Australia Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

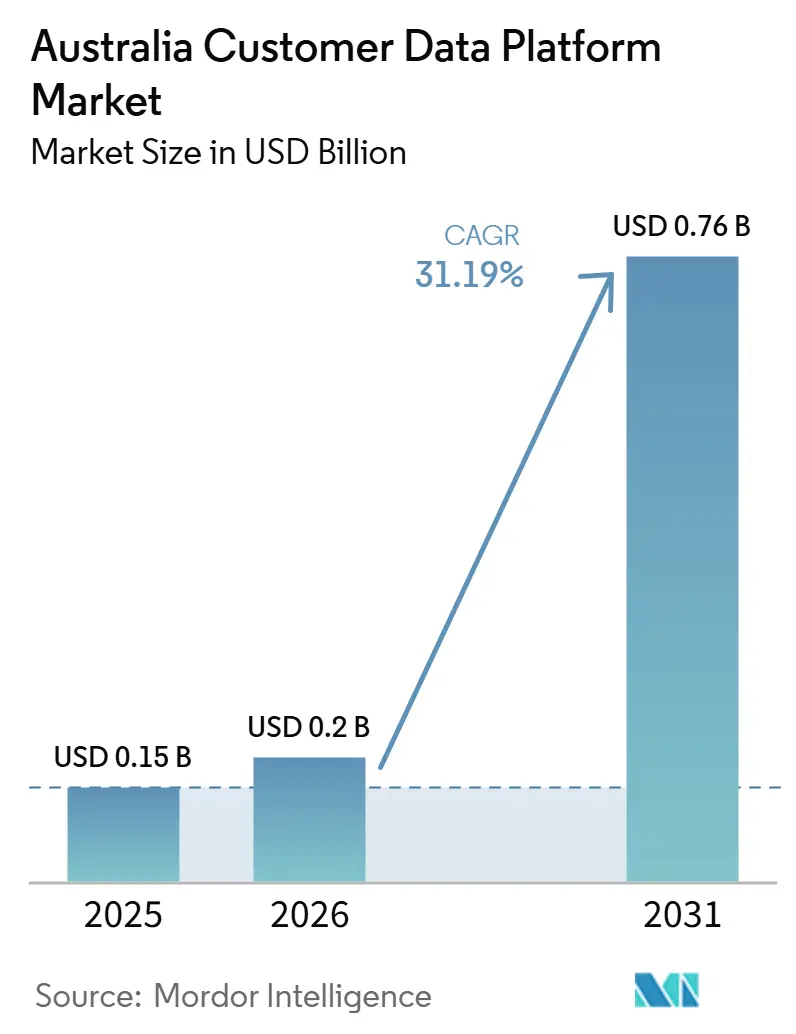

| Base Year Market Size (2025) | USD 0.15 Billion |

| Market Size (2026) | USD 0.2 Billion |

| Market Size (2031) | USD 0.76 Billion |

| Growth Rate (2026 - 2031) | 31.19% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Customer Data Platform Market Analysis by Mordor Intelligence

The Australia customer data platform market size is expected to grow from USD 0.15 billion in 2025 to USD 0.20 billion in 2026 and is forecast to reach USD 0.76 billion by 2031 at 31.19% CAGR over 2026-2031. This growth path reflects a clear shift in how organizations in Australia treat customer information, with the focus moving from campaign support tools to governed identity infrastructure. Privacy reform has made consent management, automated decision transparency, and breach accountability more central to platform selection, which is raising the value of systems that unify customer records and activation rules in one environment. The move toward first-party data has also become more urgent as third-party tracking loses reliability, which is pushing enterprises to organize behavioral, transactional, and loyalty data in a more durable way. AI-led orchestration is strengthening demand because real-time decisioning depends on clean customer profiles, current data flows, and stronger control over how information is used. Competitive activity remains centered on a small group of global vendors, while spending discipline, integration difficulty, and talent shortages continue to shape how quickly the Australia customer data platform market moves from pilots to scaled rollouts.

Key Report Takeaways

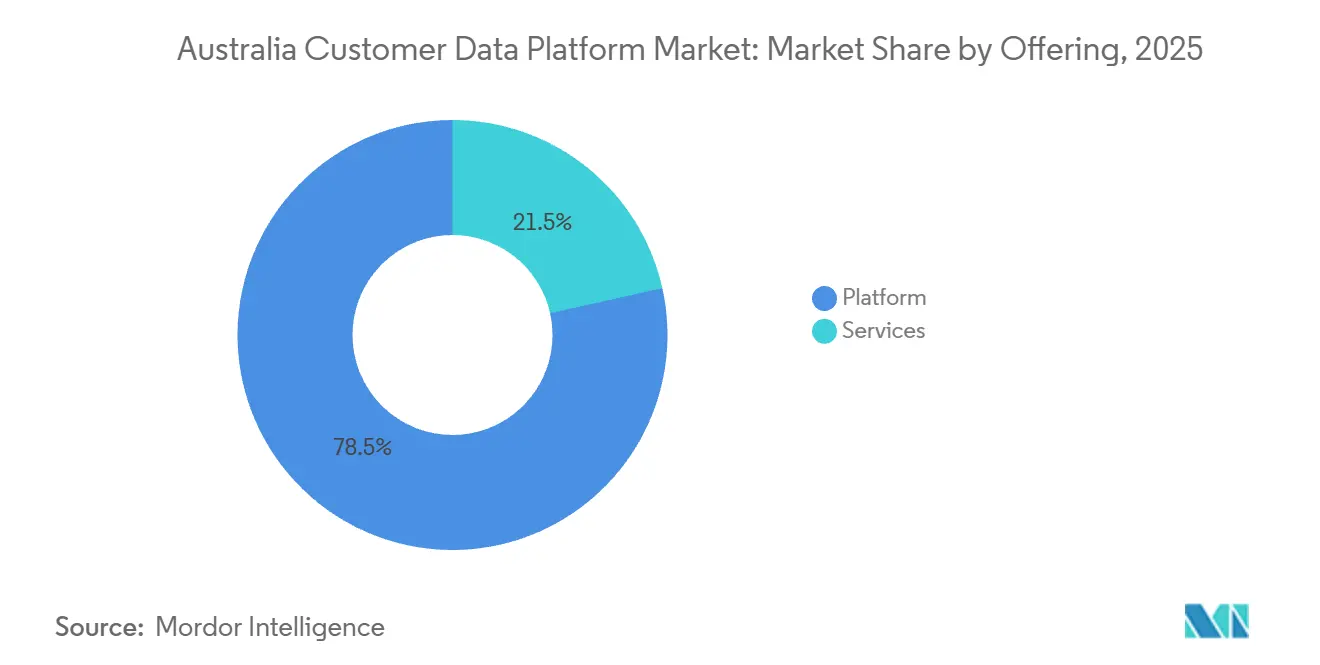

- By offering, platform led with a 78.50% of the Australia customer data platform market share in 2025, while services are projected to expand at a 32.62% CAGR through 2031.

- By deployment mode, cloud accounted for 66.41% of the Australia customer data platform market share in 2025, while hybrid is projected to grow at a 33.54% CAGR through 2031.

- By organization size, large enterprises held a 71.84% share in 2025, while SMEs are projected to record the highest CAGR at 32.16% through 2031.

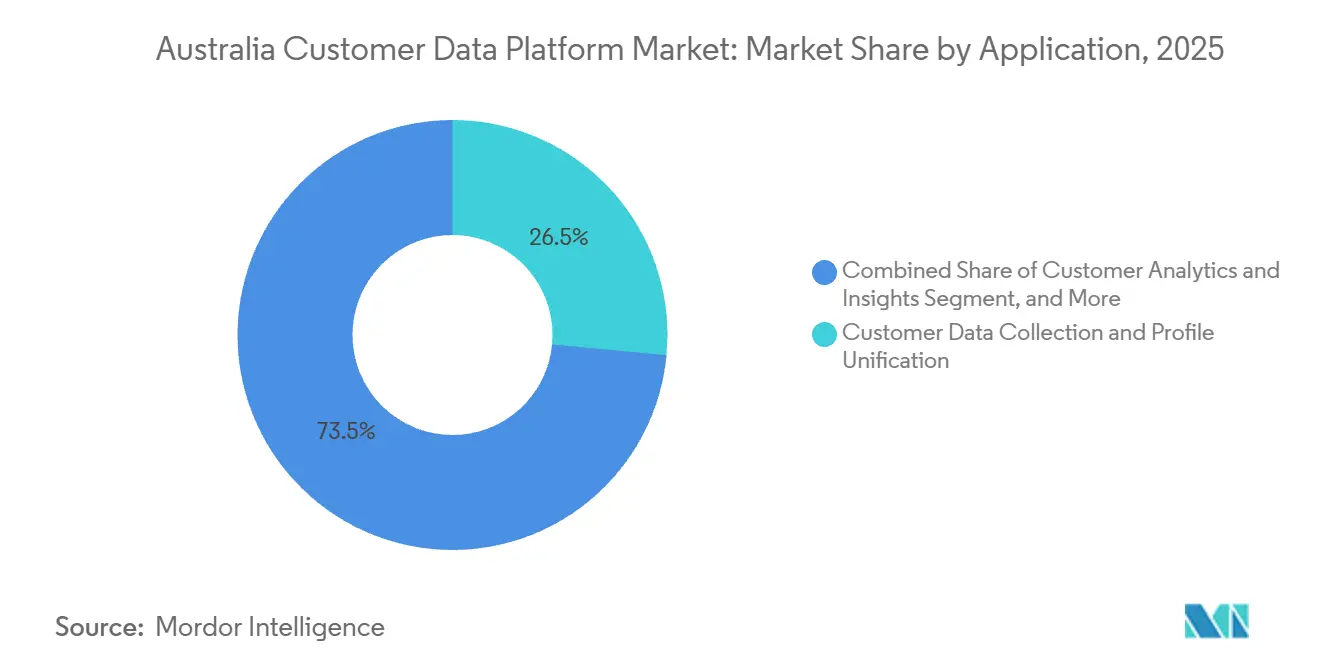

- By application, customer data collection and profile unification accounted for a 26.50% share in 2025, while customer analytics and insights are projected to expand at a 32.68% CAGR through 2031.

- By end-user industry, BFSI held a 27.35% share in 2025, while healthcare and life sciences are projected to grow at a 33.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising First-Party Data Activation Across Retail and Services | +7.5% | National, with early adoption concentrated in Sydney, Melbourne, and Brisbane retail and e-commerce corridors | Short term (≤ 2 years) |

| Privacy-First Customer Identity Unification Requirements | +6.8% | National, strongest compliance pressure in BFSI and healthcare and life sciences sectors | Short term (≤ 2 years) |

| AI-Enabled Real-Time Customer Journey Orchestration | +6.2% | National, with innovation concentration in major metropolitan markets, especially Sydney and Melbourne | Medium term (2-4 years) |

| Composable CDP Adoption with Cloud Data Warehouse Stacks | +5.1% | National, enterprise adoption led by organizations with established cloud data warehouse infrastructure in major metropolitan corridors | Medium term (2-4 years) |

| Cross-Channel Personalization Demand from Omnichannel Commerce | +3.8% | National, strongest in eastern seaboard markets where retail media network ecosystems are most developed | Medium term (2-4 years) |

| Event-Driven Data Capture from Mobile-First Customer Behavior | +3.2% | National, with highest behavioral signal density in Sydney, Melbourne, and Brisbane | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising First-Party Data Activation Across Retail and Services

Australia’s retail and services sectors are reorganizing customer data around first-party signals such as behavior, transactions, and loyalty activity because third-party tracking is losing both policy support and technical reliability. The Australia customer data platform market is benefiting from this shift because enterprises need a governed way to connect fragmented customer touchpoints into a single usable profile rather than holding them in separate systems. David Jones used Snowflake to connect e-commerce, behavioral, inventory, and supply chain data into a broader customer view, which shows how first-party activation has moved beyond campaign support and into wider enterprise data design. Retail media networks in Australia are also building monetization models around owned audience graphs, which increases the value of identity systems that allow brands to activate first-party audiences without exposing raw records. As more media, commerce, and service businesses depend on owned data assets for negotiation power and targeting control, the Australia customer data platform market is becoming a defensive investment as much as a growth tool.

Privacy-First Customer Identity Unification Requirements

The Privacy and Other Legislation Amendment Act 2024 received Royal Assent on December 10, 2024, and tightened the legal context around automated decision transparency, serious privacy invasions, and breach accountability.[1]Source: Australian Government, “Privacy and Other Legislation Amendment Act 2024,” Federal Register of Legislation, legislation.gov.au In the Australia customer data platform market, that change is pushing identity resolution closer to the center of procurement because organizations now need stronger proof of how consent links to profile creation and downstream activation decisions. Buyers in regulated sectors are giving more weight to platforms that embed consent graphs and preference management directly at the profile level instead of treating compliance as a separate layer after activation has already been designed. Vendors with Australian-region deployment options are also gaining relevance because procurement teams in BFSI and healthcare need privacy controls that align with domestic residency and sector governance expectations. This is reinforcing the role of the Australia customer data platform market as a compliance-linked infrastructure category rather than a discretionary marketing purchase.

AI-Enabled Real-Time Customer Journey Orchestration

AI-driven orchestration is changing what real-time execution means because platforms now process customer behavior, re-evaluate audience membership, and trigger actions within seconds instead of relying on fixed campaign sequences. Adobe made CX Enterprise Co-worker generally available in June 2026 on Adobe Experience Platform with Real-Time CDP, Customer Journey Analytics, and Journey Optimizer, which shows how the category is moving toward governed multi-agent workflow execution. Amperity’s Spring 2026 release introduced a real-time decision system and an MCP Server that lets AI applications draw on a single governed customer context, which further supports this movement toward live orchestration.[2]Amperity, “Amperity Spring 2026, Closing the Customer Decision Gap,” Amperity, amperity.com The Australia customer data platform market is gaining from this shift because AI applications are only as effective as the identity and consent structure feeding them. At the same time, privacy reform is placing more attention on how automated decisions use customer information, which means the strongest platforms are the ones that combine orchestration speed with clear governance.

Composable CDP Adoption With Cloud Data Warehouse Stacks

Australian enterprises are using cloud data warehouses more often as their central customer data layer, which is creating room for composable CDP models that add identity, segmentation, and reverse ETL functions without duplicating storage. The Australia customer data platform market is responding to this by shifting part of the demand away from fully packaged suites and toward modular designs that fit existing Snowflake, Databricks, BigQuery, or AWS estates. National Australia Bank’s Ada platform, built on Databricks Genie tools and connected to 180 data sources, illustrates how mature warehouse environments are narrowing the gap between core data infrastructure and activation use cases. Tealium launched CloudStream in June 2025 as a zero-copy segment builder that connects real-time data collection, warehouse-native activation, and consented audience building in a unified architecture, which directly addresses concerns around data movement and scale-up costs. This makes the Australia customer data platform market more favorable to vendors that can work with existing cloud estates instead of forcing organizations into expensive data duplication models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity Across Legacy MarTech and CRM Stacks | -4.2% | National, most acute in legacy-heavy BFSI and large retail enterprises across all major Australian markets | Medium term (2-4 years) |

| Data Residency and Consent Management Compliance Burden | -3.1% | National, amplified for multinational operators managing cross-border data flows under APP obligations | Short term (≤ 2 years) |

| Talent Shortage in CDP Implementation and Reverse ETL Workflows | -2.3% | National, most acute in non-metropolitan markets and mid-market organizations with limited specialist hiring access | Long term (≥ 4 years) |

| Total Cost of Ownership Pressure for Mid-Market Buyers | -1.8% | National, with a disproportionate impact on organizations outside the major metropolitan technology corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity Across Legacy Martech and CRM Stacks

Integration difficulty remains the main implementation barrier in the Australia customer data platform market because the platform has to connect e-commerce, CRM, loyalty, point-of-sale, and analytics systems that often run on different schemas and update cycles. That problem weakens the core promise of a unified customer profile when connectors do not resolve mismatches across web, app, and CRM data structures at the speed buyers expect. AMI documented that bill shock, API blowouts, and vendor pile-on had already affected a wide set of Australian adopters, which shows that implementation pressure is not isolated to one vendor or one vertical. David Jones’ work to wind down legacy platforms and move toward a more consolidated integration layer shows that data unification can take much longer when a business has accumulated many overlapping systems. As a result, organizations in the Australia customer data platform market are placing more emphasis on architecture fit, systems integration support, and implementation sequencing before they commit to broader rollout plans.

Data Residency and Consent Management Compliance Burden

The combination of privacy reform and domestic data handling expectations creates a heavier compliance burden in the Australia customer data platform market than in many other developed markets. The 2024 amendment strengthened protections around overseas disclosure of personal information, which increases pressure on multinational operators that rely on global infrastructure footprints. Vendors without Australian-region deployment options face weaker positioning in BFSI and healthcare because procurement teams in those sectors are balancing cloud-scale analytics with local control expectations. Compliance pressure also affects economics because stricter consent settings can reduce the number of active records that justify usage-based pricing models, which is one reason buyers are examining commercial structures more closely. This burden is likely to keep shaping vendor selection in the Australia customer data platform market as organizations try to align identity, consent, activation, and residency design in one operating model.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Platform Dominance Anchored in Enterprise Martech Consolidation

The platform segment held 78.50% of the Australia customer data platform market share in 2025, which reflected the strong preference for integrated suites that combine identity resolution, segmentation, and journey orchestration in one commercial relationship. Enterprise buyers in BFSI, retail, and media have often favored vendor-managed platforms because operating a modular stack requires stronger internal data engineering and reverse ETL capability than many teams currently hold. In the Australia customer data platform market, this preference has also supported longer platform relationships because a single suite can cover activation, analytics, and governance without the buyer stitching together separate tools. That dynamic has helped global vendors hold the center of high-value enterprise budgets even as buyers become more selective around integration and pricing.

AMP completed a three-year marketing platform transformation in 2025 and selected an Adobe CDP that unified online and offline customer data within 4 months before connecting Customer Journey Analytics and Journey Optimizer on top. Services are projected to grow at a 32.62% CAGR through 2031, which means service-led work is rising faster than the core platform layer itself. The Australia customer data platform market size for services is benefiting from implementation work, managed support, and strategic advisory as more organizations shift from packaged deployments to hybrid or composable environments. That services pull is strengthening because migration from legacy stacks to warehouse-native designs often requires integration work that no single software vendor can fully self-serve. The result is a broader service ecosystem around the Australia customer data platform market, with integrators and advisory partners becoming important revenue participants alongside the software vendors themselves.

By Deployment Mode: Hybrid Deployments Balance Residency Requirements with Cloud Agility

Cloud accounted for 66.41% of the Australia customer data platform market in 2025, which reflected the infrastructure base already established in AWS, Azure, and Google Cloud across large Australian enterprises. Those earlier cloud investments made it easier for buyers to deploy activation and analytics layers in environments they already used for broader data workloads. At the same time, the Australia customer data platform market has not moved into a pure cloud pattern because domestic data handling requirements still affect how identity and consent records are stored and governed. This is why cloud leadership has remained strong, while the fastest expansion is shifting toward a more balanced deployment design.

Hybrid is projected to grow at a 33.54% CAGR through 2031, and the Australia customer data platform market size for hybrid deployment is rising because buyers want cloud speed without giving up tighter control over sensitive customer records. Hybrid designs allow organizations to keep identity and consent data in Australian-region instances or controlled environments, while still linking those records to cloud-based activation and analytics capabilities. Meiro positions its CDP around local cloud or on-premises deployment in Australia with outbound integration to CRM and advertising systems, which shows the demand for architectures built around compliance fit.[3]Meiro, “CDP for Australia,” Meiro, meiro.io On-premises remains relevant for a narrower group of government and regulated financial buyers that want the highest degree of isolation. Even so, the Australia customer data platform market is moving toward models where hybrid is the practical compromise between sovereignty, interoperability, and the need for faster activation.

By Organization Size: Enterprise Holds Share, SMEs Drive Accelerating Volume Growth

Large enterprises held a 71.84% share of the market in 2025, which reflected the fact that enterprise-grade CDP programs have historically required dedicated engineering teams, multi-year implementation schedules, and larger licensing budgets. In the Australia customer data platform market, the biggest bank groups, insurers, and national retailers still represent the clearest example of that pattern because they manage large customer data estates and more complex regulatory obligations. Enterprise adoption has also been supported by the fact that AI-ready customer engagement depends on a strong data foundation, and large organizations have been better placed to fund that transition. This has kept large enterprises at the center of current spending even as smaller organizations become more active.

SMEs are projected to grow at a 32.16% CAGR through 2031, which makes them the fastest-moving size band in the Australia customer data platform market. Smaller organizations are entering through composable tools, embedded CDP capabilities in commerce software, and no-code activation layers that reduce dependence on specialist engineering teams. Wondaris has positioned itself around marketer-led composable customer data activation, and OFX has already cited it as a privacy-first marketing tool, which shows how the SME path differs from classic large-enterprise procurement. This part of the Australia customer data platform market is expanding because many businesses have become digitally active without becoming fully data-mature, so they now need a more structured way to use first-party information. As pricing models, packaging, and self-service tools improve, SME participation should add volume growth even if enterprise contracts continue to dominate revenue.

By Application: Customer Analytics Emerges as the Primary Value Driver Beyond Data Collection

Customer data collection and profile unification represented the largest application segment in 2025 with a 26.50% share, which reflects the usual adoption order in which companies first focus on identity resolution and data consolidation. That starting point remains important because most organizations cannot activate advanced use cases until they trust the profile layer underneath them. In the Australia customer data platform market, collection and unification have therefore acted as the operational base for segmentation, orchestration, analytics, and consent management. The early priority was not just to gather more data, but to make fragmented records usable across teams and channels.

Customer analytics and insights are projected to expand at a 32.68% CAGR through 2031, which shows that value is moving from data assembly toward decision support and optimization. The Australia customer data platform market size for customer analytics and insights is increasing as organizations seek stronger returns from the customer records they have already consolidated. Audience segmentation and personalization are scaling alongside that analytics growth because better customer models improve targeting precision and campaign efficiency. Consent and preference management is also becoming more important because privacy reform is pushing businesses to link permission status directly to activation logic rather than manage it in a separate workflow. This means the Australia customer data platform market is evolving from a unification toolset into a broader operating layer for governed customer intelligence.

By End-User Industry: BFSI Anchors Demand While Healthcare Accelerates on Interoperability Mandates

BFSI held a 27.35% share of the Australia customer data platform market in 2025, which reflected the sector’s large customer data volumes, tighter governance needs, and strong pressure to personalize service and product experiences. Financial institutions have a clear incentive to unify records because onboarding, servicing, retention, and next-best-action models all depend on current and trusted customer data. In the Australia customer data platform market, BFSI has therefore remained one of the most important demand anchors for enterprise-scale deployments. This is also the vertical where identity quality, auditability, and activation control carry especially high commercial and regulatory value.

Commonwealth Bank released 90% of its previously locked customer, account, and transactional data into AI-ready pipelines through an SAP-based core modernization, which shows how data infrastructure change can open the door to broader customer platform use. Healthcare and life sciences are projected to grow at a 33.36% CAGR through 2031, making this the fastest-growing end-user segment in the Australia customer data platform market. Telstra Health is leading the My Health Record data architecture overhaul through a FHIR-based interoperability program, which is strengthening the conditions for governed patient data movement across care settings. Retail and e-commerce, IT and telecom, and media and entertainment remain active buyers because they need strong segmentation and personalization at scale. Government and public administration are also emerging users as agencies look for more unified citizen data management under public sector compliance settings.

Geography Analysis

The Australia customer data platform market is structurally national, but demand remains concentrated in Sydney, Melbourne, and Brisbane because those metro corridors hold the largest share of financial institutions, retailers, media groups, and technology employers. Sydney and Melbourne continue to anchor most large-enterprise deployments because they also host the local operations of global platform vendors, consulting firms, and systems integrators that lead rollout programs. The eastern seaboard has become especially important for first-party data collaboration because major publisher ecosystems and retail media networks are more mature there. Adobe announced Real-Time CDP Collaboration availability in Australia and New Zealand in May 2025 with News Corp Australia, carsales, Nine, SBS, and TVNZ as local publisher partners, which shows how audience collaboration infrastructure is taking shape around the eastern corridor.[4]Adobe, “Adobe Announces Availability of Real-Time CDP Collaboration in Australia and New Zealand,” Adobe Newsroom, news.adobe.com The Consumer Data Right framework adds another national layer because it supports consented external data sharing, which increases the need for platforms that can operationalize identity and permissioned data flows.

Queensland and Western Australia form the next layer of opportunity, but their growth patterns are different. Queensland is moving from proof-of-concept activity into longer-cycle platform commitments, and RACQ’s five-year partnership with Adobe and Deloitte Digital shows that large membership organizations are now committing to broader customer experience and orchestration programs. Western Australia is not a core CDP vertical in the same way, but it still creates demand where workforce, contractor, or operational identity data needs stronger unification. Mobile behavior is supporting growth across all states because Australia had 22.34 million smartphone owners aged 14 and over and mobile traffic accounted for nearly 62% of total internet traffic in January 2026. Those event streams help make real-time activation commercially viable even outside the biggest metro clusters.

South Australia and the Northern Territory remain lower-density markets where government, healthcare, and mid-market demand carry more weight than national enterprise budgets. Healthcare interoperability mandates are helping these regions participate because FHIR-based data sharing allows regional health organizations to connect into broader patient data infrastructure without building a full enterprise stack on their own. The Reserve Bank of Australia noted in its April 2025 Financial Stability Review that digitalization in the financial sector had accelerated across fintech, AI use, and legacy modernization, which supports continued data management demand beyond the eastern seaboard. Because privacy and data handling rules are applied nationally, regional variation in the Australia customer data platform market comes more from enterprise scale and technology maturity than from different state-level regulations.

Competitive Landscape

The Australia customer data platform market has a moderately concentrated upper tier led by Adobe, Salesforce, Oracle, SAP, and Tealium, which together control a large share of large-enterprise spending through broader marketing cloud and data platform relationships. These vendors compete on integrated suites, implementation partnerships, and the ability to support both activation and governance inside the same commercial footprint. The current strategic pattern in the Australia customer data platform market is clear, with major vendors building AI orchestration into core runtime while also responding to demand for more composable and warehouse-native options. Tealium launched CloudStream in June 2025 as a zero-copy orchestration model and expanded onto the AWS Singapore Region in March 2026 to support regional data governance and performance needs. Adobe is also pushing into the next stage of orchestration through CX Enterprise Co-worker and Real-Time CDP Collaboration, which strengthens its position around both agentic workflow execution and publisher-side data collaboration.

Competition below that top tier is more fragmented, with specialist players such as mParticle, RudderStack, and Bloomreach competing on technical flexibility, event streaming, or modular architecture. Lexer Pty Ltd also adds local pressure in retail and hospitality through integrations that fit Australian loyalty and customer engagement environments more closely than some global products. The Australia customer data platform market is therefore not concentrated in the same way across all customer types, because large enterprises often buy from global suite vendors while more specialized use cases remain open to smaller providers. Amperity’s Spring 2026 release added Contextual Identity Graphs and a real-time decision layer that it positions as a stronger answer to identity reconciliation and AI application access. Oracle’s March 2026 work with Colonial First State also shows that vendors with broad cloud application portfolios are using operational transformation projects to deepen their role in customer data environments.

Two areas remain more open than the top end of the market. Mid-market buyers with meaningful first-party data but limited engineering resources are still underserved by large-enterprise pricing and implementation models, which gives more room to no-code or composable offers. Wondaris represents that direction with a marketer-led composable approach already referenced by OFX for privacy-first marketing use. A second opening sits in consent orchestration, where vendors that attach permission status directly to profile logic and activation controls should hold an advantage as compliance expectations deepen. That leaves the Australia customer data platform market with a strong top tier, but still enough white space for focused vendors that solve packaging, consent, and integration problems more directly than broad suite providers.

Australia Customer Data Platform Industry Leaders

Acquia, Inc.

Adobe Inc.

Amperity, Inc.

BlueConic, Inc.

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Infosys Finacle delivered the go-live of its Digital Banking Suite for Bank of Sydney on AWS cloud in a Software-as-a-Service deployment. The modernization enables the bank to scale customer-centric digital services and build the data infrastructure required for customer analytics, personalization, and AI-driven banking experiences on a cloud-native architecture.

- June 2026: RACQ, the Royal Automobile Club of Queensland with more than 1.7 million members, signed a five-year Lighthouse partnership with Adobe and Deloitte Digital, granting RACQ early access to agentic and generative AI capabilities across Adobe Experience Platform Agent Orchestrator, Real-Time CDP Collaboration, Experience Manager, and Workfront. Deloitte Digital leads end-to-end implementation, marking Adobe's first Lighthouse partnership in Asia Pacific and Japan.

- May 2026: Amperity announced its Spring 2026 release at Amplify 2026, introducing an AI-powered real-time customer decision system and a Model Context Protocol, MCP, Server that enables any AI application, including Microsoft Copilot, Braze AI, and Salesforce Agentforce, to access a governed, unified customer context through a single gateway, without custom pipelines or data duplication across systems.

- March 2026: Tealium launched its customer data platform on the AWS Singapore Region, expanding APAC infrastructure to address growing data governance, privacy, and performance requirements for Australian and Asia-Pacific enterprise clients as AI adoption intensifies demand for AI-ready, real-time data orchestration.

Australia Customer Data Platform Market Report Scope

The Australia Customer Data Platform (CDP) market comprises software platforms and associated services that collect, unify, manage, and activate customer data from multiple online and offline sources to create persistent, unified customer profiles. These platforms enable organizations to deliver personalized, privacy-compliant, and omnichannel customer experiences through capabilities such as identity resolution, audience segmentation, real-time data activation, customer journey orchestration, analytics, and consent management.

The Australia Customer Data Platform Market Report is Segmented by Offering (Platform, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and SMEs), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), End-User Industry (Retail and E-Commerce, BFSI, Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Platform |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| SMEs |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Platform |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| SMEs | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| BFSI | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current and forecast value of the Australia customer data platform space?

The Australia customer data platform market size was USD 0.15 billion in 2025, is USD 0.20 billion in 2026, and is forecast to reach USD 0.76 billion by 2031 at a 31.19% CAGR.

Which offering type leads revenue in Australia?

Platform leads revenue, with a 78.50% share in 2025, because enterprises still prefer integrated suites for identity, segmentation, and orchestration.

Which deployment model is growing fastest?

Hybrid is the fastest-growing deployment model, with a 33.54% CAGR through 2031, as buyers balance cloud agility with domestic data handling expectations.

Why are privacy reforms so important for customer data platforms in Australia?

The 2024 privacy amendment raised expectations around consent, automated decision transparency, and accountability, which makes governed identity and permission management more central to vendor selection.

Which application area is expanding the fastest?

Customer analytics and insights are the fastest-growing application, with a 32.68% CAGR through 2031, as organizations move from basic data unification toward decision support and optimization.

Which end-user segment offers the strongest growth outlook?

Healthcare and life sciences show the fastest growth at a 33.36% CAGR through 2031, supported by interoperability programs and stronger requirements for governed patient data exchange.

Page last updated on: