Australia CRM Marketing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

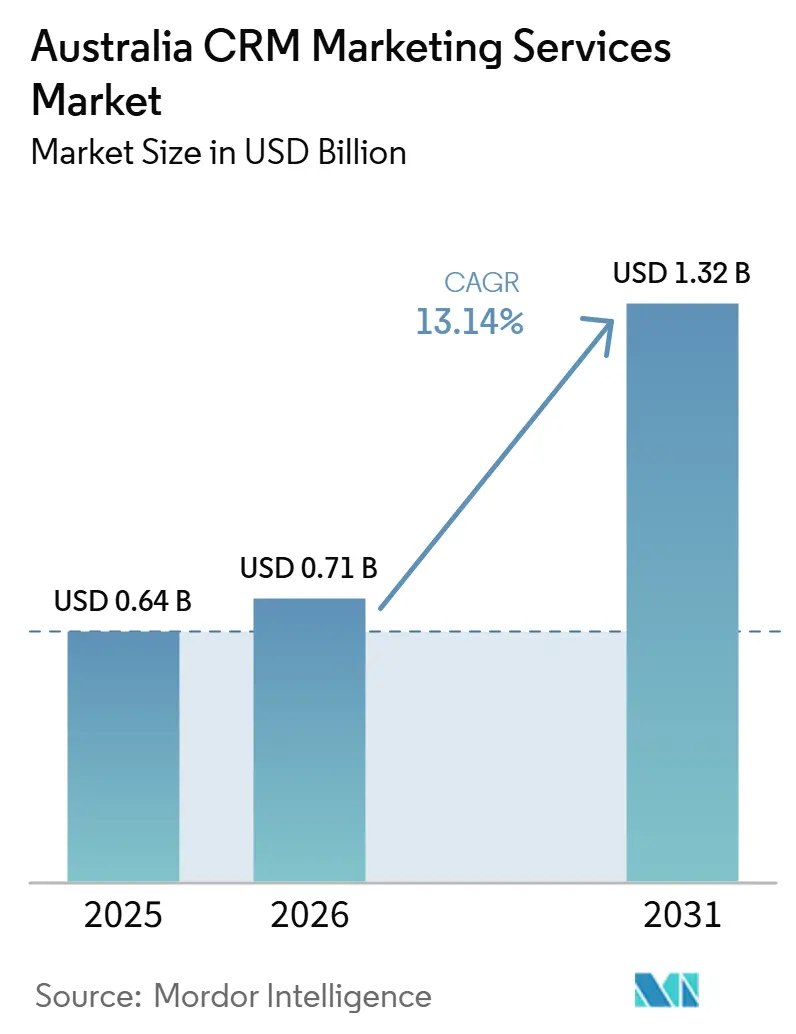

| Base Year Market Size (2025) | USD 0.64 Billion |

| Market Size (2026) | USD 0.71 Billion |

| Market Size (2031) | USD 1.32 Billion |

| Growth Rate (2026 - 2031) | 13.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia CRM Marketing Services Market Analysis by Mordor Intelligence

The Australia CRM marketing services market size is expected to grow from USD 0.64 billion in 2025 to USD 0.71 billion in 2026 and is forecast to reach USD 1.32 billion by 2031 at 13.14% CAGR over 2026-2031. The Australia CRM marketing services market is expanding because organizations now judge CRM programs by how well they connect behavior, transaction, and preference data into a single decision layer that can respond in real time during customer interactions. Spending is also moving toward managed services and personalization, as BFSI and retail firms treat AI-assisted orchestration as a core part of customer engagement rather than a premium feature. Privacy reform is shaping buying decisions at the same time, pushing companies to accelerate implementation so governance and personalization can be built together. The Australia CRM marketing services market is also benefiting from in-country infrastructure investments by major platform vendors, which have lowered data residency concerns and improved adoption conditions for regulated clients. Competition remains layered, with a concentrated platform base and a fragmented services base, which keeps room open for specialist providers that can move quickly on integration, compliance, and optimization work.

Key Report Takeaways

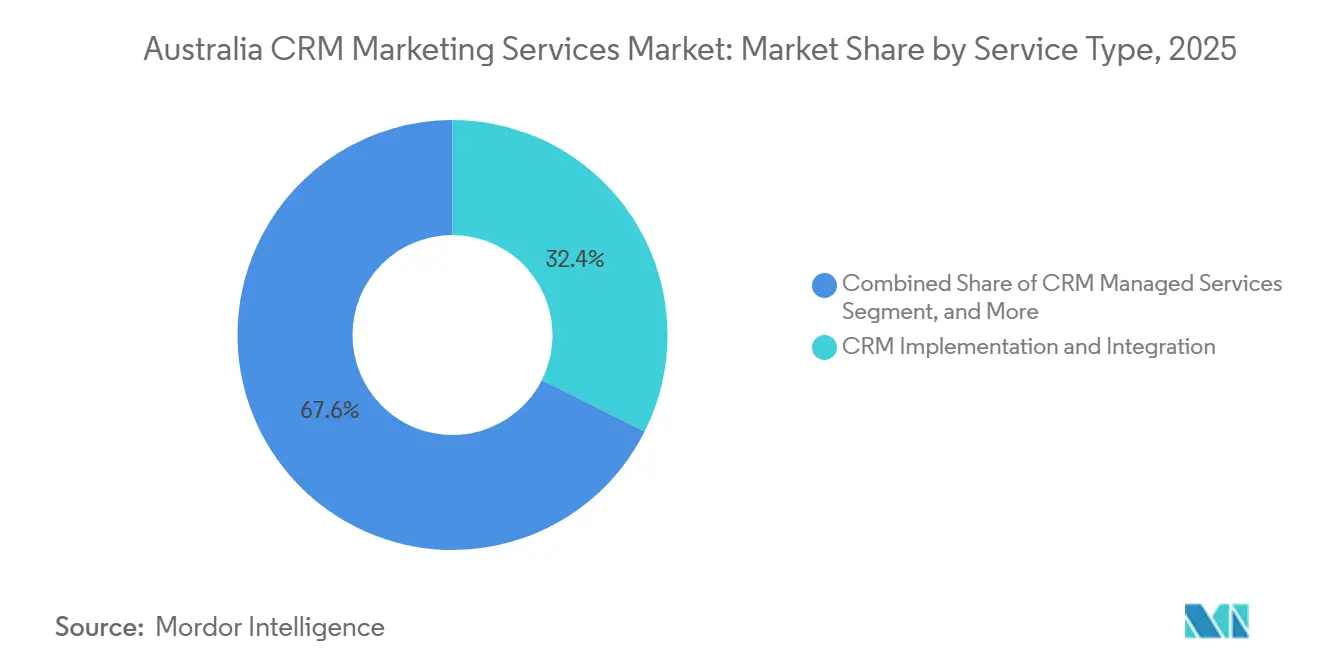

- By service type, CRM Implementation and Integration held 32.41% share in 2025, while CRM Managed Services is projected to expand at a 15.82% CAGR through 2031.

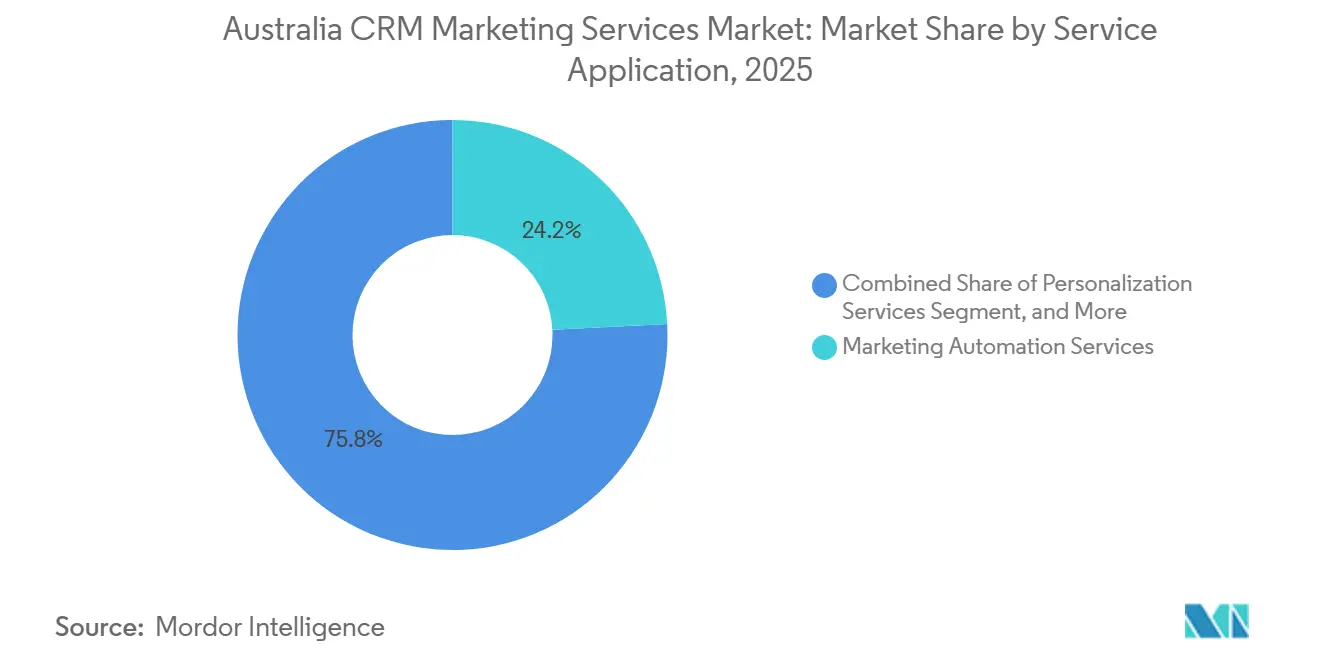

- By service application, Marketing Automation Services accounted for 24.18% share in 2025, while Personalization Services is expected to record the highest CAGR at 18.49% through 2031 in the Australia CRM marketing services market.

- By end-user industry, BFSI captured 28.62% share in 2025, while Retail and E-commerce are projected to grow at a 17.53% CAGR through 2031.

- By enterprise size, Large Enterprises held 68.43% share in 2025, while SMEs are expected to expand at a 16.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia CRM Marketing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for First-Party Customer Data Unification | +2.8% | National, with highest intensity in Sydney and Melbourne financial and retail hubs | Short term (≤ 2 years) |

| Shift From Campaign-Based Marketing to Lifecycle Engagement | +2.4% | National, strongest in BFSI and retail verticals across NSW and Victoria | Medium term (2-4 years) |

| AI-Assisted Lead Scoring and Next-Best-Action Orchestration | +2.1% | National, with early deployment in enterprise BFSI and telecommunications | Short term (≤ 2 years) |

| Cloud Migration of Mid-Market Customer Engagement Stacks | +1.7% | National, accelerating in Queensland and Western Australia mid-market | Medium term (2-4 years) |

| MarTech Consolidation to Reduce Tool Sprawl and License Duplication | +1.3% | National, highest urgency in large enterprise segments in Sydney and Melbourne | Medium term (2-4 years) |

| CRM Services Demand From Implementation, Integration, and Change Management | +1.0% | National, distributed across all states with concentration in major metros | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for First-Party Customer Data Unification

The Australia CRM marketing services market is attracting more investment in data architecture as third-party tracking weakens and privacy expectations rise. Only 59% of Australian marketers had complete access to service data, 60% had complete access to sales data, and 55% had complete access to commerce data in Salesforce’s 2026 State of Marketing findings, which shows how far many firms remain from a unified customer view.[1]Salesforce, “Tenth Edition State of Marketing,” Salesforce News, salesforce.com Marketers working with unified customer data were 42% more likely to respond consistently to customers and 60% more likely to use AI agents in marketing workflows, which raises the value of implementation and managed services that can connect fragmented systems. This gap is supporting long-cycle work in customer data platform integration, data hygiene, and consent-aware orchestration across the Australia CRM marketing services market. Australian Privacy Principles under the Privacy Act 1988 also require transparent consent and governance processes, so data unification has become a core design requirement rather than a later optimization step.

Shift From Campaign-Based Marketing to Lifecycle Engagement

The Australia CRM marketing services market is also moving away from one-off campaign execution and toward always-on lifecycle engagement. Commonwealth Bank of Australia widened its Salesforce Marketing Cloud deployment in February 2025 to support more complex lifecycle-based marketing across digital and physical banking channels. Colonial First State’s transformation, which focused on unified customer data, omnichannel reach, and AI-enabled automation, reduced data-handling effort by 95% and increased campaign volume by 120%, demonstrating that value often comes from reworking data architecture and journey logic rather than replacing the platform. This pattern extends service contracts because lifecycle programs need frequent testing, recalibration, and channel updates after launch. Organizations that completed lifecycle migration in 2024 and 2025 are now entering second-generation optimization cycles, which strengthens recurring managed services demand across the Australia CRM marketing services market.

AI-Assisted Lead Scoring and Next-Best-Action Orchestration

AI-assisted orchestration is moving into production use, and that shift is making the Australia CRM marketing services market more service-intensive. ANZ Bank completed the rollout of Salesforce Agentforce 360 across its Business and Private Bank in February 2026, bringing customer and account data from 20 legacy platforms into one AI-integrated dashboard. Oracle also reported that Australian organizations recorded a 23% surge in compute demand as AI workloads moved from experimentation to production, with another 26% increase projected in the near term, pointing to a larger infrastructure and optimization burden for AI-enabled CRM programs.[2]Oracle, “Oracle Launches AI Customer Excellence Centre to Drive Innovation Across Australia and Oceania,” Oracle News, oracle.com National Australia Bank’s use of 2,000 adaptive AI models simultaneously within its next-best-action framework shows how model governance and retraining needs can exceed the capacity of internal teams. As a result, implementation, monitoring, and optimization work are becoming a steady source of demand across the Australia CRM marketing services market.[3]Pega, “PegaWorld 2025, Customer Obsessed, Successes and Insights From National Australia Bank's Customer Brain Journey,” Pega, pega.com

Cloud Migration of Mid-Market Customer Engagement Stacks

Cloud migration in the mid-market is widening the addressable base of the Australia CRM marketing services market beyond the largest enterprise accounts. HubSpot opened a Sydney data center in February 2025, and Braze launched a Sydney facility in January 2025, adding to earlier Australian infrastructure from Adobe and Microsoft and making local hosting more practical for regulated clients. These changes matter for financial services, healthcare, and government buyers that treat data sovereignty as a compliance condition under Australian privacy rules. Salesforce’s USD 2.5 billion commitment to Australia over five years added further support through AI infrastructure, workforce programs, and ecosystem development, which improves the commercial case for longer implementation and managed services engagements. Research cited in that announcement projected that the Salesforce ecosystem in Australia would generate over 245,000 jobs and over USD 46 billion in business revenue by 2028, signaling the scale of the services layer being built around platform growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy Compliance Complexity Under Australia’s Data Handling Expectations | -1.5% | National, with highest compliance burden in BFSI and healthcare in NSW and VIC | Short term (≤ 2 years) |

| Integration Friction With Legacy ERP, Ecommerce, and Support Systems | -1.2% | National, concentrated in industrial manufacturing and government sectors | Medium term (2-4 years) |

| Skills Shortage in CRM Administration and Marketing Ops | -0.9% | National, most acute in Brisbane, Perth, and Adelaide markets | Medium term (2-4 years) |

| Budget Scrutiny for Multi-Platform MarTech Subscriptions | -0.7% | National, primarily affecting SME segment across all states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Privacy Compliance Complexity Under Australia’s Data Handling Expectations

Privacy reform is slowing parts of the Australia CRM marketing services market even as it creates demand in compliance-led consulting. Parliament passed the Privacy and Other Legislation Amendment Act 2024 on November 29, 2024, which included stronger enforcement powers for the Office of the Australian Information Commissioner and a new statutory tort for serious privacy invasions.[4]Australian Government Attorney-General's Department, “Privacy,” Attorney-General's Department, ag.gov.au The OAIC can now issue administrative fines of up to AUD 330,000 (USD 215,820 at the 2024 IRS annual average exchange rate of 0.654 USD per AUD) for minor privacy breaches without court proceedings, which raises the cost of weak governance in marketing operations. New disclosure obligations for automated decision-making will take effect on December 10, 2026, so companies using AI for scoring, personalization, and next-best-action are under pressure to document logic, data, and oversight before those workflows scale further. Suncorp Group has already adjusted customer segmentation algorithms and personalization models in response, demonstrating the cost and effort involved when governance must be retrofitted into existing CRM workflows.

Integration Friction with Legacy ERP, Ecommerce, And Support Systems

Integration friction remains a direct drag on delivery speed across the Australia CRM marketing services market. Many organizations still keep critical customer and transaction data inside ERP systems with proprietary APIs, ecommerce tools with incompatible schemas, or support platforms with weak webhook structures, and each gap adds custom work before personalization or decisioning can function reliably. Amart addressed this issue by deploying a universal customer ID via Salesforce Data Cloud, moving from fragmented systems with 24-hour delays to real-time campaign execution. The example also shows how much engineering work is needed before marketing gains appear. AMP’s three-year transformation from six separate email systems and a non-operational decisioning engine to a unified stack shows that consolidation is often measured in years rather than quarters. This issue is especially difficult in industrial manufacturing and government settings, where older operational systems often require bespoke middleware to connect cleanly with current CRM platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Implementation Commands Share, Managed Services Accelerate

CRM Implementation and Integration held 32.41% of the Australia CRM marketing services market size in 2025, and that lead reflected the lasting complexity of linking new CRM platforms to mixed enterprise technology estates. The work usually spans ERP, ecommerce, customer data, support, and telephony systems, which means service providers must handle mapping, workflow design, and change management simultaneously. This keeps implementation central to the Australia CRM marketing services market even when software platforms are already selected. CRM Strategy and Consulting supports that demand because firms often need architectural guidance and vendor-selection frameworks before committing to multi-year programs. CRM Migration and Modernization remains smaller in share, but it becomes important when contracts expire or when mergers force the consolidation of overlapping systems.

CRM Managed Services is expected to grow at a 15.82% CAGR through 2031, making it the fastest-growing service type in the Australia CRM marketing services market. The shift is tied to the growing effort required to maintain AI models, consent layers, integration endpoints, and journey rules after initial setup. Managed service teams are also taking on routine optimization work that internal marketing operations groups cannot always support at production quality. CRM Training and Support remains a high-volume activity, but it is increasingly bundled into broader managed service contracts rather than sold as a stand-alone offer. ISO/IEC 20000 and ISO 27001 remain relevant in these engagements

By Enterprise Size: Large Enterprises Anchor Spend, SMEs Gain Ground Fastest

Large Enterprises accounted for 68.43% of the Australia CRM marketing services market share in 2025, which reflects the concentration of the most complex CRM estates in the country. These organizations often run multiple clouds across sales, service, marketing, and commerce functions, and their services budgets can exceed software license costs once integration, maintenance, and training are included. The Australia CRM marketing services industry therefore depends heavily on large accounts for baseline demand, especially in banking, insurance, retail, and telecommunications. Platform vendors reinforced that pattern in 2025 when Salesforce, Microsoft, HubSpot, Braze, and Adobe maintained or expanded Australian infrastructure to support data residency and enterprise service needs. Those moves improved delivery conditions for providers working in highly regulated client environments.

SMEs are projected to grow at a 16.21% CAGR through 2031, providing the Australia CRM marketing services market with a second expansion path beyond the enterprise tier. Lower implementation costs and modular SaaS pricing are making it easier for smaller firms to adopt capabilities incrementally rather than purchasing a full suite at once. In-country residency options also removed a key barrier for SMEs in regulated sectors, which previously had to choose between lower-cost cloud tools and local privacy requirements. That shift is especially relevant for firms that delayed procurement decisions for several planning cycles and now have a clearer compliance path. As these companies move from entry deployments to optimization work, the services mix is likely to broaden from setup support into recurring administration and performance tuning.

By Service Application: Automation Leads, Personalization Defines The Next Cycle

Marketing Automation Services led this segmentation with 24.18% share in 2025, which shows its foundational role in the Australia CRM marketing services market across BFSI, retail, and telecommunications. Many organizations in these sectors have already completed first-generation automation work and are now refining those deployments with AI-enabled triggers and stronger cross-channel consistency. That keeps automation at the center of the Australia CRM marketing services industry because it acts as the operating layer for outreach, response, and reporting. Campaign Management Services still matters because it connects planning, execution, and measurement across acquisition and retention programs. Customer Acquisition, Customer Retention, and Loyalty also remain established areas where automation supports volume, timing, and message relevance.

Personalization Services is expected to grow at an 18.49% CAGR through 2031, making it the fastest-growing service application in the Australia CRM marketing services market. Salesforce reported that 80% of surveyed Australian marketers needed more personalized content than they could produce, 72% were using AI to close that gap, and 97% faced barriers to personalization, with data fragmentation cited most often. That shortfall is also lifting Customer Analytics and Insights, as scaled personalization depends on continuous model review, uplift checks, and segment recalibration. Omnichannel Customer Engagement is gaining ground for the same reason: firms need CRM data to flow across in-store, digital, social, and messaging channels without breaking the customer journey. As a result, the next cycle of service demand is likely to center less on basic automation and more on the quality, timing, and consistency of tailored interactions.

By End-User Industry: BFSI Leads, Retail And E-Commerce Drives Fastest Expansion

BFSI represented 28.62% of the Australia CRM marketing services market size in 2025, which kept it in the lead among end-user industries. The vertical combines high customer volumes, strict recordkeeping expectations, and clear commercial returns from better next-best-action and lifecycle engagement. ANZ Bank’s February 2026 deployment of Salesforce Agentforce 360 across its Business and Private Bank, with 20 legacy platforms brought into a single dashboard, shows the scale and duration of CRM service engagements this segment can deliver. Banks and insurers also tend to require stronger governance, testing, and documentation, which makes their projects broader than standard marketing implementations. That depth of need helps explain why BFSI remains a core demand center for both implementation and managed services.

Retail and E-commerce is projected to grow at a 17.53% CAGR through 2031, which makes it the fastest-expanding end-user industry in the Australia CRM marketing services market. The growth comes from omnichannel complexity because retailers must manage customer relationships across stores, ecommerce sites, social commerce, and loyalty programs at the same time. Personalization and campaign management are becoming more important as CRM shifts from a post-purchase retention tool into a pre-purchase discovery and conversion tool. Healthcare and Life Sciences also remains structurally important because patient engagement and pharmaceutical CRM programs are adopting more automation and often need extra compliance overlays. Information Technology and Telecom, Industrial Manufacturing, and Government and Public Administration round out the landscape, with government demand rising as digital citizen engagement becomes a clearer operating priority.

Geography Analysis

New South Wales and Victoria generated the majority of demand within the Australia CRM marketing services market. Sydney and Melbourne host the headquarters of major banks, insurers, retailers, and telecommunications companies, which means many CRM budget and architecture decisions are made in those two cities. Their concentration of large enterprises also supports larger implementation scopes, broader managed services contracts, and stronger demand for omnichannel personalization. Australian-based infrastructure from Salesforce, Microsoft Azure, Adobe, HubSpot, and Braze has made it easier for regulated clients in these hubs to keep sensitive customer data onshore. The tighter privacy environment after 2024 reinforced that local hosting preference, especially as firms prepare for automated decision-making disclosure requirements in December 2026.

Queensland is emerging as a distinct growth pocket within the Australia CRM marketing services market, as many mid-market firms are now completing cloud migrations that larger Sydney and Melbourne companies began earlier. Brisbane’s larger base of logistics, agritech, tourism, and property services firms creates steady demand for implementation work, onboarding support, and training. The state also has a meaningful concentration of businesses in the AUD 10 million to AUD 100 million revenue bracket, which equals USD 6.54 million to USD 65.4 million at the 2024 IRS average rate, creating a broad target base for modular CRM service offerings. Western Australia shows a different pattern, with resources and energy companies driving more sales-focused CRM programs that support long B2B cycles, complex contract structures, and dispersed field operations. Oracle’s AI Customer Excellence Center in Sydney provided a practical reference point for organizations in Queensland and Western Australia considering agentic AI within existing CRM workflows.

The Australian Capital Territory and South Australia represent smaller but distinct parts of the Australia CRM marketing services market. In the ACT, federal agencies use CRM marketing services for citizen engagement, grant communication, and public awareness programs, and these projects often need adaptation to government procurement, the Information Security Manual, and Protected classification requirements. South Australia reflects the state’s digital transformation push and the growth of Adelaide’s technology services base, which is creating early demand for CRM consulting and implementation. Tasmania and the Northern Territory contribute smaller volumes, but they remain open areas for cloud-first CRM deployment as local access to in-country infrastructure and implementation expertise improves. This positions these markets as later entrants in the domestic adoption curve rather than immediate demand leaders.

Competitive Landscape

The Australia CRM marketing services market is moderately fragmented at the platform layer and highly fragmented at the services layer. Salesforce, Microsoft, and Adobe hold significant positions across enterprise accounts through long-term relationships in BFSI, telecommunications, and retail, while a wide group of specialist partners competes in implementation, integration, and managed services. This split means the software base is concentrated, but the delivery ecosystem remains open to regional consultancies, boutique specialists, and cross-platform integrators. The Australian CRM marketing services market, therefore, rewards providers that can translate platform capability into faster deployment, stronger governance, and sector-specific execution. No single implementation or managed services provider appears to control the full service spectrum, which keeps pricing and specialization important in vendor selection.

Large vendors strengthened their position through visible strategic moves in 2025 and 2026. Salesforce announced a USD 2.5 billion investment in Australia over five years in February 2025, covering AI infrastructure, partner programs, and workforce development, and expanding the service opportunity around its platform. Oracle opened its AI Customer Excellence Center in Sydney in March 2026, creating a regional hub for proof-of-concept and production acceleration around agentic AI, generative AI, and predictive analytics in customer experience workflows. Salesforce and Google Cloud also expanded their partnership in April 2026 to support end-to-end AI workflows across both platforms, which raised the importance of multi-vendor orchestration expertise for Australian clients.

Oracle’s April 2026 launch of Fusion Agentic Applications for customer experience added another competitive step by embedding AI-driven decisioning directly into marketing workflows at no additional platform cost for Fusion customers. Salesforce’s April 2026 launch of Headless 360 similarly expanded how CRM functionality could be accessed via APIs, tools, and commands across surfaces such as Slack, voice, and WhatsApp. Smaller providers still have room in compliance-oriented governance consulting and mid-market managed services, especially for clients that completed early deployments in 2023 through 2025 and now need ongoing optimization support. Creatio and ActiveCampaign are gaining attention in that space by reducing implementation complexity for firms with limited technical capacity, which makes managed services more of an accelerator than a substitute for internal teams. The overall result is a market where major platforms shape the technical direction, but much of the services' value is still contested by providers with deeper local delivery.

Australia CRM Marketing Services Industry Leaders

Salesforce, Inc.

Microsoft Corporation

Oracle Corporation

HubSpot, Inc.

Zoho Corporation Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Salesforce released its Summer '26 update, introducing Agentic Work Units (AWUs) as the primary pricing and measurement metric for Marketing Cloud. The update, which Salesforce described as incorporating over 1,000 innovations, shifts the commercial model of AI-assisted marketing from seat-based licensing toward outcome-based unit pricing, with direct implications for how managed services contracts are structured and priced in the Australian market.

- April 2026: Salesforce and Google Cloud announced an expanded partnership at Google Cloud Next '26, enabling AI agents to execute end-to-end workflows across both platforms using Agentforce and Google Gemini Enterprise. The integration, including IDMC Google BigQuery Connectors and zero-copy lakehouse access, eliminates the need for data movement between platforms and is expected to accelerate cross-cloud marketing automation deployments among large Australian enterprise accounts.

- April 2026: Oracle launched Fusion Agentic Applications for customer experience (CX), introducing 5 new applications embedded in Oracle Fusion Cloud Customer Experience, including a Marketing Command Centre with AI agents capable of making and executing decisions within marketing processes by accessing unified enterprise data, workflows, and approval hierarchies, available to Fusion Applications customers at no additional platform cost.

- April 2026: Salesforce introduced Headless 360, exposing CRM capabilities as API, MCP tool, and CLI commands to enable AI agents and human developers to interact with Salesforce data across any surface, including Slack, voice, and WhatsApp. The associated AgentExchange marketplace aggregates 10,000 Salesforce apps, over 2,600 Slack apps, and over 1,000 Agentforce agents from third-party partners including Google, DocuSign, and Notion.

Australia CRM Marketing Services Market Report Scope

The Australia CRM (Customer Relationship Management) marketing services market encompasses the range of professional, managed, and support services provided to organizations in Australia to help them strategize, implement, optimize, and maintain CRM systems specifically for marketing functions. This market excludes the actual CRM software licenses or platform subscriptions (SaaS/on-premise), focusing entirely on the human expertise, consulting, and outsourced operations required to leverage these technologies effectively. The services covered include initial CRM strategy and consulting, system implementation and integration with existing marketing stacks, data migration and platform modernization, ongoing managed services, and user training and support. These services are used by businesses of varying sizes across multiple industries to execute specific marketing applications, including customer acquisition, retention, and loyalty programs; campaign management; marketing automation; customer analytics; omnichannel engagement; and hyper-personalization. The market value represents the revenue generated by service providers and agencies operating within Australia for these specific CRM-related marketing engagements.

The Australia CRM Marketing Services Market Report is Segmented by Service Type (CRM Strategy and Consulting, CRM Implementation and Integration, CRM Migration and Modernization, CRM Managed Services, and CRM Training and Support), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Service Application (Customer Acquisition, Customer Retention and Loyalty, Campaign Management Services, Marketing Automation Services, Customer Analytics and Insights, Omnichannel Customer Engagement, and Personalization Services), and End-user Industry, (Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Administration, and Other End-user Industries). The Market Forecasts are Provided in Terms of Value (USD).

| CRM Strategy and Consulting |

| CRM Implementation and Integration |

| CRM Migration and Modernization |

| CRM Managed Services |

| CRM Training and Support |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Acquisition |

| Customer Retention and Loyalty |

| Campaign Management Services |

| Marketing Automation Services |

| Customer Analytics and Insights |

| Omnichannel Customer Engagement |

| Personalization Services |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-user Industries |

| By Service Type | CRM Strategy and Consulting |

| CRM Implementation and Integration | |

| CRM Migration and Modernization | |

| CRM Managed Services | |

| CRM Training and Support | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Service Application | Customer Acquisition |

| Customer Retention and Loyalty | |

| Campaign Management Services | |

| Marketing Automation Services | |

| Customer Analytics and Insights | |

| Omnichannel Customer Engagement | |

| Personalization Services | |

| By End-user Industry | Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences | |

| Information Technology and Telecom | |

| Retail and E-commerce | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the size outlook for the Australia CRM marketing services market?

The Australia CRM marketing services market size was USD 0.64 billion in 2025, reached USD 0.71 billion in 2026, and is forecast to reach USD 1.32 billion by 2031 at a 13.14% CAGR.

Which service type leads spending in Australia CRM marketing services?

CRM Implementation and Integration led with 32.41% share in 2025 because enterprises still need extensive integration, mapping, and change management across mixed technology estates.

Which application area is growing fastest in Australia CRM marketing services?

Personalization Services is projected to grow at an 18.49% CAGR through 2031, supported by stronger demand for AI-enabled content delivery and better use of customer data.

Which customer sectors drive the strongest demand?

BFSI led with 28.62% share in 2025, while Retail and E-commerce is expected to post the fastest growth at a 17.53% CAGR through 2031.

Why are managed services gaining traction in this space?

CRM Managed Services is projected to grow at a 15.82% CAGR because firms need outside support to maintain AI models, consent controls, integrations, and ongoing workflow optimization.

What is the main regulatory issue affecting CRM marketing services in Australia?

The biggest issue is privacy compliance, especially new automated decision-making disclosure expectations taking effect in December 2026, which increase documentation and governance needs for AI-led CRM workflows.

Page last updated on: