Asia-Pacific Printed Circuit Board Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

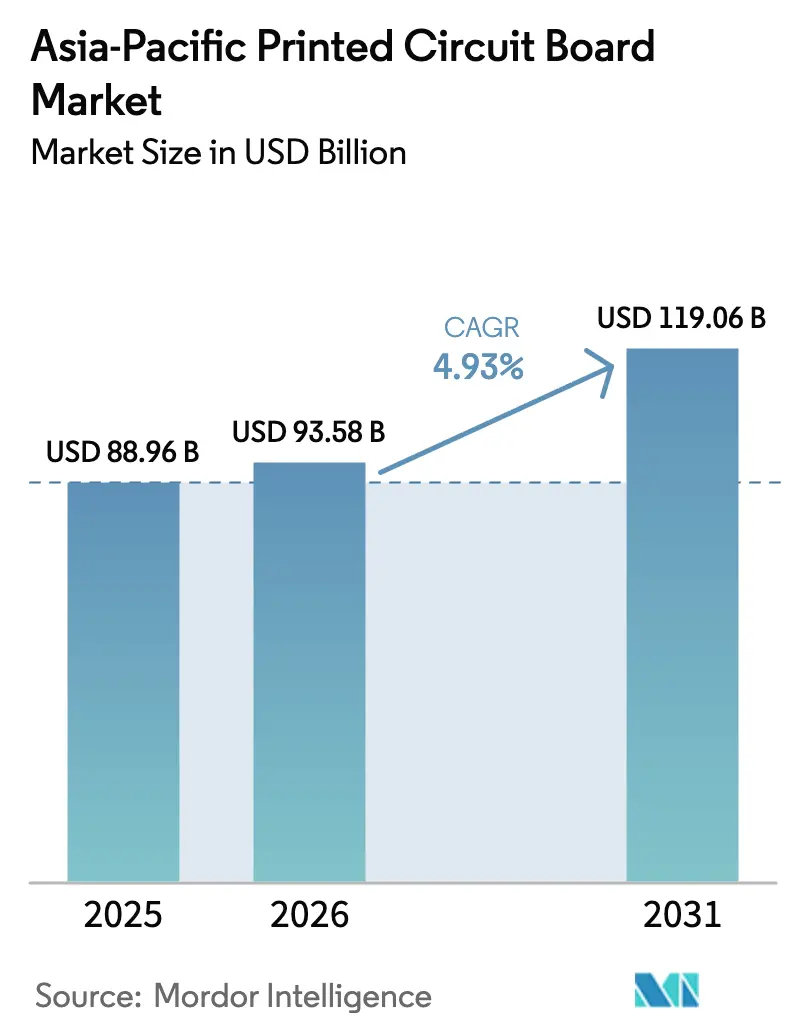

| Base Year Market Size (2025) | USD 88.96 Billion |

| Market Size (2026) | USD 93.58 Billion |

| Market Size (2031) | USD 119.06 Billion |

| Growth Rate (2026 - 2031) | 4.93% CAGR |

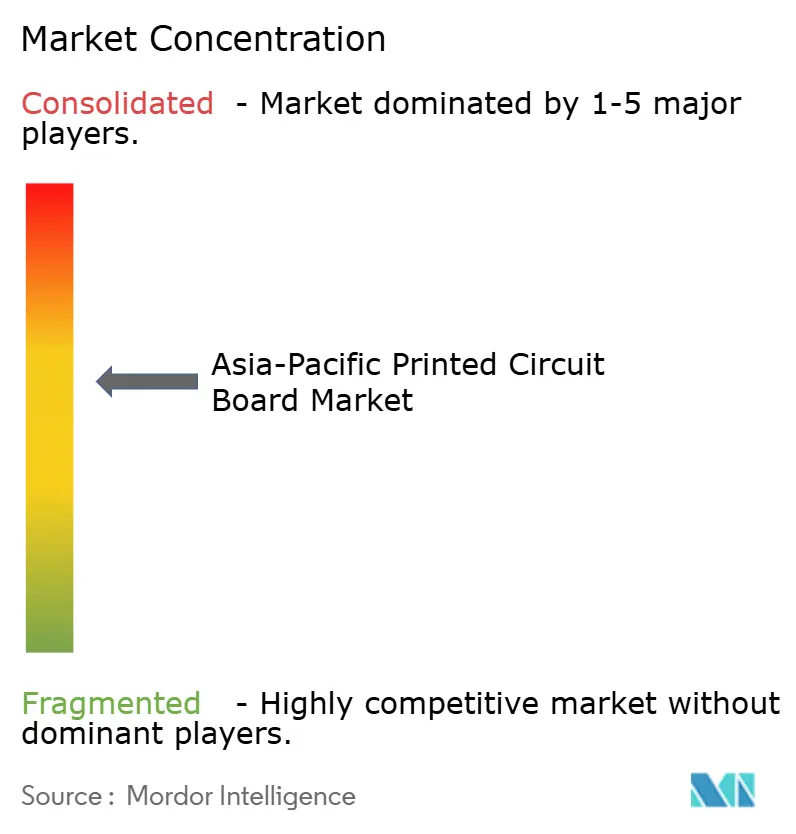

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Printed Circuit Board Market Analysis by Mordor Intelligence

The Asia-Pacific Printed Circuit Board Market is expected to grow from USD 88.96 billion in 2025 to USD 93.58 billion in 2026 and is forecasted to reach USD 119.06 billion by 2031 at 4.93% CAGR over 2026-2031. Strong regional electronics output anchors current demand, while incremental growth now revolves around advanced-node packaging, localized supply chains, and widening end-market adoption. The Asia-Pacific PCB market is benefiting from sustained data-center buildouts, rising EV penetration, and aggressive 5G roll-outs that collectively increase high-layer-count and high-speed board content. At the same time, capital intensity is rising as fabricators adopt modified semi-additive processes, laser-directed imaging, and automated optical inspection to meet sub-25-micron line-and-space requirements. Competitive dynamics favor suppliers with scale, technology depth, and regulatory compliance capabilities, yet niche specialists continue to prosper in rigid-flex, ceramic, and heavy-copper designs that serve differentiated thermal or reliability needs.

Key Report Takeaways

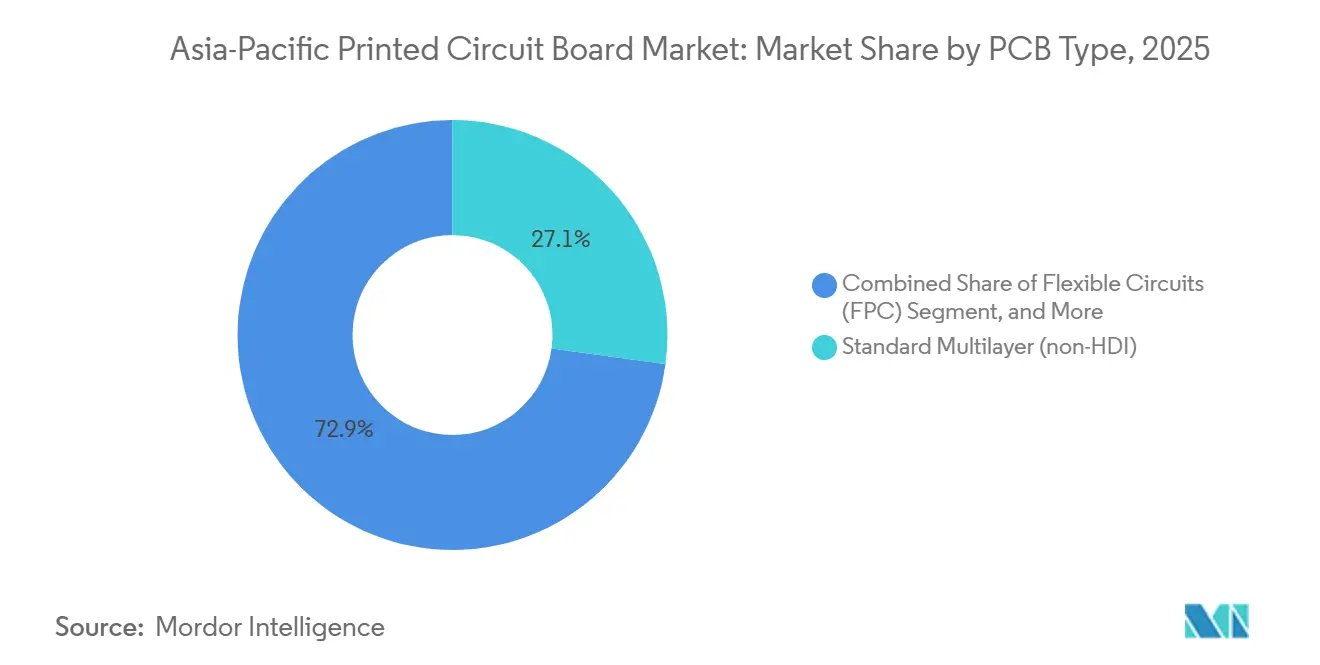

- By PCB type, standard multilayer boards accounted for 27.15% of the Asia-Pacific printed circuit board market in 2025, while flexible circuits are forecast to grow at a 5.24% CAGR through 2031.

- By substrate material, glass-epoxy FR-4 captured 42.76% revenue share in 2025, and high-speed low-loss laminates are projected to register a 5.61% CAGR between 2026 and 2031.

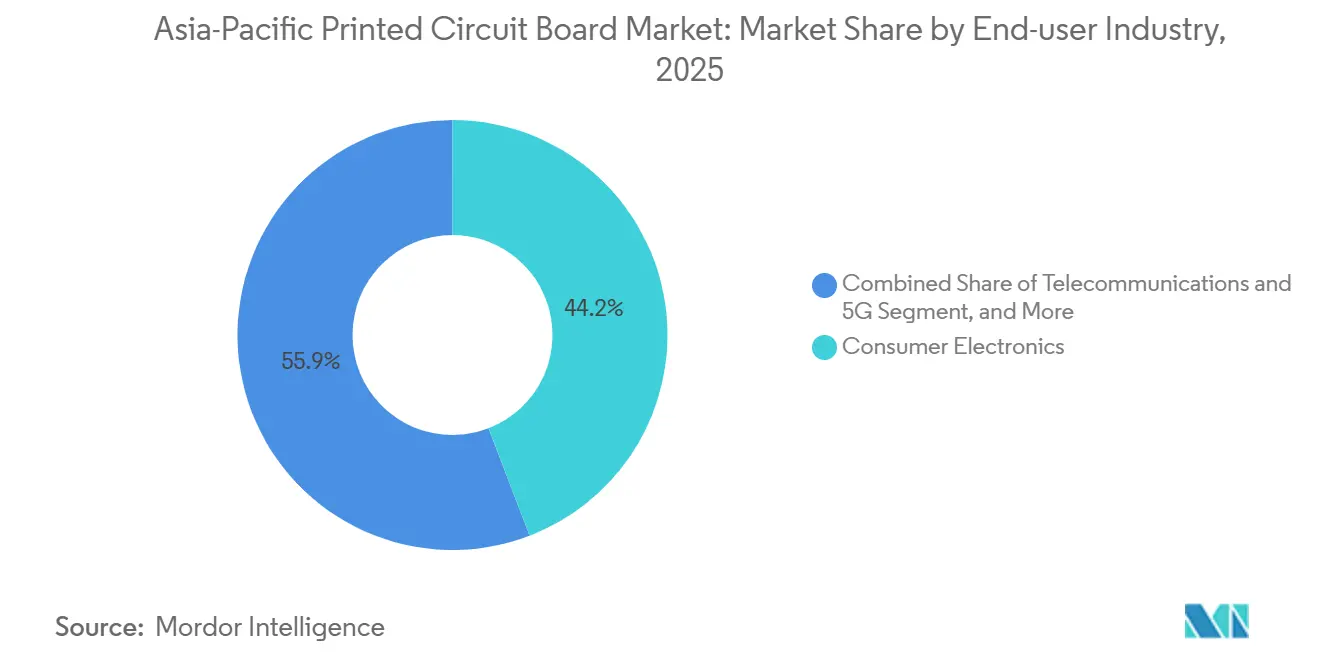

- By end-user industry, consumer electronics accounted for 44.15% of 2025 revenue, whereas telecommunications and 5G infrastructure are poised to expand at a 5.59% CAGR during the outlook period.

- By country, China held 56.62% of the Asia-Pacific PCB market share in 2025, whereas India is on track to post a 5.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Miniaturization Requirements in Consumer Electronics | +1.2% | China, South Korea, Taiwan, Vietnam | Medium term (2-4 years) |

| Expanding 5G Infrastructure Deployments | +1.1% | China, India, South Korea, Japan | Short term (≤ 2 years) |

| Surge in AI and High-Performance Computing Hardware Demand | +1.0% | China, Taiwan, Japan | Short term (≤ 2 years) |

| Government Incentives for Domestic PCB Manufacturing | +0.9% | India, China, Japan | Medium term (2-4 years) |

| Accelerating Electric Vehicle Production Targets | +0.8% | China, Japan, South Korea, India | Long term (≥ 4 years) |

| Shift Toward Module-Level System-in-Package Solutions | +0.7% | Taiwan, South Korea, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Miniaturization Requirements In Consumer Electronics

Foldable smartphones, smartwatches, and mixed-reality headsets now demand sub-50 micron trace widths and stacked micro-vias that conventional photolithography cannot pattern at acceptable yields. Samsung’s Galaxy Z Fold6 and Huawei’s Mate X5 employ eight-layer rigid-flex sections that survive more than 200,000 bend cycles without signal degradation, while Apple’s Vision Pro integrates a 14-layer HDI mainboard that cuts z-height by 18% through embedded passive components. Average smartphone layer count increased from 10 in 2023 to 12 in 2025, and flagship designs are targeting up to 16 layers by 2027, pushing fabricators to install modified semi-additive process lines that raise capital intensity by roughly 20%.

Expanding 5G Infrastructure Deployments

India operated 474,000 5G base stations by December 2025 and plans an additional 300,000 within a year, with each macro site using four to six multilayer boards that must withstand wide temperature swings and high humidity. China’s 4.76 million 5G sites are shifting toward network densification in industrial parks, increasing demand for ruggedized PCBs with extended vibration tolerance. Vietnam issued commercial 5G licenses in late 2024, and local-content rules implemented in 2025 drive domestic sourcing from Viettel High Tech. Open RAN architectures adopted in India and Japan further fragment design requirements and favor modular board layouts validated across several chipset ecosystems.

Accelerating Electric Vehicle Production Targets

China requires 45% EV penetration by 2027, a mandate that more than doubles automotive PCB area per vehicle. [1]Ministry of Industry and Information Technology, “Notice on the Development Goals for New Energy Vehicles, 2025-2027,” miit.gov.cn Japan’s Green Growth Strategy and South Korea’s K-Semiconductor tax credits spur new heavy-copper lines for zone controllers, while the International Energy Agency projects Asia-Pacific will need six times today’s power-electronics board capacity by 2030. [2]International Energy Agency, “Global EV Outlook 2025,” iea.org Each battery-electric platform now packs 2–3 m² of PCB real estate, roughly twice that of internal-combustion models, and high-voltage inverters specify 6-ounce copper to handle 105-amp continuous currents. India’s FAME-III scheme reimburses up to INR 1,50,000 per commercial EV and ties the incentive to 60% domestic PCB value addition, prompting Bharat FIH and Dixon to build local lines.

Shift Toward Module-Level System-in-Package Solutions

IPC’s 2025 roadmap documents a 28% jump in SiP layout requests, prodding fabricators to install 15-micron MSAP lines and plasma surface-finish tools. [3]IPC, “Technology Roadmap 2025,” ipc.org TSMC’s CoWoS-L uses 18-micron redistribution layers, trims package height 14%, and boosts substrate ASPs roughly 20%. Qualcomm’s Snapdragon X80 merges RF, PMIC, and memory dies on a 12-layer organic interposer, shrinking board area 35%. Apple’s M-series SiP embeds passive components to free DDR5 routing channels, demanding laminates with dielectric constants below 3.3 and dissipation factors under 0.005. The Open Compute Project’s Yosemite V3 specification mandates organic interposers for CPU cards, expanding substrate demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain Disruptions for High-End Substrates | -0.6% | Taiwan, Japan, South Korea, China, India | Short term (≤ 2 years) |

| Environmental Compliance Costs and E-Waste Regulations | -0.5% | China, Japan, South Korea, India | Medium term (2-4 years) |

| Talent Shortages in Advanced Packaging Engineering | -0.4% | China, Taiwan, India | Long term (≥ 4 years) |

| Geopolitical Trade Barriers Impacting Component Flow | -0.5% | China, Taiwan, Vietnam, Thailand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Disruptions For High-End Substrates

Ajinomoto’s Kawasaki plant expansion in 2024 lifted output by 20%, yet ABF film remained on allocation through 2025, stretching substrate lead times to 18 weeks and elevating working-capital burdens for smaller OEMs. Unimicron and Nan Ya PCB ran near 95% utilization, where defect rates rose to 12% because process windows narrowed. Alternate BT materials offered by Mitsubishi Gas Chemical lack the thermal cycling endurance needed for 400-watt server sockets, constraining substitution and delaying hyperscale platform launches.

Environmental Compliance Costs And E-Waste Regulations

China’s tightened Restriction of Hazardous Substances rules, effective January 2025, expanded mandatory third-party testing to industrial boards, adding roughly CNY 50,000 (USD 7,000) in annual costs per product family. Japan’s updated e-waste law imposed extended producer responsibility on PCB makers, requiring them to finance collection and recycling schemes that smaller firms struggle to absorb. South Korea introduced recycled-content quotas for FR-4 laminates in 2025, yet the insufficient supply of post-consumer epoxy forces manufacturers to purchase virgin resin at 8% premiums, compressing margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By PCB Type: Flexible Circuits Accelerate As Miniaturization Intensifies

Standard multilayer boards, which accounted for 27.15% of the Asia-Pacific printed circuit board market in 2025, continue to anchor automotive body-control modules and industrial drives but face 3% to 4% annual price erosion as Chinese suppliers add capacity. High-density interconnect boards enable sub-100-micron vias and are now standard in flagship phones, while IC substrates ride the wave of AI-accelerator demand, which requires 30-layer builds with high glass-transition temperatures. Flexible circuits are expected to climb at a 5.24% growth pace from 2026 to 2031, eclipsing the broader 4.93% expansion of the Asia-Pacific PCB market. Smartphone OEMs pursuing foldable designs and wearable brands embedding biosensors into compact enclosures drive this momentum.

Rigid-flex assemblies are gaining traction in automotive ADAS and LiDAR modules, where flexibility cuts connector count and improves vibration tolerance. Metal-core and ceramic boards remain niche, accounting for less than 5% of regional revenue, serving high-heat LED and power-electronics applications. Capex trends signal sustained investment in flexible and HDI capacity, as evidenced by Tripod and Kinwong installing laser-direct imaging and plasma desmear lines that achieve 25-micron line-and-space geometries. As a result, suppliers positioned in these premium niches are securing longer order backlogs and higher asset turns compared with commodity multilayer producers.

By Substrate Material: High-Speed Laminates Gain Premium As Data Rates Rise

High-speed low-loss laminates are forecast to expand at a 5.61% clip through 2031, propelled by Ethernet switch upgrades to 800 G and 1.6 T that need dielectric constants below 3.5 and dissipation factors under 0.005. Glass-epoxy FR-4 retained 42.76% Asia-Pacific printed circuit board market share in 2025 due to its USD 8 per square meter cost advantage, yet hyperscale operators increasingly adopt premium Megtron 6 and Astra MT77 grades despite 30% higher laminate pricing. Polyimide, indispensable in flexible circuits, commands USD 40 to USD 50 per square meter because few suppliers match its thermal stability at 260 °C soldering profiles.

BT and ABF resins in IC substrates represent the fastest-growing subcategory, reflecting AI and high-performance computing rollouts. Ajinomoto controls about 70% of this segment and has successfully passed raw material inflation through to customers. Metal-core and ceramic substrates address demanding thermal conditions in RF amps and LED drivers, but collectively account for less than 4% of revenue. The introduction of stricter IPC-4101 flame-retardancy limits in 2024 required requalification for many laminate families, stretching new product introduction cycles by as much as nine months for automotive and aerospace programs.

By End-User Industry: Telecommunications Outpaces Consumer Electronics

Consumer electronics still led revenue with 44.15% share in 2025, yet smartphone unit volumes plateau, so incremental PCB content arises from features like satellite connectivity rather than sheer shipment growth. Computing and data-center demand for 30-plus-layer motherboards accelerates alongside AI server deployments, a level of complexity that fewer than a dozen Asia-Pacific PCB market suppliers produce at yields above 80%. Telecommunications and 5G infrastructure are projected to advance at a 5.59% rate from 2026 to 2031, overtaking consumer electronics, which grows at 4.15%. Network densification in India and Vietnam requires ruggedized multilayer boards with conformal coatings, which add 12% to the bill of materials.

Automotive and EV platforms double PCB area compared with internal combustion vehicles, requiring heavy-copper boards for 105-amp continuous current. Industrial power electronics continue to specify thick-copper layouts for solar inverters, while medical wearables are migrating toward flexible circuits, even though regulatory approval cycles remain long. Aerospace and defense, though low in volume, command margin-rich contracts due to MIL-PRF and AS9100 traceability needs, reinforcing the value of certifications as competitive moats.

Geography Analysis

China’s 56.62% grip on the Asia-Pacific printed circuit board market in 2025 stemmed from unmatched supply-chain density, yet rising wages and tougher environmental rules are nudging capacity westward to Jiangxi and Hubei provinces. The government allocated CNY 15 billion (USD 2.1 billion) to support IC-substrate expansion, and Zhen Ding and Shennan Circuits each committed more than CNY 5 billion (USD 700 million) to capture domestic AI-chip demand. India, projected to post a 5.92% CAGR to 2031, benefits from Production Linked Incentive rebates that drive Dixon and Bharat FIH to build smartphone board lines, while additional 25% capital subsidies under the Electronics Component and Semiconductor Manufacturing scheme attract Taiwanese joint ventures.

Japan maintains leadership in high-layer-count FC-BGA substrates for server CPUs, with Ibiden and Shinko Electric accounting for roughly 60% of global output through proprietary resin and laser-drilling expertise. South Korean suppliers Samsung Electro-Mechanics and LG Innotek vertically integrate PCB capacity with handset and vehicle electronics divisions, cutting time-to-market for new modules and retaining margin that merchant fabs previously secured.

Taiwan, Vietnam, Thailand, and Malaysia together generated 20% of 2025 revenue. Taiwan’s Unimicron, Nan Ya PCB, and Tripod focus on modified semi-additive and laser-direct imaging investments aligned with TSMC’s packaging roadmap, whereas Vietnam and Thailand draw labor-intensive assembly after Chinese wage inflation. Malaysia’s Penang cluster diversifies into substrates, highlighted by AT&S pledging EUR 2 billion (USD 2.2 billion) for its Kulim plant due online in 2027.

Competitive Landscape

The Asia-Pacific printed circuit board market displays moderate concentration. Chinese champions Zhen Ding and Shennan Circuits accelerated IC-substrate output to serve Biren and Moore Threads, lessening reliance on smartphone accounts. Taiwanese leaders Unimicron and Nan Ya PCB funnel capex toward fan-out wafer-level packaging substrates that promise higher ASPs per square inch, positioning them for Apple and AMD socket wins. Ibiden maintains a near-duopoly in high-layer-count FC-BGA substrates for server CPUs thanks to resin formulations and laser-drilling recipes that maintain yields above 85%, a benchmark that only a handful of rivals approach.

South Korean conglomerates Samsung Electro-Mechanics and LG Innotek are internalizing PCB needs for smartphones and EV electronics, shrinking the addressable market for merchant suppliers. Ceramic substrates for LED lighting, heavy-copper boards for industrial inverters, and rigid-flex for medical implants all require specialized processes that deter high-volume competitors.

Technology is the fulcrum of differentiation, with fewer than twenty regional plants able to pattern 25 micron lines at commercial scale, allowing those operators to collect double-digit margin spreads over commodity board shops. Patent filings, such as AT&S’s 2025 hybrid organic-silicon interposer architecture, underscore incumbents’ intent to protect process IP, while challengers like Kinwong and FLEXium carve footholds in AR/VR and LiDAR applications where legacy fabs struggle to meet emerging size and weight constraints.

Asia-Pacific Printed Circuit Board Industry Leaders

Zhen Ding Technology Holding Limited

Shennan Circuits Co., Ltd.

Unimicron Technology Corporation

Nan Ya PCB Corporation

Ibiden Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Unimicron Technology announced a TWD 25 billion (USD 800 million) expansion in Taoyuan for AI-grade IC substrate capacity, with a Q4 2027 ramp target.

- December 2025: Samsung Electro-Mechanics completed a KRW 1.2 trillion (USD 900 million) automotive PCB facility in Busan focusing on battery-management and zone-controller boards.

- November 2025: AT&S AG secured a EUR 500 million (USD 550 million) contract to supply multilayer rigid-flex boards for European automotive ADAS cameras through 2030.

- October 2025: Ibiden committed JPY 80 billion (USD 530 million) to expand FC-BGA substrate output at its Ogaki plant, scheduled for Q2 2027 commissioning.

Asia-Pacific Printed Circuit Board Market Report Scope

Printed Circuit Boards (PCBs) are essential components used to mechanically support and electrically connect electronic components through conductive pathways, tracks, or signal traces. They are widely utilized across various industries, including consumer electronics, automotive, telecommunications, and healthcare, among others.

The Asia-Pacific Printed Circuit Board (PCB) Market Report is Segmented by PCB Type (Standard Multilayer, Rigid 1-2 Sided, High-Density Interconnect, Flexible Circuits, IC Substrates, Rigid-Flex, and Other PCB Types), Substrate Material (Glass Epoxy, High-Speed Low-Loss, Polyimide, Packaging Resins, and Other Substrate Materials), End-user Industry (Consumer Electronics, Computing and Data Centers, Telecommunications and 5G, Automotive and EV, Industrial and Power, Healthcare and Medical, Aerospace and Defense, and Other End-user Industries), and Country (China, Japan, India, South Korea, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| Standard Multilayer (non-HDI) |

| Rigid 1-2 Sided |

| High-Density Interconnect (HDI) |

| Flexible Circuits (FPC) |

| IC Substrates (Package Substrates) |

| Rigid-Flex |

| Other PCB Types |

| Glass Epoxy (FR-4) |

| High-Speed / Low-Loss |

| Polyimide (PI) |

| Packaging Resins (BT / ABF) |

| Other Substrate Materials |

| Consumer Electronics |

| Computing and Data Centers |

| Telecommunications and 5G |

| Automotive and EV |

| Industrial and Power |

| Healthcare / Medical |

| Aerospace and Defense |

| Other End-user Industries |

| China |

| Japan |

| India |

| South Korea |

| Rest of Asia-Pacific |

| By PCB Type | Standard Multilayer (non-HDI) |

| Rigid 1-2 Sided | |

| High-Density Interconnect (HDI) | |

| Flexible Circuits (FPC) | |

| IC Substrates (Package Substrates) | |

| Rigid-Flex | |

| Other PCB Types | |

| By Substrate Material | Glass Epoxy (FR-4) |

| High-Speed / Low-Loss | |

| Polyimide (PI) | |

| Packaging Resins (BT / ABF) | |

| Other Substrate Materials | |

| By End-user Industry | Consumer Electronics |

| Computing and Data Centers | |

| Telecommunications and 5G | |

| Automotive and EV | |

| Industrial and Power | |

| Healthcare / Medical | |

| Aerospace and Defense | |

| Other End-user Industries | |

| By Country | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia-Pacific printed circuit board market in 2026?

The Asia-Pacific printed circuit board market size reached USD 93.58 billion in 2026 and is projected to climb steadily through 2031.

Which PCB type is growing fastest across Asia-Pacific?

Flexible circuits are set to expand at a 5.24% CAGR between 2026 and 2031, outpacing all other board categories.

What drives demand for high-speed laminates?

Data-center upgrades to 800 G and 1.6 T Ethernet switches require low-loss materials that preserve signal integrity at elevated data rates.

Why is India the fastest-growing geography for PCBs?

Production Linked Incentive rebates and multinational OEM diversification are propelling India’s 5.92% CAGR to 2031.

Which end-user segment will overtake consumer electronics?

Telecommunications and 5G infrastructure is on track to grow at a 5.59% CAGR, surpassing consumer electronics growth during the forecast period.

Page last updated on: