Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

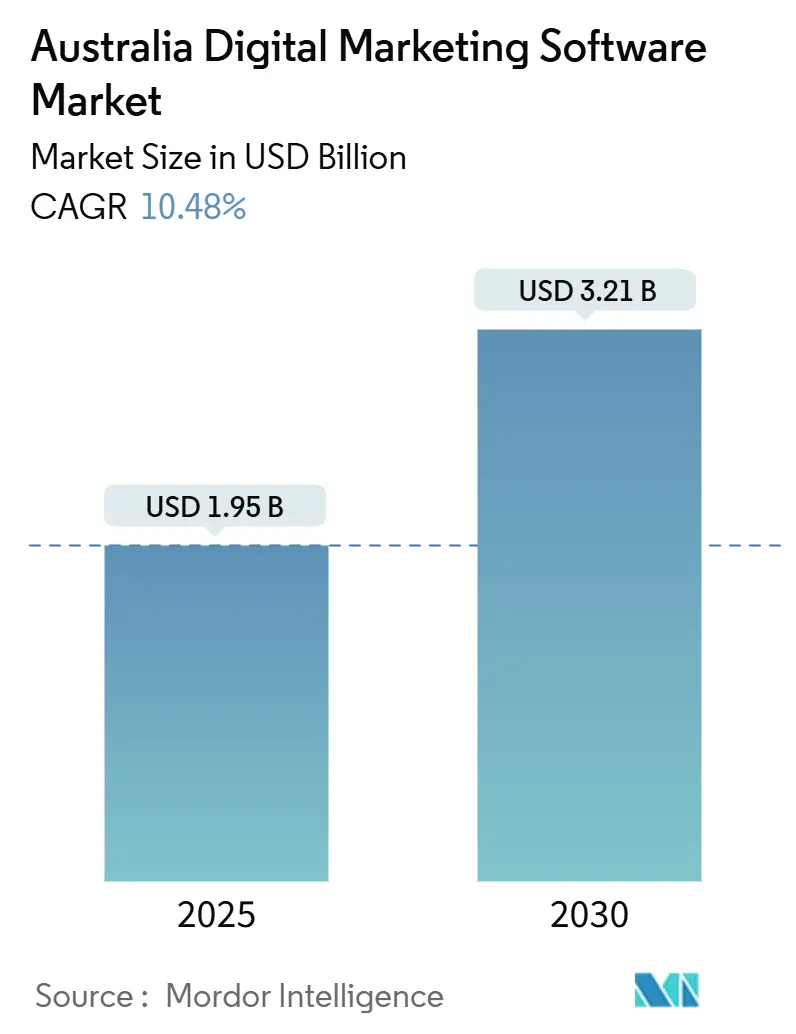

| Market Size (2025) | USD 1.95 Billion |

| Market Size (2030) | USD 3.21 Billion |

| Growth Rate (2025 - 2030) | 10.48% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Digital Marketing Software Market Analysis by Mordor Intelligence

The Australia digital marketing software market size stands at USD 1.95 billion in 2025 and is projected to climb to USD 3.21 billion by 2030, supported by a 10.48% CAGR. Growing cloud-native adoption, generous government grant programs, and surging demand for real-time analytics are reshaping vendor roadmaps and driving changes in enterprise procurement behavior. Small and medium enterprises are moving faster than large organizations thanks to software-as-a-service pricing, self-service workflows, and simplified onboarding. Retail and e-commerce remain the largest spending vertical, yet healthcare outpaces all others as telehealth providers invest in compliant engagement platforms. Intensifying mobile commerce, first-party data strategies aimed at offsetting the deprecation of cookies, and the emergence of in-country data centers from global vendors are transforming compliance infrastructure into a competitive advantage. Headwinds include fragmented state-level privacy regulations, a widening talent shortage in advanced marketing technology (martech) skill sets, and budget compression across brick-and-mortar retail chains.

Key Report Takeaways

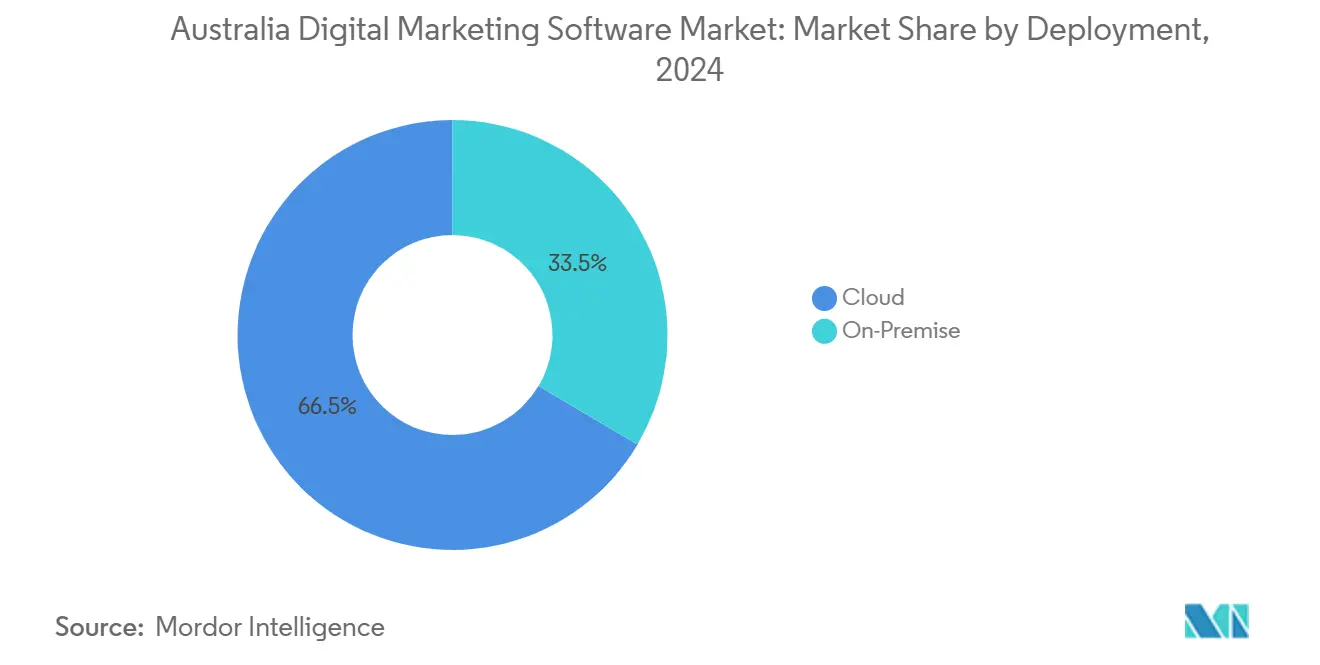

- By deployment, cloud platforms captured 66.50% of Australia digital marketing software market share in 2024 and are growing at a 12.40% CAGR through 2030.

- By software type, marketing automation experienced the fastest expansion rate, with a 14.80% CAGR between 2025 and 2030, despite email marketing retaining the largest revenue share of 28.30% in 2024.

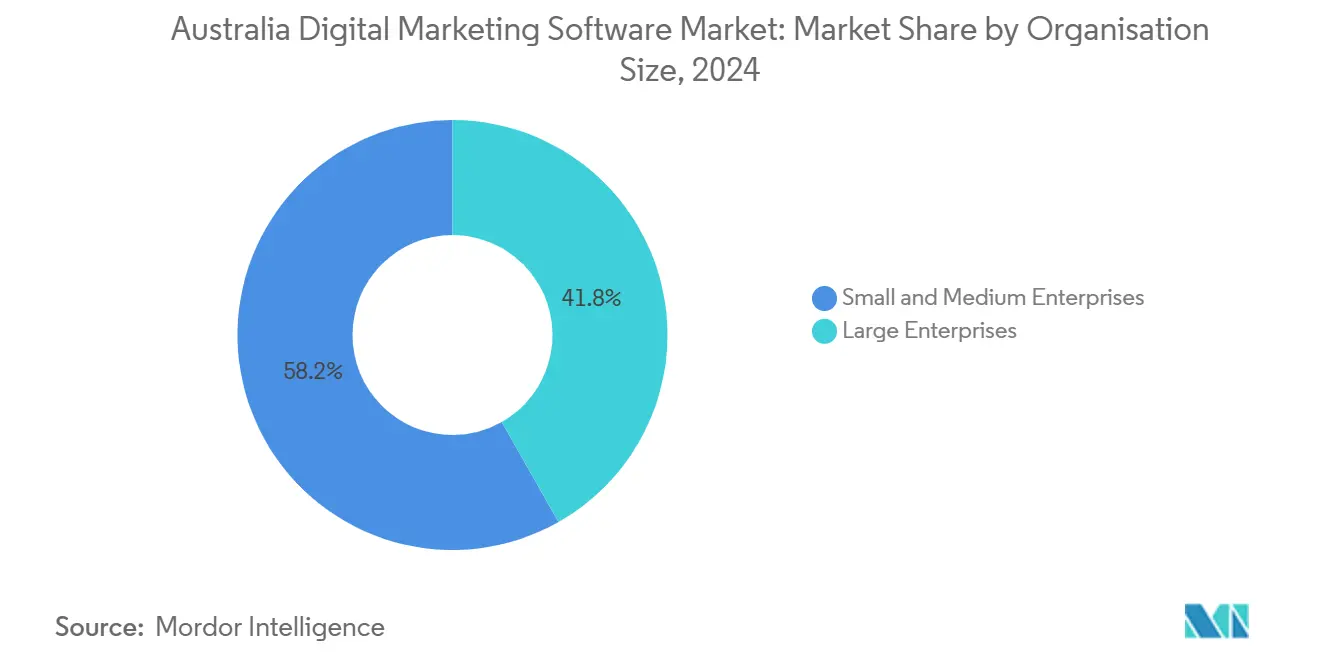

- By organisation size, small and medium enterprises commanded 58.20% of Australia digital marketing software market size in 2024 and are advancing at a 13.90% CAGR to 2030.

- By end-user industry, healthcare is projected to progress at a 15.40% CAGR through 2030, while retail and e-commerce remained the revenue leaders in 2024 at 24.50%.

Australia Digital Marketing Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Cloud Migration by SMBs | +2.1% | National, with a concentration in New South Wales and Victoria | Medium term (2-4 years) |

| Proliferation of Mobile Commerce Platforms | +1.8% | National, with higher penetration in metropolitan areas | Short term (≤ 2 years) |

| Intensifying Demand for Real-Time Customer Analytics | +1.5% | National, led by the financial services and retail sectors | Medium term (2-4 years) |

| Rise of Self-Service Martech Ecosystems | +1.3% | National, particularly among SMEs and startups | Long term (≥ 4 years) |

| Government Support for SME Digitalisation Grants | +0.9% | National, with targeted programs in regional areas | Short term (≤ 2 years) |

| Growing Adoption of Headless CMS Architectures | +0.7% | National, concentrated in the e-commerce and media sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Cloud Migration by SMBs

Small and medium-sized enterprises are embracing software-as-a-service to avoid capital expenditures and achieve elastic scalability. Microsoft reported that Australian firms adopted cloud marketing tools at a faster rate than the broader Asia-Pacific average, with customer relationship management and email modules leading the way.[1]Microsoft Australia newsroom, “Australian Businesses Accelerating Cloud Adoption,” news.microsoft.comTelstra and Omdia found that 68% of local SMBs intended to increase their cloud budgets in 2024, although 42% still expressed data-security concerns. The Digital Solutions program granted AUD 18.6 million (USD 12.46 million) in its second round, slicing typical migration timelines from three years to just 18 months for eligible firms. Vendors operating Australian-hosted, ISO 27001-certified data centers are therefore positioned to capture an outsized share.

Proliferation of Mobile Commerce Platforms

Mobile transactions reached AUD 35 billion (USD 23.45 billion) in 2024, accounting for 25% of national online purchases.[2]Boku, “Mobile Commerce in Australia,” boku.comAustralia Post reported that 9.5 million households shopped online, and half of Gen Z and millennial consumers made weekly purchases via apps, compelling retailers to prioritize mobile-first outreach. Buy-now-pay-later options embedded in checkout flows generated AUD 16 billion (USD 10.72 billion) in volume and increased conversion rates by 30% compared to credit-card-only flows. Shopify’s Oracle tie-up now synchronizes mobile-commerce data with enterprise resource planning (ERP) backends, enabling real-time inventory visibility during flash sales.

Intensifying Demand for Real-Time Customer Analytics

Enterprises are transitioning away from batch-based reporting in favor of streaming architectures. National Australia Bank’s decisioning engine evaluates 150 next-best actions per interaction, delivering tailored product prompts in milliseconds.[3]NAB, “NAB Real-Time Decisioning,” nab.com.auKmart Australia utilized Tealium and Braze to trigger messages on live browse and cart abandonment events, achieving a 20-fold response increase. Adobe’s partnership with Snowflake introduced federated audience queries that run within customer data warehouses, solving latency and data duplication friction.

Rise of Self-Service Martech Ecosystems

Low-code platforms enable marketers to build campaigns without the need for professional developers. Canva’s enterprise suite added workflow automation and brand libraries, drawing 230 million global monthly active users and USD 2.3 billion in revenue by 2024. HubSpot revealed that 78% of Australian go-to-market teams used generative artificial intelligence features to slash lead-nurture setup from two weeks to two days. Roy Morgan’s WorkSpace further democratized segmentation by letting marketers write natural-language prompts rather than SQL commands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Data Privacy Regulations Across States | -1.2% | National, with varying enforcement intensity by state | Medium term (2-4 years) |

| Talent Shortage in Advanced Martech Skillsets | -1.0% | National, most acute in regional areas | Long term (≥ 4 years) |

| Budget Compression in the Traditional Retail Sector | -0.8% | National, concentrated in brick-and-mortar retail | Short term (≤ 2 years) |

| Increasing Ad-Blocking and Cookie-Deprecation Impact | -0.6% | National, affecting display and programmatic advertising | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Data Privacy Regulations Across States

The federal Privacy Act sets a baseline, yet state statutes create divergent breach-notification deadlines and consent thresholds. The Office of the Australian Information Commissioner highlighted potential penalties of AUD 50 million or 30% of turnover for violations, prompting marketers to adopt the strictest common denominator nationwide.[4]OAIC, “Privacy Act Review,” oaic.gov.auDisparate opt-in rules for artificial intelligence training in New South Wales versus Victoria add complexity to integration, causing 38% of campaigns to slip their schedules in 2024, according to the Interactive Advertising Bureau Australia. Vendors supplying jurisdiction-aware consent management solutions are in high demand; however, structural fragmentation is likely to persist until full federal harmonization is achieved.

Talent Shortage in Advanced Martech Skillsets

LinkedIn’s 2024 Workplace Learning Report revealed that 60% of Australian marketers are not proficient in artificial intelligence tools, and 52% struggle to interpret predictive analytics. RMIT University estimates that the country will require 156,000 additional technology workers by 2027; however, graduation rates lag behind the needs by 40%. Regional businesses are hardest hit, with 87% reporting difficulty attracting martech specialists, often resorting to generalist staff who struggle with multi-channel attribution and real-time decisioning workflows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Platforms Deepen Dominance

Cloud captured 66.50% of Australia digital marketing software market share in 2024, advancing toward a 12.40% CAGR through 2030. Massive swings in seasonal demand, limited in-house IT resources, and grant-funded incentives continue to steer SMBs to cloud subscriptions that launch in days rather than months. Braze’s Sydney data center, which has been live since January 2025, satisfies the Privacy Act residency requirements while preserving global feature parity. Headless architectures reinforce cloud gravity by decoupling content from presentation and pushing microservices via application programming interfaces. WP Engine reported a 73% increase in headless usage among Australian organizations in 2024, a 14-point jump from 2021. Highly regulated banking and healthcare verticals maintain hybrid estates; yet, even they place campaign orchestration and personalization layers in public clouds to accelerate iteration cycles.

Resistance persists among risk-averse enterprises concerned about sovereignty, although ISO 27001-certified local hosting now mitigates many of these objections. Telstra’s survey noted security as the top barrier for 42% of SMB respondents, creating a premium for vendors with clear compliance roadmaps. The Digital Solutions program’s AUD 18.6 million (USD 12.46 million) subsidy continues to compress migration timelines, steering laggards toward cloud-native stacks and fueling near-term demand spikes.

By Software Type: Marketing Automation Seizes Momentum

Email marketing retained a 28.30% revenue share in 2024, yet marketing automation is expanding at a 14.80% CAGR, reflecting the pivot from one-off blasts to orchestrated, behavior-triggered journeys. Klaviyo reported that 80% of Australian marketers expected to increase automation budgets, although platform costs and disconnected toolchains still pose hurdles. Social customer relationship management and web analytics suites have evolved to incorporate predictive scoring, but specialized orchestration engines now mediate channel selection in real-time. National Australia Bank’s 150-action decision loop illustrates how sophisticated financial institutions blend automation with legacy customer relationship management cores.

Convergence trends are blurring historically distinct categories, such as e-commerce enablement and content management systems. Headless API layers let retailers surface product details and promotions from a single backend, reducing duplication and shortening campaign cycles. Iterable’s Nova release automatically adjusts send time and channel based on predicted engagement probability, raising the performance bar across the cohort.

By Organisation Size: SMEs Propel Spending Velocity

Small and medium-sized enterprises accounted for 58.20% of Australia's digital marketing software market size in 2024 and are projected to grow at a 13.90% CAGR through 2030. Grant programs reimburse up to half of eligible software spend, shortening payback periods and lowering risk thresholds. Canva’s template libraries and HubSpot’s embedded design integration slash creative bottlenecks, enabling non-technical teams to set up campaigns without relying on agencies. The partnership also eliminates context switching, further narrowing the capability gap between resource-constrained businesses and large corporations.

Enterprises still maintain complex, multi-brand portfolios that require enterprise-grade access controls, cross-domain identity resolution, and dedicated customer success. Adobe’s federated audience collaboration with Microsoft Azure offsets data duplication costs for high-scale retailers while complying with residency requirements. However, the advanced martech talent shortage penalizes smaller regional firms, many of whom must settle for rudimentary implementations that underutilize platform potential.

By End-User Industry: Healthcare Accelerates, Retail Holds Lead

Retail and e-commerce accounted for 24.50% of revenue in 2024, but tightening discretionary spending is expected to temper future growth. Healthcare, by contrast, is projected to post a 15.40% CAGR through 2030, driven by the mainstream acceptance of telehealth and the rising demand for personalized wellness journeys. Healthdirect Australia facilitated 95 million sessions in 2024, relying on compliant engagement channels for appointment reminders and post-discharge monitoring. Private hospitals install automation platforms that comply with Australian Privacy Principles to manage elective procedure waitlists and foster relationships with referring physicians.

The banking and insurance segments prioritize real-time analytics to reduce churn. The Insurance Council of Australia reported a 12-percentage-point improvement in renewal retention for carriers running real-time decisioning rather than batch offers. Media companies merge subscription analytics with content management, while manufacturing and automotive sectors integrate customer relationship management into distributor and dealer systems to orchestrate omnichannel lead nurturing.

Geography Analysis

New South Wales and Victoria host the largest installed base of digital marketing software market deployments in Australia, reflecting their density of corporate headquarters and digital talent. Regional grant programs aim to bridge adoption gaps: Western Australia’s Local Capability Fund deployed AUD 6.6 million (USD 4.42 million) to subsidize cloud tools for mining services, agriculture, and tourism businesses. Queensland’s tourism operators utilize marketing automation to manage peaks and troughs in seasonal demand, synchronizing booking platforms with email, SMS, and push channels in unified journeys.

The Australian Capital Territory and South Australia act as sandboxes for artificial intelligence pilots via public-sector and university consortia. Tasmania and the Northern Territory struggle with broadband constraints; however, Digital Solutions vouchers enable micro-enterprises to access cloud-hosted email and social media management, thereby circumventing the need for capital-intensive infrastructure. Privacy Act updates in 2024 harmonized core federal requirements, yet state-level breach timelines still vary, causing multi-state retailers to follow the strictest standard to avoid multimillion-dollar fines.

Sydney’s data center boom crystallizes the strategic importance of local hosting. Braze and HubSpot both activated facilities in 2025, reducing latency for real-time personalization and eliminating legal friction around cross-border transfers. Mobile commerce’s AUD 35 billion (USD 23.45 billion) footprint demands analytics that stitch app journeys, progressive web apps, and responsive sites, prompting vendors to emphasize unified identity resolution across device types.

Competitive Landscape

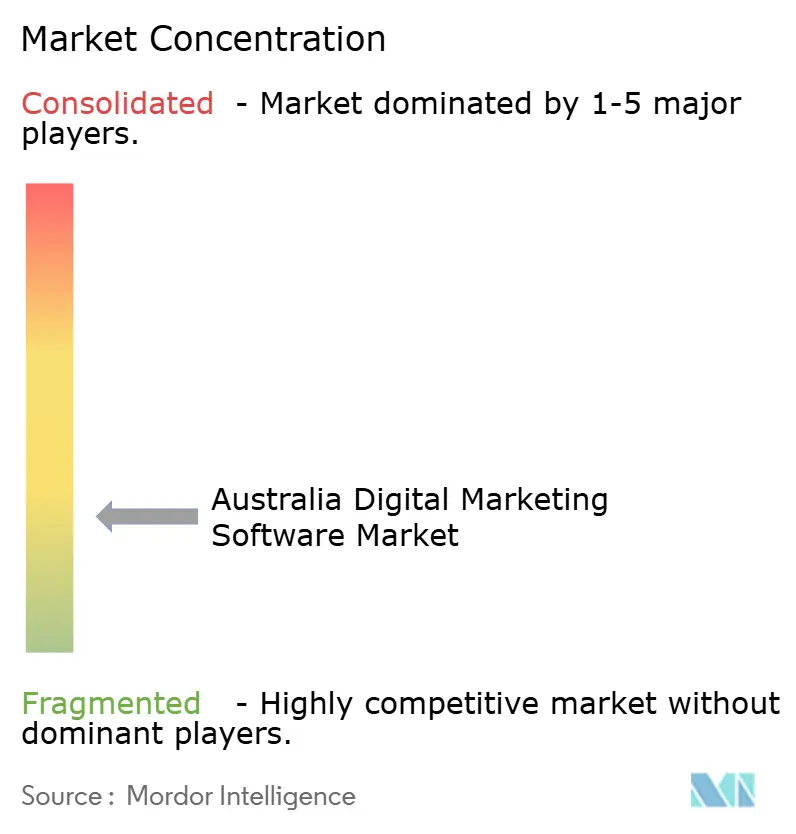

The field remains fragmented, scoring high on rivalry as global suites collide with niche specialists. Adobe, Salesforce, and HubSpot maintain top-down platform breadth, while Canva, Campaign Monitor, and Klaviyo carve audience-specific value through focused experiences. Strategy converges on three pillars: local data centers to satisfy privacy mandates, partnerships for end-to-end workflows, and artificial intelligence features that offset talent scarcity.

Adobe’s Snowflake partnership reduces integration costs and latency, allowing marketers to run secure queries within existing data warehouses. Canva’s acquisition of Affinity in March 2024 expanded its design surface from templates into professional vector editing, posing new competition to Adobe Creative Cloud.

Emerging disruptors, such as MoEngage and Iterable, emphasize predictive journey orchestration, dynamically shifting the channel mix based on user behavior patterns. Retail budget compression incentivizes full-stack suites that consolidate vendor count—an opportunity that favors Adobe Experience Cloud and Salesforce over point solutions. Meanwhile, healthcare-ready automation platforms that embed fine-grained consent and data classification controls remain a white-space ripe for specialized entrants.

Australia Digital Marketing Software Industry Leaders

Adobe Inc.

Salesforce Inc.

HubSpot Inc.

Oracle Corporation

SAS Institute Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: HubSpot opened a Sydney data center and partnered with Canva to embed design tools directly into marketing workflows.

- January 2025: Braze launched a Sydney data center to meet the requirements of the Privacy Act regarding residency.

- January 2025: Shopify introduced a Partner Solutions Center to accelerate local integration projects.

Australia Digital Marketing Software Market Report Scope

The Australia Digital Marketing Software Market Report is Segmented by Deployment (On-Premise, Cloud), Software Type (Email Marketing Software, Customer Relationship Management Software, Social CRM and Social Media Management, Web and Marketing Analytics, Marketing Automation Platforms, E-Commerce Enablement Tools, Content Management Systems), Organisation Size (Large Enterprises, Small and Medium Enterprises), End-User Industry (Information Technology, Telecom, Banking Financial Services and Insurance, Media and Entertainment, Retail and E-Commerce, Manufacturing, Healthcare, Automotive), and Geography (Australia). The Market Forecasts are Provided in Terms of Value (USD).

By Deployment

| On-Premise |

| Cloud |

By Software Type

| Email Marketing Software |

| Customer Relationship Management (CRM) Software |

| Social CRM and Social Media Management |

| Web and Marketing Analytics |

| Marketing Automation Platforms |

| E-Commerce Enablement Tools |

| Content Management Systems (CMS) |

By Organisation Size

| Large Enterprises |

| Small and Medium Enterprises |

By End-User Industry

| Information Technology |

| Telecom |

| Banking, Financial Services and Insurance |

| Media and Entertainment |

| Retail and E-Commerce |

| Manufacturing |

| Healthcare |

| Automotive |

| By Deployment | On-Premise |

| Cloud | |

| By Software Type | Email Marketing Software |

| Customer Relationship Management (CRM) Software | |

| Social CRM and Social Media Management | |

| Web and Marketing Analytics | |

| Marketing Automation Platforms | |

| E-Commerce Enablement Tools | |

| Content Management Systems (CMS) | |

| By Organisation Size | Large Enterprises |

| Small and Medium Enterprises | |

| By End-User Industry | Information Technology |

| Telecom | |

| Banking, Financial Services and Insurance | |

| Media and Entertainment | |

| Retail and E-Commerce | |

| Manufacturing | |

| Healthcare | |

| Automotive |

Key Questions Answered in the Report

How fast is spending on cloud-based marketing tools growing in Australia?

Cloud deployment is expanding at a 12.40% CAGR between 2025 and 2030, driven by government subsidies and the shift away from on-premises systems.

Which software category is scaling quickest?

Marketing automation platforms are growing at a 14.80% CAGR as enterprises transition from one-off email blasts to multi-touch journeys orchestrated in real-time.

Why are SMEs outpacing large enterprises in adoption?

Government rebates cover up to half of eligible costs, and self-service platforms like Canva and HubSpot eliminate the need for dedicated IT or design staff.

What is driving healthcare investment?

Telehealth, patient engagement mandates, and privacy-compliant automation tools, guided by Australian Privacy Principles, propel healthcare to a 15.40% CAGR through 2030.

How do fragmented state privacy laws affect marketers?

Brands must meet the most stringent breach-notification and consent standards nationwide, which prolongs implementation timelines and elevates demand for automated compliance tools.

Which vendors recently established Australian data centers?

Braze and HubSpot both launched Sydney facilities in 2025, joining Adobe and Microsoft in offering in-country data residency for real-time personalization workloads.

Page last updated on: