Australia Co-Living Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

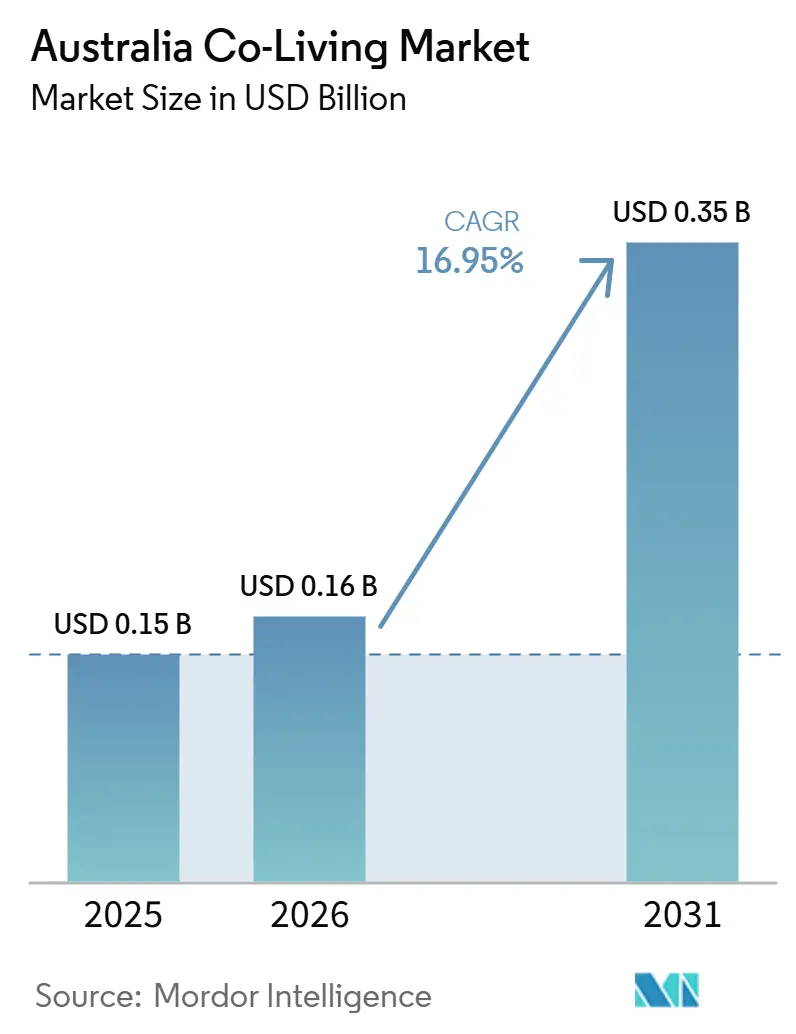

| Base Year Market Size (2025) | USD 0.15 Billion |

| Market Size (2026) | USD 0.16 Billion |

| Market Size (2031) | USD 0.35 Billion |

| Growth Rate (2026 - 2031) | 16.95% CAGR |

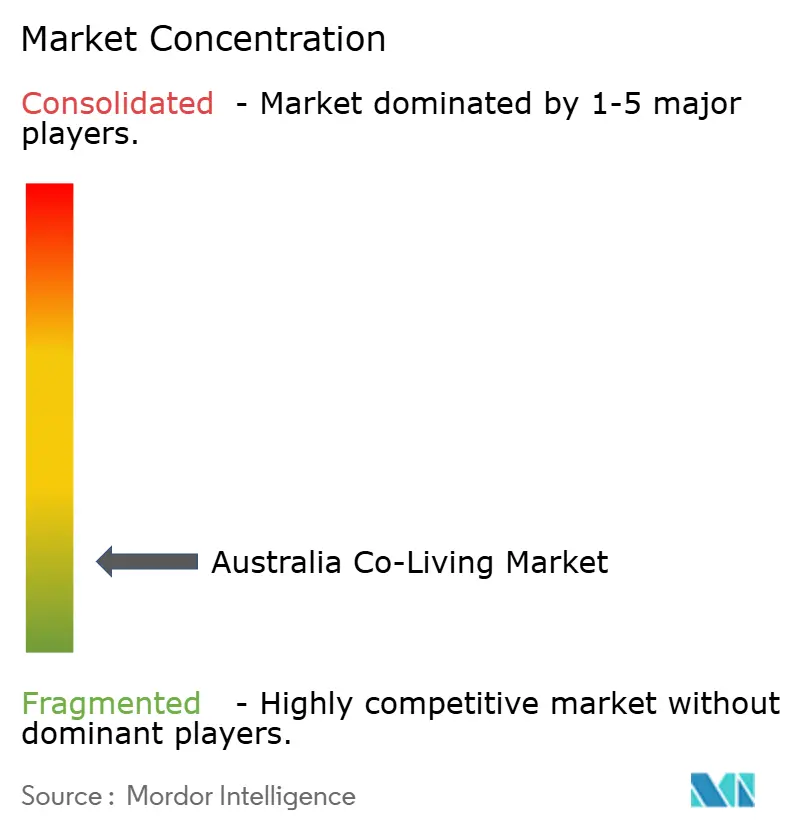

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Co-Living Market Analysis by Mordor Intelligence

The Australia Co-Living Market size is expected to increase from USD 0.15 billion in 2025 to USD 0.16 billion in 2026 and reach USD 0.35 billion by 2031, growing at a CAGR of 16.95% over 2026-2031.

Growth in the Australia co-living market is closely tied to a housing system that remains short of required supply, with the National Housing Accord period still tracking below its delivery target by a wide margin. Affordability pressure is also keeping renter demand elevated because new lease costs already absorb a record share of household income, and mortgage access remains difficult for many urban residents. Population growth continues to reinforce that demand base, as net overseas migration remained high in 2024-25 and temporary arrivals continued to concentrate in the large east coast states where rental pressure is strongest. The Australia co-living market is also gaining support from professionally managed supply additions, adaptive reuse activity, and larger capital commitments that are aimed at flexible living formats rather than only traditional rental housing. Even so, planning friction and cost pressure still limit the speed of new delivery, which keeps the Australia co-living market tight in near-term supply and favors operators that can scale within compliant urban locations.

Key Report Takeaways

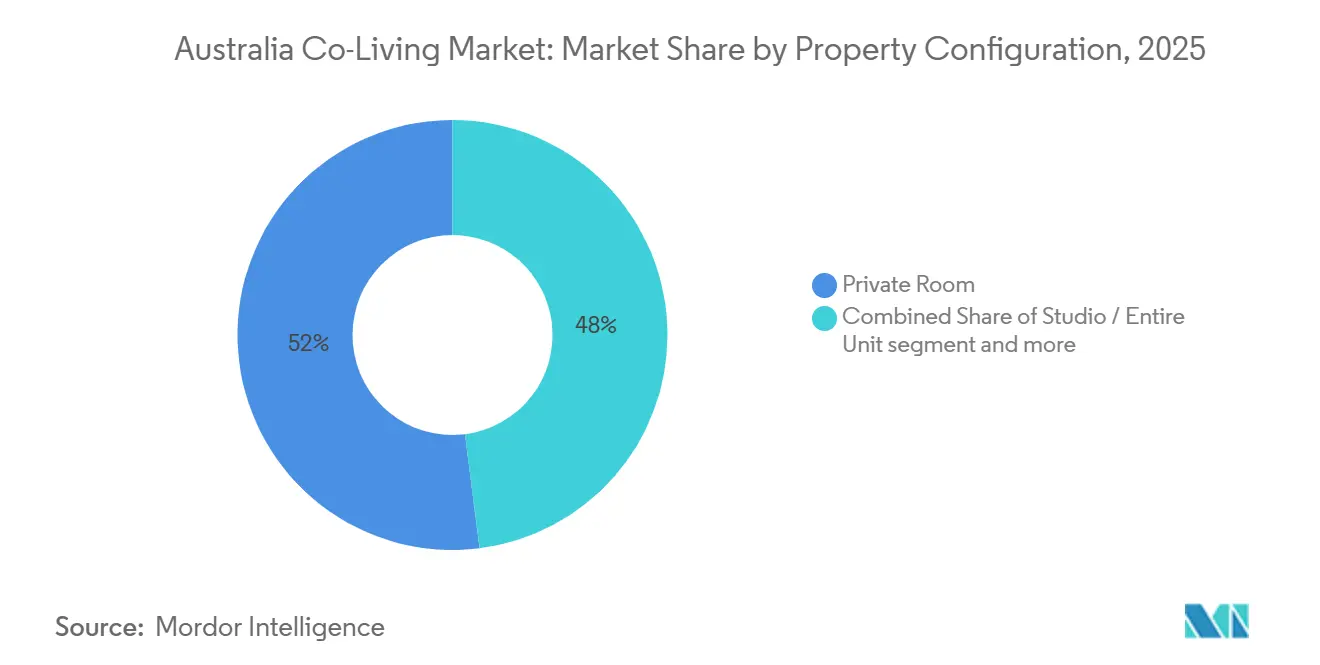

- By property configuration, private rooms led with 52% revenue share in 2025, while shared rooms are forecast to expand at a 17.00% CAGR through 2031.

- By business model, the asset-heavy own-develop-operate segment held 43% of the market in 2025, while the asset-light master lease / lease arbitrage segment is projected to record the highest CAGR of 17.50% through 2031.

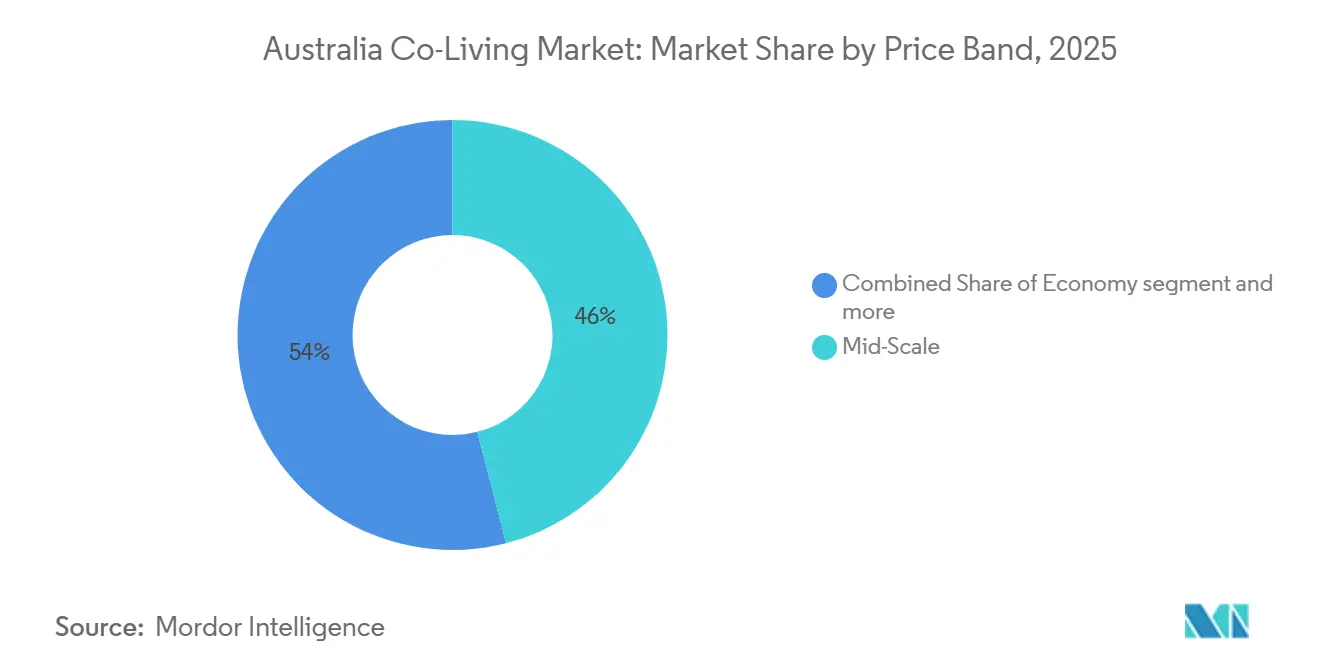

- By price band, mid-scale properties accounted for 46% of Australia co-living market share in 2025, while premium / luxury co-living is expected to grow fastest at an 18.00% CAGR through 2031.

- By end user, working professionals accounted for 56% of demand in 2025 and recorded the highest projected CAGR of 17.30% through 2031.

- By geography, Sydney held 41% of the Australia co-living market size in 2025, while Brisbane is forecast to expand at an 18.30% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Co-Living Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Housing Affordability Challenges Drive Co-Living Demand | +5.0% | National, strongest in Sydney, Melbourne, Brisbane | Short term (≤ 2 years) |

| Strong Population Growth and Net Overseas Migration Increase Housing Demand | +3.5% | National, with concentrated impact in NSW, VIC, QLD, WA | Medium term (2-4 years) |

| Growing International Student and Young Professional Population Expands Occupancy | +2.5% | Sydney and Melbourne core, spill-over to Brisbane, Perth | Medium term (2-4 years) |

| Expansion of Purpose-Built Co-Living Developments Boosts Market Growth | +1.5% | NSW-led, accelerating in QLD, WA | Medium term (2-4 years) |

| Preference for Flexible and Community-Oriented Living Increases Adoption | +1.2% | National, strongest among 20-35 demographic in capital cities | Long term (≥ 4 years) |

| Build-to-Rent Expansion Accelerates Co-Living Supply | +1.0% | National, early activity in Sydney and Melbourne | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Housing Affordability Challenges Drive Co-Living Demand

The Australia co-living market is benefiting from a housing affordability gap that widened further in 2026. The share of median household income required for a new lease reached 33% in 2026, while the years needed to save for a mortgage rose to 11.2 years, which kept a larger share of renters in the leasing pool for longer[1]National Housing Supply and Affordability Council, “State of the Housing System 2026,” NHSAC, nhsac.gov.au. That pressure matters because co-living reduces the upfront and recurring cost burden by bundling rent, furnishings, and shared services into a single managed payment. The housing shortage behind this shift is still structural, since the National Housing Accord period is expected to deliver 980,000 homes against a 1.2 million target. The Housing Industry Association (HIA) also noted that demand for housing continued to run ahead of supply in 2025, which supports the same affordability pattern seen in the Australia co-living market. As long as new delivery remains below demand, professionally managed shared housing will continue to serve renters who cannot justify a standalone apartment.

Strong Population Growth and Net Overseas Migration Increase Housing Demand

The Australia co-living market is also being lifted by population growth that continues to exceed housing completions. Net overseas migration added 306,000 people in the 2024-25 financial year, and the largest net gains were recorded in New South Wales, Queensland, and Western Australia. Those are the same states where rental pressure remains high and where new co-living supply has the clearest room to grow. Almost two in three migrant arrivals were on temporary visas, and international students accounted for the largest single cohort, with 157,000 arrivals. The Housing Industry Association (HIA) estimated that annual population growth implied demand for 190,000 to 200,000 new homes per year, a figure that remained above actual completions. This keeps vacancy tight and supports sustained occupancy conditions across the Australia co-living market.

Growing International Student and Young Professional Population Expands Occupancy

The Australia co-living market is supported by two renter groups that need flexible urban housing, international students and young professionals. University World News reported in May 2026 that student intake was running 10% to 15% below prior levels, while policy settings increasingly linked enrollment growth to demonstrated accommodation capacity. That change strengthens the case for professionally managed overflow housing because student beds remain limited relative to demand. The Property Council of Australia stated in June 2026 that purpose-built student accommodation penetration stood near 6% of the student cohort, far below the 54% level in the United Kingdom. ABC News also reported that limited and expensive student housing continued to push overseas students toward shared accommodation options in 2025. In practice, that means student demand adds breadth to the Australia co-living market without changing its core appeal to working residents who value access, flexibility, and a predictable weekly cost.

Expansion of Purpose-Built Co-Living Developments Boosts Market Growth

The Australia co-living market is also moving forward because formal project supply is becoming more visible. In May 2026, the New South Wales (NSW) Department of Planning, Housing and Infrastructure approved a mixed development at Melrose Park in Sydney that includes 154 co-living units and 197 affordable housing units under the Housing Australia Future Fund Housing Delivery Authority (HDA) pathway. That approval matters because it shows that co-living can move through a structured pathway when the use case aligns with planning and affordability priorities. Pro-Invest Group also advanced an adaptive reuse strategy in 2026 by acquiring Coogee Sands Hotel and Apartments for conversion into 80 flex-living studios. Its earlier joint venture with Kajima added another AUD 500 million (USD 318 million) to its build-to-rent development plans in Australia, reinforcing the broader capital shift toward urban rental living formats. As more compliant projects move from concept to execution, the Australia co-living market should deepen beyond a small cluster of early assets.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Development and Construction Costs Constrain Project Viability | -2.0% | National, strongest in QLD and Sydney metro | Medium term (2-4 years) |

| Regulatory and Planning Approval Complexity Delays New Developments | -1.5% | VIC, QLD, WA, less impact in NSW with Housing SEPP 2021 | Short term (≤ 2 years) |

| Rising Land Acquisition Costs Increase Development Expenses | -1.2% | Sydney and Melbourne inner precincts | Medium term (2-4 years) |

| Limited Consumer Awareness and Market Maturity Restrict Market Adoption | -0.8% | National, particularly outside Sydney | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Development and Construction Costs Constrain Project Viability

The Australia co-living market also remains exposed to cost pressure that affects feasibility, pricing, and timing. Construction cost escalation remains a near-term risk, placing additional pressure on already tight project economics for dense urban housing. National Housing Supply and Affordability Council (NHSAC) also noted in 2026 that geopolitical disruption had introduced further uncertainty into the housing delivery outlook, adding another layer of risk to already-constrained supply pipelines. When build costs rise, developers need stronger rents, cheaper land, or more efficient reuse strategies to make projects work. That is one reason adaptive reuse and institutional partnerships are becoming more common across the Australia co-living market. The restraint does not stop demand, but it does slow the pace at which supply can respond.

Regulatory and Planning Approval Complexity Delays New Developments

The Australia co-living market still faces uneven planning treatment across states. New South Wales (NSW) has a more defined pathway through the Housing SEPP framework, while Victoria, Queensland, and Western Australia do not yet offer the same level of formal recognition for co-living as a distinct land use class. That forces many projects outside New South Wales into case-by-case local approval processes, which extend timelines and increase execution risk. The Melrose Park approval in May 2026 showed that compliant projects can move forward, but it also showed how closely co-living delivery remains tied to planning structure and public policy priorities[2]PAYCE / Medianet, “PAYCE, Project Approval to Boost Sydney’s Affordable Rental Stock,” Medianet, medianet.com.au. This matters because operators need predictable approval settings before they can scale multi-city portfolios. Until that consistency improves, the Australia co-living market will keep expanding faster in locations where planning treatment is clearer.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Configuration: Private Rooms Define Yield While Shared Rooms Accelerate

Private rooms held 52% of the Australia co-living market share in 2025, which made them the leading property configuration across the country. That position reflects the basic preference of urban renters who accept shared kitchens, lounges, and services but still want a private, secure sleeping space. In the Australia co-living market, this format also gives operators a balance between density and tenant appeal. It supports higher occupancy stability because the room itself remains the minimum personal space that most long-stay residents are willing to pay for.

Studio / entire-unit formats served a smaller but more premium renter group in 2025. These layouts appeal to longer-stay tenants, higher-earning professionals, and residents who want flexible housing without sharing the front door. Shared rooms are projected to grow fastest at a 17.00% CAGR through 2031, which shows that affordability pressure is widening the addressable pool beyond the core private-room user base. Larger planned schemes also give developers greater flexibility to mix private, shared, and studio stock within a single property. As the Australia co-living market expands into more cities, operators are likely to use that mix to balance affordability, occupancy, and average revenue per room.

By Business Model: Asset-Light Master Lease / Lease Arbitrage Gain Ground as Capital Seeks Scalable Returns

The asset-heavy own-develop-operate segment accounted for 43% of the market in 2025, indicating that early supply was built by operators willing to commit land, development capital, and direct operating control. This model remains important because it gives full control over design, compliance, amenities, and tenant experience. It also lets owners retain more of the long-term operating upside when properties stabilize. In the Australia co-living market, that approach helped establish the product category before larger pools of capital became active.

Asset-light master lease and lease arbitrage are the fastest-growing models, and the Australia co-living market for this model is projected to expand at a 17.50% CAGR through 2031. This approach is gaining traction because it allows operators to scale through existing buildings rather than only through new construction. Pro-Invest Group’s adaptive reuse strategy illustrates this shift, with the group converting a Sydney hotel asset into 80 flex-living studios as part of a broader urban accommodation platform[3]Pro-Invest Group / The Hotel Conversation, “Pro-Invest Group Secures First Adaptive Reuse Urban Accommodation Asset,” The Hotel Conversation, thehotelconversation.com.au. Management agreements form a third path, especially where institutional owners want an operating partner without transferring asset ownership. That is why the Australia co-living market is moving toward a wider mix of developer-led, lease-led, and manager-led growth models rather than relying on one dominant structure.

By Price Band: Mid-Scale Leads Volume as Premium / Luxury Co-Living Outpaces the Market

Mid-scale properties accounted for 46% of the Australia co-living market size in 2025, which confirms that the core demand base still centers on affordability and value rather than luxury. This band works because it gives residents a visible cost savings compared to a standalone apartment while still preserving quality, management, and amenity standards. It is also the segment that aligns most closely with the income profile of working professionals who need access to major city locations. In practical terms, mid-scale supply remains the volume engine of the Australia co-living market.

Premium / luxury co-living is forecast to grow fastest at an 18.00% CAGR through 2031, and the Australia co-living market size for this tier is expanding from a smaller but increasingly visible base. This segment serves mobile professionals, corporate assignees, and renters who want hotel-style services with more tenancy flexibility than a traditional apartment. Economy co-living continues to matter, but it is constrained by baseline design and management standards that prevent the format from moving too far down the price curve. That leaves the market with a broad middle and a faster-growing premium edge rather than a race to the bottom on price. The result is a pricing structure where affordability drives scale, while premium formats add margin and widen customer reach.

By End User: Working Professionals Anchor Demand as Student Overflow Deepens the Market

Working professionals held 56% of demand in 2025, which made them the largest end-user group in the Australia co-living market. They are also projected to grow at the fastest pace, at 17.30% CAGR through 2031. This combination suggests that the core professional cohort is still underpenetrated rather than close to saturation. Co-living fits this group because it reduces setup costs, shortens search time, and keeps residents closer to employment hubs. It also suits renters whose work arrangements or career stage make long lease commitments less attractive.

Students remain the second major end-user segment and add an important overflow channel to the Australia co-living market. The structural shortage of student accommodation is clear, with purpose-built student accommodation penetration at just over 6% of the student population in 2026. University policy that links enrollment growth to accommodation capacity also strengthens the role of credible managed housing options outside the campus system. This means student demand does not replace the professional renter base; instead, it adds another stable stream of occupancy in areas where urban housing pressure is already high. Over time, the end-user mix should remain professional-led while becoming more diversified in age, income profile, and length of stay.

Geography Analysis

Sydney held 41% of the Australia co-living market share in 2025, which kept it far ahead of every other city segment. The city remains the most established operating base because it combines deep rental demand, strong urban density, and a clearer planning pathway than most other states. In May 2026, the Melrose Park project received planning and rezoning approval for 154 co-living units and 197 affordable housing units, demonstrating that co-living can align with broader housing delivery priorities in Sydney. Sydney also continues to act as the reference market for pricing, design, and institutional interest across the Australia co-living market. Because land is costly and apartment affordability remains stretched, higher-density shared living continues to play a practical role in the city’s rental market.

Melbourne remains the second-ranked city market, although its pipeline has been more limited than its rental demand would suggest. The absence of a formal state-level co-living planning framework and existing land tax settings continue to constrain project momentum. At the same time, Melbourne had the largest purpose-built student accommodation pipeline in Australia in June 2026, indicating that underlying renter demand is strong even as co-living delivery slows. Brisbane is the fastest-growing city segment, with a 18.3% CAGR through 2031, and the Australia co-living market in Brisbane is expanding from a smaller base, supported by migration, infrastructure activity, and strong rental pressure. That growth profile makes Brisbane one of the clearest near-term expansion markets outside Sydney. It also gives operators a chance to scale before the city reaches the maturity seen in the leading New South Wales market.

Perth and the rest of Australia remain earlier-stage opportunities within the Australia co-living market. Western Australia received a net overseas migration of 40,410 in 2024-25, while Perth continued to operate under very tight rental conditions. Perth also led the national student accommodation construction pipeline in June 2026, which indicates stronger investor confidence in rental housing demand more broadly. These markets still lack the supply depth of Sydney and Melbourne, but they offer the clearest room for first-mover advantage, given that formal co-living stock remains limited.

Competitive Landscape

The Australia co-living market remains fragmented, with supply still spread across specialist operators and a small number of emerging institutional platforms. No single operator dominates nationally, and much of the competition remains city-based rather than fully national. This structure gives early movers an advantage in operational knowledge, site sourcing, and execution planning. It also means that scale is being built gradually through new openings, adaptive reuse, and partnerships rather than through a winner-take-all pattern. The Australia co-living market therefore remains open to consolidation, but it has not reached that stage yet.

One of the clearest strategic moves came from Pro-Invest Group, which advanced an adaptive reuse platform for urban accommodation and converted the Coogee Sands Hotel and Apartments into an 80-studio flex-living project scheduled to open in late 2026. A second move came through the Pro-Invest and Kajima joint venture, which added an initial AUD 500 million (USD 318 million) of equity to build-to-rent development plans and signaled a stronger long-term capital commitment to flexible urban rental formats. A third move came from the approved Melrose Park scheme in Sydney, which showed how developers are pairing co-living with affordable housing within larger mixed projects. These actions matter because they expand the competitive field beyond small stand-alone properties. They also show that scale in the Australia co-living market will likely come from integrated platforms rather than only from one-off buildings.

Technology and operations are becoming increasingly important as platforms grow. EQT’s December 2025 investment in PropertyMe showed that institutional investors see property management software as a key layer in the operating stack for the living sector. MRI Software’s acquisition of Proptech Labs in October 2025 moved in the same direction by adding maintenance, invoicing, inspections, and automation tools to property management workflows in Australia and New Zealand. As operating platforms become more data-driven, larger groups should gain an edge in retention, response time, and cost control. That shift will not erase fragmentation immediately, but it will gradually raise the execution bar across the Australia co-living market.

Australia Co-Living Industry Leaders

UKO

The Switch

CDA Coliving

Tribe Property Group

Freecity Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The New South Wales Department of Planning, Housing and Infrastructure granted planning and rezoning approval for a mixed development at Melrose Park, Sydney, comprising 154 co-living units and 197 affordable housing units, marking the first project to achieve Concurrent Rezoning under the Housing Australia Future Fund Housing Delivery Authority (HDA) pathway. The AUD 136 million (approximately USD 86 million) project is expected to house over 700 co-living residents; Evolve Housing will own the affordable component under a 25-year HAFF funding arrangement.

- May 2026: Pro-Invest Group, in partnership with MEC Global Partners Asia, acquired the Coogee Sands Hotel & Apartments in Sydney as its first urban accommodation asset. The property is being redeveloped through adaptive reuse into an 80-studio flex-living development and is scheduled to open in Q4 2026, following the launch of Pro-Invest Group's proprietary accommodation brand and the commencement of guest bookings in Q3 2026. The project serves as the seed asset for the group's AUD 500 million urban accommodation platform targeting approximately 2,000 apartments across Australia.

- June 2025: Pro-Invest Group and Kajima Corporation announced a joint venture to develop ground-up build-to-rent properties across Australia with an initial equity commitment of AUD 500 million (USD 318 million) and a stated ambition to scale assets under management to AUD 1.5 billion (USD 952 million) over five years. The joint venture's first project is a 300-unit development in Sydney; the partnership supplements Pro-Invest's separate adaptive reuse co-living platform.

Australia Co-Living Market Report Scope

The Australia Co-Living Market Report is Segmented by Property Configuration (Studio / Entire Unit, Private Room, and Shared Room), Business Model (Asset-Light Master Lease / Lease Arbitrage and More), Price Band (Economy, Mid-Scale, and Premium / Luxury), End User (Students, and Working Professionals), and City (Sydney, Melbourne, Brisbane, Perth, and Rest of Australia). The Market Forecasts are Provided in Terms of Value (USD).

| Studio / Entire Unit |

| Private Room |

| Shared Room |

| Asset-Light Master Lease / Lease Arbitrage |

| Asset-Light Management Agreement |

| Asset-Heavy Own-Develop-Operate |

| Economy |

| Mid-Scale |

| Premium / Luxury |

| Students |

| Working Professionals |

| Sydney |

| Melbourne |

| Brisbane |

| Perth |

| Rest of Australia |

| By Property Configuration | Studio / Entire Unit |

| Private Room | |

| Shared Room | |

| By Business Model | Asset-Light Master Lease / Lease Arbitrage |

| Asset-Light Management Agreement | |

| Asset-Heavy Own-Develop-Operate | |

| By Price Band | Economy |

| Mid-Scale | |

| Premium / Luxury | |

| By End User | Students |

| Working Professionals | |

| By City | Sydney |

| Melbourne | |

| Brisbane | |

| Perth | |

| Rest of Australia |

Key Questions Answered in the Report

What is the projected value of Australia’s co-living space by 2031?

The Australia co-living market is forecast to reach USD 0.35 billion by 2031, rising from USD 0.16 billion in 2026 at a 16.95% CAGR over 2026-2031.

What is driving demand for shared urban living in Australia?

The strongest demand drivers are housing undersupply, record rental pressure, and continued migration inflows. The National Housing Supply and Affordability Council's (NHSAC) reported that lease costs absorbed 33% of median household income in 2026.

Which city leads co-living activity in Australia?

Sydney leads the country with 41% of revenue in 2025 and remains the most established location for planning, operating scale, and new project approvals.

Which renter group is most important for operators?

Working professionals are the core tenant base, holding 56% of demand in 2025 and posting the fastest projected end-user growth at 17.30% through 2031.

Page last updated on: