Asia Pacific Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

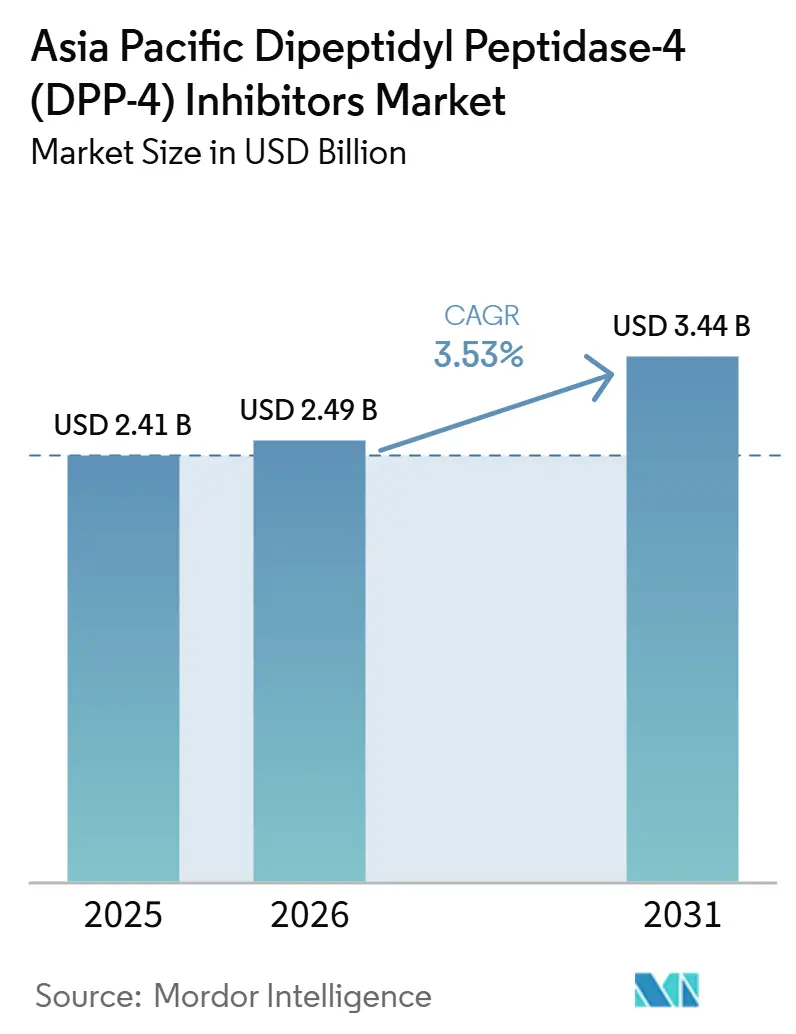

| Base Year Market Size (2025) | USD 2.41 Billion |

| Market Size (2026) | USD 2.49 Billion |

| Market Size (2031) | USD 3.44 Billion |

| Growth Rate (2026 - 2031) | 3.53% CAGR |

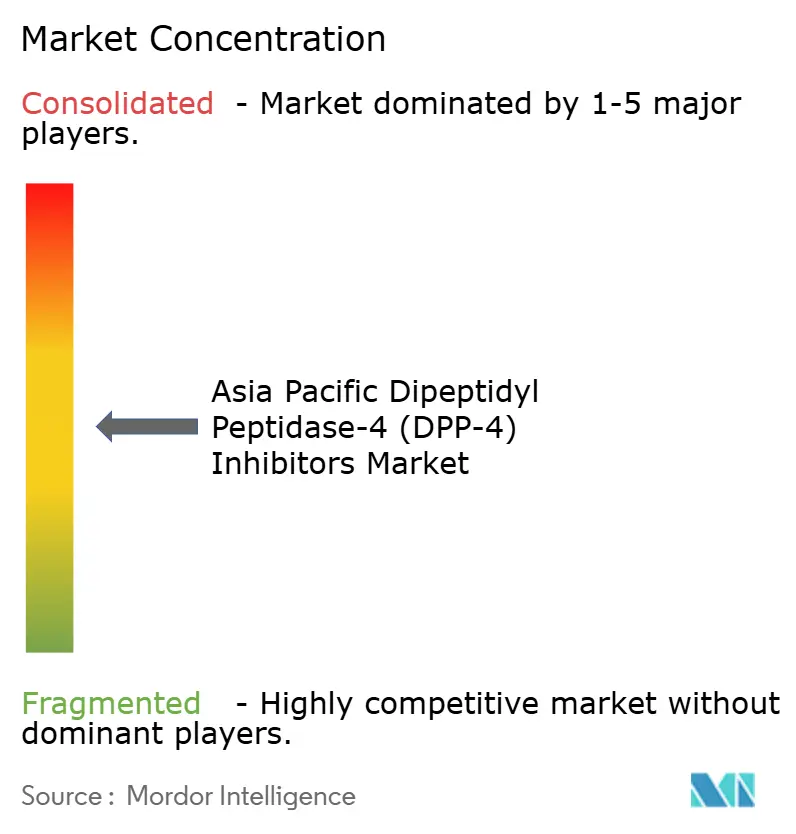

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market Analysis by Mordor Intelligence

The Asia Pacific Dipeptidyl Peptidase-4 Inhibitors Market size is projected to expand from USD 2.41 billion in 2025 and USD 2.49 billion in 2026 to USD 3.44 billion by 2031, registering a CAGR of 3.53% between 2026 to 2031.

The Asia Pacific DPP-4 inhibitors market remains supported by the large diabetes burden in China and India and by long physician familiarity with this oral class. The therapy keeps a clear role because it improves glycemic control without shifting treatment toward injectable formats, which still matters across large parts of the region. The Asia Pacific DPP-4 inhibitors market also benefits from its fit with patient groups where impaired insulin secretion, older age, and lower hypoglycemia tolerance shape treatment choice. Competition is rising from GLP-1 receptor agonists and SGLT2 inhibitors, but DPP-4 inhibitors still retain a practical position in low-risk therapy, elderly care, and combination tablets. Fixed-dose combination development, generic affordability, and broader pharmacy access keep the Asia Pacific DPP-4 inhibitors market commercially active even as pricing pressure limits upside.

Key Report Takeaways

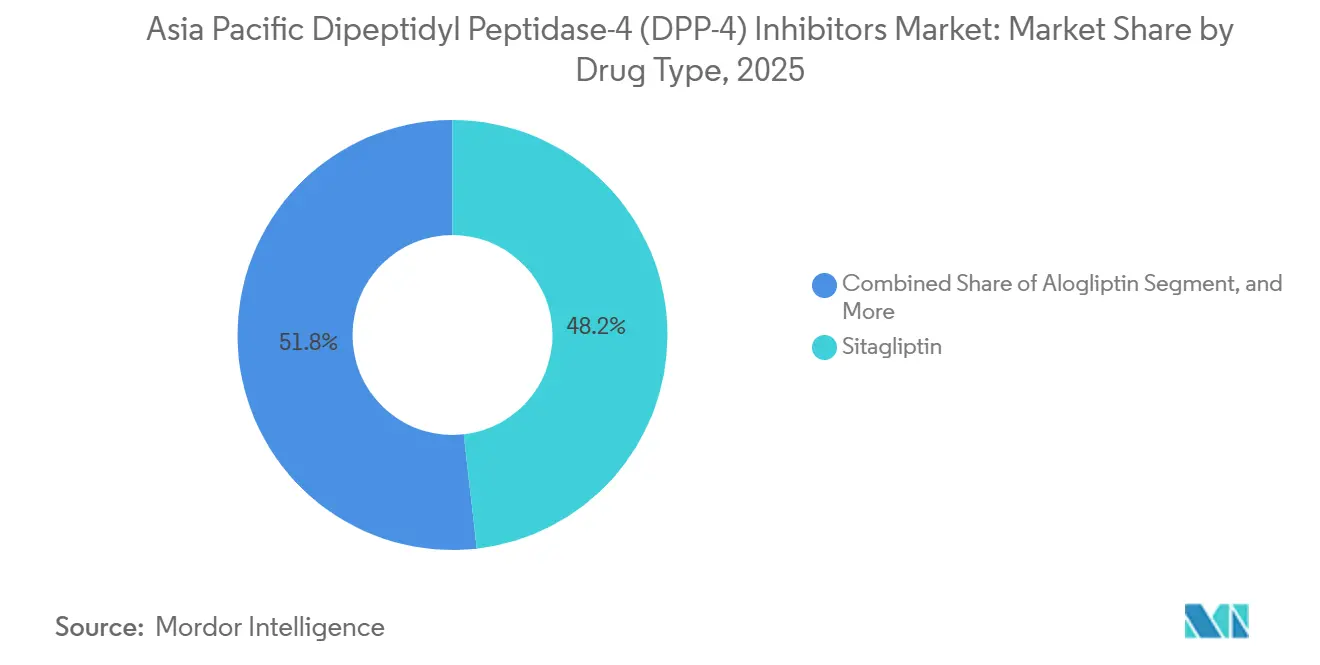

- By drug type, sitagliptin held 48.18% of the Asia Pacific DPP-4 inhibitors market share in 2025, while alogliptin is forecast to expand at a 3.98% CAGR through 2031.

- By medication type, generics accounted for 63.38% share of the Asia Pacific DPP-4 inhibitors market size in 2025, while branded formulations are projected to grow at a 4.97% CAGR through 2031.

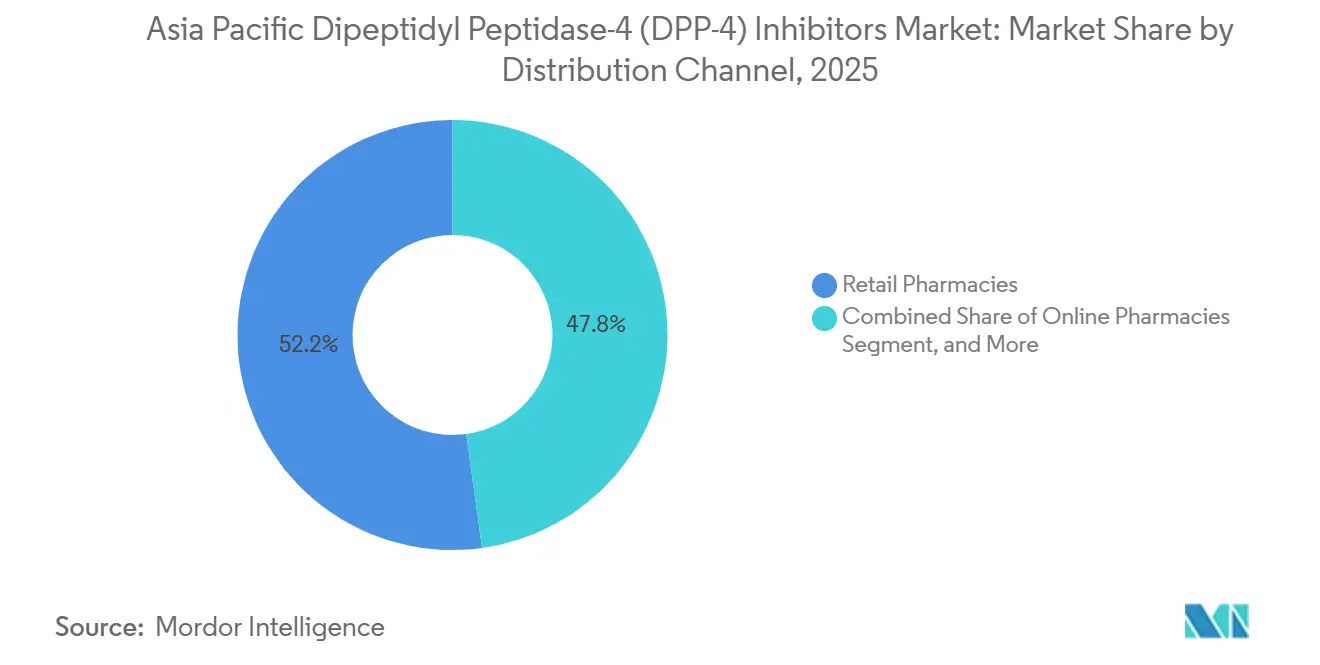

- By distribution channel, retail pharmacies captured 52.16% share of the Asia Pacific DPP-4 inhibitors market size in 2025, while online pharmacies are set to advance at a 5.05% CAGR through 2031.

- By geography, China accounted for 41.84% of the Asia Pacific DPP-4 inhibitors market in 2025, while India is expected to record the fastest CAGR at 3.27% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia Pacific Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Type 2 Diabetes Burden In China And India | +1.2% | China, India, APAC-wide demand pull | Medium term (2-4 years) |

| Favorable Oral Safety Profile And Low Hypoglycemia Risk | +0.7% | Global, pronounced in Japan, South Korea, Australia | Short term (≤ 2 years) |

| Fixed-Dose Combination Uptake With Metformin | +0.5% | China, India, South Korea | Medium term (2-4 years) |

| Expansion Of Tier-2 And Tier-3 Pharmacy Access Across Southeast Asia | +0.4% | Southeast Asia, spill-over to India | Medium term (2-4 years) |

| Patent-Led Generic Entry Expanding Affordability | +0.5% | India, China, Japan | Short term (≤ 2 years) |

| Hospital Formulary Preference For Once-Daily Gliptins In Elderly Patients | +0.3% | Japan, South Korea, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Type 2 Diabetes Burden In China And India

China and India remain the main volume engines for the Asia Pacific DPP-4 inhibitors market because both countries continue to add large numbers of adults who need long-term glucose control. India’s diagnosed adult diabetic population reached 61.3 million in 2024, which keeps the treatment pool large even before accounting for undiagnosed patients.[1]International Diabetes Federation, “India Diabetes Statistics & Health Data,” IDF Diabetes Atlas, diabetesatlas.org In China, the age-standardized prevalence rate is projected to rise by 37.19% between 2022 and 2050, so demand pressure is set to remain durable over time. The Asia Pacific DPP-4 inhibitors market is also helped by the clinical profile of Asian type 2 diabetes, where impaired insulin secretion keeps incretin-based oral therapy relevant. India still has room for broader treatment coverage, which means even modest gains in diagnosis-to-treatment conversion can lift prescription volumes for affordable generic products. This combination of scale, chronic therapy needs, and low treatment penetration gives the Asia Pacific DPP-4 inhibitors market a steady medium-term demand base.

Favorable Oral Safety Profile And Low Hypoglycemia Risk

The Asia Pacific DPP-4 inhibitors market benefits from an oral safety profile that remains highly relevant in older patient groups and in routine outpatient care. In Japan, more than 70% of patients with diabetes were aged 65 or older, which strengthens demand for agents with a low hypoglycemia risk.[2]Y.C. Zhou, “Trends and Comparisons of Diabetes Burden in China and the World from 1990 to 2021, With Forecasts to 2050, A Systematic Analysis of the Global Burden of Disease Study 2021,” Diabetology & Metabolic Syndrome, link.springer.com This matters because falls, arrhythmias, and hospital use become more serious concerns when treatment causes glucose to drop too aggressively. Japanese nationwide pharmacovigilance data did not establish causal links between DPP-4 inhibitors and acute pancreatitis or pancreatic cancer, which removed an older area of caution. A 2025 population-based study in advanced chronic kidney disease found no significant cardiovascular advantage for SGLT2 inhibitors over DPP-4 inhibitors, which preserves a meaningful prescribing niche. These factors help the Asia Pacific DPP-4 inhibitors market defend its place in elderly patients and in cases where simpler oral regimens remain preferred.

Fixed-Dose Combination Uptake With Metformin

Fixed-dose combinations are reshaping the Asia Pacific DPP-4 inhibitors market because they allow mature molecules to stay commercially relevant in newer oral regimens. In October 2025, a Hengrui subsidiary received NMPA approval for China’s first domestically developed triple fixed-dose combination that joined retagliptin, henagliflozin, and metformin in one tablet.[3]Jiangsu Hengrui Pharmaceuticals, “NMPA Approval Notice for Henagliflozin Proline, Retagliptin Phosphate and Metformin Hydrochloride Sustained-Release Tablets,” HKEXnews, hkexnews.hk In December 2025, CSPC received approval for the world’s first clinically approved triple combination of prusogliptin, dapagliflozin, and metformin. A 2026 Japanese claims database study found that fixed-dose combinations with DPP-4 inhibitors improved treatment persistence compared with free-combination regimens. The Asia Pacific DPP-4 inhibitors market, therefore keeps attracting lifecycle management even when single-molecule products face broad generic pressure. Combination-led differentiation now does more to protect franchise value than new standalone DPP-4 molecule launches.

Expansion Of Tier-2 And Tier-3 Pharmacy Access Across Southeast Asia

Wider pharmacy reach beyond major cities supports the Asia Pacific DPP-4 inhibitors market because these products are mainly used in repeat, long-duration outpatient treatment. Oral diabetes therapies benefit when patients can refill prescriptions closer to home and with fewer formal access barriers. This effect is stronger for DPP-4 inhibitors because they fit stable chronic use and do not require injection training or cold-chain handling. The same distribution pattern favors generic formulations that depend on broad physical availability rather than specialist promotion. Better pharmacy coverage also supports adherence, which matters in diabetes management where routine refill behavior shapes long-term volume. For the Asia Pacific DPP-4 inhibitors market, that makes local retail expansion an important support factor in Southeast Asia even when reimbursement remains uneven.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition From SGLT2 Inhibitors And GLP-1 Receptor Agonists | -1.3% | Global, pronounced in Japan, South Korea, Australia | Short term (≤ 2 years) |

| Pricing Pressure After Patent Expirations | -0.9% | China, India, Japan, South Korea | Short term (≤ 2 years) |

| Reimbursement Lag And Country-Level Access Friction | -0.5% | Southeast Asia, spill-over to South Asia | Medium term (2-4 years) |

| Clinical Preference Shift Toward Cardiorenal Agents In Advanced Diabetes | -0.4% | Japan, South Korea, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition From SGLT2 Inhibitors And GLP-1 Receptor Agonists

Competition from SGLT2 inhibitors and GLP-1 receptor agonists is the clearest ceiling on the Asia Pacific DPP-4 inhibitors market. The 2022-2024 ADA and EASD consensus pathway recommends a GLP-1 receptor agonist or SGLT2 inhibitor for patients with established cardiovascular disease, heart failure, or chronic kidney disease. That recommendation shifts prescribing away from DPP-4 inhibitors in the very patient groups where treatment intensity and clinical outcomes matter most. The effect is not a collapse in demand, because the overall diabetes pool is still expanding across the region. It does, however, narrow the first-line opportunity set as cardiometabolic risk stratification becomes more routine in specialist and payer-led pathways. As a result, the Asia Pacific DPP-4 inhibitors market remains relevant, but its growth ceiling stays lower than that of therapies with stronger cardiorenal positioning.

Pricing Pressure After Patent Expirations

Pricing pressure after patent expirations continues to weigh on the Asia Pacific DPP-4 inhibitors market, especially in the highest-volume countries. Sitagliptin still held 48.2% of the regional drug-type segment in 2025, so price erosion in that molecule has an outsized effect on class revenue. China, India, and Japan are all moving deeper into multi-source competition, which reduces the premium once enjoyed by originator brands. Public pricing and procurement systems also limit the revenue lift that companies can capture even when prescription counts rise. This creates a split between unit volume growth and value growth, with access improving while revenue per prescription trends lower. The Asia Pacific DPP-4 inhibitors market will therefore keep expanding more slowly in value terms than in prescription terms through 2031.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Sitagliptin Anchors The Class As FDC Platforms Redefine Competition

Sitagliptin held 48.18% of the drug-type segment in 2025, which gave it the largest base within the Asia Pacific DPP-4 inhibitors market. That lead reflects its first-in-class position, deep prescriber familiarity, and the broadest clinical evidence base in this therapy group. The molecule also benefits from a large generic active ingredient pool, which lets manufacturers in India and China use it in multiple combination strategies. Saxagliptin and vildagliptin continue to hold meaningful positions where hospital formularies and established prescribing networks still support legacy use. Even with rising therapeutic competition, sitagliptin remains the reference point for pricing, access, and lifecycle decisions across the Asia Pacific DPP-4 inhibitors industry.

Alogliptin is projected to record the fastest CAGR at 3.98% through 2031, showing that growth is still possible in selective parts of the Asia Pacific DPP-4 inhibitors market. Its momentum is linked to ongoing commercial attention in Japan and nearby markets where formulation upgrades can extend brand life. Linagliptin keeps a defensible niche because its biliary excretion avoids renal dose adjustment, which matters in elderly patients with diabetic nephropathy. China is also showing room for differentiated dosing innovation, with kogerliptin entering the 2025 NRDL after a price reduction that supported reimbursement access. At the same time, Zydus Lifesciences secured first-cycle FDA approval for Zituvio, Zituvimet, and Zituvimet XR, which shows how post-patent sitagliptin platforms can still support multi-market growth.

By Medication Type: Generic Dominance Masks A Branded FDC Resurgence

Generics accounted for 63.38% of the medication-type segment in 2025, which made low-cost supply the backbone of the Asia Pacific DPP-4 inhibitors market size at the product level. This dominance reflects years of patent expiry across older molecules in India, China, and several Southeast Asian markets. Generic availability aligns well with the chronic nature of diabetes care, where affordability often determines whether treatment is continued over time. The generic base also widens access in lower-income patient groups that still remain under-treated across the region. In the Asia Pacific DPP-4 inhibitors industry, this segment shapes volume more than branding does.

Branded formulations are projected to grow at a 4.97% CAGR through 2031, which shows that value growth in the Asia Pacific DPP-4 inhibitors market is shifting toward combination design rather than standalone brands. Much of that growth comes from fixed-dose combinations that create a fresh differentiation layer even when the underlying molecules are already commoditized. An Indian clinical review published in 2025 highlighted the role of SGLT2 inhibitors, DPP-4 inhibitors, and metformin combinations in current diabetes management, which supports the commercial logic behind triple-combination development. Public systems still keep branded spending in check, and Malaysia’s 2025 national formulary used cost-minimization tendering that favored lower-cost DPP-4 options and removed linagliptin from the formulary. That dynamic leaves branded growth concentrated in differentiated combinations, private channels, and adherence-oriented positioning rather than broad public reimbursement.

By Distribution Channel: Retail Pharmacies Lead As Digital Channels Accelerate

Retail pharmacies captured 52.16% of the distribution channel segment in 2025, which made them the leading outlet in the Asia Pacific DPP-4 inhibitors market size for channel sales. This lead comes from repeat prescription behavior, local dispensing convenience, and the routine nature of chronic diabetes management. Community pharmacies are especially important because many patients refill therapy for long periods after the initial prescription decision has already been made. Retail outlets also serve both branded and generic formats, which gives them a broad role across pricing tiers and patient income groups. In the Asia Pacific DPP-4 inhibitors market, this channel remains the clearest bridge between large diagnosed populations and regular treatment continuity.

Online pharmacies are projected to expand at a 5.05% CAGR through 2031, making them the fastest-growing channel in the Asia Pacific DPP-4 inhibitors market. Digital dispensing fits chronic oral therapies because refills can be scheduled, reminders can be automated, and price comparison is easier for patients. Hospital pharmacies still matter in Japan and South Korea because institutional prescribing often shapes the first therapy choice before long-term refill behavior shifts elsewhere. The online opportunity is still constrained by reimbursement rules and prescription handling standards that vary widely across the region. Even so, the channel mix is gradually widening, and that gives the Asia Pacific DPP-4 inhibitors market more ways to serve stable repeat-use demand.

Geography Analysis

China accounted for 41.84% of the Asia Pacific DPP-4 inhibitors market share in 2025, which made it the largest country market in the region. Its scale reflects deep urban prescribing, broad reimbursement reach, and the strong role of domestic manufacturers in shaping access and pricing. An interrupted time-series study in Shanghai showed that centralized drug procurement and price negotiation policies materially changed the use and costs of novel hypoglycemic drugs, confirming that policy remains the main market access lever in China. China also remains important because new combination approvals and reimbursement-linked pricing moves continue to redefine how the Asia Pacific DPP-4 inhibitors market competes at scale.

India is forecast to record the fastest CAGR at 3.27% through 2031, which keeps it central to forward growth in the Asia Pacific DPP-4 inhibitors market. The country had 61.3 million diagnosed adults with diabetes in 2024, and that large base still leaves room for wider treatment coverage as affordable products spread. Japan remains the most penetrated market by prescription depth, supported by its older diabetes population and its steady preference for oral agents with a lower hypoglycemia burden. South Korea sits between the mature Japanese model and the faster-volume Indian model, with active formulation work helping maintain class relevance even as therapeutic competition rises. Together, these 3 countries show how the Asia Pacific DPP-4 inhibitors market balances scale, affordability, and clinical fit across very different healthcare systems.

Australia shows measured growth because reimbursement discipline and bioequivalence standards keep competitive expansion orderly rather than abrupt. The Rest of Asia-Pacific offers the broadest long-term volume opportunity for the Asia Pacific DPP-4 inhibitors market, although fragmented payer systems still slow near-term revenue capture. Organized pharmacy expansion, wider generic supply, and gradual reimbursement improvement can support steady uptake in countries such as Indonesia, Thailand, the Philippines, Vietnam, and Malaysia. Malaysia’s 2025 national formulary update also illustrated how public procurement discipline can widen access while capping branded upside across the Asia Pacific DPP-4 inhibitors market.

Competitive Landscape

The Asia Pacific DPP-4 inhibitors market shows moderate concentration at the originator level and far broader fragmentation in the generic tier. Merck retains the strongest reference position through sitagliptin, while Boehringer Ingelheim uses linagliptin’s renal profile to defend prescribing in patients with kidney-related complexity. Novartis still holds a durable regional presence in vildagliptin, especially where older formulary relationships remain active across Southeast Asia. Takeda continues to support alogliptin through the Nesina family, which helps keep the molecule relevant in Japan, South Korea, and nearby markets. Beneath that top layer, Indian and Chinese manufacturers compete mainly on affordability, supply depth, and the ability to extend mature molecules into combination formats.

Strategic activity is now moving toward fixed-dose combinations, because that is where the Asia Pacific DPP-4 inhibitors market still offers room for differentiation. In October 2025, Hengrui’s subsidiary won approval for China’s first domestically developed triple fixed-dose combination, which shifted competition from single molecules toward platform products. In December 2025, CSPC followed with the world’s first clinically approved triple DPP-4, SGLT2, and metformin tablet, which raised the standard for combination-led lifecycle management. These moves show that the Asia Pacific DPP-4 inhibitors market is not relying only on generic copycat expansion, because companies are still trying to create new prescribing formats around established mechanisms.

Competitive positioning is also spreading across geographies, with regional manufacturers trying to use post-patent sitagliptin platforms to capture revenue beyond their home markets. Zydus Lifesciences reported first-cycle FDA approvals for Zituvio, Zituvimet, and Zituvimet XR in 2025, which strengthens its credibility as a scaled sitagliptin supplier. Clinical support for combination therapy remains relevant as well, and a 2025 systematic review found that SGLT2 inhibitor and DPP-4 inhibitor combinations improved glycemic control with stronger efficacy signals in Asian subpopulations. That evidence keeps the Asia Pacific DPP-4 inhibitors market commercially active, even though pricing pressure and guideline shifts continue to limit the class’s overall upside.

Asia Pacific Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Industry Leaders

AstraZeneca

Boehringer Ingelheim

Eli Lilly and Company

Merck and Co.

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Japan's Intellectual Property High Court upheld three Boehringer Ingelheim patents covering linagliptin (Tradjenta), rejecting invalidation challenges from generics maker Nipro and clarifying that drug patents can remain valid without direct experimental data for every claimed therapeutic use. The ruling maintains Boehringer Ingelheim's linagliptin exclusivity window in Japan, one of the class's most valuable branded markets.

- December 2025: CSPC received NMPA approval for the world's first triple DPP-4/SGLT2/metformin FDC: The prusogliptin–dapagliflozin–metformin combination tablet became the world's first clinically approved triple-drug combination integrating a DPP-4 inhibitor, an SGLT2 inhibitor, and a biguanide into a single oral dose, marking a significant formulation milestone for the entire class.

- October 2025: Hengrui received NMPA approval for China's first domestic triple FDC: Shandong Suncadia, a Hengrui subsidiary, secured approval for henagliflozin–retagliptin–metformin sustained-release tablets, the first oral triple FDC independently developed in China, marking a pivot from single-molecule competition to combination platform leadership.

Asia Pacific Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market Report Scope

The Asia Pacific Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market refers to the market for DPP-4 inhibitor medications used in the management of type 2 diabetes mellitus (T2DM) across countries in the Asia Pacific region. DPP-4 inhibitors are oral antidiabetic drugs that work by inhibiting the dipeptidyl peptidase-4 enzyme, thereby increasing incretin hormone levels, enhancing insulin secretion in a glucose-dependent manner, and reducing glucagon release to improve blood glucose control.

The Asia Pacific Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market is segmented based on drug type, medication type, distribution channel, and country. By drug type, the market is categorized into Sitagliptin, Saxagliptin, Linagliptin, Alogliptin, Vildagliptin, and other drug types, representing the key DPP-4 inhibitors used in the treatment of type 2 diabetes mellitus. Based on medication type, the market is divided into branded medications and generic medications, providing a range of treatment options that cater to varying patient preferences and healthcare budgets. By distribution channel, the market comprises hospital pharmacies, retail pharmacies, and online pharmacies, enabling broad access to DPP-4 inhibitors through institutional, community, and e-commerce healthcare channels. Geographically, the market is segmented into China, Japan, India, Australia, South Korea, and the Rest of Asia-Pacific

| Sitagliptin |

| Saxagliptin |

| Linagliptin |

| Alogliptin |

| Vildagliptin |

| Other Drug Types |

| Branded Medication |

| Generic Medication |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Drug Type | Sitagliptin |

| Saxagliptin | |

| Linagliptin | |

| Alogliptin | |

| Vildagliptin | |

| Other Drug Types | |

| By Medication Type | Branded Medication |

| Generic Medication | |

| By Distribution Channel | Hospital Pharmacies |

| Retail Pharmacies | |

| Online Pharmacies | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Asia Pacific DPP-4 inhibitors space by 2031?

It is forecast to reach USD 3.44 billion by 2031, rising from USD 2.49 billion in 2026 at a 3.53% CAGR over 2026-2031.

Which country leads regional revenue today?

China led the region in 2025 with 41.84% share, supported by broad prescribing depth, reimbursement reach, and strong policy influence on access.

Which country is growing the fastest through 2031?

India is projected to grow the fastest at a 3.27% CAGR through 2031, helped by its large diagnosed diabetes base and strong generic affordability.

Which drug type holds the largest position?

Sitagliptin remained the leading drug type in 2025 with 48.18% share, supported by long physician familiarity and broad use in combination strategies.

Why do DPP-4 inhibitors still matter despite GLP-1 and SGLT2 competition?

They remain relevant because of their oral format, low hypoglycemia risk, and continued fit in elderly patients, lower-risk therapy, and fixed-dose combinations.

Which sales channel is expanding the fastest?

Online pharmacies are expected to post the fastest channel growth at 5.05% CAGR through 2031, while retail pharmacies still held the largest channel share in 2025.

Page last updated on: