Augmented and Virtual Reality In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

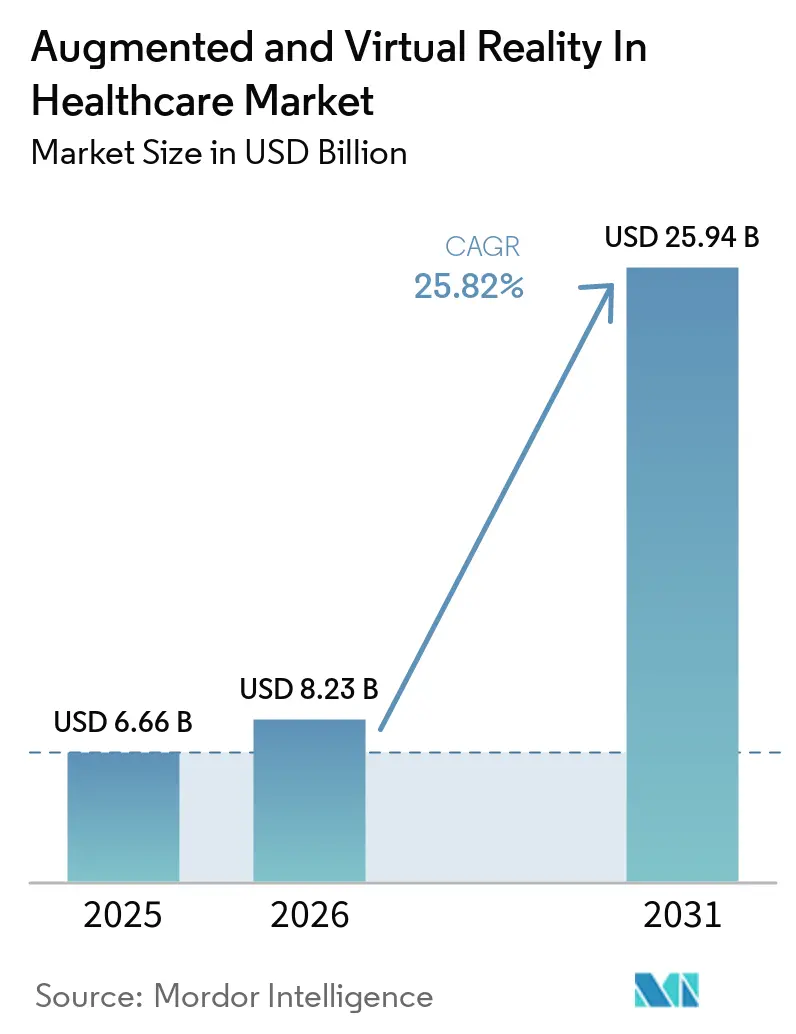

| Market Size (2026) | USD 8.23 Billion |

| Market Size (2031) | USD 25.94 Billion |

| Growth Rate (2026 - 2031) | 25.82% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Augmented and Virtual Reality In Healthcare Market Analysis by Mordor Intelligence

The Augmented And Virtual Reality In Healthcare Market size is expected to increase from USD 6.66 billion in 2025 to USD 8.23 billion in 2026 and reach USD 25.94 billion by 2031, growing at a CAGR of 25.82% over 2026-2031.

The market is growing because healthcare providers need safer training tools, more providers now accept immersive simulation in routine education, and the number of FDA-authorized AR and VR medical devices reached 104 by February 2026, which improved buying confidence among hospitals and clinical teams. The augmented and virtual reality in healthcare market is also benefiting from a widening gap between training demand and expert supervision capacity, which makes simulation platforms easier to justify in large teaching systems. A second shift is visible in the buying model, where hospitals still start with hardware purchases but increasingly move toward recurring software content and managed service contracts once the installed base is in place. The augmented and virtual reality in healthcare market is also separating into different adoption paths, with augmented reality holding the larger installed clinical base and virtual reality moving faster because it can be deployed in simulation labs, classrooms, and home care settings with less infrastructure friction. Competitive activity remains active because specialist XR firms are building depth in surgery and therapy while larger medtech groups are folding immersive tools into broader imaging and procedural ecosystems.

Key Report Takeaways

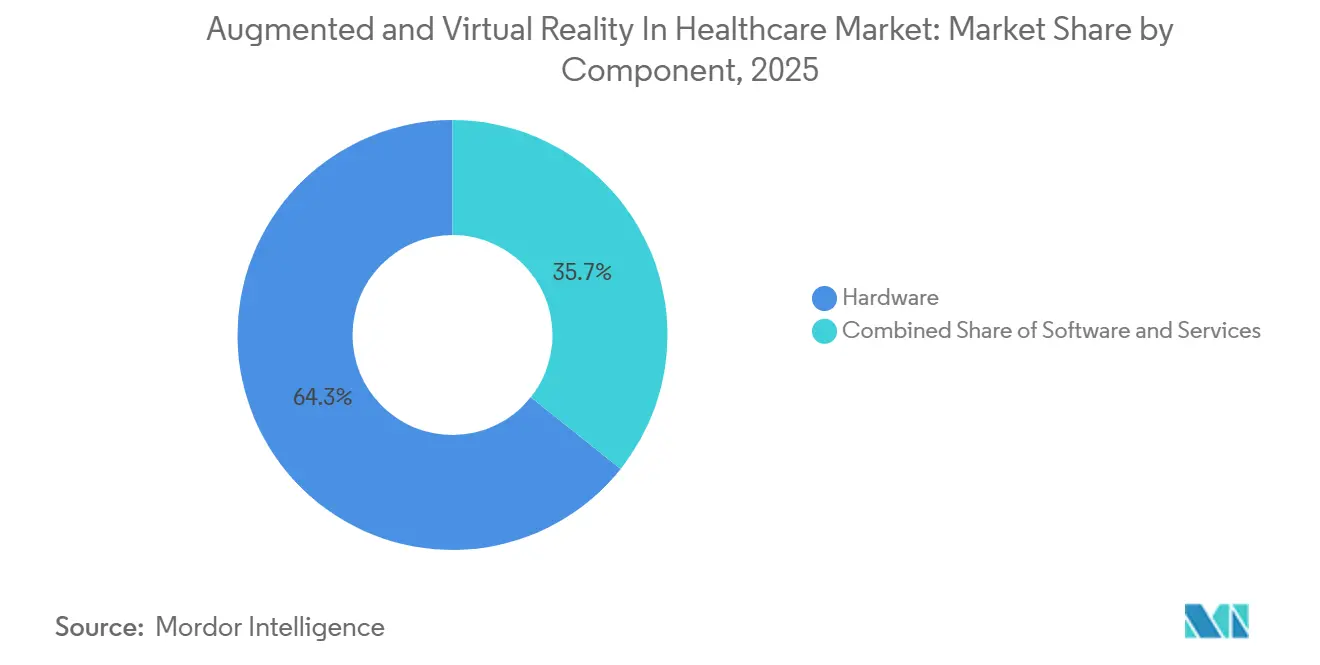

- By component, hardware held 64.31% of the augmented and virtual reality in healthcare market share in 2025, while services are projected to expand at a 26.33% CAGR through 2031.

- By technology, augmented reality held 57.68% share in 2025, while virtual reality is projected to grow at a 28.36% CAGR through 2031.

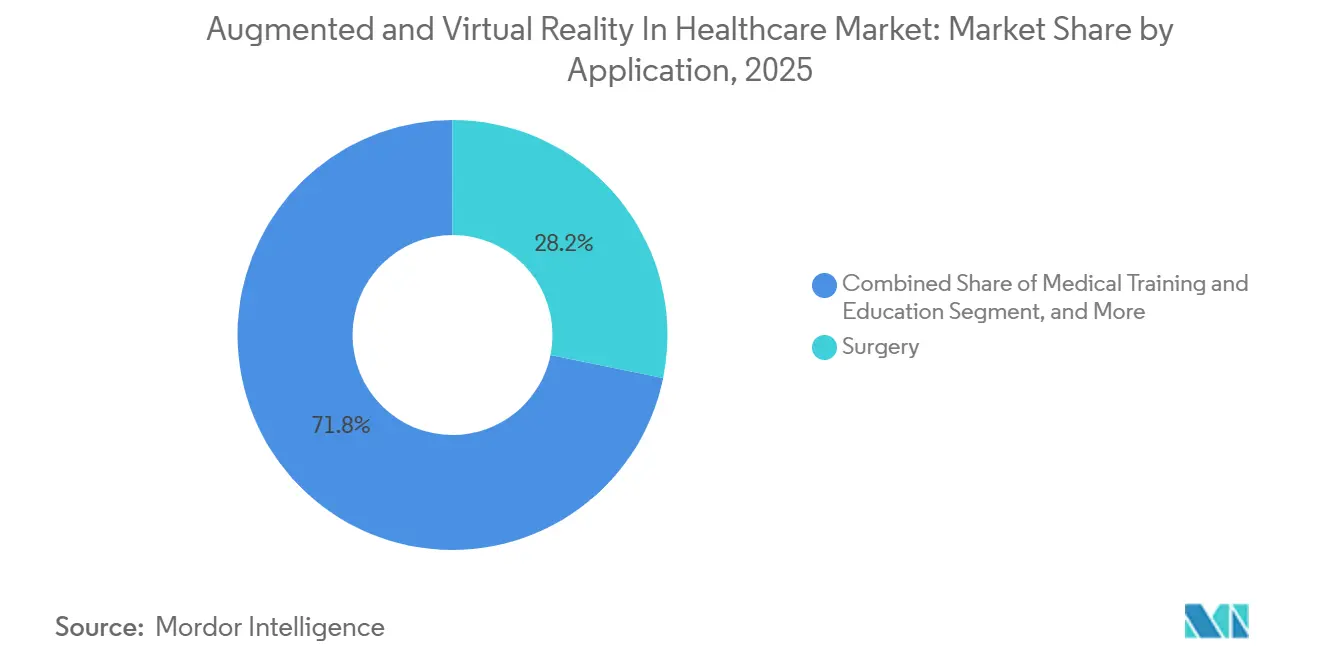

- By application, surgery accounted for 28.16% share of the augmented and virtual reality in healthcare market size in 2025, while medical training and education is forecast to expand at a 26.78% CAGR through 2031.

- By end user, hospitals held 38.62% share in 2025, while academic and research institutes are projected to grow at a 29.08% CAGR through 2031.

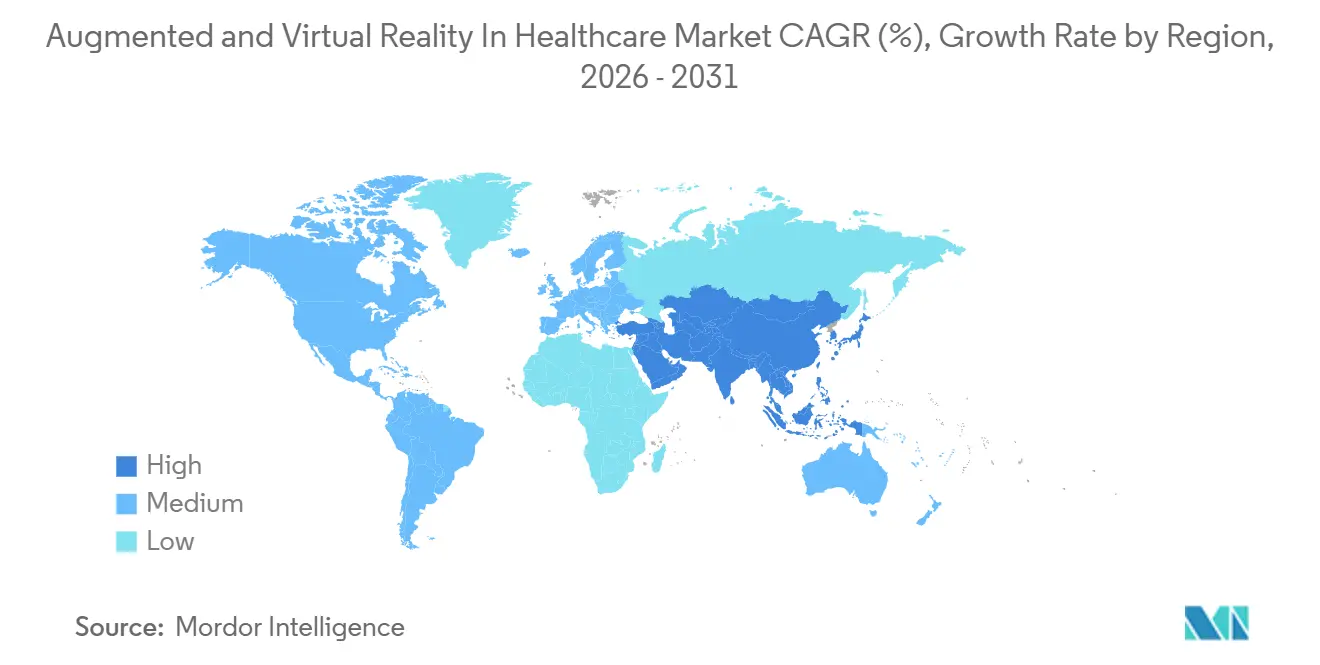

- By geography, North America held 42.64% share in 2025, while Asia-Pacific is projected to expand at a 27.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Augmented and Virtual Reality In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Need for Risk-Free Clinical Training | +5.5% | Global | Short term (≤ 2 years) |

| Expansion of Remote Care, Telemedicine, and Telementoring | +4.2% | North America and Asia-Pacific | Medium term (2-4 years) |

| Rising Use in Surgical Visualization and Procedure Guidance | +4.8% | North America and Europe | Medium term (2-4 years) |

| Increasing Adoption of Pain Distraction and Behavioral Therapy | +2.8% | North America and Europe | Short term (≤ 2 years) |

| AI-Enabled Scenario Analytics and Adaptive Learning | +3.5% | North America and Asia-Pacific | Medium term (2-4 years) |

| Falling Device Costs and Faster Enterprise Procurement Cycles | +3.1% | Asia-Pacific and Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Need for Risk-Free Clinical Training

Clinical education is facing a structural shortfall because training time is tighter, and real case exposure is harder to scale. A 2026 JMIR Medical Education review covering 11 randomized and prospective studies across 7 surgical specialties found that augmented reality training reduced technical errors in all 5 studies that measured them and shortened learning curves for novice trainees.[1]JMIR Medical Education, “Augmented Reality in Surgical Training: Systematic Review of Its Impact on Technical Performance in Surgical Trainees,” JMIR Medical Education, mededu.jmir.org The same review found weaker gains for experienced surgeons, which means the strongest commercial demand is concentrated in early-stage training rather than expert refresh programs. A May 2026 JMIR Perioperative Medicine study also found that a single virtual reality session improved orthopedic trauma task completion time and self-rated competence, and participants viewed the format as useful in low-resource settings. In the augmented and virtual reality in healthcare market, this demand pattern favors residency programs, hospital systems with large trainee cohorts, and education networks that need more repetitions without adding live patient risk.

Expansion of Remote Care, Telemedicine, and Telementoring

Remote clinical support is becoming more practical because augmented overlays now improve how mentors guide trainees during procedures. A March 2026 usability study in JMIR Human Factors showed that dynamic augmented reality cues helped trainees follow remote instructions with fewer errors than gesture-based or pointer-based guidance, without raising cognitive load.[2]JMIR Human Factors, “Dynamic Augmented Reality Cues for Telementoring in Laparoscopic Surgery: Usability Study,” JMIR Human Factors, humanfactors.jmir.org The American College of Surgeons also published protocols in April 2026 that described safe and scalable telementoring frameworks built around high-definition video, low-latency guidance tools, and secure audiovisual platforms. A 2025 Journal of Robotic Surgery review noted that emerging 5G and XR combinations are important for low-latency surgical training systems, which matters most in settings that need real-time guidance across distance. In the augmented and virtual reality in healthcare market, countries with advanced 5G rollouts, such as South Korea, Japan, and China, are positioned to adopt remote AR-assisted care and training faster than markets with weaker network readiness.

Rising Use in Surgical Visualization and Procedure Guidance

Surgical visualization is moving from pilot use to repeatable clinical use, especially in spine and orthopedic procedures. The FDA device list shows a growing base of authorized AR and VR medical devices, which has made immersive guidance easier to position as part of mainstream digital surgery rather than a niche experiment. A 2026 Frontiers in Medicine study documented a clinical case that combined 3D visualization, augmented reality, and magnetic-assisted robotic surgery across multiple specialties, which shows that these tools are increasingly being deployed together.[3]Frontiers in Digital Health, “Artificial Intelligence, Extended Reality, and Emerging AI-XR Integrations in Medical Education,” Frontiers in Digital Health, frontiersin.org Spain’s Hospital Clínico San Carlos also used AI-fused augmented reality overlays during percutaneous coronary interventions in 2025, which showed that intraoperative use is spreading beyond a small set of U.S. reference centers. In the augmented and virtual reality in healthcare market, this supports higher value use cases where clinicians want better spatial awareness without losing direct visibility of the patient.

AI-Enabled Scenario Analytics and Adaptive Learning

AI is changing immersive training from static content delivery into a system that can adjust to learner performance. Frontiers in Digital Health mapped how AI supports intelligent tutoring, virtual patient simulation, and predictive analytics inside XR-based medical education, which allows learning paths to adapt with far less manual setup. This matters because traditional simulation libraries are expensive to configure and often depend on scarce expert time. Adaptive training design also improves scalability, since a larger part of the feedback loop can be embedded in the platform instead of being delivered live by faculty. In the augmented and virtual reality in healthcare market, vendors that combine immersive content with AI-led assessment are better placed to serve institutions that need more throughput without matching increases in specialist staffing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Integration and Content Creation Costs | -2.5% | Global, especially Asia-Pacific developing markets | Short term (≤ 2 years) |

| Regulatory Uncertainty Across Clinical Use Cases | -1.8% | Global | Medium term (2-4 years) |

| Limited Clinical Workflow Integration and Staff Readiness | -1.5% | Europe and Asia-Pacific | Medium term (2-4 years) |

| Data Privacy, Security, and Patient Consent Complexity | -1.2% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Integration and Content Creation Costs

Cost remains the clearest short-term barrier, especially for community hospitals and smaller systems. A 2025 ITIF review noted that many U.S. hospitals were still operating under margin pressure, which limited discretionary technology spending even when immersive training could lower long-run costs. The upfront burden includes headsets, software licenses, onboarding, workflow setup, and custom content creation for specific specialties. A 2025 Scientific Reports study found that hybrid virtual reality models can improve cost effectiveness by reducing reliance on expensive physical simulators while preserving useful training fidelity. In the augmented and virtual reality in healthcare market, this is one reason services are growing faster than hardware, because subscriptions spread content and support costs across a wider user base.

Regulatory Uncertainty Across Clinical Use Cases

Regulation is becoming clearer in surgical navigation, but it remains less settled in therapy, pain management, and behavioral care. The European Union’s Medical Device Regulation requires evidence that is aligned with device risk, which makes software-based therapeutic pathways more demanding than many hardware deployments. The FDA’s February 2026 list showed 104 AR and VR device decisions, but only 2 of them were De Novo authorizations, which means many companies are still entering through predicate-based clearance rather than a new therapeutic framework. That helps near-term entry, but it does not answer the reimbursement question because coverage still depends on evidence tied to the specific intended use. In the augmented and virtual reality in healthcare market, countries without a comparable predicate pathway face slower commercialization even when hospital and clinician demand is already present.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware-led deployment gives way to services economics

Hardware held 64.31% of the augmented and virtual reality in healthcare market share in 2025 because hospitals first spent on head-mounted displays, AR headsets, and haptic peripherals before they expanded software and service budgets. This pattern reflects an early deployment phase where clinical sites need the physical device layer in place before they can scale content, analytics, and workflow tools. It also means that current hardware installations create a base for recurring revenue over the next several years. In the augmented and virtual reality in healthcare market, this installed base is shaping a broader transition from one-time purchases toward longer contractual relationships.

Services are projected to grow at 26.33% CAGR through 2031 because health systems increasingly prefer subscription-based content libraries and managed training contracts over building content alone. This shift shows that the augmented and virtual reality in healthcare industry is moving toward a model closer to healthcare software platforms than pure device sales. Vendors that manage onboarding, content refresh, and usage analytics are likely to capture more value once a hospital has already committed to immersive deployment. Software remains the middle layer by share, and its role is expanding as content libraries cover more specialties and as adaptive learning tools move into commercial use.

By Technology: AR holds scale, VR captures faster expansion

Augmented reality held 57.68% share in 2025 because surgeons need to keep direct visibility of the patient during intraoperative guidance and navigation. That made AR the better fit for spine, orthopedic, and image-guided workflows where overlays support action without blocking the field of view. Its lead also reflects stronger clinical alignment with procedures that already carry high value and high documentation standards. In the augmented and virtual reality in healthcare market, AR therefore benefits most from procedural use cases that reward precision, workflow fit, and operating room acceptance.

Virtual reality is projected to grow at 28.36% CAGR through 2031 because it can be deployed with fewer infrastructure demands across training, rehabilitation, behavioral therapy, and pain management. A 2025 study in npj Digital Medicine found that telehealth virtual reality reduced pain intensity, anxiety, and sleep disturbance in patients with chronic pain conditions, which supports wider use beyond hospital walls. Standalone VR systems are also easier to use in classrooms, simulation labs, and home settings because they do not depend on the same spatial mapping needs as AR-guided clinical systems. Within the augmented and virtual reality in healthcare industry, this creates two distinct commercial paths, one tied to high-acuity procedure support and the other tied to scalable education and therapy delivery.

By Application: Surgery anchors current value while training drives the next wave

Surgery accounted for 28.16% share of the augmented and virtual reality in healthcare market size in 2025 because procedures carry high reimbursement value and a strong clinical need for spatial guidance, rehearsal, and post-case review. This segment includes pre-surgical planning, intraoperative overlays, and post-procedure visualization, each of which solves a different workflow problem. The concentration of regulatory clearances around surgical guidance has also supported this leadership because hospitals can buy into a category with clearer validation. In the augmented and virtual reality in healthcare market, surgery remains the strongest near-term revenue pool because clinical risk and technology value are closely matched.

Medical training and education are projected to grow at 26.78% CAGR through 2031 because medical schools, residency programs, and hospital credentialing systems are embedding immersive simulation into more formal learning pathways. A 2026 Frontiers in Medicine scoping review found that XR modalities are now used across anatomy teaching, emergency response, procedural rehearsal, and surgical training in U.S. healthcare education, with 60% of reviewed studies showing measurable knowledge gains. Behavioral therapy and patient care management are smaller today, but they remain strategically important because FDA-authorized prescription VR for chronic lower back pain has already moved beyond proof of concept. Medical imaging is also emerging as a meaningful niche because mixed-reality ultrasound tools have shown that novice users can move closer to expert spatial accuracy with real-time 3D visualization.

By End User: Hospitals lead spending while academic institutes deepen the evidence base

Hospitals held 38.62% share in 2025 because they are the main buyers of surgical navigation AR, intraoperative visualization systems, and higher acuity rehabilitation platforms. Their buying logic is tied to outcome improvement, procedural differentiation, and the rising expectation that complex procedures should be supported by validated simulation training. Hospitals also have the broadest mix of departments that can reuse immersive assets across surgery, nursing education, and rehabilitation. In the augmented and virtual reality in healthcare market, that makes hospitals the main commercial gateway even when the first proof points come from academic settings.

Academic and research institutes are projected to grow at 29.08% CAGR through 2031 because they serve both as early adopters and as the institutions that generate publishable validation. OTH Regensburg launched its VReduMED mobile VR lab in July 2025 and deployed VR systems free of charge to nursing schools, which showed how immersive learning can move beyond flagship university programs into routine healthcare education. Surgical centers are a strong opportunity because they often face lower integration complexity than large academic hospitals and can adopt simulation tools with shorter procurement cycles. Clinics, diagnostic centers, and life sciences companies are also relevant users, especially where immersive tools improve anxiety management, staff training, and commercial education programs.

Geography Analysis

North America held 42.64% of the augmented and virtual reality in healthcare market share in 2025, supported by a mature FDA pathway and a strong base of hospital and academic early adopters. The United States accounts for most of this regional weight because it combines venture-backed specialist firms, large health systems, and a reimbursement environment that is slowly becoming more open to digital therapeutics. MindMaze Therapeutics reported that it achieved a CMS Category III reimbursement code in 2025 for home-based digital neurorehabilitation, which marked an important step for home VR therapy coverage in the U.S. Canada is also contributing through research-led AR surgical guidance development, which adds depth to the regional innovation base.

Europe remains the second-largest region, with Germany, the UK, and France leading institutional adoption. Germany embedded AR scenarios into formal medical education at Martin Luther University Halle-Wittenberg in 2025, which showed that immersive training is entering structured curricula rather than staying in isolated pilots. T-Systems and Universitätsklinikum Bonn also developed a VR nurse training platform with AI-driven patient avatars, which reduced geographic barriers in staff training. France has added procedural momentum through AR-guided orthopedic surgery and mixed-reality shoulder procedures, which signals that adoption is spreading through real hospital use rather than only through research centers.

Asia-Pacific is the fastest-growing part of the augmented and virtual reality in healthcare market size, with a projected 27.92% CAGR through 2031. Regional growth is being driven by healthcare modernization in China and India, strong 5G readiness in South Korea, and a large medical student base that makes scalable simulation more attractive. A 2025 global mixed-methods study highlighted practical digital transformation workshops at Shenzhen’s Longgang District Hospital, which showed that immersive tools can be integrated across healthcare settings with different infrastructure conditions. South America and the Middle East and Africa are smaller today, but they remain structurally important because public hospitals in Argentina have already used AR-assisted surgery and Gulf health systems continue to include immersive tools in smart hospital programs. In the augmented and virtual reality in healthcare market, these regions matter less for present scale and more for the speed at which validated models can be transferred into newer digital health programs.

Competitive Landscape

The augmented and virtual reality in healthcare market remains moderately fragmented, with no single company holding more than a low-double-digit share across all applications. Competition is split between diversified medtech groups such as Siemens Healthineers, GE HealthCare, Koninklijke Philips, and Intuitive Surgical, and specialist firms such as Osso VR, Augmedics, Medivis, Surgical Theater, FundamentalXR, AppliedVR, and MindMaze. The larger medtech groups benefit from installed clinical relationships and can add immersive functions into imaging or procedural platforms that hospitals already use. The specialists compete more on content depth, workflow design, outcomes evidence, and speed inside narrow clinical use cases.

Osso VR and similar training-focused firms benefit from a growing preference for evidence-based simulation, where buyers want measurable proof that immersive learning improves performance. Augmedics and other surgery-focused firms are positioned around procedure-specific utility, which makes their adoption path different from therapy or classroom vendors. AppliedVR is more directly relevant to the augmented and virtual reality in healthcare market than broad medtech companies without disclosed XR programs because its RelieVRx platform already has FDA authorization in chronic lower back pain and fits the behavioral therapy segment described in the report. MindMaze strengthened its commercial position in May 2026 through a channel partnership with Vibra Healthcare to scale its FDA-cleared neurotherapeutics platform across U.S. health systems. HealthpointCapital’s June 2025 acquisition of ImmersiveTouch also showed that investors see value in consolidating procedure-focused XR platforms around musculoskeletal and trauma applications.

The augmented and virtual reality in healthcare market is also changing because competitive advantage is shifting away from simple headset access and toward reimbursement readiness, adaptive content, and integration quality. Firms that can show fit with hospital workflows, payer expectations, and measurable training outcomes are likely to defend pricing better than firms that only sell devices. This dynamic also explains why academic validation and hospital deployment often move together, since published evidence helps unlock broader procurement. The augmented and virtual reality in healthcare market therefore rewards companies that can bridge clinical evidence, software delivery, and enterprise adoption rather than relying on hardware novelty alone.

Augmented and Virtual Reality In Healthcare Industry Leaders

GE HealthCare

Hologic, Inc.

Koninklijke Philips N.V.

Siemens Healthineers

XRHealth

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: MindMaze Therapeutics and Vibra Healthcare signed a definitive channel partnership agreement to scale MindMaze's FDA-cleared digital neurotherapeutics platform across leading US health systems, with the partnership expected to be a primary driver of new customer acquisition in H2 2026; the collaboration follows a two-year multi-site RWE study demonstrating technology-enabled high-dose neurorehabilitation significantly enhances stroke recovery.

- April 2026: Pixee Medical received FDA 510(k) clearance (K253805) for its Knee+ AR-guided knee arthroplasty system, extending its European market presence (where the NextAr system already achieved CE marking for knee and shoulder applications) to the US orthopedic market.

- January 2026: Medacta International received FDA 510(k) clearance (K252847) for the NextAR Hip Platform in 123 days, demonstrating a shortening review cycle as FDA develops institutional familiarity with AR-guided orthopedic navigation as a device category.

- November 2025: Augmedics received a new 510(k) clearance (K251639) for an updated version of its xvision Spine System, reinforcing its regulatory foundation for expanded US commercial deployment of AR-guided spinal surgery and maintaining its position as the primary cleared AR spine navigation platform

Global Augmented and Virtual Reality In Healthcare Market Report Scope

The Augmented and Virtual Reality in Healthcare Market refers to the use of immersive AR and VR technologies to improve patient care, medical training, diagnostics, and treatment outcomes. These tools overlay digital information onto real-world environments (AR) or create fully simulated environments (VR), enabling enhanced visualization, simulation, and interactivity in healthcare.

The Augmented and Virtual Reality in Healthcare Market is segmented across multiple dimensions that capture the breadth of technologies, applications, and end users. By component, it includes Hardware, Software, and Services. By technology, the market is divided into Augmented Reality and Virtual Reality. By application, AR and VR are used in Surgery, Medical Training and Education, Patient Care Management, Fitness Management, Behavioral Therapy, and Medical Imaging. By end user, the market serves Hospitals, Academic and Research Institutes, Surgical Centers, Clinics and Diagnostic Centers, and Pharma and Life Sciences Companies.

Geographically, the market spans North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe), Asia‑Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Middle East & Africa (GCC, South Africa, Rest of MEA), and South America (Brazil, Argentina, Rest of South America).

| Hardware |

| Software |

| Services |

| Augmented Reality |

| Virtual Reality |

| Surgery |

| Medical Training and Education |

| Patient Care Management |

| Fitness Management |

| Behavioral Therapy |

| Medical Imaging |

| Hospitals |

| Academic and Research Institutes |

| Surgical Centers |

| Clinics and Diagnostic Centers |

| Pharma and Life Sciences Companies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Technology | Augmented Reality | |

| Virtual Reality | ||

| By Application | Surgery | |

| Medical Training and Education | ||

| Patient Care Management | ||

| Fitness Management | ||

| Behavioral Therapy | ||

| Medical Imaging | ||

| By End User | Hospitals | |

| Academic and Research Institutes | ||

| Surgical Centers | ||

| Clinics and Diagnostic Centers | ||

| Pharma and Life Sciences Companies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast value of augmented and virtual reality in healthcare by 2031?

The augmented and virtual reality in healthcare market is expected to reach USD 25.94 billion by 2031, rising from USD 8.23 billion in 2026 at a 25.82% CAGR over 2026-2031.

Why is adoption rising so quickly in clinical training?

Hospitals and academic centers need safer and more scalable training, and published 2026 studies showed lower technical errors and faster learning for novice trainees using immersive tools.

Which technology is growing faster, AR or VR?

VR is growing faster at 28.36% CAGR because it is easier to deploy across training, rehabilitation, pain care, and home-based use, while AR held the larger 57.68% share in 2025.

Which application currently brings in the most revenue?

Surgery led with 28.16% share in 2025 because high-value procedures justify spending on navigation, visualization, and rehearsal tools.

Which end users are driving the strongest growth?

Hospitals remained the largest end user at 38.62% share in 2025, while academic and research institutes are growing fastest at 29.08% CAGR because they validate and scale immersive training models.

Which region offers the strongest near-term growth opportunity?

Asia-Pacific stands out with a 27.92% CAGR through 2031, supported by healthcare modernization, 5G readiness, and a large student and trainee base.

Page last updated on: