market is segmented into hospitals, EMS providers, military & defense, and ambulatory surgical centers & specialty clinics.

Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Piston-driven (piston/arm) |

| Load-distributing band (vest) |

| Battery-electric |

| Pneumatic/oxygen-driven |

| Hospitals |

| EMS Providers |

| Military & Defense |

| Ambulatory Surgical Centers & Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Type | Piston-driven (piston/arm) | |

| Load-distributing band (vest) | ||

| By Power Source | Battery-electric | |

| Pneumatic/oxygen-driven | ||

| By End User | Hospitals | |

| EMS Providers | ||

| Military & Defense | ||

| Ambulatory Surgical Centers & Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the Automated CPR devices market by 2031?

The market is forecast to reach USD 367.6 million by 2031 at an 8.33% CAGR.

Which device type leads current sales?

Piston-driven systems held 68.90% share in 2025 and continue to dominate through installed-base loyalty

Why are battery-electric platforms growing faster than pneumatic units?

They remove oxygen-cylinder logistics, cut setup time below 5 seconds, and allow safe operation in helicopters and narrow spaces

Which end-user category is expanding the quickest?

EMS providers are advancing at 9.05% CAGR by 2031 as transport protocols mandate continuous compressions.

Page last updated on: