Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 10.90 Billion |

| Market Size (2026) | USD 11.35 Billion |

| Market Size (2031) | USD 14.60 Billion |

| Growth Rate (2026 - 2031) | 5.17% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Alfalfa Market Analysis by Mordor Intelligence

The Asia Pacific alfalfa market size is anticipated to grow from USD 10.90 billion in 2025 and USD 11.35 billion in 2026 to reach USD 14.60 billion by 2031 at a 5.17% CAGR from 2026 to 2031. The 2025 base reflected a structural rise in contracted commercial procurement, not a short-lived price spike, which shows that the Asia Pacific alfalfa market is becoming more organized on the demand side. Large dairy farms in China remain the main force behind regional demand because they are raising per-cow productivity targets faster than domestic forage supply can keep up, while India is adding a second source of demand through the steady expansion of organized dairy cooperatives. The Asia Pacific alfalfa market is also changing at the product level, as pellets and other processed formats are gaining space in long-haul trade because they travel better, store better, and fit automated feeding systems more easily. Competitive behavior is moving toward multi-origin sourcing, certified processing, and traceable supply chains, while water stress, freight volatility, and slow varietal commercialization continue to limit how quickly new supply can enter the Asia Pacific alfalfa market.

Key Report Takeaways

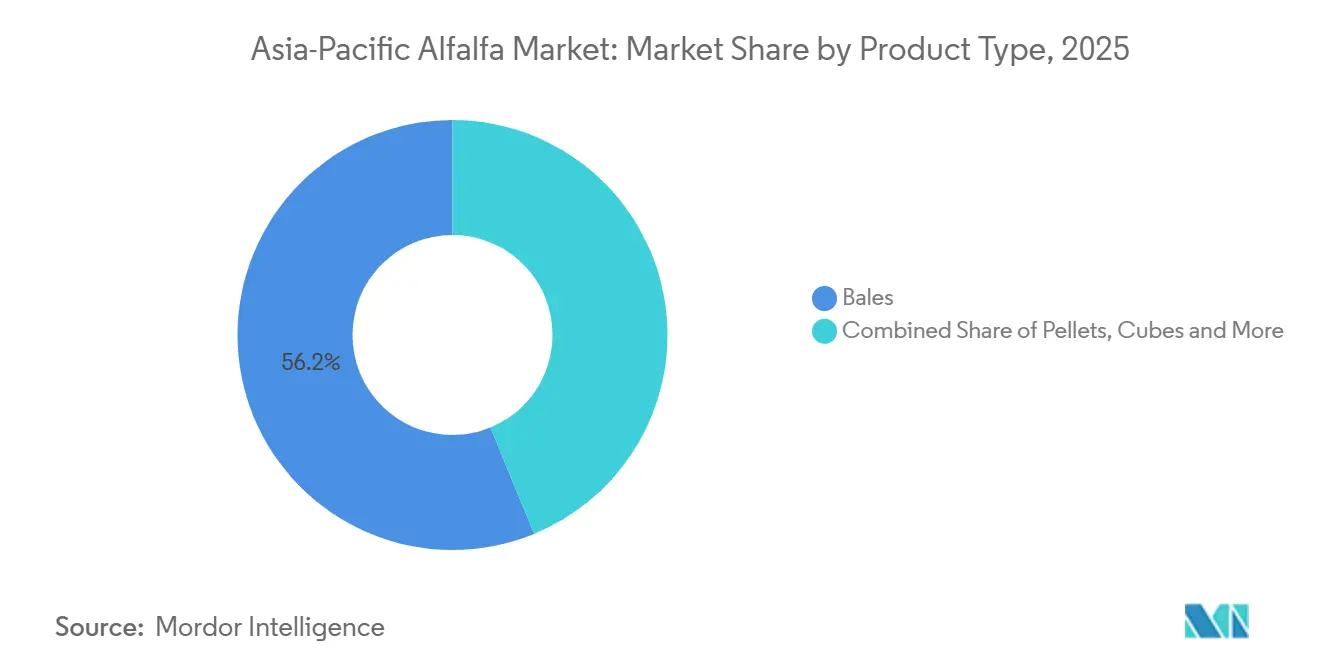

- By product type, bales accounted for 56.2% of the Asia Pacific alfalfa market share in 2025, while pellets are estimated to grow at the fastest CAGR of 7.4% between 2026 and 2031.

- By application, dairy cattle feed accounted for 49.5% share of the Asia Pacific alfalfa market size in 2025, while equine feed is anticipated to expand at a CAGR of 6.8% between 2026 and 2031.

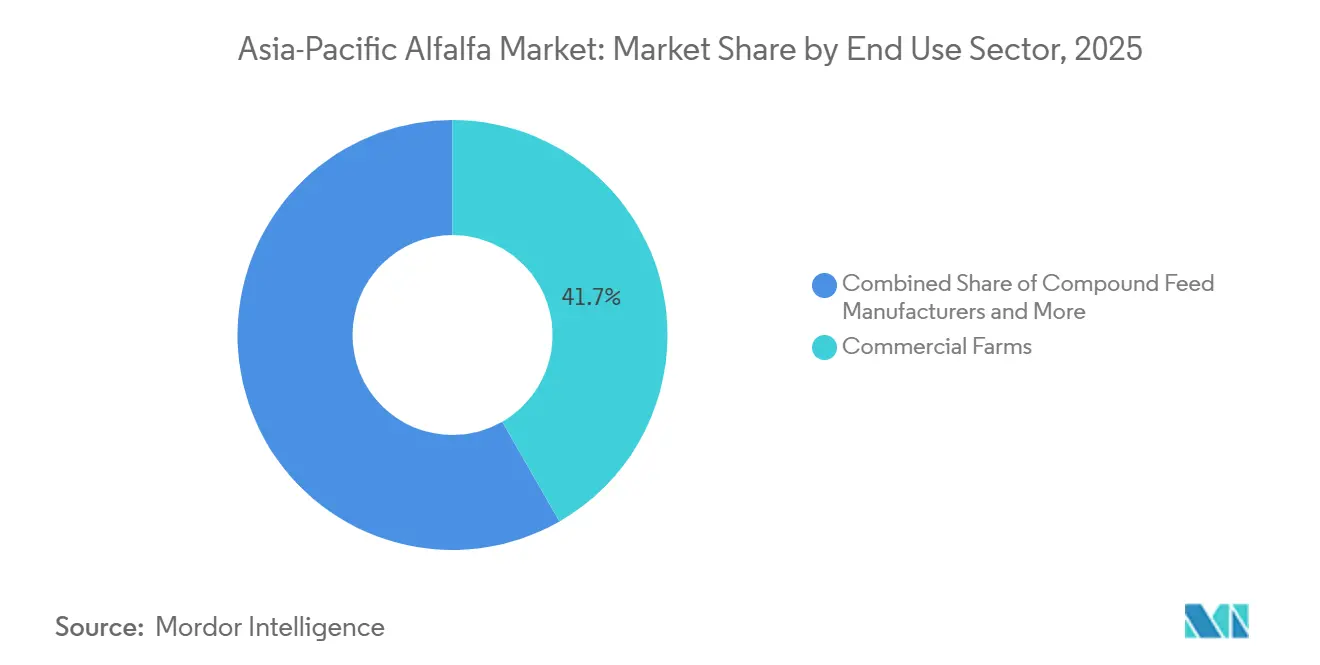

- By end-use sector, commercial farms led with 41.7% share in 2025, while pet food and specialty nutrition are estimated to advance at a CAGR of 7.1% between 2026 and 2031.

- By geography, China led with 35.1% share in 2025, while India is forecast to grow at the fastest CAGR of 8.9% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Alfalfa Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising commercial dairy consolidation in China | +1.20% | China, especially Inner Mongolia and Hebei dairy clusters | Short term (≤ 2 years) |

| Premium forage adoption in India's organized dairy co-ops | +0.80% | India, especially Gujarat, Maharashtra, Punjab, Haryana, and Uttar Pradesh | Medium term (2-4 years) |

| Export quality upgrades, traceability, and contracted supply premiums | +0.70% | Australia, Spain, Romania, China, Japan, and South Korea | Medium term (2-4 years) |

| Greenhouse-grade forage demand from urban and peri-urban livestock systems | +0.40% | China and India urban and peri-urban livestock belts | Medium term (2-4 years) |

| Mechanized dehydration and pelletization expanding shelf-life and trade reach | +0.90% | Major Asia Pacific trade corridors | Short term (≤ 2 years) |

| Climate risk hedging through multi-origin feed procurement | +0.50% | China, South Korea, Australia, Spain, Romania, Egypt, and South Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Commercial Dairy Consolidation in China

China's dairy sector is in a recovery and restructuring phase in 2026 after several years of oversupply and weak milk prices. Mega-farms now account for more than 68.0% of national milk output in 2025, according to the United States Department of Agriculture (USDA), and that shift keeps demand concentrated among fewer but much larger buyers in the Asia Pacific alfalfa market. These farms depend on standardized high-protein rations, which raises the need for a dependable alfalfa supply throughout every season. During the 125% tariff period on United States alfalfa in early 2025, some Chinese farms reduced daily alfalfa use per cow from 3 kilograms to 1.5 kilograms. That adjustment reduced milk yield and herd health, which showed how difficult premium alfalfa is to replace in high-output systems. Inner Mongolia expanded artificial forage planting to 1.39 million hectares, and total forage supply moved past 75 million metric tons in 2025[1]Source: Xinhua News Agency, “China Livestock Powerhouse Improves Pasture Management in Eco-Friendly Productivity Quest,” english. news.cn. Longer procurement contracts are therefore becoming more common, which gives major suppliers better visibility on forward volumes in the Asia Pacific alfalfa market

Premium Forage Adoption in India's Organized Dairy Co-Ops

India's organized dairy system is expanding faster than its premium forage base, which is creating a clear pull for alfalfa in the Asia Pacific alfalfa market. In May 2025, the Government of India announced three multi-state cooperative societies focused on animal feed production, disease control, and dairy development. The initiative is anticipated to strengthen certified fodder procurement, increase demand for quality forage, and support wider adoption of alfalfa in organized dairy supply chains[2]Source: National Cooperative Union of India, "Sahakar Jagran ", 2025, NCUI, ncui.coop. The Malabar Regional Cooperative Milk Producers' Union distributed USD 882,00 in fodder subsidies in 2025 to help farmers manage higher feed costs. India still faces a structural forage deficit because domestic alfalfa output does not consistently match the protein standards required by larger organized buyers. Seed improvement work with the Indian Grassland and Fodder Research Institute is also moving ahead, which supports medium-term productivity gains. As cooperatives scale milk collection and ration planning, the buying season for premium forage is likely to become longer and more predictable across the Asia Pacific alfalfa market.

Export Quality Upgrades, Traceability, and Contracted Supply Premiums

The move toward traceable and contracted trade is becoming a basic requirement in the Asia Pacific alfalfa market rather than a niche feature. Buyers are paying more attention to documentation, lab testing, and shipment consistency because the 2025 tariff shock exposed the cost of weak supplier controls. According to the ITC Trade Map, Chinese alfalfa meal and pellets imports were down 43.2% between 2024 and 2025[3]Source: International Trade Centre, “Trade Map,” 2025, trademap.org. That pattern shows buyers were willing to accept higher unit costs in exchange for dependable and quality-certified supply. Guangdong Yantang Dairy selected 6 certified import suppliers in a formal tender during March 2026, which signals a more structured supplier approval process among large dairy processors. This shift rewards exporters that can support full chain traceability and regular technical compliance. It also supports margin expansion for processed products and premium contracts across the Asia Pacific alfalfa market.

Greenhouse-Grade Forage Demand from Urban and Peri-Urban Livestock Systems

A smaller but important specialty channel is emerging in the Asia Pacific alfalfa market through urban and peri-urban livestock systems. Farms located near major consumption centers need forage with stable nutrient quality and tighter control over weed seeds, heavy metals, and aflatoxins. These operations often work under certified milk supply programs, so feed consistency matters as much as cost. In northern China, continuous-belt dehydration facilities are expanding to serve such buyers with year-round standardized products. In India, peri-urban livestock systems are increasingly linked to cooperative buying programs rather than open spot purchases. This demand channel is still smaller than mainstream dairy feed, but its willingness to pay for verified quality supports stronger margins. As a result, specialty processing and compliance are becoming more relevant to supplier positioning in the Asia Pacific alfalfa market

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water stress and irrigation competition in key producing belts | -0.60% | China Northwest, Inner Mongolia, Australia Riverina, and Murray-Darling Basin | Long term (≥ 4 years) |

| High freight volatility and port congestion on intra-Asia trade lanes | -0.50% | China, Japan, and South Korea import lanes | Short term (≤ 2 years) |

| Land costs and yield uncertainty near export corridors | -0.40% | Australia Riverina and China northern plains | Medium term (2-4 years) |

| Limited salt-tolerant and heat-tolerant varietal commercialization | -0.30% | South Asia, Southeast Asia, coastal India, and Northwest China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Water Stress and Irrigation Competition in Key Producing Belts

Alfalfa is a crop that requires significant water input and consistent irrigation to achieve optimal yields. Seasonal water shortages in northern China and parts of western India hinder the expansion of domestic production. In Punjab and Haryana, groundwater depletion has led to increased regulatory scrutiny of water-intensive crops. Similarly, China’s water-use reforms impose restrictions on irrigation in water-stressed provinces. The Central Ground Water Board (CGWB), in collaboration with State Governments, has completed the annual Dynamic Ground Water Resource assessment for the year 2025. According to the Central Groundwater Board (CGWB) of India, the total Annual groundwater recharge in the country is 448.52 Billion Cubic Meters (BCM), while the extractable groundwater resources amount to 407.75 BCM[4]Source: Ministry of Jal Shakti, “Dynamic Groundwater Resources Assessment, 2025,” pib.gov.in. This shift production to less water-stressed areas, such as Australia’s Murray-Darling Basin or China’s Xinjiang, where irrigation infrastructure is more developed, though higher transport costs to demand centers remain a challenge.

High Freight Volatility and Port Congestion on Intra-Asia Trade Lanes

Freight volatility is still a direct cost problem for the Asia Pacific alfalfa market because much of the trade depends on containerized shipments. In mid-2025, Singapore operated near 90.0% yard capacity and vessel waiting times reached up to 2 days, while congestion was also reported at Shanghai, Ningbo, Busan, Port Klang, and Sydney. Ocean carriers also added emergency surcharges. The July 2025 Asia Pacific freight update from Dimerco Express Group also noted tight capacity across key east-west and intra-Asia lanes. Alfalfa shipments are especially exposed because the product has a lower value density than many other agricultural goods. When equipment shortages, rolled cargo, and added surcharges appear together, supplier margins compress quickly, and lower-value bale formats become harder to place. This keeps freight conditions as a real commercial restraint on the Asia Pacific alfalfa market, even when underlying feed demand remains firm.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pellets Gain Ground on Bales in Long-Haul Trade

Bales held 56.2% of the Asia Pacific alfalfa market by value in 2025, making them the leading format across China, Japan, and South Korea. Their lead came from long-standing trade links between exporters in Australia, the United States Pacific Northwest, and Spain, and large dairy buyers that already use bale handling systems. Compressed bales, pellets, and cubes made up the balance of demand, with each format serving different freight, storage, and ration needs in the Asia Pacific alfalfa market.

Pellets are anticipated to record the fastest 7.4% CAGR between 2026 and 2031, supported by better container utilization, lower storage losses, and easier use in automated feeding systems. Cubes continue to appeal to equine and specialty livestock buyers because they are lower-dust and easier to portion at the farm level. Compressed bales remain relevant on long-haul export routes where freight efficiency matters, while standard bales should continue growing at a steadier pace because they remain the most familiar format for large dairy procurement teams. China's tighter feed-grade compliance framework is also strengthening the position of processed formats supplied by certified dehydration plants.

By Application: Dairy Cattle Feed Anchors Demand as Equine Feed Expands Faster

Dairy cattle feed accounted for 49.5% share of the Asia Pacific alfalfa market size in 2025, which kept it well ahead of the other application groups. This leadership came from the non-discretionary role of alfalfa in high-yield dairy rations, especially in China and South Korea, where commercial milk systems depend on consistent protein forage. Beef cattle feed followed as another meaningful outlet, while poultry, equine, small ruminant, camelids, and other livestock feed formed smaller but still established demand pools in the Asia Pacific alfalfa market.

Equine feed is anticipated to grow at the fastest 6.8% CAGR between 2026 and 2031, as equestrian infrastructure, leisure horse ownership, and premium forage use expand across Japan, South Korea, and Southeast Asia. Beef cattle feed should continue to rise on the back of quality-driven finishing programs in Australia, while poultry feed remains a smaller but steady user of alfalfa meal for fiber and pigmentation. Small ruminant demand should remain stable in organized goat and sheep milk chains, and camelids and other livestock feed should stay limited in volume but firm in value because the buyer base is less price sensitive.

By End Use Sector: Commercial Farms Lead While Specialty Nutrition Adds Faster Growth

Commercial farms held 41.7% of the Asia Pacific alfalfa market in the end-use sector segmentation in 2025, reflecting their role as the main channel for bulk and premium dairy procurement. Large farms, especially in China, are standardizing purchases through longer contracts, which keeps commercial farms ahead of compound feed manufacturers, household owners, and specialty buyers in the Asia Pacific alfalfa market. Compound feed manufacturers represent the next important outlet, while household owners remain the smallest by volume but support higher packaged product pricing.

Pet food and specialty nutrition are estimated to grow at the fastest 7.1% CAGR between 2026 and 2031, as alfalfa protein concentrate enters premium pet food and specialty nutrition applications in Japan, South Korea, and Australia. Compound feed manufacturers should continue growing through volume-based purchases, though they remain more price sensitive than direct commercial farms. Household owners should keep supporting demand for cubes and pellets in small animal and equine uses, while commercial farms continue to provide the broadest and most stable base for the Asia Pacific alfalfa market. This shift toward application-specific buying is improving the revenue mix for suppliers that can serve both bulk and premium channels.

Geography Analysis

China held 35.1% of the Asia Pacific alfalfa market share in 2025 and remained the region's largest demand center by a clear margin. Mega-farm consolidation has concentrated purchases among fewer but larger dairy operators, and that has increased the use of long-term contracts and multi-origin procurement in the Asia Pacific alfalfa market. The rising tariff on United States alfalfa exposed the cost of relying too heavily on one source, as some farms lowered daily inclusion rates and saw weaker performance. Japan remained the region's premium import market, with landed alfalfa prices generally in the USD 390 to USD 500 per metric ton range in 2025 and procurement shaped by strict quality standards.

India is estimated to record the fastest 8.9% CAGR in the Asia Pacific alfalfa market from 2026 to 2031 because organized dairy demand is rising faster than the premium forage supply. The May 2025 announcement of new multi-state cooperative societies is strengthening institutional feed demand and supports more formal procurement in large dairy states. Australia remains the key regional supply geography, with irrigated alfalfa production concentrated in the Riverina and Goulburn Valley districts. Water allocation pressure in the Murray-Darling Basin has intensified in 2026, which limits export flexibility and favors operators with stronger farming-to-port integration.

South Korea remained a premium import market in the Asia Pacific alfalfa market. The June 2026 memorandum of understanding between the Korea Agriculture Technology Promotion Agency and the Korea Dairy and Beef Farmers Association marked a more formal effort to build domestic forage capacity. The rest of Asia Pacific, especially Vietnam, Indonesia, and Thailand, is still earlier in development but is showing rising demand as commercial livestock systems expand and feed quality requirements improve. South Korea's compound feed sector remains mature, but disease-led fluctuations in poultry and swine herds are adding some short-term volatility to feed demand in 2026.

Competitive Landscape

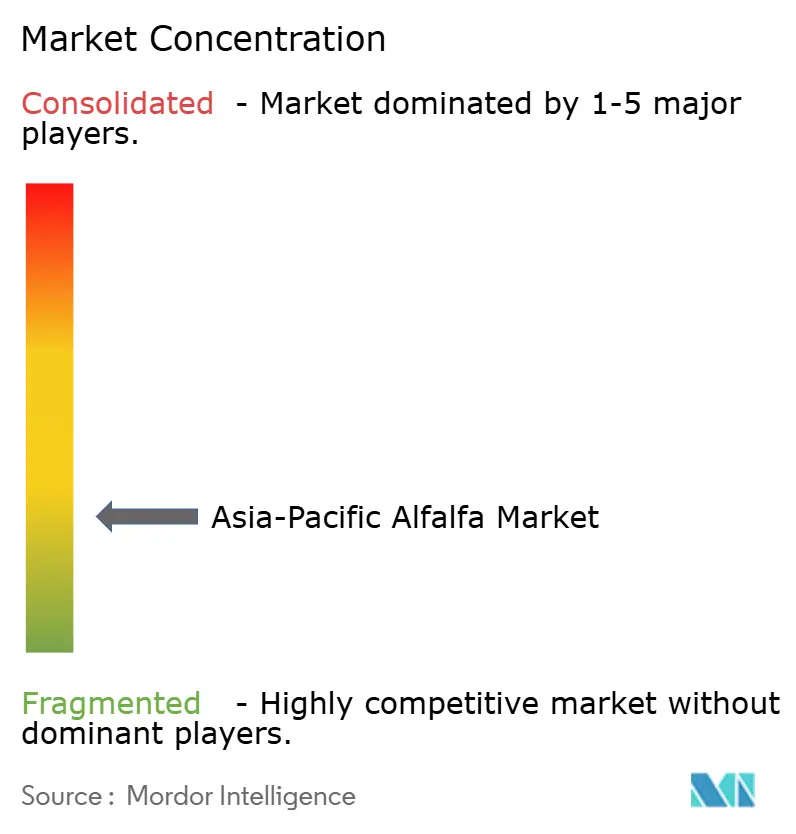

The Asia Pacific alfalfa market remained fragmented in 2025, with the top five players accounting for a significant share of the market alongside numerous regional exporters and suppliers. Al Dahra Holding LLC accounted for the significant share in 2025, supported by a multi-origin sourcing platform that covers more than 100,000 hectares across Spain, Romania, Egypt, Australia, and Argentina. That network allows the company to redirect shipments and change supply origins quickly when policy changes disrupt normal trade flows. Anderson Hay and Grain Co., Inc. remains a leading supplier on Asia Pacific trade routes, supported by its strong export network and long-standing relationships across China, Japan, and South Korea. The company has been adapting its strategy by increasing focus on domestic United States equine buyers while improving operational efficiency, creating opportunities for other exporters to strengthen their presence across key Asia Pacific import markets.

Standlee Premium Products, LLC continues to focus on premium forage formats that command higher retail prices than commodity bales. Cubeit Hay Company LLC operates in a similar premium segment through cubes, pellets, and specialty forage products for equine and other specialized buyers. This positioning provides both companies with greater resilience against the pricing pressures experienced in the bulk dairy hay segment. Standlee further strengthened its portfolio through the launch of NutriBakes and its collaboration with Triple Crown Nutrition's Diamond Line. Hay Australia (AgTrade Holdings), remains a key Australian exporter, supplying Japan, China, South Korea, Taiwan, and the Middle East through an integrated sourcing, processing, and export network.

The broader supplier landscape includes Calaway Trading, Inc., Border Valley Trading Ltd., S.L. Follen Company, Green Prairie International, Bailey Farms Inc., Alfalfa Monegros, S.L., M&C Hay Ltd., and Riverina, highlighting the presence of numerous regional and export-oriented participants. Calaway Trading, Inc. has established a strong international export network, while Border Valley Trading Ltd. operates one of the largest forage processing and storage facilities. S.L. Follen Company maintains a well-developed processing and export network serving Asian markets. Riverina, backed by Mitsubishi Corporation, and M&C Hay Ltd. further strengthen the supplier base, while increasing emphasis on traceability, feed quality compliance, and export documentation continues to shape competition across the Asia Pacific alfalfa market.

Asia-Pacific Alfalfa Industry Leaders

-

Standlee Premium Products, LLC

-

Anderson Hay & Grain Co., Inc.

-

Hay Australia (AgTrade Holdings)

-

Al Dahra Holding LLC

-

Cubeit Hay Company LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Al Dahra Holding LLC and Qatar's Baladna signed a memorandum of understanding to explore strategic farming collaboration and long-term animal feed supply. The collaboration is estimated to increase demand for imported alfalfa, creating export opportunities for Asia Pacific suppliers, particularly Australia, and supporting regional forage trade.

- December 2025: DLF Seeds launched the We Love Alfalfa campaign to promote alfalfa’s importance and support forage innovation, breeding collaboration, and grower engagement that can benefit Asia-Pacific markets through improved genetics and knowledge transfer.

- January 2025: The Punjab Government promoted collaborative initiatives to incorporate alfalfa into the state's forage system to enhance livestock productivity and agricultural sustainability. This initiative is estimated to boost alfalfa cultivation and adoption, supporting forage production and strengthening the Asia Pacific alfalfa market.

Asia-Pacific Alfalfa Market Report Scope

Alfalfa is obtained from the alfalfa plant, which is also known as Lucerne and Medicago sativa. It is cultivated as an important forage crop in many countries worldwide. The Asia-Pacific Alfalfa Market Report is Segmented by Product Type (Bales, Pellets, and More), by Application (Dairy Cattle Feed, Beef Cattle Feed, and More), by End Use Sector (Commercial Farms, Compound Feed Manufacturers, and More), and by Geography (China, Japan, India, Australia, South Korea, and Rest of Southeast Asia). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

By Product Type

| Bales |

| Pellets |

| Cubes |

| Compressed Bales |

By Application

| Dairy Cattle Feed |

| Beef Cattle Feed |

| Poultry Feed |

| Equine Feed |

| Small Ruminant Feed |

| Camelids and Other Livestock Feed |

By End Use Sector

| Commercial Farms |

| Compound Feed Manufacturers |

| Household and Hobby Animal Owners |

| Pet Food and Specialty Nutrition |

By Geography

| China |

| India |

| Japan |

| Australia |

| South Korea |

| Rest of Asia Pacific |

| By Product Type | Bales |

| Pellets | |

| Cubes | |

| Compressed Bales | |

| By Application | Dairy Cattle Feed |

| Beef Cattle Feed | |

| Poultry Feed | |

| Equine Feed | |

| Small Ruminant Feed | |

| Camelids and Other Livestock Feed | |

| By End Use Sector | Commercial Farms |

| Compound Feed Manufacturers | |

| Household and Hobby Animal Owners | |

| Pet Food and Specialty Nutrition | |

| By Geography | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia Pacific |

Key Questions Answered in the Report

What is the projected Asia-Pacific alfalfa market size in 2031?

The Asia-Pacific alfalfa market size was valued at USD 10.90 billion in 2025 and estimated to grow from USD 11.35 billion in 2026 to reach USD 14.60 billion by 2031, at a CAGR of 5.17% during the forecast period (2026-2031).

Which country leads regional demand?

China led with 35.1% of regional value in 2025. Its position comes from concentrated buying by large dairy farms and continued dependence on premium forage for ration consistency.

Which product format is growing the fastest?

Pellets are the fastest-growing product type with a 7.4% CAGR between 2026 and 2031. Better freight efficiency, lower storage loss, and easier use in automated feeding systems are supporting this shift.

Which application uses the most alfalfa in the region?

Dairy cattle feed is the largest application, with 49.5% share in 2025. Alfalfa remains difficult to replace in high-yield dairy rations because of its protein and fiber profile.

Page last updated on: