Asia-Pacific Electric Vehicle Wireless Charging Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

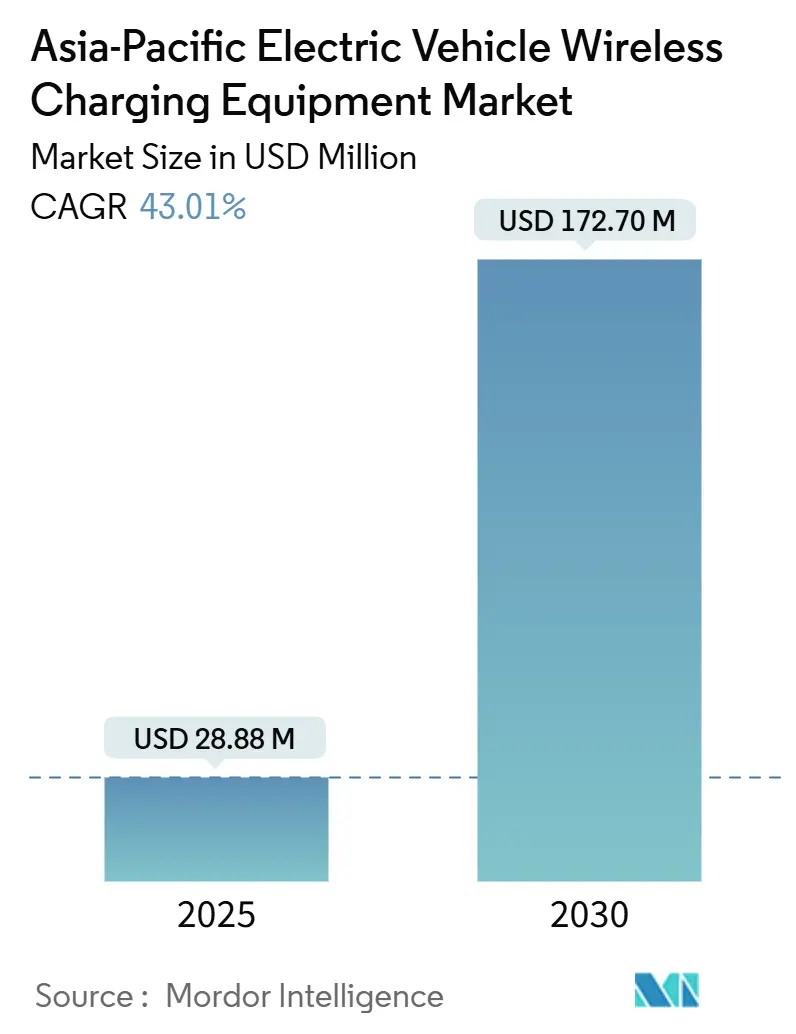

| Market Size (2025) | USD 28.88 Million |

| Market Size (2030) | USD 172.70 Million |

| Growth Rate (2025 - 2030) | 43.01% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Electric Vehicle Wireless Charging Equipment Market Analysis by Mordor Intelligence

The Asia-Pacific Electric Vehicle Wireless Charging Equipment Market size is estimated at USD 28.88 million in 2025, and is expected to reach USD 172.70 million by 2030, at a CAGR of 43.01% during the forecast period (2025-2030).

Electric vehicle (EV) wireless charging equipment enables contactless power transfer between a ground-side transmitter and an in-vehicle receiver through inductive magnetic coupling. The system typically includes a ground-mounted pad or coil with power electronics and control units, along with a secondary coil and rectifier integrated into the vehicle. Compared with plug-in charging, wireless charging supports hands-free operation, lowers mechanical wear on connectors, and enables opportunity charging at depots, taxi stands, and public parking facilities. In addition, dynamic or in-motion charging is being evaluated through pilot deployments on select road corridors.

Asia-Pacific represents a key demand center for EV wireless charging equipment. The region hosts the largest EV manufacturing base globally, led by China, Japan, and South Korea. Moreover, high urban density across major cities limits the scalability of curbside plug-in infrastructure, increasing the relevance of wireless charging solutions. Furthermore, governments and industry bodies in the region are actively supporting standardization initiatives and pilot programs for both static and dynamic wireless charging. As a result, Asia-Pacific is identified as a high-growth region within the EV wireless charging ecosystem through 2030【1】“Policy Sequencing for EV Charging Infrastructure Deployment,” International Council on Clean Transportation (ZEV Transition Council), theicct.org.

Key Report Takeaways

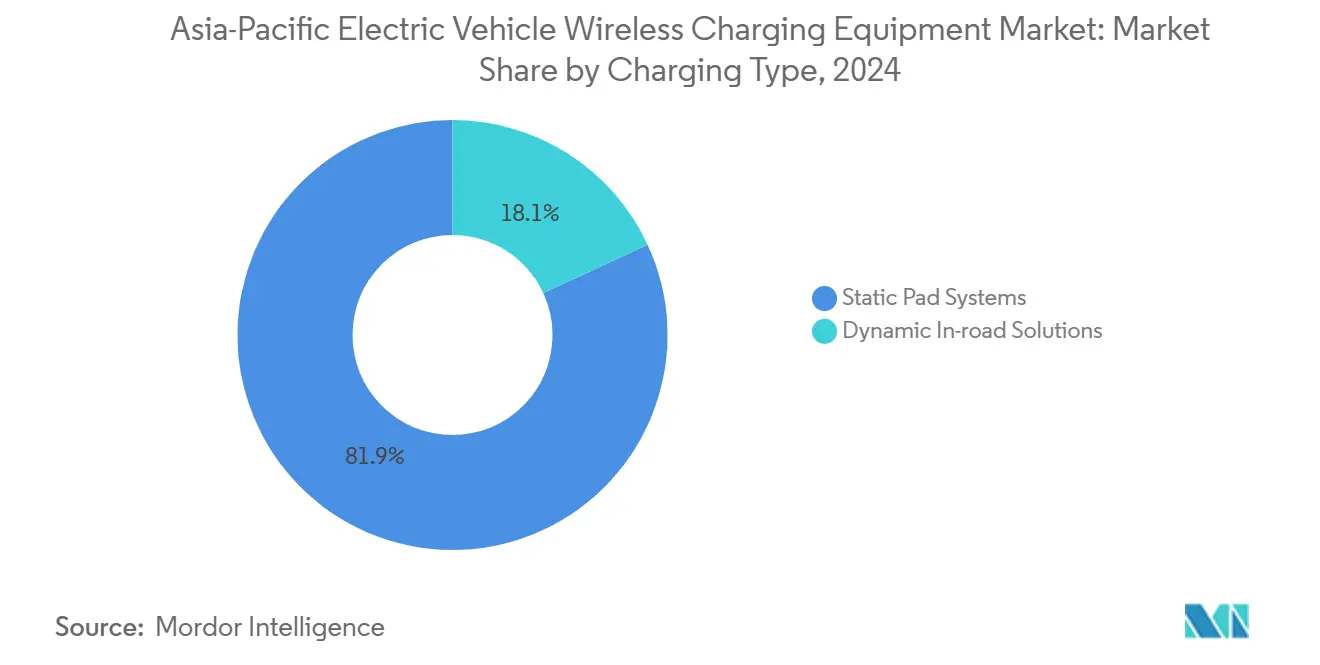

- By charging type, static pad systems led with 81.90% share in 2024, while dynamic in-road solutions are forecast to grow at 62.05% CAGR through 2030.

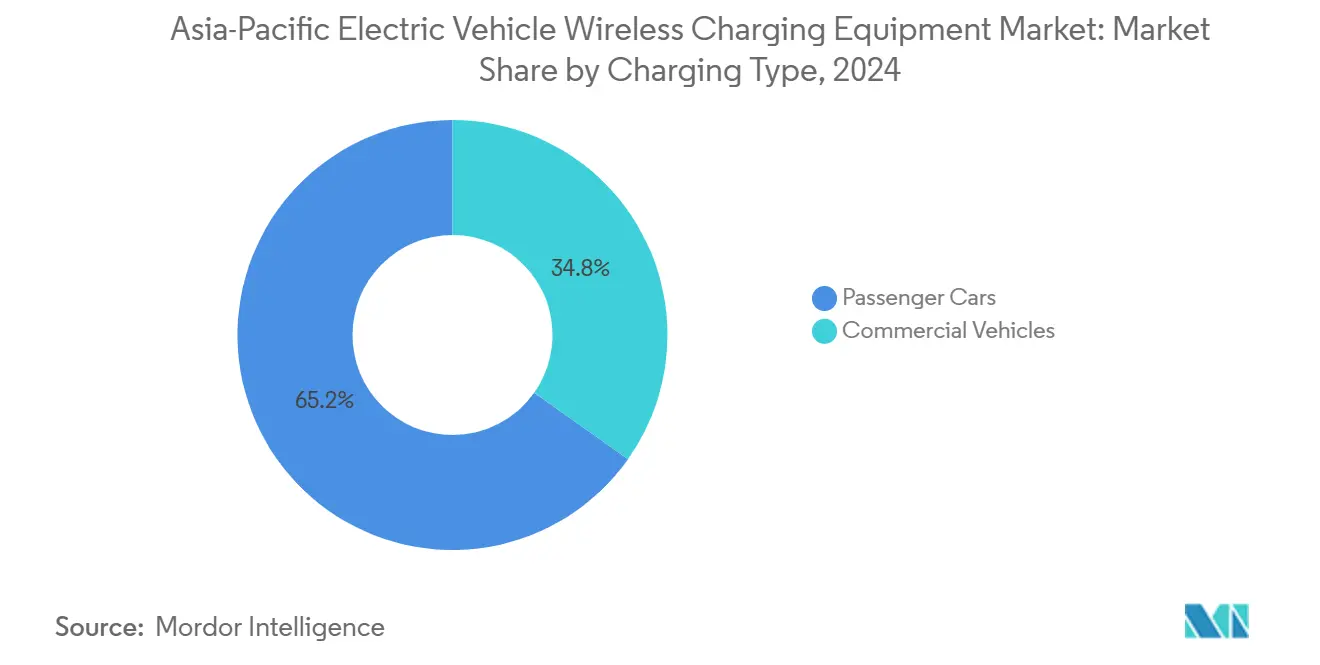

- By vehicle type, passenger cars held 65.20% of 2024 revenue; buses and coaches are projected to expand at 48.22% CAGR through 2030.

- By power output, up to 11 kW units accounted for 57.80% of 2024 market size; installations above 150 kW are expected to grow at 70.30% CAGR over the same period.

- By installation site, home garages represented 71.20% of 2024 market size, while highway lane projects show the highest outlook at 57.21% CAGR through 2030.

- By technology platform, inductive resonant coupling led with 74.30% share in 2024; magnetic field alignment multi-coil systems are forecast to grow at 66.45% CAGR through 2030.

- By geography, China accounted for 74.22% of the 2024 market size, while Southeast Asia is projected to be the fastest-growing region, registering a CAGR of 65.45% through 2030.

Worldwide, activity is shaped by contributions from multiple regions, with Asia representing one of the more structurally developed among them. The global report on electric vehicle wireless charging equipment market by Mordor Intelligence reflects how these regional layers combine into a single system.

Asia-Pacific Electric Vehicle Wireless Charging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability Standards Maturing | +1.1% | Japan, South Korea, Australia; spillover to ASEAN | Medium term (2–4 years) |

| Fleet Opportunity-Charging Economics | +1.0% | China metros, Japan, Korea; depot-heavy fleets | Short term (≤ 2 years) |

| Dynamic In-Road Showcase Corridors | +0.8% | Japan (Expo-linked), selected China/Korea pilots | Medium term (2–4 years) |

| APAC OEM Feature Adoption For Premium EVs | +0.7% | Japan & South Korea premium segments | Medium term (2–4 years) |

| Local Supply-Chain Scaling In Coils & SiC Power Modules | +0.6% | China, Japan, South Korea manufacturing clusters | Long term (≥ 4 years) |

| Autonomy-Readiness For Hands-Free Charging | +0.6% | Dense cities across APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Interoperability Standards Maturing

The maturation of interoperability standards reduces engineering risk for OEMs and infrastructure providers. These standards define alignment tolerances, communication protocols, safety concepts, and certification pathways. The release of SAE J2954:2024 provides a clear reference point for OEM sourcing decisions and supports multi-brand deployment planning across shared charging sites【2】“Global EV Outlook 2024,” International Energy Agency, iea.org.

Fleet Opportunity-Charging Economics

Wireless charging delivers the strongest value proposition in use cases where vehicle utilization improves and manual handling is minimized. This is particularly relevant for bus depots, taxi queues, and fixed-route fleet operations. As a result, fleet deployments are often the first to scale, even as private passenger vehicle adoption progresses at a slower pace.

Dynamic In-Road Showcase Corridors

Public demonstration corridors play a critical role in validating system reliability, including coil durability beneath pavement, energy transfer at operating speeds, and operational models for transit authorities. In Japan, Expo-linked initiatives explicitly reference in-motion wireless charging for electric buses. These programs increase visibility and strengthen confidence in dynamic wireless charging concepts.

APAC OEM Feature Adoption for Premium EVs

In Asia-Pacific, premium OEM strategies act as a key catalyst for adoption. Early factory-fit offerings or pilot-ready vehicle trims support installed-base learning and accelerate supplier ecosystem development for receiver integration and software controls. However, OEM investment decisions remain closely tied to return on investment and real-world efficiency. Consequently, progress in standardization and performance remains a critical enabler.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront CapEx And ROI Uncertainty | -1.30% | Across APAC; strongest in price-sensitive markets | Short term (≤ 2 years) |

| Efficiency, Alignment, And EMF Compliance Complexity | -1.00% | Urban deployments and high-power applications | Medium term (2–4 years) |

| Limited Factory-Fit Models And Homologation Lead Times | -0.80% | Japan & South Korea (OEM gating), ASEAN imports | Medium term (2–4 years) |

| Competitive Pressure From Fast Wired Charging | -0.60% | China & Korea (high-power DC build-out) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront CapEx and ROI Uncertainty

Wireless charging deployments require investment in both ground infrastructure and in-vehicle receiver hardware. This increases total installed costs compared with many plug-in charging alternatives. In locations with uncertain utilization, such as public parking, or where electricity pricing is unfavorable, payback periods can extend significantly. This dynamic shifts early adoption toward fleet and controlled-use environments.

Achieving high power-transfer efficiency depends on precise alignment, coil design, and robust foreign object detection and safety systems. These requirements become more complex at higher power levels. Compliance with international frameworks, such as the IEC 61980 series, reflects the engineering intensity required for safe wireless power transfer. Moreover, real-world pilot projects have shown that performance and cost trade-offs can lead to program delays or scope revisions when efficiency targets are not achieved within acceptable cost thresholds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Charging Type: Static dominates; dynamic drives growth

Static wireless charging remains the commercial “workhorse” of the market, holding 81.90% share in 2024. The category benefits from clearer installation playbooks (garage/depot pads, known civil works, predictable user behavior) and a more straightforward safety/EMF validation path versus roadway-embedded systems. In Asia-Pacific, the static segment is also where most early deployments concentrate because it aligns with premium-home and fleet-depot use cases that can be controlled, monitored, and serviced more easily.

Dynamic wireless charging, by contrast, is still scaling from pilots but is expected to be the fastest growth vector at 62.05% CAGR through 2030. The growth logic is tied to high-duty routes (transit corridors, logistics lanes) where continuous or opportunistic energy transfer can reduce dwell time and reshape vehicle/battery sizing economics—yet it requires coordinated infrastructure investment and long permitting timelines, which is why its ramp is later and more project-based than static pads.

By Power Output: Low power today; high power next

Wireless charging systems rated up to 11 kW accounted for 57.80% of the market in 2024. This range reflects strong adoption in residential and light-commercial environments, where electrical upgrades are limited and alignment requirements are manageable. Moreover, this power band represents the most mature product ecosystem, with standardized pads, receivers, and control systems that are easier to integrate across vehicle platforms.

Higher-power systems above 150 kW are expected to grow at a CAGR of 70.22% through 2030. Demand is driven by fleet and depot use cases that prioritize shorter dwell times and higher vehicle utilization, as well as corridor-based concepts requiring meaningful energy transfer over limited time or distance. However, adoption is constrained by increased engineering complexity, including thermal management, EMF compliance, and safety validation, which elevate costs and execution risk.

By Installation Site: Homes scale first; highways later

Home garages represented the largest installation segment, capturing 71.20% of market share in 2024. Adoption is driven by premium convenience positioning, where private users value frictionless charging and predictable availability. From an execution standpoint, residential installations involve fewer stakeholders and allow repeatable deployment models. In Asia-Pacific, structured private parking in residential towers and gated communities further supports this trend.

Highway lane installations are projected to grow at a CAGR of 57.30% through 2030, making them the fastest-growing site category. These projects are typically multi-stakeholder initiatives involving road authorities, utilities, EPC contractors, and technology providers. Growth is linked to the strategic importance of enabling long-distance travel and high-utilization commercial routes. However, deployment timelines remain uneven, owing to dependence on public budgets, civil works, and regulatory approvals.

By Vehicle Type: Passenger leads; fleets accelerate adoption

Passenger cars accounted for 65.20% of market revenue in 2024. Early adoption is largely feature-driven, with wireless charging positioned as a comfort and user-experience differentiator in premium vehicle trims. Passenger vehicles also benefit from standardized usage patterns, such as overnight charging, and clearer integration pathways when OEMs offer factory-fit solutions rather than aftermarket retrofits.

Commercial vehicles, particularly buses and coaches, are expected to record a CAGR of 48.21% through 2030. Fleet operators can justify wireless charging through improved uptime, reduced manual handling, and standardized depot operations. Predictable routes and scheduling further compress payback periods, which explains why many pilot programs and corridor deployments prioritize transit fleets over private vehicles.

By Technology Platform: Mature inductive today; multi-coil next

Inductive resonant coupling held a 74.30% share of the market in 2024, reflecting its status as the most commercially deployed wireless charging architecture. The technology benefits from a well-established supplier ecosystem and proven scalability across residential, depot, and controlled public environments. In Asia-Pacific, this maturity reduces adoption risk for OEMs and infrastructure operators seeking to move beyond pilot deployments.

Magnetic field alignment multi-coil systems are projected to grow at a CAGR of 66.45% through 2030. Growth is driven by the need to reduce alignment sensitivity and improve real-world usability. Multi-coil designs expand the effective charging zone, increasing charging success rates in less-controlled parking environments. This becomes increasingly important as deployments extend into shared parking facilities and large fleet operations, where consistency directly impacts return on investment.

Geography Analysis

By geography, China accounted for 74.22% of the Asia-Pacific market in 2024, supported by the region’s largest EV parc and a high concentration of fleet applications such as bus depots, autonomous shuttles, and structured parking, where wireless charging improves operational efficiency. China leads the Asia-Pacific wireless EV charging market by combining the region’s largest EV parc with a dense concentration of fleet applications where wireless charging improves operational efficiency. Bus depots, autonomous shuttle services, and structured parking facilities support early commercialization through repeatable deployments. Moreover, China’s ability to fund both static installations and dynamic corridor demonstrations lowers per-site costs and accelerates learning on alignment, durability, and safety, sustaining its position as the largest revenue contributor in the region.

Southeast Asia is projected to be the fastest-growing market at a CAGR of 65.45% through 2030, driven by policy-backed EV scaling, dense urban environments, and clustered fleet-led deployments that expand gradually as standards mature and unit economics improve. Dense urban environments and limited charging space increase the relevance of hands-free charging for fleets and shared mobility. Growth is expected to follow a clustered rollout model, with initial deployments in high-density cities and fleet depots, followed by gradual expansion as standards mature and unit economics improve.

Mordor Intelligence provides coverage of the electric vehicle wireless charging equipment market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The wireless EV charging market is moderately concentrated, anchored by a limited group of technology licensors, Tier-1 automotive suppliers, and infrastructure integrators. Competitive positioning is shaped by three primary factors: ownership of core intellectual property and interoperability certifications; access to OEM integration and validation programs; and a track record of field deployments that reduce reliability, safety, and regulatory risk. As a result, early commercial wins tend to reinforce incumbency, particularly in fleet and transit applications where performance assurance is critical.

Technology licensors focus on standards-aligned architectures and OEM-ready reference designs, while Tier-1 suppliers emphasize vehicle integration, power electronics, and functional safety. Infrastructure specialists differentiate through system-level delivery, including civil works coordination, grid interfaces, and lifecycle service capabilities. Partnerships between these groups are common, reflecting the need to combine IP depth with automotive-grade manufacturing and on-site execution. In Asia-Pacific, collaboration with local OEMs, transit authorities, and EPC partners is a key route to scale.

Competition is also influenced by the split between static and dynamic charging. Static systems favor players with mature, certified solutions that can be deployed repeatedly across depots and residential sites. Dynamic charging remains more project-driven, with success tied to government-backed pilots and corridor demonstrations that validate durability and cost. Over time, standardization progress and declining system costs are expected to broaden participation; however, near-term growth remains concentrated among players with proven deployments and strong OEM relationships.

Asia-Pacific Electric Vehicle Wireless Charging Equipment Industry Leaders

WiTricity Corporation

InductEV Inc.

Electreon Wireless Ltd.

HEVO Inc. (HEVO Power)

Plugless Power Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Japan’s NEDO highlighted Expo 2025 Osaka demonstrations where Level 4 autonomous e-buses charge wirelessly via coils embedded in the road, involving Kansai Electric Power, DAIHEN, Osaka Metro, Obayashi, and others.

- April 2024: WiTricity announced it would be a founding member of Japan’s EV Wireless Power Transfer Council and said it planned to open WiTricity Japan KK.

- January 2024: Japan’s Sinanen Holdings signed an official partnership agreement with WiTricity to accelerate deployment of WiTricity’s wireless charging systems in Japan (including licensing/industry-association efforts).

Asia-Pacific Electric Vehicle Wireless Charging Equipment Market Report Scope

Electric vehicle wireless charging equipment refers to hardware and embedded control/communication systems that enable contactless power transfer between a ground-side transmitter (pad/coil + power electronics + controls) and a vehicle-side receiver (coil + rectification/control), supporting static (park-and-charge) and dynamic (in-motion) wireless charging configurations.

The scope includes segmentation by Charging Type (Static and Dynamic), Vehicle Type (Passenger Cars and Commercial Vehicles), Power Output (Up to 11 kW, 11–50 kW, 50–150 kW, and Above 150 kW), Installation Site (Home, Commercial/Depot, Public Parking, and Highway/Lane), Technology Platform (Inductive Resonant Coupling, Multi-Coil Alignment Platforms, and Others), Distribution Channel (OEMs and Aftermarket), and Geography (China, Japan, South Korea, India, Australia, ASEAN, Rest of Asia-Pacific). The market forecasts are provided in terms of value (USD).

| Static |

| Dynamic |

| Passenger Cars |

| Commercial Vehicles |

| Up to 11 kW |

| 11–50 kW |

| 50–150 kW |

| Above 150 kW |

| Home |

| Commercial/Depot |

| Public Parking |

| Highway/Lane |

| Inductive Resonant Coupling |

| Multi-Coil Alignment Platforms |

| Others |

| OEMs |

| Aftermarket |

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Southeast Asia |

| Rest of Asia-Pacific |

| Segmentation by Charging Type (Value, USD) | Static |

| Dynamic | |

| Segmentation by Vehicle Type (Value, USD) | Passenger Cars |

| Commercial Vehicles | |

| Segmentation by Power Output (Value, USD) | Up to 11 kW |

| 11–50 kW | |

| 50–150 kW | |

| Above 150 kW | |

| Segmentation by Installation Site (Value, USD) | Home |

| Commercial/Depot | |

| Public Parking | |

| Highway/Lane | |

| Segmentation by Technology Platform (Value, USD) | Inductive Resonant Coupling |

| Multi-Coil Alignment Platforms | |

| Others | |

| Segmentation by Distribution Channel (Value, USD) | OEMs |

| Aftermarket | |

| Segmentation by Country/Cluster (Value, USD) | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Southeast Asia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

1) Which charging type leads today and which grows fastest?

Static pad systems lead in 2024, while dynamic in-road solutions record the fastest growth through 2030.

2) Which vehicle type dominates now and which scales faster?

Passenger cars dominate current revenue, while commercial vehicles grow faster owing to fleet economics.

3) What power output range leads deployments and future growth?

Up to 11 kW systems lead today, while above 150 kW systems drive future growth.

4) Where are most installations today and where is growth highest?

Home garages dominate current installations, while highway lane projects grow the fastest.

5) Which technology platform leads and which gains traction?

Inductive resonant coupling leads today, while multi-coil platforms gain traction for wider adoption.

Page last updated on: