Australia Pet Veterinary Diets Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

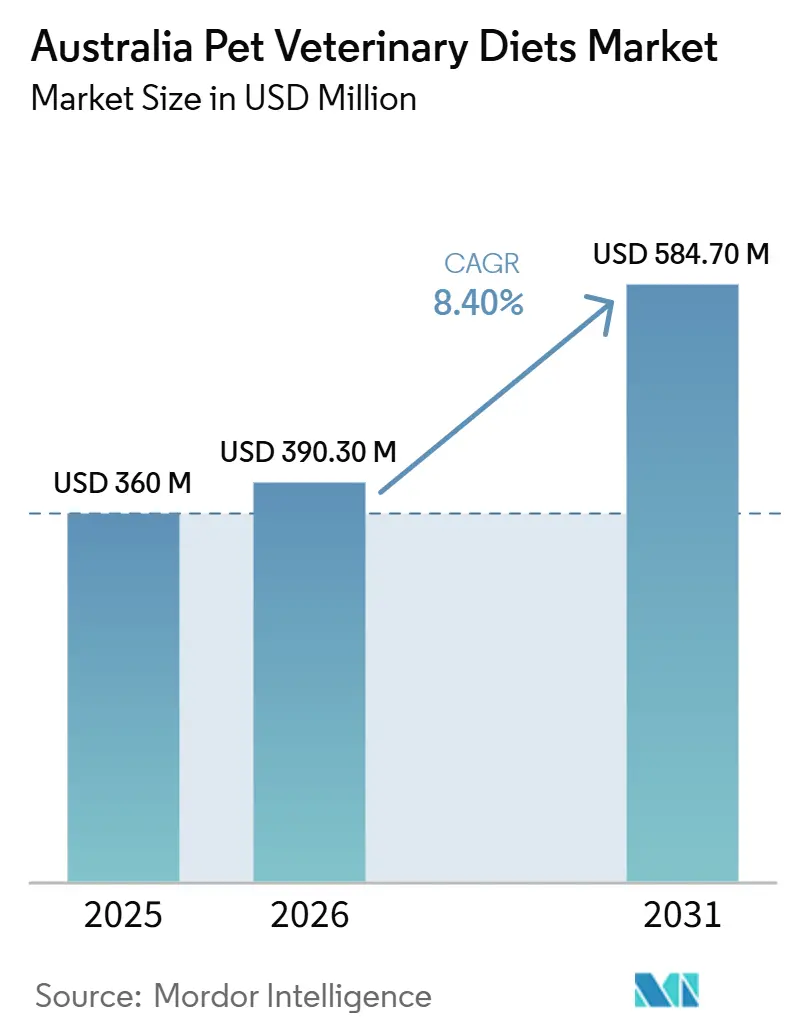

| Base Year Market Size (2025) | USD 360 Million |

| Market Size (2026) | USD 390.30 Million |

| Market Size (2031) | USD 584.70 Million |

| Growth Rate (2026 - 2031) | 8.40% CAGR |

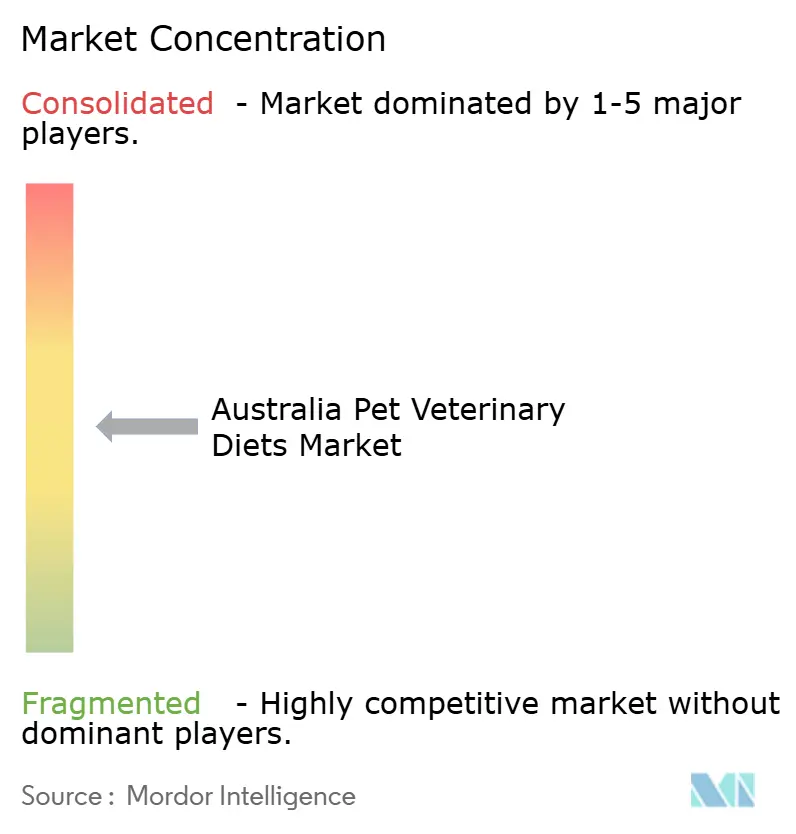

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Pet Veterinary Diets Market Analysis by Mordor Intelligence

The Australia pet veterinary diets market size is projected to expand from USD 360 million in 2025 and USD 390.30 million in 2026 to USD 584.70 million by 2031, registering a CAGR of 8.40% between 2026 and 2031. Australia's large and mature pet population provides a resilient foundation for veterinary nutrition demand. In 2025, 7.7 million households representing 73% of all Australian households owned companion animals, totaling 31.6 million pets. This extensive ownership base continues to support sustained expenditure on premium pet care, including pet food, reinforcing the shift toward therapeutic and premium nutrition[1]Source: Animal Medicines Australia, “Australia's Most Comprehensive Pet Survey Shows Nearly Three Quarters of Australian Homes Now Have a Pet,” animalmedicinesaustralia.org.au. The supplier base is moderately concentrated, with the top five players capturing 58.6% of revenue in 2025. Key competitive factors include product innovation, veterinary partnerships, and access to online reorder channels. However, ingredient cost pressures and the absence of a mandatory national pet food framework continue to pose risks, potentially impacting trust, compliance, and profit margins in the Australia pet veterinary diets market.

Key Report Takeaways

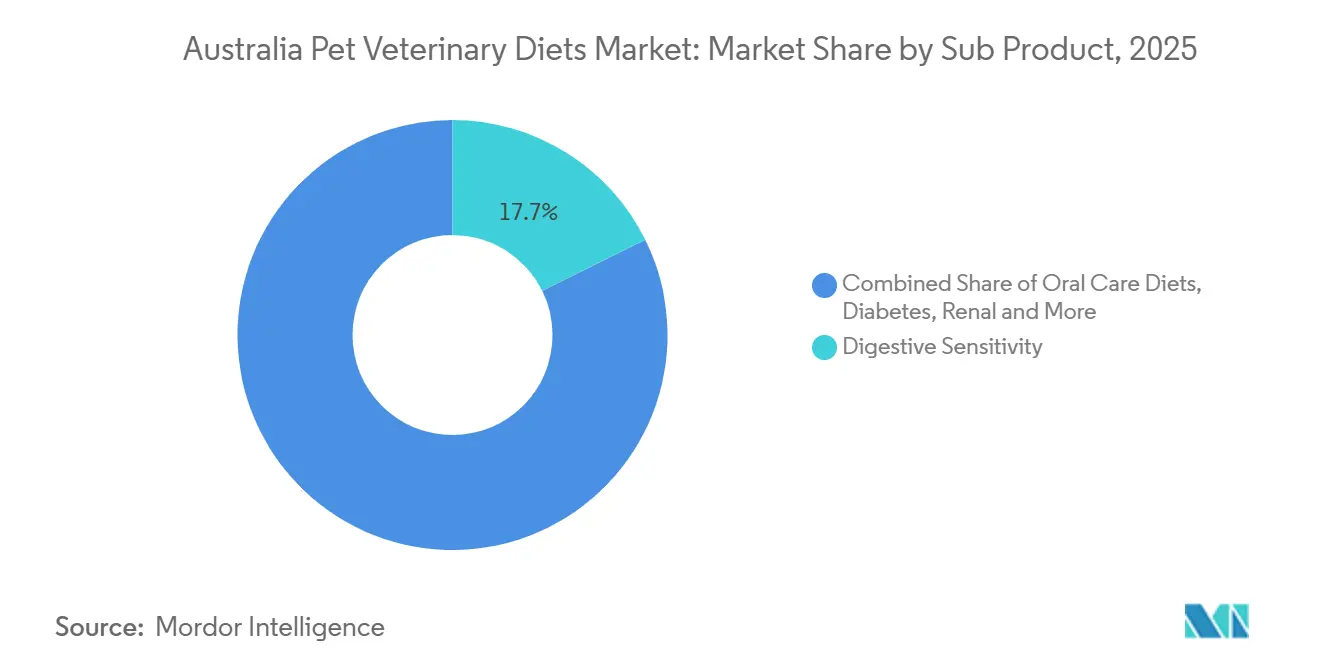

- By sub product, digestive sensitivity led with 17.7% market share in 2025, while oral care diets are forecast to expand at 9% CAGR through 2031.

- By pet type, dogs held 43.6% of the Australia pet veterinary diets market share in 2025, while cats recorded the highest projected CAGR at 8.7% through 2031.

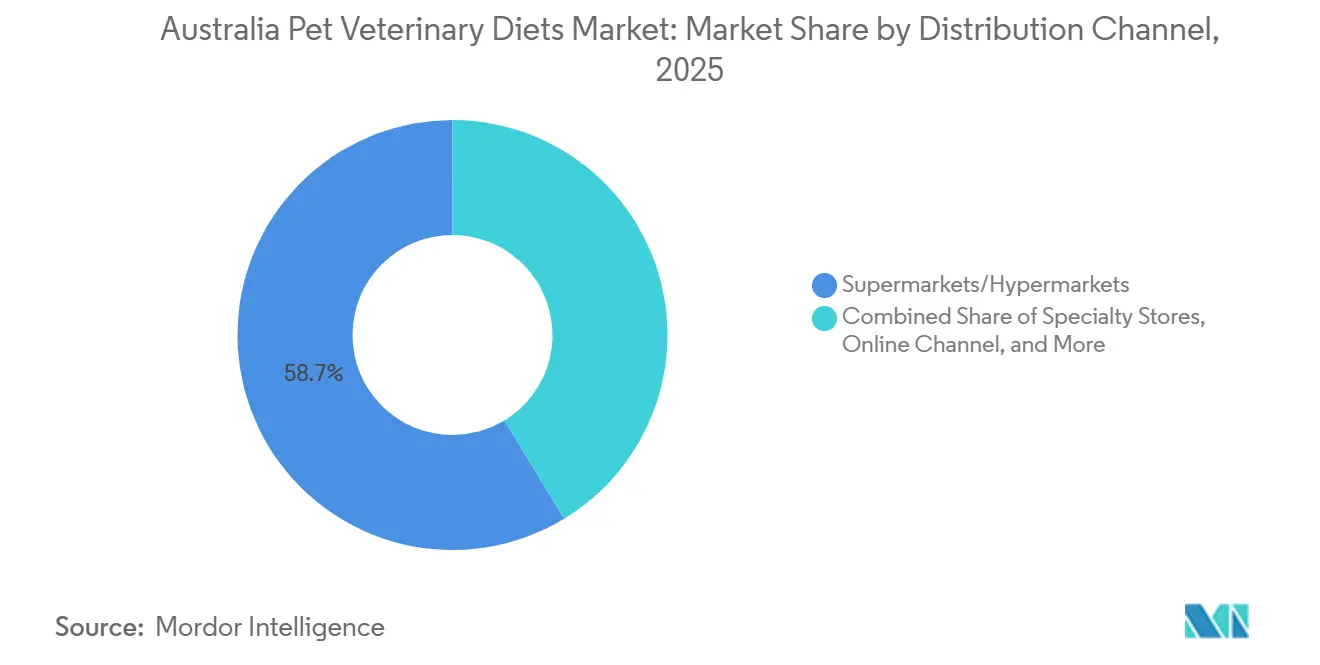

- By distribution channel, supermarkets/hypermarkets accounted for 58.7% share of the Australia pet veterinary diets market size in 2025, while the online channel is advancing at 10.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Pet Veterinary Diets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Pet Humanization and Willingness to Pay for Prescription Nutrition | +2.5% | National, strongest in Sydney, Melbourne, Brisbane, and Perth metro areas | Short term (≤ 2 years) |

| Higher Veterinary Diagnosis Rates for Chronic Conditions | +2.0% | National, highest concentration in major metropolitan veterinary networks | Medium term (2-4 years) |

| Clinic-Linked Compliance Improves Reorder Frequency | +1.2% | National, deepest impact in urban and suburban veterinary practice chains | Short term (≤ 2 years) |

| E-Commerce Prescription Fulfillment Expands Access Beyond Major Cities | +1.5% | National, with outsized gains in regional and semi-rural areas of Queensland, New South Wales, and Victoria | Medium term (2-4 years) |

| Premiumization of Functional and Therapeutic Diets | +1.8% | National, early adoption concentrated in Sydney, Melbourne, and Southeast Queensland | Medium term (2-4 years) |

| Tele-Veterinary Consultation Adoption Supports Diet Switching | +0.8% | National, with clear benefit in regional and remote Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Pet Humanization and Willingness to Pay for Prescription Nutrition

Australian pet owners increasingly consider pets as integral members of their households, driving higher spending on therapeutic pet diets. According to Animal Medicines Australia, Australian pet ownership remained at a record 73% of households in 2025, equivalent to 7.7 million pet-owning homes caring for 31.6 million companion animals. The organization also reported that Australians spent AUD 21.3 billion (USD 13.5 billion) on pet-related products and services during the year, of which AUD 9.8 billion (USD 6.2 billion) was allocated to pet food, highlighting the category's dominant share of overall pet expenditure. As this younger demographic becomes a larger segment of the customer base, the Australian pet veterinary diets market benefits from a growing pool of owners who are more inclined to adopt premium medical nutrition. This trend also supports longer treatment adherence, as owners who view food as part of therapy are less likely to revert to standard diets after initial symptom improvement.

Higher Veterinary Diagnosis Rates for Chronic Conditions

The Australia pet veterinary diets market is positively influenced by the earlier diagnosis and prolonged management of chronic conditions. According to PetSure Pty Ltd’s 2025 Pet Health Monitor, which analyzed claims from over 700,000 insured pets, gastrointestinal conditions, urinary tract disorders, and skin infections and allergies are among the most common reasons for treatment in cats and are also significant conditions in dogs. These conditions are notable as they often necessitate long-term dietary adjustments rather than short-term treatment cycles. Chronic conditions such as kidney disease, urinary disease, food sensitivities, and inflammatory bowel disease require ongoing dietary management, driving repeat purchases on 30-90 day intervals. This makes therapeutic nutrition a more stable category compared to acute care, where demand fluctuates with single episodes. Additionally, Greencross introduced IDEXX Cancer Dx blood-based lymphoma screening into its Senior Lifestage wellness plans in 2025, highlighting the growing adoption of earlier diagnostic pathways in routine care. As diagnostic standards improve, the Australia pet veterinary diets market is positioned to capture more first-time prescriptions and sustain recurring demand through follow-up care.

Clinic-Linked Compliance Improves Reorder Frequency

Veterinary clinics play a crucial role beyond the initial purchase, as they influence whether pet owners continue the therapeutic diet. The Australia pet veterinary diets market benefits when prescription feeding is integrated with wellness visits, nurse follow-ups, or chronic care plans that encourage owners to maintain treatment. Greencross, which operates a large national network, implemented Heidi Health’s AI medical scribe across its clinics in 2025 to reduce administrative tasks for veterinarians. The reported time savings allow for greater focus on nutrition counseling and follow-up discussions, thereby enhancing compliance. This is significant because many therapeutic diets fail not at the diagnosis stage but when owners discontinue reordering after the initial purchase. Clinics that monitor progress, clearly explain the diet, and connect feeding to symptom management typically achieve higher repeat purchase rates. As a result, clinic-linked support serves as a practical demand driver for the Australia pet veterinary diets market, even when subsequent reorders shift to retail or digital channels.

E-Commerce Prescription Fulfillment Expands Access Beyond Major Cities

Online fulfillment is expanding access and simplifying long-term reordering for pet owners in areas outside major urban centers. The Australia pet veterinary diets market is increasingly supported by digital channels, as chronic care diets align well with subscription and auto-ship models. In May 2024, Nestlé Purina announced that its entire Pro Plan Veterinary Diets portfolio would be available on Amazon, highlighting how global pet care companies are leveraging large digital platforms for clinical nutrition[2]Source: Nestlé Purina, “Purina Pro Plan Veterinary Diets Announces Availability in Amazon Store,” newscenter.purina.com. This approach is particularly relevant in Australia, where distance to veterinary clinics poses a significant challenge for many owners, especially in regional communities. According to Animal Medicines Australia, 12% of pet owners required financial assistance for veterinary care in 2025, indicating that travel time and repeated clinic visits can add barriers beyond the cost of products. A robust online reordering system helps mitigate these challenges by maintaining therapeutic feeding after the initial consultation. For the Australia pet veterinary diets market, this factor is critical not only for convenience but also for improving geographic accessibility and ensuring consistent refill behavior.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Price Premium Versus Maintenance Pet Food | -1.8% | National, strongest among lower-income households and rental-heavy demographics | Short term (≤ 2 years) |

| Prescription and Labeling Compliance Limits Digital Conversion | -0.6% | National, most acute in online retail settings that require prescription documentation | Medium term (2-4 years) |

| Volatility in Meat, Protein, and Specialty Ingredient Costs | -1.0% | National, with upstream exposure to global hydrolyzed protein and novel protein cycles | Short term (≤ 2 years) |

| Limited Veterinary Clinic Coverage in Regional Australia | -0.5% | Regional and remote Australia beyond major state capitals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Price Premium Versus Maintenance Pet Food

Price remains a significant constraint on the widespread adoption of therapeutic diets across the broader pet-owning population. The Australia pet veterinary diets market experiences strong clinical demand. However, sustained usage largely depends on pet owners' ability to manage recurring costs that exceed those of standard pet food. According to Animal Medicines Australia, in 2025, 12% of pet owners required financial assistance for veterinary care, while 18% of cat owners and 14% of dog owners reported making health-related compromises, such as delaying check-ups or reducing medications. Similarly, PetSure Pty Ltd’s 2024 Pet Health Monitor revealed that half of the surveyed pet owners reduced their spending on veterinary care, with 21% delaying visits to observe the situation before seeking treatment[3]Source: PetSure, “PetSure Launches 2024 Pet Health Monitor Report,” petsure.com.au. This trend is critical because prescription diets are most effective when combined with continuous follow-up care, rather than being used solely during acute health episodes. When food, consultation, medication, and insurance premiums are paid in a single month, some households revert to maintenance diets despite veterinary recommendations. As a result, affordability remains a key limitation on volume growth in the Australia pet veterinary diets market, particularly outside high-income metropolitan areas.

Prescription and Labeling Compliance Limits Digital Conversion

The regulatory environment in Australia facilitates access to pet veterinary diets but undermines long-term compliance in certain parts of the distribution channel. The Australian pet veterinary diets market is distinctive, as therapeutic diets can be distributed through online and retail channels without a stringent national prescription enforcement framework. In 2024, ABC reported that Australia lacked federal pet food regulations, with discussions on mandatory standards at the state and territory level still under consideration. While easier access supports initial purchase conversions, it disrupts the clinical connection between the recommending veterinarian and the pet owner during subsequent reorders. This weakens the feedback loop that typically enhances adherence and brand loyalty. In contrast, Virbac’s 2025 launch of Vikaly in Europe demonstrates a model where medicated feed operates within a well-defined prescription and dispensing framework. Until Australia adopts a more unified national approach, the pet veterinary diets market will continue to weigh the benefits of channel convenience against the challenges posed by less-regulated therapeutic diet sales.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Product: Digestive and Oral Health Drive the Growth

Digestive Sensitivity accounted for 17.7% of the Australia pet veterinary diets market size in 2025, while Oral Care Diets are projected to achieve the fastest growth, with a 9% CAGR through 2031. Digestive products remain the largest category, as gastrointestinal issues are among the most common claims for insured pets in Australia. This provides veterinarians with a consistent rationale for recommending dietary interventions. Oral care diets are experiencing faster growth as dental disease is increasingly recognized as a broader health issue rather than merely a cosmetic concern. This shift has encouraged pet owners to adopt preventive diets for extended periods. Renal and urinary tract disease diets remain stable in volume, as these conditions often require lifelong nutritional management after diagnosis. According to PetSure Pty Ltd, urinary tract disorders were among the most expensive conditions for cats aged 1-8 years in 2024, with average treatment claims of AUD 1,519 (USD 964) per episode, driving demand for diets aimed at reducing recurrence.

The market is increasingly moving toward multi-condition formulations, which reduce the need for separate diets within a single household. For example, Hill’s launched Prescription Diet Metabolic + j/d in April 2026, followed by k/d + Derm Complete and k/d + z/d Hydrolyzed in June 2026. These products address two conditions within one feeding plan, enhancing convenience and improving compliance, particularly for older pets with overlapping health issues. Additionally, Royal Canin renewed its obesity research partnership in March 2026, and Dechra Pharmaceuticals PLC introduced SPECIFIC Heart and Kidney Support Hydrolysed diets in April 2026, highlighting the continued focus on obesity and renal care as key product areas. While diabetes and other veterinary diets remain smaller segments, they are gaining importance as feline obesity and related metabolic conditions receive increased clinical attention from veterinarians.

By Pets: Canine Value Coexists with Significant Feline Share Gain

Dogs accounted for 43.6% of the Australia pet veterinary diets market share in 2025, while cats are projected to grow at a CAGR of 8.7% through 2031. Dogs remain the largest segment, accounting for 49% of pet-owning households in Australia, or 7.4 million dogs. This strong installed base supports consistent demand for canine diets, driven by needs such as obesity management, digestive care, joint support, and allergy management. The segment benefits from an already established prescription pattern. Cats, however, are experiencing faster growth due to past underdiagnosis, creating opportunities for new prescriptions in areas such as renal, urinary, and metabolic care. According to Animal Medicines Australia, 75% of cats visited a veterinarian in 2025, compared with 89% of dogs. This indicates a larger, untreated feline population, which contributes to the segment's growth potential. The gap in veterinary visits is significant because cats are disproportionately affected by conditions requiring long-term dietary management. Urinary disorders and chronic kidney disease, in particular, drive repeat purchases once diagnosed, providing the feline segment with a strong recurring revenue profile.

The Australia pet veterinary diets market also includes a small "Other Pets" category, encompassing birds, rabbits, and small mammals. However, product development in this category remains limited. Growth in this segment is likely to remain constrained until formulation standards, clinical guidance, and channel support for these species are further developed. Virbac’s acquisition of Thyronorm in December 2025 highlights the increasing integration of therapeutic nutrition and veterinary diets in feline care. This acquisition strengthens Virbac’s position in managing feline diseases and underscores the growing focus on specialized nutrition for cats. However, growth outside the cat and dog segments is estimated to remain limited in the near term due to the lack of advancements in supporting smaller species.

By Distribution Channel: Supermarket Reach Offsets Online Surge

Supermarkets/Hypermarkets accounted for 58.7% of the Australia pet veterinary diets market size in 2025, while the online channel is projected to grow at a CAGR of 10.6% through 2031. Large grocery chains provide significant visibility for the category and facilitate entry-level purchases of therapeutic and functional diets, which explains their dominant market share. In contrast, the online channel is expanding rapidly due to its alignment with the recurring nature of chronic condition treatments and the 30-90 day refill cycles typical of prescription feeding. For instance, Purina’s decision to offer its complete Pro Plan Veterinary Diets range on Amazon in May 2024 highlights how major suppliers are enhancing digital access to clinical nutrition. Specialty stores remain strategically relevant as they offer a broader product assortment along with in-store veterinary support and knowledgeable staff.

Distribution networks are becoming increasingly interconnected across wholesale, clinic, and retail systems. For example, EBOS Group Limited’s integration of its branded pet food business with the SVS veterinary wholesale network has improved inventory flow and visibility, linking clinic demand with downstream fulfillment. This integration benefits the Australia pet veterinary diets market, as reliable availability and simplified reordering are critical for prescription feeding. However, the rapid growth of digital channels poses challenges, such as potentially reducing margins for clinic-dispensed sales, which may discourage some practices from promoting specific brands. Despite this, the convenience, regional accessibility, and subscription-based purchasing behavior are anticipated to sustain online channels as the fastest-growing distribution segment through 2031.

Geography Analysis

Australia is one of the strongest veterinary diet markets in the Asia-Pacific region, driven by high pet ownership rates, a focus on premium pet care, and widespread acceptance of medically guided nutrition. The Australian pet veterinary diet market is expanding faster than the broader domestic pet food category, indicating a genuine shift toward condition-specific feeding rather than simple market inflation. With a 73% household pet ownership rate and 31.6 million companion animals, Australia provides a substantial base for veterinary care and demand for therapeutic foods. This base is particularly valuable as prescription diets rely on recurring needs rather than occasional discretionary purchases.

There is a clear division between metropolitan demand centers and regional areas in Australia. Cities such as Sydney, Melbourne, Brisbane, and Perth account for the majority of prescription diet volumes due to their dense clinic networks, higher income levels, and better access to pet insurance and specialty retail outlets. While pet ownership is also strong in regional areas, the adoption of therapeutic diets is limited by fewer clinics and longer travel times for diagnostics. Mars, Incorporated demonstrated confidence in the domestic market by announcing a AUD 112.6 million (USD 71.5 million) investment in its Wodonga cat food facility in 2024, which enhances local supply capacity.

The regulatory framework presents a unique factor for the Australian market. In 2024, ABC reported that there was no federal pet food regulation in place, and mandatory adoption of AS5812 standards was still under discussion. This regulatory gap facilitates easier market access in the short term, particularly for online sales, but it also raises concerns about uneven compliance and potential quality issues. If mandatory standards are implemented, larger multinational companies may benefit due to their established manufacturing and compliance systems in other markets. Consequently, the Australian pet veterinary diets market could become more concentrated over time, as smaller local brands may face higher costs to remain competitive under stricter regulations.

Competitive Landscape

The Australian pet veterinary diets market is moderately consolidated, with the top five players being Mars, Incorporated, Nestlé S.A. (Purina), Colgate-Palmolive Company (Hill’s Pet Nutrition, Inc.), EBOS Group Limited, and The Real Pet Food Company. The market is dominated by global brands that have established strong veterinary education programs, clinical research partnerships, and extensive therapeutic diet portfolios over the years. Mars, Incorporated through Royal Canin, and Colgate-Palmolive Company, through Hill’s Pet Nutrition, continue to lead in the clinical segment by combining brand trust with robust professional channel relationships. This advantage is challenging for smaller entrants to replicate quickly, even when they offer competitive products.

By 2026, competition is increasingly focused on product depth and channel control rather than mere shelf presence. Hill’s Pet Nutrition launched two combination diet platforms in 2026, including Metabolic + j/d and a kidney plus skin support line, emphasizing multi-condition feeding. Royal Canin is also maintaining a steady innovation pipeline, previewing therapeutic product launches at VMX 2026 and renewing its obesity research partnership in March 2026. Additionally, Colgate-Palmolive Company (Hill's Pet Nutrition, Inc.)’s acquisition of Prime100 for AUD 500 million (USD 317.5 million) in early 2025 strengthens its position in the fresh pet food segment including therapeutic food, bridging clinical feeding with premium fresh formats.

The next tier of competition is shaped by companies employing alternative market strategies. EBOS Group Limited leverages its distribution strength and veterinary wholesale access, while Virbac is enhancing its role in nutrition-adjacent areas through medicine-led disease management. Virbac’s acquisition of Thyronorm and the launch of Vikaly demonstrate how therapy, diagnosis, and nutrition are becoming more integrated, particularly in feline care. Domestic brands still have opportunities in the functional therapeutic middle tier but require stronger veterinary access and more clinical validation to compete effectively with market leaders. Overall, the Australia pet veterinary diets market remains open to selective growth opportunities. However, sustained leadership in this market depends on clinical credibility, continuous innovation, and efficient multi-channel fulfillment strategies.

Australia Pet Veterinary Diets Industry Leaders

Mars Incorporated

Colgate-Palmolive Company (Hill’s Pet Nutrition, Inc.)

Nestlé S.A. (Purina)

EBOS Group Limited

The Real Pet Food Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Hill's Pet Nutrition launched Prescription Diet k/d + Derm Complete and k/d + z/d Hydrolyzed, 2 new combination kidney and skin sensitivity formulations featuring ActivBiome+ Kidney Defense technology. These products target multi-condition management in cats and dogs.

- April 2026: Dechra Pharmaceuticals PLC launched new SPECIFIC Heart and Kidney Support Hydrolyzed dry diets for dogs and cats, targeting the growing segment of chronic kidney disease management.

- April 2026: Hill's Pet Nutrition, Inc. launched Prescription Diet Metabolic + j/d, the first feline formulation combining weight management and joint mobility support in a single therapeutic diet

Australia Pet Veterinary Diets Market Report Scope

Pet veterinary diets (also known as therapeutic or prescription diets) are specialized, scientifically formulated pet foods designed to treat, prevent, or manage specific medical conditions.

The Australia Pet Veterinary Diets Market Report is segmented by sub product (Diabetes, Renal, Urinary Tract Disease, Digestive Sensitivity, Oral Care Diets, Derma Diets, Obesity Diets, and Others), by pets (Cats, Dogs, and Other Pets), by distribution channel (Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets, and others). The market forecasts are provided in terms of value in USD and volume in metric tons.

| Diabetes |

| Renal |

| Urinary Tract Disease |

| Digestive Sensitivity |

| Oral Care Diets |

| Derma Diets |

| Obesity Diets |

| Other Veterinary Diets |

| Cats |

| Dogs |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/ Hypermarkets |

| Other Channels |

| By Sub Product | Diabetes |

| Renal | |

| Urinary Tract Disease | |

| Digestive Sensitivity | |

| Oral Care Diets | |

| Derma Diets | |

| Obesity Diets | |

| Other Veterinary Diets | |

| By Pets | Cats |

| Dogs | |

| Other Pets | |

| By Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/ Hypermarkets | |

| Other Channels |

Key Questions Answered in the Report

What is the forecast outlook for the Australia pet veterinary diets market through 2031?

The Australia pet veterinary diets market is forecast to rise from USD 390.30 million in 2026 to USD 584.70 million by 2031 at an 8.40% CAGR.

Which sub product category leads revenue in Australia pet veterinary diets?

Digestive sensitivity leads the category with 17.7% share in 2025, supported by the high frequency of gastrointestinal conditions in insured pets.

Which pet type is growing fastest in veterinary diets market in Australia?

Cats are the fastest-growing pet type, with an estimated 8.7% CAGR through 2031, driven by stronger diagnosis of renal, urinary, and metabolic conditions.

Why is online distribution growing quickly for veterinary diets in Australia?

The Online Channel is projected to grow at 10.6% CAGR because therapeutic diets fit refill behavior well and improve access for regional owners.

What is the main challenge limiting wider use of therapeutic pet diets?

Price remains the biggest barrier, because therapeutic diets often need to be purchased alongside consultations, diagnostics, medication, and insurance costs.

Page last updated on: