Asia Pacific Talent Acquisition Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

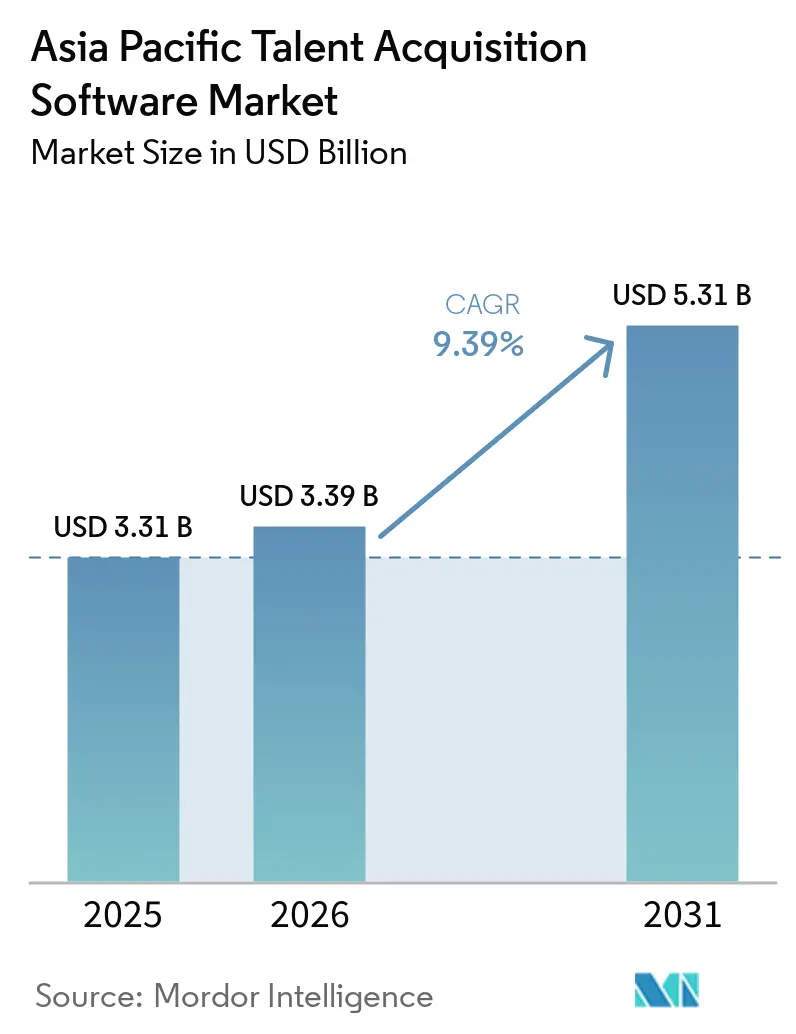

| Base Year Market Size (2025) | USD 3.31 Billion |

| Market Size (2026) | USD 3.39 Billion |

| Market Size (2031) | USD 5.31 Billion |

| Growth Rate (2026 - 2031) | 9.39% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Talent Acquisition Software Market Analysis by Mordor Intelligence

The Asia Pacific talent acquisition software market size is expected to grow from USD 3.31 billion in 2025 to USD 3.39 billion in 2026 and is forecast to reach USD 5.31 billion by 2031 at 9.4% CAGR over 2026-2031. The market is being reshaped by a move away from manual and disconnected hiring processes toward integrated, AI-native platforms that link recruiting with broader workforce planning. A large mobile-first workforce, strong competition for digital talent, and country-specific compliance needs continue to favor software that is built for local operating conditions rather than generic global deployments. Cloud adoption has already become the default buying pattern in the region, which means buyers now expect scalability, automated compliance updates, and regular AI model improvements as standard product features. China continues to anchor regional demand with its scale and fast normalization of AI-assisted screening, while India is broadening the growth base as structured recruiting spreads beyond the largest urban centers. Data privacy rules, bias concerns around AI, and the cost of advanced platforms in SME-heavy economies still slow some decisions, but the demand outlook for the Asia Pacific talent acquisition software market remains firm because hiring pressure and public digitalization programs continue to support investment.

Key Report Takeaways

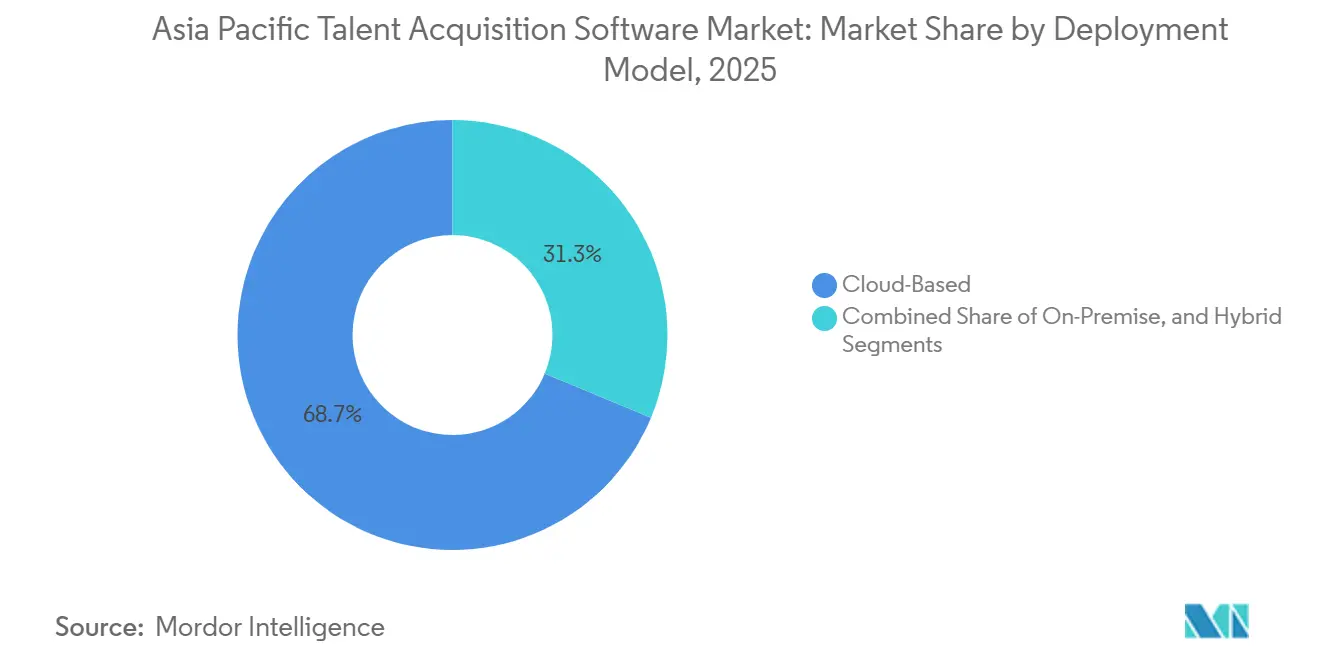

- By deployment model, cloud-based deployments accounted for 68.7% in 2025 and were also the fastest-growing segment, with a 10.6% CAGR through 2031.

- By application, applicant tracking systems accounted for 29.8% of revenue in 2025, while interview management and assessment are projected to grow at an 11.4% CAGR through 2031.

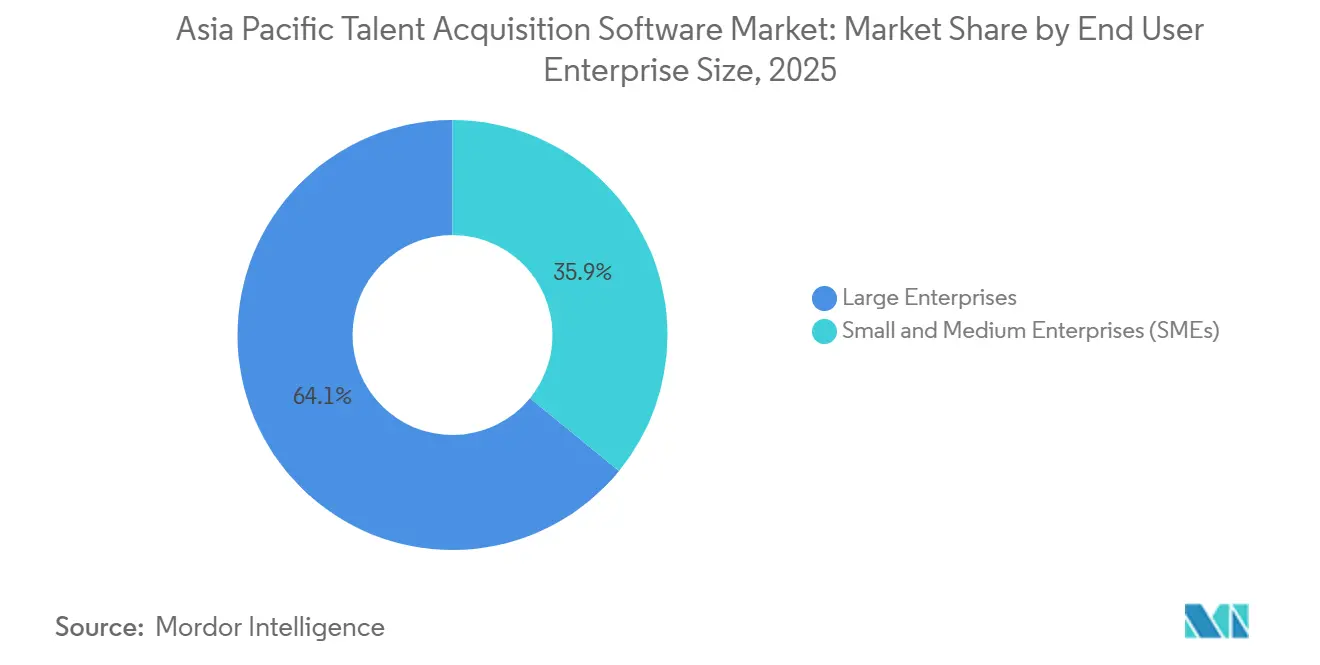

- By end-user enterprise size, large enterprises held 64.1% in 2025, while small and medium enterprises are forecast to expand at a 10.9% CAGR through 2031.

- By end-user industry vertical, information technology and telecom led with 25.2% in 2025, while healthcare and life sciences are expected to advance at an 11.3% CAGR through 2031

- By geography, China held 31.8% in 2025, while India is projected to record the highest growth at a 12.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia Pacific Talent Acquisition Software Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption Of AI-Based Candidate Matching And Screening | +2.5% | Global, with APAC core, concentrated in India, China, South Korea, Singapore, Australia | Short term (≤ 2 years) |

| Accelerating Cloud-First HR Digitalization | +1.8% | Global, concentrated in India, Southeast Asia, Australia | Medium term (2-4 years) |

| Intensifying Competition For Digital Talent In High-Growth Sectors | +1.3% | India, China, Singapore, Australia | Short term (≤ 2 years) |

| Shift Toward Skills-Based Hiring Frameworks | +0.9% | APAC core, early gains in Singapore, Australia, India | Medium term (2-4 years) |

| Government Incentives For Workforce Digital Transformation | +0.7% | Singapore, Australia, South Korea, India, spill-over to Malaysia, Thailand | Medium term (2-4 years) |

| Expansion Of Internal Talent Marketplaces Among Large Enterprises | +0.5% | Singapore, Australia, Japan, early-stage in Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption Of AI-Based Candidate Matching And Screening

AI has moved from a pilot tool to a core operating layer in the Asia Pacific talent acquisition software market. In Singapore, 82% of organizations were already using AI for hiring, onboarding, or training in Q2 2025, ahead of the regional average of 81% and the global average of 67%, indicating how quickly the region has normalized AI-led people workflows.[1]ManpowerGroup, “Employment Outlook Survey Q2 2025,” ManpowerGroup, manpowergroup.com In South Korea, a survey published in April 2026 found that 65% of companies had adopted or were considering AI recruiting agents, with sourcing and applicant review standing out as the main targets for automation. This shift matters because employers are no longer buying AI only to reduce screening time; they are also using it to widen candidate reach and support more consistent evaluation across large hiring volumes. In China and major technology hubs across the region, AI-assisted screening has already become part of standard recruitment practice, raising the minimum product expectations for vendors serving the Asia Pacific talent acquisition software market. As regulations become tighter, buyers also want tools that can show audit trails, provide human oversight, and support explainable decision-making rather than just speed and automation.

Accelerating Cloud-First HR Digitalization

Cloud delivery has become the default architecture for much of the Asia Pacific talent acquisition software market because it reduces deployment friction and keeps compliance updates up to date across multiple jurisdictions. The value case is especially strong in markets where earlier HR technology stacks were limited, as organizations can move directly to API-first systems rather than spend on legacy migrations. A case study on Omni HR reported a 50% reduction in customer onboarding time and 25-30% lower IT costs after the cloud migration, underscoring why cloud economics are appealing to lean HR teams in Southeast Asia.[2]Amazon Web Services, “Omni HR Case Study,” Amazon Web Services, aws.amazon.com The operational case is equally important because cloud platforms can automate updates to statutory contribution rules, such as Singapore's Central Provident Fund, Malaysia's Employees Provident Fund, and Thailand's Social Security Office, reducing the need for repeated manual effort for cross-border hiring teams. SAP reinforced this direction in April 2026 when it released the 1H 2026 SuccessFactors update, featuring agentic AI across recruiting, payroll, and onboarding, with features that depend on cloud infrastructure for continuous improvement and cross-module data use. As a result, cloud is no longer a feature choice in the Asia Pacific talent acquisition software market; it is increasingly the base requirement for advanced recruiting capability.

Intensifying Competition For Digital Talent In High-Growth Sectors

Persistent talent shortages are changing how employers evaluate software across the Asia Pacific talent acquisition software market. Japan shows how tight the environment has become, since a survey from December 2025 found that only 46.3% of hiring decision-makers believed they could recruit as before, while 40.6% could not secure their targeted new-graduate headcount.[3]Mynavi, “Survey Of Hiring Decision-Makers In Japan,” Mynavi, mynavi.jp Australia faces a different but related pressure, with the APS Digital Workforce Insights Report documenting a projected shortfall of more than 61,000 digital roles by 2030. Under these conditions, workflow efficiency alone is no longer enough for many buyers. Employers increasingly want platforms that can expand candidate pools, improve passive talent engagement, and support faster outreach into scarce labor segments. That shift gives an advantage to vendors with strong candidate databases, matching depth, and intelligence layers, which is why competition in the Asia Pacific talent acquisition software market is moving beyond simple ATS functionality.

Shift Toward Skills-Based Hiring Frameworks

Skills-based hiring is becoming more important in the Asia Pacific talent acquisition software market because job requirements are changing faster than static credentials can reflect. Research published in June 2025 found that the skills required for jobs changed by 40% between 2016 and 2024 and are projected to change by another 70% by 2030. The same research showed that removing unnecessary qualification filters can expand the potential candidate pool by up to 11.4 times in India, 9.5 times in Indonesia, and 7.7 times in Australia. That change reduces reliance on resumes as the main filter and raises demand for structured interviews, assessment tools, and better skills mapping. It also increases the value of internal mobility tools that can identify existing employees with adjacent skills before an employer starts an external search. Singapore has added public policy support to this shift through programs tied to MyCareersFuture and Workforce Singapore, which help align employer practices with software that supports competency-based selection.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Data-Privacy Regulations Across Asia-Pacific | -1.4% | APAC-wide, concentrated in China, South Korea, Australia, India, Malaysia, Thailand | Short term (≤ 2 years) |

| Integration Complexity With Legacy HR Information Systems | -1.1% | Japan, China, South Korea, spill-over to large enterprises in India and Australia | Medium term (2-4 years) |

| Persistent AI Bias And Explainability Concerns | -0.8% | Global, concentrated in Singapore, Australia, Hong Kong | Medium term (2-4 years) |

| Cost Barriers Limiting SME Adoption Of Advanced Platforms | -0.5% | APAC-broad, concentrated in Southeast Asia and India Tier 2 and Tier 3 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Data-Privacy Regulations Across Asia-Pacific

Skills-based hiring is becoming more important in the Asia Pacific talent acquisition software market because job requirements are changing faster than static credentials can reflect. Research published in June 2025 found that the skills required for jobs changed by 40% between 2016 and 2024 and are projected to change by another 70% by 2030.[4]King and Wood Mallesons, “China PIPL Compliance Audit Measures,” King and Wood Mallesons, kwm.com The same research showed that removing unnecessary qualification filters can expand the potential candidate pool by up to 11.4 times in India, 9.5 times in Indonesia, and 7.7 times in Australia. That change reduces reliance on resumes as the main filter and raises demand for structured interviews, assessment tools, and better skills mapping. It also increases the value of internal mobility tools that can identify existing employees with adjacent skills before an employer starts an external search. Singapore has added public policy support to this shift through programs tied to MyCareersFuture and Workforce Singapore, which help align employer practices with software that supports competency-based selection.

Integration Complexity With Legacy HR Information Systems

Integration problems continue to slow parts of the Asia Pacific talent acquisition software market, especially in countries where payroll, benefits, and employment records are deeply embedded in older enterprise systems. In Japan, China, and South Korea, many HR information systems remain tied to broader ERP environments, which turns a standalone ATS rollout into a longer integration program rather than a simple add-on deployment. Australia provides a clear public-sector example, since more than 40% of surveyed government systems were legacy-heavy and required meaningful modernization before newer hiring platforms could be layered on top. This creates a defensive advantage for incumbent HCM vendors, as recruitment data must be reliably transferred to payroll, social insurance, and workforce administration systems. Buyers may prefer specialist recruiting tools at the feature level, but many still stay with suite vendors because operational risk rises when those flows are broken. That friction slows the pace at which best-of-breed products can take share in the Asia Pacific talent acquisition software market, particularly within large enterprises and regulated institutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Consolidates Dominance As Hybrid Gains Traction

Cloud-based deployment accounted for 68.7% in 2025, indicating it already represented the core of spending in the Asia Pacific talent acquisition software market, and it is also projected to grow at a 10.6% CAGR through 2031. That combination is notable because the leading model is still gaining share through new implementations, expansion into SMEs, and public-sector modernization. In practical terms, buyers are choosing the cloud because they want frequent feature updates, easier integration across recruiting steps, and less local maintenance. The compliance argument is strong as well, since cross-border employers need systems that can update statutory and data-handling workflows without long internal release cycles. For many organizations, the decision is no longer cloud versus on-premise, but how much of the workflow should sit in the cloud and how quickly the remaining local systems can be connected.

Cloud adoption also supports the product direction of the Asia Pacific talent acquisition software industry, as new AI functions depend on continuous model updates and data access across modules. SAP's April 2026 1H release embedded agentic AI across recruiting and onboarding, which reinforced the dependence of modern talent workflows on cloud infrastructure. AWS also documented operational gains in its Omni HR case study, where cloud migration reduced onboarding time by 50% and lowered IT costs by 25-30%, a result with clear relevance for regional HR teams with limited internal support. On-premise systems still hold a place in highly regulated settings such as defense and some financial environments in Japan and South Korea, where data sovereignty remains a serious design issue. Hybrid deployment is therefore gaining traction as a bridge model, since it lets employers keep sensitive data in-country while still using cloud-based analytics and matching tools. That balance explains why the Asia Pacific talent acquisition software market continues to move toward the cloud, while not eliminating local infrastructure in certain segments.

By Application: ATS Anchors Revenue As Interview Management Accelerates

Applicant tracking systems accounted for 29.8% of application-layer revenue in 2025, making ATS the largest single segment in the Asia Pacific talent acquisition software market at the application level. ATS remains the entry point for many purchases because it acts as the system of record for requisitions, applicant consent, workflow tracking, and hiring documentation. Large enterprises still treat this layer as the operational backbone onto which candidate relationship management, recruitment marketing, analytics, and onboarding modules are added over time. That role has become even more important as privacy rules require clearer audit trails and more structured records. The purchasing pattern also favors incumbents because once the core workflow is in place, adjacent modules are easier to add than replace. This is why ATS retains a central position even while the broader Asia Pacific talent acquisition software market expands into more specialized tools.

The fastest-growing momentum now lies in interview management and assessment, which is projected to grow at a 11.4% CAGR through 2031 as employers place less weight on credentials alone. Research on skills change helps explain the shift because rapid movement in job requirements makes static resumes weaker indicators of future fit. Employers are responding by building more structured evaluation processes, including competency checks, guided interviews, and role-relevant assessments. That in turn lifts demand for software that supports consistent scoring, panel coordination, and better evidence capture during the selection process. The application mix is therefore becoming more layered, with ATS holding the process center while assessment tools expand around it. For vendors in the Asia Pacific talent acquisition software market, the implication is clear: winning the core workflow is helpful, but growth increasingly depends on how well they support skills-led evaluation around it.

By End User Enterprise Size: SMEs Emerge As The Next Growth Engine

Large enterprises accounted for 64.1% of revenue in 2025, making them the largest share of the Asia Pacific talent acquisition software market. Their lead reflects bigger compliance burdens, larger hiring volumes, and stronger existing relationships with global HCM vendors. These buyers also have the internal teams needed to manage integrations, governance, and cross-country workflows, which gives them a higher capacity to absorb broad platform suites. Workday's position in India illustrates the scale effect, since the company reported more than 3.8 million monthly active users and over 1,800 global customers in the country as of early 2025. Global capability centers and large enterprise service hubs continue to reinforce this spending pattern by creating recurring demand for standardized recruiting systems at scale.

Small and medium enterprises are the fastest-growing size band, with a 10.9% CAGR expected through 2031, and this is where much of the next wave of adoption will come from. The Asia Pacific talent acquisition software market benefits from a simple structural fact: many SMEs across the region do not carry the same legacy HR systems burden as seen in larger Western organizations. That makes it easier for them to move directly into cloud-native recruiting workflows without paying for long migrations or deep internal customization. Vendors that simplify setup, automate compliance tasks, and support mobile-first hiring are well placed to capture that demand. The pattern is particularly relevant outside top-tier cities, where formal recruiting is spreading into newer business clusters and digital hiring habits are improving quickly. In that sense, the Asia Pacific talent acquisition software industry is entering a broader adoption phase in which enterprise accounts still drive scale, but SMEs increasingly shape the direction of growth.

By End User Industry Vertical: IT And Telecom Leads While Healthcare Reshapes Growth Dynamics

Information technology and telecom accounted for 25.2% of revenue in 2025, giving the segment the largest share of the Asia Pacific talent acquisition software market among end-user verticals. Its lead comes from constant demand for digital skills, frequent role changes, and the need to support both campus recruiting and experienced lateral hiring. In many regional technology labor markets, employers face active poaching, short response windows, and the need to screen large applicant volumes without compromising quality. BFSI also remains a major buyer because consumer banking and insurance hiring generate steady volume, while documentation requirements increase the value of reliable process records. Industrial manufacturing and retail are also adding momentum as employers formalize blue-collar, technical, and mobile-first recruiting across China, Vietnam, India, and Southeast Asia. The result is a broadening demand base for the Asia Pacific talent acquisition software market beyond its original technology-centered core.

Healthcare and life sciences are the fastest-growing verticals, with an 11.3% CAGR expected through 2031, and their rise reflects a more structural hiring need tied to aging populations and sustained clinical workforce pressure. Japan, Australia, and South Korea all face ongoing demand for nurses, paramedical staff, and specialized healthcare workers, which keeps hiring intensity elevated. This vertical also needs more than generic applicant tracking because credential verification, compliance checks, and role-specific screening are essential parts of the hiring process. That makes healthcare a strong fit for vendors that can extend core ATS functions with licensing validation and specialized workflow controls. Public-sector digital workforce plans in markets such as Australia also create a nearby opportunity because formal hiring requirements spill into related health and administrative staffing needs. As these requirements deepen, the Asia Pacific talent acquisition software market is likely to see stronger vertical specialization rather than a one-size-fits-all product approach.

Geography Analysis

China held 31.8% in 2025, giving it the largest national position in the Asia Pacific talent acquisition software market size, while India is projected to expand at a 12.2% CAGR through 2031 and remains the fastest-growing country market. China continues to stand out for its mobile-first recruiting behavior and the normalization of AI-assisted screening across technology and manufacturing employers. The PIPL audit regime, which took effect in May 2025, has also pushed large enterprises to modernize candidate management systems to make it easier to maintain consent records, transfer controls, and audit readiness. Japan faces different pressures, as hiring constraints are driven by labor scarcity and weak recruiter confidence in securing enough candidates through traditional methods. A December 2025 survey showed that only 46.3% of hiring decision-makers believed they could continue hiring as before, which helps explain the appetite for AI-enabled sourcing and more proactive talent discovery.

India's growth profile is supported by the formalization of technology hiring, the expansion of global capability centers, and a large graduate workforce that is already comfortable with platform-based application behavior. Workday's rollout of a local India data center in the first half of 2026 shows how vendors are adjusting to the country's scale and its growing expectations around local data handling. Singapore plays a different role in the Asia Pacific talent acquisition software market share structure, serving as a strategic entry point for regional product launches, compliance-led enterprise sales, and advanced AI use cases. Vendors competing in Singapore increasingly need to demonstrate measurable productivity gains and strong data governance, rather than simply showing that AI features exist. Australia remains a mature market where public-sector workforce plans and healthcare recruiting needs continue to support demand for structured digital hiring systems.

Malaysia, Thailand, and the wider Rest of Asia Pacific region form the next growth tier, where regulation and foreign investment are pushing employers toward more formal candidate data management. Malaysia's data protection rules for organizations handling large volumes of personal data have drawn attention to consent management and recordkeeping, which supports demand for compliant recruiting systems. Thailand's enforcement environment has also become more active, prompting more compliance reviews among employers handling local candidate information. Vietnam adds a separate demand signal because strong foreign direct investment inflows, which reached USD 21.5 billion in H1 2025 and rose 32.6% year over year, are drawing in manufacturers that need more structured hiring infrastructure from the start. Across Southeast Asia, internal mobility and skills-mapping modules are also becoming more relevant as employers seek to leverage existing talent before expanding external searches, broadening the functional scope of the Asia Pacific talent acquisition software market.

Competitive Landscape

The Asia Pacific talent acquisition software market is moderately concentrated at the top platform layer, where SAP, Oracle, and Workday hold an outsized position in large enterprise accounts, while the mid-market and SME tiers remain much more fragmented. That structure creates two parallel competitive patterns: one based on suite economics and enterprise relationships, and another based on regional flexibility, price, and speed of implementation. Large vendors benefit from existing payroll and HCM footprints, which reduce switching appetite among major employers. Smaller and regional providers still compete effectively where mobile-first workflows, local language support, or simpler rollout requirements matter more than full-suite breadth. As a result, the Asia Pacific talent acquisition software market does not behave like a winner-take-all category, even though the top enterprise tier is clearly defended by a small group of incumbents.

SAP made a major strategic move when it completed the SmartRecruiters acquisition in September 2025 and began embedding the product more directly into SuccessFactors in 2026. That combination allows SAP to position AI-driven recruiting as a connected part of a broader HCM suite instead of a separate workflow layer. Workday responded by acquiring Paradox in August 2025, bringing conversational AI for high-volume frontline hiring into its broader talent stack and strengthening its reach in retail, healthcare, and manufacturing use cases. Oracle also reinforced its position in October 2025 with the launch of Oracle Career Coach, an agentic AI capability inside Fusion Cloud Recruiting that supports job recommendations, interview preparation, and scheduling across mobile and messaging channels. These moves highlight how conversational interfaces, embedded AI, and end-to-end orchestration have become expected product requirements in the Asia Pacific talent acquisition software market rather than optional differentiators.

A second line of competition is forming around skills intelligence, local compliance, and product fit by customer size. Eightfold AI has sought to distinguish itself through a deep learning architecture trained on billions of career paths and deployed across more than 155 countries and 24 languages, giving it a strong foundation in talent intelligence rather than basic workflow automation. Zoho remains relevant in the SME segment because its regional cost structure and channel reach are difficult for larger global vendors to match on total ownership cost. White-space opportunities are still visible in Japan, in healthcare hiring workflows, and across Southeast Asian SMEs where manual recruiting processes are being replaced. Compliance engineering is also becoming a harder barrier to entry because vendors must now support local privacy rules, data residency requirements, and stronger audit standards across several jurisdictions simultaneously. As a result, the Asia Pacific talent acquisition software market is likely to remain competitive, but vendors that can combine enterprise-grade compliance with practical product fit for local hiring conditions will be best positioned to succeed.

Asia Pacific Talent Acquisition Software Industry Leaders

SAP SE

Oracle Corporation

Workday Inc.

iCIMS Inc.

SmartRecruiters Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: TalentX launched the MyTalent Platform in Japan, adopted by Mitsui Knowledge. It integrates CRM, referral recruiting, and AI benchmarking, with approximately 600 employees using it monthly, showing strong early engagement.

- April 2026: SAP released the 1H 2026 SuccessFactors update, adding agentic AI across recruiting, payroll, and onboarding, plus pay transparency and enhanced skills governance for compliance-focused enterprises.

- March 2026: SAP advanced SmartRecruiters integration with SuccessFactors, enabling unified login, bidirectional data flow, and fraud detection, offering approximately 4,000 customers a migration path aligned with existing HCM systems.

- November 2025: Eightfold AI opened a 22,000 sq. ft. office in Bangalore, expanding to approximately 300 engineers. India became its APAC AI hub, supporting growth while serving 150+ Fortune 500 firms across 155 countries.

Asia Pacific Talent Acquisition Software Market Report Scope

The Asia Pacific talent acquisition software market refers to digital platforms and solutions that streamline recruitment, onboarding, assessment, and workforce management across diverse industries in the region. It encompasses applicant tracking systems, cloud-based hiring tools, AI-driven screening, and compliance-focused workflows, enabling employers to efficiently manage large-scale, skills-based, and cross-border talent acquisition.

The Asia Pacific Talent Acquisition Software Report is segmented by Deployment Model (Cloud, On-Premise, and Hybrid), Application (Applicant Tracking System, Candidate Relationship Management, Recruitment Marketing, Onboarding, Interview Management and Assessment, and Other Talent Acquisition Applications), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (Information Technology and Telecom, Banking Financial Services and Insurance, Healthcare and Life Sciences, Industrial Manufacturing, Retail and eCommerce, Government and Public Sector, and Others), and Geography (China, India, Japan, South Korea, Singapore, Malaysia, Thailand, Australia, and Rest of Asia Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-Premise |

| Hybrid |

| Applicant Tracking System (ATS) |

| Candidate Relationship Management (CRM) |

| Recruitment Marketing |

| Onboarding |

| Interview Management and Assessment |

| Other Applications |

| Large Enterprises |

| Small and Medium Enterprises |

| Information Technology (IT) and Telecom |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Industrial Manufacturing |

| Retail and eCommerce |

| Government and Public Sector |

| Other End User Enterprise Industry Verticals |

| China |

| India |

| Japan |

| South Korea |

| Singapore |

| Malaysia |

| Thailand |

| Australia |

| Rest of Asia Pacific |

| By Deployment Model | Cloud |

| On-Premise | |

| Hybrid | |

| By Application | Applicant Tracking System (ATS) |

| Candidate Relationship Management (CRM) | |

| Recruitment Marketing | |

| Onboarding | |

| Interview Management and Assessment | |

| Other Applications | |

| By End User Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By End User Enterprise Industry Vertical | Information Technology (IT) and Telecom |

| Banking, Financial Services and Insurance (BFSI) | |

| Healthcare and Life Sciences | |

| Industrial Manufacturing | |

| Retail and eCommerce | |

| Government and Public Sector | |

| Other End User Enterprise Industry Verticals | |

| By Country | China |

| India | |

| Japan | |

| South Korea | |

| Singapore | |

| Malaysia | |

| Thailand | |

| Australia | |

| Rest of Asia Pacific |

Key Questions Answered in the Report

How large is the Asia Pacific talent acquisition software market?

The Asia Pacific talent acquisition software market stood at USD 3.39 billion in 2026 and is projected to reach USD 5.31 billion by 2031, growing at a 9.4% CAGR over 2026-2031.

Which deployment model leads spending across the region?

Cloud-based deployment led with a 68.7% share in 2025 and is also the fastest-growing deployment model, with a 10.6% CAGR expected through 2031.

Which application area is expanding the fastest in hiring technology across Asia Pacific?

Interview management and assessment is the fastest-growing application segment, advancing at an 11.4% CAGR through 2031 as employers rely more on competency evaluation and less on resume-only screening.

Which country is growing the fastest for talent acquisition software adoption?

India is the fastest-growing country market, with a projected 12.2% CAGR over 2026-2031, supported by formalization in technology hiring and continued expansion of global capability centers.

Which end-user vertical generates the most demand for recruiting software?

Information technology and telecom led all verticals with a 25.2% share in 2025 because the sector faces persistent demand for digital talent and high hiring velocity.

Why are vendors investing so heavily in AI and compliance features in this space?

Buyers now expect AI-assisted screening, structured assessments, and stronger privacy controls because hiring volumes are high, skills are changing quickly, and cross-country privacy rules have become harder to manage.

Page last updated on: