Asia-Pacific Graphics Processing Unit (GPU) Liquid Cooling Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

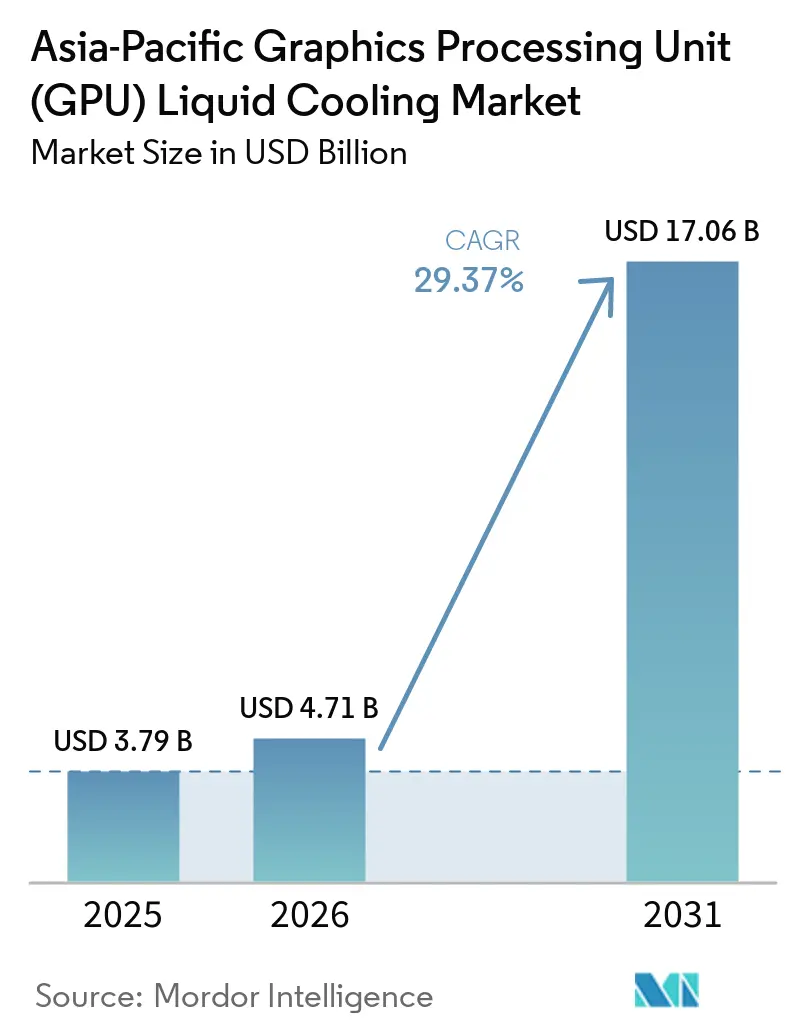

| Base Year Market Size (2025) | USD 3.79 Billion |

| Market Size (2026) | USD 4.71 Billion |

| Market Size (2031) | USD 17.06 Billion |

| Growth Rate (2026 - 2031) | 29.37% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Graphics Processing Unit (GPU) Liquid Cooling Market Analysis by Mordor Intelligence

The Asia-Pacific graphics processing unit (GPU) liquid cooling market size is expected to grow from USD 3.79 billion in 2025 to USD 4.71 billion in 2026 and is forecast to reach USD 17.06 billion by 2031 at 29.37% CAGR over 2026-2031. Rising rack-level densities above 100 kilowatts, NVIDIA GB200 deployments exceeding 1,200 watts per accelerator, and energy-efficiency mandates that target PUE 1.3 or lower are moving liquid cooling from pilot projects to baseline specification. Single-phase direct-to-chip systems dominate early rollouts, yet two-phase immersion designs are scaling on the back of mechanical-equipment majors pairing with specialist vendors to address chips that operate beyond the 1,000-watt threshold. Colocation operators are embedding coolant distribution units during shell-and-core construction so enterprises can lease liquid-ready capacity without handling fluids on-site. China commands nearly one-half of regional revenue, but India, Southeast Asia, and South Korea are recording the fastest growth as land constraints and power-allocation policies reward dense racks that minimize cooling overhead.

Key Report Takeaways

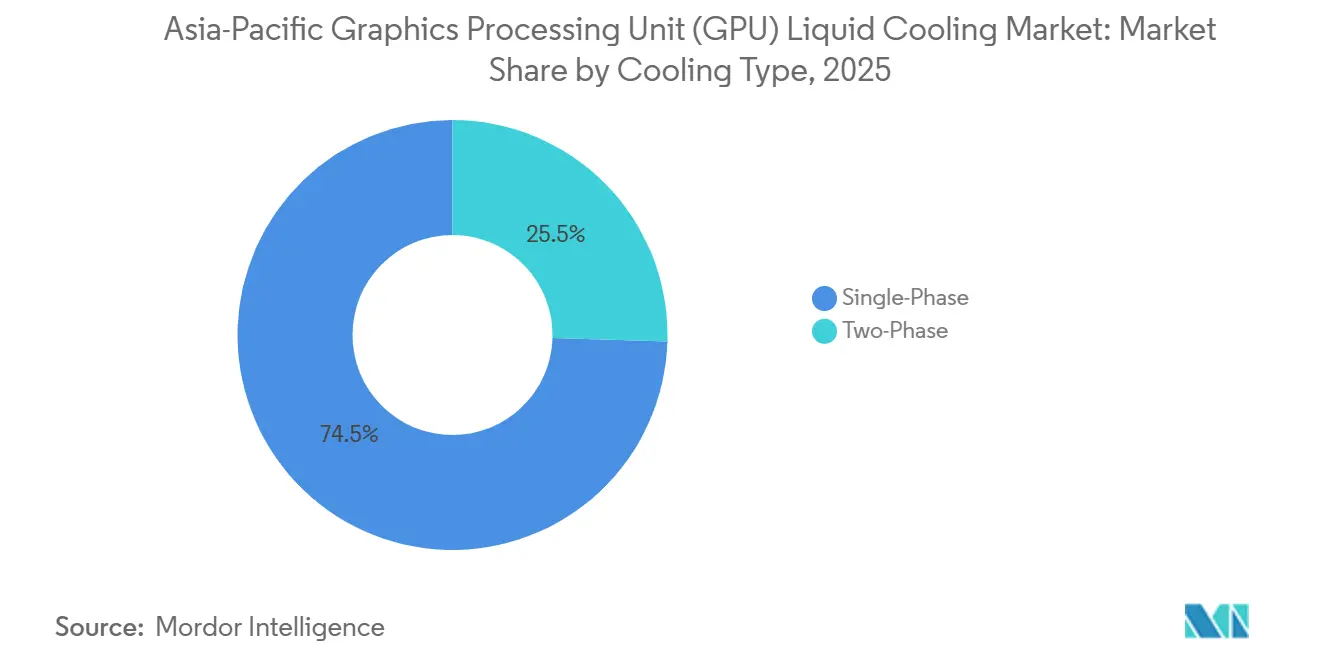

- By cooling type, single-phase liquid cooling led with 74.51% of the Asia-Pacific GPU liquid cooling market share in 2025, while two-phase immersion systems are advancing at a 32.17% CAGR through 2031.

- By cooling level, component-level solutions captured 55.72% of the Asia-Pacific GPU liquid cooling market size in 2025, and rack-level architectures are expanding at 30.96% CAGR over 2026-2031.

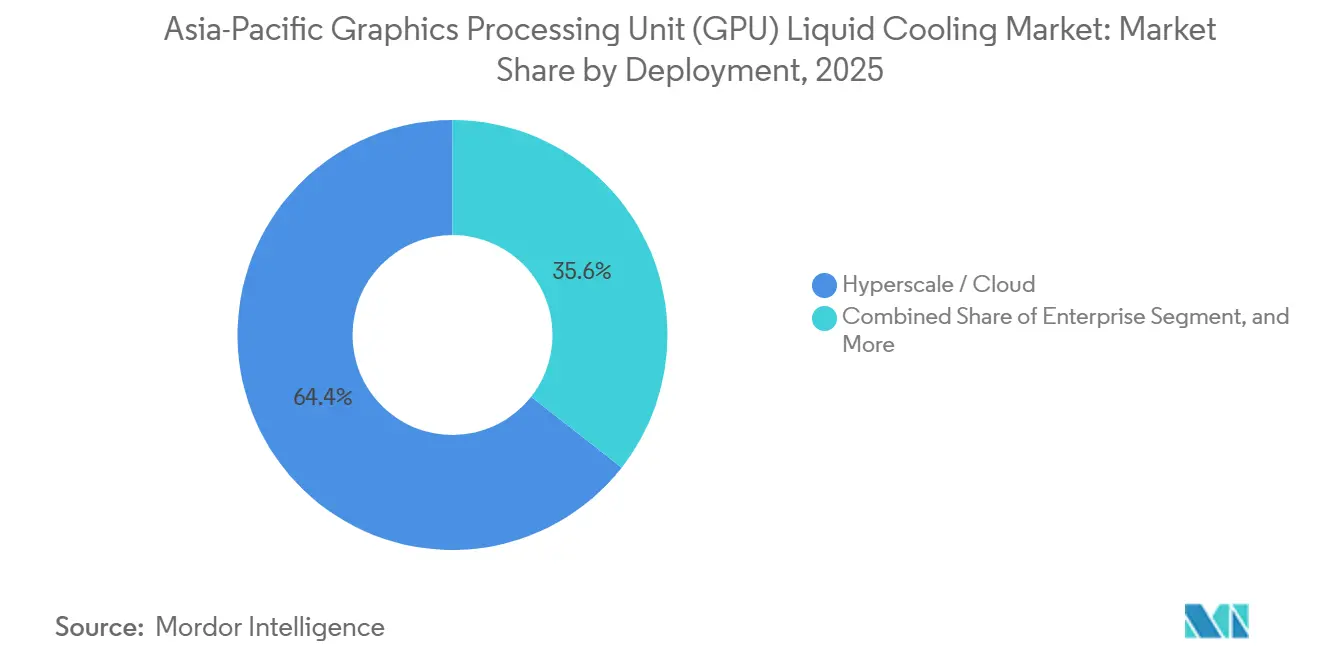

- By deployment, hyperscale and cloud operators held 64.41% revenue share in 2025, whereas enterprise rollouts are projected to log a 32.04% CAGR to 2031.

- By GPU power density, the 300-watt-to-700-watt class accounted for 53.44% of the Asia-Pacific GPU liquid cooling market share in 2025, and the above-700-watt segment is set to grow at a 30.04% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Graphics Processing Unit (GPU) Liquid Cooling Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstream AI-Led Hyperscale Expansions Drive Liquid-Cooling Adoption | +8.5% | China, Japan, South Korea, Singapore, spill-over to India and Southeast Asia | Medium term (2–4 years) |

| Mandatory Energy-Efficiency Regulations Across East and South-East Asia | +6.2% | Japan, China, South Korea, Singapore, emerging influence in India and Thailand | Long term (≥ 4 years) |

| Rapid Growth of Edge-AI Inference Nodes in 5G Networks | +4.8% | India, Thailand, Vietnam, Indonesia, China | Medium term (2–4 years) |

| Data-Center Land Constraints in Tier-1 Cities Boost Rack-Level Density | +3.9% | Tokyo, Seoul, Singapore, Hong Kong, secondary impact in Mumbai and Bangkok | Short term (≤ 2 years) |

| Availability of Turn-Key Liquid-Ready Colocation Capacity | +2.7% | Singapore, Malaysia, Japan, Australia, expanding to India and Thailand | Short term (≤ 2 years) |

| Advancements in Coolant Chemistry Enabling Non-Conductive Two-Phase Designs | +2.1% | Global with early adoption in Japan, South Korea, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mainstream AI-Led Hyperscale Expansions Drive Liquid-Cooling Adoption

Alibaba, Samsung SDS, OpenAI, and Global Switch are commissioning facilities where racks surpass 100 kilowatts, and GPUs draw up to 1,200 watts, a regime that renders air cooling uneconomic. Alibaba’s Feitian platform already operates more than 100,000 GPUs in immersion tanks at PUE 1.09, cutting facility energy bills by roughly one-half. Samsung SDS broke ground on a 60 megawatt AI campus in Gumi in March 2026 that allocates KRW 427.3 billion (USD 320 million) to hybrid liquid infrastructure, underscoring long-term confidence in direct-to-chip systems.[1]Samsung Electronics, “Samsung SDS Gumi Megawatt Data Center Press Release,” samsung.com Global Switch Hong Kong added 30 megawatts of liquid-cooled capacity, while Nxera’s DC Tuas in Singapore installed 58 megawatts of warm-water loops for sovereign AI workloads. The Asia-Pacific GPU liquid cooling market, therefore, follows hyperscalers’ cadence: as model sizes inflate, cooling budgets shift from optimization to outright replacement of air systems.

Mandatory Energy-Efficiency Regulations Across East and South-East Asia

Japan’s Ministry of Economy, Trade, and Industry requires PUE 1.4 by 2030 and PUE 1.3 for new builds from 2029, effectively outlawing traditional chillers in humid climates.[2]Government of Japan, “Green Growth Strategy Through Achieving Carbon Neutrality,” meti.go.jp China’s energy labeling for chillers and its provincial power-quota regime likewise favor facilities that remove heat at the chip rather than at the room level.[3]Government of China, “Data Center Energy Labeling Rules,” gov.cn Lenovo’s Neptune operates at 45 °C inlets, letting operators reuse waste heat, bypass chillers that consume up to 40% of facility power, and meet emerging carbon budgets. Singapore’s Green Data Center Roadmap adds further pressure by tying new electricity allotments to demonstrated PUE improvements. Consequently, the Asia-Pacific GPU liquid cooling market benefits from a policy that makes efficiency a prerequisite for power and land access.

Rapid Growth of Edge-AI Inference Nodes in 5G Networks

Telecom carriers are embedding GPUs at thousands of 5G base stations to run latency-critical analytics, autonomous-vehicle coordination, and AR overlays. Cabinets no larger than street furniture must dissipate 5-10 kilowatts in ambient temperatures above 40 °C, a scenario solved by sealed liquid modules that tolerate intermittent grid power.[4]IEEE Staff, “Thermal Design for 5G Edge Cabinets,” ieee.org India added 38,231 edge GPUs in 2025 with direct-to-chip or adiabatic cooling, where water is scarce. ZutaCore and Submer now offer waterless two-phase packages that telcos in Thailand and Vietnam deploy to avoid condensation risk in tropical humidity. Edge proliferation diversifies the Asia-Pacific GPU liquid cooling market beyond hyperscale campuses and increases demand for standardized plug-and-play designs.

Data-Center Land Constraints in Tier-1 Cities Boost Rack-Level Density

Urban land costs often exceed USD 1,000 per square meter, pushing operators in Tokyo, Seoul, and Singapore to triple compute inside existing shells. Equinix’s SG6, due in Q1 2027, will spend USD 260 million on direct liquid cooling to support densities above 120 kilowatts per rack. STT GDC’s Johor campus offers 120 megawatts using rack-level coolant distribution that compresses floor area to one-third of air-cooled footprints. Macquarie Data Centers in Sydney installed immersion tanks to reach 130 kilowatt racks, sidestepping expensive land acquisition. Highland values, therefore, accelerate the adoption of rack-level systems within the Asia-Pacific GPU liquid cooling market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front Capex and Retrofit Complexity for Brownfield Facilities | -3.8% | Japan, Australia, South Korea, secondary impact in Singapore and India | Short term (≤ 2 years) |

| Limited Skilled Workforce for Liquid-Cooling O&M Across Emerging Markets | -3.2% | India, Thailand, Vietnam, Indonesia, rest of Asia-Pacific | Medium term (2–4 years) |

| Supply-Chain Bottlenecks in Precision Cold Plates and Quick Disconnects | -2.4% | Global focus in China, Japan, South Korea | Short term (≤ 2 years) |

| PFAS Regulatory Uncertainty for Two-Phase Dielectric Fluids | -1.9% | Japan, South Korea, Australia, scrutiny rising in China, India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Capex and Retrofit Complexity for Brownfield Facilities

Direct-to-chip retrofits cost USD 500-USD 800 per kilowatt, more than double air-cooling upgrades, and demand phased cutovers that must preserve uptime. Operators often need structural reinforcement for pipes, electrical upgrades for pumps, and revised fire suppression, stretching payback to three to five years and deterring sites with rack densities below 50 kilowatts. Custom engineering erodes economies of scale, so many legacy owners wait until thermal ceilings force a wholesale move rather than incremental retrofits.

Limited Skilled Workforce for Liquid-Cooling O&M Across Emerging Markets

Two-thirds of Asia-Pacific operators cite shortages of technicians who understand coolant chemistry and leak-detection protocols, with India’s Skills Shortage Index for AI roles at 47 and wages surpassing USD 1,000 per day for imported specialists.[5]CBRE, “Asia Pacific Data Center Talent Report,” cbre.com Itochu and Castrol created training academies in Japan in December 2025, yet coverage remains thin across Thailand, Vietnam, and Indonesia. Talent scarcity slows deployment velocity and raises operational risk, capping near-term growth of the Asia-Pacific GPU liquid cooling market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cooling Type: Two-Phase Designs Move Beyond Pilot Projects

Single-phase solutions accounted for 74.51% of the Asia-Pacific GPU liquid cooling market share in 2025, a position built on mature water loops that integrate with standard facility infrastructure. Lenovo Neptune and HPE ProLiant XD685 operate at 45 °C inlets, achieve a PUE of near 1.1, and provide a familiar maintenance model for staff already versed in chilled-water plants. Two-phase systems, although only 25.49% in 2025, are racing ahead at 32.17% CAGR as ZutaCore and Mitsubishi Heavy Industries prove rack-level partial PUE near 1.01 and remove facility water from the white space.

Chips such as the NVIDIA GB200 and AMD MI300X are pushing past the 1,000-watt mark. At this threshold, water's thermal headroom becomes limited, and the required flow rates demand significant pump power, making traditional cooling methods less efficient. This has led to increased interest in alternative cooling solutions, particularly two-phase cooling systems. Carrier's investment in ZutaCore, coupled with Trane's acquisition of LiquidStack, underscores a pivotal shift in the industry. These strategic moves by HVAC behemoths highlight their confidence in two-phase cooling roadmaps, which offer enhanced efficiency and scalability. As a result, the Asia-Pacific GPU liquid cooling market is expected to pivot towards dielectric fluids by 2028, marking a significant transformation in cooling technologies.

By Cooling Level: Rack-Level Architectures Attract Colocation Providers

In 2025, component-level cold plates accounted for 55.72% of the Asia-Pacific GPU liquid cooling market, aligning with hyperscalers' focus on optimizing individual chips. These cold plates are designed to provide per-chip cooling, which is critical for managing the high heat output of GPUs in hyperscale environments. Supermicro's DLC-2, a prominent solution in this space, boasts the ability to extract 92% of server heat. This capability allows operators to seamlessly integrate GPU and CPU nodes without requiring extensive rack modifications. On the other hand, colocation operators are increasingly adopting rack-level coolant distribution units (CDUs) to streamline heat removal processes. These units treat heat removal as a shared service, offering a centralized approach to cooling that simplifies operations and enhances efficiency.

Rack-level solutions, such as ZutaCore’s 2 megawatt end-of-row CDU and CoolIT’s CHx500 stack, are becoming integral to retrofits by major players like Equinix and STT GDC. These solutions enable landlords to maintain control over critical aspects such as metering, maintenance, and service level agreements (SLAs). With rack-level offerings growing at a 31.60% CAGR, the market is witnessing a significant shift in cooling strategies. Tenants are moving away from individually plumbing racks and are instead subscribing to cooling as a service. This model aligns with the market's transition toward multi-tenant AI clusters, which demand scalable and efficient cooling solutions to support their high-performance computing needs.

By Deployment: Enterprise Acceleration Follows Turn-Key Capacity

Hyperscale and cloud groups retained 64.41% share in 2025, leveraging standard designs across campuses and securing volume discounts on cold plates and manifolds. These groups benefit from economies of scale, ensuring cost efficiency and streamlined operations. Google’s Chonburi campus incorporated liquid-ready bays for TPUs, showcasing its readiness for advanced cooling technologies. Meanwhile, Alibaba and Samsung committed to immersion designs during the shell-stage construction of their facilities. This proactive approach helps mitigate risks associated with coolant-supply volatility, ensuring uninterrupted operations. Such strategies highlight the dominance of hyperscalers in the Asia-Pacific GPU liquid cooling market.

Enterprise demand is climbing at a 32.04% CAGR, driven by the increasing adoption of advanced cooling solutions. Colocation landlords, such as YTL Power and GreenSquareDC, are pre-installing pipework and CDUs, simplifying the integration process for tenants. This approach allows tenants to easily plug in rear-door heat exchangers or cold plates, reducing setup complexities. Vertiv’s collaboration with Netweb offers racks rated at 200 kilowatts, catering to the high-performance needs of Indian banks and pharmaceutical firms. These developments illustrate how the market is lowering entry barriers by transferring the engineering burden to facilities. As a result, enterprises can focus on their core operations while benefiting from efficient cooling solutions.

By GPU Power Density: Above-700-Watt Class Becomes the Growth Engine

GPUs in the 300-watt-to-700-watt band represented 53.44% of the Asia-Pacific GPU liquid cooling market size in 2025 because A100 and H100 accelerators dominate installed fleets. Lenovo Neptune handles these thermals with warm water, enabling operators to defer chiller upgrades. Yet next-gen silicon pushes thermal design above 1,000 watts per device, and that segment is expanding at 31.40% CAGR. An eight-card B200 server draws up to 16 kilowatts, making liquid mandatory. Compal and ZutaCore showcased a two-phase chassis at Yotta 2025 with a rack-level PUE near 1.04, confirming that dielectric evaporation will carry the heaviest loads.

As accelerator roadmaps target 1,500 watts, the market is poised to expand its share in the above-700-watt segment. This growth is expected to drive significant advancements in cooling technologies to meet the increasing thermal management demands of high-performance GPUs. The market is likely to witness heightened supply-chain investments in precision vapor chambers, which offer efficient heat dissipation solutions. Additionally, the shift toward non-PFAS coolants, driven by environmental regulations and sustainability goals, will further shape the market dynamics. These developments underscore the region's pivotal role in addressing the evolving needs of the GPU liquid cooling industry.

Geography Analysis

China anchored nearly half of the Asia-Pacific GPU liquid cooling market size in 2025, powered by Alibaba’s Feitian immersion clusters at PUE 1.09 and provincial quotas that prioritize energy-efficient facilities. Shenzhen’s Pengcheng Cloud Brain adopted immersion cooling in Q2 2026, while Guian Phase II reached PUE 1.12 in a subtropical climate, validating liquid adoption as a route to regulatory power allocations. Cold plates still hold 65% share, but immersion tanks are scaling as operators chase PUE below 1.2 to obtain preferential tariffs and grid connections.

Japan follows due to METI rules that cap PUE at 1.3 for new builds starting in 2029. Fujitsu, NTT, and Rapidus are already tapping liquid-ready colocation space to satisfy semiconductor R&D loads, and Mitsubishi Heavy Industries is piloting dielectric fluids with 94% cooling-power reduction. South Korea’s Samsung SDS committed KRW 427.3 billion (USD 320 million) for a 60 megawatt hybrid liquid campus in Gumi, while STT GDC opened Seoul capacity in June 2026, indicating that domestic cloud and AI training need liquid as a competitive baseline.

India is the fastest-growing market, supported by long-term tax holidays and a robust data-center pipeline extending through the next decade. Vertiv and Netweb are rolling out 200 kilowatt racks, Schneider Electric opened a Motivair plant in Bengaluru, and Submer teamed with Anant Raj for immersion builds. Southeast Asia’s momentum comes from land-constrained Singapore, Malaysia’s Johor corridor, and Thailand’s STT Bangkok 1, all of which market themselves as sovereign-AI hubs needing densified racks. Australia rounds out the region with Macquarie Data Centres and ResetData promoting immersion-cooled liquid as a service, positioning the broader market for balanced growth across mature and emerging economies.

Competitive Landscape

Competition balances HVAC incumbents against specialist disruptors; the market is moderately consolidated. Vertiv, Schneider Electric, and Carrier still profit from chillers, yet their strategic statements highlight rack-level and component-level portfolios after Carrier invested in ZutaCore and Trane bought LiquidStack. Lenovo, HPE, and Supermicro integrate cold plates at the server level to preserve margin as GPU-heavy configurations outpace commodity x86 boxes. Iceotope’s 200-plus patents make it a licensor of precision immersion designs, an approach that lets hyperscalers adopt sealed servers without maintaining their own fluid R&D.

Colocation landlords such as Equinix, STT GDC, and YTL Power use turnkey liquid ecosystems to differentiate on SLA and density, absorbing the complexity customers want to avoid. NTT’s partnership with Rapidus shows how third-party providers can host semiconductor workloads that need tooling-compatible liquid systems. Meanwhile, edge-AI segments invite micro-module specialists like Firmus and ResetData to supply sealed 5-10 kilowatt cabinets deployable at base-station sites.

Supply discipline is tightening; Asetek’s USD 35 million order book through 2027 and CoolIT’s new CDU line demonstrate that long-term contracts are now standard to secure components whose lead times stretch to 12 weeks. Technology leadership therefore rests on coolant innovation, pump-energy efficiency, and compatibility with NVIDIA DGX reference architectures, all of which influence purchasing in the Asia-Pacific GPU liquid cooling market.

Asia-Pacific Graphics Processing Unit (GPU) Liquid Cooling Industry Leaders

CoolIT Systems Inc.

Asetek A/S

Vertiv Holdings Co.

Schneider Electric SE

Huawei Technologies Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: NTT provided liquid-cooled capacity to Rapidus for semiconductor R&D workloads in Japan, allowing chip testing at production power without dedicated infrastructure.

- April 2026: Iceotope surpassed 200 granted and pending patents covering chassis, dielectric fluids, and rack-scale thermal management.

- March 2026: ZutaCore launched 1.2 megawatt and 2.0 megawatt waterless end-of-row CDUs using low-GWP dielectric fluid.

- March 2026: In Gumi, Samsung SDS constructed a 60-megawatt AI data center featuring hybrid liquid cooling, scheduled for Mar 2029 completion.

Asia-Pacific Graphics Processing Unit (GPU) Liquid Cooling Market Report Scope

The Asia-Pacific Graphics Processing Unit (GPU) Liquid Cooling Market covers cooling systems and services that remove heat from GPUs using liquid-based methods rather than traditional air cooling. It includes direct-to-chip cooling, cold plates, immersion cooling, coolant distribution units, pumps, heat exchangers, and related thermal management solutions. Demand is driven by the need for better thermal efficiency, lower energy use, quieter operation, and support for high-performance GPU clusters.

The Asia-Pacific Graphics Processing Unit (GPU) Liquid Cooling Market Report is Segmented by Cooling Type (Single-Phase Liquid Cooling, and Two-Phase Liquid Cooling), Cooling Level (Component-Level Cooling, and Server/Rack-Level Cooling), Deployment (Hyperscale/Cloud, Enterprise, Government and Research HPC, and Edge AI), GPU Power Density (Below 300W, 300W-700W, and Above 700W), and Geography (China, Japan, South Korea, India, Southeast Asia, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| Single-Phase Liquid Cooling |

| Two-Phase Liquid Cooling |

| Component-Level Cooling |

| Server / Rack-Level Cooling |

| Hyperscale / Cloud |

| Enterprise |

| Government and Research (HPC) |

| Edge AI |

| Below 300W |

| 300W - 700W |

| Above 700W |

| China |

| Japan |

| South Korea |

| India |

| Southeast Asia |

| Rest of Asia-Pacific |

| By Cooling Type | Single-Phase Liquid Cooling |

| Two-Phase Liquid Cooling | |

| By Cooling Level | Component-Level Cooling |

| Server / Rack-Level Cooling | |

| By Deployment | Hyperscale / Cloud |

| Enterprise | |

| Government and Research (HPC) | |

| Edge AI | |

| By GPU Power Density | Below 300W |

| 300W - 700W | |

| Above 700W | |

| By Geography | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current Asia-Pacific GPU liquid cooling market size and how fast is it growing?

The Asia-Pacific GPU liquid cooling market size stands at USD 4.71 billion in 2026 and is forecast to reach USD 17.06 billion by 2031, expanding at a 29.37% CAGR according to Mordor Intelligence.

Which cooling type dominates installations across the region?

Single-phase direct-to-chip systems lead with 74.51% market share in 2025, favored for their mature water loops and facility compatibility.

Which segment shows the fastest growth trajectory?

Two-phase liquid cooling is the fastest growing, projected at 32.17% CAGR, as chips surpass 1,000 watts and operators seek dielectric fluids that remove heat at the source.

Why are colocation providers investing in rack-level liquid cooling?

Rack-level CDUs let colocation landlords meter, maintain, and guarantee thermal SLAs across multi-tenant AI clusters, removing plumbing duties from enterprise customers and driving a 30.96% CAGR for the segment.

Which country is expected to record the strongest growth through 2031?

India is forecast to expand on the back of tax holidays, a USD 70-USD 100 billion data-center pipeline, and turnkey liquid-ready capacity from local and global providers.

How are regulations influencing technology choices?

Energy-efficiency mandates such as Japan's PUE 1.3 requirement for new builds from 2029 and Chinas chiller labeling policies push operators toward liquid architectures that can meet strict PUE thresholds without large chillers.

Page last updated on: