Asia-Pacific Aviation Manufacturing Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

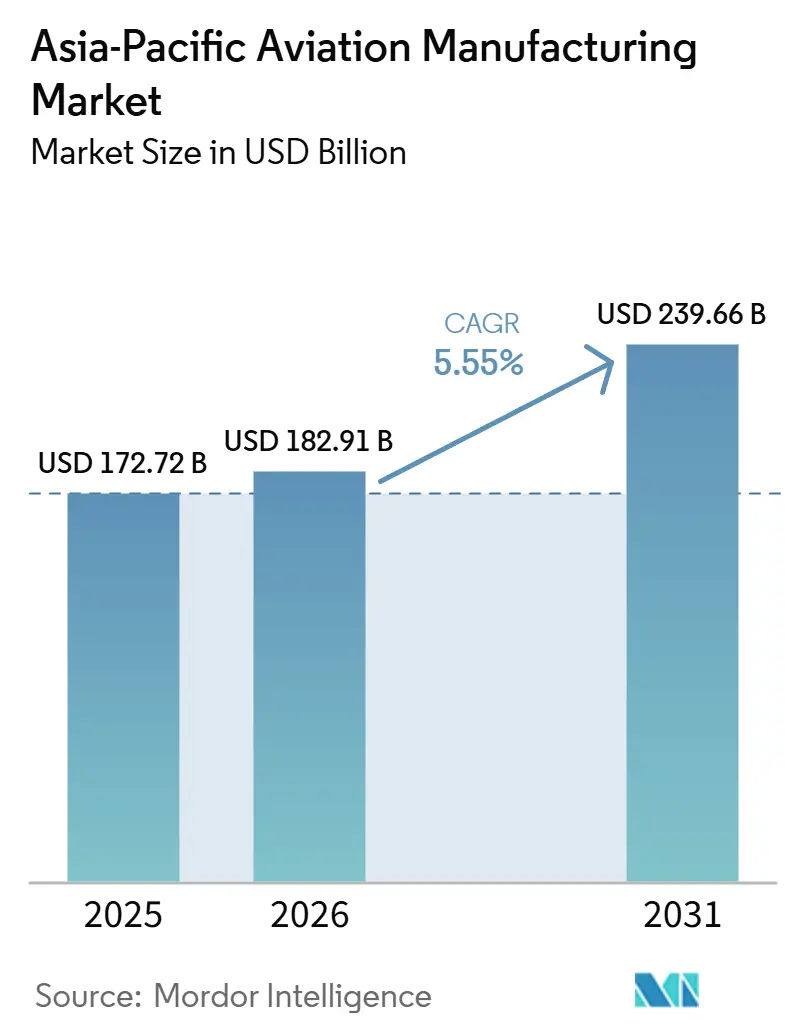

| Base Year Market Size (2025) | USD 172.72 Billion |

| Market Size (2026) | USD 182.91 Billion |

| Market Size (2031) | USD 239.66 Billion |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Aviation Manufacturing Market Analysis by Mordor Intelligence

The Asia-Pacific aviation manufacturing market size is expected to grow from USD 172.72 billion in 2025 to USD 182.91 billion in 2026 and is forecast to reach USD 239.66 billion by 2031 at a 5.55% CAGR over 2026-2031. Commercial programs continue to anchor final assembly volumes as narrowbody demand recovers with regional traffic, while defense programs add stability through multi-year procurement cycles. Materials shifts remain visible as composites adoption advances on weight and range benefits, even while aluminum alloys retain a large installed base in single-aisle workhorses. System complexity is rising across landing gear, actuation, and avionics due to safety, digitalization, and efficiency mandates, which is lifting value per shipset. Regional supply risks persist around engines and skilled labor, keeping production below demand and channeling more revenue to maintenance and retrofit activities in the near term.

Key Report Takeaways

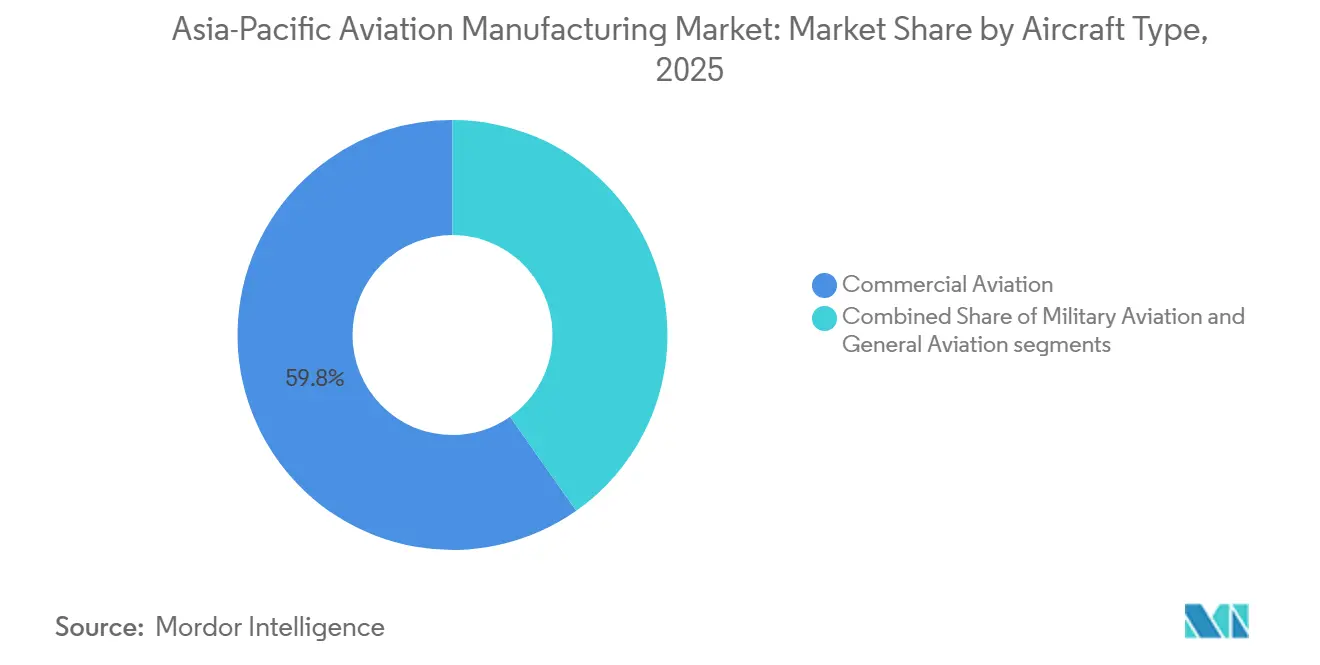

- By aircraft type, commercial aviation led with a 59.76% share of the Asia-Pacific aviation manufacturing market size in 2025, while military aviation is projected to be the fastest-growing sector, with a 7.76% CAGR through 2031.

- By component, airframe structures accounted for 39.81% of the Asia-Pacific aviation manufacturing market size in 2025, while landing gear and actuation systems are the fastest-growing segment, with a 6.90% CAGR from 2026 to 2031.

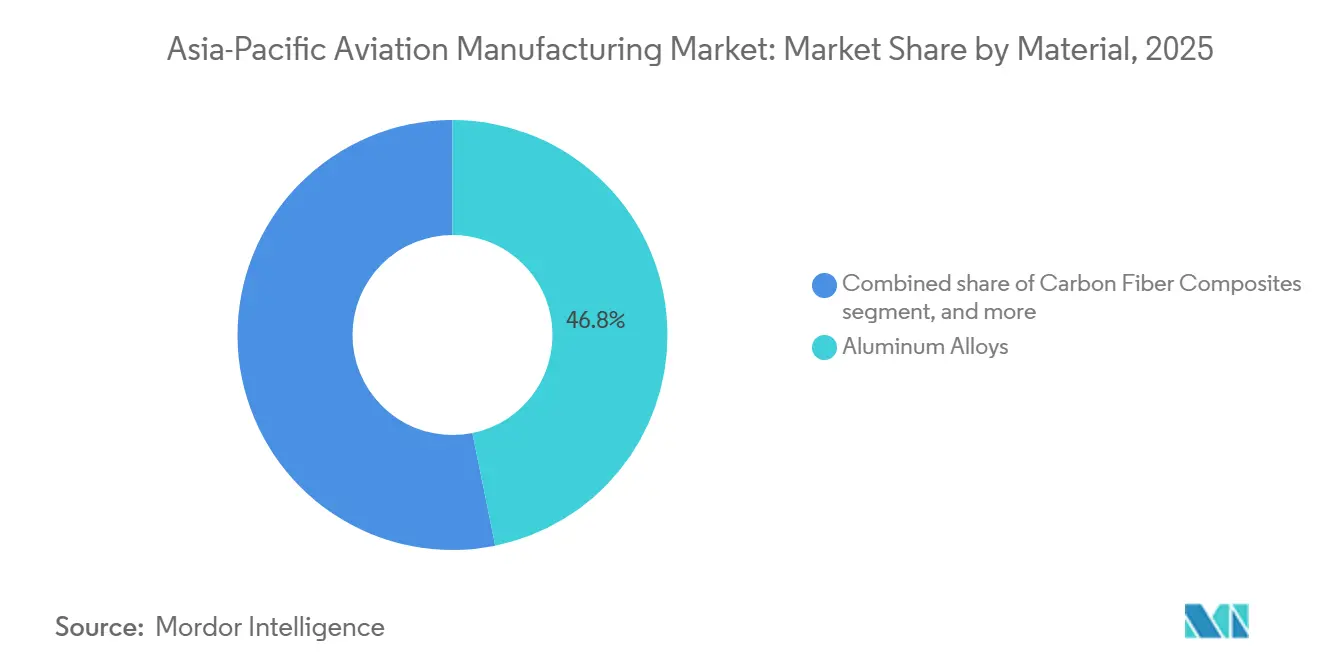

- By material, aluminum alloys accounted for 46.81% of the Asia-Pacific aviation manufacturing market in 2025, while carbon-fiber composites are the fastest-growing at 7.02% CAGR through 2031.

- By geography, China accounted for 65.98% of the Asia-Pacific aviation manufacturing market in 2025, while India is the fastest-growing with an 7.21% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Aviation Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commercial air-travel rebound fuels OEM backlogs | +1.8% | Global, peak in China, India, Southeast Asia | Short term (≤ 2 years) |

| Surge in Asia-Pacific low-cost–carrier narrowbody orders | +1.2% | India, Indonesia, Thailand, Vietnam | Medium term (2-4 years) |

| Government offsets and local-content mandates | +0.9% | India, Indonesia, China, South Korea | Medium term (2-4 years) |

| Regional push for SAF-ready production lines | +0.7% | Singapore, Japan, India, Australia with regional spillover | Long term (≥ 4 years) |

| Defense modernization accelerates military-aircraft procurement | +0.6% | China, India, Indonesia, Japan, South Korea, Philippines | Long term (≥ 4 years) |

| Aftermarket and retrofit demand uplift from engine inspections | +0.5% | China, India, Southeast Asia, Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Commercial Air-Travel Rebound Fuels OEM Backlogs

Asia-Pacific carriers posted a 9.3% year-over-year increase in revenue passenger kilometers in 2025, outpacing other global regions and reinforcing the case for steady single-aisle output. Airbus delivered 793 aircraft in 2025 after 766 in 2024, and a significant portion of the single-aisle flow went to Asia-Pacific operators as airlines restored capacity.[1]Airbus SE, “Airbus Annual Report 2024,” Airbus, airbus.com Boeing projects sustained large-scale procurement in the region, with growth and replacement both supporting demand. India’s carriers continue to expand their order books, which stretch into the next decade, building on headline commitments that locked in delivery slots across the A320neo family. The combination of restored load factors and constrained deliveries keeps backlogs firm and strengthens pricing power for selected configurations.

Surge in Asia-Pacific Low-Cost–Carrier Narrowbody Orders

Low-cost carriers have reshaped traffic within South and Southeast Asia by prioritizing high-frequency point-to-point routes that favor single-aisle economics. The A320neo and B737 MAX families deliver lower fuel burn and per-seat maintenance costs, which align with LCC utilization targets and improve cash-cost positions on dense domestic and regional pairs. Expanded fleets at leading LCCs in India and Southeast Asia also elevate demand for landing gear, brakes, and avionics spares as utilization extends daily block hours. Secondary-city connectivity is becoming more viable as new aircraft reduce trip costs and improve reliability, supporting incremental orders even as airport infrastructure is still maturing. Procurement pacing remains tethered to engine availability and shop-visit capacity, while the structural demand for narrowbody aircraft continues to underpin the Asia-Pacific aviation manufacturing market.

Government Offsets/Local-Content Mandates

Industrial participation rules are steering workshare into Asia through licensed assembly, subsystem packages, and long-term offset credits that bind global programs to local suppliers. India’s Make in India policies have already translated into the final assembly of C295 transports and broader aerostructure activity, anchoring supply-chain skills and tooling onshore. China’s self-sufficiency agenda is channeling capital into engines, avionics, and materials, while arms-related revenues at Aero Engine Corporation of China highlight a deepening industrial base. South Korea and Japan are capturing steady, high-value work in wing structures and advanced manufacturing for global platforms, reinforcing their long-standing roles as tier-one and tier-two specialists. These mandates create near-term complexity for global sourcing, yet they accelerate technology transfer and broaden the supplier pool serving the Asia-Pacific aviation manufacturing market.

Regional Push for SAF‐Ready Production Lines

Policy signals across Asia-Pacific point to rising sustainable aviation fuel use over the decade, which requires validating fuel systems, seals, and combustion architectures across production and retrofit applications. Airframers have committed to stepping up SAF readiness, and Airbus has stated a target to enable 100% SAF use across production aircraft by 2030, subject to certification, which implies upstream component changes and test plans.[2]Airbus SE, “Sustainable Aviation Fuels,” Airbus, airbus.com The scale-up of regional SAF supply encourages airlines to lock in offtake and introduces new requirements for on-wing system resilience to different fuel chemistries. Engine OEMs and fuel-system suppliers will invest in material compatibility and sensor upgrades that can be line-fitted or retrofitted, creating new product lanes for Asia-based factories. Over time, these changes support efficiency and emissions goals that align with the capital allocation priorities of airlines and lessors in the region.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic LEAP and PW-GTF engine shortages | -1.4% | Global, acute in India, Southeast Asia, Australia | Short term (≤ 2 years) |

| Skilled-labor gaps in composite lay-up and automation | -0.8% | India, Vietnam, Thailand, Indonesia | Medium term (2-4 years) |

| Prolonged MRO turnaround times and parts inflation | -0.6% | Global, acute in Asia-Pacific engine shops | Short term (≤ 2 years) |

| Certification and qualification bottlenecks for new materials and processes | -0.5% | Japan, Singapore, China, India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chronic LEAP and PW-GTF Engine Shortages

Pratt & Whitney’s PW1100G inspections related to powder-metal anomalies continue to ground aircraft and constrain fleet availability, with the company signaling extended remediation timelines and material cash costs. Airlines have reported losses linked to aircraft-on-ground events, and OEM support packages reflect the magnitude of compensation and repair expense under current inspection regimes. CFM LEAP families face their own throughput constraints and shop-visit pressures, which keep turnaround times elevated and require more spares coverage to maintain schedules. These headwinds cap near-term delivery profiles for new narrowbodies and delay retirement of older fleets, which redistributes spend toward maintenance and component life extensions. The Asia-Pacific aviation manufacturing market, therefore, grows amid tighter supply conditions that prioritize reliability and aftermarket readiness over short-term volume.

Skilled-Labor Gaps in Composite Lay-Up and Automation

Demand for trained aviation personnel is rising faster than training pipelines can supply, with the Asia-Pacific region needing large additions of maintenance technicians over the long term. Singapore allocated funds in 2024 to modernize training and curricula, with a focus on composite repair, digital diagnostics, and additive workflows. The first cohorts will enter the labor pool later in the decade, creating a timing gap for manufacturers in the region. India’s regulator authorized new maintenance engineer training organizations between 2022 and 2025 to expand capacity. Yet, OEMs still fund apprenticeships to ensure hands-on proficiency in carbon-fiber prepreg and automated fiber placement. Tight labor markets in emerging aerospace hubs can drive higher turnover and wage inflation, thereby increasing the cost to serve precision assemblies such as wing-to-body joints and nacelles. Closing these gaps is essential to meet OEM rate ambitions later in the decade and to expand the qualified supplier base across the Asia-Pacific aviation manufacturing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Military Outpacing Commercial on Defense Budgets

Commercial aviation accounted for 59.76% of the Asia-Pacific aviation manufacturing market size in 2025, reflecting the weight of narrowbody programs in regional build schedules. Military aviation is projected to expand at 7.76% CAGR to 2031 as governments anchor procurement pipelines for combat aircraft, transports, and rotorcraft that align with long-term readiness needs. Within commercial, single-aisle programs remain the backbone due to typical stage lengths and the economics of high-frequency service across domestic and regional routes. The widebody mix remains concentrated in areas where long-haul demand supports dual-aisle utilization, with Northeast Asian carriers and operators in Oceania maintaining steady intake for intercontinental networks.

Defense modernization gives the military segment durable visibility because platform updates and fleet expansions are sequenced over many years. As air forces refresh multi-role fighters and add missionized aircraft for patrol and lift, suppliers across metals, composites, avionics, and actuation benefit from cross-platform commonality. On the civil side, narrowbody dominance holds given predictable block-hour profiles and improved operating economics of new engine options. The Asia-Pacific aviation manufacturing industry continues to balance these cycles by relying on defense stability to smooth commercial variability, while incremental growth in business and general aviation adds diversity to downstream demand.

By Component: Landing Gear Gains from Heavier, More Complex Aircraft

Airframe structures accounted for 39.81% of the Asia-Pacific aviation manufacturing market in 2025, consistent with the value concentration in fuselage, wing, and empennage assemblies. Landing gear and actuation are the fastest-growing component families, advancing at 6.90% CAGR from 2026 to 2031 as safety rules tighten and platform weights increase on new single-aisle variants. The A321XLR illustrates this trend, with higher maximum takeoff weights driving engineering changes to struts, brakes, and attachment hardware on single-aisle platforms. Regulators in the region, including Japan’s civil aviation authority, have introduced additional oversight for gear inspection regimes that reinforce preventive maintenance and replacement planning. Propulsion and avionics each hold meaningful value pools and are shaped by certification cadence and digital upgrades, yet competition across multiple capable suppliers tempers pricing power on standard configurations.

Cabin retrofits continue to support steady interiors spending as airlines align hard products with yield management and network strategies. The shift to brake-by-wire, smart sensors, and predictive health monitoring extends across narrowbodies and is reshaping the bill of materials in favor of integrated electromechanical solutions. Automation investments at major final assembly sites, including Airbus Tianjin, are reducing touch labor and improving process stability, thereby shifting the value mix between labor, tooling, and software across the Asia-Pacific aviation manufacturing market. Over time, these upgrades support higher rates once engine availability and supply-chain bottlenecks ease.

By Material: Carbon Fiber Surge Tracks Weight-Reduction Imperatives

Aluminum alloys accounted for 46.81% of 2025 shipments, reflecting the dominant installed base of single-aisle aircraft and the maturity of certified aluminum supply chains for airframe structures. Carbon fiber composites are expanding at 7.02% CAGR through 2031 as OEMs target lower fuel burn and extended range, building on the performance seen in composite-intensive widebodies. The B787 and A350 programs demonstrated significant structural weight savings with composites, and their efficiency outcomes continue to guide materials choices for future narrowbody and regional designs. Composite content is also influenced by certification timelines and the maturity of the repair ecosystem, which determine how quickly new materials can move from secondary to primary structures. Titanium plays a critical role in high-stress, high-temperature zones where performance margins matter more than cost per kilogram.

As carriers focus on unit costs in a higher energy-price environment, material choices that support lower fuel consumption gain priority in fleet and retrofit decisions. Supplier landscapes differ by material: aerospace-grade aluminum requires traceability and tighter tolerances, limiting the number of qualified mills, while composite feedstocks and automated layup capacity are expanding in regional clusters. Standards and certification frameworks, including new additive manufacturing standards in Singapore, provide clearer pathways for qualifying parts that support composite and hybrid-material assemblies. These developments reinforce a gradual but persistent shift toward lighter structures across the Asia-Pacific aviation manufacturing market as rates recover and new programs advance.

Geography Analysis

China commanded 65.98% of the Asia-Pacific aviation manufacturing market share in 2025, supported by state-backed programs and sustained single-aisle assembly throughput that serves large domestic networks. COMAC’s C919 entered service after CAAC certification, and its longer-range delivery ambitions illustrate domestic intent to add a third airframer to the regional ecosystem over the decade. Airbus’s Tianjin line celebrated the 700th A320 assembly in 2024, further embedding final assembly capability and creating demand for local tier-one and tier-two suppliers. The Asia-Pacific aviation manufacturing market remains centered in China in terms of volume, while other geographies scale in specific niches and subsystems.

India is the fastest-growing geography, with an 7.21% CAGR projected for 2026 to 2031, reflecting sustained single-aisle orders and deepening industrial collaboration, including licensed assembly and aerostructure work. The Tata–Airbus program for C295 assembly in Vadodara serves as an anchor for local capability building and attracts adjacent suppliers for metallics, composites, and avionics content. Japan and South Korea contribute high-value subsystems, notably in advanced wing structures and materials research, which align with the needs of global widebody platforms. Singapore continues to strengthen its MRO and aerospace engineering footprint with standards and training that support complex component work and digital diagnostics at scale.

Southeast Asian countries, including Indonesia, Thailand, Vietnam, and Malaysia, are capturing growth through component manufacturing, aerostructure work, and exposure to heavy maintenance linked to expanding regional fleets. Australia’s manufacturing ecosystem is smaller, but it participates in specialized systems and R&D initiatives that support sustainment and decarbonization agendas. Across the region, air traffic recovery strengthens the case for localized parts production and repair, thereby diversifying supplier bases and reducing logistics risk for airlines and OEMs.[3]Source: International Air Transport Association, “Reviving the Commercial Aircraft Supply Chain,” IATA, iata.org Together, these dynamics sustain a broad demand profile for the Asia-Pacific aviation manufacturing market as volume and capability deepen in parallel.

Competitive Landscape

Airbus and Boeing maintain a dominant position in commercial airframes across narrowbody and widebody platforms, reflecting decades of certification, supply coordination, and global support networks. Fragmentation is greater across subsystems, including propulsion, avionics, interiors, and landing gear, where multiple qualified suppliers compete for shipset awards and aftermarket contracts. Engine availability and inspection cycles have shifted spending toward maintenance and spares, making reliability and shop throughput differentiators for propulsion OEMs and independent MROs. The Asia-Pacific aviation manufacturing market, therefore, balances a duopoly in airframes with more open competition in component domains where certification cycles and lifecycle economics shape switching costs.

Strategic moves continue to realign portfolios and supply risk. Airbus reported higher deliveries in 2025 and remains focused on single-aisle rate readiness while working to stabilize widebody supply chains. Airbus also moved to acquire select Spirit AeroSystems sites in late 2025 to reinforce control over critical fuselage and wing work scopes, which supports schedule stability. RTX disclosed significant financial support for customers and maintenance related to GTF inspections, as well as progress on portfolio actions, including the planned sale of certain actuation and flight-control assets to Safran.[4]RTX Corporation, “RTX 2024 Annual Report,” RTX, rtx.com These steps show how leading suppliers are responding to quality, capacity, and cost pressures with targeted investments and divestments that sharpen focus on core franchises.

COMAC’s C919 program underscores the region’s multi-polar shift in airframes as certification and deliveries scale within China, which could incrementally reframe supply choices over time. Japan and South Korea remain embedded in global programs through high-value structural packages, while Southeast Asian suppliers deepen participation in metallics, composites, and MRO. Cybersecurity, export controls, and sustainability requirements favor capitalized suppliers that can absorb compliance costs and integrate new materials and digital tools at a rate. Against this backdrop, the Asia-Pacific aviation manufacturing market continues to reward reliability, certified quality, and lifecycle economics across both line-fit and aftermarket work.

Asia-Pacific Aviation Manufacturing Industry Leaders

Airbus SE

The Boeing Company

Mitsubishi Heavy Industries, Ltd.

Commercial Aircraft Corporation of China, Ltd. (COMAC)

Korea Aerospace Industries, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Airbus opened a new technology center in Bengaluru, signifying a significant expansion of its strategic presence in India. This facility will function as a hub for engineering, digital transformation, customer services, and procurement, reinforcing the company's commitment to its 'Make in India' initiative.

- February 2026: Japan Airlines and Safran entered into a nine-year "Support By the Hour" (SBH) contract, covering up to 35 A350-900 and A350-1000 aircraft. This agreement marks a significant milestone as it integrates four Safran companies, Safran Landing Systems, Safran Electronics & Defense, Safran Electrical & Power, and Safran Ventilation Systems, into a single contract to provide a comprehensive support solution for Japan Airlines' A350 fleet.

Asia-Pacific Aviation Manufacturing Market Report Scope

The Asia-Pacific aviation manufacturing market includes the production of commercial, military, and general aviation aircraft, along with their components and systems. The market benefits from a geographically concentrated demand in the region, particularly India and China.

The Asia-Pacific aviation manufacturing market is segmented by aircraft type, component, material, and geography. By aircraft type, the market is segmented into commercial aviation, military aviation, and general aviation. By component, the market is segmented into airframe structures, propulsion systems, avionics and flight control systems, cabin and interior modules, landing gear and actuation, and other components. By material, the market is segmented into aluminum alloys, carbon fiber composites, titanium alloys, high-strength steel, and other materials. The report also covers the market sizes and forecasts for the aviation manufacturing market in six countries across the region. For each segment, the market size and forecast are provided in terms of value (USD).

Source: https://www.mordorintelligence.com/industry-reports/aviation-manufacturing-market

| Commercial Aviation | Narrowbody Aircraft |

| Widebody Aircraft | |

| Regional Jets | |

| Military Aviation | Combat Aircraft |

| Non-Combat Aircraft | |

| Helicopters | |

| General Aviation | Business Jets |

| Turboprop Aircraft | |

| Piston Aircraft | |

| Helicopters |

| Airframe Structures |

| Propulsion Systems |

| Avionics and Flight Control Systems |

| Cabin and Interior Modules |

| Landing Gear and Actuation |

| Other Components |

| Aluminum Alloys |

| Carbon Fiber Composites |

| Titanium Alloys |

| High-Strength Steels |

| Other Materials |

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Singapore |

| Rest of Asia-Pacific |

| By Aircraft Type | Commercial Aviation | Narrowbody Aircraft |

| Widebody Aircraft | ||

| Regional Jets | ||

| Military Aviation | Combat Aircraft | |

| Non-Combat Aircraft | ||

| Helicopters | ||

| General Aviation | Business Jets | |

| Turboprop Aircraft | ||

| Piston Aircraft | ||

| Helicopters | ||

| By Component | Airframe Structures | |

| Propulsion Systems | ||

| Avionics and Flight Control Systems | ||

| Cabin and Interior Modules | ||

| Landing Gear and Actuation | ||

| Other Components | ||

| By Material | Aluminum Alloys | |

| Carbon Fiber Composites | ||

| Titanium Alloys | ||

| High-Strength Steels | ||

| Other Materials | ||

| By Geography | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the size and growth outlook for the Asia-Pacific aviation manufacturing market to 2031?

The Asia-Pacific aviation manufacturing market size is expected to grow from USD 172.72 billion in 2025 to USD 182.91 billion in 2026 and is forecast to reach USD 239.66 billion by 2031 at a 5.55% CAGR over 2026-2031.

Which aircraft type leads Asia-Pacific production today?

Commercial programs lead and accounted for 59.76% share in 2025, with military aviation growing fastest through 2031 due to multi-year modernization pipelines.

What components are growing fastest in the Asia-Pacific aviation manufacturing market?

Landing gear and actuation systems are the fastest growing component families at a 6.90% CAGR for 2026 to 2031 as aircraft weights rise and safety requirements evolve.

Which materials are gaining share in Asia-Pacific programs?

Carbon-fiber composites are expanding at 7.02% CAGR through 2031, while aluminum alloys still hold the largest 2025 share due to the large single-aisle installed base.

Which geographies drive the Asia-Pacific aviation manufacturing market?

China led with 65.98% share in 2025, while India is the fastest growing to 2031 supported by large narrowbody orders and local assembly initiatives.

How are engine inspection requirements affecting output and spend in Asia-Pacific?

GTF and LEAP constraints are holding back new deliveries and pushing more revenue to maintenance and retrofit activities, keeping near-term supply tight while demand remains firm.

Page last updated on: