Australia Construction Consulting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

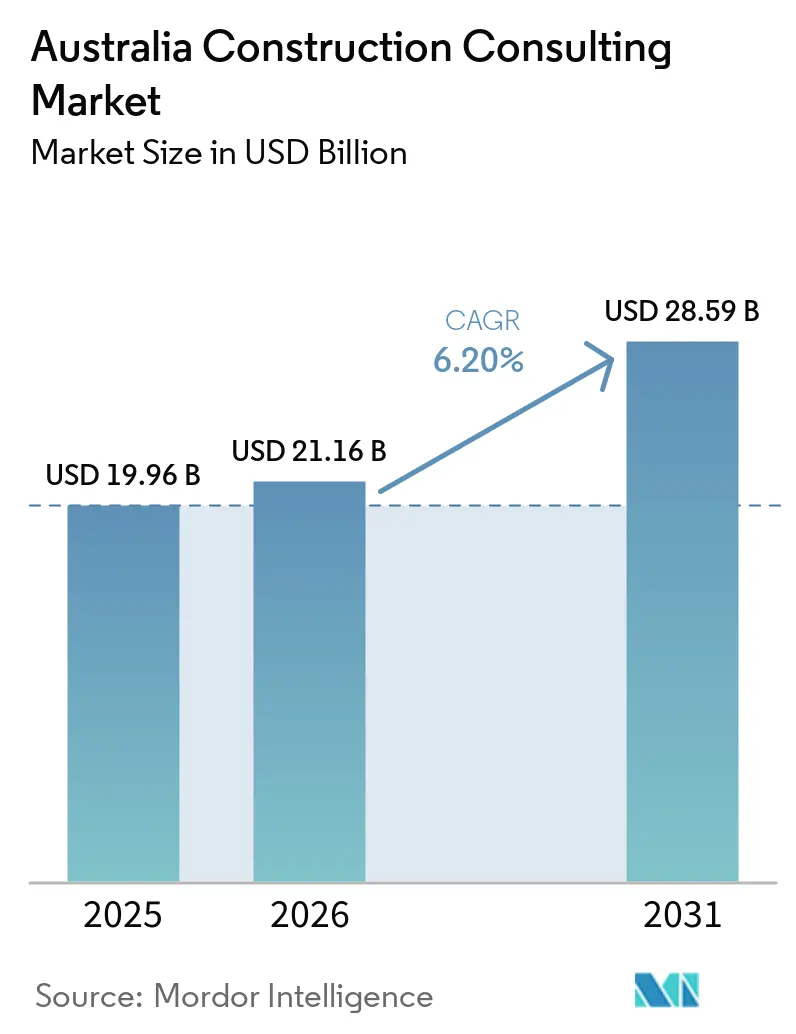

| Base Year Market Size (2025) | USD 19.96 Billion |

| Market Size (2026) | USD 21.16 Billion |

| Market Size (2031) | USD 28.59 Billion |

| Growth Rate (2026 - 2031) | 6.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Construction Consulting Market Analysis by Mordor Intelligence

The Australia Construction Consulting Market size is expected to increase from USD 19.96 billion in 2025 to USD 21.16 billion in 2026 and reach USD 28.59 billion by 2031, growing at a CAGR of 6.20% over 2026-2031.

Mandatory climate-related financial disclosures that began in January 2025, the federal government’s USD 160 billion (AUD 242 billion) Multi-Year Pipeline of Infrastructure Projects, and an expected wave of data-center announcements in March 2026 are reshaping procurement and delivery models. Program Management Consultancy (PMC) dominated 2025 revenue, but master-planning demand is accelerating as public and private owners seek early-stage guidance on compliance, site selection, and decarbonization. Labor shortages remain acute, yet rapid adoption of digital tools such as building information modeling (BIM) and artificial intelligence (AI) allows advisors to unlock productivity gains and command premium fees. At the same time, amendments to the Commonwealth Procurement Rules that reserve sub-USD 82,500 (AUD 125,000) contracts for domestic firms are redistributing smaller assignments toward local consultancies.

Key Report Takeaways

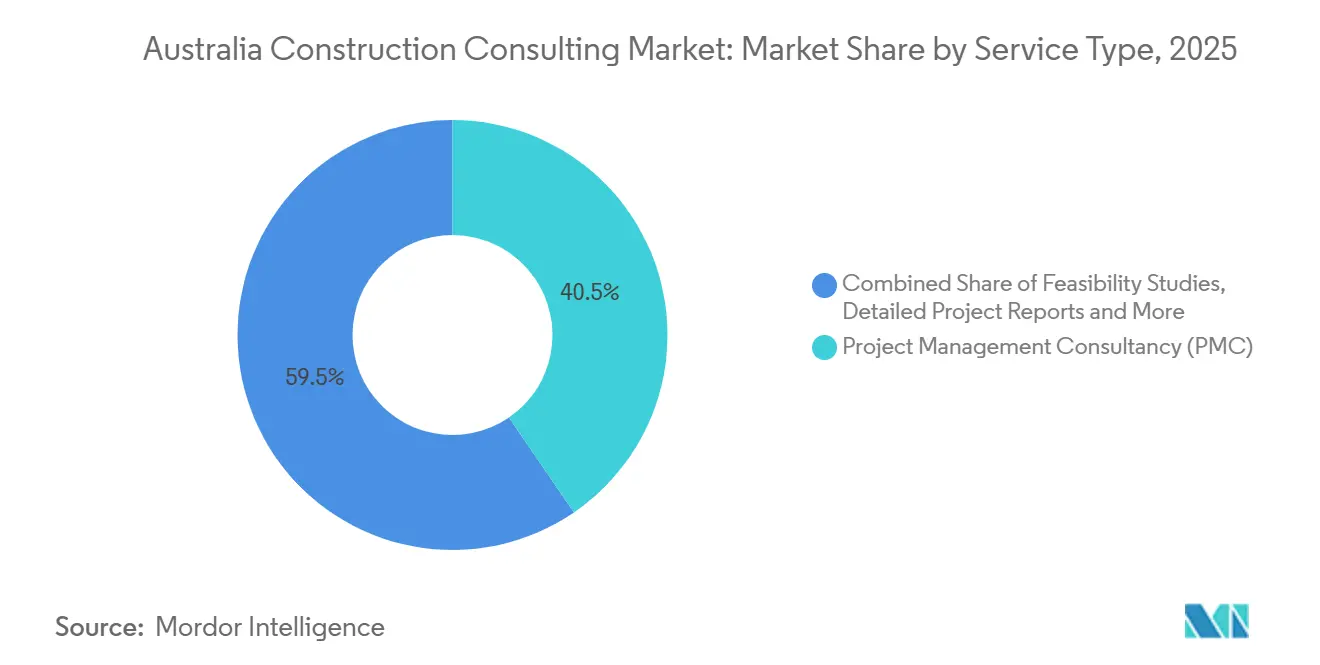

- By service type, Project Management Consultancy captured 40.45% of the Australia construction consulting market share in 2025, while Master Planning and Other Services is projected to expand at a 7.65% CAGR between 2026-2031.

- By sector, residential projects accounted for 37.8% of the Australia construction consulting market size in 2025, whereas infrastructure and civil consulting is forecast to grow at a 7.6% CAGR through 2031.

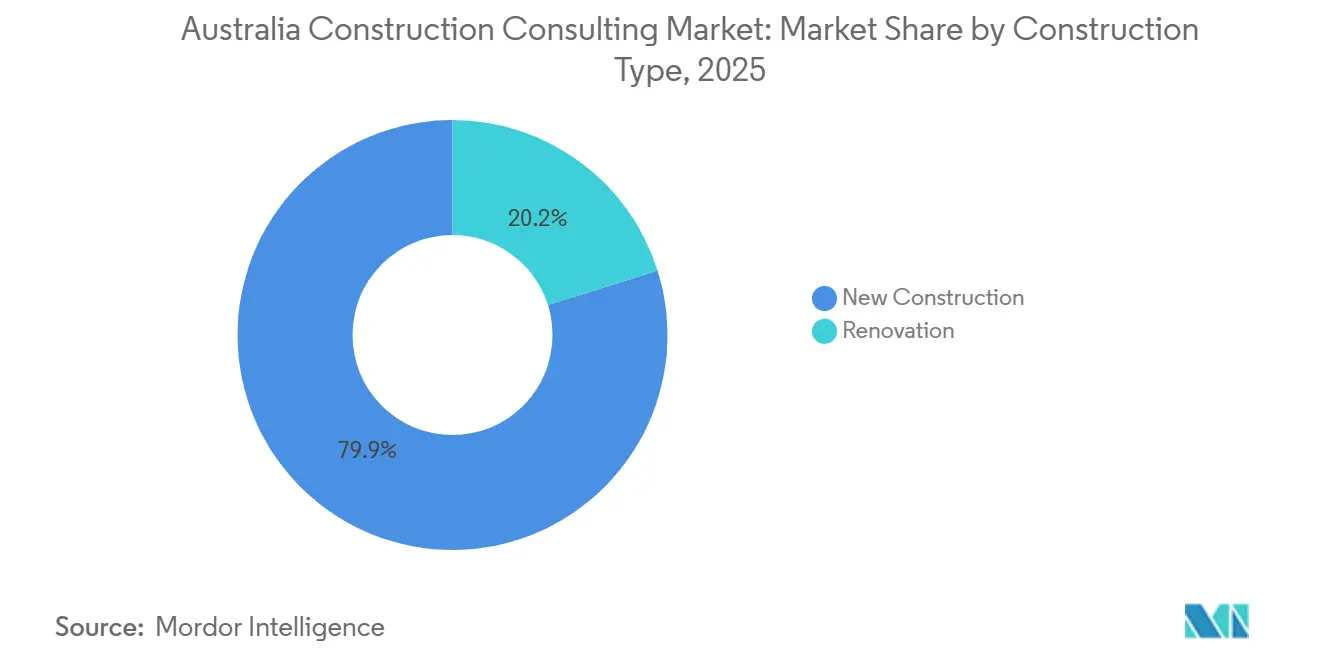

- By construction type, new construction held 79.85% of the Australia construction consulting market share in 2025, and renovation, as well as retrofit consulting, is expected to climb at an 8.85% CAGR to 2031.

- By investment source, private capital accounted for 90.2% of 2025 spending, yet public-sector consulting is anticipated to grow at an 8.45% CAGR during 2026-2031.

- By geography, New South Wales led with 33.65% of the Australia construction consulting market share in 2025, while Western Australia is forecast to register the fastest regional growth at a 7.85% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Construction Consulting Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal Infrastructure Outlay (MPIP and State Programs) | +1.8% | National, the highest in New South Wales, Victoria, Queensland, and Western Australia | Medium term (2–4 years) |

| Explosive Data-Center Construction Pipeline | +1.5% | New South Wales, Victoria, Queensland, and spillover to Western and South Australia | Short term (≤2 years) |

| ESG and Decarbonization Compliance Mandates | +1.2% | National, stricter in New South Wales and Victoria | Medium term (2–4 years) |

| Rapid Uptake of Design-Build and Progressive Design-Build Models | +0.9% | National, early use in New South Wales and Queensland | Short term (≤2 years) |

| Climate-Liability Resilience Advisory Need | +0.7% | Coastal New South Wales, Queensland, Northern Territory | Long term (≥4 years) |

| Executive-Talent Gap Creating Advisory Demand | +0.5% | Regional Western Australia and South Australia | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Federal Infrastructure Outlay (MPIP and State Programs)

Australia’s USD 160 billion (AUD 242 billion) infrastructure pipeline for 2024-29 is driving sustained demand for feasibility studies, project controls, and program-management services[1]Australian Government, “Budget 2024-25 Infrastructure Investment Program,” infrastructure.gov.au. Western Australia alone committed USD 7.1 billion (AUD 10.7 billion) to transport upgrades over four years, while Queensland raised road and rail allocations in its 2026 budget. Large multiyear programs require integrated advisory teams that combine engineering, commercial, and digital expertise. As state outlays fluctuate, firms with flexible regional resourcing protect utilization and margins. Overall, infrastructure funding adds 1.8 percentage points to the Australia construction consulting market CAGR.

Explosive Data-Center Construction Pipeline

Fifteen data-center projects received concierge approvals from Infrastructure NSW in early 2026, part of a USD 34.3 billion (AUD 51.9 billion) investment slate[2]Infrastructure NSW, “Investment Delivery Authority Project List March 2026,” infrastructure.nsw.gov.au. Hyperscale facilities exceed 20 kW per rack, requiring specialist mechanical, electrical, and plumbing design, as well as power-quality studies. Investors require independent technical due diligence before committing USD 660 million-plus per campus, expanding the premium advisory pool. Because data-center electrical equipment competes with renewable-energy supply chains, procurement consulting that secures transformers and switchgear is now mission-critical. The segment contributes 1.5 percentage points to the market CAGR.

ESG and Decarbonization Compliance Mandates

National rules that began in 2025 oblige large companies to report Scope 1 and 2 emissions, with Scope 3 phasing in later. New South Wales requires upfront embodied-carbon declarations for projects above USD 33 million (AUD 50 million) in buildings and USD 66 million (AUD 100 million) in infrastructure. Consultants offering lifecycle-carbon modeling, low-carbon material specification, and certification pathways (Green Star, NABERS) command premium fees. The Green Building Council of Australia estimates 66 MtCO₂e in potential annual savings from the built environment by 2035[3]Green Building Council of Australia, “Built Environment Sector Plan,” gbca.org.au. These mandates raise the Australia construction consulting market growth by 1.2 percentage points.

Rapid Uptake of Design-Build and Progressive Design-Build Models

Owners are embracing integrated delivery to shorten schedules and pass risk to private consortia. The USD 4.7 billion (AUD 7.1 billion) Brisbane 2032 Olympic Venues contract awarded to Unite32 (Laing O’Rourke and AECOM) illustrates consultants’ expanding role inside construction alliances. Design-build compresses hand-offs but lowers billable hours, so advisors are differentiating through digital twins and real-time cost modeling. Early contractor involvement also increases scope for skills-training compliance under the Australian Skills Guarantee. The shift adds 0.9 percentage points to growth in the Australia construction consulting market.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute Skilled-Labor Shortages Elevate Costs | -1.3% | National, severe in regional Western Australia, Queensland, and South Australia | Short term (≤ 2 years) |

| Slow Federal Fund Disbursements and Political Uncertainty | -0.8% | National, with Western Australia and South Australia most affected by per capita funding declines | Medium term (2-4 years) |

| Rising Professional-Liability Insurance Premiums | -0.4% | National, disproportionate impact on mid-tier and SME consultancies | Short term (≤ 2 years) |

| Domestic Content and Local Procurement Requirements Complicate Procurement | -0.3% | National, with Western Australia enforcing the strictest local manufacturing preferences | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acute Skilled-Labor Shortages Elevate Costs

The Housing Industry Association Trades Availability Index fell to −0.47 in Q4 2025 as bricklaying and ceramic-tiling trades slipped past −0.8. Construction cost inflation reached 3.4% annually by June 2025, peaking at nearly 6.5% year-over-year in Brisbane. Escalating wages and overtime premiums compress consulting margins when fee indexation lags. Although 44,000 employer-sponsored visas were allocated for 2024-25, processing delays mean relief is at least a year away. Capacity constraints subtract 1.3 percentage points from the Australia construction consulting market CAGR.

Slow Federal Fund Disbursements and Political Uncertainty

Infrastructure Partnerships Australia ranked Western Australia last for per-capita spending at USD 3,100 (AUD 4,700) in 2025-26, 10.4% below the prior year. Simultaneously, the national major-projects pipeline contracted from USD 223 billion (AUD 338 billion) to USD 100 billion (AUD 152 billion). Election cycles have lengthened bid timelines, causing consultants to carry overhead longer before notice-to-proceed. Smaller firms with limited balance sheets defer hiring, curbing industry capacity. The drag lowers projected growth by 0.8 percentage points.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Strategy-Led Master Planning Gains Ground

The master-planning, feasibility, and “other advisory” cluster held 40.45% of the Australia construction consulting market share in 2025, reflecting owners’ need for early-stage clarity on regulation, land constraints, and carbon compliance. Demand for program management consultancy remains high on megaprojects such as Sydney Metro West, yet commoditization is squeezing unit fees. Master-planning revenue is projected to grow at a 7.65% CAGR, the fastest among services, as public agencies front-load analysis to de-risk approvals. Consultancies that bundle digital-twin simulation with stakeholder engagement capture price premiums. The Australia construction consulting market size for master-planning work is forecast to exceed USD 7 billion by 2031.

Design and engineering services still represent essential spend on complex builds. Bechtel’s February 2025 appointment as capital-portfolio partner for Perth Airport highlights how integrated teams can cover concept through commissioning. However, leading contractors now internalize core design to protect margins, pushing pure design firms into alliances or niche specialties. In response, AECOM and WSP’s February 2026 joint venture on Sydney Metro West packages systems integration, digital engineering, and commissioning into a single scope, defending their share against vertical integration.

By Sector: Infrastructure and Civil Consulting Accelerates

Residential consulting contributed 37.8% of 2025 revenue, underpinned by housing-supply pressures and state incentive grants. Yet infrastructure and civil assignments are forecast to grow at a 7.6% CAGR through 2031, lifted by rail, road, and water programs. The Australia construction consulting market size attached to transport corridors alone could surpass USD 9 billion by the end of the decade. Data-center demand is also inflating commercial-sector fees; edge facilities springing up in regional hubs require rapid site due diligence and high-capacity grid tie-ins. Conversely, office and retail projects lag as hybrid work and e-commerce erode asset values.

Energy and utilities consulting is pivoting toward desalination and renewable energy storage. The Alkimos Seawater Desalination Plant, a USD 1.8 billion (AUD 2.8 billion) program that will create 1,500 jobs, exemplifies the multidisciplinary advisory needed for pipeline design and environmental permitting. Social infrastructure gains momentum from the USD 660 million (AUD 1 billion) Disaster Ready Fund that ties approvals to resilience standards, widening the lane for climate specialists. As public portfolios tilt toward smaller, distributed works, portfolio-management consulting eclipses bespoke megaproject staffing.

By Construction Type: Retrofit Advisory Outpaces Ground-Up Builds

New construction accounted for 79.85% of Australia construction consulting market share in 2025, heavily weighted to data centers, logistics hubs, and greenfield highways. Yet renovation and retrofit consulting is projected to grow at an 8.85% CAGR, driven by policy incentives and embodied-carbon goals. The Social Housing Energy Performance Initiative will upgrade more than 100,000 dwellings, triggering demand for thermal modeling, façade engineering, and grant-compliance services. Green Building Council of Australia analysis shows the potential to cut 66 MtCO₂e annually from the building stock by 2035, positioning retrofit as a lever in the national carbon strategy.

Insurers and lenders increasingly require climate-adaptation assessments on existing assets. Deloitte’s estimate of USD 48.2 billion in annual disaster costs by 2060 underscores the value of resilience retrofits. Consultants with hydrology and bushfire-science capability are advising on flood-barrier design for coastal properties and ember-attack testing for regional schools. Although new construction remains the larger spend category, retrofit work is now the growth engine and a hedge against cyclical greenfield slowdowns.

By Investment Source: Public Spend Rises Faster Than Private

Private investors generated 90.2% of consulting revenue in 2025, buoyed by strong demand in commercial real estate, manufacturing, and logistics. However, public-sector consulting is forecast to grow at a 8.45% CAGR through 2031 as governments outsource program controls to offset labor shortages. The November 2025 Commonwealth Procurement Rules lifted the direct-sourcing ceiling to USD 82,500 (AUD 125,000) for local firms, channeling hundreds of smaller studies to domestic specialists. For contracts above USD 6.6 million (AUD 10 million), the Australian Skills Guarantee now embeds apprenticeship targets, expanding the scope of compliance advisory.

State frameworks such as Western Australia’s General Procurement Direction 2025/15, which allows direct procurement of local products up to USD 3.3 million (AUD 5 million), reinforce the localization trend. While data-center and logistics owners still award privately funded megadeals, their growth rates lag those of government infrastructure. The rebalancing gives mid-tier consultancies with public-sector credentials an avenue to diversify away from developer pipelines.

Geography Analysis

New South Wales generated 33.65% of 2025 consulting revenue, anchored by Infrastructure NSW’s USD 34.3 billion (AUD 51.9 billion) project slate and 15 data-center schemes receiving concierge support. The state’s Decarbonizing Infrastructure Delivery Policy, active since April 2025, mandates embodied-carbon reporting above USD 33 million (AUD 50 million) for buildings and USD 66 million (AUD 100 million) for infrastructure, driving demand for specialist carbon advisory services. Sydney Metro West awards to AECOM-WSP (February 2026) and Jacobs-GHD-WSP (April 2026) illustrate the mega-scale multidisciplinary scopes cultivated in NSW. Upcoming Climate Change State Environmental Planning Policy amendments will broaden assessment criteria, further enlarging the advisory pool.

Victoria and Queensland follow in absolute spend. Victoria’s AI Mission and Sustainable Data Center Action Plan have spurred mechanical-electrical-plumbing (MEP) and grid-integration consulting. Conversely, Queensland’s infrastructure expansion, bolstered by the Brisbane 2032 Olympic build-up, contrasts with contractions in NSW and Victoria, creating relocation opportunities for national practices. Fast approvals and the progressive adoption of design-build underpin the Australia construction consulting market share gain in Queensland.

Western Australia is the fastest-growing region, forecast to post a 7.85% CAGR through 2031. The state’s USD 7.1 billion (AUD 10.7 billion) four-year transport plan, USD 1.8 billion (AUD 2.8 billion) desalination program, and USD 462 million (AUD 700 million) Kwinana Freeway upgrade boost early-stage engineering scopes. Despite WA allocating only 7.4% of general-government spending to infrastructure in 2025-26, its long-term pipeline is stable, favoring multi-year advisory relationships. Elsewhere, South Australia’s hydrogen projects, Tasmania’s energy-storage builds, and the Northern Territory’s defense precincts offer niche growth anchored by resource and defense spending, ensuring geographic diversification for national consultancies.

Competitive Landscape

International majors AECOM, Jacobs, Turner & Townsend, Arcadis, and WSP secure headline rail, airport, and water assignments thanks to depth in digital engineering and global balance sheets. Domestic mid-tiers such as GHD, Tonkin + Taylor, and Bligh Tanner leverage state relationships and local codes proficiency to win precinct and retrofit programs. The Australia construction consulting market remains moderately fragmented: the top five participants hold roughly 55% combined share.

A consolidation wave is underway. AtkinsRéalis bought ADG in December 2025 and, in April 2026, added WGA’s 800-person platform to build national scale across buildings and environmental services. DCWC’s January 2026 merger with RP Infrastructure created a 500-strong civil and transport advisory group, signaling private-equity appetite for roll-ups. RSK Group’s combination of Projence and Western Project Services earlier in 2025 shows investors value regional footholds that unlock federal defense and resources programs.

Joint-venture delivery dominates megaprojects. Unite32 (Laing O’Rourke and AECOM) controls the USD 4.7 billion Olympic Venues program, while AECOM-WSP handles line-wide systems, and Jacobs-GHD-WSP oversees station packages on Sydney Metro West. These alliances spread risk and pool scarce digital-engineering skills. Technology adoption is a competitive wedge: Deloitte reports Australian contractors now use 6.2 of 16 tracked technologies, up 20% from 2023, and 37% employ AI/ML, compared with 26% two years earlier consultants embedding BIM-first workflows and predictive analytics secure higher margins even amid rising professional-indemnity premiums.

Australia Construction Consulting Industry Leaders

AECOM

Jacobs

Turner & Townsend

CBRE (PDS)

JLL Project & Development Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: AtkinsRéalis agreed to acquire WGA, adding 800 professionals across Australia and New Zealand to its multidisciplinary portfolio.

- April 2026: Jacobs, GHD, and WSP formed a joint venture for five Sydney Metro West stations, one of the country’s largest urban-rail design mandates.

- February 2026: AECOM and WSP created a joint venture to deliver line-wide systems for Sydney Metro West, covering signaling, power, and platform-screen doors.

- January 2026: DCWC merged with RP Infrastructure, forming a 500-employee national civil and infrastructure advisory platform.

Australia Construction Consulting Market Report Scope

| Project Management Consultancy (PMC) |

| Feasibility Studies |

| Detailed Project Reports (DPR) |

| Design and Engineering Services |

| Master Planning and Other Services |

| Residential | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Data Center | |

| Others - Institutional, Hospitality etc. | |

| Infrastructure/Civil | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Social Infrastructure | |

| Others |

| New Construction |

| Renovation |

| Public |

| Private |

| New South Wales |

| Victoria |

| Queensland |

| Western Australia |

| Rest of Australia |

| By Service Type | Project Management Consultancy (PMC) | |

| Feasibility Studies | ||

| Detailed Project Reports (DPR) | ||

| Design and Engineering Services | ||

| Master Planning and Other Services | ||

| By Sector | Residential | |

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Data Center | ||

| Others - Institutional, Hospitality etc. | ||

| Infrastructure/Civil | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Social Infrastructure | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Investment Source | Public | |

| Private | ||

| By Geography | New South Wales | |

| Victoria | ||

| Queensland | ||

| Western Australia | ||

| Rest of Australia | ||

Key Questions Answered in the Report

What is the current size of the Australia construction consulting market?

Mordor Intelligence values the market at USD 19.96 billion in 2025 and projects it to reach USD 28.59 billion by 2031.

Which service line leads revenue?

Program Management Consultancy held 40.45% of 2025 revenue, ahead of design and master-planning services.

Which segment will grow fastest to 2031?

Master Planning and Other Services is expected to post a 7.65% CAGR, driven by demand for climate-compliance and precinct planning.

Which state represents the largest geographic market?

New South Wales captured 33.65% of national consulting revenue in 2025, anchored by the Sydney Metro and data center pipelines.

How severe are labor shortages affecting consultants?

Infrastructure Australia predicts a 300,000-worker gap by 2027; HIA’s index shows persistent trade shortages, pushing cost inflation to 3.4% in 2025.

Will public or private investment grow faster?

Public-sector consulting is forecast to rise at an 8.45% CAGR through 2031, outpacing private capital despite the latter’s larger base.

Page last updated on: