At-Home Peptic Ulcer Testing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 317.76 Million |

| Market Size (2030) | USD 438.03 Million |

| Growth Rate (2025 - 2030) | 6.63% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

At-Home Peptic Ulcer Testing Market Analysis by Mordor Intelligence

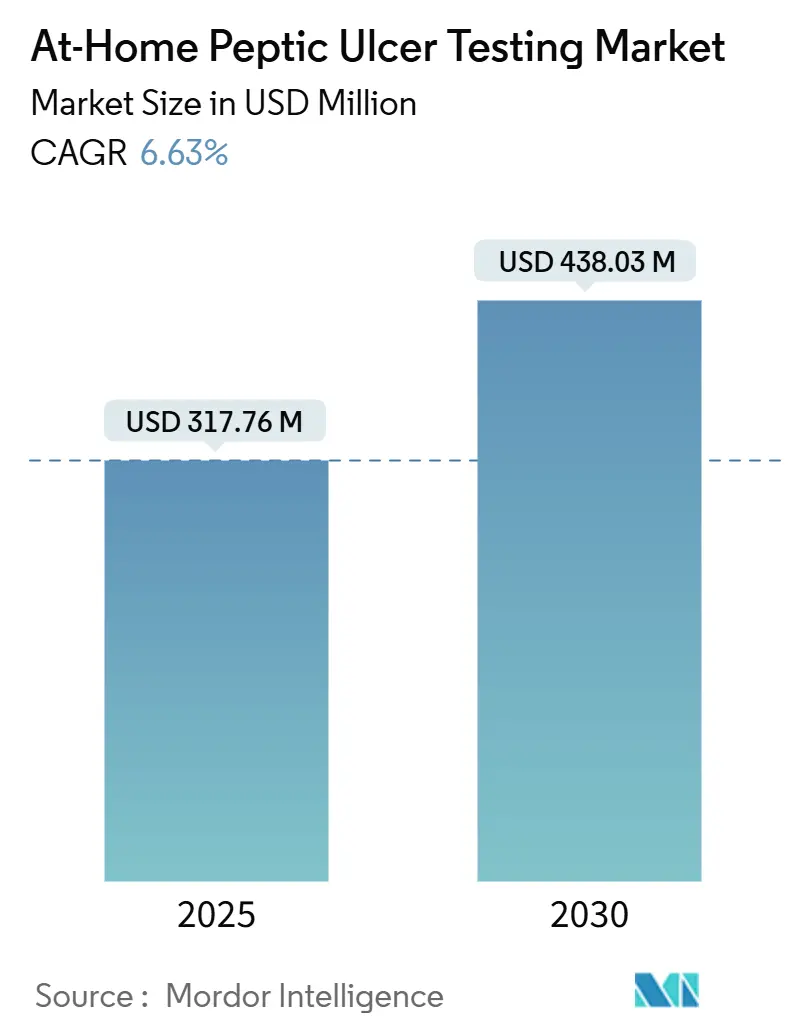

The At-Home Peptic Ulcer Testing Market size is estimated at USD 317.76 million in 2025, and is expected to reach USD 438.03 million by 2030, at a CAGR of 6.63% during the forecast period (2025-2030).

Demand accelerates as payers replace invasive endoscopy with home-based Helicobacter pylori detection, regulators tighten evidence expectations for lay-user kits, and aging populations in Asia and Europe sustain prevalence rates that exceed 50% among individuals aged 60 and above [1]World Health Organization, “Helicobacter pylori Prevalence and Gastric Cancer Risk,”. Category legitimacy also rises after the U.S. Food and Drug Administration excluded home-collection devices from enforcement discretion in its May 2024 laboratory-developed test rule, compelling manufacturers to meet full medical-device standards yet giving institutional buyers confidence in product quality [2]U.S. Food and Drug Administration, “Laboratory Developed Tests Final Rule,” . Meanwhile, direct-to-consumer (DTC) platforms bundle diagnostic kits with telehealth prescriptions, converting a positive result into therapy within hours and driving channel preference among consumers who value convenience over clinic visits. Finally, retail pharmacies upgrade wellness clinics to perform point-of-care testing, positioning themselves as treatment gateways for dyspepsia and mild ulcer symptoms and capturing referral flows that once defaulted to hospital laboratories.

Key Report Takeaways

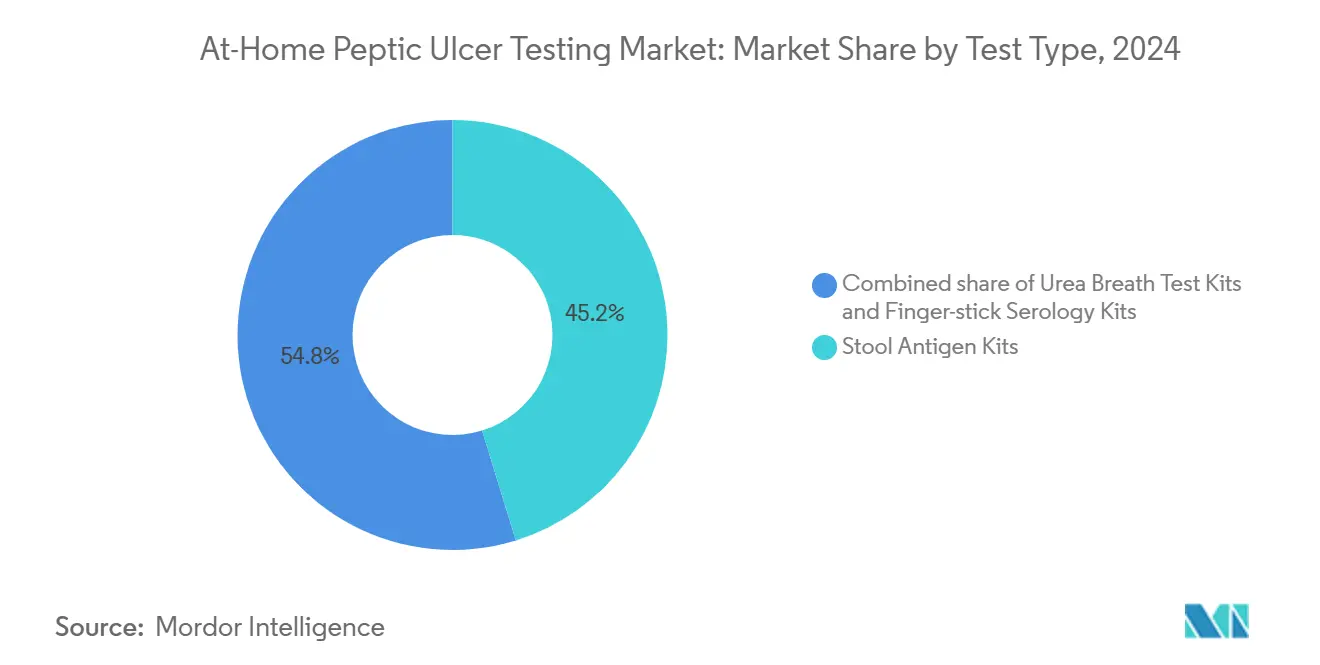

- By test type, stool antigen kits captured 45.23% of at-home peptic ulcer testing market share in 2024, while finger-stick serology is forecast to expand at a 12.34% CAGR through 2030.

- By distribution channel, online direct-to-consumer models held 55.1% share of the at-home peptic ulcer testing market size in 2024, whereas retail pharmacies are advancing at a 13.8% CAGR between 2025 and 2030.

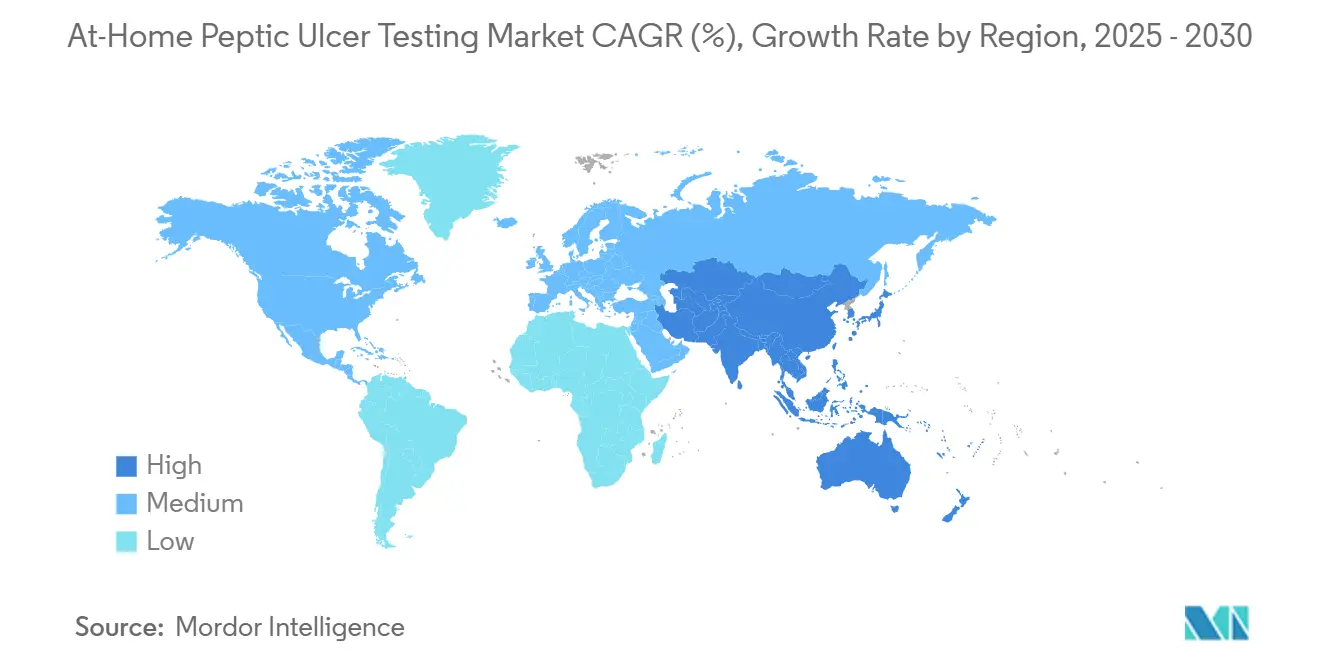

- By geography, North America led with 37.22% revenue share in 2024; Asia-Pacific is projected to record the fastest regional CAGR at 9.67% to 2030.

Global At-Home Peptic Ulcer Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift from invasive endoscopy to non-invasive home diagnostics | +1.8% | North America, Western Europe | Medium term (2-4 years) |

| Growth of direct-to-consumer lab testing platforms | +1.5% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Rising H. pylori prevalence in aging populations | +1.2% | Asia-Pacific, Eastern Europe, Latin America | Long term (≥ 4 years) |

| Retail pharmacy test-to-treat programs | +1.0% | United States, United Kingdom, Australia | Medium term (2-4 years) |

| AI-enabled quantitative breath analyzers | +0.9% | United States, Germany, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift From Invasive Endoscopy to Non-Invasive Home Diagnostics

Endoscopy carries a perforation risk ranging from 0.03% to 0.1%, and sedation complications escalate among elderly patients, prompting gastroenterology societies to recommend non-invasive first-line testing for uncomplicated dyspepsia. A 2025 National Institutes of Health study confirmed that lay-administered stool antigen kits match clinical accuracy thresholds, satisfy patient comfort expectations, and materially reduce hospital throughput pressure. Payers reinforce the movement because a USD 16 home test plus a USD 15 telehealth consultation costs roughly one-tenth of an outpatient endoscopy episode. Supply-demand mismatches intensify this preference: India maintains only 0.5 gastroenterologists per 100,000 people versus 4.6 per 100,000 in the United States, converting home diagnostics from a convenience solution into a capacity-expansion tool. The underlying regulatory landscape solidified when the FDA’s March 2024 guidance mandated lay-user validation, a move that increased development costs but delivered the product rigor clinicians expect.

Growth of Direct-To-Consumer Lab Testing Platforms

Direct-to-consumer operators circumvent traditional gatekeeping by shipping collection kits straight to patients, then delivering results through secure portals that trigger telehealth prescriptions. This model dominated with 55.1% distribution share in 2024, supported by policies allowing lab-initiated testing without a prior prescription in 37 U.S. jurisdictions. Kihealth integrated an H. pylori stool antigen assay into a USD 99 subscription wellness bundle in August 2024, demonstrating how recurring touchpoints can monetize gut-health enthusiasm beyond one-off testing. Logistics remain the Achilles’ heel: stool samples lose antigen stability beyond 48 hours at ambient temperature, and platforms that underinvest in cold-chain shipping experience false-negative rates above 10%, inviting Food and Drug Administration scrutiny. Competitive defenses therefore rely on turnaround-time guarantees and physician network depth rather than on proprietary assay technology.

Rising H. pylori Prevalence in Aging Populations

Global H. pylori prevalence hits 44%, climbing above 50% among adults older than 60 in Asia, Latin America, and parts of Eastern Europe. Japan subsidizes eradication therapy regardless of symptoms to mitigate escalating gastric-cancer risk in a population where 29% are now over age 65. China recorded an 18% increase in hospitalization for peptic ulcer disease among seniors (70+) between 2019 and 2024, attributing the rise to polypharmacy and persistent bacterial infection. Home testing sidesteps mobility and specialty-care barriers that particularly burden older adults in rural areas, enabling caregivers to manage the diagnostic process with minimal clinical supervision. Macro-demographics further inflate demand: the United Nations projects that the 60-plus cohort will double to 2.1 billion people by 2050, with the steepest growth occurring in regions already battling high seroprevalence.

Retail-Pharmacy Test-To-Treat Programs Bundling H. pylori Kits

Retail pharmacies increasingly embed gastrointestinal diagnostics alongside vaccination and chronic-disease monitoring. Boots UK validated the model by launching finger-prick micronutrient tests in March 2024, creating operational blueprints for adding rapid H. pylori serology. In the United States, Walgreens and CVS extend pandemic-era test-to-treat workflows to peptic-ulcer management through collaborative practice agreements that now cover 23 states. Pharmacists follow protocol algorithms: review positive results, counsel on antibiotic regimens, and dispense triple therapy on the spot. Economics line up because pharmacies generate margin on both the kit and the prescription, while insurers avoid costly emergency-department episodes from bleeding ulcers. Friction persists where over-the-counter status remains unavailable; pharmacies must link with physician networks to bridge the prescription gap, slowing rollout in restrictive jurisdictions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Variable accuracy of at-home serology vs active-infection tests | -0.7% | Global | Short term (≤ 2 years) |

| Stringent FDA/CE evidence for home-use labeling | -0.5% | North America, Europe | Medium term (2-4 years) |

| Tariff-driven cost spikes for isotope & immunoassay reagents | -0.4% | North America, Europe | Short term (≤ 2 years) |

| Clinician pushback on self-medication and antibiotic misuse | -0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Variable Accuracy of At-Home Serology vs Active-Infection Tests

Serology detects IgG antibodies that can linger long after eradication, limiting its utility for treatment confirmation. A 2024 Cochrane review pegged serology sensitivity between 76% and 96%, with specificity sliding to as low as 79% among patients recently exposed to antibiotics. Clinicians therefore trust stool antigen or urea breath formats for post-therapy verification, constraining serology’s share in North America where follow-up testing accounts for up to 40% of diagnostic volume. Dual-marker kits that combine antibodies and antigen show promise yet face complex regulatory pathways, as the Food and Drug Administration demands clinical validation for each analyte separately. False positives drive unnecessary antibiotic use, while false negatives postpone ulcer management, exposing manufacturers to liability and reputation damage.

Stringent FDA/CE Evidence for Home-Use Labeling

The FDA’s May 2024 laboratory-developed test rule removed enforcement discretion for any device intended for home sample collection or home use, obliging companies to submit 510(k) or de novo dossiers that include lay-user studies of 200-plus participants across diverse literacy levels. European Medical Device Regulation 2017/745 enforces parallel requirements and rigorous post-market surveillance across the continent. Budget impact is acute for small innovators; Abingdon Health, for example, reported GBP 6.1 million (USD 7.7 million) in 2024 revenue, yet a single pivotal usability trial can cost USD 0.5-1 million. This evidence hurdle primes the market for consolidation as resource-constrained firms seek partnerships or exit.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Stool Antigen Dominance Meets Serology’s Rapid Growth

Stool antigen kits accounted for 45.23% of at-home peptic ulcer testing market share in 2024, propelled by their ability to detect active infection and comply with American College of Gastroenterology guidelines that consider the format equivalent to urea breath tests for eradication confirmation. Biomerica’s 2024 FDA clearance for its HP Detect ELISA stool test validated scalable home-collection logistics, as specimens ship to CLIA-certified laboratories under ambient conditions for enzyme immunoassay processing.

Finger-stick serology, while smaller in absolute revenue, is set to advance at a 12.34% CAGR through 2030. Colloidal-gold lateral-flow cassettes yield results in under 10 minutes, retail below USD 10, and fit retail-pharmacy workflows that emphasize speed over post-treatment monitoring accuracy. Urea breath tests hover between these poles: accuracy surpasses 95%, but dependence on isotope-labeled urea lifts reagent costs by USD 15-25 and requires specialized sample-shipping materials. Tariff volatility amplifies the cost burden, especially for smaller producers without long-term isotope contracts. The FDA’s lay-user validation mandate further tilts competitive advantage toward stool antigen kits, which separate collection from lab analysis and thus avoid some usability pitfalls inherent to onsite breath analyzers

By Distribution Channel: Retail Pharmacies Outpace Online Growth

Online DTC channels controlled 55.1% of the at-home peptic ulcer testing market size in 2024, benefiting from consumers’ desire for privacy and bundle offerings that combine H. pylori diagnostics with microbiome sequencing and ongoing telehealth oversight. Platforms such as 1health support national reach and subscription revenue structures, integrating results into electronic medical records that trigger physician review.

Retail pharmacies, however, are forecast to grow at 13.8% CAGR to 2030 as chains embed point-of-care diagnostics into existing wellness clinics and tap collaborative practice agreements that permit pharmacist-led prescribing in 23 U.S. states. The brick-and-mortar edge lies in immediacy: a consumer can test and receive antibiotics within a single visit, a service that DTC mail operations cannot match. Telehealth hybrids sit between DTC and retail, pairing mailed kits with virtual consults to satisfy jurisdictions that still mandate physician involvement. The General Data Protection Regulation burdens skew European competition toward pharmacies, which already maintain secure patient-consent workflows.

Geography Analysis

North America held 37.22% revenue share in 2024 as U.S. insurers reimbursed non-invasive tests under preventive-care mandates and CLIA-waived kits proliferated in retail settings. Enforcement of the FDA’s LDT final rule will escalate compliance costs yet also increase institutional trust, encouraging hospital systems to integrate home diagnostics into population-health programs. Canada and Mexico provide incremental upside; Mexico’s Ministry of Health reports H. pylori prevalence above 60% in citizens older than 50, spurring demand for home testing in regions where specialty clinics remain scarce.

Asia-Pacific is projected to log a 9.67% CAGR through 2030, underpinned by India’s diagnostics market rising from USD 13 billion in 2023 to USD 25 billion by 2028. Companies such as MyDiagnostics offer stool antigen kits at INR 2,500 (USD 30) with doorstep collection, undercutting hospital labs and winning urban middle-class users. China supplements demand by funding primary-care expansion in tier-2 and tier-3 cities, where endoscopy capacity historically lags ulcer prevalence [3]National Health Commission China, “Peptic Ulcer Hospitalization Trends. Regulatory cycles vary: Australia accepts overseas clinical data, while China stipulates domestic trials, elongating launch timelines by up to two years.

Europe contributes the remainder, anchored by Germany and the United Kingdom where National Health Service pilots couple at-home breath tests with digital symptom trackers, trimming gastroenterology wait lists by 28% in early deployments. Middle Eastern demand concentrates in Gulf states that host large South Asian expatriate communities with high seroprevalence, and where private healthcare systems pay premium prices for rapid diagnostics. South America’s upside resides in Brazil and Argentina, where insurers reimburse non-invasive tests to manage endoscopy backlogs.

Competitive Landscape

Competition is moderate, split across breath, stool, and serology modalities, each with discrete supply-chain requirements. LabCorp and Quest Diagnostics leverage existing home-collection networks to bundle H. pylori panels with lipid and thyroid profiles, securing payer contracts that smaller players cannot easily match. Specialist firms such as Biomerica, Omed Health, and Abingdon Health chase regulatory clearances to unlock new channels; Biomerica’s FDA clearance for HP Detect ELISA and its April 2025 UAE approval for the Fortel Ulcer Test illustrate a dual-market strategy targeting U.S. laboratories and Middle Eastern point-of-care settings.

Strategic divergence hinges on vertical integration versus component specialization. Kihealth’s partnership with Genova Diagnostics exemplifies the integrated route, controlling collection logistics, lab processing, and telehealth prescribing. Abingdon Health pursues a component model, providing lateral-flow cassettes to pharmacy brands and contract-manufacturing clients in North America. White-space opportunities cluster in tele-gastroenterology, where AI-enhanced breath analyzers feed real-time metrics to remote physicians, and in isotope-free spectroscopy that slashes per-test costs. The Food and Drug Administration’s heightened validation demands accelerate consolidation, as under-capitalized startups struggle to finance pivotal trials and post-market surveillance.

At-Home Peptic Ulcer Testing Industry Leaders

PRIMA Lab SA

Biomerica, Inc.

Owlstone Medical Limited

Biometrix Corporation

LabCorp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Omed Health debuted OMED Health Plans in Great Britain, integrating its CE-marked breath analyzer with a smartphone app and clinician pathway; the device recorded over 90% concordance with lab hydrogen-methane tests .

- August 2025: Biomerica, Inc. gained United Arab Emirates clearance for the Fortel Ulcer Test, broadening its footprint into Middle East markets with high South Asian expatriate populations.

- August 2024: Kihealth and Genova Diagnostics have partnered to offer advanced gut health testing directly to consumers through retail pharmacies, making these innovative diagnostics more accessible.

Global At-Home Peptic Ulcer Testing Market Report Scope

According to the report's scope, the at-home peptic ulcer testing kit is used to detect H. pylori. There are various tests available to detect H. pylori, including stool antigen tests, blood antibody tests, and urea breath tests. At-home testing is helpful for initial screening and follow-up treatment.

The at-home peptic ulcer testing market is segmented by test type, distribution channel, and geography. By test type, the market is segmented into urea breath test kits, stool antigen home kits, and finger-stick serology kits. By distribution channel, the segmentation includes online direct-to-consumer sales, retail pharmacies, and telehealth partnerships. Geographically, the market is analyzed across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Urea Breath Test Kits |

| Stool Antigen Home Kits |

| Finger-stick Serology Kits |

| Online Direct-to-Consumer |

| Retail Pharmacies |

| Tele-health Partnerships |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Type | Urea Breath Test Kits | |

| Stool Antigen Home Kits | ||

| Finger-stick Serology Kits | ||

| By Distribution Channel | Online Direct-to-Consumer | |

| Retail Pharmacies | ||

| Tele-health Partnerships | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the at-home peptic ulcer testing market in 2025?

The market stands at USD 317.76 million in 2025.

What CAGR is forecast through 2030?

Revenue is expected to grow at a 6.63% CAGR.

Which test format holds the largest share today?

Stool antigen kits lead with a 45.23% share.

Which sales channel is growing the fastest?

Retail pharmacies are projected to expand at 13.8% CAGR to 2030.

Page last updated on: