Asia-Pacific Machining Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

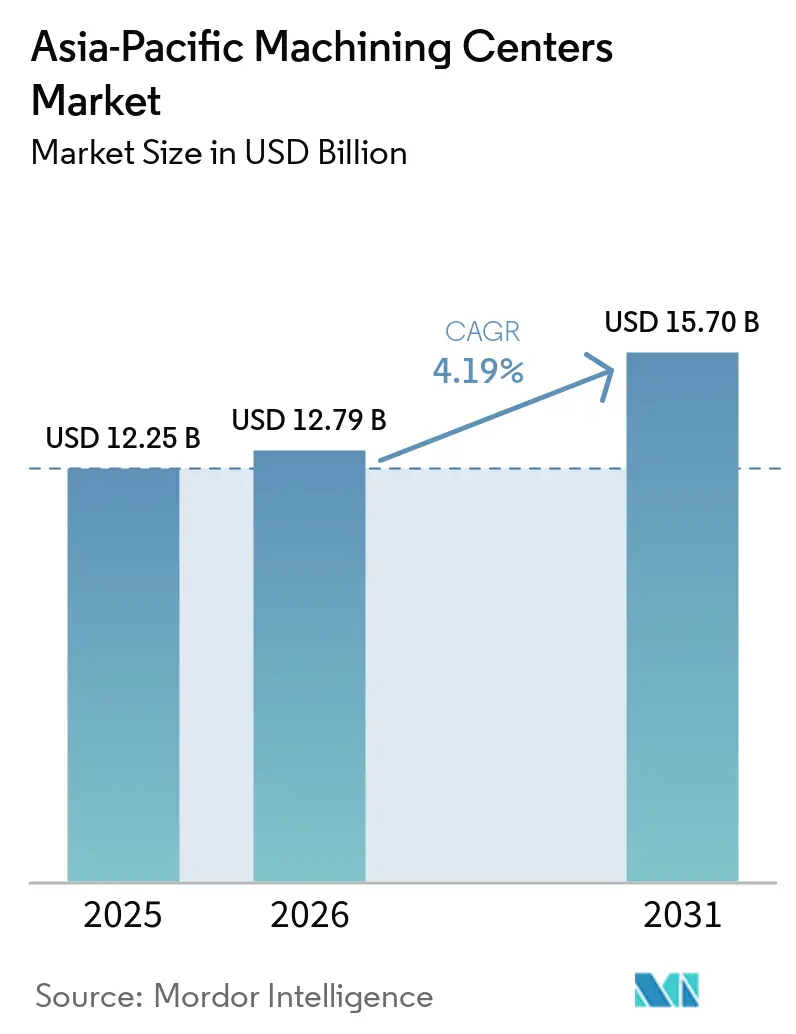

| Base Year Market Size (2025) | USD 12.25 Billion |

| Market Size (2026) | USD 12.79 Billion |

| Market Size (2031) | USD 15.70 Billion |

| Growth Rate (2026 - 2031) | 4.19% CAGR |

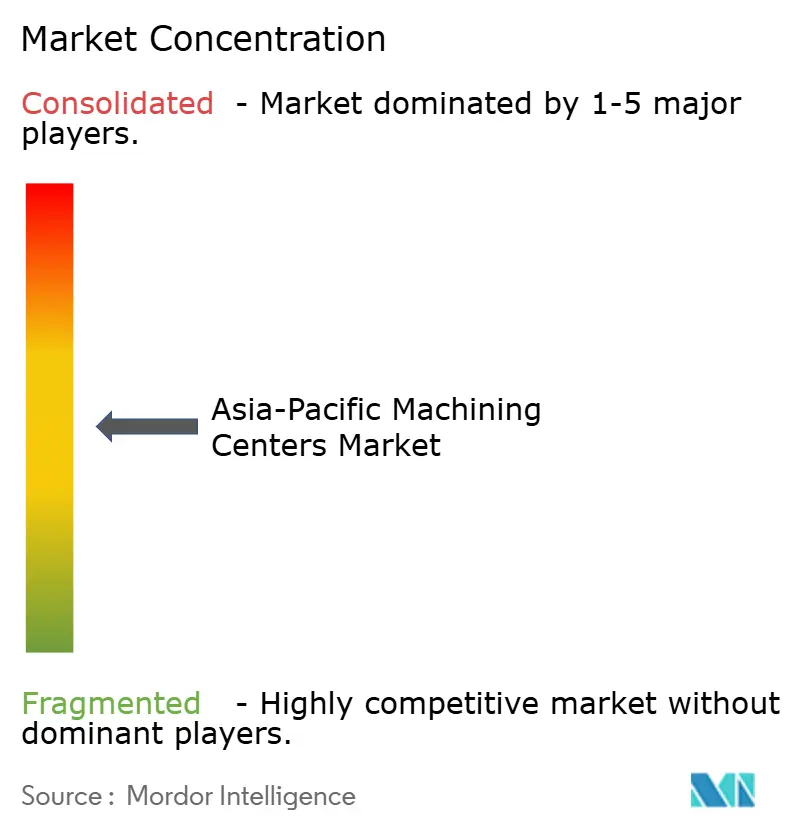

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Machining Centers Market Analysis by Mordor Intelligence

The Asia-Pacific Machining Centers Market size was valued at USD 12.25 billion in 2025 and is estimated to grow from USD 12.79 billion in 2026 to reach USD 15.70 billion by 2031, at a CAGR of 4.19% during the forecast period (2026-2031). China’s shrinking factory workforce, down by 30 million since 2013, continues to accelerate automation, prompting a pivot to lights-out machining lines. Vertical machining centers retained a 38% foothold in 2025, yet multitasking platforms are outpacing them as buyers in automotive and aerospace consolidate milling and turning into a single system. India is emerging as the fastest-growing regional market, supported by USD 410 million in Production-Linked Incentives for medical devices and a wave of electronics reshoring. Semiconductor-fab equipment spending will rise to USD 133 billion in 2026, a momentum that pulls demand for ultra-precision machining of vacuum chambers and wafer-handling robots.[1]International Federation of Robotics, “World Robotics 2025,” ifr.org

Key Report Takeaways

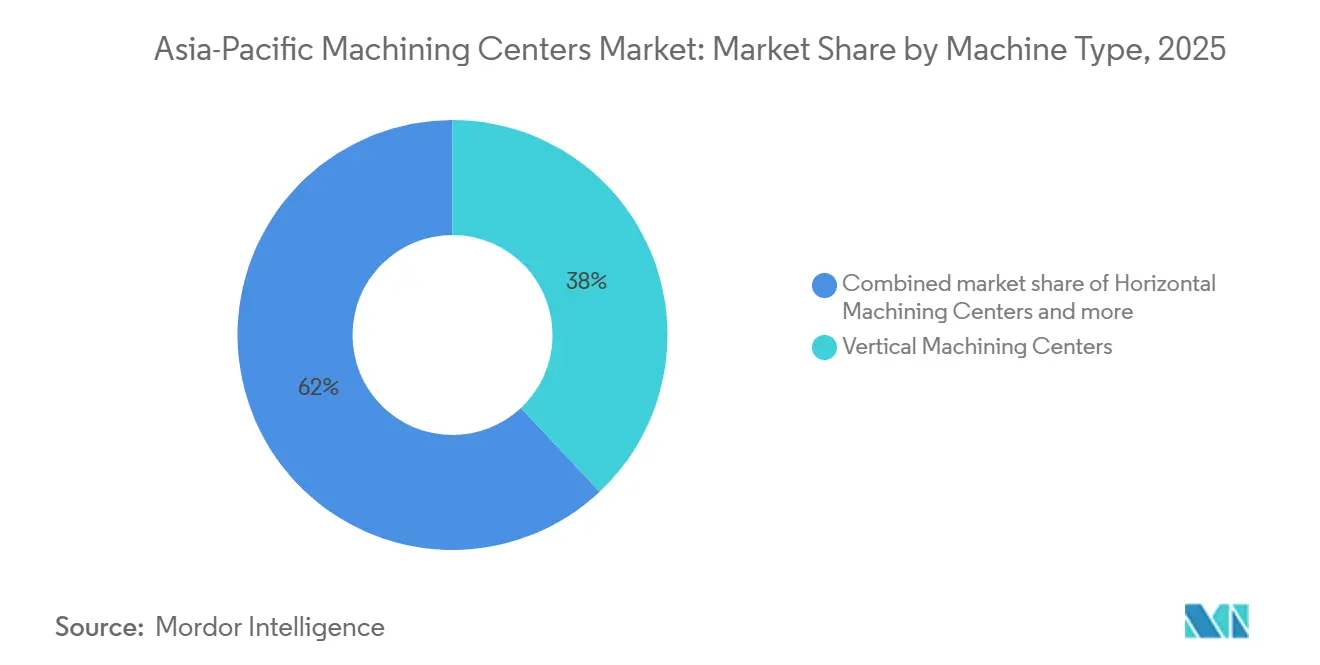

- By machine type, vertical machining centers led with 38% of the Asia-Pacific Machining Centers Market share in 2025, while multi-tasking machining centers are projected to expand at a 6.20% CAGR through 2031.

- By axis configuration, 3-axis systems commanded 46% of the Asia-Pacific Machining Centers Market size in 2025; 5-axis & above are advancing at a 6.80% CAGR to 2031.

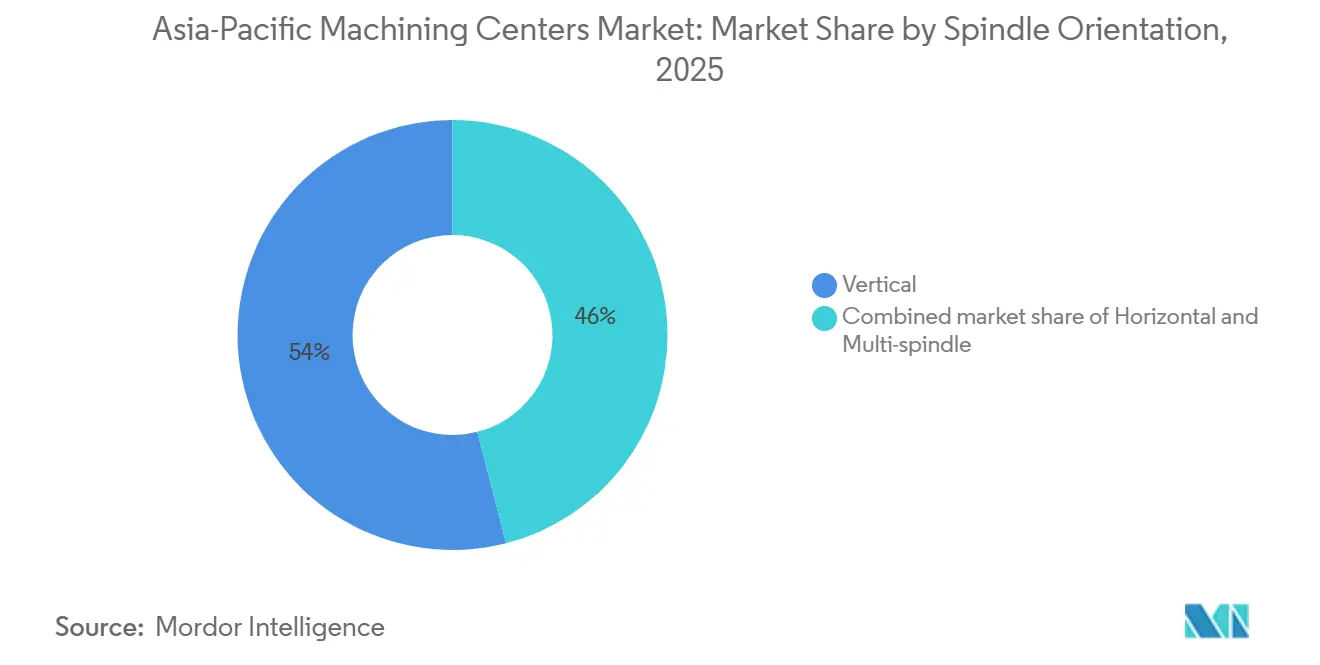

- By spindle orientation, vertical spindles accounted for 54% of the Asia-Pacific Machining Centers Market share in 2025, whereas multi-spindle setups are forecast to grow at 6.50% CAGR over the same period.

- By structure type, column-type frames accounted for 41% of the Asia-Pacific Machining Centers Market size in 2025, and gantry-type machines are set to grow at a 6.10% CAGR through 2031.

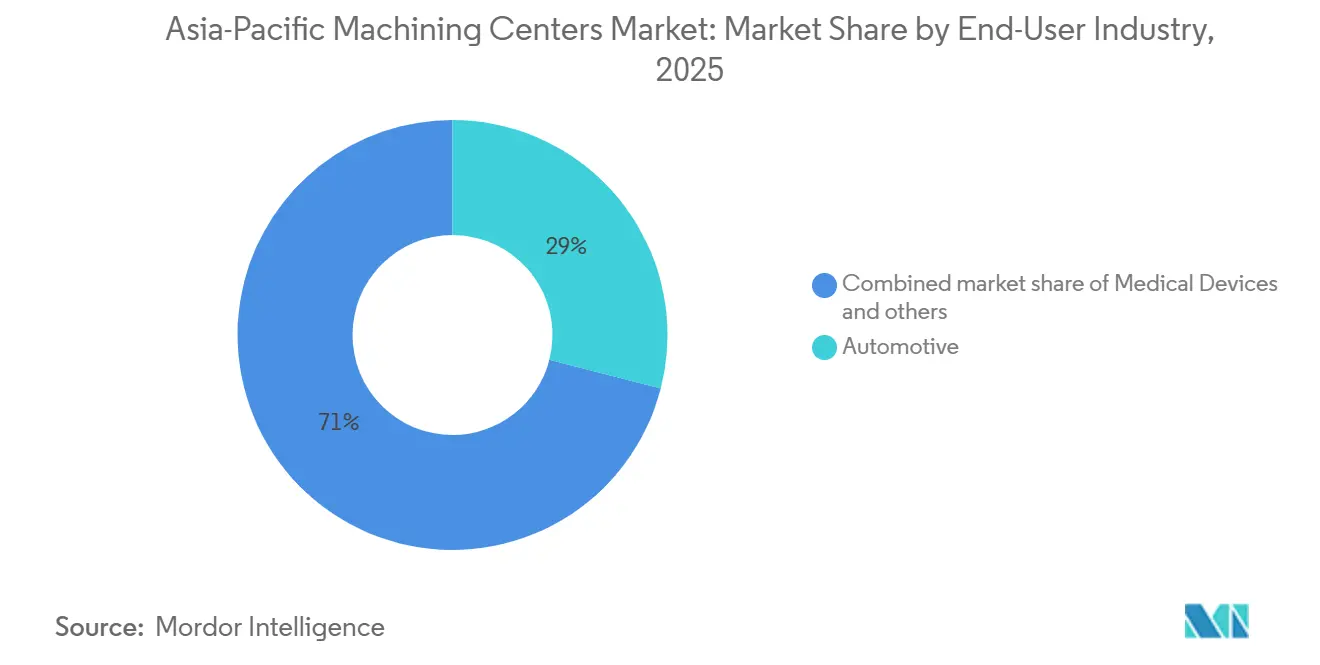

- By end-user industry, automotive accounted for 29% of the Asia-Pacific Machining Centers Market size in 2025, yet medical devices are on track for a 6.90% CAGR through 2031.

- By geography, China held 49% of the Asia-Pacific Machining Centers Market share in 2025, while India is poised for the fastest 7.20% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Machining Centers Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electronics manufacturing reshoring in Asia-Pacific accelerates precision machining demand | +1.2% | Vietnam, India, Thailand; spillover to Malaysia and Indonesia | Medium term (2-4 years) |

| Internal Combustion Engine (ICE)-to-Electric Vehicle (EV) powertrain shift drives multi-axis machining adoption across automotive sector | +1.0% | China, Japan, South Korea, India | Long term (≥ 4 years) |

| Smart factory incentives in China, Japan, and South Korea boost Computer Numerical Control (CNC) automation investments | +0.9% | China, Japan, South Korea; early pilots in Taiwan | Short term (≤ 2 years) |

| Dark factory expansion in China and Singapore drives automated machining center deployment | +0.7% | China (tier-1 cities), Singapore; trials in South Korea | Medium term (2-4 years) |

| Titanium implant manufacturing growth in India raises need for high-precision machining | +0.4% | India (Pune, Bengaluru clusters); exports to ASEAN | Medium term (2-4 years) |

| Asia-Pacific space start-ups increase demand for advanced precision machining capabilities | +0.3% | Japan, India, Australia; nascent in Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electronics Manufacturing Reshoring in Asia-Pacific Accelerates Precision Machining Demand

As electronics assemblers and printed circuit board manufacturers diversify their geographic footprints, the establishment of new production lines is driving the need for precision milling and turning equipment to produce essential molds, jigs, and dies. In Vietnam, Samsung's six major manufacturing complexes and the robust Apple supplier corridors in the northern provinces have established a dominant electronics manufacturing hub, collectively boosting current and forward-looking orders for compact vertical machining centers. Meanwhile, India's expanding tech supply chain saw the addition of a USD 30 million aluminum-housing facility in Chennai, designed to produce 1.2 million units per month, underscoring the growing need for flexible machining cells. Further south, Thailand's Board of Investment approved a total of USD 8.91 billion in electronics and electrical appliance investments for 2025. This surge will heavily depend on high-speed spindle platforms for advanced connector tooling. Overall, procurement trends are shifting away from traditional mass production toward high-mix, small-batch capabilities, further accelerating the regional machining centers market. Because mandatory ISO 9001 quality audits are required to enter these lucrative tech supply chains, even mid-tier machine shops are being compelled to upgrade their legacy equipment.[2]Ministry of Electronics and Information Technology, Government of India, “PLI Scheme for Large Scale Electronics Manufacturing,” meity.gov.in

Internal Combustion Engine (ICE)-to-Electric Vehicle (EV) Powertrain Shift Drives Multi-Axis Machining Adoption Across Automotive Sector

Shifting from internal-combustion engines to battery power removes many legacy parts yet introduces new precision needs for motor housings, battery trays, and reduction gears that call for simultaneous five-axis cutting. Uno Minda invested USD 51 million in its Pune plant to install 5-axis cells dedicated to aluminum battery trays, with production slated for 2026. Japan's trade ministry's export controls on advanced five-axis controllers underscore the technology’s strategic value. As EV volumes rise, the Asia-Pacific machining centers market benefits as suppliers either upgrade three-axis lines with rotary tables or buy full multi-axis platforms. Furthermore, the automotive push to offset the massive weight of batteries with large-scale aluminum structural castings is accelerating demand for large-envelope, high-torque multi-axis centers. This structural shift ensures sustained capital expenditure from Tier 1 suppliers eager to secure lucrative, long-term EV platform contracts.

Smart Factory Incentives in China Japan and South Korea Boost Computer Numerical Control (CNC) Automation Investments

Governments are subsidizing sensor retrofits, cloud dashboards, and edge computing for machine tools, cutting unplanned downtime and raising plant utilization. South Korea reserved approximately USD 336 million in 2025 for smart-manufacturing infrastructure and will co-fund artificial-intelligence modules from 2026. China aims to certify 10,000 lighthouse factories by 2030, with each factory required to connect at least 70% of its equipment in real time. Japan’s builders reported that connected options were selected on 38% of new machining-center orders in 2025, up from 22% two years earlier. Small and mid-sized firms in ASEAN lack funding for such upgrades, widening the technology gap and channeling more high-spec orders toward China, Japan, and South Korea. These policy pushes accelerate revenue flow into the Asia-Pacific machining centers market while also setting new baselines for digital twins and ISO 16739 compliance.

Dark Factory Expansion in China and Singapore Drives Automated Machining Center Deployment

The expansion of capital-intensive "dark factories" running continuously with minimal human intervention is accelerating globally. However, formidable upfront costs largely restrict this strategy to major original equipment manufacturers and Tier-1 contract manufacturers. In the high-volume consumer electronics sector, these investments are funding near-total automation, exemplified by Xiaomi’s Changping plant, which leverages high-density robotics to produce 10 million flagship smartphones annually. This lights-out methodology is also rapidly penetrating diverse legacy supply chains, with massive textile facilities now relying entirely on automated guided vehicles to operate thousands of looms around the clock with zero on-floor workers. Furthermore, extreme automation combined with machine learning is yielding exponential gains in production efficiency, enabling major EV assembly plants in Shanghai to slash manufacturing cycle times as production volume scales drastically. Ultimately, while this hyper-automation risks concentrating supply chains in tier-1 hubs at the expense of smaller regional suppliers, jurisdictions like Singapore are actively piloting lights-out machining cells to offset chronic national labor shortages strategically.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital expenditure (CAPEX) and long payback periods limit new equipment investments | -0.8% | ASEAN (Vietnam, Thailand, Indonesia); tier-2 cities in China and India | Short term (≤ 2 years) |

| Skilled labor shortages across ASEAN hinder machining center utilization | -0.6% | Vietnam, Thailand, Indonesia, Philippines; spillover to Taiwan precision clusters | Medium term (2-4 years) |

| Retrofit preference over new machine purchases in Japan slows market growth | -0.5% | Japan (concentrated in SME job shops and tier-2 automotive suppliers) | Long term (≥ 4 years) |

| Semiconductor capex volatility disrupts machining equipment demand cycles | -0.4% | South Korea, Taiwan, China (memory fabs); Japan (equipment suppliers) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure (CAPEX) and Long Payback Periods Limit New Equipment Investments

A mid-range five-axis machining center can cost up to USD 800,000, while total ownership over five years often exceeds USD 1.2 million, including installation and tooling. Small firms in Vietnam and Thailand run on net margins below 8% and struggle to secure bank financing without state co-investment. Machine builders now push modular designs so buyers can start with a three-axis frame and bolt on rotary tables later, spreading cash outlay across several years. Leasing and pay-per-spindle-hour models are emerging in India and Indonesia, lowering barriers yet creating dependence on vendor uptime guarantees. Until financing terms ease, this restraint will weigh on the Asia-Pacific machining centers market, especially among tier-2 suppliers.

Skilled Labor Shortages Across ASEAN Hinder Machining Center Utilization

A profound skilled-labor gap continues to challenge industrial expansion across ASEAN economies, with CNC programmers among the most scarce trades. In Vietnam, current graduation rates from vocational schools fall drastically short of the government's massive enrollment targets aimed at meeting the nation's expanding industrial needs. Taiwan’s precision hub reports night shifts running at just 60% capacity because qualified staff are unavailable, even as new machines arrive on the floor. Thailand’s Smart Technician scheme will train 5,000 machinists by 2028, yet many graduates quickly leave for higher wages in Singapore and Japan. The shortage accelerates automation adoption, but without seasoned operators to program and maintain equipment, utilization rates remain below their potential in the Asia-Pacific machining centers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Vertical Platforms Anchor High-Volume Output

Vertical machining centers accounted for 38% of the Asia-Pacific machining centers market share in 2025 because they cut common prismatic parts such as engine blocks and mold bases at the lowest cost per spindle hour. Widespread dealer support across China, India, and Thailand keeps maintenance costs low and lets job shops add capacity quickly. Orders from consumer-electronics suppliers in Vietnam and Malaysia also favor vertical formats that fit tight floor plans and evacuate chips by gravity, preserving surface finish on aluminum housings. The Asia-Pacific machining centers market gains additional pull from Thailand’s 47 electronics projects, many of which specify high-speed VMC cells for connector tooling.

The Asia-Pacific machining centers market size for multi-tasking machining centers is projected to expand at a 6.20% CAGR between 2026 and 2031 as buyers consolidate milling and turning to save floor space. DMG Mori’s NTX series, ACCUWAY turn-mill lines, and Tongtai’s three-turret platform enable aerospace and medical shops to finish complex parts in a single setup, reducing work-in-process by up to 40%. These machines demand operators fluent in both G-code families, which is scarce across ASEAN, so builders bundle simulation software and remote support to speed adoption. As automotive suppliers retool for electric-vehicle battery trays, they increasingly specify multi-tasking capability to combine roughing, finishing, and probing on the same platform, reinforcing the growth trajectory.

By Axis Configuration: Three-Axis Remains the Workhorse

Three-axis systems held 46% of the Asia-Pacific machining centers market share in 2025 because they achieve tolerances acceptable for most steel and aluminum parts while keeping programming simple. Tier-2 automotive and appliance vendors rely on these machines to meet short delivery windows with minimal operator training. Chinese and Indian refurbishers also supply used three-axis units at 60% of new-machine prices, further extending their footprint.

Five-axis platforms are advancing at a 6.80% CAGR through 2031, reflecting demand for turbine blades, aerospace brackets, and electric-vehicle motor housings that require simultaneous contouring. Yumoto Denki’s 32-pallet automated cell now runs five-axis machines 18 hours unattended, proving the productivity boost achievable with advanced setups. Export controls on sub-3-micron accuracy units from Japan reinforce regional sourcing, concentrating technical support and training in Japan, South Korea, and Taiwan.[3]Ministry of Economy, Trade and Industry, Government of Japan, “Security Export Control,” meti.go.jp

By Spindle Orientation: Vertical Heads Dominate, Multi-Spindle Gains Speed

Vertical spindles accounted for 54% of total demand in 2025 because gravity-assisted chip flow keeps pockets clear and allows compact machines to fit densely packed lines. Electronics and medical-device firms favor this format when cutting thin aluminum or titanium parts that cannot tolerate recutting chips. The Asia-Pacific machining centers market benefits from Brother’s SPEEDIO family, which offers 27,000 RPM spindles and rapid tool change for smartphone housings and orthopedic screws.

Multi-spindle configurations are forecast to grow at a 6.50% CAGR during 2026-2031 as contract manufacturers pursue shorter cycle times and 24-hour lights-out operations. Automotive transmission plants in China now deploy horizontal multi-spindle cells with pallet pools, achieving Overall Equipment Effectiveness (OEE) above 85% and trimming unit costs for cast-iron housings. The Asia-Pacific machining centers market size tied to these high-output lines rises as suppliers integrate load-balancing software that equalizes tool wear across spindles. Although fixtures are more complex, savings in floor space and labor offset the upfront engineering expense within two years for high-volume contracts.

By Structure Type: Column Frames Hold Ground While Gantry Machines Stretch Boundaries

Column-type frames captured 41% of the Asia-Pacific machining center market share in 2025 because they offer high rigidity within a small footprint, making them suitable for parts up to 1 meter cubed. Thousands of small and medium enterprises across India and Indonesia install these machines inside standard industrial units that lack reinforced floors or overhead cranes. Widespread use of common replacement parts such as ball screws, guides, and spindle cartridges keeps downtime low and encourages repeat purchases.

Gantry types are set to expand at a 6.10% CAGR through 2031 as wind-turbine hubs, aircraft spars, and composite molds exceed the working envelope of column designs. Okuma’s gantry line spans up to 6 meters of X-travel, enabling aerospace primes in Japan and Australia to finish an entire wing spar in a single setup, reducing alignment effort and improving geometric accuracy. The Asia-Pacific machining centers market size linked to gantry sales is, therefore, most visible in regions where renewable-energy and aerospace programs overlap. Moving-table variants provide a middle ground for heavy castings, although slower acceleration limits adoption where takt time is critical.

By End-User Industry: Automotive Still Leads, Medical Devices Accelerate

Automotive applications accounted for 29% of the Asia-Pacific machining centers market size in 2025, reflecting long-standing demand for engine blocks, transmission cases, and suspension components. Even as electric vehicles drop many internal-combustion parts, factories still need precise milling for battery enclosures and reduction gears. Chinese battery-tray makers order five-axis centers to machine large aluminum castings in a single pass, keeping takt time below 2 minutes per tray.

Medical devices are the fastest-growing niche, set to climb at a 6.90% CAGR to 2031 as Indian incentives worth USD 410 million push local implant output. Kalyani Medicomp cut the lead time for cranial-plate production from six weeks to 10 days after installing Makino a51nx five-axis machines, demonstrating how lights-out machining supports mass customization. Sushrut Surgicals blends metal-injection molding for high-volume parts with CNC finishing for custom geometries, illustrating a hybrid path that still relies on precision mills. The Asia-Pacific machining centers market benefits from such diversification, helping cushion volatility in automotive demand.

Geography Analysis

China retained 49% of the Asia-Pacific machining centers market share in 2025, underpinned by more than 2 million factory robots and a robot density of 392 units per 10,000 workers, triple the global mean. The nation’s push toward lights-out production is evident at Xiaomi’s Changping complex, which runs 81% of its operations automatically and turns out 10 million smartphones annually on vertically integrated machining lines. India is tracking a 7.20% CAGR to 2031, the region’s fastest pace, helped by USD 410 million in Production-Linked Incentives that channel orders for five-axis cells into domestic implant, electronics, and battery-tray plants. The Asia-Pacific machining centers market in India is growing further as Tsugami’s new Chennai assembly plant aims to reach 500 units per year by 2027 and offers localized service that halves lead times. Together, China’s automation surge and India’s capacity build-out anchor demand momentum for the wider region.

Japan’s domestic buyers kept orders flat in early 2026, even though total bookings jumped 25.3% year-on-year to JPY 145.6 billion (USD 0.91 billion), because the growth stemmed from overseas customers, mainly Thailand and Vietnam, rather than local replacement cycles. Many Japanese shops retrofit 15-year-old units at 50-65% of the cost of a new machine, reflecting a risk-averse culture that limits new installations but sustains a large aftermarket for controls and spindles. South Korea earmarked USD 336 million for smart-factory subsidies in 2025, and its new “AI Track” scheme, launching in 2026, will co-fund edge-computing nodes on legacy equipment, accelerating data-driven upgrades. Australia’s emerging space sector, backed by the national agency, has begun sourcing precision components from Melbourne and Adelaide, spurring early demand for gantry five-axis machines capable of finishing an entire wing spar in a single setup.

Rest-of-Asia-Pacific, including Vietnam, Thailand, Indonesia, Malaysia, and smaller economies, absorbed a wave of electronics reshoring, with Thailand alone approving 47 projects worth USD 2.5 billion in 2025 that specify high-speed vertical machining centers for connector tooling. “Smart Technician” initiative will train 5,000 machinists by 2028 but faces attrition as graduates migrate to higher-paying roles in Singapore and Japan, reinforcing a regional skills gap. Electronics reshoring and EV supply-chain expansion give the Asia-Pacific machining centers market size a diversified geographic foundation that tempers single-country risk.[4]Australian Space Agency, “Local Supply Chain Roadmap,” space.gov.au

Competitive Landscape

The Asia-Pacific machining centers market exhibits moderate concentration. Leading suppliers anchor the Asia-Pacific machining centers market through broad dealer networks and tiered product lines that range from entry-level three-axis frames to premium five-axis, multi-tasking cells. Japanese and South Korean incumbents Yamazaki Mazak, DMG Mori, Okuma, Makino, DN Solutions, and Hyundai WIA retain much of their historical share because long-cycle aerospace, automotive, and medical contracts favor proven platforms that come with field service in every major manufacturing hub. Chinese challengers such as Dalian Machine Tool, Shenyang Machine Tool, and Guangdong Taikan address the price-sensitive tier-2 buyer with machines that cost 30-40% less and arrive with plug-and-play robot loaders that shorten installation time. The resulting two-tier structure keeps average selling prices stable at the top end while intensifying discount pressure in the value segment.

Since 2025, competitive dynamics in the industry have been shaped by acquisitions, capacity expansion, and tighter supply chain control. DN Solutions bought Germany’s Heller Machining for USD 176 million in January 2026 to gain horizontal-boring expertise and expand its European footprint, while SMEC absorbed Hyundai WIA’s machine-tool division for USD 249.5 million the following month, securing castings and heat-treatment capacity in-house. Japan’s Ministry of Economy, Trade and Industry blocked MBK Partners’ USD 1.6 billion bid for Makino on national-security grounds, signaling tighter scrutiny of foreign investment in precision equipment. DMG Mori’s “MX Machining Transformation” program released 18 new machines and six digital applications in 2025, packaging predictive-maintenance analytics with each sale to lock in recurring software revenue.

Technology differentiation now revolves around connectivity and hybrid processes. Premium builders bundle OPC UA-ready controllers, edge-computing boxes, and ISO 16739-compliant digital twin files so factories can feed real-time data into manufacturing execution systems. Value-oriented suppliers counter with modular frames that accept add-on rotary axes, probing, or pallet pools when cash flow allows, letting customers delay part of the capital outlay. Fanuc’s March 2026 partnership with Ty Robotics integrates cobots directly into its CNC kernel, opening a path for small job shops to automate loading without safety cages. Mazak expanded its Kentucky iSmart Factory in November 2025 and swapped CO₂ lasers for fiber units, trimming energy use by 67% while raising throughput on five-axis lines. Intensifying rivalry in automation, software, and service keeps switching costs high and sustains moderate concentration despite new entrants.

Asia-Pacific Machining Centers Industry Leaders

Yamazaki Mazak Corporation

DMG Mori Co., Ltd.

Okuma Corporation

Makino Milling Machine Co., Ltd.

Doosan Machine Tools Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Japan’s Ministry of Economy, Trade and Industry blocked MBK Partners’ USD 1.6 billion acquisition of Makino Milling Machine, citing national-security concerns. By halting the Makino acquisition, Japan has firmly prioritized national security, chilling foreign private-equity consolidation of advanced machining technologies in the Asia-Pacific region.

- April 2026: FANUC Corporation, an industrial automation company, introduced its next-generation numerical control system, the FS500i-A CNC. This system is designed for high-precision, complex machining environments.

- February 2026: Okuma Corporation, a machine tool manufacturer, announced a JPY 14 billion (USD 87.94 million) investment to redevelop its Konan Plant in Aichi Prefecture, Japan. The move transforms the site into a "one-stop" production center for automation systems.

- January 2026: DN Solutions, a manufacturer of CNC machine tools, completed the USD 176 million purchase of Heller Machining and signed an MoU to build a plant in India. By acquiring Heller’s premium five-axis technology and expanding production into India, DN Solutions significantly elevates its global competitive stance against top-tier European and Japanese incumbents in both advanced aerospace and high-growth emerging markets.

Asia-Pacific Machining Centers Market Report Scope

| Horizontal Machining Centers (HMC) |

| Vertical Machining Centers (VMC) |

| Universal/5-Axis Machining Centers |

| Multi-Tasking Machining Centers (MTM) |

| Others (Gantry/Bridge-Type Centers, Turn-Mill Centers) |

| 3-Axis |

| 4-Axis |

| 5-Axis & Above |

| Horizontal |

| Vertical |

| Multi-spindle |

| Column-Type |

| Gantry-Type |

| Moving-Table |

| Automotive |

| Aerospace & Defense |

| Energy (Oil-Gas, Renewables) |

| Medical Devices |

| Mold and Die Manufacturing |

| Others (General Manufacturing, Job Shops, Electronics, etc.) |

| China |

| Japan |

| India |

| Australia |

| South Korea |

| Rest of Asia-Pacific |

| By Machine Type | Horizontal Machining Centers (HMC) |

| Vertical Machining Centers (VMC) | |

| Universal/5-Axis Machining Centers | |

| Multi-Tasking Machining Centers (MTM) | |

| Others (Gantry/Bridge-Type Centers, Turn-Mill Centers) | |

| By Axis Configuration | 3-Axis |

| 4-Axis | |

| 5-Axis & Above | |

| By Spindle Orientation | Horizontal |

| Vertical | |

| Multi-spindle | |

| By Structure Type | Column-Type |

| Gantry-Type | |

| Moving-Table | |

| By End-User Industry | Automotive |

| Aerospace & Defense | |

| Energy (Oil-Gas, Renewables) | |

| Medical Devices | |

| Mold and Die Manufacturing | |

| Others (General Manufacturing, Job Shops, Electronics, etc.) | |

| By Country | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia-Pacific machining centers market?

The market stands at USD 12.79 billion in 2026 and is projected to reach USD 15.70 billion by 2031, growing at a 4.19% CAGR over 2026-2031.

Which country is the fastest-growing buyer of machining centers in Asia-Pacific?

India leads with a forecast 7.20% CAGR to 2031, supported by government incentives for medical devices and electronics reshoring.

What machine type dominates current installations?

Vertical machining centers hold 38% of 2025 revenue because they provide affordable, high-volume cutting capacity.

Why are five-axis & above machines gaining popularity?

Complex EV battery trays, aerospace blades, and medical implants need simultaneous multi-face cuts, driving five-axis & above demand at 6.80% CAGR through 2031.

How will semiconductor spending influence machining center orders?

SEMI projects fab-equipment outlays of USD 133 billion in 2026, which should lift orders for ultra-precision machining of vacuum chambers despite cyclical risk.

What restrains new machine purchases among ASEAN SMEs?

High capital costs that exceed USD 1.2 million over five years force many small shops to favor retrofits or lease-per-spindle-hour models.

Page last updated on: