Asia-Pacific Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

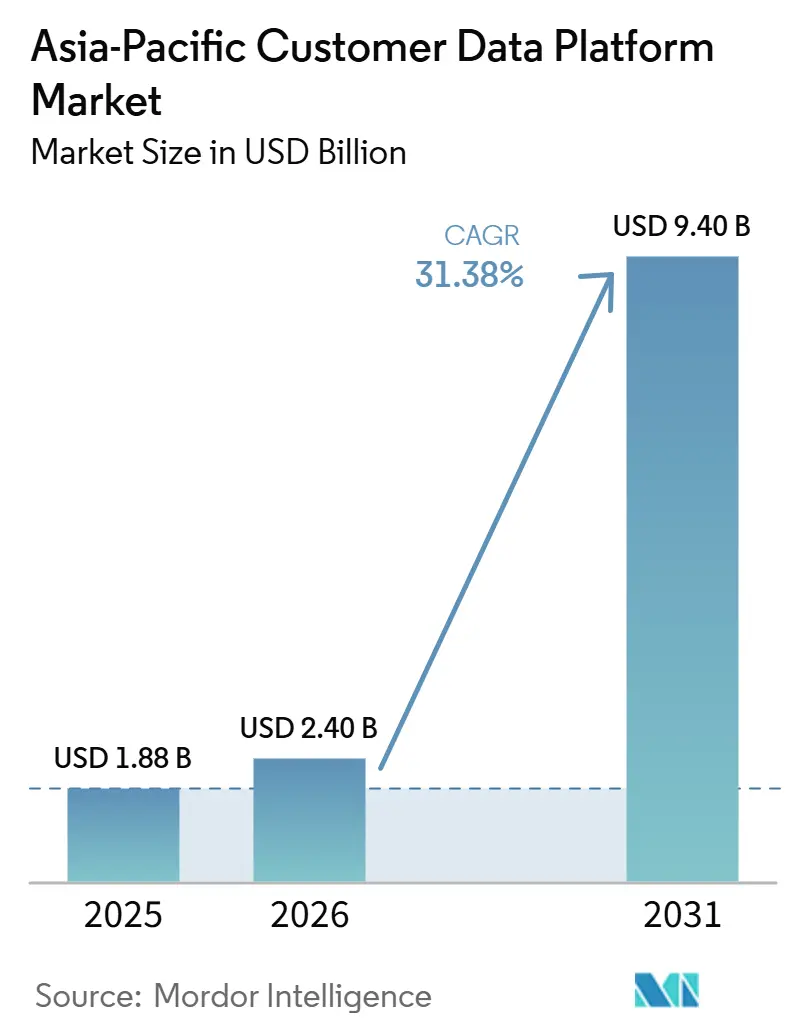

| Base Year Market Size (2025) | USD 1.88 Billion |

| Market Size (2026) | USD 2.40 Billion |

| Market Size (2031) | USD 9.40 Billion |

| Growth Rate (2026 - 2031) | 31.38% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Customer Data Platform Market Analysis by Mordor Intelligence

The Asia-Pacific customer data platform market size is expected to grow from USD 1.88 billion in 2025 to USD 2.40 billion in 2026 and is forecast to reach USD 9.40 billion by 2031 at 31.38% CAGR over 2026-2031. The region is moving through a fast enterprise adoption cycle as third-party data access weakens, AI-led personalization becomes more practical, and privacy rules become harder to defer. The Asia-Pacific customer data platform market is seeing its strongest demand in countries where mobile-first commerce, fragmented customer touchpoints, and digital-native operating models create a data unification problem that standard marketing clouds do not solve well. Competition centers on ecosystem depth, local hosting capabilities, and the ability to support country-specific operating needs, while specialist vendors are trying to stand out through tighter architecture and use-case fit. Growth is also being shaped by a widening overlap between CDP platforms and lakehouse-native activation tools, which is raising buyer scrutiny on product scope and long-term pricing. That pressure is likely to favor vendors that can separate core profile unification, identity resolution, and governed activation from front-end packaging.

Key Report Takeaways

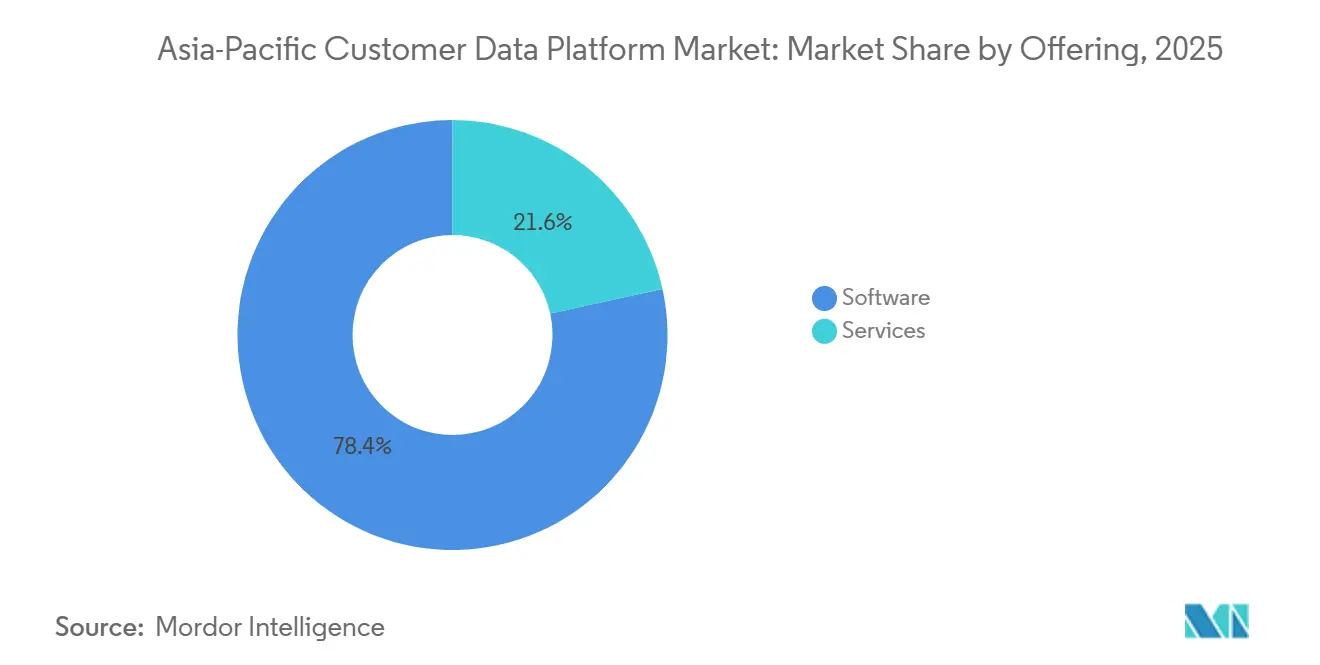

- By offering, software accounted for 78.43% of revenue in 2025, while services are projected to expand at a 33.74% CAGR through 2031.

- By deployment mode, cloud is projected to expand at a 34.28% CAGR through 2031 in the Asia-Pacific customer data platform market.

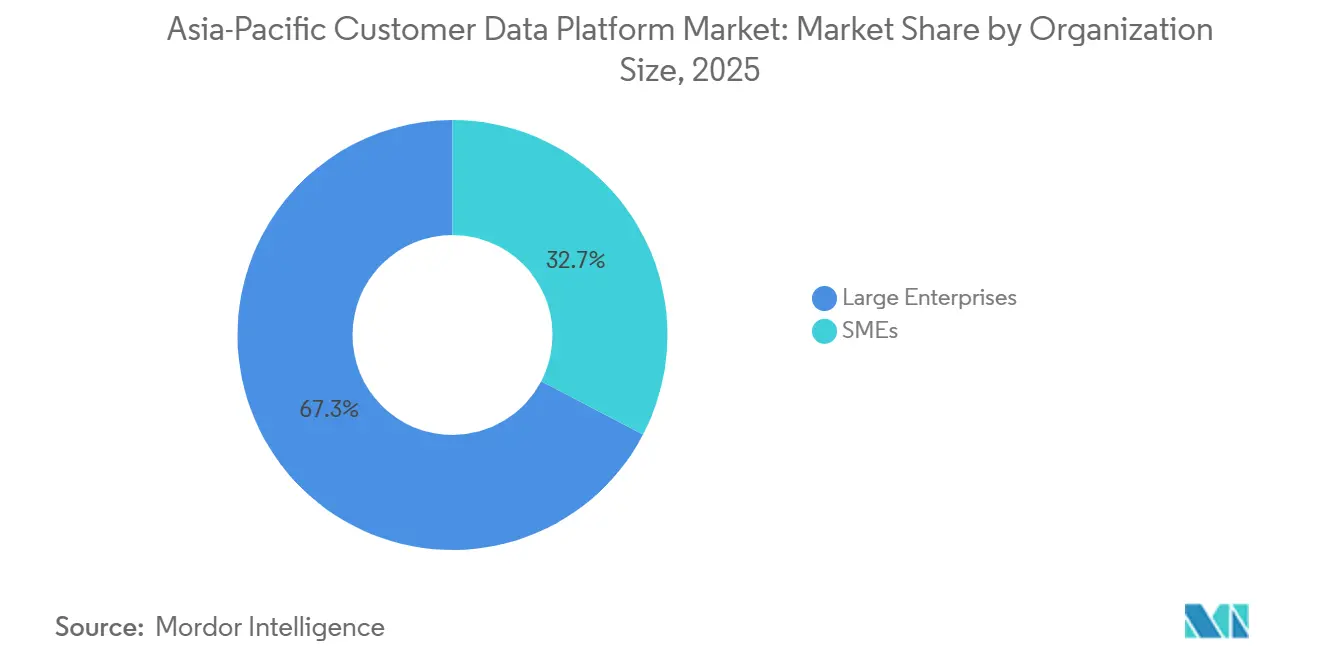

- By organization size, large enterprises accounted for 67.34% of revenue in 2025, while SMEs are projected to grow at a 35.21% CAGR through 2031.

- By application, Customer Data Collection and Profile Unification held 29.18% share in 2025, while Customer Analytics and Insights are projected to advance at a 35.69% CAGR through 2031.

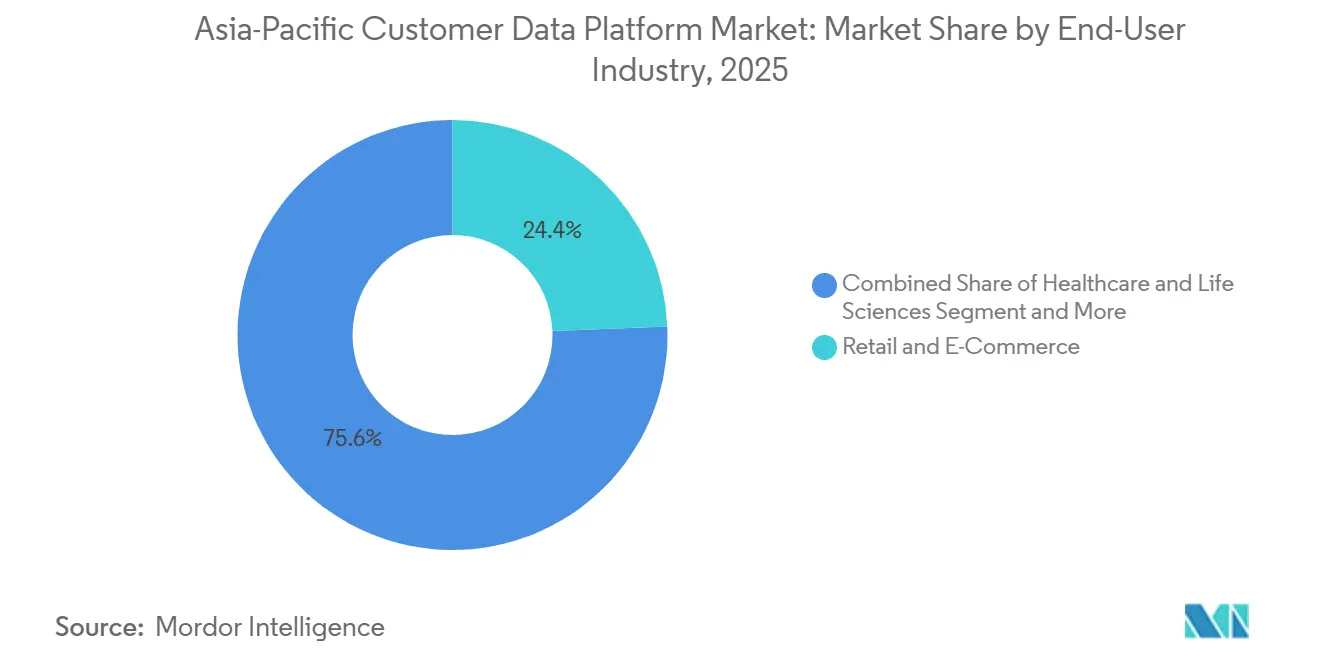

- By end-user industry, Retail and E-Commerce held 24.37% share in 2025, while Healthcare and Life Sciences are projected to expand at a 36.16% CAGR through 2031.

- By geography, China held 37.46% share in 2025, while India is projected to grow at a 37.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Unified First-Party Data Across Distributed Touchpoints | +8.2% | Global, concentrated in Asia-Pacific core, China, India, Southeast Asia, and Japan | Medium term (2-4 years) |

| Accelerating Shift to Privacy-First Customer Activation Architectures | +6.5% | China, India, ASEAN with spillover to Japan and South Korea | Short term (≤ 2 years) |

| Rapid Adoption of AI-Driven Identity Resolution and Propensity Modeling | +5.9% | Global, with intensity in Asia-Pacific retail and financial services enterprises | Medium term (2-4 years) |

| Composable CDP Adoption by Digital-Native Commerce Teams | +4.1% | India, Australia, Southeast Asia, and emerging in Japan | Medium term (2-4 years) |

| Growth of Real-Time Personalization Use Cases in High-Frequency Consumer Markets | +3.2% | Southeast Asia, India, and China across quick commerce, food delivery, and fintech super-apps | Short term (≤ 2 years) |

| Expansion of Local Data Residency Requirements Across Asia-Pacific | +2.3% | China, India, Indonesia, Vietnam, and Thailand | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand For Unified First-Party Data Across Distributed Touchpoints

First-party data is widely available across the region, but much of it remains separated across platforms and systems. A single customer may move across WeChat mini-programs in China, LINE in Japan and Thailand, Shopee and Lazada in Southeast Asia, and UPI-linked apps in India, with each environment producing different schemas and identity structures. That makes customer unification harder than it appears in standard software demonstrations. Many enterprises are increasing first-party data spending because the data already exists, but turning it into a usable customer profile still needs deeper integration work than many packaged tools provide. Companies that secure direct first-party data access through platform relationships gain a stronger behavioral view than competitors that still depend on paid media retargeting. This is one of the clearest demand drivers for the Asia-Pacific customer data platform market, as the unification layer is becoming operational infrastructure rather than a discretionary marketing tool.

Accelerating Shift To Privacy-First Customer Activation Architectures

Privacy compliance is now shaping data architecture decisions across the region. India’s Digital Personal Data Protection Rules, 2025, introduced an 18-month phased compliance window and required consent managers to be India-incorporated entities, prompting enterprises to examine in-country hosting and consent handling much earlier in their planning cycle.[1]Ministry of Electronics and Information Technology, India, “Digital Personal Data Protection Rules, 2025,” Government of India, pib.gov.in Enterprises operating across Singapore, Thailand, Indonesia, Vietnam, and India are dealing with a patchwork of local consent and data-handling requirements that cannot be managed effectively with a single generic configuration. Each added localization rule tends to raise per-enterprise spend because regional deployments, controls, and governance logic must be repeated. Salesforce expanded Hyperforce data residency for Data Cloud and Agentforce to Singapore as part of a USD 1 billion, five-year regional investment, underscoring how localization of infrastructure has become a core competitive requirement.[2]Salesforce, “Salesforce to Invest USD 1B in Singapore Over 5 Years,” Salesforce, salesforce.com The Asia-Pacific customer data platform market is benefiting from privacy and customer activation spending moving through the same buying process.

Rapid Adoption Of AI-Driven Identity Resolution And Propensity Modeling

Identity resolution in this region extends well beyond cookie matching. Many large consumer markets still combine digital engagement with offline transactions, leaving deterministic identity systems with significant blind spots. AI-based matching can combine loyalty IDs, hashed email variants, phone numbers, and device signals to build a more complete profile. Amperity said in April 2025 that one retail user of its Identity Resolution Agent surfaced 3.5 million previously unreachable customer email records through AI-driven probabilistic stitching.[3]Amperity, “Amperity Unveils Industry’s First Identity Resolution Agent, Accelerating AI Readiness for Enterprise Brands,” Amperity, amperity.com Adobe’s Customer AI applies propensity scoring to estimate purchase probability, churn, and engagement using behavioral customer data, demonstrating how identity and prediction are increasingly linked within the same workflow. This shift supports the Asia-Pacific customer data platform market, as enterprises seek greater profile accuracy and stronger activation logic without creating a separate compliance burden.

Composable CDP Adoption By Digital-Native Commerce Teams

Composable CDP models are changing the economics of deployment across the region. In this model, identity, segmentation, and activation logic sit on top of the customer’s cloud warehouse, rather than forcing profile data into a separate, proprietary store. That approach can make sense for mid-market retailers working across several countries when they already have warehouse investments in place. The tradeoff is that composable deployments still depend on capable engineers to manage connectors, dbt models, and activation pipelines over time. Twilio Segment released Warehouse Writeback and Warehouse Extraction Optimization to general availability in April 2026, and the company said the upgrades reduced median audience execution times by 80-90% across major warehouse environments.[4]Twilio, “New Advanced Audiences Features in Twilio Segment,” Twilio, twilio.com That progress makes the Asia-Pacific customer data platform market more accessible to digital-native teams in India, Australia, and Southeast Asia that want flexibility without giving up activation speed.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Burden Across Legacy CRM, ERP, and Commerce Stacks | -4.8% | Japan, South Korea, and large enterprises across Asia-Pacific | Long term (≥ 4 years) |

| Shortage of Reverse-ETL and Customer Data Engineering Talent | -3.9% | Global, with disproportionate pressure in Tier 2 Asia-Pacific markets | Medium term (2-4 years) |

| Privacy Enforcement Risk Under Fragmented National Data Laws | -2.6% | ASEAN markets with early-stage enforcement, Indonesia, Vietnam, and Thailand | Short term (≤ 2 years) |

| Vendor Overlap With Marketing Cloud and Data Warehouse-Native Tools | -1.8% | Global, with increasing pressure in Asia-Pacific enterprise segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Integration Burden Across Legacy CRM, ERP, And Commerce Stacks

The biggest barrier to deployment is often not budget. It is the amount of engineering work required to connect systems that were never designed to cleanly share customer-level data. Japan and South Korea still have large footprints in older ERP and CRM environments, which means custom connectors are often needed before unified profiles can be built. Those connectors create a maintenance burden that continues after deployment and often grows when upstream systems change. Multi-market implementations also need normalization across order schemas, marketplace adapters, real-time event handling, and a stable identity layer. This slows time-to-value and makes managed integration support more important for vendors serving the Asia-Pacific customer data platform market.

Shortage Of Reverse-ETL And Customer Data Engineering Talent

The region also faces a shortage of people capable of building and maintaining modern activation pipelines. Reverse-ETL and customer data engineering roles are central because these teams move unified profiles from the data layer into campaign, analytics, and customer experience tools. The shortage is pushing more enterprises toward managed service models because they cannot keep the full workflow stable with internal teams alone. CDP Institute reported in 2026 that 85% of organizations believed they still needed additional data engineers despite growing automation capabilities. Training pipelines across many markets have not kept up with the shift from basic SQL work toward event streaming, transformation frameworks, and lakehouse-native activation. This continues to slow composable adoption in the Asia-Pacific customer data platform market, especially in data-nascent markets where internal engineering depth is limited.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Anchors Demand While Services Gain Strategic Weight

Software accounted for 78.43% of revenue in 2025, making it the largest offering segment by a wide margin. That result reflects the common buying pattern in which enterprises license the platform first and then expand the implementation scope later. In the early stages of deployment, the software layer is still considered the core procurement decision because it controls identity logic, profile construction, segmentation, and activation rules. The Asia-Pacific customer data platform market maintained this software-heavy structure because many buyers were still formalizing their unification stacks before expanding their service commitments.

Services are projected to grow at a 33.74% CAGR through 2031, making them the fastest-growing offering category. That acceleration reflects the reality that many deployments need sustained support for integration, governance, model tuning, and local configuration after the initial contract is signed. Vendors are also bundling more professional services and managed activation into platform agreements as core software features become easier to compare across suppliers. In more mature countries such as China and Japan, this shift points to a later stage of adoption, where buyers spend less on first-time setup and more on ongoing optimization, model refinement, and cross-channel execution.

By Deployment Mode: Cloud Lifts Speed While Hybrid Preserves Control

The Asia-Pacific customer data platform market size for cloud deployment is projected to expand at a 34.28% CAGR through 2031. Cloud is gaining ground because many regional use cases depend on faster activation rather than simple infrastructure flexibility. Flash sales, quick commerce, food delivery, and app-led engagement are all reward systems that can move from event capture to audience action with very little delay. This makes cloud deployment attractive for operators that need consistent activation logic across multiple countries without duplicating infrastructure in each new market.

On-premises deployments still matter in regulated sectors such as healthcare and financial services, especially in Japan, South Korea, and Australia. These buyers often prefer tighter control over sensitive profile data, even while still wanting downstream activation in digital channels. Hybrid architecture is emerging as a practical middle path because it allows profile governance to remain close to the source while routing approved activation flows into real-time cloud channels. That structure fits well with the Asia-Pacific customer data platform market, as many enterprises are balancing strict internal controls with growing pressure to improve activation speed.

By Organization Size: Large Enterprises Lead While SME Momentum Builds

Large enterprises accounted for 67.34% of revenue in 2025, maintaining their lead by organization size. These companies have the scale, existing cloud contracts, engineering staff, and procurement leverage needed to absorb the cost and complexity of full deployment. They also tend to run broader channel portfolios, which increases the value of unified profiles and governed activation. In China and Japan, many large organizations have already moved beyond first deployment and are now focused on optimization, audience experimentation, and more advanced decisioning.

SMEs are projected to expand at a 35.21% CAGR through 2031, making them the fastest-growing segment. The biggest reason is that the cost barrier is easing as warehouse-native and composable approaches lower the need for a full proprietary stack. Direct-to-consumer brands, fintech platforms, and quick-commerce operators in India are especially relevant because they rely on event-driven retention and cross-sell workflows to protect unit economics. Even so, the growth path is not frictionless, because smaller organizations often still lack the engineering depth needed to capture the full value of deployment at speed.

By Application: Intelligence Moves Ahead Of Basic Data Unification

Customer Data Collection and Profile Unification accounted for 29.18% of revenue in 2025, making it the largest application segment. That result aligns with the stage of regional adoption, as many organizations still need to establish a reliable customer profile foundation before expanding into more advanced use cases. Initial deployments tend to focus on bringing data together across channels, matching identities, and making that unified profile accessible to downstream teams. This foundation remains essential because all subsequent use cases depend on profile accuracy and consistent customer identifiers.

The Asia-Pacific customer data platform market size for Customer Analytics and Insights is projected to expand at a 35.69% CAGR through 2031. This points to a shift from simply collecting and organizing data to generating predictions, prioritizing, and taking action from that data. Buyers that already built unified profiles in earlier deployment waves are now focusing more on churn prediction, next-best-action models, customer lifetime value scoring, and propensity-based segmentation. Audience segmentation, journey orchestration, and consent management remain important middle-tier use cases, but the faster momentum is clearly moving toward the intelligence layer because it is harder to replace and more closely tied to commercial results.

By End-User Industry: Retail Stays Largest While Healthcare Gains Fastest

Retail and E-Commerce held 24.37% of the Asia-Pacific customer data platform market share in 2025. The segment led because the link between unified profiles and commercial outcomes is direct in digital commerce, loyalty, and omnichannel conversion programs. Large retailers in the region are already using profile unification to connect point-of-sale and online behavior, improve cross-sell models, and trigger real-time cart recovery. In high-cash markets, the next stage of value comes from reconnecting offline shoppers to digital identities so that personalization can extend beyond known online users.

Healthcare and Life Sciences are projected to expand at a 36.16% CAGR through 2031, which makes them the fastest-growing end-user group. Salesforce said in May 2025 that Takeda selected Life Sciences Cloud for Customer Engagement and deployed Data Cloud and Agentforce to support consent-governed personalized outreach to healthcare professionals.[5]Salesforce, “Takeda Selects Salesforce Life Sciences Cloud for Customer Engagement,” Salesforce, salesforce.com That example matters because it shows how profile precision is becoming useful well beyond consumer commerce. BFSI, IT and Telecom, Media and Entertainment, Industrial Manufacturing, and Government and Public Administration also remain important, with BFSI standing out for governance complexity and IT and Telecom standing out for very high event data volume.

Geography Analysis

China held 37.46% of the Asia-Pacific customer data platform market share in 2025, while India is projected to grow at a 37.82% CAGR through 2031. China remains the largest national market because its digital ecosystems generate immense volumes of first-party data across commerce, payments, and super-app activity. That scale supports bigger deployment opportunities and deeper localization needs than most regional peers. India is growing faster because UPI-linked payments, quick commerce, and direct-to-consumer activity are producing large event streams that legacy CRM structures were not built to manage. India’s Digital Personal Data Protection Rules, 2025, introduced an 18-month phased compliance window, prompting enterprises to review their consent architecture and hosting models more urgently. Salesforce also announced in May 2026 that MuleSoft on Hyperforce in India would support local data residency, which shows how global vendors are now treating India as a dedicated in-country infrastructure market.

Japan remains one of the most technically mature markets in the region. Demand there is supported by sophisticated customer engagement priorities, even though older enterprise system footprints make implementation harder. South Korea is also important because AI governance reviews are prompting enterprises to reassess how personal data flows through AI-enabled systems. Australia serves as an important regional proving ground for Western vendors. Adobe announced Real-Time CDP Collaboration in Australia and New Zealand in May 2025, with publisher partners including News Corp Australia, Carsales, Nine, SBS, and Singapore. Singapore continues to act as a regional operating anchor. Salesforce said in 2025 and 2026 that it was expanding local data residency and AI operations there through Hyperforce and new data and AI programs.

ASEAN is the high-velocity growth frontier within the Asia-Pacific customer data platform market. Indonesia, Vietnam, Thailand, and the Philippines are seeing digital customer behavior expand faster than the capacity for enterprise data governance, creating clear demand for profile unification. Regional operators are increasingly using multi-country deployment models that can begin in one market and then scale as governance and channel maturity improve elsewhere. The main near-term constraint is uneven enforcement across local privacy regimes, which means deployment timing can vary even when commercial demand is strong.

Competitive Landscape

The Asia-Pacific customer data platform market remained moderately fragmented at the platform layer, with Salesforce Data Cloud, Adobe Real-Time CDP, and Oracle Unity CDP holding the strongest enterprise positions. Specialist vendors such as Tealium, Amperity, Bloomreach, RudderStack, and Lexer compete less on scale and more on architecture fit, use-case depth, and regional configurability. Consolidation in 2024 and 2025 narrowed the room for independent mid-tier suppliers as Rokt acquired mParticle, Uniphore acquired ActionIQ, and Contentstack acquired Lytics. These transactions strengthened bundle economics and gave larger platforms greater scope to combine activation, analytics, and broader customer experience tools into a single commercial package. Salesforce reinforced its regional position through a USD 1 billion five-year investment in Singapore that expanded Hyperforce data residency for Data Cloud and Agentforce.

A more disruptive shift is coming from data infrastructure platforms that are moving directly into CDP functionality. Bloomreach announced in June 2026 that it was a launch partner for Databricks CustomerLake, which connected Bloomreach’s Loomi marketing agent with unified profiles inside the Databricks lakehouse. That kind of design eliminates duplication between the data platform and the activation layer, reducing latency and simplifying governance. Adobe also deepened its regional presence by launching Real-Time CDP Collaboration in Australia and New Zealand for advertisers and publishers using first-party audience workflows. For the Asia-Pacific customer data platform market, this means standalone vendors now face pressure both from above, through enterprise suites, and from below, through lakehouse-native activation tools.

The clearest white space remains in the middle market. Many organizations are ready for composable or hybrid architectures, but they still need managed integration support to connect legacy commerce, CRM, and consent systems. Enterprise suites remain strongest where buyers want deeper CRM and marketing cloud alignment, while specialists keep an opening where governed activation, architecture flexibility, or sector-specific implementation matter more. Competition is likely to stay active because differentiation now depends less on collecting more data and more on how quickly vendors can unify, govern, and activate it under regional operating constraints.

Asia-Pacific Customer Data Platform Industry Leaders

Salesforce, Inc.

Oracle Corporation

Adobe Inc.

SAP SE

Twilio Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Bloomreach announced a strategic partnership with Databricks on June 16, 2026, as the launch partner for Databricks CustomerLake, a new agentic CDP. The integration connects Bloomreach's Loomi marketing agent with unified customer profiles in the Databricks lakehouse, enabling a direct path from governed enterprise data to real-time personalized execution across email, web, and messaging channels without data duplication or additional silos.

- May 2026: Salesforce announced the upcoming availability of MuleSoft Anypoint Platform on Hyperforce in India on May 19, 2026, bringing local data residency and AI governance to integrations for Indian enterprises in regulated sectors including financial services, healthcare, and public administration. The release includes MuleSoft Agent Fabric and Omni Gateway for unified governance across APIs, AI agents, and large language models within India's geographic borders.

- May 2026: Tealium unveiled AI at the Edge and AI Decisioning features on May 7, 2026, extending its AI Partner Ecosystem with in-platform capabilities for real-time customer decisioning at millisecond latency. The features allow enterprises to apply AI models at the data collection layer itself, reducing round-trip latency for time-sensitive activation use cases in retail, e-commerce, and financial services.

- April 2026: Twilio Segment released Warehouse Writeback and Warehouse Extraction Optimization to general availability in April 2026, enabling audience entry and exit events to sync back to Snowflake, BigQuery, Databricks, and Redshift, and reducing median audience execution times by 80-90% through lean extraction processing.

Asia-Pacific Customer Data Platform Market Report Scope

The Asia-Pacific Customer Data Platform Market is Segmented by Offering (Software and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises and SMEs), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, and more), End-User Industry (Retail and E-Commerce, IT and Telecom, and more), and Country. The Market Forecasts are in Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| SMEs |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| China |

| Japan |

| India |

| South Korea |

| Australia |

| ASEAN |

| Rest of Asia-Pacific |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| SMEs | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| BFSI | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries | |

| By Country | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| ASEAN | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the size of the Asia-Pacific customer data platform market?

The Asia-Pacific customer data platform market was valued at USD 1.88 billion in 2025, reached USD 2.40 billion in 2026, and is forecast to reach USD 9.40 billion by 2031 at a 31.38% CAGR.

Which country leads regional demand and which one is growing the fastest?

China held the largest share at 37.46% in 2025, while India is projected to post the fastest growth at a 37.82% CAGR through 2031.

Which application area is expanding the fastest across the region?

Customer Analytics and Insights is the fastest-growing application, with a projected 35.69% CAGR through 2031, showing that buyers are moving from data collection toward prediction and activation.

Why are privacy rules becoming such a major buying trigger in this space?

Local consent and hosting rules are pushing enterprises to redesign data architecture, especially in India and Southeast Asia, so privacy spending is increasingly tied to customer activation spending.

Which end-user group is creating the strongest near-term revenue opportunity?

Retail and E-Commerce remained the largest end-user segment at 24.37% share in 2025, while Healthcare and Life Sciences is projected to grow fastest at a 36.16% CAGR.

Page last updated on: