ASEAN Frontline Worker Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

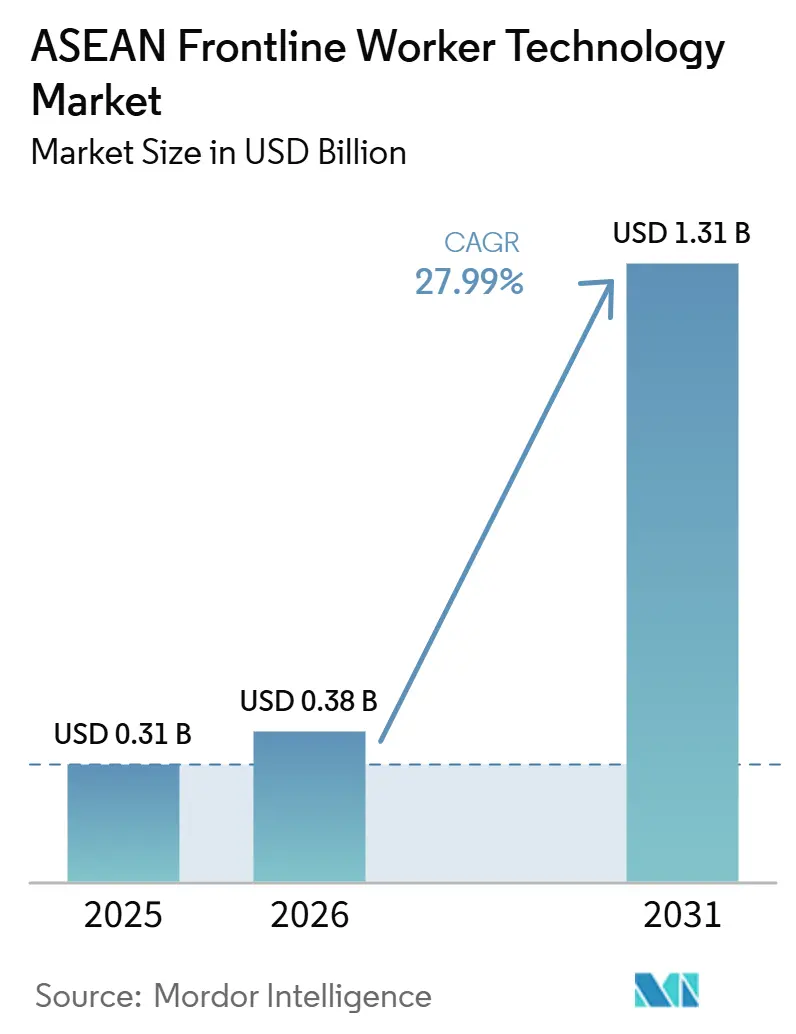

| Base Year Market Size (2025) | USD 0.31 Billion |

| Market Size (2026) | USD 0.38 Billion |

| Market Size (2031) | USD 1.31 Billion |

| Growth Rate (2026 - 2031) | 27.99% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Frontline Worker Technology Market Analysis by Mordor Intelligence

The ASEAN frontline worker technology market size stood at USD 0.31 billion in 2025 and is forecast to reach USD 1.31 billion by 2031, at a CAGR of 27.99% during 2026-2031. Growth is being supported by the wider shift from manual frontline coordination to software-led task execution, communication, and compliance management across factories, warehouses, and field operations. The ASEAN frontline worker technology market is also benefiting from the region’s push to digitize industrial operations, which is shortening enterprise buying cycles and widening adoption beyond large anchor accounts. Cloud deployment is helping buyers connect multiple sites into a single operational layer, which is especially important in regions where many companies manage dispersed workforces across several countries. Safety and audit requirements are making it harder to postpone frontline platforms, as employers now need more structured worker records, clearer escalation flows, and stronger site-level visibility. Competition remains fragmented, which leaves room for specialist vendors that can combine software, rugged devices, and support services into solutions that fit local operating conditions.

Key Report Takeaways

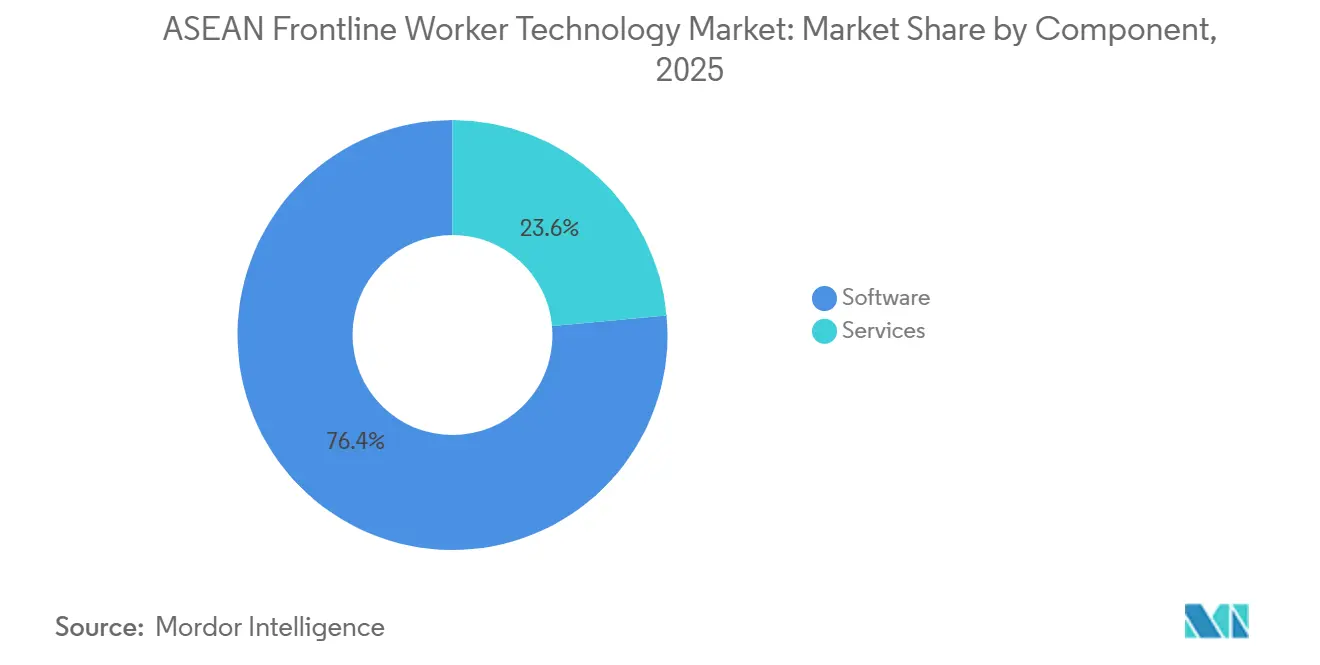

- By component, software held 76.44% of the ASEAN frontline worker technology market share in 2025, while services are projected to expand at a 30.84% CAGR through 2031.

- By deployment, cloud-based solutions accounted for 69.12% of the ASEAN frontline worker technology market share in 2025 and are projected to expand at a 30.27% CAGR through 2031.

- By organization size, large enterprises held 66.81% of the ASEAN frontline worker technology market share in 2025, while small and medium enterprises are projected to expand at a 30.58% CAGR through 2031.

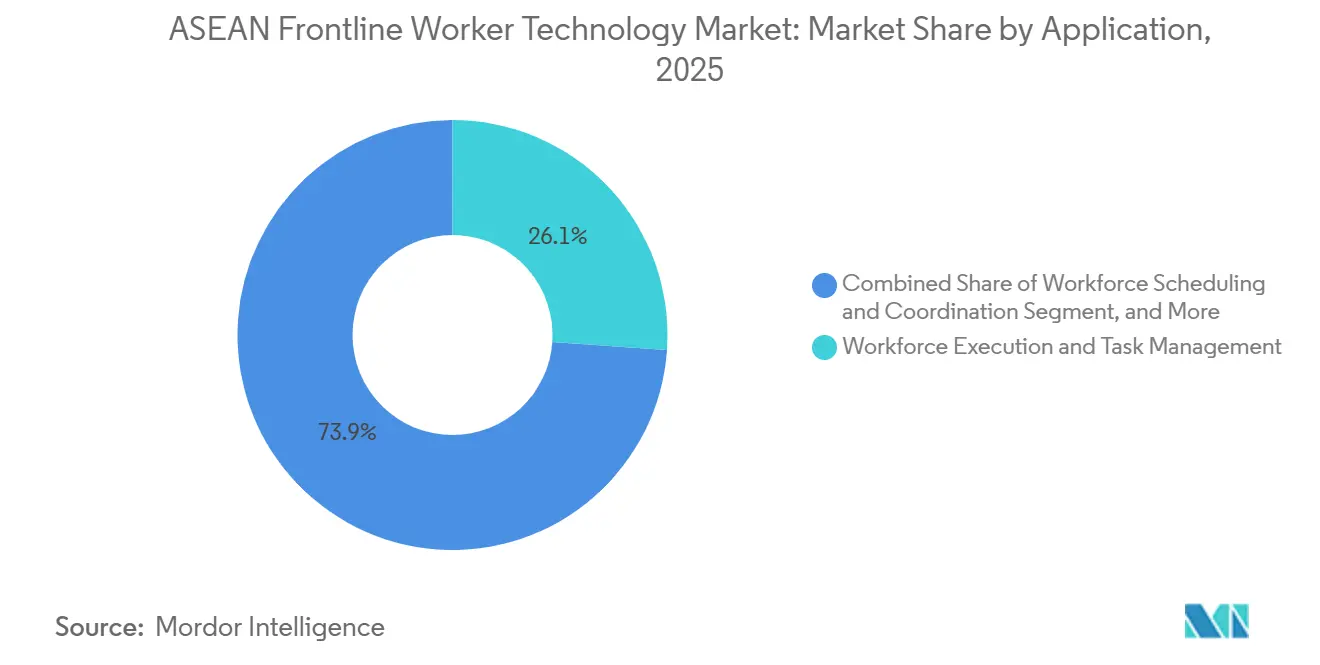

- By application, workforce execution and task management accounted for 26.11% of the ASEAN frontline worker technology market share in 2025, while safety and compliance management is projected to expand at a 29.74% CAGR through 2031.

- By end-user industry, industrial manufacturing held 24.54% of the ASEAN frontline worker technology market share in 2025, while transportation and logistics is projected to expand at a 29.45% CAGR through 2031.

- By geography, Indonesia held 38.16% of the ASEAN frontline worker technology market share in 2025, while Vietnam is projected to expand at a 29.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

ASEAN Frontline Worker Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Industrial Digitization in ASEAN Manufacturing Hubs | +8.5% | Indonesia, Vietnam, Thailand, Malaysia | Short term (≤ 2 years) |

| Expansion of Connected Worker and Rugged Device Deployment | +6.2% | Indonesia, Malaysia, Thailand | Medium term (2-4 years) |

| Compliance Pressure for Worker Safety, Traceability, and Auditability | +5.8% | ASEAN-wide, with early gains in Singapore and Indonesia | Medium term (2-4 years) |

| AI-Enabled Real-Time Task Orchestration at the Edge | +4.1% | Singapore, Malaysia, Vietnam | Long term (≥ 4 years) |

| Cloud Adoption for Frontline Operations and Field Data Capture | +3.7% | ASEAN-wide | Short term (≤ 2 years) |

| Multisite Workforce Scheduling Across Distributed Operations | +3.4% | Indonesia, Philippines, Vietnam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Industrial Digitization in ASEAN Manufacturing Hubs

Industrial modernization is changing how the ASEAN frontline worker technology market is bought and deployed across manufacturing corridors. Procurement is moving closer to plant-level operational outcomes because companies want faster coordination, better exception handling, and stronger visibility across production workflows. This shift is being reinforced by regional policy support for interoperable digital standards and cross-border digital coordination under the ASEAN Digital Master Plan 2030. Firm-level automation plans across Southeast Asia also point to a deeper reworking of worker processes rather than isolated technology upgrades, which supports sustained demand for execution and communication platforms. The ASEAN frontline worker technology market is therefore moving in step with industrial policy and operating pressure, reducing the room for delayed adoption. Vendors that can localize service delivery, meet compliance expectations, and support multisite rollouts are better placed to convert this demand into recurring contracts.

Expansion of Connected Worker and Rugged Device Deployment

The ASEAN frontline worker technology market is becoming increasingly device-intensive as companies connect workers in physically demanding, time-sensitive environments. Rugged handhelds, tablets, scanners, wearables, and guided-work tools are being adopted as part of a broader workflow redesign rather than as stand-alone hardware purchases. Honeywell’s January 2026 launch of Performance+ for Guided Work showed how voice guidance, analytics, and multilingual support are being tied directly to operational performance in warehouse and logistics settings. Blackline Safety’s G8 announcement also showed that safety wearables are now expected to combine communication, monitoring, and cloud connectivity into a single platform, reflecting a wider move toward integrated frontline stacks. This matters for the ASEAN frontline worker technology market because bundled device-and-software deployments raise switching costs and deepen vendor relationships over time. It also expands the role of services, since companies need setup, integration, training, and ongoing support to make these deployments work across large frontline teams.

Compliance Pressure for Worker Safety, Traceability, and Auditability

Worker safety rules and supply chain accountability requirements are pushing the ASEAN frontline worker technology market toward platforms that can generate consistent digital records. Employers increasingly need evidence of worker checks, incident escalation, training completion, and site-level compliance actions rather than scattered paper-based records. Regional workplace safety work has highlighted the need for stronger occupational safety frameworks across Southeast Asia, which supports more formal use of connected tools and structured reporting systems. The ILO forum in Indonesia also underscored how artificial intelligence and digitalization are becoming part of the discussion around health and safety management in work environments. In the ASEAN frontline worker technology market, this pressure favors platforms with audit trails, alerting tools, worker-level visibility, and centralized records. It also strengthens the case for software-led deployments because compliance needs tend to widen from one site or one task category to broader enterprise operations.

Multisite Workforce Scheduling across Distributed Operations

The ASEAN frontline worker technology market is also gaining traction due to the need to coordinate work across multiple sites, countries, and labor environments. Regional operators often run warehouses, factories, and field teams across multiple jurisdictions, making manual scheduling increasingly difficult to sustain as operations expand. Honeywell built language support for more than 48 languages into Performance+ for Guided Work, reflecting the practical need to coordinate dispersed, multilingual frontline teams with fewer handoff errors. Broader automation plans across Southeast Asia also suggest that firms are preparing for more digitally coordinated operations, which raises the value of scheduling, task allocation, and live work visibility. The ASEAN frontline worker technology market benefits when buyers shift from single-site tools to platforms that can manage labor allocation across distributed facilities. That shift usually increases contract scope because scheduling tools often link with communication, compliance, and analytics modules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Rugged Devices and Deployment Ecosystems | -4.5% | Indonesia, Philippines, Vietnam (SME-heavy markets) | Short term (≤ 2 years) |

| Fragmented Connectivity Across Industrial and Remote Sites | -3.8% | Indonesia (outer islands), Philippines, rural Malaysia | Medium term (2-4 years) |

| Limited Frontline Change Readiness and Training Gaps | -2.9% | Indonesia, Vietnam, Philippines | Medium term (2-4 years) |

| Data Security and Device Management Complexity | -2.3% | Singapore, Malaysia (high data sensitivity sectors) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Rugged Devices and Deployment Ecosystems

Upfront deployment cost remains a clear drag on the ASEAN frontline worker technology market, especially in price-sensitive manufacturing and logistics environments. The issue is not limited to the device itself, because full deployment often includes device management, support, integration, and worker training. Research on digital transformation in occupational safety management in Indonesia identified structural limits that many firms face when moving from interest to execution. Subscription and leasing responses are emerging, and the June 2025 partnership between CHN and The Joy Factory showed how suppliers are trying to reduce the capital burden through service-oriented hardware access. Even so, the ASEAN frontline worker technology market still faces uneven adoption, as smaller operators often prioritize shorter-payback software modules before committing to a full rugged device estate. This restraint is most visible in the SME segment, where demand is growing quickly but the cost of a broad rollout still limits deployment depth.

Fragmented Connectivity across Industrial and Remote Sites

Connectivity gaps continue to slow the ASEAN frontline worker technology market where real-time coordination depends on stable network access. This challenge is strongest in remote industrial zones, plantation areas, outer islands, and distributed logistics environments where coverage quality can vary sharply. Telkomsel’s private 5G deployment for PT Pegaunihan’s smart factory in Batam showed that reliable frontline connectivity often needs dedicated infrastructure investment rather than a simple software rollout.[1]Telkomsel, “Telkomsel Launches 5G for IoT and AI in PT Pegaunihan’s Smart Factory,” Telkomsel, telkomsel.com The ASEAN Digital Master Plan 2030 also highlighted the importance of stronger digital infrastructure and cross-border interoperability, which confirms that connectivity remains a foundational issue across member states. In the ASEAN frontline worker technology market, weak connectivity forces many platforms to operate in a partial offline mode, which reduces the value of real-time analytics, alerting, and field data capture. Until site connectivity improves more broadly, some deployments will remain narrower in scope and slower to scale from the pilot stage to full network use.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominates as Services Delivery Scales

Software accounted for 76.44% of the ASEAN frontline worker technology market in 2025, indicating that buyers were allocating the largest budgets to workflow, communication, analytics, and compliance layers. That mix suggests the ASEAN frontline worker technology market had already moved beyond a device-led phase in which hardware alone defined frontline digitization. Buyers increasingly preferred platforms that could unify task execution, worker communication, incident handling, and reporting under one operating layer. This also increased the value of software modules that can be rolled out across multiple sites without replacing existing devices. In that context, software remained the anchor for expansion because it could improve workforce coordination even before companies completed larger infrastructure upgrades.

Services are projected to grow at a 30.84% CAGR through 2031, reflecting the implementation burden that often accompanies real deployments in the ASEAN frontline worker technology industry. Rollouts usually require language setup, device enrollment, workflow design, training, and support after go-live, which gives service providers a larger role than simple software resale. Scandit’s SDK 8 release in November 2025 demonstrated how intelligent data capture is moving deeper into operational workflows, increasing the need for integration and configuration work around frontline deployments. Safety and audit expectations are also making implementation more complex, as companies seek cleaner records, stronger escalation paths, and better reporting discipline across sites. As a result, the ASEAN frontline worker technology market size for services is rising on the back of deployment complexity rather than simple volume growth alone.

By Deployment: Cloud-Based Solutions Lead Frontline Connectivity

Cloud-based deployment accounted for 69.12% of the ASEAN frontline worker technology market in 2025, underscoring buyers' desire for a simpler way to manage multiple frontline locations under a single environment. Cloud models lower the burden of maintaining site-by-site infrastructure and make it easier to roll out updates, track usage, and standardize workflows across countries. This matters in the ASEAN frontline worker technology market because many operators run distributed facilities and need consistent visibility across their frontline teams. Cloud deployment also meets the needs of organizations seeking faster implementation cycles and lower internal IT overhead. It has therefore become the default route for many new deployments, especially when software scope spans communication, tasking, and compliance tracking.

Hybrid deployment is gaining traction when latency, local processing, or internal policy make a fully cloud-based setup impractical. On-premises deployment still matters in facilities that handle sensitive information or operate under tighter internal controls. The ASEAN Digital Master Plan 2030 supports broader digital interoperability across the region, which helps cloud-led solutions scale with fewer structural barriers over time. Even so, the ASEAN frontline worker technology market will continue to support a mixed deployment base, as site conditions and enterprise requirements vary widely across industries. Vendors that offer flexible deployment paths are likely to maintain an advantage, as buyers want cloud benefits without losing control over site-specific operational needs.

By Organization Size: SMEs Emerge as High-Growth Adopters

Large enterprises held 66.81% of the ASEAN frontline worker technology market in 2025, which reflected their earlier start in buying enterprise software, rugged devices, and support services at scale. They had the budgets, internal teams, and operating complexity needed to justify broad frontline deployments across multiple facilities. Large organizations also tended to move first because they faced more formal reporting, compliance, and productivity management requirements. In many cases, they used frontline technology to reduce coordination delays across large workforces rather than to solve one isolated workflow issue. This kept large enterprises at the center of current demand even as the user base widened.

Small and medium enterprises are projected to grow at a 30.58% CAGR through 2031, making them the most dynamic growth segment in the ASEAN frontline worker technology market. The shift is being helped by cloud pricing, lower setup friction, and a gradual move toward modular software that can be deployed without a full rugged device estate. Leasing and service-based hardware access models also improve affordability for smaller operators that would otherwise delay investment. Regional digital policy support and wider enterprise automation intent are creating a more favorable environment for SME adoption over time. The ASEAN frontline worker technology market is therefore broadening from a top-account business into a more distributed buyer base, although many SMEs will still start with software-first deployments before expanding further.

By Application: Execution Tools Anchor Budgets as Safety Compliance Accelerates

Workforce execution and task management accounted for 26.11% of the ASEAN frontline worker technology market in 2025, indicating that the first budget priority remained operational throughput. Buyers continue to fund tools that assign work, guide execution, flag exceptions, and provide line-of-sight into daily frontline performance. This segment stays central because it gives immediate value in factories, warehouses, and service environments where work needs to be coordinated minute by minute. It also acts as the base layer for later adoption of analytics, safety, and communication modules. In the ASEAN frontline worker technology market, execution tools remain the most direct way to turn digital investment into measurable workflow control.

Safety and compliance management is projected to expand at a 29.74% CAGR through 2031, reflecting the growing importance of worker protection and auditability in frontline operations. Regional workplace safety discussions are pushing organizations toward more structured digital monitoring and reporting systems. The ILO-linked forum in Indonesia also reinforced that artificial intelligence and digitalization are becoming part of practical safety management conversations. Blackline Safety’s G8 launch illustrated how vendors are answering this demand with connected wearables that combine monitoring, communication, and cloud visibility. The ASEAN frontline worker technology market for safety applications is therefore growing, as compliance expectations now intersect with operational risk control and workforce traceability.

By End-User Industry: Logistics Growth Challenges Manufacturing Dominance

Industrial manufacturing accounted for 24.54% of the ASEAN frontline worker technology market in 2025, maintaining its position as the largest end-user segment in current revenue terms. Manufacturing remains the largest buyer because it combines dense labor environments, repetitive task structures, and strong demand for visibility on throughput and exceptions. It also offers a broad installed base where software upgrades and device refresh cycles can keep spending active even when new site launches are slow. In the ASEAN frontline worker technology market, manufacturing has therefore remained the main reference point for product design and enterprise sales. Its position is supported by the region’s role in electronics, automotive, chemicals, and broader industrial production.

Transportation and logistics are projected to grow at a 29.45% CAGR through 2031, making it the fastest-growing end-user category in the ASEAN frontline worker technology market. This segment benefits from the pressure to coordinate picking, loading, routing, and warehouse work in real time, often across large labor pools and tight service windows. Honeywell’s Performance+ for Guided Work directly targeted this environment with voice-led workflows and analytics for distributed logistics operations. Connected worker deployments in construction environments also show how site-intensive sectors are increasingly overlapping with industrial use cases in practical terms.[2]Accent Systems, “First Balfour, Digital Transformation in Philippine Construction,” Accent Systems, accent-systems.com The ASEAN frontline worker technology market share is therefore likely to widen across sectors, even if manufacturing keeps the largest current revenue base.

Geography Analysis

Indonesia held 38.16% of the ASEAN frontline worker technology market share in 2025, making it the largest market in the region. Its lead reflects workforce scale, manufacturing depth, and the fact that even a modest rise in digital penetration creates visible software demand. The ASEAN frontline worker technology market in Indonesia also benefits from the country’s broad industrial footprint, which gives vendors access to manufacturing, logistics, and field operations within a single geography. Telkomsel’s private 5G deployment for a smart factory in Batam showed that frontline digitization is increasingly tied to dedicated connectivity investment in industrial settings. Singapore and Malaysia remain important because they shape regional procurement decisions, host enterprise coordination functions, and support higher-value deployments across regulated and technology-intensive operating environments.

Vietnam is projected to expand at a 29.98% CAGR through 2031, which makes it the fastest-growing geography in the ASEAN frontline worker technology market. The country is benefiting from rising manufacturing activity, a broader base of digitalizing enterprises, and a stronger interest in software-led frontline coordination. Regional policy momentum toward digital integration and interoperable frameworks supports that direction and, over time, reduces friction for multinational operating models.[3]ASEAN Secretariat, “ASEAN Digital Master Plan 2030,” ASEAN Secretariat, asean.org Thailand also remains significant because its industrial base creates steady demand for traceability, workflow discipline, and multisite worker coordination. Together, Vietnam and Thailand strengthen the center of gravity of the ASEAN frontline worker technology market in mainland Southeast Asia, where factory-led demand is closely tied to broader industrial upgrading.

The Philippines and the rest of ASEAN still represent an earlier-stage opportunity within the ASEAN frontline worker technology market. In the Philippines, adoption is supported by growing demand for better coordination in site-based environments and expanding operational needs across service and industrial activities. The connected worker deployment by First Balfour showed that location tracking and automated worker movement records are already being adopted in large project environments across the country. Across the rest of ASEAN, market progress depends more on basic digital infrastructure and the gradual spread of enterprise-ready operating models, which sustain long-term potential even where current adoption remains limited.

Competitive Landscape

The ASEAN frontline worker technology market is fragmented, with competition spread across rugged device makers, workflow software firms, mobile device management providers, and systems integration partners. No single company holds a dominant position, so buyers can still assemble solutions from different vendor layers based on their operating needs. Even so, the market is becoming more difficult for smaller participants because enterprise customers increasingly prefer platforms that tie devices, software, analytics, and support into a single operating framework. This has shifted competition away from one-product selling and toward ecosystem depth across operational use cases. The ASEAN frontline worker technology market, therefore, rewards vendors that can stay relevant beyond the initial purchase and support wider rollout over time.

Zebra Technologies strengthened that model in June 2026 when it launched Zebra Nucleus and new Workcloud tools that link device fleets, business intelligence, and workflow orchestration under a more unified software environment. Honeywell took a similar path with Performance+ for Guided Work, where guided execution and analytics were positioned together for warehouse and logistics users.[4]Honeywell, “Honeywell Launches New Performance+ for Guided Work to Enable Faster, Smarter Supply Chain Operations,” Honeywell, honeywell.com Scandit approached the market from the intelligent capture layer, using SDK 8 to reduce workflow friction at the point of scanning and data entry. Blackline Safety also pushed the platform model further with G8, combining safety monitoring, worker protection, communication, and cloud connectivity into a single connected wearable. These moves show that the ASEAN frontline worker technology market is being shaped by vendors that prioritize recurring software and service revenue over one-time hardware revenue.

White space remains meaningful in the SME segment, where full rugged device programs can still be too expensive or too complex for many buyers. This leaves room for SaaS-led entrants, mixed-device deployment models, and service-based access strategies that lower the barrier to entry. At the same time, safety expectations, workflow accountability, and regional digital integration goals are raising the standard for what buyers expect from suppliers. The ASEAN frontline worker technology market is therefore likely to remain fragmented, but the stronger players will be those that can offer scalable deployments, credible support, and a clear path from pilot use to enterprise-wide adoption.

ASEAN Frontline Worker Technology Industry Leaders

Zebra Technologies Corporation

Honeywell International Inc.

Datalogic S.p.A.

Advantech Co., Ltd.

Kontron AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Zebra Technologies launched Zebra Nucleus, Workcloud Business Intelligence, and Workcloud Integration and Orchestration at its ZONE 2026 customer conference in Nashville. The new platforms form a unified software layer for device fleet management, AI-powered operational dashboards, and workflow orchestration, representing a major expansion of its software portfolio step forward forfor frontline operations across its global customer base.

- March 2026: Blackline Safety began shipping its G8 connected safety wearable, consolidating multi-gas detection, lone worker protection, two-way radio communication, NFC-based zone management, and real-time cloud monitoring into a single industrial platform. The G8 was positioned as a consolidation tool for worksite safety for industrial operators across more than 75 countries.

- January 2026: Honeywell launched Performance+ for Guided Work, a connected workforce solution that combines voice-directed task guidance with advanced analytics, supporting over 48 languages. Available to APAC customers, including Malaysia and Singapore, the solution enabled real-time performance monitoring across distributed warehouse and logistics operations.

- January 2026: SOTI released SOTI ONE Platform version 2026.1, delivering enhanced shared-device security, automated issue detection and recovery, and new SOTI Snap frontline communication features. The update specifically addressed high-turnover shared-device environments common in ASEAN retail and logistics operations.

ASEAN Frontline Worker Technology Market Report Scope

The ASEAN Frontline Worker Technology Market comprises software platforms, mobile applications, and connected workforce technologies that digitize and optimize frontline operations across Southeast Asian economies. These solutions enable employee communication, workforce coordination, task management, skills development, safety monitoring, and performance management across retail, manufacturing, healthcare, logistics, hospitality, construction, and public-sector organizations. Growing enterprise technology adoption, expanding digital infrastructure, increasing smartphone penetration, and workforce modernization initiatives across the region support the market. The market focuses on improving workforce productivity, engagement, compliance, and operational agility within frontline-intensive industries.

The ASEAN Frontline Worker Technology Market Report is Segmented by Component (Software, and Services), Deployment (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Employee Communication and Engagement, Workforce Execution and Task Management, Workforce Scheduling and Coordination, Learning and Knowledge Enablement, Workforce Analytics and Performance Management, Safety and Compliance Management, and Other Applications), End-User Industry (Retail and E-Commerce, Industrial Manufacturing, Healthcare and Life Sciences, Transportation and Logistics, Hospitality, Construction, Government and Public Administration, and Other End-User Industries), and Geography (Singapore, Indonesia, Malaysia, Philippines, Thailand, Vietnam, and Rest of ASEAN). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Employee Communication and Engagement |

| Workforce Execution and Task Management |

| Workforce Scheduling and Coordination |

| Learning and Knowledge Enablement |

| Workforce Analytics and Performance Management |

| Safety and Compliance Management |

| Other Applications |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Hospitality |

| Construction |

| Government and Public Administration |

| Other End-User Industries |

| Singapore |

| Indonesia |

| Malaysia |

| Philippines |

| Thailand |

| Vietnam |

| Rest of ASEAN |

| By Component | Software |

| Services | |

| By Deployment | Cloud-Based |

| Hybrid | |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Employee Communication and Engagement |

| Workforce Execution and Task Management | |

| Workforce Scheduling and Coordination | |

| Learning and Knowledge Enablement | |

| Workforce Analytics and Performance Management | |

| Safety and Compliance Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Industrial Manufacturing | |

| Healthcare and Life Sciences | |

| Transportation and Logistics | |

| Hospitality | |

| Construction | |

| Government and Public Administration | |

| Other End-User Industries | |

| By Geography | Singapore |

| Indonesia | |

| Malaysia | |

| Philippines | |

| Thailand | |

| Vietnam | |

| Rest of ASEAN |

Key Questions Answered in the Report

What is the current size and forecast for the ASEAN frontline worker technology space?

It stood at USD 0.31 billion in 2025 and is forecast to reach USD 1.31 billion by 2031 at a CAGR of 27.99% during 2026-2031.

Which component category leads current revenue?

Software led with a 76.44% share in 2025 because buyers prioritized workflow, analytics, communication, and compliance functionality over stand-alone device spending.

Which buyer group is expanding the fastest?

Small and medium enterprises are projected to grow at a 30.58% CAGR through 2031 as cloud pricing and lower-friction deployments improve access.

Which application area is growing the fastest?

Safety and compliance management is projected to grow at a 29.74% CAGR through 2031 as worker protection, traceability, and audit needs become more formalized.

Which end-user vertical offers the strongest growth outlook?

Transportation and logistics is projected to grow at a 29.45% CAGR through 2031 because operators need stronger coordination across warehousing, fulfillment, and moving field work.

Which country is the largest and which is the fastest-growing in the region?

Indonesia held the largest share at 38.16% in 2025, while Vietnam is projected to grow the fastest at a 29.98% CAGR through 2031.

Page last updated on: