Asia-Pacific ESIM Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

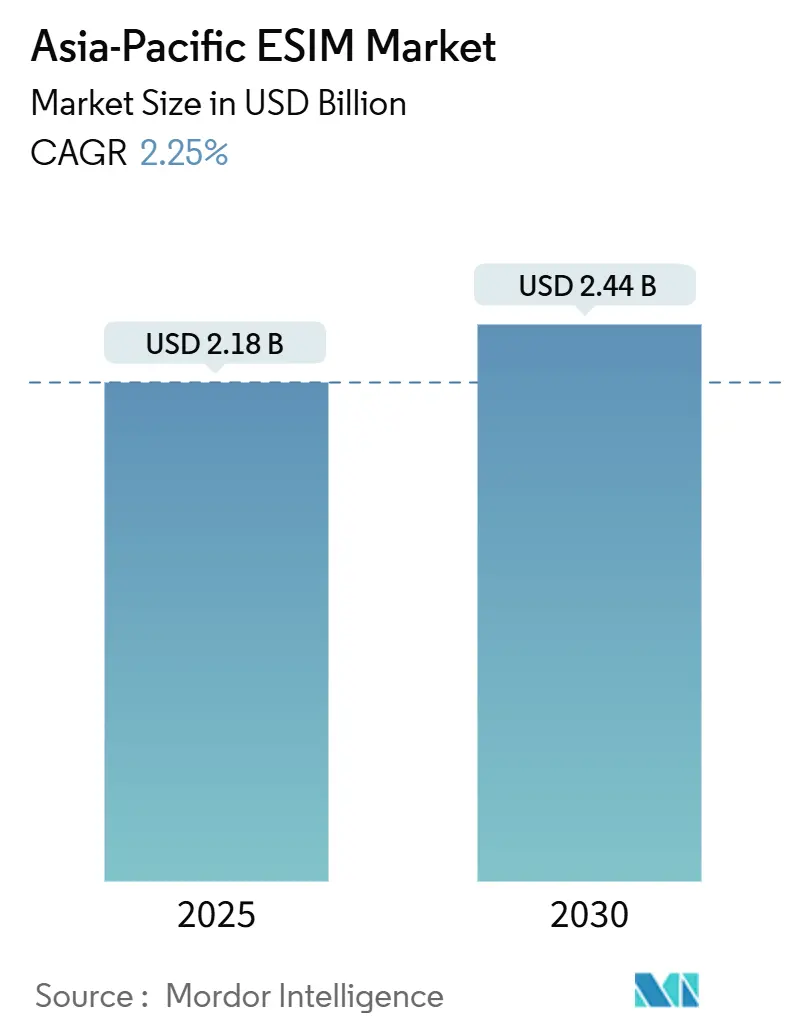

| Market Size (2025) | USD 2.18 Billion |

| Market Size (2030) | USD 2.44 Billion |

| Growth Rate (2025 - 2030) | 2.25% CAGR |

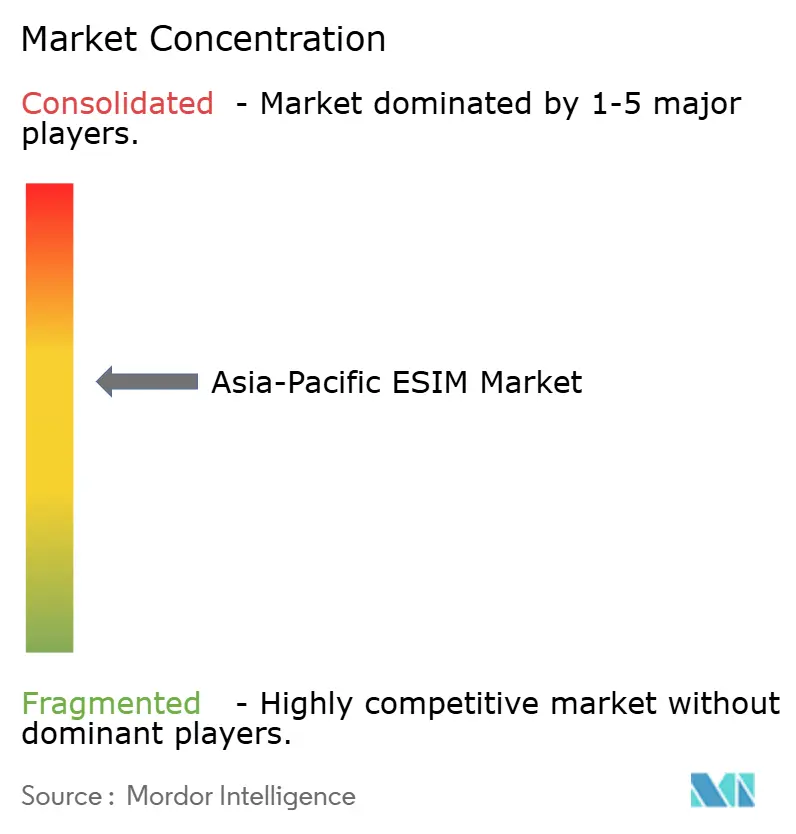

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific ESIM Market Analysis by Mordor Intelligence

The Asia-Pacific eSIM Market size is estimated at USD 2.18 billion in 2025, and is expected to reach USD 2.44 billion by 2030, at a CAGR of 2.25% during the forecast period (2025-2030). In terms of shipment volume, the market is expected to grow from 220.08 million units in 2025 to 260.75 million units by 2030, at a CAGR of 3.45% during the forecast period (2025-2030). Modest top-line expansion masks sharp differences across countries, with Japan growing fastest and China remaining the largest contributor after lifting long-standing limits on consumer smartphone eSIM. Operator investments in 5G standalone cores, private-network build-outs in factories, and a steady pivot from plastic SIM inventory to remote provisioning support growth even as fragmented certification regimes and higher hardware bills of material constrain momentum. Vendor strategies focus on integrating secure elements into application processors, expanding standards compliance, and targeting high-value verticals, including connected vehicles and industrial automation. M2M and IoT modules outpace smartphones in percentage terms, while software-based subscription management platforms post software-like margins once scale is achieved.

Key Report Takeaways

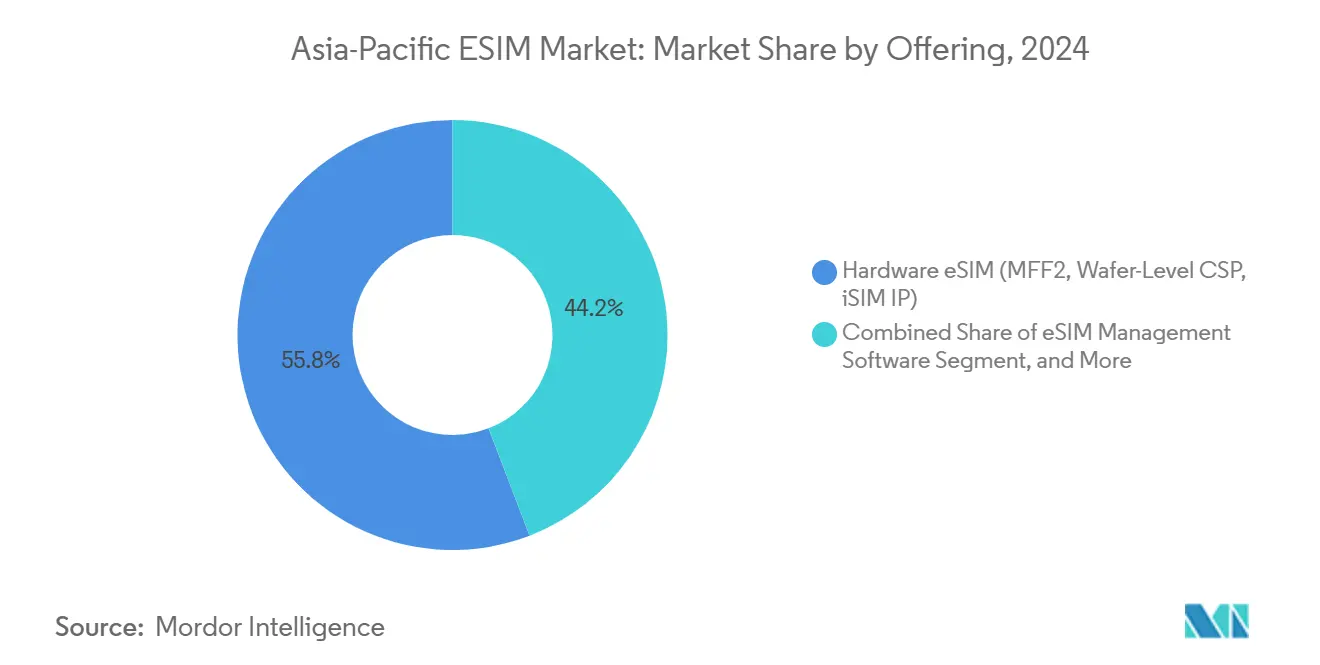

- By offering, the hardware eSIM (MFF2, Wafer-Level CSP, iSIM IP) segment led in the Asia-Pacific eSIM market with a 55.84% share in 2024, whereas remote SIM provisioning services are projected to expand at a 6.40% CAGR through 2030.

- By device type, smartphones and feature phones accounted for 65.33% of the Asia-Pacific eSIM market in 2024, whereas M2M/IoT modules are projected to grow at an 8.99% CAGR through 2030.

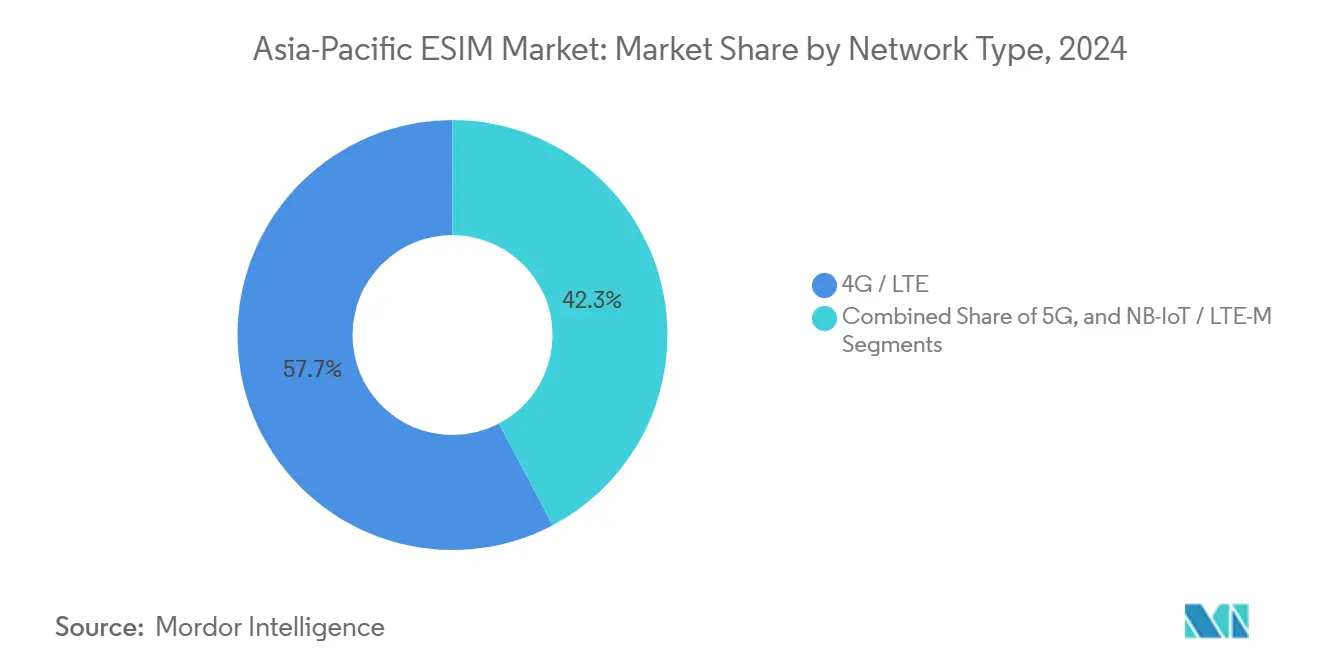

- By network type, 4G/LTE retained 57.71% share of the Asia-Pacific eSIM market in 2024, while 5G is forecast to surge at 11.30% CAGR to 2030.

- By end-user industry, the consumer electronics segment accounted for 59.30% of the Asia-Pacific eSIM market in 2024, while industrial and manufacturing segments are poised for the fastest growth, with a 13.67% CAGR through 2030.

- By country, China captured 39.42% of the Asia-Pacific eSIM market in 2024, while Japan is projected to register a 5.66% CAGR through 2030.

Asia-Pacific ESIM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in 5G-Enabled Device Shipments | +0.8% | China, Japan, South Korea, India | Medium term (2-4 years) |

| Government Mandates for Integrated SIM in M2M Devices | +0.5% | China, Japan, India, Rest of Asia-Pacific | Long term (≥ 4 years) |

| Operator Cost Savings from Remote SIM Provisioning | +0.4% | Japan, South Korea, Rest of Asia-Pacific | Short term (≤ 2 years) |

| Cross-Border Travel Roaming Demand Post-COVID | +0.3% | Japan, South Korea, Rest of Asia-Pacific | Short term (≤ 2 years) |

| On-Device Privacy Controls Driving Consumer Uptake | +0.2% | Japan, South Korea, India | Medium term (2-4 years) |

| Expansion of Private 5G Campus Networks in Factories | +0.3% | Japan, China, South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in 5G-Enabled Device Shipments

Asia Pacific shipped more than 320 million 5G handsets in 2024, led by 241 million units in China and a combined 80 million units across Japan, South Korea, and India. The installed base removes technical barriers to eSIM because 5G standalone eliminates legacy circuit-switched dependencies and streamlines over-the-air profile downloads. Qualcomm’s Snapdragon X80 modem integrates eSIM and RedCap support, enabling device makers to reclaim board space and reduce component counts. A similar integration is also present in MediaTek’s T300 series for reduced-capability wearables. Growing 5G coverage also accelerates operator investment in subscription-management data-preparation servers, which are essential for remote provisioning but still scarce in Vietnam and Indonesia. Collectively, these shifts lift total addressable demand for embedded connectivity across both consumer and industrial devices.

Government Mandates for Integrated SIM in M2M Devices

Japan’s regulator enforced multi-SIM emergency-call routing in July 2025, compelling devices with multiple profiles to default to public-safety networks during disasters.[1]Misato Suzuki, “Multi-SIM Emergency Call Requirements,” Ministry of Internal Affairs and Communications, soumu.go.jp China has signaled plans to require eSIMs in connected-vehicle telematics and smart meters, aligning with its Data Security Law, which prioritizes centralized data governance.[2]Zhang Wei, “Data Security Law Implementation Rules,” MIIT China, miit.gov.cn India’s standards body is drafting eSIM specifications for utility meters, aiming to cut field-deployment costs at state electricity boards. These mandates ensure baseline demand in industrial and public infrastructure projects, shielding module vendors from fluctuations in consumer spending cycles. Compliance with GSMA SGP.32 for vehicles and SGP.24 for IoT acts as a barrier to entry, favoring suppliers with a certification track record.

Operator Cost Savings from Remote SIM Provisioning

Ericsson’s 2024 field analysis shows that eSIM halves SIM-card procurement expense, trims logistics costs by 30%, and reduces call-center traffic by 20%, yielding USD 5-USD 8 in annual savings per subscriber for large carriers. Vodafone corroborates those numbers, citing a 30% drop in operating expense once eSIM penetration surpasses 40% of its base. Savings are even more pronounced in archipelagic nations such as Indonesia and the Philippines, where last-mile distribution costs run 40%–60% above urban benchmarks. In these environments, remote provisioning enhances EBITDA margins and accelerates the payback period on 5G infrastructure.

Expansion of Private 5G Campus Networks in Factories

NTT Docomo has activated over 1,000 private 5G networks across Japanese plants, connecting autonomous vehicles and collaborative robots that require zero-touch provisioning. SK Telecom follows suit at Samsung Electronics’ semiconductor fabs, using eSIM to issue credentials without entering clean-room environments. China Mobile deploys similar solutions at ports and mines, employing network slicing to guarantee sub-10 ms latency. These cases underscore the eSIM’s suitability for industrial automation, where downtime incurs a high opportunity cost. Consulting surveys suggest that industrial IoT will absorb 37% of eSIM connections by 2030, overtaking consumer electronics in terms of units.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Certification and Compliance Standards | -0.4% | China, India, Rest of Asia-Pacific | Medium term (2-4 years) |

| Higher BOM Cost Versus Legacy SIM Cards | -0.3% | India, Rest of Asia-Pacific, Global | Short term (≤ 2 years) |

| Scarcity of LPA Back-End Hosting Nodes in Emerging Markets | -0.2% | Vietnam, Indonesia, Philippines | Long term (≥ 4 years) |

| Data-Localization Laws Hindering Remote Provisioning | -0.2% | China, India, Indonesia, Vietnam | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Certification and Compliance Standards

GSMA SAS-SM and SAS-UP audits require 6-9 months and cost up to USD 200,000 per platform, while separate Common Criteria EAL4+ evaluations for secure elements can take up to 18 months.[3]GSMA, “SAS-SM and SAS-UP Audit Guide,” gsma.com Country-specific rules add further delay; Indonesia’s Regulation 71 requires local data storage, which forces the replication of subscription-manager infrastructure and increases costs. Vietnam’s Cybersecurity Law and India’s lawful-intercept protocols impose further testing layers. As a result, vendors face 18-24 months longer time-to-market than in harmonized regions, reducing new-entrant participation in smaller Southeast Asian economies.

Higher BOM Cost Versus Legacy SIM Cards

An MFF2 eSIM package, priced at USD 1.50-USD 3.00, costs roughly three times as much as a plastic SIM. This deters low-cost smartphone brands, notably Xiaomi, Oppo, and Vivo, from introducing eSIM-ready handsets in India, where only 10%-15% of devices supported the feature as of late 2024. Although integrated-SIM technology promises to erase discrete-component costs, Qualcomm’s iSIM remains confined to premium models as of 2025. The price gap clouds adoption in entry-level M2M modules used for smart-meter rollouts, delaying migration until volume economics improve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Hardware Dominates, Services Scale Faster

Hardware held a 55.84% market share in the Asia Pacific eSIM market in 2024, primarily driven by MFF2 secure elements inside smartphones, wearables, and tablets. Remote-provisioning services, however, are growing at a 6.40% CAGR as carriers invest in subscription-manager data-preparation servers that automate over-the-air activation. Thales, Giesecke+Devrient, and IDEMIA leverage decades-long OEM relationships, while Kigen licenses iSIM intellectual property that embeds secure enclaves inside Cortex-M processors. Qualcomm’s Snapdragon X80 pushes the shift toward on-die integration, but wide adoption will lag because mid-tier devices typically refresh every three years. In the longer term, software’s annuity-like economics may outpace one-time hardware revenue, reshaping value capture for suppliers.

The hardware pipeline nonetheless remains robust through 2030, as existing devices without iSIM continue to exhaust their lifespan. STMicroelectronics and Infineon supply automotive-grade secure elements that withstand extreme temperatures and vibrations. Simultaneously, cloud-native eSIM management software reduces the per-subscriber marginal cost, allowing MVNOs and travel-eSIM aggregators to scale “pay-as-you-go” plans across 200 countries. When combined, these forces create a two-speed market, in which legacy hardware shipments plateau while service revenue continues to compound.

By Device Type: Smartphones Dominate, IoT Quickens

Smartphones still account for the largest share, 65.33% in 2024, owing to the Apple iPhone and Samsung Galaxy lines, which ship dual-eSIM variants in nearly every market outside mainland China. These devices enable travelers to switch carriers from a hotel lobby, rather than a kiosk, a convenience now promoted by tour operators in Tokyo and Seoul. Apple added a second eSIM channel in the 2024 iPhone 16 series, so a single handset can carry one personal and one business line, a feature that lifted activation rates among remote workers in Australia.

M2M/IoT modules are expected to grow at an 8.99% CAGR through 2030. Fibocom and Quectel have already bundled 5G eSIM into their automotive-grade designs, so that a Chinese excavator or Japanese robot leaves the factory with remote provisioning built in. Warehouse operators in Singapore report a 40% reduction in forklift downtime after switching to eSIM, as technicians no longer need to swap cards during annual safety checks.

By Network Type: 4G Holds the Base, 5G Drives Upsell

Most active profiles still operate on 4G and LTE, which together cover 57.71% of 2024 traffic, but revenue momentum now follows the 5G standalone. China Mobile, China Telecom, and China Unicom operate more than 3 million 5G base stations, and each one supports network slicing that cuts latency to single-digit milliseconds, a prerequisite for remote-controlled cranes in Ningbo Port. In Japan, NTT Docomo links 5G eSIM phones directly to its disaster-alert network so that emergency warnings bypass commercial data congestion during an earthquake.

Low-power segments matter too. NB-IoT and LTE-M modules in Indonesia’s smart-meter rollout wake up only once a day, send a reading, then sleep; yet, they still require secure credentials that survive a decade in tropical heat. Operators prefer eSIM here because field trucks no longer need to revisit homes to replace damaged cards, resulting in service costs being cut by up to 50% in Jakarta’s outer districts.

By End-User Industry: Consumer Electronics Anchor, Industrial Surges

Consumer electronics retained 59.30% of 2024 revenue, but industrial and manufacturing are expected to drive growth at a 13.67% CAGR to 2030. At a Toyota supplier in Aichi, collaborative robots fitted with eSIM routers roam between assembly cells, switching from the site’s private 5G slice to NTT Docomo’s public band the moment they cross the loading dock, all without a manual profile change. In South Korea, SK Telecom provisions every piece of clean-room equipment at Samsung’s chip fab over the air, avoiding physical entry that would otherwise halt production and risk particle contamination.

Automotive follows close behind. Thales and Cubic expect their February 2025 contract to ship 23 million SGP.32-compliant eSIMs, which will enable each vehicle to roam across 200 countries and update carrier plans during routine software patches. Logistics firms in Melbourne and Manila place a similar value on over-the-air swaps. Refrigerated trailers driving from Brisbane to Bangkok now cycle through four operators automatically, ensuring that temperature alerts never drop during handoffs. Energy utilities seek the same reliability. China’s State Grid embeds eSIMs in smart meters, allowing linemen to remotely de-energize a pole before climbing, thereby boosting worker safety in rural Anhui.

Geography Analysis

China, commanding 39.42% of the 2024 revenue, is witnessing a swift evolution in its eSIM landscape. While consumer eSIMs in smartphones were largely confined to minor trials until October 2025, growth has predominantly stemmed from industrial and wearable sectors. With the Ministry of Industry and Information Technology greenlighting nationwide trials, domestic giants such as Xiaomi and Vivo are poised to integrate the feature. This is contingent upon subscription-manager nodes relocating within China's borders, aligning with stringent data security mandates. In 2024, China dispatched 241 million 5G phones, representing a staggering 92% of its total handset volume, underscoring a significant latent demand awaiting the resolution of policy challenges.

Japan is witnessing a 5.66% CAGR, fueled by regulatory shifts and a tourism boom. The Ministry of Internal Affairs and Communications has mandated that all multi-SIM devices must route emergency calls through a reliably connected network. This regulation incentivizes consumers to maintain an active domestic profile, even when utilizing a short-term travel eSIM. Tourists can now purchase eSIM packages at airports in under two minutes, effortlessly overcoming the previous language barriers that complicated kiosk activations. Additionally, the private 5G sector is thriving. Over 1,000 factories across Japan have established campus networks, with each machine floor equipped with an eSIM or iSIM credential, which can be conveniently updated by maintenance staff from their laptops.

South Korea and India showcase contrasting approaches. By 2023, Seoul achieved near-complete 5G coverage. Consequently, SK Telecom and KT have begun bundling eSIMs into their premium data offerings and private network agreements with affiliates such as Samsung and LG. Conversely, India imposes a six-month limit on foreign profiles; exceeding this duration mandates a switch to a domestic plan. While this regulation safeguards Airtel and Jio from customer churn, it inadvertently hampers adoption rates among frequent travelers desiring a year-round home profile. By late 2024, only 10%-15% of Indian devices were eSIM-compatible, as local manufacturers hesitated to shoulder the hardware premium in a market sensitive to pricing.

Competitive Landscape

Competition in the Asia Pacific eSIM market is neither fully fragmented nor entirely consolidated. The top five players, Thales, Giesecke+Devrient, IDEMIA, Qualcomm, and MediaTek, command a significant share, wielding enough influence to shape industry standards, yet leaving room for challengers. While seasoned veterans in secure-element manufacturing leverage decades of experience, they face mounting pressure as integrated SIM technology increasingly merges with application processors. Qualcomm has set a precedent with its Snapdragon X80 modem, which melds eSIM logic directly onto the 5G baseband die, optimizing board space and enhancing power efficiency. Meanwhile, Kigen's licensing of similar intellectual property for Cortex-M microcontrollers hints at a potential shift, drawing smaller IoT devices away from traditional silicon.

Strategic maneuvers often hinge on vertical specialization. For instance, Thales integrates its secure elements with Cubic’s back-office platform, targeting automotive contracts with an eye on vehicles that will need profile refreshes over the next decade. On the other hand, Chinese module manufacturers like Fibocom, Quectel, and SIMCom, capitalize on domestic demand for smart meters and surveillance cameras. By bundling modules with data plans from China Mobile’s international division, they offer Indonesian scooter trackers the ability to roam across Asian networks, sidestepping separate agreement hassles and undercutting Western competitors.

Digital-native brands like Airalo and Holafly have revolutionized the travel eSIM market, enabling users to purchase packs in mere thirty-second app transactions, completely sidestepping traditional operator stores. While Japan and South Korea have readily adopted this model, countries like India and Indonesia enforce stringent Know Your Customer regulations. These rules mandate comprehensive identity verification, inadvertently slowing adoption rates and bolstering the position of established carriers. Looking ahead, the next competitive frontier appears to be in subscription-manager hosting.

Asia-Pacific ESIM Industry Leaders

Thales Group

Giesecke+Devrient GmbH

IDEMIA Group S.A.S.

MediaTek Inc.

Qualcomm Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: China’s MIIT authorized China Mobile, China Telecom, and China Unicom to begin commercial smartphone eSIM trials, ending years of consumer restrictions.

- May 2025: Japan’s MIC enforced rules requiring multi-SIM devices to prioritize public-safety networks for emergency calls, affecting smartphones and wearables with eSIM.

- February 2025: Qualcomm launched the Snapdragon X80 5G modem-RF system with integrated eSIM, promising 10 Gbps peak download and 20% lower power than prior generations.

- January 2025: Thales and Cubic Transportation Systems agreed to deliver GSMA SGP.32 automotive eSIM for 23 million connected vehicles across 200 countries, enabling multi-operator roaming without hardware recalls.

- October 2024: Qualcomm introduced the Snapdragon 8 Elite platform, featuring iSIM embedded directly in the application processor, which eliminates the need for discrete eSIM hardware.

Asia-Pacific ESIM Market Report Scope

The Asia-Pacific eSIM Market Report is Segmented by Offering (Hardware eSIM [MFF2, Wafer-Level CSP, iSIM IP], eSIM Management Software, Remote SIM Provisioning Services), Device Type (Smartphones and Feature Phones, Tablets and Laptops, Wearables, M2M/IoT Modules), Network Type (5G, 4G/LTE, NB-IoT/LTE-M), End-user Industry (Consumer Electronics, Automotive and Transportation, Industrial and Manufacturing, Logistics and Asset Tracking, Energy and Utilities, Healthcare and Wearables), and Country (China, Japan, South Korea, India, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Hardware eSIM (MFF2, Wafer-Level CSP, iSIM IP) |

| eSIM Management Software |

| Remote SIM Provisioning Services |

| Smartphones and Feature Phones |

| Tablets and Laptops |

| Wearables |

| M2M/IoT Modules |

| 5G |

| 4G/LTE |

| NB-IoT/LTE-M |

| Consumer Electronics |

| Automotive and Transportation |

| Industrial and Manufacturing |

| Logistics and Asset Tracking |

| Energy and Utilities |

| Healthcare and Wearables |

| China |

| Japan |

| South Korea |

| India |

| Rest of Asia-Pacific |

| By Offering | Hardware eSIM (MFF2, Wafer-Level CSP, iSIM IP) |

| eSIM Management Software | |

| Remote SIM Provisioning Services | |

| By Device Type | Smartphones and Feature Phones |

| Tablets and Laptops | |

| Wearables | |

| M2M/IoT Modules | |

| By Network Type | 5G |

| 4G/LTE | |

| NB-IoT/LTE-M | |

| By End-User Industry | Consumer Electronics |

| Automotive and Transportation | |

| Industrial and Manufacturing | |

| Logistics and Asset Tracking | |

| Energy and Utilities | |

| Healthcare and Wearables | |

| By Country | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the projected value of the Asia Pacific eSIM market in 2030?

The market is expected to reach USD 2.44 billion by 2030.

Which country contributes the most revenue today?

China accounted for 39.42% of 2024 revenue.

Which segment shows the fastest CAGR?

Industrial and manufacturing applications are growing at 13.67% CAGR through 2030.

How fast will 5G-based eSIM profiles grow?

5G profiles are forecast to expand at an 11.30% CAGR to 2030.

Why are operators adopting remote provisioning?

ESIM cuts SIM procurement and logistics costs by up to 50% and raises EBITDA margins.

What restrains small vendors in Southeast Asia?

Divergent certification rules and data-localization laws add up to 24 months of extra compliance time.

Page last updated on: