Asia-Pacific Pumps Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

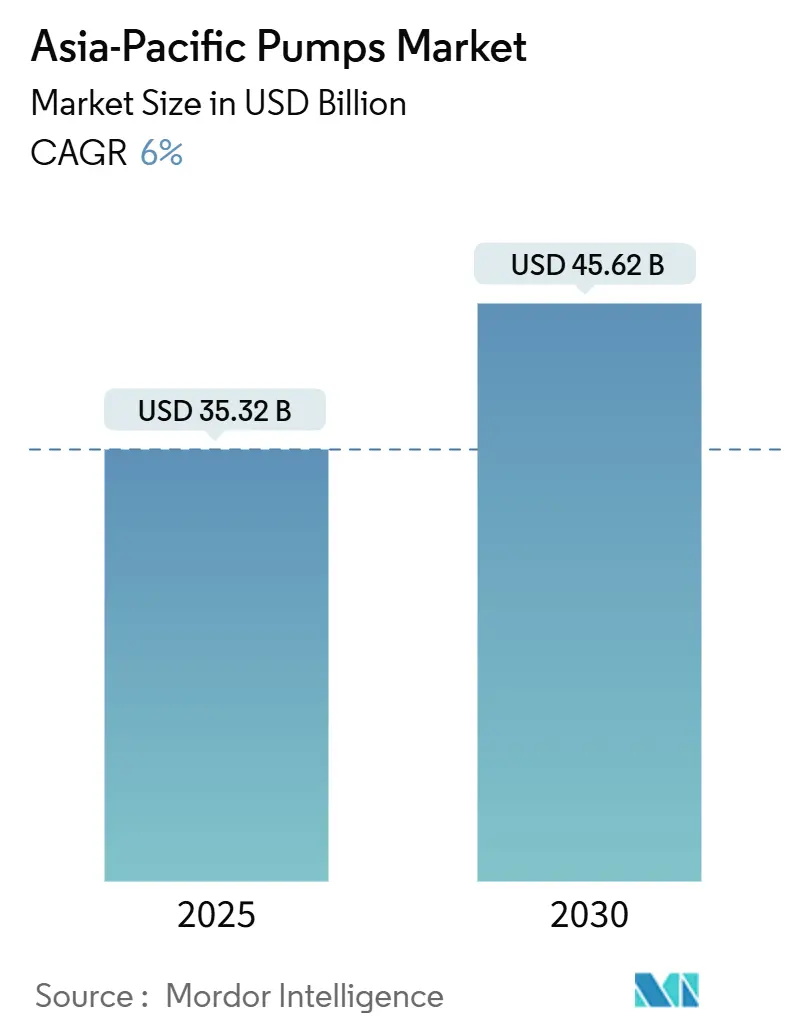

| Market Size (2025) | USD 35.32 Billion |

| Market Size (2030) | USD 45.62 Billion |

| Growth Rate (2025 - 2030) | 6.00% CAGR |

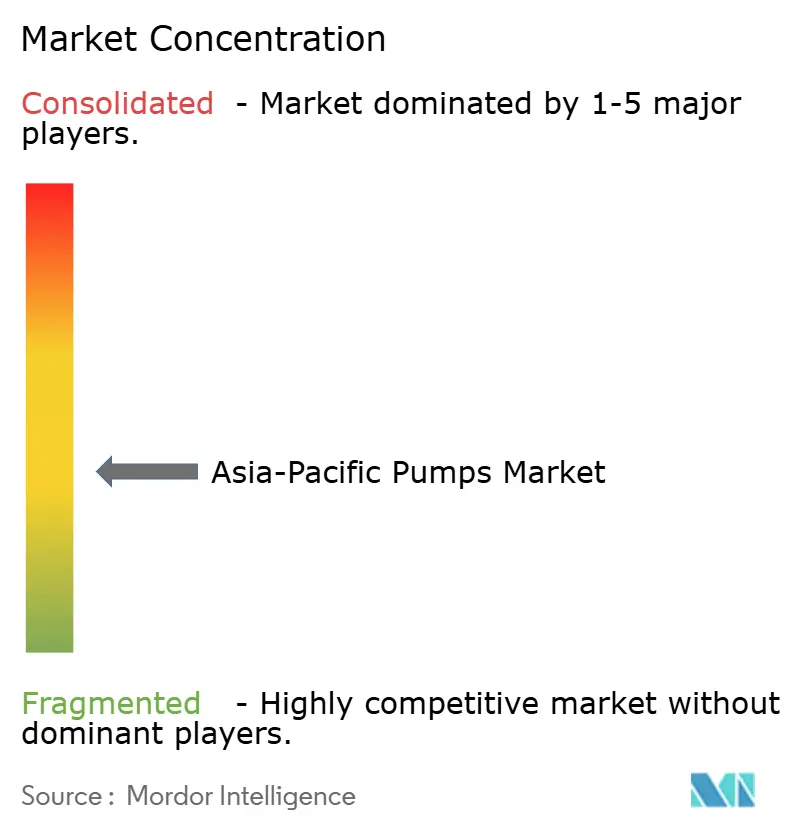

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Pumps Market Analysis by Mordor Intelligence

The Asia-Pacific Pumps Market size is estimated at USD 35.32 billion in 2025, and is expected to reach USD 45.62 billion by 2030, at a CAGR of 6% during the forecast period (2025-2030).

Climate-adaptation programs, urban water-infrastructure upgrades, and hydrogen-economy build-outs are pulling forward procurement across municipal, industrial, and energy verticals. Centrifugal dominance, rapid adoption of variable-frequency drives, and growing preference for corrosion-resistant materials are improving lifecycle performance and lowering the total cost of ownership. Renewable-powered units are moving from pilots to mainstream purchase lists as off-grid mines and farming cooperatives replace diesel pumps to curb operating expenditure. Meanwhile, supply-chain re-routing, local casting integration, and digital-twin services are reshaping competitive positioning and pricing strategies across the Asia-Pacific pumps market.[1]National Bureau of Statistics, “Statistical Communiqué on 2024 National Economic and Social Development,” stats.gov.cn

Key Report Takeaways

- By pump type, centrifugal pumps held 55.2% of the Asia-Pacific pumps market share in 2024; positive-displacement pumps are forecast to expand at a 6.8% CAGR through 2030.

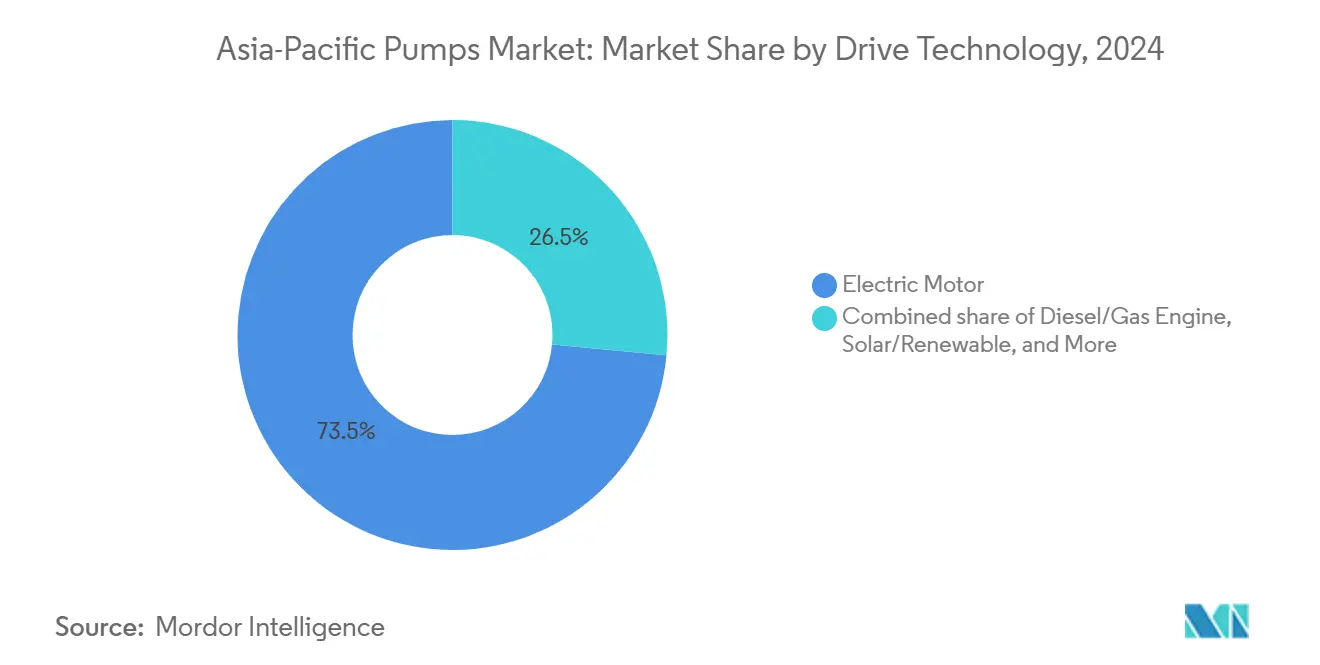

- By drive technology, electric-motor units led with 73.5% share of the Asia-Pacific pumps market size in 2024, while solar and other renewable-powered pumps are rising at a 9.3% CAGR to 2030.

- By position, surface pumps commanded a 58.7% share in 2024, whereas submersible units represent the swiftest 7.0% CAGR path through 2030.

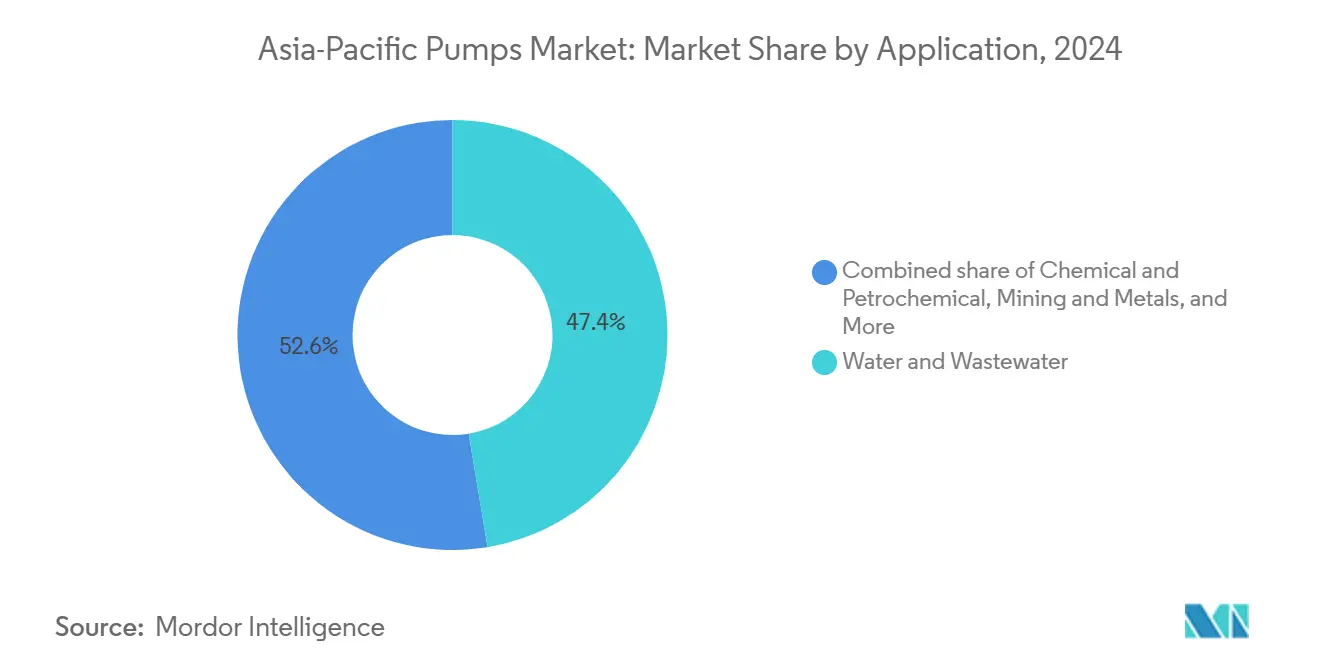

- By application, water and wastewater held 47.4% of demand in 2024 and are on track for a 6.6% CAGR to 2030.

- By geography, China captured a 39.9% share in 2024, but India is slated to deliver the region’s fastest 7.1% CAGR during the forecast horizon.

Asia-Pacific Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| Rapid Urbanisation & Water-infrastructure Boom | +1.2% | China, India, Vietnam, Indonesia, Thailand, Philippines | Medium term (2-4 years) | |

| Industrial Output Expansion across APAC | +0.9% | China, India, South Korea, Vietnam, Thailand | Short term (≤ 2 years) | |

| Capex Surge in Oil, Gas & Petrochemical | +0.8% | China, India, Malaysia, Australia, Indonesia | Medium term (2-4 years) | |

| Government Energy-efficiency & Smart-city Mandates | +0.7% | China, Japan, South Korea, Singapore, India, Malaysia | Long term (≥ 4 years) | |

| Stricter Flood-control Spend post 2024 Climate Events | +0.6% | China, Thailand, Vietnam, India, Bangladesh | Short term (≤ 2 years) | |

| Hydrogen Electrolyser Build-out Requiring Specialised Pumps | +0.4% | Japan, South Korea, Australia, China, India | Long term (≥ 4 years) | |

| Source: Mordor Intelligence | ||||

Rapid Urbanisation & Water-infrastructure Boom

Municipal agencies are fast-tracking pump-station tenders as urban populations swell and existing networks near end-of-life. China budgeted CNY 1.2 trillion in 2024 to push sewerage coverage toward 95% by 2030, driving bulk orders for submersible and vertical-turbine units.[2]Ministry of Housing and Urban-Rural Development, “2024 Urban Water-Infrastructure Investment Plan,” mohurd.gov.cn India’s Jal Jeevan Mission issued contracts for 12 million new household tap connections that require distribution pumps tolerant of sediment interruptions. Vietnam secured USD 8.5 billion in Asian Development Bank loans to safeguard Mekong Delta water systems from saltwater intrusion, spurring relocations of shoreline pump stations inland. Indonesia’s new capital, Nusantara, mandates turnkey pump rooms with remote-monitoring capability, favoring vendors offering digital-twin simulations. Rural electrification in India and Bangladesh is simultaneously triggering a diesel-to-electric replacement cycle across borehole installations.

Industrial Output Expansion across APAC

Manufacturing growth underpins steady demand for process pumps in chemicals, food and beverage, and electronics plants. China recorded 5.6% industrial production growth in Q1 2025, led by a 7.2% jump in chemical output that relies on corrosion-resistant centrifugal and diaphragm designs. India commissioned 48 new API plants in 2024, each specifying sanitary lobe or progressive-cavity pumps that meet cGMP criteria. South Korea’s semiconductor fabs circulated 1.2 billion m³ of ultrapure water via magnetically driven sealless pumps to cut particulate risk. Vietnam attracted USD 36 billion in FDI that fuels orders for cooling-tower and dye effluent pumps, while Thailand logged 1,200 factory approvals requiring stainless hygienic units and wash-down systems. Near-shoring to ASEAN members is prompting Malaysian and Indonesian estates to pre-install shared pump rooms, shortening tenant ramp-up time.

Capex Surge in Oil, Gas & Petrochemicals

Multi-year upstream and downstream projects are booking large-volume API-610 compliant pumps. PETRONAS awarded USD 2.1 billion in offshore contracts during 2024 that specify subsea injection and topside transfer units for sour-gas service. India’s ONGC earmarked USD 5.4 billion to develop deepwater fields necessitating high-pressure multistage centrifugals. China’s Sinopec turned on a 10 million tonne ethylene complex that chose duplex stainless API pumps for cracked-gas handling. LNG exporters in Australia depend on cryogenic designs capable of minus-162 °C service, while Indonesia’s refinery upgrades to Euro-5 fuels demand hydrocracker charge pumps with hardened impellers that extend the mean time between overhauls to 36 months.

Government Energy-efficiency & Smart-city Mandates

Efficiency norms are reshaping specifications toward IE4 motors, variable-speed integration, and real-time monitoring. China’s mandate covering pumps above 7.5 kW lifts upfront prices yet trims decade-long electricity outlays by one-fifth.[3]Ministry of Industry and Information Technology, “Notice on Promoting High-Efficiency Motors in Industrial Pumps,” miit.gov.cn Japan’s Top Runner rules require 5% yearly efficiency gains, pressuring laggard suppliers. Singapore’s SS 530:2024 standard compels buildings to embed dashboards that track pump energy intensity. Malaysia’s USD 120 million grant program subsidizes variable-frequency retrofits for municipal utilities, targeting 30% savings by 2027. South Korea is piloting blockchain-based pump registries that store energy and maintenance history, while India drafts star-rating labels that will introduce a compliance gap for legacy inventory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Energy Consumption & OPEX | -0.8% | China, India, Indonesia, Vietnam, Thailand, Malaysia | Short term (≤ 2 years) |

| Fragmented Local Manufacturing Base | -0.6% | India, Indonesia, Vietnam, Thailand, Philippines, Bangladesh | Medium term (2-4 years) |

| PFAS-linked Fluoropolymer Restrictions on Pump Linings | -0.4% | Japan, South Korea, Australia, China, Singapore | Long term (≥ 4 years) |

| Shipping-route Instability for Casting Inputs | -0.3% | Regional, acute on islands and inland provinces | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Energy Consumption & OPEX

Industrial tariffs climbed 8%–12% across major economies during 2024, driving users to stretch maintenance cycles and defer replacements. China lifted peak-hour rates to CNY 0.92/kWh, forcing textile plants to postpone upgrades. India’s time-of-day pricing penalizes daytime pumping, while Indonesia’s diesel-subsidy rollback pushed genset OPEX up 18%. Ten-year lifecycle cost of a 100 kW centrifugal unit in India now tops USD 180,000, with electricity representing 72% of the total. Utilities in Vietnam and Thailand are testing energy-performance contracts that shift savings guarantees onto suppliers. The expense pressure is accelerating demand for high-efficiency motors and VFD retrofits, but may drag on near-term volume sales.

Fragmented Local Manufacturing Base

More than 1,200 mostly small Indian assemblers and 340 Indonesian firms price aggressively yet struggle with ISO 9001 certification and on-time spares. Vietnamese traders rebrand imports, complicating warranty claims when tropical humidity and voltage swings cause premature failures. Absence of standardized part catalogs forces large end-users to stock multiple inventories, tying up working capital. Thailand’s investment board now offers tax incentives for firms meeting ASEAN Cosmetic Directive compliance, a move that could accelerate consolidation. Precision machining needs for positive-displacement rotors keep the segment dependent on imports from Europe and Japan, sustaining higher landed costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pump Type: Centrifugal Resilience Anchors Growth

Centrifugal models captured 55.2% of the Asia-Pacific pumps market share in 2024, and the segment will climb at a 6.8% CAGR through 2030 as high-flow, low-maintenance performance and VFD compatibility align with utilities’ efficiency mandates. Split-case variants enable in-situ impeller swaps, trimming outage from two days to six hours, a compelling metric for treatment-plant operators. Positive-displacement pumps fill metering, slurry, and viscous-fluid niches where constant flow overrides higher maintenance. Japan’s cGMP update pushed pharma plants toward lobe designs, while South Korea’s dairy sector adopted 3-A sanitary pumps with tool-free disassembly. Australia’s iron-ore miners ordered 240 ceramic-lined progressive-cavity pumps in 2024, showing deep-niche durability.

Expansion of abrasive-service requirements drives ceramic-rotor and tungsten-carbide seal adoption. Ebara’s 14% shipment rise to Southeast Asian water utilities underscores centrifugal momentum, as stainless-steel impellers address brackish-water corrosion in Vietnam and Indonesia. Meanwhile, centrifugal OEMs embed IoT sensors for real-time efficiency monitoring, facilitating energy-performance contracts tied to guaranteed kilowatt-hour reductions.

By Drive Technology: Electric Dominance, Renewable Surge

Electric motors held a 73.5% share of the Asia-Pacific pumps market in 2024, but growth moderates as replacement cycles stretch beyond 12 years in mature urban zones. Solar and battery-backed pumps expand at 9.3% CAGR, buoyed by India’s 18-GW solar addition, which enabled 42,000 diesel-to-solar swaps and cut 1.2 million tonnes of CO₂ annually.[4]Ministry of New and Renewable Energy, “Annual Solar Deployment Report 2024,” mnre.gov.in Australian open-pit mines run hybrid solar-diesel sets that shrink genset runtime 60%, saving USD 120,000 per site each year.

Voltage swings of ±15% on rural grids in India, Indonesia, and Vietnam prompt OEMs to widen motor tolerance and embed surge-protect devices. Diesel-driven pumps remain indispensable for mobile flood relief and firefighting due to fuel access and rapid deployment. Sealless and magnetically driven units grow within the hydrogen, semiconductor, and pharma verticals by eliminating fugitive emissions. Japan’s NEDO trialed lithium-iron-phosphate batteries that sustain six-hour nighttime irrigation autonomy, addressing solar intermittency. Economic breakeven arrives wherever diesel tops USD 1.20/litre, now common across most of Southeast Asia and the Pacific Islands.

By Position: Surface Leads, Submersibles Accelerate

Surface pumps represented 58.7% of 2024 installations as industrial and agricultural operators favor above-ground accessibility for frequent impeller changes and multi-point intake schemes. Submersible orders will climb at a 7.0% CAGR through 2030 because borewell, sewage, and flood-control duties reward compact footprints and noise suppression. India’s Jal Jeevan Mission specified 100-m-head submersible sets for 8.2 million rural connections. Thailand installed 14,000 VFD-equipped borewell pumps with soil-moisture sensors that trimmed electricity draw by 28%.

Vertical in-line designs are replacing horizontal end-suction pumps in data centers, cleanrooms, and high-rise buildings, where they free 60% floor space and simplify piping. Singapore’s SS 530:2024 mandates live dashboards and predictive-maintenance alerts, accelerating in-line adoption. Motor cooling poses the chief submersible hurdle in shallow wells and high-temperature effluent; water-jacketed casings and thermal cut-outs mitigate overload. Vietnam’s flood-control agency deployed 1,800 trailer-mounted submersibles capable of autonomous cellular-based operation, illustrating mobility’s rising value.

By Application: Water Dominates, Diversification Emerges

Water and wastewater uses held 47.4% of 2024 demand and will register a 6.6% CAGR through 2030 thanks to pipeline rehabilitation and sewerage build-outs across China, India, and Indonesia. Chemical plants require duplex-steel, titanium, or ETFE-lined pumps priced from USD 15,000 to USD 80,000, illustrated by PETRONAS’s USD 2.1 billion offshore platform contracts specifying sour-gas injection units. HVAC systems absorb chilled water, and condenser water pumps are tied to data-center and commercial real-estate growth. Upstream and midstream oil and gas rely on API 610-compliant multistage centrifugals, while food processors demand 3-A or EHEDG sanitary models.

Mining calls for abrasion-resistant slurry designs, as seen in Australia’s 1,400 hard-metal orders during 2024. Japan’s nuclear restart required 320 seismic-qualified reactor-coolant pumps, and South Korea’s fabs installed 2,600 magnetically driven ultrapure-water sets. Pharmaceuticals consume validation-ready lobe and progressive-cavity pumps, totaling 12,000 units in India during 2024. Application diversity forces OEMs to maintain parallel product lines and spares, elevating overhead but widening resilience against sector downturns.

Geography Analysis

China maintained a 39.9% share of the Asia-Pacific pumps market in 2024, buoyed by domestic production scale despite housing-sector headwinds. The government earmarked CNY 1.2 trillion for urban water infrastructure, aiming for 95% sewerage coverage in prefecture-level cities by 2030. India leads growth at a 7.1% CAGR, funded by central infrastructure bonds and state water-grid tenders that pull forward procurement. Rural programs require 2.4 million pumps, spurring local motor and casting integration in Coimbatore, Gujarat, and Pune.

Japan’s USD 12.1 billion renewal budget keeps replacement volumes steady, with demand skewing toward IoT-enabled, energy-efficient units. South Korea’s USD 18 billion petrochemical capex pipeline secures high-spec API pumps. Malaysia, Thailand, Indonesia, and Vietnam channel FDI into industrial parks that pre-install shared pump rooms, cutting tenant ramp-up time. Indonesia’s capital relocation to Nusantara forecasts USD 420 million in pump outlays through 2028, while Malaysia’s USD 2.1 billion non-revenue-water program emphasizes leakage-reducing VFD retrofits.

Australia and New Zealand still represent high-value niches for rugged slurry or dewatering sets, supported by steady iron-ore and dairy output, respectively. The Philippines, Bangladesh, and Pacific Island nations import refurbished pumps to bridge capital gaps, saving 40%-60% versus new units but enduring shorter life and patchy warranties. Certified remanufacturing programs offering documented testing and limited guarantees are emerging as a middle ground.

Competitive Landscape

Global multinationals hold about 35%-40% of the Asia-Pacific pumps market, leveraging advanced materials, IoT suites, and energy-performance contracts that justify 20%-30% price premiums. Chinese producers exploit vertical integration from castings to motors, pricing 15%-25% lower yet striving to overturn legacy quality perceptions in API-610 and sanitary domains. Indian firms now export to Africa and West Asia, often via joint ventures to access sealing technology and remote-monitoring platforms.

White-space pockets include hydrogen-electrolyser pumps, solar-hybrid off-grid kits, and VFD retrofit modules for legacy install bases. Brands such as Shimge and Zhejiang Doyin address residential niches through direct-to-consumer e-commerce and 48-hour delivery, skirting distributor margins. Grundfos disclosed 62% of its 2024 shipments carried remote-monitoring hardware, proving connectivity is now mainstream. ISO 9001 and API 610 certification remain prerequisites for large tenders, splitting bids between qualified multinationals and rising regional challengers.

Shipping instability and PFAS rulemaking intensify vertical-integration imperatives. Mid-tier players without foundry capacity or energy hedges face a margin squeeze as raw-material premiums mount. Strategic moves like Kirloskar’s solar-submersible launch and Sulzer’s Perth repair-hub expansion underline the pivot toward service revenue, cushioning cyclical equipment sales.

Asia-Pacific Pumps Industry Leaders

Grundfos Holding A/S

Ebara Corporation

Kirloskar Brothers Ltd.

Xylem Inc.

Flowserve Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Under the “Magel Tyala Solar Pump” initiative, the Government of Maharashtra achieved a historic milestone in renewable energy-driven irrigation by completing a Guinness World Records attempt. In a remarkable feat, the state installed 45,911 solar water pumps in just one month, setting a record for one of the fastest and largest deployments worldwide.

- November 2025: Chinese researchers introduced a groundbreaking hybrid wind-solar heat pump, boasting enhanced energy efficiency and the potential to slash household energy costs by over 50%. This cutting-edge heat pump, harnessing both wind and solar energy, is the brainchild of scientists from Shenyang Jianzhu University and Shanghai Jiao Tong University.

- October 2025: The Tamil Nadu government has greenlit an allocation of INR 12.98 crore for establishing a state-of-the-art centre dedicated to advanced pump motor manufacturing. The Southern India Engineering Manufacturers Association (SIEMA) has announced that the Scientific and Industrial Testing and Research Centre (SiTarc) will not only provide the land and building for the initiative but will also shoulder 10% of the project's total cost.

- December 2024: Through its wholly owned subsidiary, Aver Asia (S) Pte Ltd. (Aver Asia), Sumitomo Corporation has taken full control, acquiring 100% of the shares of PT. Resource Equipment Indonesia (REL). REL specializes in renting out large pumps, primarily catering to mining sites across Indonesia.

Asia-Pacific Pumps Market Report Scope

Pumps, mechanical devices, convert energy to elevate, transport, or compress fluids, be it liquids or gases. By transforming mechanical energy into hydraulic or pneumatic energy, pumps generate a pressure difference, propelling fluids from lower to higher pressure zones.

The Asia-Pacific pumps market is segmented by pump type, drive technology, position, application, and geography. By pump type, the market is segmented into centrifugal and positive-displacement. By drive technology, the market is segmented into electric motor, diesel/gas engine, solar/renewable, and magnetically-driven/sealless. By position, the market is segmented into surface, submersible, and vertical in-line. By application, the market is segmented into water and wastewater, chemical and petrochemical, HVAC and building services, oil and gas, food and beverage, mining and metals, power generation, pharmaceuticals and biotech, and others. The report also covers the market sizes and forecasts for the Asia-Pacific pumps market across major countries. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Centrifugal |

| Positive-Displacement |

| Electric Motor |

| Diesel/Gas Engine |

| Solar/Renewable |

| Magnetically-Driven/Sealless |

| Surface |

| Submersible |

| Vertical In-Line |

| Water and Wastewater |

| Chemical and Petrochemical |

| HVAC and Building Services |

| Oil and Gas (Upstream, Midstream, Downstream) |

| Food and Beverage |

| Mining and Metals |

| Power Generation (Thermal, Nuclear, Renewables) |

| Pharmaceuticals and Biotech |

| Others |

| China |

| India |

| Japan |

| South Korea |

| Malaysia |

| Thailand |

| Indonesia |

| Vietnam |

| Australia |

| Rest of Asia-Pacific |

| By Pump Type | Centrifugal |

| Positive-Displacement | |

| By Drive Technology | Electric Motor |

| Diesel/Gas Engine | |

| Solar/Renewable | |

| Magnetically-Driven/Sealless | |

| By Position | Surface |

| Submersible | |

| Vertical In-Line | |

| By Application | Water and Wastewater |

| Chemical and Petrochemical | |

| HVAC and Building Services | |

| Oil and Gas (Upstream, Midstream, Downstream) | |

| Food and Beverage | |

| Mining and Metals | |

| Power Generation (Thermal, Nuclear, Renewables) | |

| Pharmaceuticals and Biotech | |

| Others | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Australia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How big is the Asia-Pacific pumps market in value terms?

It totals USD 35.32 billion in 2025 and is forecast to reach USD 45.62 billion by 2030.

Which pump type leads regional demand?

Centrifugal models command 55.2% of 2024 sales owing to versatility in water, HVAC, and cooling duties.

Where is the fastest growth expected geographically?

India is projected to post the region’s quickest 7.1% CAGR through 2030 as infrastructure bonds and water-grid tenders accelerate procurement.

Are renewable-powered pumps gaining real traction?

Yes, solar and battery-backed units are rising at a 9.3% CAGR, especially in agriculture and remote mining.

What drives current pump replacement cycles?

Flood-control mandates, energy-efficiency rules, and tariff-driven OPEX pressure are prompting utilities and industries to adopt VFD-equipped, high-efficiency designs.

How are PFAS rules affecting material choices?

Anticipated bans are steering chemical-duty pump buyers toward ETFE linings and ceramic coatings despite 18%-25% higher material cost.

Page last updated on: