Austria OOH And DOOH Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

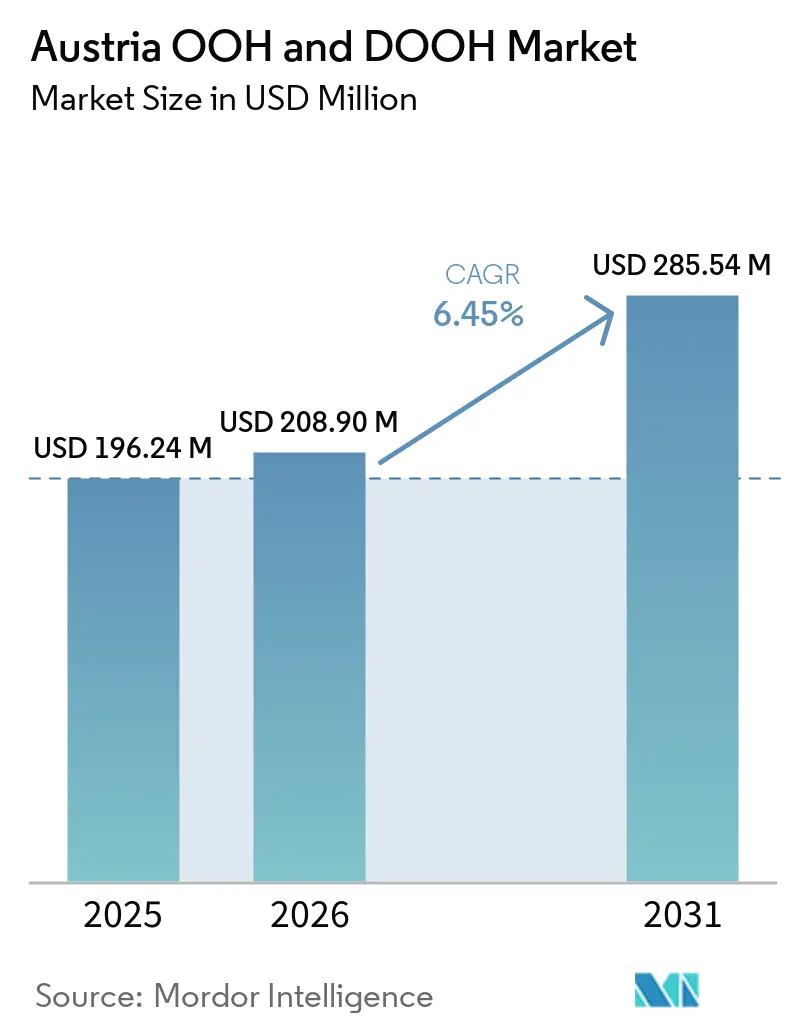

| Base Year Market Size (2025) | USD 196.24 Million |

| Market Size (2026) | USD 208.90 Million |

| Market Size (2031) | USD 285.54 Million |

| Growth Rate (2026 - 2031) | 6.45% CAGR |

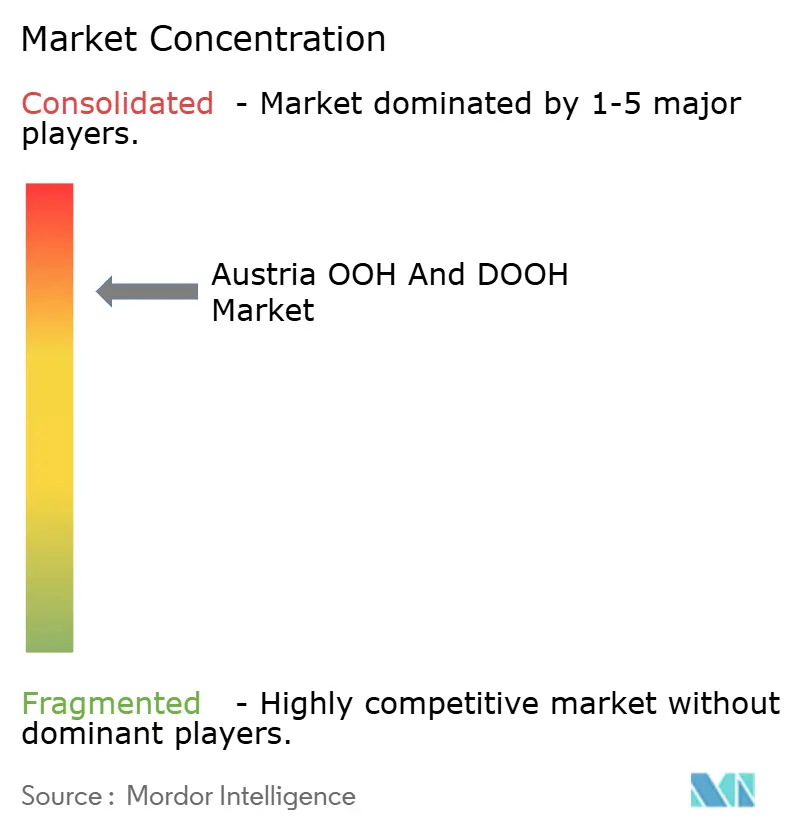

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Austria OOH And DOOH Market Analysis by Mordor Intelligence

The Austria OOH and DOOH market size is expected to grow from USD 196.24 million in 2025 to USD 208.90 million in 2026 and is forecast to reach USD 285.54 million by 2031 at 6.45% CAGR over 2026-2031. The Austria OOH and DOOH market is expanding on the back of steady demand for broad-reach outdoor media and a faster shift toward digital screens that can be sold in more flexible ways. The strongest change inside the category is the move from fixed poster cycles to programmatic, impression-based buying, which is gradually changing how inventory is priced and how campaigns are planned. Vienna remains the center of activity because it combines dense transit usage, premium digital inventory, and the highest concentration of national advertisers and tourist traffic. Growth is also supported by strong audience exposure at transit hubs, airports, and retail sites, which continue to justify premium pricing for brand-led campaigns even as online video and social media compete for budgets. At the same time, the market still faces practical limits from permitting rules, screen restrictions in sensitive locations, and data privacy constraints that make outdoor targeting less flexible than online advertising.

Key Report Takeaways

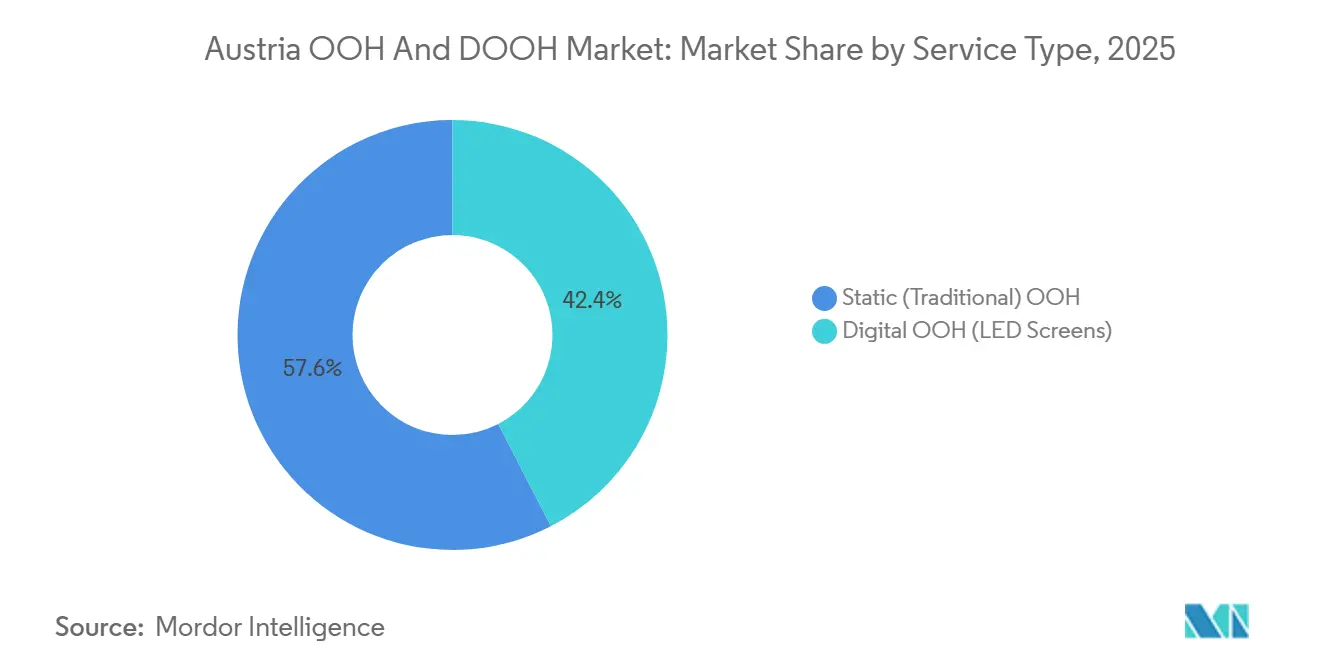

- By service type, Static OOH led with 57.56% share in 2025, while Digital OOH is forecast to expand at a 6.54% CAGR through 2031.

- By application, Billboard advertising held 44.25% share in 2025, while Transportation is projected to record the highest CAGR at 6.65% through 2031.

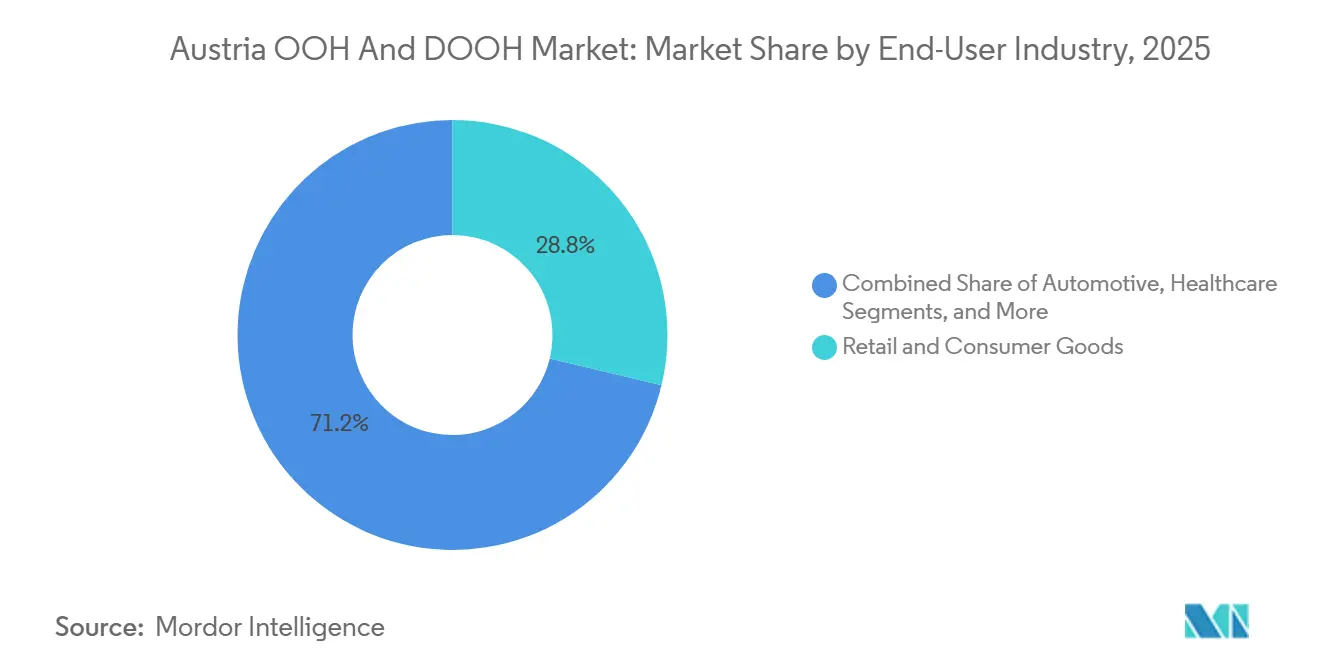

- By end-user industry, Retail and Consumer Goods accounted for 28.76% share in 2025, while Entertainment and Media Streaming is expected to grow fastest at a 6.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Austria OOH And DOOH Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising DOOH Spend and Strong Category Growth | +2.3% | National, with Vienna and Graz as core demand centers | Short term (≤ 2 years) |

| Dense Public Transport and Walkable Urban Mobility | +1.1% | Vienna, Graz, Salzburg, Linz | Medium term (2-4 years) |

| High Programmatic Bookability of Austrian DOOH Inventory | +0.9% | National, early gains in Vienna | Medium term (2-4 years) |

| Tourism and Airport Passenger Records Expanding Premium Audiences | +0.7% | Vienna, Salzburg, Tyrol, Innsbruck | Medium term (2-4 years) |

| Measurement Upgrades Through OSA Multi-Source Mobility Data | +0.5% | National | Medium term (2-4 years) |

| Retail Media and Place-Based Screen Expansion | +0.3% | Urban Austria, with early gains in Tyrol and Vienna | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising DOOH Spend and Strong Category Growth

Austria's DOOH gross advertising spend reached EUR 109.5 million (USD 118.3 million) in 2024, up 14.8% from the prior year, and carried a further 7.0% growth estimate into 2025, while classical OOH formats were projected to grow only 1.2% over the same period.[1]FOCUS Institut, “FOCUS Jahresbilanz 2024,” FOCUS Institut, focusmr.com Source: Azerion Austria, “FOCUS 2025 Österreich,” Azerion Austria, azerion.at DOOH's share of Austrian OOH gross spend reached 32.1% in 2024 and climbed to an estimated 34.4% by 2025, showing that spend is moving steadily toward digital formats inside a stable outdoor category. OOHA also reported that OOH reached an 8.9% share of Austria's above-the-line advertising market in H1 2025, which marked a stronger position for the channel within national ad budgets. For the Austria OOH and DOOH market, this means digital growth is not only pulling money from online channels, but is also taking share from static formats inside the same category. That internal shift is narrowing the pricing gap between digital and traditional outdoor inventory and making DOOH easier to justify for performance-led media teams. The next step for the Austria OOH and DOOH market is whether operators can turn mid-market advertisers into repeat buyers through simpler self-service and programmatic tools.

Dense Public Transport and Walkable Urban Mobility

Wiener Linien passed 900 million annual passenger journeys for the first time in 2025 and reached 903 million, with a daily average of 2.47 million passengers and 1.34 million season ticket holders.[2]Rathauskorrespondenz / Presse-Service der Stadt Wien, “Bilanz 2025: Wiener Linien Durchbrechen 900 Millionen Fahrgäste-Schallmauer,” Stadt Wien, wien.gv.atÖBB crossed 511 million total passengers in 2024, while local and regional rail ridership rose 10% year over year across a network of 1,058 stations. Vienna's 2024 modal split put public transport at 34% of all trips and walking at 30%, while private car use fell to 25%, which raises dwell time and repeat exposure for transit shelters, street furniture, and in-vehicle screens. On a national basis, 68.3% of Austrians walk at least 250 meters daily, and the federal mobility agenda continues to support higher active mobility over time. Wiener Linien also planned EUR 759.9 million (USD 828.3 million) of investment in 2026, led by the U2xU5 expansion, which adds more station environments and future advertising touchpoints. This keeps audience delivery strong across the Austria OOH and DOOH market because route-loyal commuters create a predictable exposure base that operators can map with increasing precision.

High Programmatic Bookability of Austrian DOOH Inventory

OOHA stated that 90% of Austrian DOOH surfaces are programmatically bookable, which places the country among the more mature outdoor markets in Europe for real-time, impression-based trading. Gewista routes its full digital portfolio of around 800 surfaces through the VIOOH supply-side platform and uses OSA data for contact-based billing with placement-level transparency.[3]Gewista, “Programmatic OOH by Gewista,” Gewista, gewista.at In December 2024, Gewista launched a proprietary DMP that combined OSA measurements, geo-location data, sociodemographic profiles, and proximity-to-retail parameters in one planning environment. OSA also updated its multi-source mobility model in January 2025, which improved the quality of audience measurement available to campaign planning and reporting. In practical terms, this cuts campaign lead times from weeks to hours and gives buyers more room to use weather, event, or audience triggers in the Austria OOH and DOOH market. As that process becomes normal, the Austria OOH and DOOH market is becoming easier to buy through the same workflow logic that agencies already use for premium digital media.

Tourism and Airport Passenger Records Expanding Premium Audiences

Vienna Airport handled 32.6 million passengers in 2025, a new record, with Far East traffic up 21.2% and Middle East traffic up 10.6%, which widened the pool of international travelers moving through high-value airport media locations. Austria recorded 157.29 million overnight stays in 2025, up 1.9%, while Vienna crossed 20 million overnight stays for the first time and U.S. visitor nights reached 2.6 million. Those flows matter because they raise the share of affluent, time-rich, and location-concentrated audiences at airports, rail hubs, historic centers, and resort corridors. Seasonal leisure traffic also creates periods when contact density rises faster than resident population would suggest, especially in ski and alpine districts. In December 2025, Azerion Austria and Airport Media executed the first programmatic DOOH campaign at Vienna Airport, which showed that premium aviation media can move toward measurable, impression-based selling. The Vienna Airport Southern Terminal Expansion, targeted for a 2027 opening, is set to add 70,000 m² of dwell space and supports the longer-term premium audience case for the Austria OOH and DOOH market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Municipal Permitting and Protected-Zone Approvals | -1.5% | National, with highest complexity in Vienna, Salzburg, and Innsbruck | Long term (≥ 4 years) |

| Creative Motion Restrictions for Road-Facing Screens | -0.9% | National, StVO-governed roads outside built-up areas | Long term (≥ 4 years) |

| Data Privacy Limits on Location-Based Targeting and Attribution | -0.7% | National, EU-wide GDPR and Austrian TKG 2021 | Medium term (2-4 years) |

| Competition From Online Video, Social, and Retail Media Budgets | -0.5% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Municipal Permitting and Protected-Zone Approvals

Austria's outdoor advertising framework combines federal road traffic law, state building codes, and municipal rules, which creates uneven approval conditions across the country and slows national digital rollout plans. Outside built-up areas, Austrian road rules impose strict limits on advertising close to road edges, which reduces the number of viable locations for new roadside screens. Vienna's Environmental Protection Authority reviews outdoor advertising structures under a formal admissibility process that can stretch beyond a three-month window when environmental or landscape issues are involved. Salzburg applies townscape protection rules with five-year renewable permit terms and architectural fit checks, while Innsbruck requires parallel approvals under local and regional frameworks in sensitive areas. Historic districts therefore remain harder to scale than transit-adjacent or retail-linked locations. For the Austria OOH and DOOH market, that means inventory growth tends to move first into formats and places where approvals are more predictable.

Creative Motion Restrictions for Road-Facing Screens

Austrian roadside advertising rules allow authorities to intervene when an installation may distract drivers, obstruct visibility, or be confused with traffic signals, which places practical limits on animation, luminance, and screen behavior. Tyrol's advertising approval guidance also treats dazzling light and confusing motion as disqualifying factors, which adds another barrier in a region with important tourism corridors. These restrictions reduce the creative flexibility that often helps large-format DOOH compete against online video for automotive, FMCG, and entertainment campaigns. They also make cross-border campaign standardization harder when advertisers want to run the same animated assets across DACH markets. As a result, operators are directing more capital toward indoor, transit, shopping center, and airport formats where those motion limits are less restrictive. That shift helps explain why transportation and retail-linked screens are gaining ground inside the Austria OOH and DOOH market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Static Formats Defend Share as Digital Revenue Mix Shifts

Static (Traditional) OOH held 57.56% of the Austria OOH and DOOH market share in 2025, supported by an estimated 170,000 advertising surfaces nationwide and by the lower-cost reach that poster formats still offer for broad campaigns. Digital OOH is the fastest-growing type, with a 6.54% CAGR forecast through 2031, as screen deployment, transit digitization, and programmatic trading continue to deepen across the Austria OOH and DOOH market. FOCUS data showed that DOOH gross advertising spend rose 14.8% in 2024 and carried a further 7.0% growth estimate into 2025, which was much stronger than the pace of classical OOH formats. DOOH's share of total Austrian OOH gross spend widened to an estimated 34.4% by 2025, showing that the digital mix is rising faster than the headline value of the category. This leaves static formats in a stable but changing role where they still anchor national reach while digital formats take a larger share of premium pricing and flexible buying.

Programmatic OOH is becoming the most important digital sub-segment for long-term pricing within the Austria OOH and DOOH market. OOHA reported that 90% of Austrian DOOH surfaces are programmatically bookable, which gives buyers a much more liquid marketplace than in many other countries. Gewista's digital estate of around 800 surfaces is connected through VIOOH and supports contact-based billing using OSA data, which makes campaign delivery easier to compare with premium online display. Gewista's DMP launch in December 2024 added geo-location, sociodemographic, and retail proximity layers to that process, which improved planning depth for advertisers and agencies. The April 2026 launch of Gewista Map then reduced planning friction further and made hybrid campaign design easier across the Austria OOH and DOOH industry.

By Application: Billboards Anchor Spend While Transit Inventory Accelerates

Billboard advertising accounted for 44.25% share of the Austria OOH and DOOH market size in 2025, and FOCUS Institut valued billboard advertising at EUR 150.94 million (USD 163.0 million) in 2024, up 12.2% year over year. Transportation is the fastest-growing application, with a 6.65% CAGR forecast through 2031, backed by Wiener Linien's 903 million passengers in 2025, ÖBB's 511 million passengers in 2024, and Vienna Airport's 32.6 million passengers in 2025. ÖBB-Werbung operated 22,661 advertising spaces in 2024, up 8.4% year over year, including 159 digital screens, which shows that rail media is expanding with passenger traffic rather than staying fixed. That combination gives transit inventory a scale and repetition advantage that few other applications can match. As mobility volumes keep rising, transportation is taking on a larger strategic role within the Austria OOH and DOOH market.

Street furniture continues to benefit from Vienna's pedestrian-heavy urban pattern, where walking accounted for 30% of trips in 2024. Retail and mall screens are also gaining traction because they place messaging close to purchase decisions and give advertisers more contextual control over creative. In August 2025, Billa's entrance-screen network used weather-triggered content and delivered up to 5 million weekly contacts, which showed that retail-linked DOOH can operate at meaningful scale. Starting in August 2025, the MPREIS-DIGOOH partnership installed 250 digital city-light posters across Tyrol, Salzburg, Carinthia, Vorarlberg, and Upper Austria, which widened place-based coverage beyond Vienna. In February 2026, Azerion Austria added 436 screens across 77 fitness centers through airtango media, which extended venue-based reach into another high-value audience category.

By End-User Industry: Retail Dominance Coexists With Streaming's Rise

Retail and Consumer Goods held 28.76% share of the Austria OOH and DOOH market size in 2025, which reflected the continuing weight of grocery, FMCG, and fashion brands in Austrian outdoor advertising. Entertainment and Media Streaming is the fastest-growing end-user segment, with a 6.67% CAGR projected through 2031, as subscription platforms keep using outdoor media to build broad awareness in a market where digital CPMs have risen. That preference fits the strength of large-format OOH and DOOH at launch moments because they create simultaneous reach in a way that online display often cannot do without heavy repeat exposure. FOCUS Institut's SujetFOCUS 2024 survey also showed strong creative recall for campaigns from Hofer, Billa, and Billa Plus, which supports the continued importance of retail-led advertiser demand. The result is a category mix where retail remains the largest demand pool even as streaming adds faster incremental growth across the Austria OOH and DOOH market.

Automotive advertisers still hold a visible position in premium outdoor and large digital formats, while BFSI brands use Vienna transit media to reach a dense commuter base of 1.34 million season ticket holders. That audience is important because it is repeat-exposed, economically active, and easier to map through route-based planning supported by OSA-linked data systems. Healthcare and pharma campaigns continue to benefit from high-frequency exposure in transit settings, even though product-level rules constrain some messaging categories. Government and public sector campaigns also provide a stable non-commercial revenue layer through public information, infrastructure messaging, and election activity. At the same time, the retail media buildout at Billa and MPREIS is shifting some trade budgets inside the Austria OOH and DOOH industry, while streaming and BFSI are well placed to absorb any released inventory through more flexible buying models.

Geography Analysis

Vienna is the structural core of the Austria OOH and DOOH market because it combines the country's deepest concentration of premium digital screens, transit assets, and programmatic-ready inventory. The city's 2024 modal split put public transport at 34%, walking at 30%, cycling at 11%, and private car use at 25%, which creates a high-contact urban setting for street furniture and transit media. Vienna also passed 20 million overnight stays in 2025 for the first time, which broadened the premium audience base in central districts and visitor-heavy corridors. Vienna Airport reinforced that position with 32.6 million passengers in 2025, which gives the city a strong blend of commuter and international exposure. Approval controls in protected zones still slow some new deployment, but transit and shopping-center environments have remained more expandable than heritage-sensitive street locations.

Graz, Salzburg, Linz, and Innsbruck make up the second tier of the Austria OOH and DOOH market and remain important for regional campaigns and tourism-led demand. Salzburg and Tyrol both benefit from heavy visitor volumes, which support premium audience density in compact urban centers and resort-linked corridors. The market is especially attractive in places where visitors spend long periods near rail stations, pedestrian cores, ski access points, and retail clusters. Salzburg's protected historic environment limits some digital expansion, which keeps supply tighter and supports value at approved locations. The Koralmbahn connection completed in December 2025 is expected to strengthen rail usage between Graz and Klagenfurt over the forecast period and should gradually support more transit-led advertising opportunities.

Rural and peripheral regions remain less developed because lower population density and stricter roadside rules reduce the economic case for large outdoor networks. Austria's national mobility plan supports wider public transport and active mobility growth over time, which should improve the long-term audience base in secondary cities and suburban corridors. The MPREIS-DIGOOH rollout is one of the clearest signs that place-based retail screens can extend the Austria OOH and DOOH market beyond the Vienna-Graz axis. That pattern suggests regional growth is more likely to come from retail, transit-adjacent, and indoor formats than from a broad roadside digital buildout.

Competitive Landscape

The Austria OOH and DOOH market remains moderately concentrated at the national level, with Gewista and EPAMEDIA holding the broadest reach across classic and digital outdoor formats. Gewista's position is reinforced by its scale, its connection to JCDecaux, and its continued investment in programmatic infrastructure and planning tools. The market's measurement backbone is also relatively centralized through the Outdoor Server Austria framework, which gives the leading operators a strong role in how campaigns are measured and compared. Gewista strengthened that position through its DMP launch in December 2024 and the rollout of Gewista Map in April 2026, both of which lowered planning friction and improved data-backed execution. Those moves matter because they help the Austria OOH and DOOH market attract budgets that previously stayed in digital display ecosystems.

EPAMEDIA has pursued its own digital transition by connecting inventory to modern content and booking systems, which has helped it remain a strong national counterweight in the Austria OOH and DOOH market. The company also benefited from the broader shift toward flexible scheduling and more dynamic digital screen management. Below the two largest operators, competitive pressure is rising from programmatic aggregators and venue-led screen owners that do not need to control the largest physical footprint to influence buying flows. Azerion Austria is the clearest example because it combines multi-operator screen access with its Hawk DSP and has expanded both its network and its DACH operating role from Vienna. Its December 2025 airport campaign with Airport Media and its February 2026 fitness-center expansion through airtango show how aggregation can open new inventory pools without building a traditional nationwide estate.

White-space opportunities still exist in indoor venue screens, secondary city street furniture, and place-based media tied to retail and mobility. DIGOOH's MPREIS rollout and MAXFIVE's Billa entrance-screen model show that new supply is increasingly appearing in commerce-linked environments rather than only in classic roadside or poster formats. That is gradually spreading competition across more layers of the value chain, from screen ownership to data, software, and demand aggregation. Even so, the Austria OOH and DOOH market still rewards operators that combine scale, measurement access, and programmatic readiness better than smaller rivals can.

Austria OOH And DOOH Industry Leaders

Gewista Werbegesellschaft m.b.H.

EPAMEDIA GmbH

ÖBB-Werbung GmbH

mw monitorwerbung GmbH

Azerion Austria GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Gewista and dentsu Austria deepened their programmatic DOOH cooperation, with dentsu deploying the AI-assisted Displayce DSP, part of the JCDecaux/Gewista technology ecosystem, and accessing Gewista's DMP for automated briefing-to-campaign-launch workflows, dentsu's initial campaigns accessed inventory from multiple Austrian OOH providers, marking a structural move by a leading media agency group into programmatic DOOH as a standard buying channel.

- May 2026: Azerion Austria appointed Philipp Hengl as Director Digital Out-of-Home DACH and established a central DOOH competence center for the entire DACH region in Vienna, positioning Austria as the strategic hub for Azerion's expanding cross-border digital out-of-home operations.

- April 2026: Gewista launched Gewista Map, an interactive GIS-based online planning tool enabling route-specific search across 24,000+ Austrian OOH locations with Google Street View integration, direct booking inquiry, and audience exposure data, reducing the planning friction that has historically limited OOH to large-agency buyers.

- February 2026: EPAMEDIA restructured its management team to sharpen strategic focus on digitalization and market proximity in the rapidly evolving OOH environment, and installed a new digital Posterlight network at Verteilerkreis Favoriten in Vienna.

Austria OOH And DOOH Market Report Scope

The Austria OOH and DooH Market refers to the sector of advertising in Austria that encompasses both Out-of-Home (OOH) media, such as billboards, transit advertisements, and street furniture, and Digital Out-of-Home (DooH) formats, which include dynamic, screen-based advertising displays in public spaces like shopping centers, airports, and urban transit hubs.

The Austria OOH and DOOH Report is Segmented by Service Type (Static (Traditional) OOH, Digital OOH (LED Screens) (Programmatic OOH, Other OOH (LED Screens)), Application (Billboard, Transportation (Transit) (Airports, Other Transportation (Transit) (Buses, etc.)), Street Furniture, Other Place-Based Media), End-User Industry (Automotive, Retail and Consumer Goods, Healthcare, BFSI, IT and Telecom, Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Static (Traditional) OOH | |

| Digital OOH (LED Screens) | Programmatic OOH |

| Other Digital OOH (LED Screens) |

| Billboard | |

| Transportation (Transit) | Airports |

| Other Transportation (Transit) (Buses, etc.) | |

| Street Furniture | |

| Other Place-Based Media |

| Automotive |

| Retail and Consumer Goods |

| Healthcare |

| BFSI |

| IT and Telecom |

| Other End-User Industries |

| By Service Type | Static (Traditional) OOH | |

| Digital OOH (LED Screens) | Programmatic OOH | |

| Other Digital OOH (LED Screens) | ||

| By Application | Billboard | |

| Transportation (Transit) | Airports | |

| Other Transportation (Transit) (Buses, etc.) | ||

| Street Furniture | ||

| Other Place-Based Media | ||

| By End-User Industry | Automotive | |

| Retail and Consumer Goods | ||

| Healthcare | ||

| BFSI | ||

| IT and Telecom | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

How large is Austria OOH and DOOH in 2026, and where is it heading by 2031?

The category is expected to reach USD 208.90 million in 2026 and is forecast to rise to USD 285.54 million by 2031 at a 6.45% CAGR over 2026-2031.

Which format is leading today, and which one is growing fastest?

Static OOH held the largest share at 57.56% in 2025, while Digital OOH is the fastest-growing type with a 6.54% CAGR through 2031.

Why is transit advertising becoming more important in Austria?

Public transport use remains very high, with Wiener Linien reaching 903 million passenger journeys in 2025 and ÖBB crossing 511 million passengers in 2024, which supports repeated exposure in rail and urban transit environments.

What is pushing programmatic DOOH adoption in Austria?

High digital bookability is the main factor, with 90% of Austrian DOOH surfaces programmatically bookable, supported by OSA measurement and newer tools such as Gewista's DMP and planning platform.

Which advertiser groups are shaping demand the most?

Retail and Consumer Goods led with 28.76% share in 2025, while Entertainment and Media Streaming is the fastest-growing end-user category with a 6.67% CAGR through 2031.

What are the biggest limits on future screen rollout?

The main limits are municipal permitting complexity, protected-zone approvals, and creative restrictions for road-facing digital screens, especially in heritage-sensitive and traffic-regulated locations.

Page last updated on: