Asia-Pacific Automotive Reed Sensors Switches Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

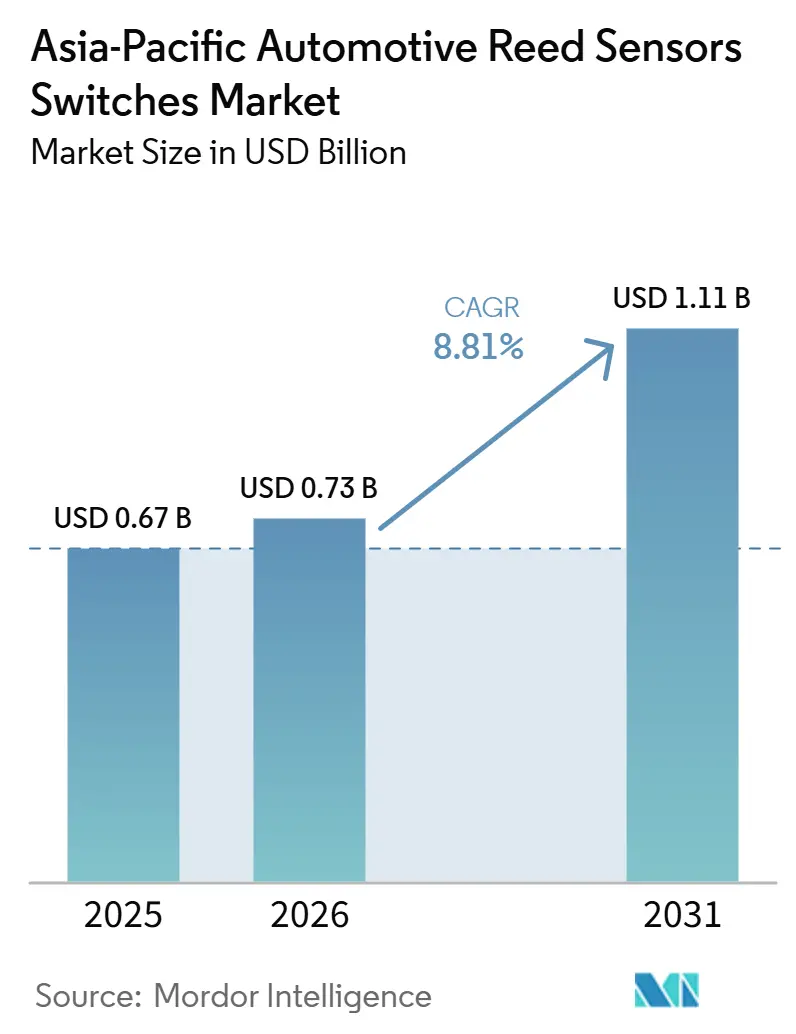

| Base Year Market Size (2025) | USD 0.67 Billion |

| Market Size (2026) | USD 0.73 Billion |

| Market Size (2031) | USD 1.11 Billion |

| Growth Rate (2026 - 2031) | 8.81% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Automotive Reed Sensors Switches Market Analysis by Mordor Intelligence

The Asia-Pacific automotive reed switches market size is projected to expand from USD 0.67 billion in 2025 to USD 0.73 billion in 2026, and to USD 1.11 billion by 2031, registering a CAGR of 8.81% between 2026 and 2031. Electrification is increasing the number of sensing points in battery packs, charging inlets, and high-voltage circuits. The region also retains a large base of conventional vehicles that supports demand in body electronics and fluid-level sensing. Suppliers are balancing cost pressure from local manufacturers with the need to qualify advanced components for electric vehicle platforms. Battery and charging applications offer a clearer route to higher-value demand than mature body-electronics positions. The Asia-Pacific automotive reed switches market, therefore, depends on continued vehicle production, reliable deployment of charging infrastructure, and suppliers' access to OEM design programs.

Key Report Takeaways

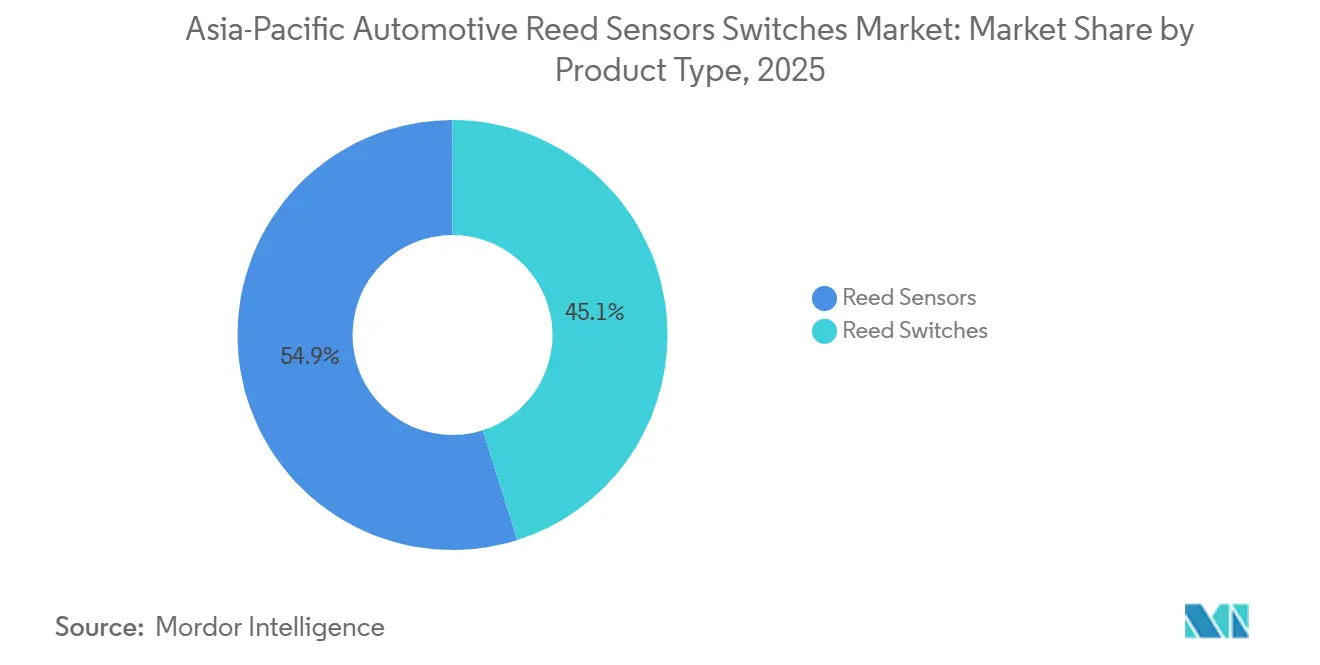

- By product type, reed switches held 54.89% of the Asia-Pacific automotive reed sensors switches market share in 2025, while reed sensors are forecast to grow at a 10.54% CAGR through 2031.

- By application, body electronics accounted for 27.61% of the Asia-Pacific automotive reed sensors switches market share in 2025, while battery and charging systems are forecast to advance at a 14.24% CAGR through 2031.

- By application, body electronics accounted for 27.61% of the Asia-Pacific automotive reed sensors switches market share in 2025, while battery and charging systems are forecast to advance at a 14.2% CAGR through 2031.

- By sales channel, OEMs held 82.83% revenue share in 2025 and are projected to expand at a 9.24% CAGR through 2031.

- By propulsion type, ICE vehicles held 43.27% revenue share in 2025, while battery electric vehicles are forecast to grow at a 15.24% CAGR through 2031.

- By geography, China held 59.89% revenue share in 2025, while the Rest of Asia-Pacific is forecast to grow at a 21.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Automotive Reed Sensors Switches Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| China-Driven Volume Scale | +1.6% | China (Spillover To APAC) | Short term (≤ 2 years) |

| Emerging APAC EV Acceleration | +1.3% | India + SEA + Oceania | Short term (≤ 2 years) |

| Charging Ecosystem Expansion | +1.1% | Urban + Highway Corridors | Short term (≤ 2 years) |

| Passenger Car Production Base | +0.9% | Pan-APAC | Medium term (2-4 years) |

| Commercial Fleet Electrification | +0.7% | China + India + SEA | Medium term (2-4 years) |

| OEM Localization And Cost-Down | +0.5% | Key Manufacturing Hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

China’s NEV Scale Accelerates EV-Linked Sensing Demand

China's new-energy vehicle sales have reached significant volumes, representing nearly half of total vehicle sales. This scale is driving demand for switching components in battery management, isolation monitoring, and high-voltage disconnect systems. Battery-electric vehicles account for the majority of China's NEV mix, according to the Oxford Institute for Energy Studies[1]“China New Energy Vehicle Update: A Slowdown and Shift to Battery-Electric Vehicles,” Oxford Energy Comment, oxfordenergy.org.. Each battery-electric platform requires additional sensing functions beyond those used in conventional vehicles. China's expanding NEV exports are also extending the use of regionally assembled components into overseas vehicle programs. Qualification against automotive standards and IATF 16949 requirements remains important for suppliers seeking domestic OEM business.

Emerging APAC Markets Are Posting High-Growth EV Adoption From a Smaller Base

Electric car sales outside China in the Asia-Pacific region have risen significantly year over year, according to the International Energy Agency. This pace indicates that electric vehicle adoption is expanding across several secondary manufacturing and sales markets. India has reported substantial EV sales growth, with market penetration increasing steadily [2]“Global EV Outlook 2026 Executive Summary,” International Energy Agency, iea.org..

Thailand has registered a notable number of battery-electric vehicles, with electric vehicles accounting for a growing share of new-car sales. Indonesia's zero-emission passenger-car sales have also crossed a significant threshold, according to the International Council on Clean Transportation. These trends are increasing demand for low-cost sensing components used in volume vehicle platforms.

Charging Infrastructure Programs Strengthen the EV Ramp and Charging-Module Ecosystem

Charging infrastructure creates demand for sensing components beyond the vehicle itself. India's PM E-Drive scheme allocated funds for public charging stations, targeting tens of thousands of fast chargers, with a portion of the funds already approved. Thailand and Indonesia are also developing charging networks to support broader electric vehicle adoption. Charging inlet assemblies can require interlocks for shock and tilt detection. These installations represent a separate source of demand for the Asia-Pacific automotive reed switches market, alongside vehicle production.

Large Passenger-Vehicle Base Sustains Body-Electronics Demand While EV Grows

Passenger vehicles accounted for the largest share of the vehicle-type segment. The installed base supports demand for door latches, window actuators, seat sensors, seat-belt interlocks, and fluid-level gauges. A conventional or hybrid passenger vehicle can use a significant number of reed sensing points across these functions.

Hybrid and plug-in hybrid vehicles retain many legacy sensing positions while adding battery and motor-isolation functions. Some electric vehicle designs consolidate body sensing through domain controllers. Sustained OEM design engagement is therefore more important than vehicle-volume exposure alone for the Asia-Pacific automotive reed switches market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Solid-State Sensor Substitution | -1.3% | Pan-APAC | Medium term (2-4 years) |

| Policy Volatility Across Markets | -1.0% | Rest Of APAC | Short term (≤ 2 years) |

| Uneven Charging Reliability | -0.7% | Emerging APAC | Medium term (2-4 years) |

| Localization Compliance Burden | -0.5% | Key Manufacturing Hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Substitution Pressure From Solid-State Sensors in Some Use Cases

Hall-effect and tunneling magnetoresistance integrated circuits are increasingly used in steering-column, pedal-position, and transmission-speed sensing. These applications require diagnostics and functional-safety performance that discrete reed switches cannot provide on their own. Melexis introduced a programmable device capable of detecting multiple positions in door and e-latch systems.

Substitution remains limited in battery-sleep interlocks, high-voltage disconnect circuits, and fluid-level sensing. Reed components maintain galvanic isolation at high-voltage thresholds and operate without quiescent current draw in the cited design context. The Asia-Pacific automotive reed switches market faces pressure in select body-electronics nodes while demand remains in applications with strict isolation requirements.

Policy and Market Corrections Can Re-Sequence Near-Term Ramps

Changes to electric vehicle incentives can alter the timing of vehicle and component orders. China's NEV purchase-tax framework encouraged demand ahead of an earlier policy deadline. Thailand revised its EV3 and EV3.5 terms to support export-oriented manufacturers. Such adjustments can reduce visibility for suppliers supporting new vehicle programs.

Reed suppliers with qualifications across multiple countries can reduce exposure to a single subsidy schedule. They can also maintain business in conventional vehicle applications while electric vehicle production plans change.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reed Switches Lead; Reed Sensors Expand Faster

Reed switches held 54.89% of product-type value in 2025, while reed sensors are forecast to grow at a 10.54% CAGR through 2031. Reed sensors are gaining use because electric vehicle systems require integrated sensing assemblies rather than bare glass-tube switches.

The Asia-Pacific automotive reed switches market continues to rely on reed switches for high-volume body-electronics positions. China, India, Japan, and South Korea have large conventional vehicle fleets that support this use. Zero standby current and hermetic sealing remain valuable in moisture-prone door and fluid-level applications. Reed sensors are generally used in battery-state detection, cooling monitoring, and isolation circuits with tighter reliability specifications. This mix supports a shift toward higher-value components without eliminating demand for basic switches. Nippon Aleph identifies IATF 16949 quality management credentials for automotive applications, including safety-related uses. Established qualification requirements can limit access for suppliers that compete only on unit price.

By Application: Body Electronics Anchor Demand; Battery and Charging Systems Drive Growth

Battery and charging systems are forecast to grow at a 14.2% CAGR from 2026 to 2031. The segment benefits from battery-state sensing, isolation monitoring, and charging-inlet interlocks on each new battery-electric platform. Body electronics held the largest application share at 27.6% in 2025. It includes familiar positions in doors, seats, windows, latches, and safety circuits. It also faces more direct replacement risk from solid-state devices in e-latch and multi-position door functions. The Asia-Pacific automotive reed switches market size for battery and charging applications rises as vehicle electrification adds high-voltage sensing needs.

Engine and powertrain systems, safety and security systems, and transmission and braking systems remain established mid-tier applications. These functions retain reed switch components where price, design history, and qualification requirements favor existing solutions. Infotainment and comfort systems represent a smaller application area, with demand linked to vehicle equipment levels. Battery and charging systems offer a more favorable growth profile compared to mature body electronics positions. A supplier focused on body electronics may face pressure on pricing and volume as solid-state alternatives displace reed switches. A supplier qualified for battery and charging systems is better positioned to serve new platform programs. According to the ICCT, battery-electric heavy trucks have captured a significant sales share in China, with adoption continuing to grow. Heavy-truck battery packs require isolation and condition-monitoring components that increase sensing content per vehicle. Application mix, therefore, shapes supplier exposure within the Asia-Pacific automotive reed switches market.

By Vehicle Type: Passenger Cars Dominate; Commercial Vehicles Grow Faster

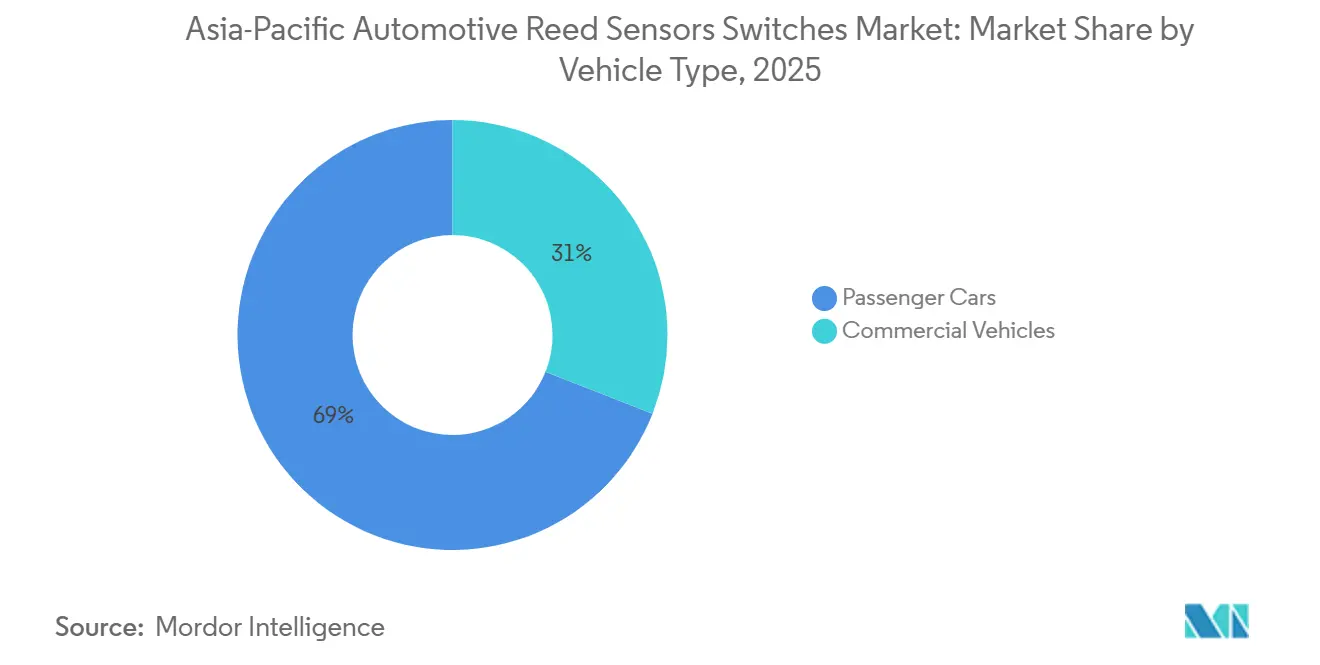

Passenger vehicles accounted for 69.03% of vehicle-type value in 2025, while commercial vehicles are forecast to grow at a 9.74% CAGR through 2031. Electrification programs in China and India support growth in commercial vehicles. China’s new-energy heavy-duty trucks reached 29% sales penetration in 2025 in the supplied material. Monthly penetration reached a majority share within the recent review period. China has set a NEV penetration target for this vehicle category within the coming decade. These programs are increasing the demand for battery isolation and monitoring components.

India's electric commercial vehicle sales rose significantly year over year, according to recent data. Electric commercial vehicles accounted for a notable share of India's total commercial vehicle sales during that period. India is also expected to deploy a large number of electric buses within the coming years. Passenger cars still account for most value due to China's large passenger fleet and India's growing car base. Commercial electric trucks and buses require more reed sensing positions than passenger cars. Battery-pack isolation, cooling-circuit fluid detection, and high-voltage disconnection increase component content per vehicle. Early OEM qualification in buses and heavy trucks can create durable supplier relationships. These applications have lower exposure to solid-state substitution than body-electronics positions. The Asia-Pacific automotive reed switches market stands to benefit as commercial electrification advances alongside passenger-vehicle production.

By Sales Channel: OEMs Dominate and Remain the Primary Growth Engine

OEMs held 82.83% of sales-channel value in 2025 and are projected to record a 9.24% CAGR through 2031. Reed components are typically selected through vehicle-platform design and qualification processes. This makes OEM programs more important than short-term spot purchases. OEM qualification includes component performance, manufacturing consistency, price, and local supply capability. The aftermarket is smaller because hermetically sealed switches can have long service lives. Replacement demand is also lower than it is for components that wear through mechanical contact. OEM purchasing, therefore, remains the central route to volume in the Asia-Pacific automotive reed switches market.

Chinese NEV manufacturers are increasing localization requirements for their supplier bases. These requirements can favor companies with domestic engineering and production facilities. Thailand’s EV3.5 program also ties incentives to domestic production conditions in the supplied material. Global manufacturers must demonstrate local supply-chain credentials to retain platform qualifications in Thai vehicle programs. The aftermarket remains relevant in India and Indonesia because both markets have large and aging vehicle populations. Door latches, fluid-level systems, and safety interlocks can require replacement components during the service life of conventional vehicles. Fragmented distribution channels support this replacement activity. However, the long replacement cycle limits aftermarket growth relative to OEM demand. Channel access will remain tied to supplier qualification and localization decisions across the Asia-Pacific automotive reed switches market.

By Propulsion Type: ICE Anchors the Base; BEVs Drive Incremental Growth

ICE vehicles held 43.27% of the propulsion-type value in 2025, while battery-electric vehicles are forecast to grow at a 15.24% CAGR through 2031. Battery-electric growth reflects wider adoption across China, India, Thailand, Indonesia, and Vietnam. China’s battery-electric vehicles represented a significant share in 2025. Conventional vehicles will continue to contribute revenue throughout the forecast period as the regional fleet changes gradually. Their body-electronics and fluid-level functions retain established reed switch positions. The Asia-Pacific automotive reed switches market must therefore serve both legacy and electric powertrains.

Hybrid and plug-in hybrid platforms retain an internal-combustion sensing set while adding battery-isolation and charging-monitoring functions. This can raise the reed content per vehicle during the transition to fully electric transport. Fuel-cell vehicles remain in their early stages in the region. They may use reed relays for hydrogen refueling valves and for isolation monitoring, similar to battery systems. Japan and South Korea remain relevant early-adopter locations for these applications. Battery-electric platforms also operate near high-current inverters and motor drives. The supplied material cited a 2025 patent application describing directed activation and shielding to reduce stray-field effects. These designs can help support switching reliability in dense electromagnetic environments. Propulsion changes are therefore altering both the number and specification of components required by the Asia-Pacific automotive reed switches market.

Geography Analysis

China held 59.89% of the Asia-Pacific automotive reed switches market share in 2025. Its scale makes it the region’s central hub for vehicle production and electric-vehicle demand. NEV unit sales have grown significantly in recent periods. Chinese OEMs such as BYD, Geely, and Changan have large component purchasing requirements and favor domestic supplier qualification, which shifts pricing leverage toward local manufacturers. Zhejiang Xurui Electronic, Kunshan Golden Light Electronic, and Ningbo Huaxing Sensor Tech compete for these domestic programs. China's heavy-truck electrification target adds further demand for battery-related sensing. Local standards and content requirements influence which suppliers gain OEM design access.

The Rest of Asia-Pacific is forecast to grow at a 21.8% CAGR through 2031. Thailand, Indonesia, Vietnam, and Australia each add different forms of electric vehicle demand. Thailand’s local production incentives encourage in-country component sourcing. Indonesia’s electric vehicle policy and battery supply-chain expansion support proximity demand for sensing components. Vietnam’s high electric vehicle penetration increases sensing demand despite its smaller overall vehicle base. Australia remains smaller, but fleet electrification and charging investment support gradual growth. Regional expansion gives suppliers opportunities outside China but also requires local manufacturing, qualification, and distribution capacity.

Competitive Landscape

Competition in the Asia-Pacific automotive reed sensors and switches market is defined by stringent automotive qualification requirements, including resistance to temperature cycling, vibration, and long-life operating conditions. OEMs and Tier-1 suppliers prioritize components that can deliver consistent performance over extended service life, particularly in high-volume body electronics and safety-related applications. Compliance with automotive standards and proven field reliability remain baseline requirements for supplier participation across regional platform programs.

Miniaturization and surface-mount readiness are increasingly important competitive differentiators as electronics modules become denser and more integrated. Demand is shifting toward compact, automotive-grade packages that support automated assembly and stable manufacturability. At the same time, the accelerating shift toward electrified architectures increases demand in battery and charging-related applications, where reliability and packaging efficiency are critical. Given the region’s OEM-heavy channel mix and localization expectations across multiple Asia-Pacific markets, suppliers with strong Tier-1 relationships, program support capabilities, and regional manufacturing alignment are better positioned to secure and sustain design wins over the forecast period.

Asia-Pacific Automotive Reed Sensors Switches Industry Leaders

Standex Electronics

Coto Technology

Littelfuse Inc.

TE Connectivity Ltd.

PIC GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Standex announced participation at Electronica India 2025 (Bengaluru), explicitly highlighting reed switches & sensors and fluid/level sensors—a relevant go-to-market signal for automotive-adjacent sensing/switching demand tied to India’s growing electronics design/manufacturing base.

- September 2025: Pickering Electronics announced it will showcase high-voltage customizable reed relays at SEMICON Taiwan 2025 (Taipei)—another indicator of continued innovation in reed-based switching used in semiconductor test environments that intersect with automotive electronics qualification.

Asia-Pacific Automotive Reed Sensors Switches Market Report Scope

Automotive reed sensors and reed switches are magnetically actuated switching/sensing components used to detect position, proximity, presence, or limit states in vehicle systems. Reed switches typically use hermetically sealed contacts actuated by a magnetic field, while reed sensors generally package the reed element into application-ready formats (e.g., molded housings or SMD-friendly packages) suited to module integration.

The scope includes segmentation by Product Type (Reed Switches and Reed Sensors), Application (Body Electronics, Battery and Charging Systems, and Others), Vehicle Type (Passenger Cars and Commercial Vehicles), Sales Channel (OEMs and Aftermarket), Propulsion Type (Internal Combustion Engine (ICE) Vehicles, Hybrid Electric Vehicles (HEV), Plug-in Hybrid Electric Vehicle (PHEV), Battery Electric Vehicles (BEV), and Fuel Cell Electric Vehicles (FCEV)), and Country(China, India, Japan, South Korea, Australia, Thailand, Indonesia, and Rest of Asia-Pacific). The market forecasts are provided in terms of value (USD).

| Reed Sensors |

| Reed Switches |

| Engine and Powertrain Systems |

| Body Electronics |

| Safety and Security Systems |

| Infotainment and Comfort Systems |

| Transmission and Braking Systems |

| Battery and Charging Systems |

| Other Applications |

| Passenger Cars |

| Commercial Vehicles |

| OEMs |

| Aftermarket |

| Internal Combustion Engine (ICE) Vehicles |

| Hybrid Electric Vehicles (HEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Battery Electric Vehicles (BEV) |

| Fuel Cell Electric Vehicles (FCEV) |

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Thailand |

| Indonesia |

| Rest of Asia-Pacific |

| Segmentation by Product Type (Value, USD) | Reed Sensors |

| Reed Switches | |

| Segmentation by Application (Value, USD) | Engine and Powertrain Systems |

| Body Electronics | |

| Safety and Security Systems | |

| Infotainment and Comfort Systems | |

| Transmission and Braking Systems | |

| Battery and Charging Systems | |

| Other Applications | |

| Segmentation by Vehicle Type (Value, USD) | Passenger Cars |

| Commercial Vehicles | |

| Segmentation by Sales Channel (Value, USD) | OEMs |

| Aftermarket | |

| Segmentation by Propulsion Type (Value, USD) | Internal Combustion Engine (ICE) Vehicles |

| Hybrid Electric Vehicles (HEV) | |

| Plug-in Hybrid Electric Vehicle (PHEV) | |

| Battery Electric Vehicles (BEV) | |

| Fuel Cell Electric Vehicles (FCEV) | |

| Segmentation by Country (Value, USD) | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Thailand | |

| Indonesia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is driving demand for automotive reed switches in Asia-Pacific?

Vehicle electrification increases demand in battery packs, charging inlets, isolation monitoring, and high-voltage disconnect systems.

What is the projected growth rate through 2031?

The Asia-Pacific automotive reed switches market is forecast to grow at an 8.83% CAGR from 2026 to 2031.

Why do reed switches remain relevant in electric vehicles?

They provide galvanic isolation and zero quiescent current draw in functions such as battery-sleep interlocks and fluid-level sensing.

How are solid-state sensors affecting reed switch suppliers?

They replace reed components in selected body-electronics functions, while reed technology remains useful in isolation-sensitive applications.

Which country has the largest regional demand base?

China held 59.89% of regional value in 2025 and has the largest electric vehicle production scale.

Page last updated on: